Medical Alert System/Personal Emergency Response System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

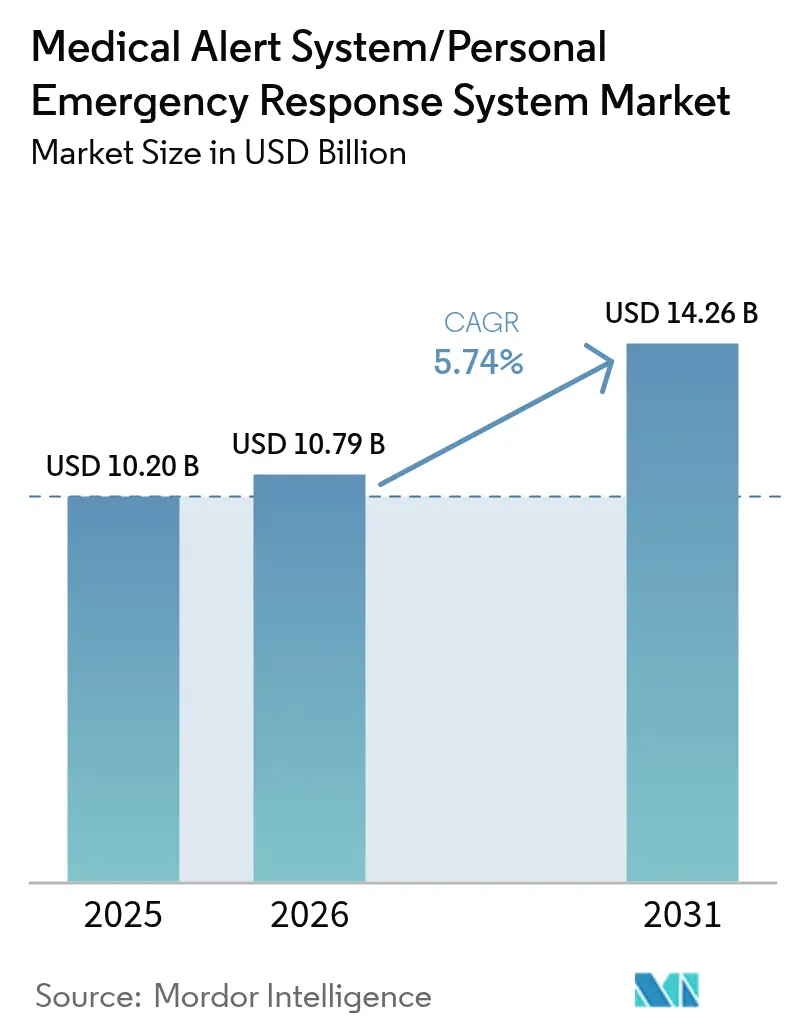

| Market Size (2026) | USD 10.79 Billion |

| Market Size (2031) | USD 14.26 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

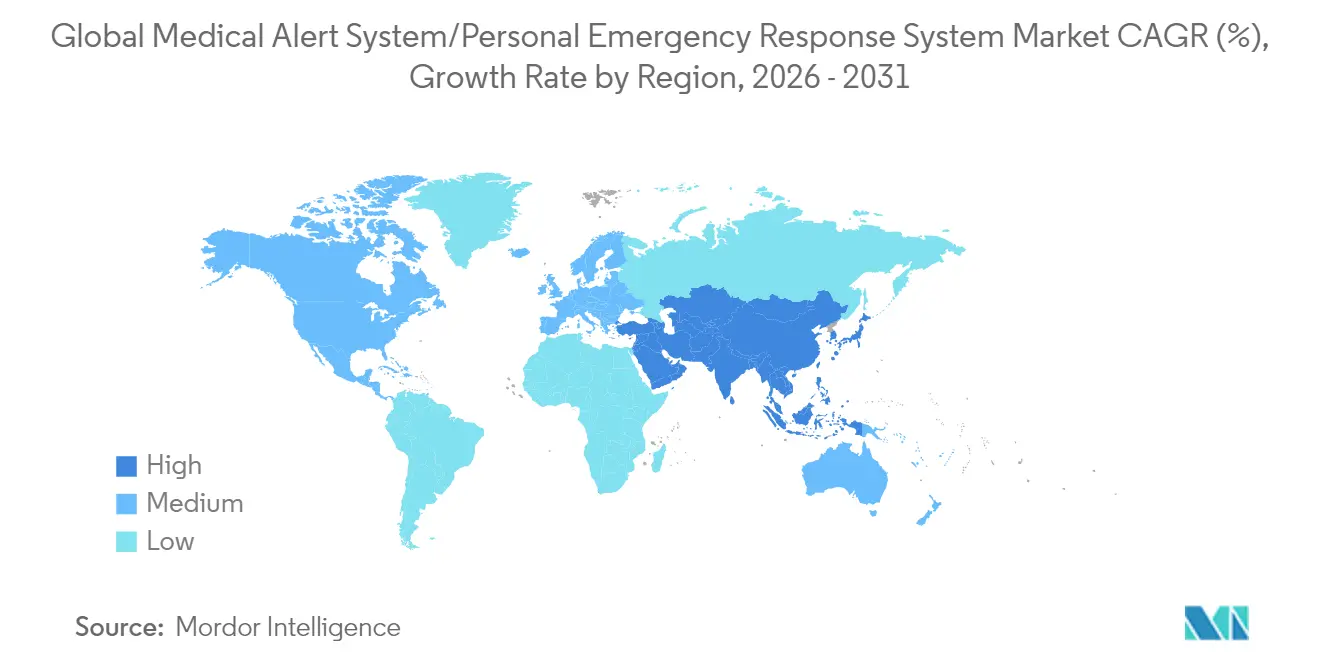

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Alert System/Personal Emergency Response System Market Analysis by Mordor Intelligence

The medical alert system/personal emergency response system market size in 2026 is estimated at USD 10.79 billion, growing from 2025 value of USD 10.20 billion with 2031 projections showing USD 14.26 billion, growing at 5.74% CAGR over 2026-2031. Demand is underpinned by simultaneous improvements in cellular, GPS, and voice-assistant technologies that shorten response times and enhance user peace of mind. Vendors now bundle alert devices inside remote patient monitoring kits, creating predictable subscription revenue from payers and provider groups. Medicare Advantage pilots, plus employer duty-of-care mandates for lone workers, are broadening the customer base and lifting average selling prices. An aging population with rising fall prevalence continues to fuel replacement cycles, while analytics allow insurers to demonstrate avoided emergency department costs. Competitive intensity is moderate as differentiation pivots on seamless device-to-cloud integration and predictive insights rather than hardware alone.

Key Report Takeaways

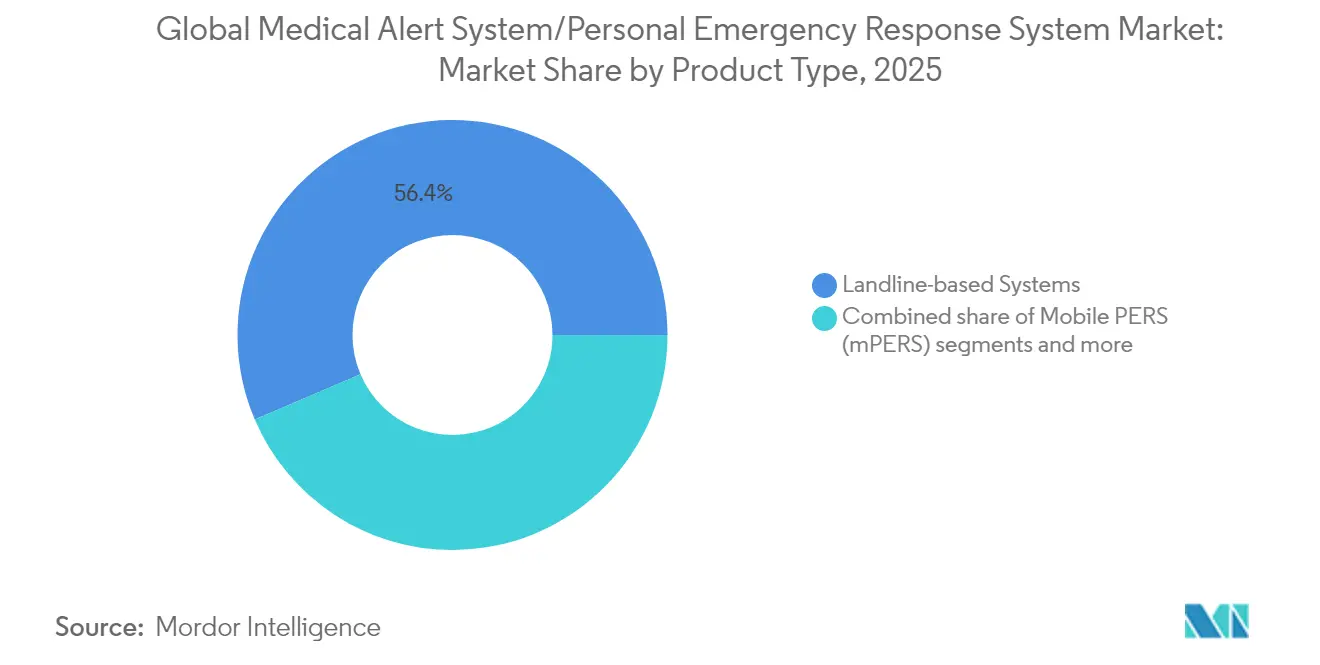

- By product type, landline-based systems held 56.42% of medical alert system/personal emergency response system market share in 2025 while mobile PERS is forecast to achieve a 6.05% CAGR through 2031.

- By connectivity technology, landline connections accounted for 60.10% of the medical alert system/personal emergency response system market size in 2025 and GPS-enabled platforms are expected to log the strongest 6.22% CAGR to 2031.

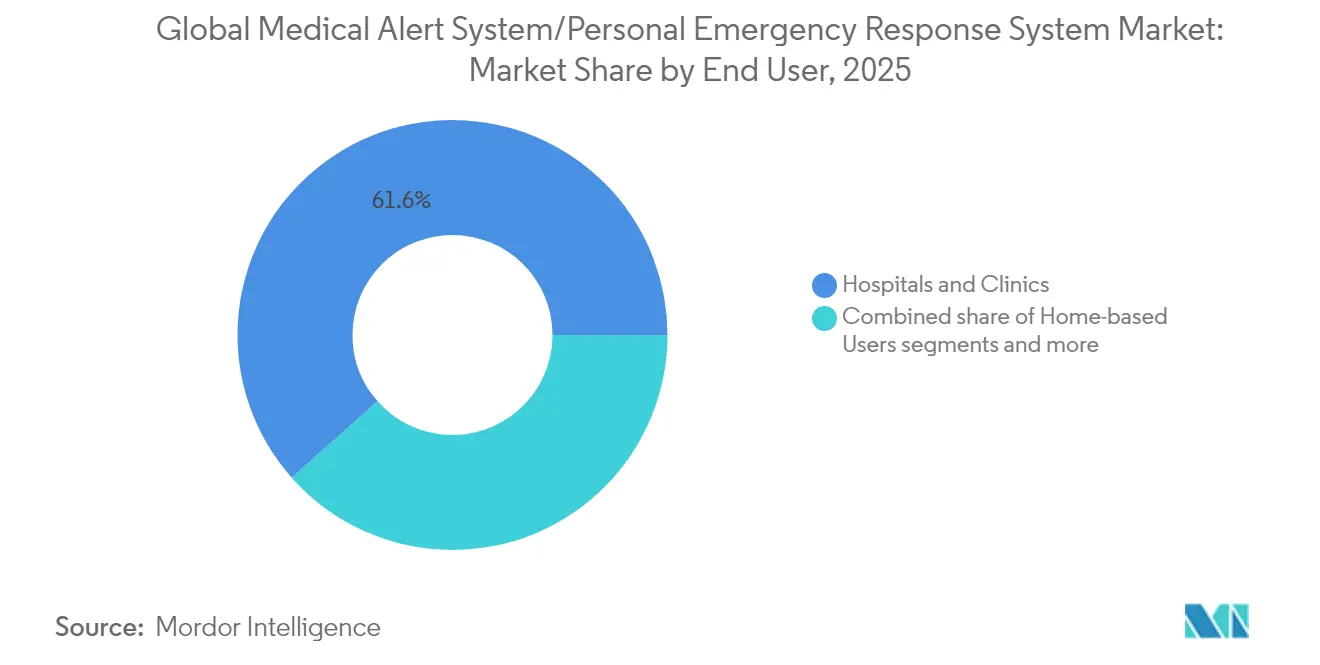

- By end user, hospitals and clinics represented 61.55% of medical alert system/personal emergency response system market share in 2025, whereas senior housing and assisted living facilities are likely to expand at a 6.35% CAGR during the forecast window.

- By component, hardware generated 11.60% revenue share in 2025, but software and services should post the fastest 6.55% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Alert System/Personal Emergency Response System Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & fall prevalence | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Shift toward independent living & home healthcare | +1.4% | Global | Medium term (2–4 years) |

| Advancements in fall detection, GPS & cellular tech | +1.2% | Global | Short term (≤ 2 years) |

| Integration with remote patient monitoring ecosystems | +1.0% | North America, Asia-Pacific | Medium term (2–4 years) |

| Insurance reimbursement pilots (Medicare Advantage etc.) | +0.9% | United States | Short term (≤ 2 years) |

| Duty-of-care adoption for lone workers | +0.7% | Europe, North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Aging population and higher fall prevalence

A steadily expanding cohort of adults aged 65 years and older raises the incidence of unintentional falls, which remain the leading cause of injury-related deaths among seniors. Hospitals and insurers acknowledge the economic benefit of rapid intervention, fueling procurement of monitored devices inside both homes and care institutions. Government guidelines in mature economies link long-term-care reimbursement to documented fall-prevention strategies, prompting hospital purchasing consortia to incorporate alert buttons into discharge bundles. Manufacturers respond with wearable designs that feature tactile surfaces and loud audio prompts for hearing-impaired users. These demographic and policy forces underpin recurring revenue from replacement and upgrade cycles.

Shift toward independent living and home healthcare

Caregivers, social-service agencies, and payers promote aging-in-place because it preserves quality of life and curtails institutional care costs. Vendors emphasize discreet wearables and smart-speaker integrations that let users call for help without complicated interfaces. Health systems running hospital-at-home pilots include compliant devices in supply kits so clinicians can intervene when biometric thresholds or fall events trigger alerts. Bundled wellness check-in calls and caregiver applications increase perceived value, stimulating subscription take-up.

Advances in fall detection, GPS, and cellular technologies

Tri-axial accelerometers, machine-learning models at the edge, and multi-constellation GNSS chips have increased motion-pattern accuracy while reducing false alarms. eSIM activation streamlines logistics, and dual-SIM designs improve redundancy in weak-signal areas. Capabilities once reserved for premium tiers—indoor positioning via Wi-Fi triangulation, proactive check-in reminders, and two-way voice—now appear in mid-priced units, driving mass-market adoption. With carriers sunsetting 3G, replacement demand spikes for LTE/GPS units, giving vendors a near-term volume lift[1]Source: Federal Communications Commission, “Transitioning From 3G Networks,” fcc.gov .

Integration with remote patient monitoring ecosystems

Open APIs feed fall alerts into electronic health record dashboards, allowing clinicians to correlate events with blood-pressure excursions or arrhythmias. Predictive models, enriched by PERS data, help care managers triage nursing visits and allocate resources effectively. Payers exploring capitated models subsidize hardware when enrollees consent to continual monitoring, which raises attach rates for connected vitals peripherals. Software portals give employer duty-of-care teams unified visibility, expanding enterprise use cases[2]Source: Centers for Medicare & Medicaid Services, “Hospital-at-Home Expands Coverage,” cms.gov .

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & subscription cost | −1.3% | Latin America, MEA | Short term (≤ 2 years) |

| False-alarm rates & workflow burden | −1.0% | Global | Medium term (2–4 years) |

| Privacy concerns with voice/GPS data | −0.9% | Europe, North America | Long term (≥ 4 years) |

| 2G/3G sunset driving hardware obsolescence | −0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High device and subscription cost

Retail prices remain prohibitive for low-income seniors in emerging markets, and monthly fees can consume a significant share of fixed pensions. Reimbursement across public health systems varies, leaving many households to self-finance solutions. Semiconductor inflation raises bill-of-materials costs, limiting how aggressively manufacturers can discount new LTE hardware. Rental programs mitigate upfront expense but have yet to achieve scale in rural districts, slowing diffusion where budget sensitivity is acute.

False-alarm rates and workflow burden

Accelerometer thresholds sometimes classify rapid sitting motions as falls, prompting unnecessary dispatches and driving up call-center labor expense. Repeated false positives can erode user trust and hamper rollout in institutional settings. Vendors deploy firmware updates that incorporate context signals such as barometric pressure or gyroscope data, but model retraining requires large labeled datasets and time. Until accuracy improves, purchasing committees remain cautious about institutional upgrades, especially in regulated hospital environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile momentum accelerates

Landline-based units captured 56.42% of medical alert system/personal emergency response system market share in 2025 because many seniors view the fixed button as reliable and familiar. Hospitals also perceive low technical risk, preserving their deployments in rehabilitation wings. Growth, however, is shifting toward mobile PERS, which is projected to expand at a 6.05% CAGR through 2031. Cellular connectivity lets active seniors feel protected while shopping, driving, or exercising outdoors. Vendors enhance devices with two-way voice that automatically routes calls to monitoring stations. Data plans bundled in the monthly fee help carriers secure recurring revenue. In rural areas that lack robust LTE coverage, the basic fixed pendant will remain relevant, but nationwide marketing campaigns focus on mobile freedom.

The medical alert system/personal emergency response system market size for mobile PERS will grow as manufacturers add voice-assistant functionality, enabling medication reminders or weather queries. Hybrid “all-in-one” models that connect via landline at home and cellular outside the premises introduce redundancy, appealing to risk-averse caregivers. Stand-alone wall buttons serve budget shoppers but face competitive pressure from smart-watch applications that piggyback on consumer wearables. Voice-activated speakers, meanwhile, attract users with dexterity challenges and integrate smoothly into broader smart-home ecosystems offered by telecom operators. Portfolio variety will be key to retaining users across different activity levels and price points.

By Connectivity Technology: GPS leads future adoption

Landline telephony commanded 60.10% of medical alert system/personal emergency response system market size in 2025, reflecting years of PSTN reliance in North America and Western Europe. Carrier copper retirement plans, however, will gradually erode this base, pushing households toward cellular or VoIP alternatives. GPS-enabled devices are primed to realize the fastest 6.22% CAGR through 2031 because next-generation chipsets improve indoor-location precision and shorten emergency response times. Accurate geolocation reduces false dispatches to incorrect addresses, improving trust among public safety agencies.

Dual-mode devices that switch between landline and cellular networks smooth the migration path and guard against single-network outages. Bluetooth and Wi-Fi beacons help institutions achieve room-level tracking inside large campuses, aiding compliance documentation for state inspections. As 5G coverage widens, low-latency video streaming will enable real-time teletriage for complex incidents, further differentiating cellular-first models. Cost, however, remains a barrier in lower-income geographies, so vendors offer trade-in rebates to accelerate user transitions from analog to digital infrastructure.

By End User: Institutional dominance rises

Hospitals and clinics represented 61.55% of medical alert system/personal emergency response system market share in 2025 after administrators embedded devices into post-discharge care bundles aimed at lowering readmissions. Emergency departments also deploy alert buttons on inpatient beds to ensure rapid assistance during overnight shifts. The segment will maintain volume leadership because value-based purchasing incentives reward proven intervention technologies. Senior housing and assisted living facilities, meanwhile, are forecast to grow at a 6.35% CAGR through 2031. Operators install enterprise dashboards that monitor hundreds of residents simultaneously and integrate incident data with electronic medication administration records. Bulk procurement lowers per-unit costs, and staff training programs ensure consistent triage.

Home-based users remain important even though their proportional share has declined. Families appreciate self-install kits priced under USD 30 monthly that pair pendants with caregiver smartphone apps. Lone-worker verticals such as utility maintenance and social work adopt ruggedized variants, but demand is price sensitive and often tied to corporate risk budgets. Vendors building firmware that toggles between medical and occupational safety protocols will capture this cross-vertical opportunity, reinforcing revenue diversity.

By Component: Services sprint ahead

Hardware produced 11.60% revenue share in 2025 as many suppliers still rely on device sales before layering monitoring fees. Commoditization squeezes margins and encourages a transition toward cloud dashboards and analytics, which are projected to log a 6.55% CAGR through 2031. Predictive algorithms analyze historical activity to flag elevated fall risk and notify care managers of early intervention opportunities. Subscription bundles now include caregiver portals, medication prompts, and telehealth escalation buttons that connect to a nurse triage line. These add-ons raise average revenue per user without requiring costly hardware redesigns.

The medical alert system/personal emergency response system market size for software and services will expand as hospitals prove that data-driven triage improves quality metrics. White-label portals allow insurers to brand wellness dashboards under chronic-care initiatives, generating incremental B2B revenue for technology vendors. Hardware innovation will persist but focus on modular add-ons such as wall-mounted radar sensors that detect motion without wearables. Nonetheless, sticky recurring revenue tied to analytics will remain the primary growth engine.

Geography Analysis

North America controlled 43.80% of the medical alert system/personal emergency response system market in 2025, supported by Medicare Advantage supplemental benefits that subsidize monitored alert devices. Retail distribution through big-box pharmacies and e-commerce accelerates activation, while carrier marketing emphasizes fast LTE coverage. Canadian provinces allocate telehealth budgets that include PERS, and remote communities rely on satellite backhaul to mitigate cellular gaps. Competitive positioning now centers on electronic health record integration and HIPAA-compliant data storage, which resonate with hospital CIOs.

Europe follows closely, with Germany, the United Kingdom, and France leading adoption. National health insurers reimburse device subscriptions when prescribed by physicians, lowering out-of-pocket expense for seniors. The medical alert system/personal emergency response system market size in Southern Europe is smaller due to fragmented payer models, yet EU digital-health grants fund pilot rollouts in Italy and Spain. General Data Protection Regulation compliance shapes product architecture, requiring local data residency options. Although Brexit has increased certification paperwork, U.K. demand remains resilient because local councils earmark age-friendly community budgets for safety technology.

Asia-Pacific is forecast to post the fastest 6.85% CAGR to 2031, led by Japan, South Korea, and China where population aging is most advanced. Japanese municipalities subsidize devices for seniors living alone and integrate alerts into citywide dispatch systems. Chinese manufacturers leverage domestic scale to release lower-priced hardware, widening access in rural provinces. In India, telecom operators bundle pendant rentals with prepaid data, enabling penetration among lower-income segments. Australia’s National Disability Insurance Scheme lists PERS in assistive-technology catalogs, fostering uptake among younger adults with mobility challenges.

Latin America and the Middle East & Africa remain nascent but promising. Brazil experiences gradual adoption inside private hospital chains, though currency volatility and import tariffs constrain premium imports. Argentina’s telecom regulators encourage VoIP devices that bypass patchy fixed-line infrastructure. Gulf Cooperation Council smart-city projects integrate alert sensors into age-friendly housing, but market value is small. South Africa pushes lone-worker monitoring in mining and security, creating niches for ruggedized wearables. Vendors pursuing tiered pricing and micro-financing instruments are best positioned to overcome affordability barriers.

Competitive Landscape

The competitive arena blends diversified electronics giants with specialized monitoring service providers. Koninklijke Philips refreshes its Lifeline portfolio with LTE upgrades and predictive analytics dashboards that classify subscriber fall risk. ADT leverages its nationwide security call centers and brand recognition to market rapid emergency dispatch. Tunstall Healthcare partners with municipal social-service agencies across Europe, supplying devices bundled with bilingual nurse triage. Connect America focuses on value-based care contracts, integrating its platform into population health software to evidence readmission avoidance.

Consumer electronics leaders Samsung Electronics and Huawei Technologies embed PERS functionality in smartwatches, cross-selling into established mobile ecosystems. Niche innovators such as QMedic and Freeus apply proprietary algorithms to detect deviations from baseline activity, reducing false positives. Best Buy Health exploits its Geek Squad network for in-home installation, differentiating through customer service. Regional providers like Bay Alarm and Guardian Medical Monitoring maintain community trust and fast local support, resonating with users wary of large brands.

Recent strategic maneuvers illustrate intensifying competition. In 2024, Medical Guardian embedded machine-learning modules in its MyGuardian portal to predict fall likelihood from gait speed. MobileHelp signed an exclusive distribution agreement with a leading pharmacy chain, securing prime end-cap shelf space. Essence SmartCare launched AI-enabled radar sensors that detect falls without wearables, potentially disrupting pendant dominance. Becklar’s Freeus unit acquired a Midwest operator to extend call-center redundancy and lower per-alarm costs. Forward integration with remote patient monitoring software is likely as players chase differentiated value beyond hardware.

Medical Alert System/Personal Emergency Response System Industry Leaders

Bay Alarm Medical

ADT Corporation

Connect America, LLC (Lifeline)

Life Alert Emergency Response Inc.

Medical Guardian LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nomo Smart Care revolutionized in-home care with artificial intelligence powered technology. Instead of cameras.

- November 2024: Vesta Healthcare and Medical Guardian collaborated to deliver a comprehensive chronic care management and remote patient monitoring (RPM) solution for Medicaid and Medicare members.

Global Medical Alert System/Personal Emergency Response System Market Report Scope

As per the scope of the report, personal emergency response systems (PERS), also known as medical emergency response systems, allow users to call for help during an emergency by pushing a button. The medical alert system/personal emergency response system market is segmented by type, end-user and geography. By type, the market is segmented into landline PERS, mobile PERS, and other types. Other types include standalone PERS, smart wearable devices and others. By end-user, the market is segmented into home-based users, assisted living facilities and other end-users. Other end users include nursing homes, hospitals and clinics, and others). By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of USD value.

| Landline-based Systems |

| Mobile PERS (mPERS) |

| Stand-alone Devices |

| Voice-Activated Systems |

| Cellular |

| Dual (Landline + Cellular) |

| GPS-enabled |

| Bluetooth / Wi-Fi |

| Home-based Users |

| Senior Housing & Assisted Living Facilities |

| Hospitals & Clinics |

| Lone Workers & Others |

| Hardware |

| Software & Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Landline-based Systems | |

| Mobile PERS (mPERS) | ||

| Stand-alone Devices | ||

| Voice-Activated Systems | ||

| By Connectivity Technology | Cellular | |

| Dual (Landline + Cellular) | ||

| GPS-enabled | ||

| Bluetooth / Wi-Fi | ||

| By End User | Home-based Users | |

| Senior Housing & Assisted Living Facilities | ||

| Hospitals & Clinics | ||

| Lone Workers & Others | ||

| By Component | Hardware | |

| Software & Services | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the medical alert system/personal emergency response system market in 2031?

It is expected to reach USD 14.26 billion, reflecting a 5.74% CAGR from 2026.

Which product type is expanding the fastest in this sector?

Mobile PERS is projected to grow at a 6.05% CAGR between 2026 and 2031.

Which region will experience the highest growth through 2031?

Asia-Pacific is set for the fastest 6.85% CAGR during the forecast period.

Why are hospitals leading device adoption?

Hospitals embed monitored pendants into post-discharge bundles to cut readmissions, giving them a 61.55% share of the market in 2025.

How is 3G sunset influencing hardware sales?

The shift to LTE and GPS-enabled devices accelerates replacement demand as legacy units become obsolete.

Page last updated on: