Europe Neurostimulation Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

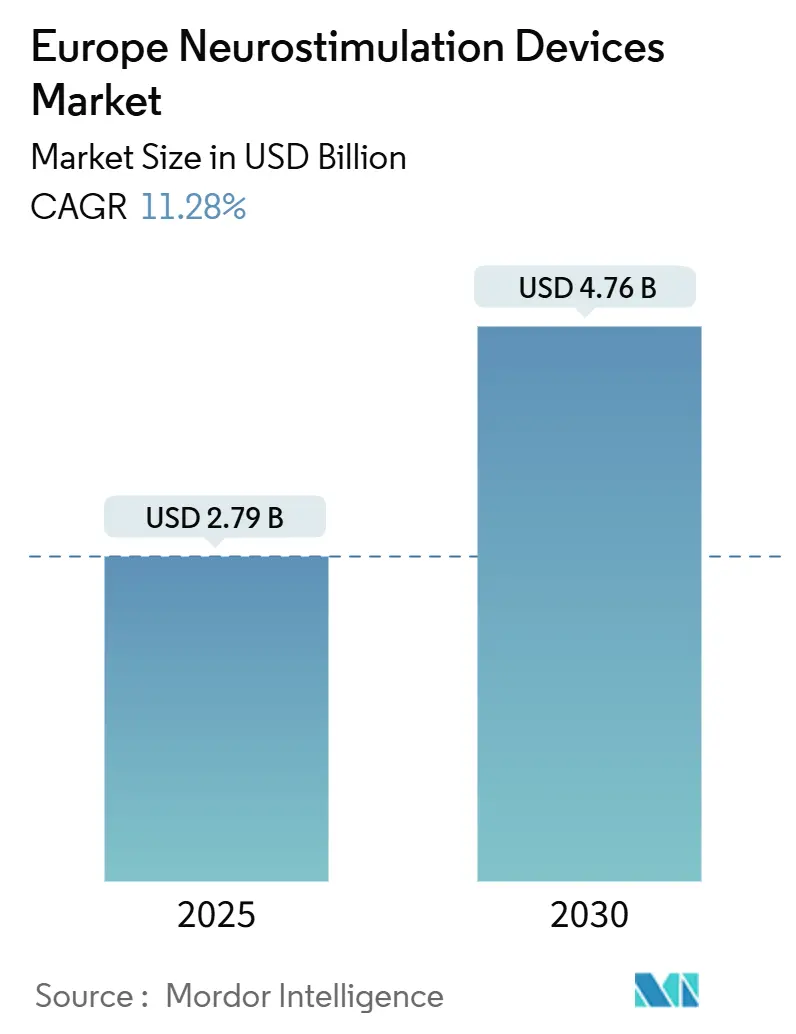

| Market Size (2025) | USD 2.79 Billion |

| Market Size (2030) | USD 4.76 Billion |

| Growth Rate (2025 - 2030) | 11.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Neurostimulation Devices Market Analysis by Mordor Intelligence

The Europe Neurostimulation Devices Market size is estimated at USD 2.79 billion in 2025, and is expected to reach USD 4.76 billion by 2030, at a CAGR of 11.28% during the forecast period (2025-2030).

Demographic aging, a rising neurological disease burden, and steady regulatory support nurture a demand up-curve for sophisticated neuromodulation options. Continuous engineering advances—especially AI-enabled closed-loop systems—sharpen therapeutic precision and widen the addressable patient pool. At the same time, non-invasive alternatives win mindshare by lowering surgical risk, shortening recovery, and increasing adoption in outpatient and home settings. Intensifying vendor consolidation, led by Globus Medical’s acquisition of Nevro, signals a strategic race to command platform breadth and data science capabilities. However, Europe-specific supply-chain checks on rare-earth elements and extended EU-MDR review cycles add cost and scheduling friction that firms must navigate to preserve growth momentum.

Key Report Takeaways

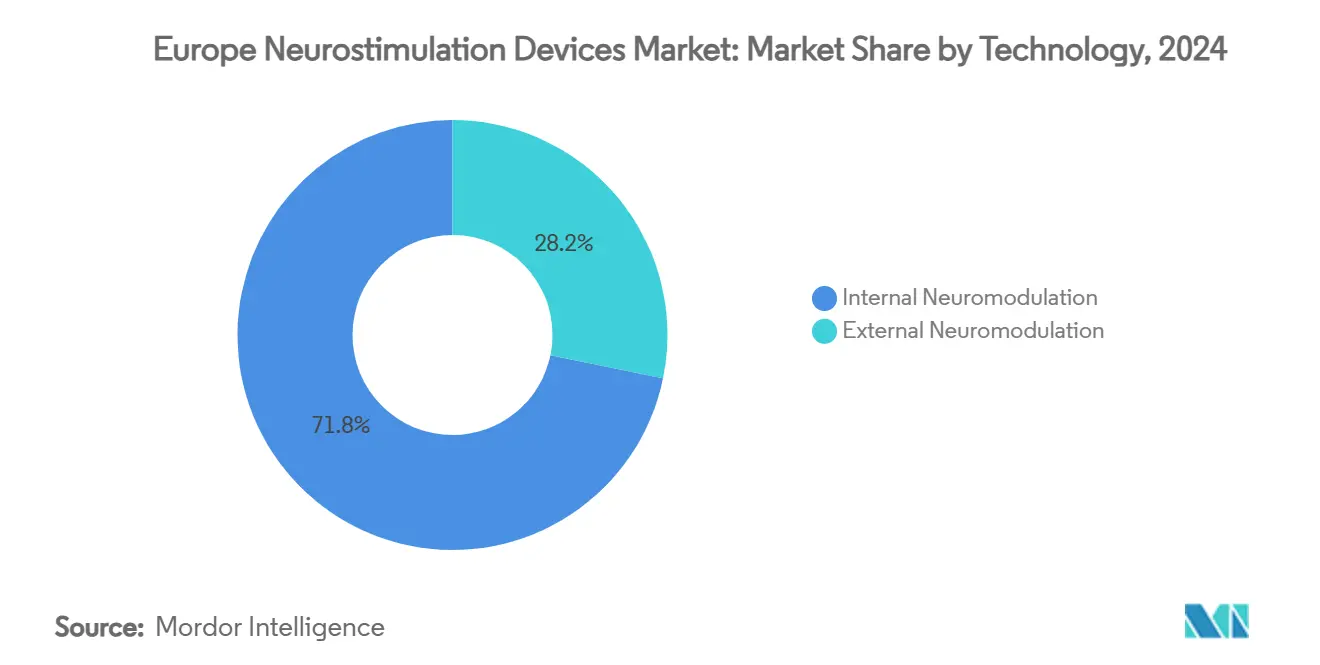

- By technology, internal neuromodulation led with 71.77% revenue share in 2024; external neuromodulation is projected to expand at 11.98% CAGR through 2030.

- By application, pain management accounted for 39.98% share of the Europe Neurostimulation Devices market size in 2024, while epilepsy is forecast to grow at 12.03% CAGR through 2030.

- By end-user, hospitals captured 47.87% share in 2024; home-care is set to grow at 12.11% CAGR to 2030.

- By geography, Germany held 29.91% share in 2024, whereas France is expected to record the fastest 12.32% CAGR by 2030.

Europe Neurostimulation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & neurological disease burden | +2.1% | Germany, Italy | Long term (≥ 4 years) |

| Escalating demand for minimally-invasive pain therapies | +1.8% | Western → Eastern Europe | Medium term (2-4 years) |

| Rapid product upgrades | +1.2% | Germany, France, UK | Short term (≤ 2 years) |

| Home-based TENS/TMS adoption via e-commerce | +0.9% | Northern urban markets | Medium term (2-4 years) |

| EU-MDR driven replacement cycle of legacy implants | +0.8% | High-penetration EU states | Short term (≤ 2 years) |

| Opioid-reduction programs | +0.7% | Western Europe, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Neurological Disease Burden

Europe’s demographic shift raises the prevalence of Parkinson’s, epilepsy, and chronic pain, with neurological disorders now affecting 19% of European adults [1]Pierluigi Diotaiuti , "Evaluating the effectiveness of neurofeedback in chronic pain management: a narrative review," Frontiers in Psychology, frontiersin.org. Direct Parkinson’s care costs reached EUR 25,649 per patient over a three-month period in Sweden, underscoring fiscal pressure on state systems. Projections pointing to a 112% hike in Parkinson’s incidence by 2050 intensify the need for scalable, economically sustainable interventions [2]Christopher Kruse, "Care of Late-Stage Parkinsonism: Resource Utilization of the Disease in Five European Countries," International Parkinson and Movement Disorder Society, movementdisorders.onlinelibrary.wiley.com. Neurostimulation devices—because they are reusable, adjustable, and often opioid-sparing—fit payer imperatives to tame lifetime treatment spend while sustaining quality of life. As longevity extends, device replacement and upgrade cycles generate recurring revenue streams that underpin the Europe Neurostimulation Devices market’s resilient expansion path.

Escalating Demand for Minimally-Invasive Pain Therapies

Closed-loop spinal cord stimulation (SCS) has trimmed mean pain scores from 8.2 to 2.6 in real-world European cohorts and delivered 92% patient satisfaction, strengthening clinical confidence [3]Harold Nijhuis, "Durability of Evoked Compound Action Potential (ECAP)-Controlled, Closed-Loop Spinal Cord Stimulation (SCS) in a Real-World European Chronic Pain Population," Pain and Therapy, link.springer.com. Reversibility and programmability differentiate SCS from ablative procedures, aligning it with evidence-based opioid substitution policies now embedded in Western Europe’s pain guidelines. ECAP-controlled systems provide objective neuro-feedback, allowing physicians to titrate energy in precise, reproducible increments. These attributes position neuromodulation as the default escalation step when pharmacologic regimens plateau, driving steady unit demand and ancillary revenue from software upgrades.

Rapid Product Upgrades

The innovation cadence has accelerated, led by Nevro’s CE-marked HFX iQ and Medtronic’s adaptive BrainSense DBS, both approved within the last 18 months. AI layers learn patient-specific neural signatures and self-tune parameters, shrinking clinic visits and elevating long-term responder rates. Market leaders are racing to add MRI compatibility, battery life extensions, and smartphone dashboards, raising the technical bar for new entrants. Shorter upgrade cycles also refresh installed-base revenues because payers authorize replacements when platforms promise measurable functional gains, bolstering the Europe Neurostimulation Devices market.

Home-Based TENS/TMS Adoption via E-commerce

Direct-to-consumer portals now sell CE-marked TENS units with 64 preset programs, matching clinic-grade versatility while costing a fraction of in-office regimens. Non-invasive vagus nerve stimulators such as Nurosym, shipped with tele-monitoring apps, widen access for rural and mobility-limited users. E-commerce fulfilment plus tele-consultation accelerate therapy initiation, especially in Northern Europe’s digitally enabled health ecosystems. Consumer familiarity with wearables normalizes the concept of at-home neuro-modulation and feeds an upgrade funnel toward more sophisticated, prescription-grade devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse events & explant risks | −1.5% | Europe-wide | Medium term (2-4 years) |

| Lengthy EU-MDR approval timelines | −0.8% | All EU member states | Short term (≤ 2 years) |

| High device cost & patchy reimbursement | −1.2% | Eastern & Southern Europe | Long term (≥ 4 years) |

| Supply-chain pinch in implant-grade rare earths | −0.9% | High-tech device segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Events & Explant Risks

Explant procedures carry surgical risk and average USD 39,106 in hospital reimbursement, prompting stricter patient selection and real-time performance monitoring mandates. Negative outcomes erode referring-physician confidence, slowing conversion rates despite mounting evidence of long-term efficacy. Regulators have responded by tightening post-market surveillance, obliging manufacturers to finance larger registries and faster-cycle root-cause investigations. Sustained progress in lead durability, infection control, and predictive maintenance algorithms is pivotal to neutralize this drag on the Europe Neurostimulation Devices market.

Lengthy EU-MDR Approval Timelines

The EU-MDR’s expanded clinical evidence requirements doubled average dossier sizes and stretched notified-body queues, delaying market entry by up to 12 months for Class III implants. Firms juggling legacy renewals with novel platform filings confront resource strain and pipeline congestion. Additionally, China’s export license stipulations on gadolinium and yttrium lengthen customs clearance windows for implant components, complicating “just-in-time” production philosophies. Collectively, these procedural hurdles temper the velocity of innovation diffusion across Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: External Momentum Upshifts as AI Matures

Internal neuromodulation commanded 71.77% of Europe Neurostimulation Devices market share in 2024, reflecting three decades of clinical routine and reimbursement familiarity. Yet external modalities trailblazed an 11.98% CAGR through 2030, propelled by next-generation rTMS platforms that deliver 10,000 pulses in under four minutes, trim session counts, and present minimal contraindications. The Europe Neurostimulation Devices market size for external modalities is expected to nearly double, helped by cloud-linked TMS headsets that document outcomes in payers’ preferred data formats. Rotating-coil multi-locus systems, now piloted in Germany, permit instantaneous cortical focus changes, improving efficacy for comorbid depression and insomnia.

Internal platforms are hardly static. Closed-loop SCS leveraging ECAP feedback maintains durable pain relief at 12 months, anchoring replacement cycles that underpin manufacturer annuity revenue. Adaptive DBS expands beyond Parkinson’s into severe addiction use-cases under the Brain-PACER study in Cambridge, projecting new adoption curves once early clinical endpoints read out. Meanwhile, sacral and gastric stimulators continue serving niche bowel-motility disorders, reinforcing the technology’s multi-organ versatility.

By Application: Pain Supremacy Faces Epilepsy Upswing

Pain indications represented 39.98% of the Europe Neurostimulation Devices market in 2024 as SCS, DRG stimulation, and peripheral nerve platforms secured cost-utility endorsements from major payers. Nonetheless, epilepsy emerges as the fastest mover at a 12.03% CAGR, buoyed by AI-enabled seizure prediction and vagus nerve stimulators that can trigger pre-emptive pulses. The Europe Neurostimulation Devices market size for epilepsy therapy lines is forecast to cross USD 1 billion by 2030, marking a material diversification of revenue mixes.

Complementary demand drivers include adaptive DBS for Parkinson’s, high-frequency gastric pacing for obesity trials, and TMS for major depressive disorder. Multi-therapy convergence—where one implant treats pain and movement disorders via firmware upgrades—could unlock synergistic reimbursement codes, smoothing hospital procurement cycles.

By End-User: Hospital Core, Home-Care Surge

Hospitals retained 47.87% revenue share in 2024 because complex implant surgeries, MRI scans, and intra-operative programming still require specialized theatres and imaging suites. Ambulatory surgery centers now compete on same-day discharge convenience, nibbling at select volume bundles like DRG implants. In parallel, the home-care category’s 12.11% CAGR underscores patient demand for self-managed, non-invasive sessions. Home-approved TMS hoods and app-guided TENS devices extend physician oversight via encrypted telemetry, satisfying payer conditions for outcome documentation.

The Europe Neurostimulation Devices market share expansion in home-care is further aided by national telehealth reimbursement codes adopted during the pandemic. Rapid-charge lithium polymer batteries and wireless firmware updates reduce maintenance visits, aligning with chronic-care funding models that emphasize out-of-hospital cost containment.

Geography Analysis

Germany’s 29.91% stake stems from universal statutory coverage, an organized sickness-fund network, and the Digital Health Care Act, which fast-tracks the listing of connected devices. Manufacturers leverage Germany as a launch pad because early DiGA approvals translate into pan-EU credibility. France, advancing at a 12.32% CAGR, blends generous pain-therapy reimbursements with an agile clinical-trial ecosystem centered on Paris and Lyon. That mix attracts venture-backed neurotech SMEs keen to secure CE evidence in a single-payer environment.

The United Kingdom preserves strategic relevance despite post-Brexit regulatory bifurcation. The MHRA’s fast-track pathway for “innovative implantables” and NHS England’s MedTech Funding Mandate give local trials global visibility. Southern markets like Italy and Spain accelerate adoption as demographic aging climbs and EU recovery funds modernize neurology infrastructure. Eastern Europe, though budget-constrained, shows rising procurement under cross-border reimbursement frameworks, opening second-wave growth for value-oriented device configurations.

Nordic nations integrate neuromodulation into national e-referral portals, enabling seamless prescription of home-based TENS and TMS kits. Meanwhile, Ireland and Benelux benefit from multinational manufacturing hubs that shorten supply lead times. Collectively, these regional nuances require adaptive go-to-market playbooks but sustain the overall trajectory of the Europe Neurostimulation Devices market.

Competitive Landscape

Industry concentration remains moderate. Medtronic, Boston Scientific, Abbott, and LivaNova command the top tier, yet their combined slice stays below the 60% threshold, leaving room for midsize specialists. Globus Medical’s USD 250 million purchase of Nevro in April 2025 integrates high-frequency SCS and AI analytics into a spine-implant powerhouse, signaling a premium on data-rich pain platforms. Boston Scientific’s new DBS software, which secures CE clearance for symptom-specific segmentation, tightens the race for adaptive neuro-algorithms.

Start-ups carve white spaces: Salvia BioElectronics develops bio-electronic foils for migraine, whereas Newronika deploys implantable closed-loop DBS headsets with cloud-based learning loops. Fundraising trends confirm enthusiasm; neurotech ventures raised USD 2.3 billion across 129 deals in 2024, with half directed to Europe-headquartered firms. Component suppliers also feel consolidation pressure as OEMs seek secure rare-earth pipelines and vertically integrate firmware. Competitive intensity is thus forecast to escalate, rewarding players that balance innovation tempo with EU-MDR compliance discipline.

Europe Neurostimulation Devices Industry Leaders

-

Medtronic PLC

-

Abbott Laboratories

-

The Magstim Company Limited

-

Renishaw PLC

-

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Globus Medical announced its acquisition of Nevro Corp for USD 250 million, merging the HFX spinal cord stimulation suite with Globus Medical’s broader pain platform.

- January 2025: Medtronic secured CE mark approval for its adaptive deep brain stimulation technology targeting Parkinson’s treatment in European markets.

- November 2024: Nevro Corp received CE Mark certification for its HFX iQ system, the first cloud-linked, AI-driven high-frequency spinal cord stimulator in Europe.

- June 2024: Boston Scientific obtained CE mark approval for its deep brain stimulation software upgrade, enhancing clinical programming flexibility.

Europe Neurostimulation Devices Market Report Scope

As per the scope of this report, neurostimulation therapies include invasive and noninvasive approaches that involve the application of electrical stimulation, to drive neural function within a circuit. The market is segmented by technology, application, and geography.

| Internal Neuromodulation | Spinal Cord Stimulation (SCS) |

| Deep Brain Stimulation (DBS) | |

| Vagus Nerve Stimulation (VNS) | |

| Sacral Nerve Stimulation (SNS) | |

| Gastric Electrical Stimulation (GES) | |

| External Neuromodulation | Transcutaneous Electrical Nerve Stimulation (TENS) |

| Transcranial Magnetic Stimulation (TMS) | |

| Respiratory Electrical Stimulation (RES) |

| Pain Management |

| Parkinson's Disease |

| Epilepsy |

| Depression |

| Dystonia |

| Others |

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty Clinics |

| Home-care Settings |

| Others |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Technology | Internal Neuromodulation | Spinal Cord Stimulation (SCS) |

| Deep Brain Stimulation (DBS) | ||

| Vagus Nerve Stimulation (VNS) | ||

| Sacral Nerve Stimulation (SNS) | ||

| Gastric Electrical Stimulation (GES) | ||

| External Neuromodulation | Transcutaneous Electrical Nerve Stimulation (TENS) | |

| Transcranial Magnetic Stimulation (TMS) | ||

| Respiratory Electrical Stimulation (RES) | ||

| By Application | Pain Management | |

| Parkinson's Disease | ||

| Epilepsy | ||

| Depression | ||

| Dystonia | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Specialty Clinics | ||

| Home-care Settings | ||

| Others | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current Europe Neurostimulation Devices market size and projected growth?

The market is valued at USD 2.79 billion in 2025 and is expected to reach USD 4.76 billion by 2030, representing an 11.28% CAGR.

Which technology segment is expanding fastest?

External neuromodulation technologies, including advanced TMS systems, are forecast to grow at 11.98% CAGR through 2030.

Why is epilepsy therapy gaining momentum in Europe?

AI-supported seizure prediction and broadened reimbursement for vagus nerve stimulation are driving a 12.03% CAGR in epilepsy applications.

How are home-care settings influencing market dynamics?

Patient preference for convenience and reimbursement for tele-monitored devices underpin a 12.11% CAGR in home-care adoption.

What regulatory factors could slow device launches?

Lengthy EU-MDR review timelines and stricter clinical evidence demands can delay market entry by up to a year for new implants.

Which countries represent the largest and fastest-growing markets?

Germany held 29.91% share in 2024, while France is projected as the fastest grower with a 12.32% CAGR to 2030.

Page last updated on: