Deep Brain Stimulation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

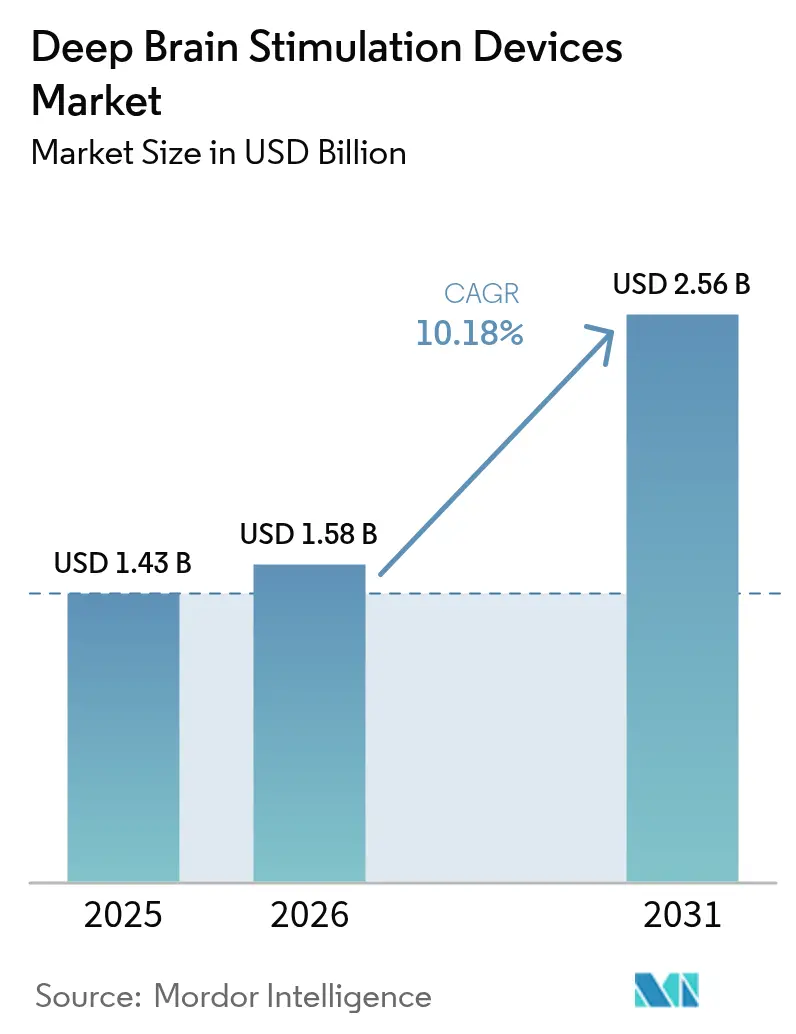

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Deep Brain Stimulation Devices Market Analysis by Mordor Intelligence

The deep brain stimulation devices market size in 2026 is estimated at USD 1.58 billion, growing from 2025 value of USD 1.43 billion with 2031 projections showing USD 2.56 billion, growing at 10.18% CAGR over 2026-2031. Rising adoption of sensing-enabled closed-loop generators, broader reimbursement for earlier-stage Parkinson’s patients, and a steady pipeline of adaptive algorithms are accelerating procedure volumes. Hospitals remain the primary implant setting, but migration toward ambulatory surgical centers is lifting capacity without comparable capital spend. Miniaturized rechargeable IPGs that last 9-15 years are lowering lifetime ownership costs, while AI-guided candidate selection tools improve responder rates and justify payor coverage. North America anchors global revenue, yet Asia-Pacific is closing the gap as surgeon-training initiatives and government neurotechnology programs scale access. Tight ^99Mo supply and post-implant infection risk temper momentum but also stimulate innovation in diagnostics and antimicrobial hardware.

Key Report Takeaways

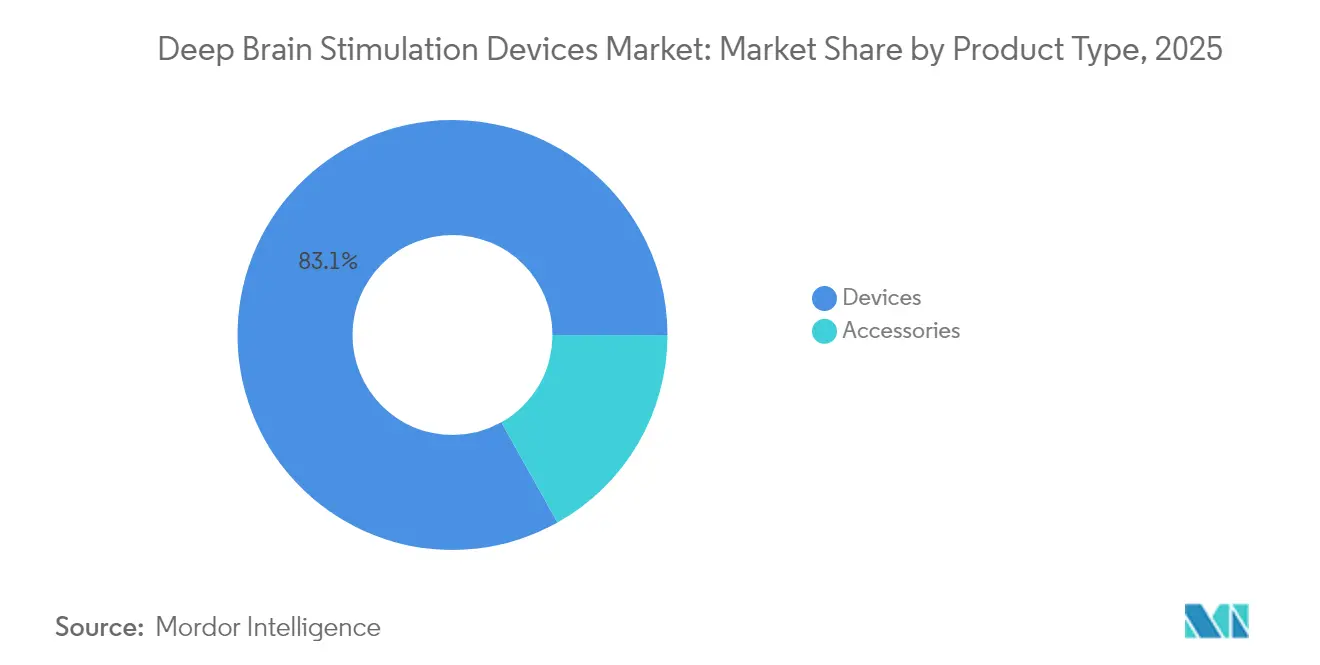

- By product type, Devices held 83.12% of deep brain stimulation devices market share in 2025, while Accessories are forecast to grow at a 10.47% CAGR to 2031.

- By application, Parkinson’s disease accounted for 61.21% share of the deep brain stimulation devices market size in 2025 and Depression is advancing at an 10.74% CAGR through 2031.

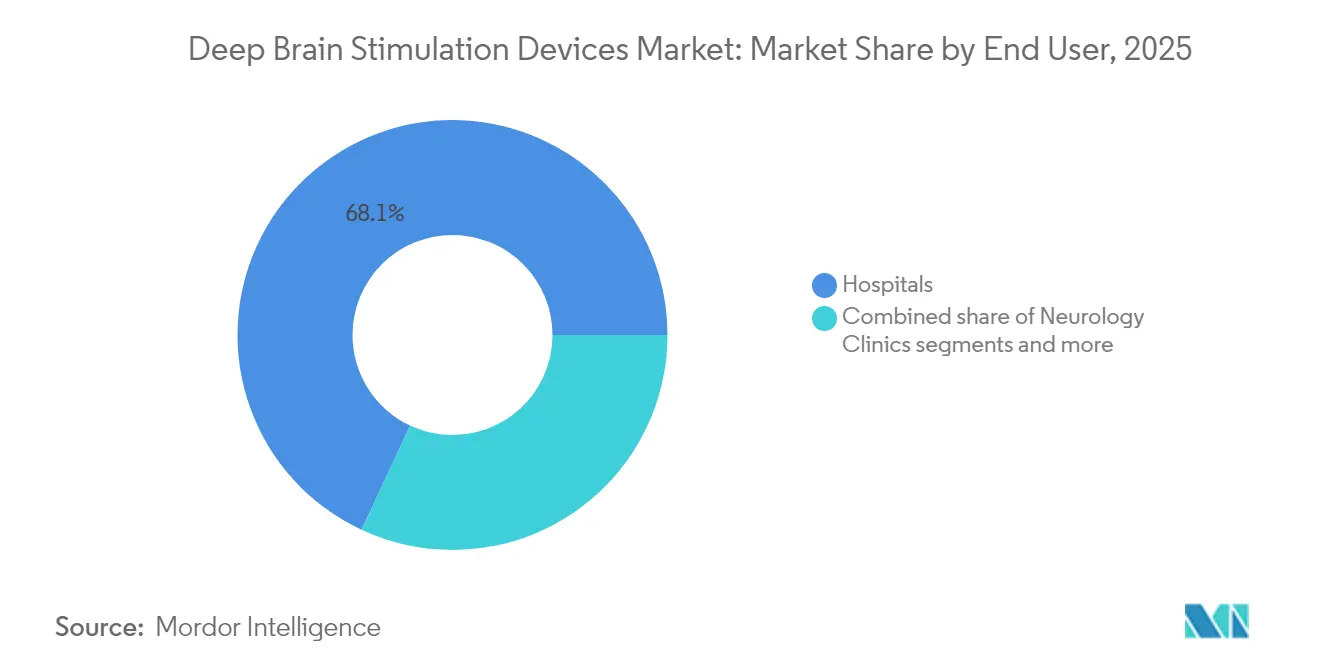

- By end user, Hospitals led with 68.05% revenue share in 2025; Ambulatory Surgical Centers are set to expand at an 10.93% CAGR through 2031.

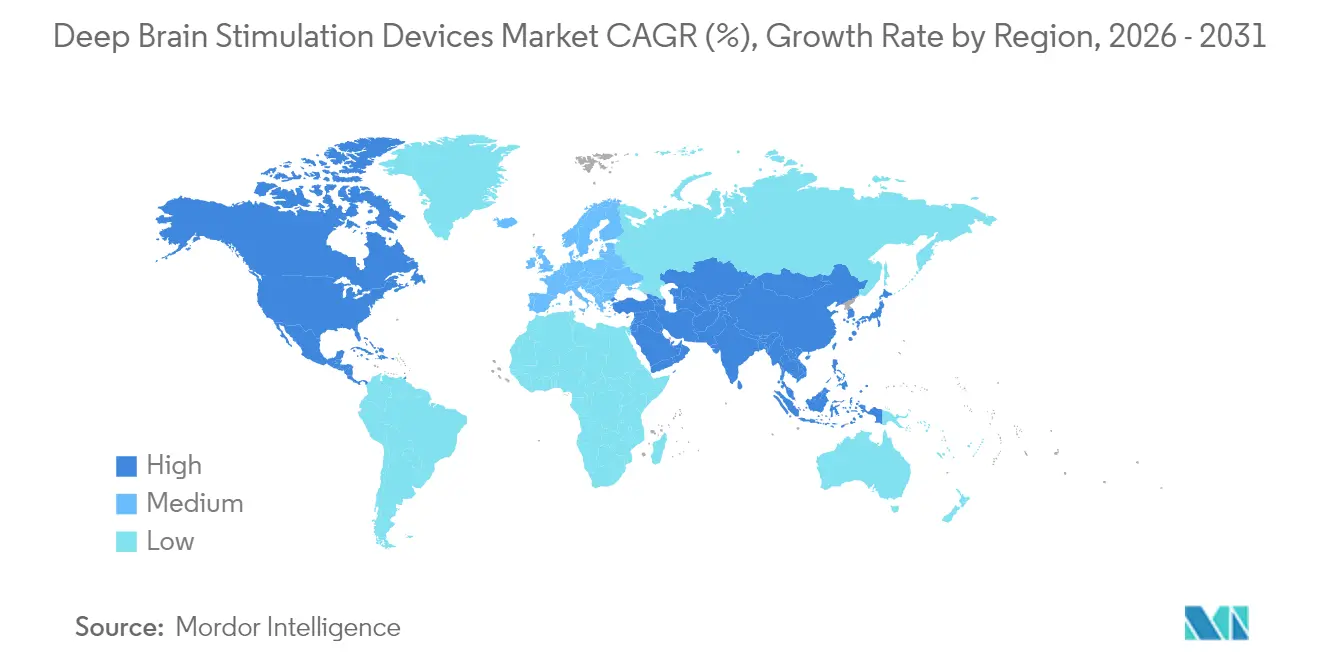

- By geography, North America captured 41.88% of deep brain stimulation devices market share in 2025, whereas Asia-Pacific records the highest projected CAGR at 11.12% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Deep Brain Stimulation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of sensing-enabled closed-loop IPGs | +2.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Reimbursement expansion for earlier-stage Parkinson's patients | +1.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Surge in Asia-Pacific neurosurgeon training programs | +1.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Miniaturised rechargeable IPGs lengthen replacement cycles | +1.4% | Global | Medium term (2-4 years) |

| FDA fast-track for adaptive DBS algorithms | +1.2% | Global, led by North America | Short term (≤ 2 years) |

| AI-guided patient selection improves responder rates | +1.0% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid uptake of sensing-enabled closed-loop IPGs

BrainSense Adaptive DBS won FDA clearance in February 2025, marking the first commercial closed-loop platform that automatically titrates stimulation from real-time neural signals[1]Source: Medtronic, “Medtronic earns U.S. FDA approval for the world's first Adaptive deep brain stimulation system for people with Parkinson's,” Medtronic, news.medtronic.com . Multicenter data show median 50% motor-symptom reduction compared with open-loop systems, alongside a one-third cut in programming visits[2]Source: Parkinson’s Foundation, “New Study Further Personalizes Deep Brain Stimulation,” Parkinson’s Foundation, parkinson.org . Physicians report faster optimization curves and fewer side effects, improving patient satisfaction and health-economic value. Early adoption is strongest in U.S. and German centers where reimbursement rewards outcome-based models. Expanding indications in epilepsy and depression further widen the deep brain stimulation devices market.

Reimbursement expansion for earlier-stage Parkinson’s patients

Medicare removed the “advanced-stage only” criterion in late 2024, instantly enlarging the U.S. eligible population. Private payors aligned policies within six months, accelerating referral volumes. Comparable moves by France’s HAS and Germany’s G-BA support broader European uptake. Earlier intervention improves long-term functional status and reduces levodopa cost burden, reinforcing the deep brain stimulation devices market outlook. Manufacturers are funding outcomes registries to generate real-world evidence that sustains the policy shift.

Surge in Asia-Pacific neurosurgeon training programs

China, India, and South Korea launched VR-based surgical curricula that shorten mastery time while maintaining safety. Shanghai’s Ruijin Hospital now trains 120 fellows annually, a five-fold jump over 2023, and similar hubs in Mumbai and Seoul replicate the model. Each added neurosurgeon enables 50-75 DBS implants yearly, directly boosting regional procedure capacity. Government grants subsidize cadaver labs and simulation suites, reducing the upfront burden on hospitals. These investments underpin the deep brain stimulation devices market’s double-digit growth in Asia-Pacific.

Miniaturized rechargeable IPGs lengthen replacement cycles

Boston Scientific’s Vercise Genus battery lasts up to 15 years and recharges in under 30 minutes, cutting lifetime surgical revisions by 60%. Extended life translates to lower cumulative device spend and fewer infection opportunities, strengthening the value proposition for younger patients. Medtronic’s Percept RC combines long-life power with sensing, blunting competitive differentiation. Payors increasingly favor rechargeables, accelerating their share within the deep brain stimulation devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-implant infection rates driving precautionary revisions | -1.8% | Global, higher impact in developing markets | Short term (≤ 2 years) |

| Global shortage of ^99Mo for imaging prolongs diagnosis windows | -1.2% | Global, acute in regions dependent on reactor supply | Medium term (2-4 years) |

| Cyber-security vulnerability disclosures for Bluetooth-enabled IPGs | -0.9% | Global, concentrated in connected device markets | Short term (≤ 2 years) |

| High capital cost of intra-operative imaging suites in South America | -0.7% | South America, extending to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-implant infection rates driving precautionary revisions

Hardware-related infections occur in 2.6-6.9% of implants, often requiring complete system explantation and extended antibiotic courses. Revision costs exceed USD 20,000 per episode and stall new referrals when publicized outcomes erode confidence. Summer seasonality and comorbidity prevalence escalate risk, especially in facilities lacking laminar airflow theaters. Antimicrobial-coated leads and stricter peri-operative protocols are lowering rates in high-volume U.S. centers, yet widespread uptake in emerging markets remains limited. Persistent infection fears moderate the deep brain stimulation devices market’s penetration curve.

Global shortage of ^99Mo for imaging prolongs diagnosis windows

DaTscan depends on ^99Mo supply from six aging research reactors. Outages in 2024 lengthened scheduling backlogs to eight weeks in parts of Latin America, delaying surgical clearance. FDA stability-testing rules increased production costs by USD 3 million per site, dissuading smaller compounders. Limited imaging access slows patient throughput and postpones device orders, constraining the deep brain stimulation devices market until isotope supply or alternative MRI biomarkers scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Retain Dominance as Accessories Accelerate

Devices generated 83.12% revenue in 2025, anchored by implantable pulse generators that integrate sensing, rechargeable batteries, and MRI safety features. Dual-channel generators now surpass single-channel units in new implants, reflecting bilateral procedure growth. Accessories—directional leads, sensing electrodes, and extensions—grow at 10.47% CAGR as closed-loop systems require specialized hardware upgrades. Replacement cycles are shorter for accessories, creating an annuity stream that triples lifetime revenue per patient. Deep brain stimulation devices market size for accessories is projected to reach USD 0.44 billion by 2031, amplified by software-based programming kits adopted by community neurologists. Competitive pressure centers on electrode geometry and material science rather than standalone pricing, protecting margins.

Technological breakthroughs in segmented leads deliver more precise targeting and reduce adverse effects, spurring conversion from legacy systems. Manufacturers bundle upgrade paths with existing generators, raising switching barriers for hospitals. Regulatory clearances in Europe and the United States for adaptive leads position accessories as the primary innovation frontier. Growth in refurbishment and resterilization services for extensions also contributes to segment revenue, especially in cost-sensitive markets. Consequently, accessories will outpace device unit growth yet remain reliant on installed generator bases within the deep brain stimulation devices market.

By Application: Parkinson’s Prevails While Depression Surges

Parkinson’s disease retained 61.21% share in 2025 owing to robust clinical evidence and payor familiarity. Average implant age has dropped from 65 to 58 years since guideline revisions, extending the revenue tail per patient. Essential tremor remains steady, but dystonia benefits from expanded offspring forms like cervical dystonia protocols. Depression is the fastest mover at 10.74% CAGR, driven by Abbott’s TRANSCEND trial and FDA breakthrough device designation for treatment-resistant disease. Deep brain stimulation devices market size for depression is forecast to triple by 2030 should pivotal data secure full approval.

Epilepsy advances through NeuroPace’s responsive neurostimulation, blurring lines between DBS and cranial-closed-loop systems and drawing new competitors into the neuromodulation arena. Obsessive-compulsive disorder remains niche but benefits from cross-disciplinary psychiatric-surgical collaborations. Application diversity mitigates revenue concentration risk while demanding nuanced regulatory and clinical strategies across indications. These trends collectively reinforce the deep brain stimulation devices market.

By End User: Hospitals Lead but Outpatient Sites Gain Traction

Hospitals captured 68.05% of 2025 revenue, leveraging integrated imaging, critical care, and multidisciplinary teams. However, streamlined surgical workflows now allow same-day discharge in selected cohorts, lifting ambulatory surgical center (ASC) appeal at an 10.93% CAGR. ASCs reduce procedure cost by up to 25% and free hospital OR slots for complex cases, a boon amid staffing shortages.

Neurology clinics handle long-term programming and follow-up through cloud-based platforms, expanding patient reach beyond metropolitan hubs. Remote programming cuts travel burden and lifts adherence, especially in rural America and Australia. Capital barriers—USD 3-5 million intra-operative MRI suites—slow ASC diffusion in South America but catalyze public-private imaging ventures. Companies offer turnkey service models that include surgical training and device logistics, smoothing the transition from hospital dominance to mixed-site delivery in the deep brain stimulation devices market.

Geography Analysis

North America remained the revenue anchor with 41.88% deep brain stimulation devices market share in 2025, bolstered by broad Medicare coverage, high neurosurgeon density, and early adoption of closed-loop systems. U.S. growth continues as outpatient implants rise, while Canada’s universality sustains steady volume albeit with tighter device margins.

Europe contributes a quarter of global sales, characterized by stable reimbursement and consistent procedure volumes across leading German, French, and Nordic centers. Adoption of rechargeable generators and directional leads is mature, yet bureaucratic procurement processes elongate replacement cycles.

Asia-Pacific leads expansion at 11.12% CAGR, propelled by China’s pricing frameworks for brain-computer interfaces and aggressive capacity building in tertiary hospitals. Japan’s aging demographics and robust research output sustain premium device demand, whereas India advances value-engineered solutions to address affordability constraints. Local manufacturing partnerships and regulatory harmonization initiatives lower entry barriers, making the region the strategic battleground for the deep brain stimulation devices market. Middle East and Africa record single-digit growth, limited by capital equipment scarcity and reimbursement gaps, yet Gulf states invest in centers-of-excellence that could seed broader adoption.

Regulatory Landscape

Deep brain stimulation (DBS) systems are regulated as high-risk implantable neuromodulation devices in major markets, driving stringent premarket evidence and lifecycle-change controls. In the United States, the FDA PMA pathway sits under 21 CFR Part 814, and PMA supplements are a common route for software and feature updates; for example, a February 2025 PMA supplement decision supported an adaptive DBS programming feature (P960009/S478). In Europe, DBS implants fall under the EU Medical Device Regulation (Regulation (EU) 2017/745, MDR) as Class III devices, requiring conformity assessment by a Notified Body and ongoing postmarket surveillance. MDR implementation continues to influence timelines and documentation for implants and software, and where a device is integral to a medicinal product, MDR Article 117 introduces the need for a Notified Body Opinion against the General Safety and Performance Requirements (GSPRs). Across regions, recognized clinical evidence standards for implantable devices (including ISO 14155-aligned clinical investigation practices) remain central to submissions supporting new indications and algorithm-driven therapy modes.

Value Chain Analysis

The DBS value chain spans upstream R&D of neural sensing algorithms, firmware, and programming software, component sourcing (implant-grade metals, precision electrodes, batteries, and advanced microelectronics such as high-reliability semiconductor packages), regulated manufacturing and sterilization, and distribution to neurosurgical implant centers. Downstream value capture is strongly service-led: surgeon training, procedure support, post-implant programming, and long-term therapy optimization drive recurring revenue and customer retention. Regulatory milestones and clinical evidence generation are embedded throughout the chain, with approvals such as Medtronic's January 2025 CE Mark for BrainSense adaptive DBS and the February 2025 FDA approval for adaptive DBS features reinforcing the shift toward software-defined therapy management. While clinical programs in 2026 continue to inform practice, including ongoing research on gait-adaptive stimulation, this research emphasizes the need for integrated sensing analytics and patient-tailored programming within commercial workflows.

Competitive Landscape

Market concentration is moderate: Medtronic, Boston Scientific, and Abbott collectively command majority of revenue through broad portfolios and clinician-support ecosystems. Medtronic’s BrainSense set the benchmark for adaptive systems, reinforcing its premium positioning. Boston Scientific differentiates with the Vercise Genus platform’s battery longevity and directional stimulation, while Abbott targets psychiatry with the Liberta rechargeable and TRANSCEND program.

Asian challengers Beijing PINS and SceneRay gain traction in China’s public tenders via cost leadership and local service networks. European innovators such as Newronika secured CE Mark for adaptive DBS, signaling nascent competition in closed-loop algorithms. Strategic moves include Boston Scientific’s February 2025 FDA clearance for Cartesia X leads, Medtronic’s software-update business model, and Abbott’s AI-enabled programming suite.

All players emphasize evidence generation and surgeon training to create stickiness; data-driven programming ecosystems augment device features and erect switching costs. Cybersecurity disclosures around Bluetooth-enabled IPGs spur collaborative hardening efforts, adding a protective moat for incumbents that can afford security certification. Consolidation is expected as niche software or electrode suppliers seek scale within the deep brain stimulation devices market.

Deep Brain Stimulation Devices Industry Leaders

Boston Scientific Corporation

Renishaw PLC

NeuroPace Inc.

Beijing Pinchi Medical Equipment Co., Ltd.

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Software-led differentiation is widening whitespace in DBS beyond core implant hardware, especially in adaptive (closed-loop) programming, image-guided targeting, and workflow tools that reduce follow-up burden. The February 2025 FDA approval of Medtronic's BrainSense Adaptive DBS and the January 2025 CE Mark for BrainSense adaptive DBS in the EU/UK provide tangible regulatory precedent for device-software combinations, encouraging additional algorithm modules and therapy-management features within existing installed bases. Procedural capacity and consistency also present clear commercial openings. Outpatient migration and standardized training programs create demand for turnkey service models (training, logistics, and remote programming support), while the known infection burden (2.6-6.9% of implants in the current evidence base) elevates opportunities for antimicrobial hardware, improved peri-operative toolkits, and post-implant monitoring offerings that lower revision rates and protect center reputations. MRI- and connectivity-informed targeting (including patient-specific high-field imaging approaches reported in 2026 academic studies) expands the opportunity for planning and programming ecosystems that integrate imaging analytics with directional lead control, benefiting OEMs and software partners that can demonstrate reproducible outcomes under Class III regulatory expectations.

Recent Industry Developments

- April 2026: UCSF initiated a 24-hour adaptive DBS trial, testing real-time sensing and patient-specific programming in a chronic setting. The study informs practical deployment of closed-loop DBS and may influence software updates and clinical workflows.

- June 2026: Academic feasibility work published on gait-synchronized adaptive DBS demonstrates real-time sensing aligned to gait, supporting integration of imaging analytics with directional leads.

- December 2025: NeuroPace filed a Premarket Approval Supplement (PMA-S) with the US FDA seeking an expanded labeled indication for its RNS System to include antiseizure-medication resistant idiopathic generalized epilepsy.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from deep brain stimulation (DBS) systems used to deliver electrical stimulation to specific brain targets for approved and commonly adopted neurological indications, along with key implantable and external components needed to complete the therapy.

Scope exclusions: External neuromodulation therapies not involving DBS implantation (for example spinal cord, vagus nerve, and peripheral nerve stimulation) are excluded.

Segmentation Overview

- By Product Type

- Device

- Single-Channel Systems

- Implantable Pulse Generators

- Dual-Channel Systems

- Accessories

- Leads / Electrodes

- Extensions & Accessories

- Device

- By Application

- Parkinson’s Disease

- Essential Tremor

- Dystonia

- Epilepsy

- Obsessive-Compulsive Disorder

- Depression (Investigational)

- By End User

- Hospitals

- Neurology Clinics

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the clinical and procedural context and to anchor assumptions that are difficult to observe directly from company disclosures. We referred to public sources such as the US FDA device databases and recall notices, the US Centers for Medicare and Medicaid Services payment files, the OECD health statistics, and WHO health system indicators to understand procedure coverage and treatment access.

To keep the demand pool realistic, we also reviewed peer reviewed clinical literature on DBS adoption by indication, along with hospital and academic center publications that discuss patient selection, revision rates, and device longevity. Company filings, investor presentations, and reputable press were used to track product launches and geographic expansion. Where helpful, paid subscriptions for company financials and patent intelligence supported cross checks on revenue direction and technology refresh signals. This list is not exhaustive, and other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating procedure volumes, typical component mix, and pricing movement across regions, since these drivers change by reimbursement and hospital procurement practices. We spoke with a mix of device ecosystem participants and clinical stakeholders, and balanced inputs across APAC, EMEA, and the Americas to avoid over-generalizing regional adoption timing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 39% |

| Mid tier: 51% | Functional/Unit leaders: 42% | EMEA: 35% |

| Smaller Players: 15% | Managers: 46% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top down approach where epidemiology and treated population logic are converted into a procedure based demand pool, and then translated into annual device revenue through utilization and pricing assumptions. The model starts with diagnosed and treated patients for key DBS indications, and then applies annual implant and replacement rates (including revision behavior) to estimate the number of systems and components consumed.

To keep outputs grounded, we corroborated results with selective bottom up approximations such as sampled average selling price (ASP) ranges by region, channel checks on hospital purchasing patterns, and sanity checks on component mix per procedure. Key inputs tracked include DBS implant volumes, replacement cycle assumptions, share of rechargeable versus non rechargeable pulse generators, lead and extension attach rates, and regional reimbursement coverage trends. For forecasting, scenario analysis was used, and adoption curves were adjusted using expert consensus on referral growth, center capacity limits, and the pace of new indication uptake. Where gaps existed in country level volume signals, we used proxy metrics like neurosurgery center counts and reimbursement availability, and then calibrated back to regional totals.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as procedure trend direction, reimbursement updates, and the timing of major product refreshes, and then exceptions were investigated before final sign off. Large variances triggered a return to assumptions, followed by targeted re contacts with interviewees to confirm whether the shift came from volumes, pricing, or mix.

A multi step review is followed, where a second analyst rechecks arithmetic, unit logic, and country aggregation, and then a lead reviewer validates that assumptions align with public policy and clinical practice. Reports are refreshed annually, and interim updates are made when material events occur such as major approvals, safety actions, or reimbursement rule changes. Before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Deep Brain Stimulation Devices Market Sizing Compared With Other Published Estimates

Published market values for DBS devices can look far apart, even when the topic name is the same, because the scope boundaries and the timing of price and currency assumptions are not aligned. Differences also show up when one study weights procedures more heavily and another leans on company revenue disclosures without checking how much comes from accessories, replacements, or services.

A refresh led gap is common in this market because ASPs shift when new rechargeable systems scale, discounting changes by tender cycles, and currency rates move year to year, so the time stamp used for conversion can sway the USD total. When we align pricing to the prevailing procurement period and re validate implant and replacement volumes with clinical and channel feedback before publishing, the spread seen below becomes easier to explain, a validation habit maintained by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.58 B (2026) | |

| Industry Publisher A | USD 0.95 B (2024) | Uses an earlier base year, and the value appears more conservative on procedure and replacement counting, which can understate revenue when accessory and replacement demand is rising. |

| Global Consultancy B | USD 1.54 B (2025) | Applies a different base year and horizon, and the total can move depending on how ASP progression is handled across rechargeable adoption and which currency conversion point is used for multi region aggregation. |

Taken together, the differences are mainly explained by base year selection, the way replacements and accessories are treated, and how pricing and currency timing are applied. By keeping the demand pool tied to procedures and then cross checking the revenue math with practical price and mix signals, we aim to provide a number that can be replicated and updated with clear inputs.

Key Questions Answered in the Report

How large will the deep brain stimulation devices market be by 2031?

It is forecast to reach USD 2.56 billion, up from USD 1.58 billion in 2026 at a 10.18% CAGR.

Which therapeutic area grows fastest in deep brain stimulation?

Treatment-resistant depression shows the strongest trajectory with an 10.74% CAGR through 2031 on the back of pivotal trial momentum.

Why are ambulatory surgical centers gaining share in DBS procedures?

Enhanced recovery protocols and reduced overhead lower per-procedure cost by up to 25%, drawing payor support and boosting ASC volumes.

What technology shift most influences future DBS device adoption?

Sensing-enabled closed-loop generators that auto-adjust stimulation based on neural activity improve outcomes and cut clinic visits.

Which region is set to add the most new DBS capacity?

Asia-Pacific, driven by large-scale neurosurgeon training programs and supportive government neurotechnology policies.

How does battery longevity affect patient economics?

Rechargeable IPGs lasting up to 15 years slash revision surgeries by 60%, lowering lifetime costs and infection exposure.

Page last updated on: