Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.72 Billion |

| Market Size (2031) | USD 6.05 Billion |

| Growth Rate (2026 - 2031) | 10.21% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

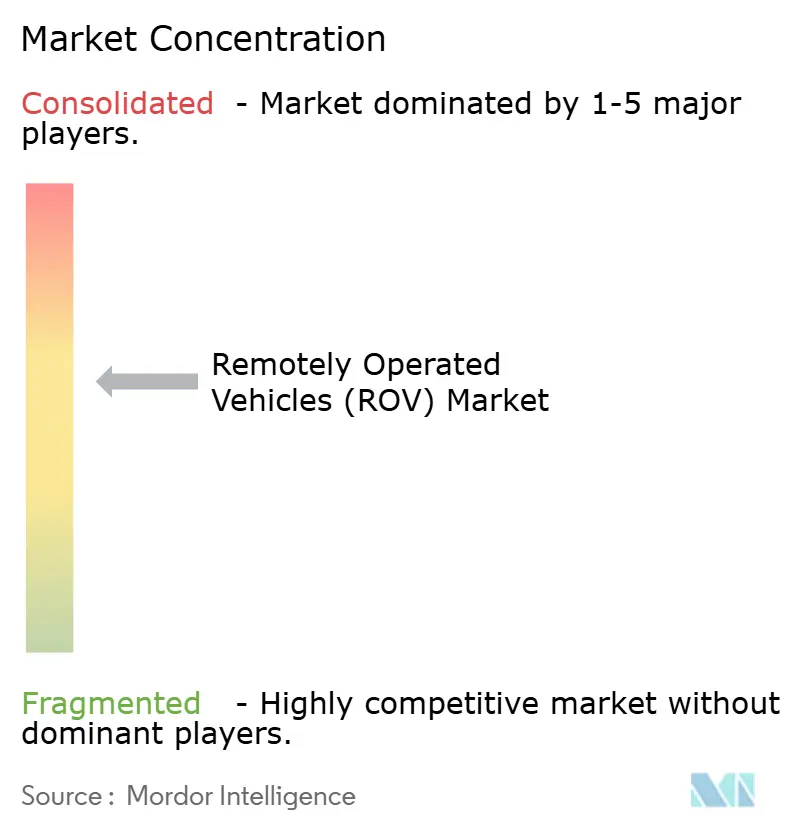

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Remotely Operated Vehicles (ROV) Market Analysis by Mordor Intelligence

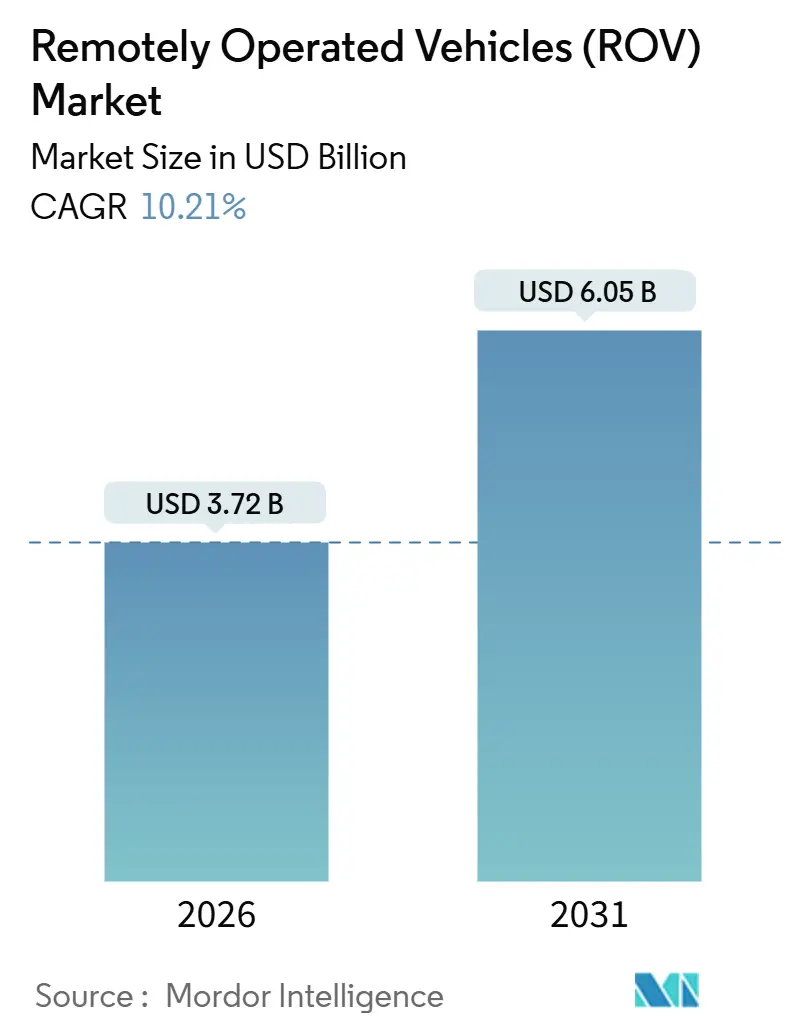

The Remotely Operated Vehicles Market size is estimated at USD 3.72 billion in 2026, and is expected to reach USD 6.05 billion by 2031, at a CAGR of 10.21% during the forecast period (2026-2031).

Rising multi-year capital programs in ultra-deep reservoirs and a parallel boom in offshore wind construction are rewriting the subsea economics that underpin the Global ROV market. National oil companies in the Middle East and Latin America are resuming pre-pandemic drilling schedules, European utilities are laying thousands of kilometers of inter-array cable that need frequent inspection, and battery breakthroughs are extending mission endurance for electric vehicles, enlarging the addressable Global ROV market. Work-class systems dominate heavy-lift tasks, yet shallow-water fleets are scaling quickly in response to turbine-foundation inspections. Operators with resident vehicles docked subsea are already reducing mobilization days and cutting inspection turnaround times, sharpening competitive dynamics inside the Global ROV market.

Key Report Takeaways

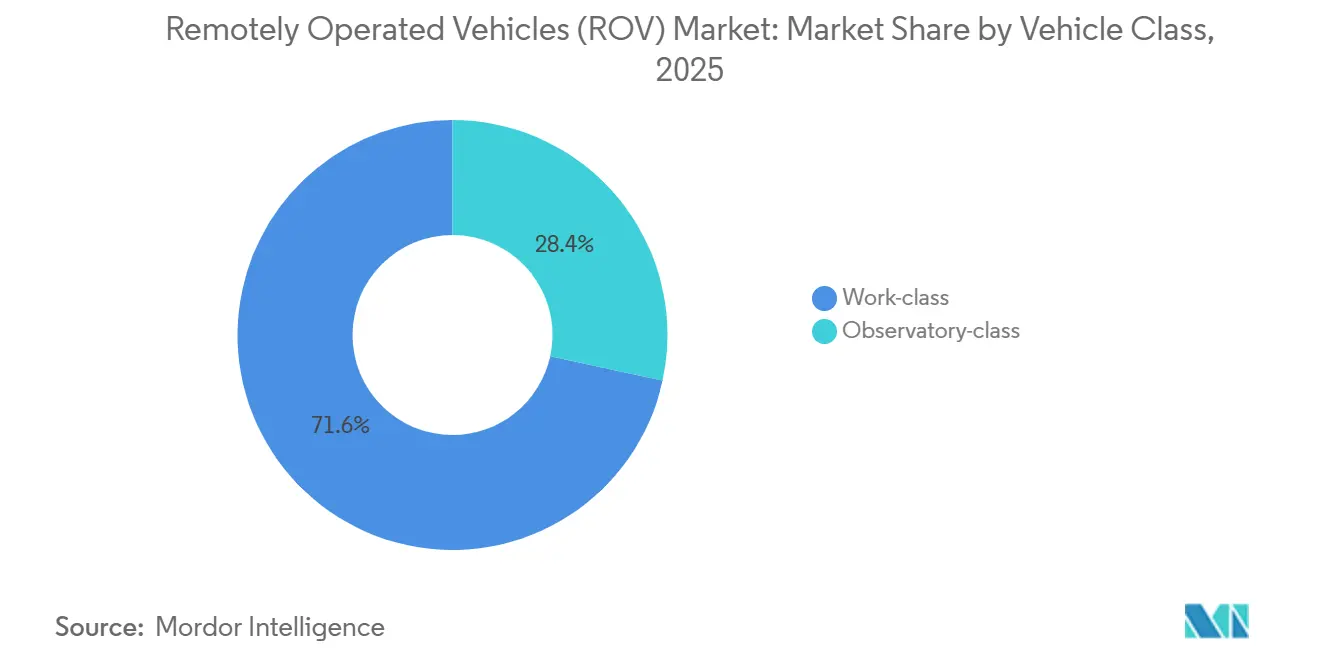

- By vehicle class, work-class platforms held 71.6% of the Global ROV market share in 2025 and are forecast to expand at an 11.7% CAGR to 2031.

- By depth rating, deep-water operations above 1,000 meters captured 56.3% of revenue in 2025, while shallow-water deployments up to 300 meters are advancing at a 13.1% CAGR.

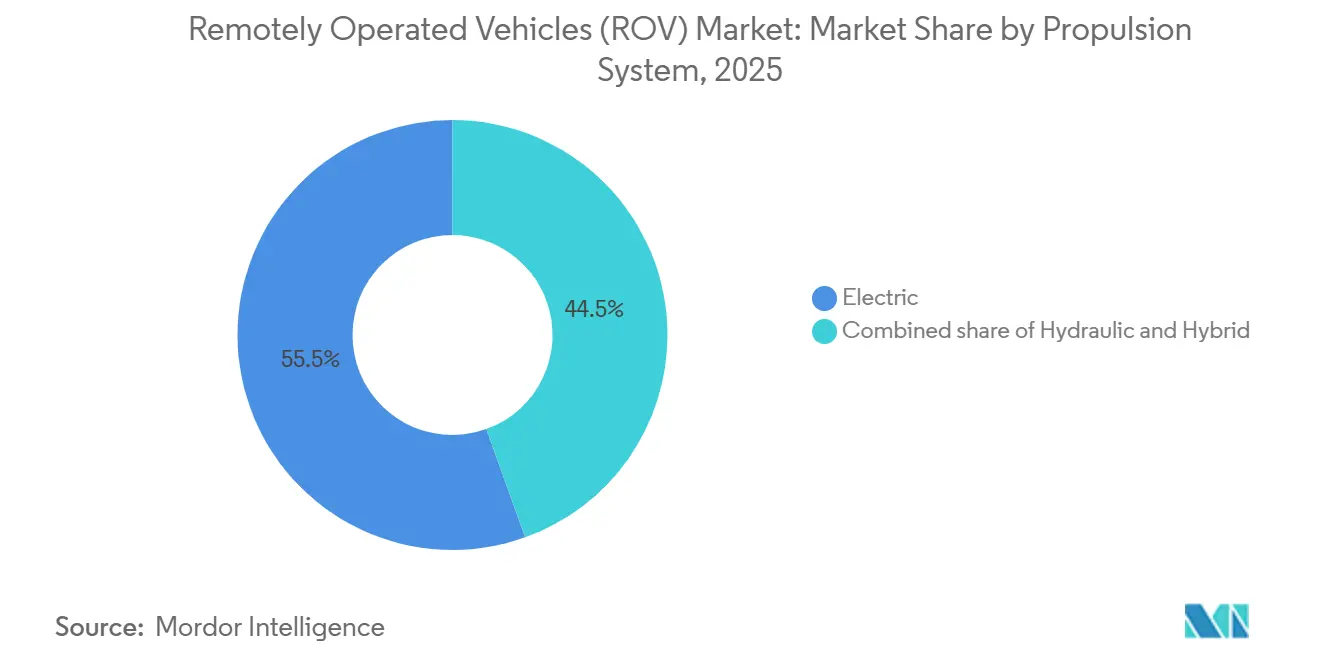

- By propulsion system, electric vehicles commanded 55.5% of 2025 revenue, growing at an 11.3% CAGR through 2031.

- By activity, inspection-repair-maintenance accounted for 34.7% of spending in 2025 and is rising at an 11.0% CAGR.

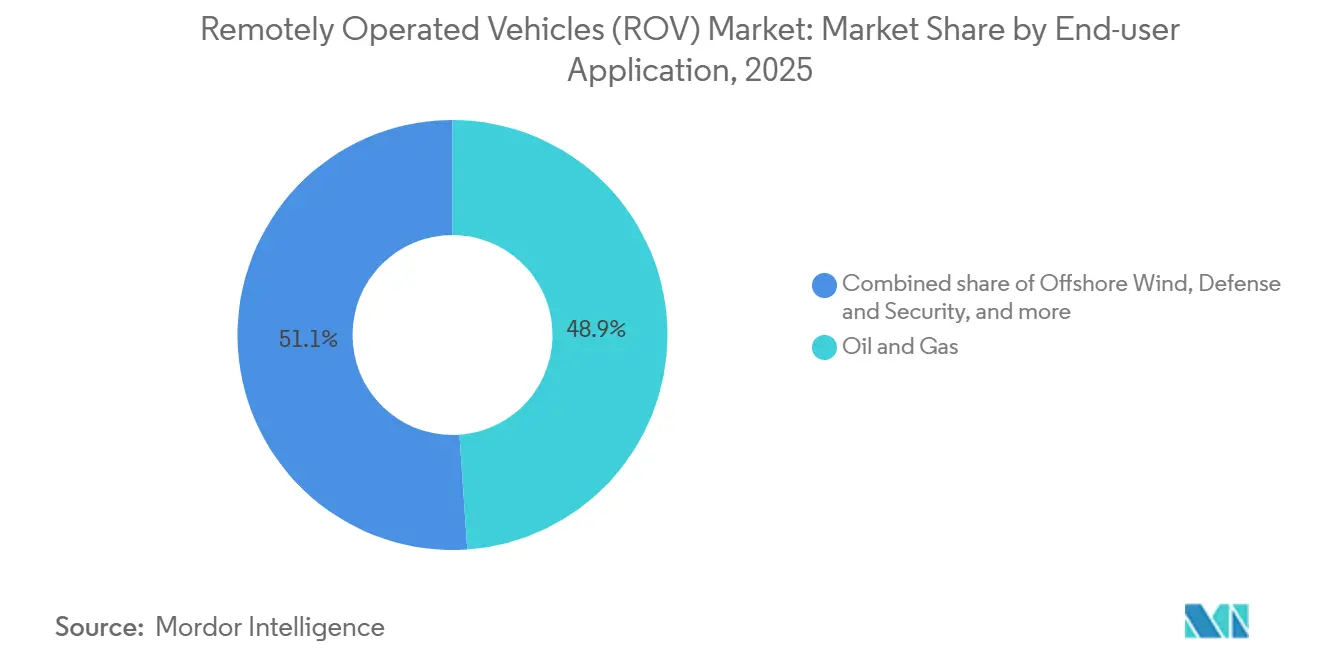

- By end-user application, oil and gas led with 48.9% of revenue in 2025, yet offshore wind is the fastest-growing segment at an 18.8% CAGR.

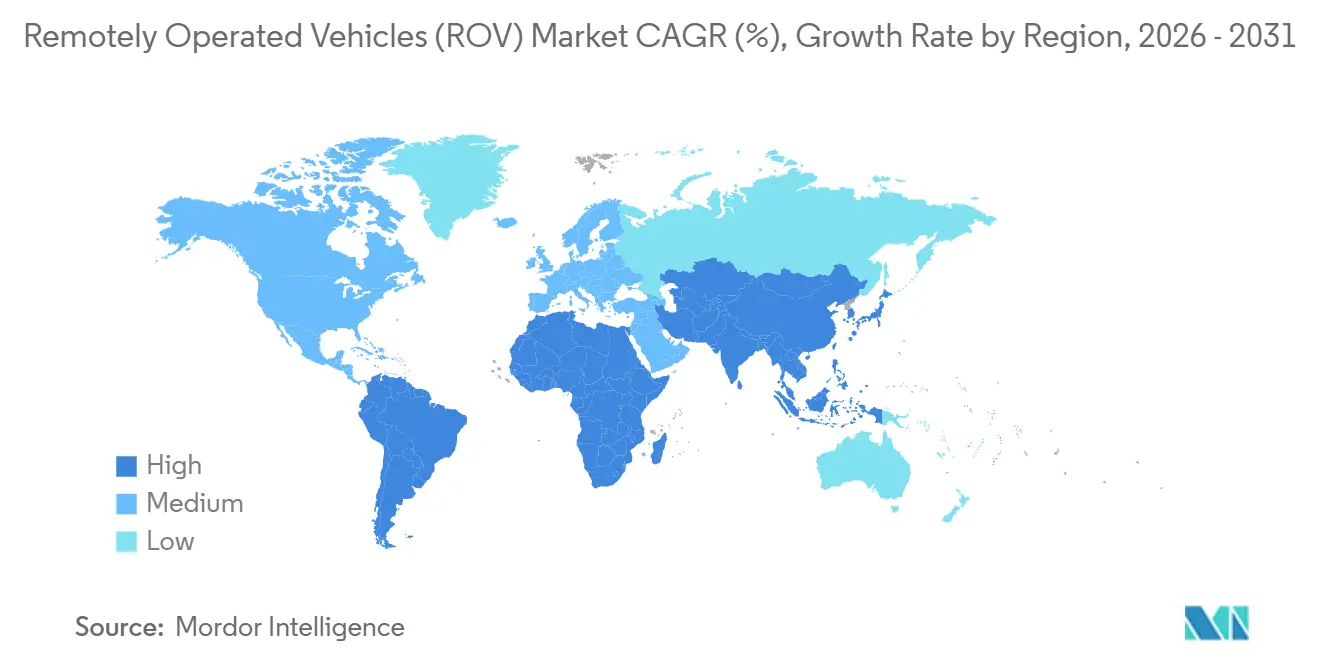

- By geography, North America held 37.1% of 2025 revenue, while Europe is the fastest-advancing region at a 16.5% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Remotely Operated Vehicles (ROV) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Offshore Oil & Gas Exploration Capex Rebound | 2.50% | Gulf of Mexico, North Sea, Brazil, Middle East | Medium term (2-4 years) |

| Expansion of Offshore Wind Farms and Subsea Cabling | 2.80% | UK, Norway, Denmark, Germany, China, Taiwan, South Korea | Long term (≥ 4 years) |

| Rising IRM Demand for Ageing Subsea Infrastructure | 1.90% | Gulf of Mexico, North Sea, mature Asian fields | Medium term (2-4 years) |

| Deep-Water Capex Surge by NOCs | 1.70% | Saudi Arabia, UAE, Qatar, Brazil, Mexico, Nigeria, Angola | Long term (≥ 4 years) |

| Resident ROV Systems Enabled by Subsea Docking | 0.80% | Early adoption in Gulf of Mexico and North Sea | Long term (≥ 4 years) |

| Seabed Mineral-Mining Pilot Programs | 0.50% | Clarion-Clipperton Zone, Indian Ocean | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Offshore Oil & Gas Exploration Capex Rebound

Global upstream budgets have normalized after the 2020-2023 downturn, with Chevron allocating USD 14.5 billion to upstream in 2025, much of it in the Gulf of Mexico.[1]Chevron Corporation, “Investor Presentation 2025,” chevron.com Shell’s Whale project reached first oil in late 2024 at 2,500 meters and required continuous work-class support.[2]Reuters, “Shell Whale Project First Oil,” reuters.com Fitch Ratings expects annual upstream spending to top USD 500 billion through 2027, with deep-water claiming 22% of that outlay.[3]Fitch Ratings, “Upstream Capex Outlook 2025-2027,” fitchratings.com The International Energy Agency projects offshore production to rise by 1.8 million barrels per day between 2025 and 2030, almost entirely from deep-water assets.[4]International Energy Agency, “World Energy Outlook 2025,” iea.org These commitments enlarge the Global ROV market because only heavy work-class units can handle hydraulic manipulation at depths beyond 1,500 meters.

Expansion of Offshore Wind Farms and Subsea Cabling

Europe is on track for 120 gigawatts of offshore wind by 2030, requiring 35,000 kilometers of cables that must be inspected annually. Ørsted’s Hornsea 3 will install 231 turbines across 696 square kilometers and deploy shallow-water vehicles for foundation surveys. Equinor’s Hywind Tampen floating project introduced mooring-line inspections that depend on multi-beam-equipped ROVs. China surpassed 40 gigawatts in 2025 and targets 100 gigawatts by 2030, generating sustained procurement of battery-electric units. The Celtic Sea leasing round added 4.5 gigawatts with contracts mandating yearly scour assessments, guaranteeing decades of recurring demand.

Rising IRM Demand for Ageing Subsea Infrastructure

The Gulf of Mexico hosts more than 2,000 wells installed before 2010, and inspection cycles have shortened from five to three years as corrosion accelerates. Oceaneering reported a 14% rise in IRM awards during the first nine months of 2024, lifting utilization to 69%. TechnipFMC secured a five-year North Sea framework in 2025 covering 120 trees and 18 manifolds. Norway requires annual assessments on installations older than 15 years, creating a USD 800 million captive market. Subsea 7’s resident vehicle cut inspection turnaround from 21 days to 7 days, demonstrating the efficiency gains resonating across the Global ROV market.

Deep-Water Capex Surge by NOCs

Saudi Aramco’s Marjan and Berri redevelopments include deep-water tie-backs running to 2028. Petrobras allocated USD 102 billion for 2025-2029, with 60% for pre-salt prospects deeper than 2,000 meters. ADNOC awarded a USD 1.65 billion subsea system for Hail and Ghasha in early 2025. Mexico’s Pemex restarted Perdido exploration in 2024, issuing multi-year vehicle tenders. IMCA estimates national companies represented 58% of subsea capex in 2024, up from 47% in 2020.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Offshore E&P Moratoriums & Environmental Activism | -0.60% | California, U.S. Atlantic, select European zones | Short term (≤ 2 years) |

| High Capex & OPEX of Work-Class ROV Fleets | -0.40% | Global, smaller contractors | Medium term (2-4 years) |

| Regulatory Grey Zones for Autonomous Subsea Ops | -0.30% | Global | Medium term (2-4 years) |

| Fiber-Optic Umbilical Bandwidth Constraints | -0.20% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Offshore E&P Moratoriums & Environmental Activism

The U.S. federal pause on new leases announced in 2025 removed 12 million acres from near-term exploration. California extended its drilling moratorium to 2030, freezing ROV demand in the Santa Barbara Channel. Norway deferred Barents licensing until impact studies finish in 2027. The EU’s Renewable Energy Strategy closed 18% of the North Sea to hydrocarbon activity. Meanwhile, environmental groups pressured the International Seabed Authority to postpone commercial mining licenses until 2028.

High Capex & OPEX of Work-Class ROV Fleets

A heavy work-class system costs more than USD 5 million, and yearly operations add USD 1.2 million. Fleet utilization must average 75% across 320 days for a 15% return, a ratio only consistent in the Gulf of Mexico and the North Sea. DOF Subsea sold eight older units in 2024 during restructuring to ease debt. Smaller contractors struggle to secure financing because lenders view the assets as specialized with limited resale value. Although resident units trim long-run OPEX, they require high upfront investment in docking infrastructure, further elevating barriers to entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Class: Work-Class Units Anchor Deep-Water Complexity

Work-class systems held 71.6% of the ROV market share in 2025 and will climb at an 11.7% CAGR to 2031. The ROV market size for work-class units is projected to expand by USD 1.9 billion over the forecast, reflecting monopoly on tasks that demand 200-kilogram manipulator force. Saab Seaeye launched the Leopard in 2024, pairing electric transit with hydraulic lift to cut fuel use 18%. Observatory-class vehicles remain essential for shallow inspections but command lower day rates. Forum’s Sub-Atlantic Mohawk Lite targets mid-tier tasks with a tool skid that reconfigures in under two hours. This bifurcation ensures parallel growth paths inside the ROV market as offshore wind favors compact electric units while oil and gas relies on heavy work-class capacity.

Work-class innovations now center on fiber-optic telemetry that enables real-time 4K video, closing a data gap that historically forced post-mission downloads. Oceaneering’s Millennium Plus demonstrated seamless multi-beam streaming in Gulf of Mexico trials. Smaller observatory fleets focus on agility and battery endurance, typified by VideoRay’s Pro 5 with a 10-hour lithium-ion package. Hybrid architecture is emerging as a compromise, letting operators satisfy environmental guidelines without sacrificing payload.

By Depth Rating: Shallow-Water Momentum from Offshore Wind

Deep-water projects above 1,000 meters controlled 56.3% of revenue in 2025, yet shallow-water fleets up to 300 meters are pacing the Global ROV market at a 13.1% CAGR. The Global ROV market size for shallow-water operations is projected to more than double by 2031 as turbine-foundation inspections proliferate. Ørsted’s Hornsea 3 requires annual verification across 231 turbines located at 40-60 meters. VideoRay’s Pro 5 and Deep Trekker’s Revolution target this domain with battery swaps under five minutes.

Mid-water zones covering 300-1,000 meters serve mature North Sea fields and deeper coastal wind sites. EU directives mandate yearly cable checks in waters shallower than 200 meters, creating a captive shallow-water revenue stream of USD 450 million annually. These compliance obligations ensure long-run visibility for operators pursuing recurrent contracts inside the Global ROV market.

By Propulsion System: Electric Vehicles Scale on Efficiency

Electric systems secured 55.5% revenue in 2025 and are moving ahead at an 11.3% CAGR thanks to 14.8 kilowatt-hour battery packs that support eight-hour missions. The Global ROV market share for electric units will widen as marine protected areas restrict hydraulic leaks. Kongsberg’s eROV prototype leverages hybrid energy storage, switching to fuel cells for resident deployments. Norway’s safety regulator now encourages electric or hybrid propulsion within 500 meters of protected zones.

Hydraulic units still rule heavy intervention work because manipulator force remains unmatched. Saab Seaeye’s Sabertooth hybrid demonstrates that pairing electric thrusters with hydraulic power can reduce consumption 22% while preserving lift capacity. The propulsion pivot underscores how environmental compliance and cost efficiency are converging inside the Global ROV market.

By Activity: IRM Outpaces Drilling and Construction

Inspection-repair-maintenance commanded 34.7% revenue in 2025 and is growing at an 11.0% CAGR, reflecting North Sea life-extension programs and Gulf of Mexico integrity mandates. The Global ROV market size for IRM is on course to surpass USD 2 billion by 2031 as decommissioning accelerates. Subsea 7’s resident vehicle cut mobilization costs by 40% during a 2024 pilot. Drilling support remains vital for Brazil, West Africa, and Mexico where blowout-preventer installation demands heavy work-class capacity.

Construction work is buoyant in offshore wind, with 35,000 kilometers of cable laying planned across Europe and Asia by 2030. Environmental monitoring remains a modest segment but is expanding as developers conduct benthic surveys under EU directives, reinforcing the recurrent inspection cycle that underpins the Global ROV market.

By End-User Application: Offshore Wind Becomes the Growth Engine

Oil and gas retained 48.9% of revenue in 2025, yet offshore wind’s 18.8% CAGR leads future expansion. Europe alone will need yearly surveys on 120 gigawatts of turbines by 2030. China targets 100 gigawatts by 2030, favoring electric fleets that avoid hydraulic leakage. Equinor’s Hywind Tampen demands dynamic-cable inspection, modulating tooling requirements for Global ROV industry vendors.

Defense, research, and aquaculture form smaller but growing niches. Navies are adopting mine-countermeasure vehicles, while salmon farms in Norway deploy compact units for net checks, broadening the Global ROV market beyond traditional energy clients.

Geography Analysis

North America generated 37.1% of 2025 revenue, anchored by Gulf of Mexico lease rounds that drew USD 382 million in bids. Chevron’s upstream budget signals a durable deep-water appetite, and Canada’s approvals in Newfoundland add new drilling campaigns through 2027. Pemex revived Perdido exploration in 2024, enhancing medium-term demand. Policy headwinds persist as the federal leasing pause and California moratorium constrain near-shore growth.

Europe is the fastest-advancing region with a 16.5% CAGR, scaling the Global ROV market through offshore wind build-out and decommissioning. The Crown Estate’s Celtic Sea leases add 4.5 gigawatts with compulsory yearly inspections. Norway’s annual integrity rules create a USD 800 million captive IRM market. Denmark’s Energinet let contracts for 1,200 kilometers of export cables in 2024. Germany targets 30 gigawatts of wind by 2030.

Asia-Pacific, the Middle East, and Latin America represent high-growth corridors. China already crossed 40 gigawatts of offshore wind in 2025. India’s ONGC awarded contracts for deep-water KG-Basin blocks. Saudi Aramco, Petrobras, and ADNOC together plan more than 60 subsea trees per year through 2028, sustaining heavy work-class utilization. ASEAN pipeline inspection work is rising as Malaysia and Indonesia expand gas exports.

Competitive Landscape

The top five operators, Oceaneering, TechnipFMC, Subsea 7, Fugro, and DOF Subsea, control roughly 62% of worldwide fleet capacity, indicating moderate concentration. Oceaneering’s 250-unit fleet achieved 69% utilization and USD 10,576 daily revenue per vehicle in Q3 2024. TechnipFMC bundles ROV services with production systems, deepening client lock-in. Subsea 7 leads resident deployments, logging 92% uptime in its pilot. Disruptors such as Blue Robotics and Deep Trekker supply low-cost electric units that suit offshore wind developers and research institutes.

Strategic priorities include resident operations, hybrid propulsion, and high-bandwidth telemetry. Oceaneering’s Liberty e-ROV trims vessel days, Saab Seaeye’s Sabertooth cuts fuel 22%, and Fugro is partnering with Kongsberg on autonomous cable-inspection vehicles. Autonomous and semi-autonomous deployments account for less than 3% of fleet hours, suggesting ample runway as DNV’s remote-operations framework gains traction.

Remotely Operated Vehicles (ROV) Industry Leaders

DeepOcean AS

DOF Subsea AS

Oceaneering International Inc.

TechnipFMC PLC

Helix Energy Solutions Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Indian Navy signed an INR 47 crore contract with Kochi-based startup EyeROV for advanced underwater ROVs, including the Trout model. These ROVs, equipped with high-definition cameras and payload options, are rated for deep operations and will support underwater reconnaissance, inspection, and surveillance missions, enhancing indigenous naval capabilities.

- March 2025: Forum Energy Technologies (FET) signed a contract to sell its Sub Atlantic Super Mohawk II ROV and launch/recovery system to a North American subsea group. The observation-class ROV will support shallow water tasks such as riverbed surveying and inspection, marking FET’s entry into riverine ROV applications alongside its offshore operations.

- January 2025: At India’s Auto Expo 2025, Lexus showcased a hydrogen-powered ROV (Recreational Off-highway Vehicle) concept designed for off-road driving, alongside the LF-ZC electric sedan. The ROV combines rugged off-road capabilities with sustainability, offering a premium lifestyle vehicle aimed at navigating diverse terrains while exploring future mobility trends.

- January 2025: FET’s Subsea product line will supply a Perry XLX EVO II ROV and Dynacon LARS system to ACSM, a global maritime survey and ROV services operator. Scheduled for delivery in Q3 2025, the ROV will assist with construction support, pipeline/platform inspection, surveys, salvage, and dredging in challenging underwater environments.

Global Remotely Operated Vehicles (ROV) Market Report Scope

A remotely operated vehicle (ROV) is an unoccupied robot, a highly maneuverable underwater machine attached to a series of cables that can explore ocean depths. These cables convey command and control signals between the operator and the ROV, allowing remote vehicle navigation.

The ROV market is segmented by vehicle class, depth rating, propulsion system, activity, end-user application, and geography. By vehicle class, they are segmented into work-class and observatory-class. By depth rating, the market is divided into shallow, mid-water, and deep-water. By propulsion system, the market is divided into electric, hydraulic, and hybrid. By activity, the market is segmented into drilling and development, construction and installation, IRM, and others. By end-user application, the market is segmented into oil and gas, offshore wind, defense and security, and Others. The report also covers the market size and forecasts for the ROV market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Vehicle Class

| Work-class | Light Work-class |

| Medium Work-class | |

| Heavy Work-class | |

| Observatory-class |

By Depth Rating

| Shallow (Up to 300 m) |

| Mid-water (300 to 1,000 m) |

| Deep-water (Above 1,000 m) |

By Propulsion System

| Electric |

| Hydraulic |

| Hybrid |

By Activity

| Drilling and Development |

| Construction and Installation |

| Inspection, Repair and Maintenance (IRM) |

| Decommissioning |

| Environmental Monitoring |

By End-user Application

| Oil and Gas |

| Offshore Wind |

| Defense and Security |

| Research and Academia |

| Aquaculture and Marine Infrastructure |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Norway | |

| Denmark | |

| Germany | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Vehicle Class | Work-class | Light Work-class |

| Medium Work-class | ||

| Heavy Work-class | ||

| Observatory-class | ||

| By Depth Rating | Shallow (Up to 300 m) | |

| Mid-water (300 to 1,000 m) | ||

| Deep-water (Above 1,000 m) | ||

| By Propulsion System | Electric | |

| Hydraulic | ||

| Hybrid | ||

| By Activity | Drilling and Development | |

| Construction and Installation | ||

| Inspection, Repair and Maintenance (IRM) | ||

| Decommissioning | ||

| Environmental Monitoring | ||

| By End-user Application | Oil and Gas | |

| Offshore Wind | ||

| Defense and Security | ||

| Research and Academia | ||

| Aquaculture and Marine Infrastructure | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Norway | ||

| Denmark | ||

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Global ROV market today and where is it heading?

The Global ROV market size reached USD 3.72 billion in 2026 and is forecast to rise to USD 6.05 billion by 2031 at a 10.21% CAGR.

Which vehicle class dominates current demand?

Work-class units led with 71.6% revenue in 2025 because heavy manipulators and high payloads are essential for deep-water construction.

What end-user segment is expanding the fastest?

Offshore wind is advancing at an 18.8% CAGR as Europe and China lay thousands of kilometers of subsea cable that require annual inspection.

Why are electric propulsion systems gaining market share?

Battery advances are extending mission endurance beyond eight hours and regulators prefer zero-leakage vehicles in marine protected zones.

Which regions offer the strongest growth outlook?

Europe leads with a 16.5% CAGR thanks to wind build-outs and North Sea decommissioning, while Asia-Pacific follows on rapid Chinese capacity additions.

What is the competitive intensity among service providers?

The top five operators control around 62% of global fleet capacity, creating a moderately concentrated landscape with meaningful but not overwhelming pricing power.

Page last updated on: