Riyadh Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.17 Billion |

| Market Size (2026) | USD 3.3 Billion |

| Market Size (2031) | USD 4.04 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Riyadh Construction Market Analysis by Mordor Intelligence

The Riyadh Construction Market size was valued at USD 3.17 billion in 2025 and estimated to grow from USD 3.3 billion in 2026 to reach USD 4.04 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). This steady expansion flows from Vision 2030’s USD 400 billion city-focused investment pool, which is reshaping land use, transportation, housing, and public amenities across the capital. The push is anchored by catalytic schemes such as the USD 180 billion New Murabba downtown and the King Salman International Airport, each positioned to elevate Riyadh’s global standing while unlocking large, multi-year workloads for contractors. Rapid contract-award momentum, stronger private-sector participation, and the institutionalization of digital design mandates further stabilize the growth path. At the same time, material-cost swings and labor shortfalls test profit margins, spurring faster uptake of modular building systems and localized material production hubs.

Key Report Takeaways

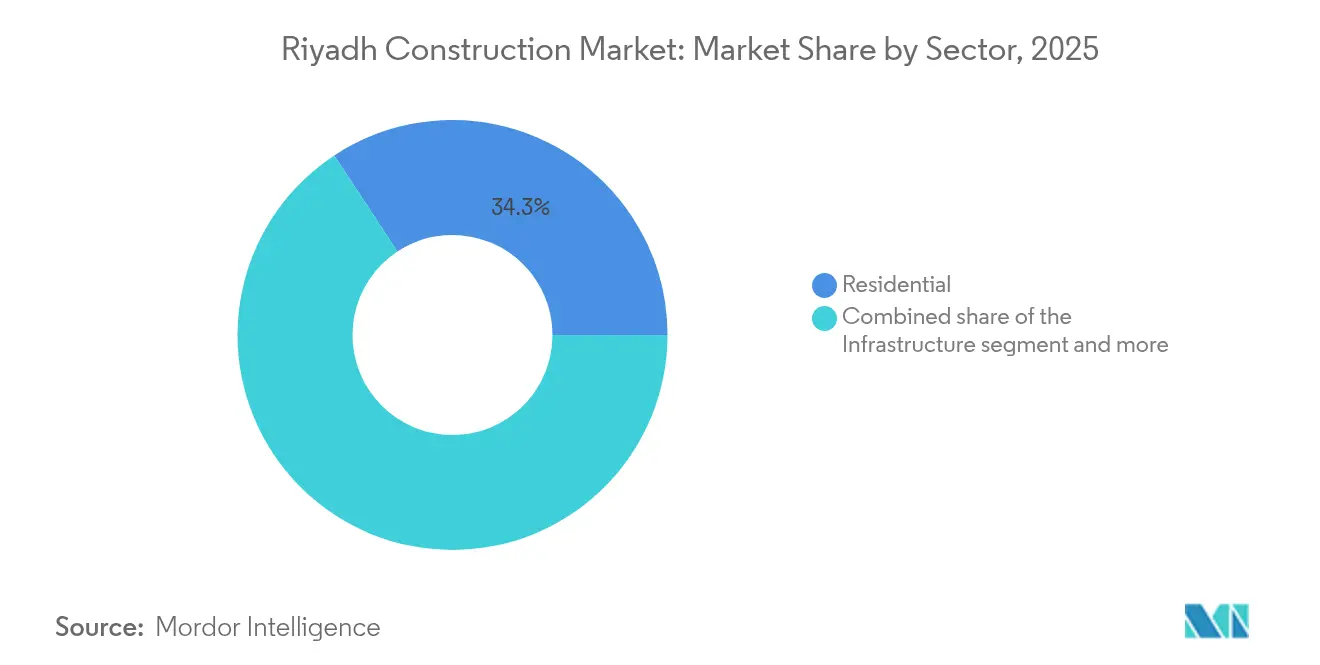

- By sector, residential construction led with 34.27% of the Riyadh construction market share in 2025, while infrastructure is projected to expand at a 5.91% CAGR through 2031.

- By construction type, new-build activity accounted for 79.45% of the Riyadh construction market size in 2025, whereas renovation is advancing at a 4.99% CAGR to 2031.

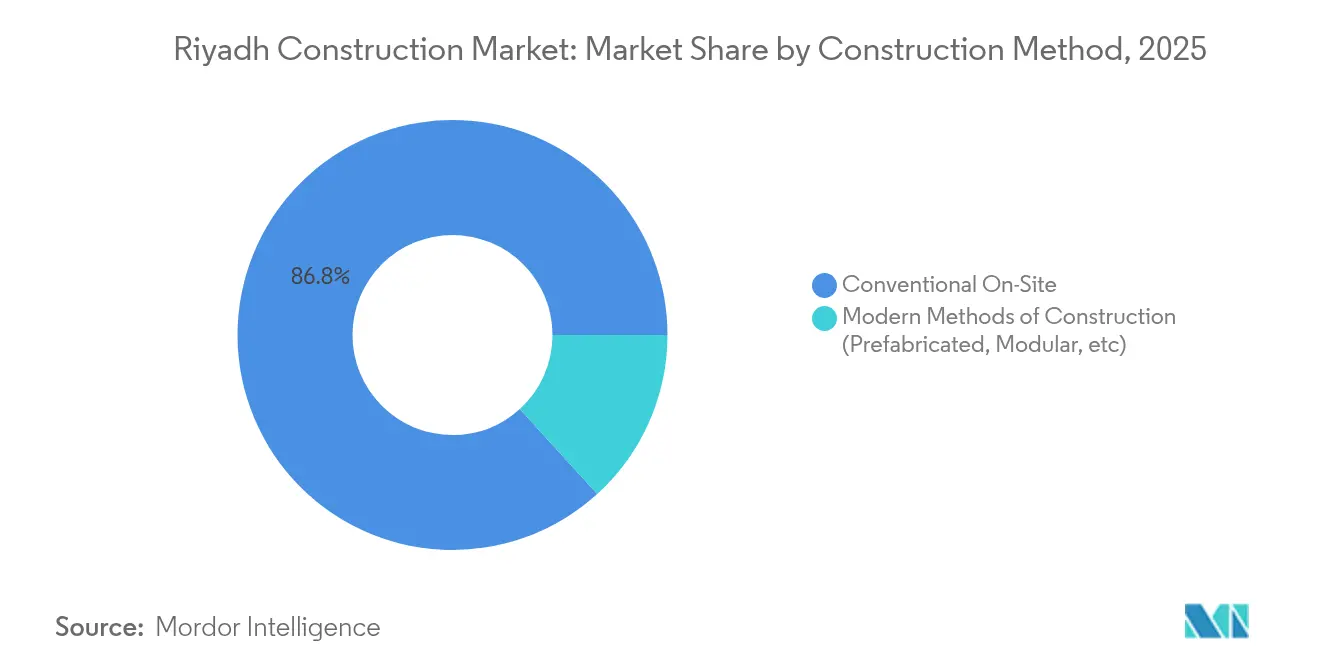

- By construction method, conventional on-site techniques retained 86.75% share of the Riyadh construction market size in 2025, yet modern methods are moving ahead at a 6.50% CAGR.

- By investment source, the public sector captured a 60.78% share of the Riyadh construction market size in 2025; the private segment records the higher CAGR at 5.73% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Riyadh Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga-project pipeline acceleration | +1.5% | Riyadh core, NEOM & Red Sea tie-ins | Long term (≥ 4 years) |

| Surge in contract awards under Vision 2030 | +1.2% | Riyadh metro area; Eastern Province spillover | Long term (≥ 4 years) |

| Green & sustainable-building mandates | +0.8% | National; early roll-out in Riyadh & Jeddah | Medium term (2-4 years) |

| Modular/off-site methods were adopted to ease labor gaps | +0.6% | Riyadh & major urban nodes | Medium term (2-4 years) |

| Riyadh Expo 2030 urban-revamp program | +0.4% | Riyadh metropolitan area | Short term (≤ 2 years) |

| Digital-twin requirements for new developments | +0.3% | Key cities; Riyadh smart-city focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga-Project Pipeline Acceleration

Saudi Arabia’s public ledger lists a pipeline of USD 1.1 trillion, with 70% of allocations in housing, leisure, and cultural developments centered on Riyadh. The King Salman International Airport alone is being developed to handle 100 million passengers annually and targets LEED Platinum status. Qiddiya’s USD 1 billion multipurpose stadium and Diriyah’s USD 63.2 billion heritage complex reinforce the capital’s tourism proposition. Project phasing has been sequenced so that workload peaks around 2025-2026, smoothing resource deployment. Broad use of Building Information Modeling (BIM) across packages reduces design clashes and rework, compresses schedules, and supports a 1.5 percentage-point boost to the overall growth rate.

Surge in Contract Awards Under Vision 2030

High-velocity tendering defines current demand conditions. The Royal Commission for Riyadh City alone released more than USD 3.47 billion equivalent in road projects during 2024, supplying predictable backlogs for civil contractors. Nationally, construction contract value grew 47% year-on-year to USD 49.3 billion in H1 2024, with real-estate and infrastructure schemes in the capital as top contributors. Financing risk is muted because the Public Investment Fund (PIF) commonly sits as an anchor sponsor, signaling payment reliability. Stricter capacity criteria set by the Saudi Contractor Authority further filter entrants, keeping bid lists manageable and margins comparatively stable. Taken together, these factors lift revenue visibility and add roughly 1.2 percentage points to the five-year CAGR outlook[1]ABDULLAH BIN TURKI, “SR13 Billion Riyadh Road Upgrades Awarded,” Royal Commission for Riyadh City, rcrc.gov.sa.

Green & Sustainable-Building Mandates

The 2024 update to the Saudi Building Code introduces SBC 601 energy-performance thresholds, effective June 2025. Requirements around thermal-insulation values, district-cooling hookups, and LEED gold targeting in marquee projects add specialist consulting and materials demand. Local concrete producers, such as Abdallah Abdin Ready-Mix, have already secured Concrete Sustainability Council certification, signaling an early-mover advantage. Government programs like Mostadam provide scoring frameworks that will soon influence refinancing costs, thus embedding sustainability into capital-allocation decisions. The mandate’s incremental efficiency upgrades and corresponding material substitutions lift long-run activity by an estimated 0.8 percentage points[2]KHALID AL-ABDULRAHMAN, “Saudi Building Code 2024—SBC 601 Energy Efficiency Requirements,” Ministry of Municipal, Rural Affairs and Housing, momrah.gov.sa.

Modular/Off-Site Methods were Adopted to Ease Labor Gaps

China Harbour Engineering Company opened a 200,000 m² modular facility in February 2025 to supply Sedra’s prefabricated villas, leveraging robotics for rapid panel assembly. Modular prototypes at NEOM’s The LINE demonstrate 25-30% time savings versus conventional builds, which in turn promote faster revenue recognition for developers. Factory settings improve worksite safety, a factor tied to Saudization rules that require 30% Saudi employment in technical positions. Off-site solutions, therefore, cushion labor-supply shocks while advancing quality control, adding 0.6 percentage points to medium-term CAGR[3]FEIYANG LI, “China Harbour Starts Riyadh Modular Building Factory Operations,” China Harbour Engineering Company, chec.bj.cn.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating building-material costs | -0.9% | National; sharpest in Riyadh hub | Short term (≤ 2 years) |

| Skilled-labor scarcity | -0.7% | Riyadh plus other build-intense zones | Medium term (2-4 years) |

| Lengthy permitting & land-assembly hurdles | -0.5% | Riyadh metropolitan area | Medium term (2-4 years) |

| Water-scarcity compliance costs | -0.3% | Countrywide; water-heavy trades | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Building-Material Costs

In 2024, cement touched 16-year highs, even as steel shed 4% over nine months, illustrating divergent commodity trajectories. Iron prices fell 10% to roughly USD 769 per ton, whereas cable prices rose 2.6%, blunting any savings from rebar declines. Contractors respond by splitting purchase orders across multiple suppliers and expanding local fabrication footprints, as shown by MS-Metals’ automated plant in Tabuk. Yet volatility complicates fixed-price bids, prompting clients to accept price-escalation clauses. The mix of uncertainties chips 0.9 percentage points off near-term CAGR.

Skilled-Labor Scarcity

Delayed wages, low remuneration, and site-accommodation issues depress retention, especially among specialized trades. Saudization decrees now mandate a 30% local quota across 269 engineering professions, tightening the labor pool. Private institutes such as Nesma High Training Institute are scaling vocational programs, but upskilling cycles take time. Modular factories lighten onsite head-count needs, yet not enough to fully offset shortages. Collectively, the constraint subtracts 0.7 percentage points from growth across the medium horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Acceleration Outpaces Residential Dominance

The residential segment preserved leadership with 34.27% of the Riyadh construction market share in 2025, backed by National Housing Strategy initiatives to raise ownership to 70% by 2030. Infrastructure, however, registers the swiftest expansion at a 5.91% CAGR through 2031, lifted by USD 3.47 billion worth of road programs and the USD 6.13 billion Riyadh Metro build-out. This pivot enlarges the Riyadh construction market size for heavy civil works and signals widening procurement opportunities for specialized EPC contractors.

Rapid transportation upgrades, such as the 56-kilometer southern ring road, complete with 32 bridges, underscore the shift toward integrated mobility corridors. Energy and utilities projects, including the USD 544 million Jubail desalination link, add resilient demand streams as the urban population swells. Commercial development rides Expo 2030 timelines, while logistics platforms rise amid manufacturing-diversification pushes. Overall, sector interplay keeps order books balanced, maintaining a broad earnings base amid cyclical housing swings.

By Construction Type: Renovation Gains Momentum Despite New-Build Leadership

New construction absorbed 79.45% of spending during 2025, reflecting ground-up mega-projects such as the USD 180 billion New Murabba district. Yet renovation work edges higher at a 4.99% CAGR thanks to retrofits mandated by updated building codes. These upgrades expand the Riyadh construction market size for energy-efficiency solutions and smart-asset management systems.

Legacy road networks are being widened, utilities are modernized to optimize capacity, and public venues undergo green retrofits in advance of Expo 2030. The Saudi Building Code’s retroactive clause pushes older assets to install insulation, high-efficiency glazing, and district-cooling interfaces. Digital CMMS deployments further reduce lifecycle costs, validating the business case for renovation despite higher initial outlays.

By Construction Method: Modern Methods Challenge Conventional Dominance

Conventional on-site activity still claims 86.75% of 2025 volume, driven by established procurement structures and cost familiarity. However, modern methods clock a 6.50% CAGR as labor constraints, safety concerns, and schedule pressures converge. Each new modular factory, exemplified by China Harbour’s 200,000 m² facility, extends capacity to serve giga-projects without logistical bottlenecks.

Industry 4.0 advances, such as 3D printing and robotics, are progressively embedded into off-site lines, yielding consistent component tolerances. BIM integration across design, manufacturing, and assembly stages minimizes errors and supports just-in-time deliveries to congested urban sites. The LINE at NEOM showcases modular high-rise construction at unprecedented scale, setting benchmarks that ripple back into the Riyadh construction market. Given demonstrated time savings of up to 30%, project financiers increasingly favor modern methods to de-risk delivery windows.

By Investment Source: Private-Sector Momentum Builds on Public Foundation

Public funding remained dominant in 2025 at 60.78%, reflecting the PIF’s sponsorship of transformative assets. Yet private capital posts the sharper 5.73% CAGR as clearer legal frameworks and special economic zones reduce entry barriers. The Civil Transactions Law, live since December 2023, bolsters the enforceability of contracts and accelerates dispute resolution, enhancing lender confidence.

Recent examples include USD 10 billion in maritime-industrial offtake deals at Ras Al-Khair and cross-border ventures such as Petro Rabigh’s specialty-chemicals tie-up with India’s Rossari. FDI inflows also track incentive packages of low taxation and customs relief across newly designated zones. The evolving mix invites fresh project-delivery models, PPP, concession, and build-operate-transfer, broadening the Riyadh construction market’s financing toolkit.

Geography Analysis

Riyadh captures the lion’s share of Saudi contract allocations, anchored by mega-schemes like the USD 180 billion New Murabba and the forthcoming airport designed for 100 million annual passengers. The Royal Commission’s road‐upgrade portfolio alone spans 500 kilometers and supports the city’s ambition to double its population by 2030. Capital-city advantages include proximity to regulatory agencies, a mature contractor network, and direct PIF oversight, all of which increase project-execution velocity. Expo 2030 status injects deadline-driven procurement, concentrating activity in the next four years and amplifying auxiliary builds in hospitality and transport.

Beyond the capital, the national map shows complementary but differentiated demand nodes. The Eastern Province leads hydrocarbon-driven civil works, contributing 41% of total contract awards in H1 2024. In the northwest, NEOM’s USD 500 billion blueprint underwrites steady orders for tunneling, utilities corridors, and smart-city infrastructure, though much of the design is managed in Riyadh. The Red Sea Project and Diriyah heritage cluster extend tourism-centric construction, forming an ecosystem of regional mega-projects that share suppliers, labor pools, and technology workflows. Common regulatory baselines such as the 2024 Saudi Building Code unify practices nationwide, but Riyadh remains the administrative nerve center for approvals and finance.

Inter-regional synergies are furthered by nationwide rail and highway linkages, reducing material-delivery times and balancing resource allocation. Contractors headquartered in Riyadh increasingly establish satellite yards near remote giga-projects, yet maintain design hubs in the capital to leverage advisory clusters and digital-twin labs. While water scarcity constraints affect the whole kingdom, Riyadh’s dense consumption profile triggers earlier adoption of reuse systems, providing pilot learnings for replication elsewhere. Overall, the city’s primacy in policy, capital flow, and workforce makes it the fulcrum of the Saudi construction narrative through 2030.

Competitive Landscape

Riyadh’s construction arena exhibits moderate concentration: domestic majors, global EPC firms, and joint-venture consortiums jostle for capacity-draining giga-projects. Nesma & Partners, buoyed by PIF affiliations, leads large mixed-use packages and broadened its engineering reach by completing Kent’s acquisition in early 2024. El Seif Engineering, China State Construction Engineering Corporation (CSCEC), and Midmac operate in alliances, exemplified by their USD 1.4 billion Diriyah Opera House win, signaling a preference for consortium formats to share risk and aggregate specialized skills. Egis Group’s purchase of Riyadh designer Omrania brings high-end architectural talent under an international umbrella, sharpening the firm’s cultural-asset credentials.

Technology adoption shapes competitive edges. BIM is mandatory on public projects since 2024, and digital-twin deliverables spark demand for data analytics capability that smaller firms may lack. Robotics-ready modular factories, China Harbour’s new facility being the bellwether, function as competitive moats, allowing rapid unit turnarounds and consistent quality. Firms investing early in such capacity secure repeat orders from giga-projects chasing compressed timelines. Local content targets under Saudization rules reward players with active training programs; Nesma’s vocational institute and CSCEC’s Saudi graduate initiatives showcase the trend.

White-space opportunities blossom in green-material supply chains, carbon-capture-ready cement, and integrated O&M packages that extend revenue beyond handover. Emerging disruptors include AI scheduling platforms that cut idle time and energy analytics firms that optimize district cooling loads. Although newcomers lack scale, they forge partnerships with tier-one builders seeking specialist inputs. As Vision 2030 spending enters peak disbursement, differentiation will hinge on cost-certainty guarantees, ESG compliance, and the ability to localize advanced manufacturing footprints swiftly within Riyadh’s industrial zones.

Riyadh Construction Industry Leaders

Bechtel

Nesma & Partners Contracting

Fluor Corporation

KEO International Consultants

Parsons Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Miahona won a USD 267 million contract for a wastewater treatment plant under the Modon initiative, broadening Riyadh’s environmental infrastructure capacity.

- February 2025: China Harbour Engineering Company began operations at its 200,000 m² modular building factory in Riyadh to supply prefabricated components for Sedra villas.

- February 2025: The Public Investment Fund acquired 30% of Masdar Building Materials and issued a USD 1.5 billion package for the Sedra community project during its private-sector forum.

- November 2024: Hyundai E&C secured a USD 725 million contract to construct a 500 kV HVDC line linking Riyadh to Kudmi, spanning 1,089 kilometers.

Riyadh Construction Market Report Scope

The construction market is defined as companies engaged in building or engineering projects, such as bridges and roads. Construction also takes place when renovating existing buildings. The report provides a complete background analysis of the Riyadh construction market, comprising an evaluation of the sector and its contribution, market overview and size estimation for critical segments, the impact of COVID-19, prominent countries, emerging trends in the market segments, market dynamics, and key statistics on goods flow. The construction market in Riyadh is segmented by sector (commercial construction, residential construction, industrial construction, infrastructure [transportation] construction, and energy and utility construction). The report offers market size and forecasts in value (USD) for all the above segments.

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

| Public |

| Private |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

Key Questions Answered in the Report

How large is the Riyadh construction market in 2026?

The industry’s market size is USD 3.3 billion in 2026 and is projected to climb to USD 4.04 billion by 2031 on a 4.12% CAGR trajectory.

Which segment is growing fastest within Riyadh’s construction activity?

Infrastructure shows the most rapid expansion, advancing at a 5.91% CAGR through 2031 as mega-roads, metro lines, and airport packages dominate new awards.

Why are modular building systems gaining traction?

Modular approaches cut delivery times by up to 30%, ease skilled-labor shortages, and align with Saudization efforts; China Harbour’s new 200,000 m² factory exemplifies this shift.

What role does the private sector play in upcoming projects?

Although public entities still fund most builds, private capital records the higher 5.73% CAGR as legal reforms and special economic zones reduce investment risk.

How will Expo 2030 affect construction timelines?

Expo-related contracts worth USD 7.8 billion compress schedules between 2025 and 2029, intensifying demand for fast-track design-build solutions.

Page last updated on: