China After-School Tutoring Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 99.30 Billion |

| Market Size (2030) | USD 168.87 Billion |

| Growth Rate (2025 - 2030) | 11.23% CAGR |

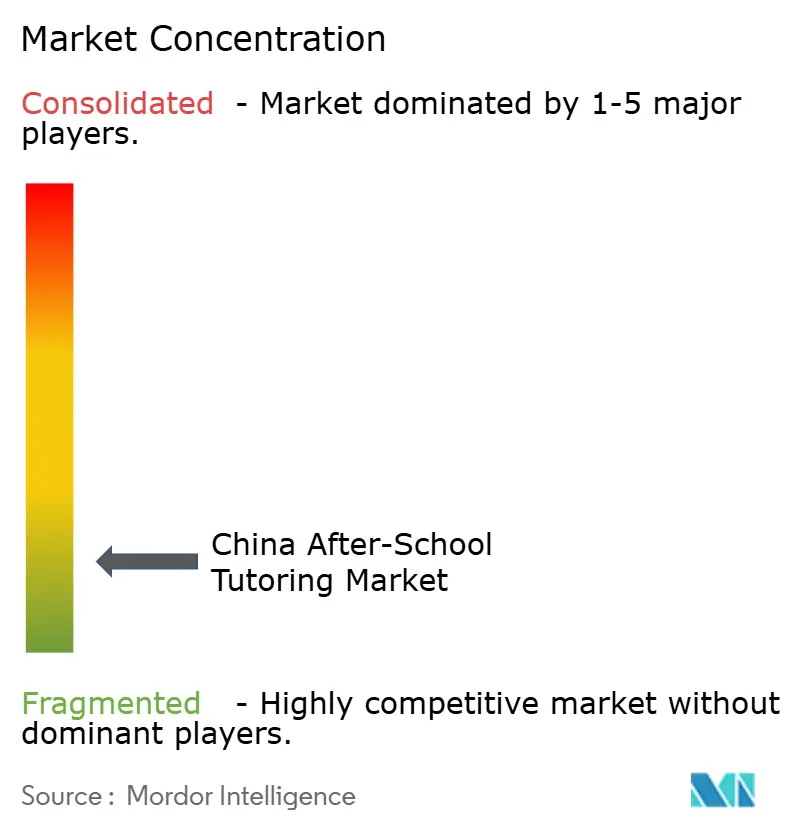

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China After-School Tutoring Market Analysis by Mordor Intelligence

The China after-school tutoring market reached USD 99.30 billion in 2025 and is expected to grow to USD 168.87 billion by 2030, registering an 11.23% CAGR, confirming robust market size expansion despite the “Double-Reduction” overhaul. Innovation flourished as large and small providers accelerated AI-powered platforms, diversified into STEM enrichment, and embraced hybrid delivery, converting regulatory adversity into fresh opportunities. Parental expectations around Gaokao performance, rising disposable income in lower-tier cities, and government STEM incentives continue to underpin sustained demand and revenue visibility. Providers that master compliance, AI personalization, and WeChat private-domain engagement are widening competitive gaps, while investors are migrating capital to companies able to scale beyond Tier 1 geographies. Fragmentation stays high because micro-studios and niche specialists proliferate faster than consolidation, keeping price competition intense and service differentiation essential.

Key Report Takeaways

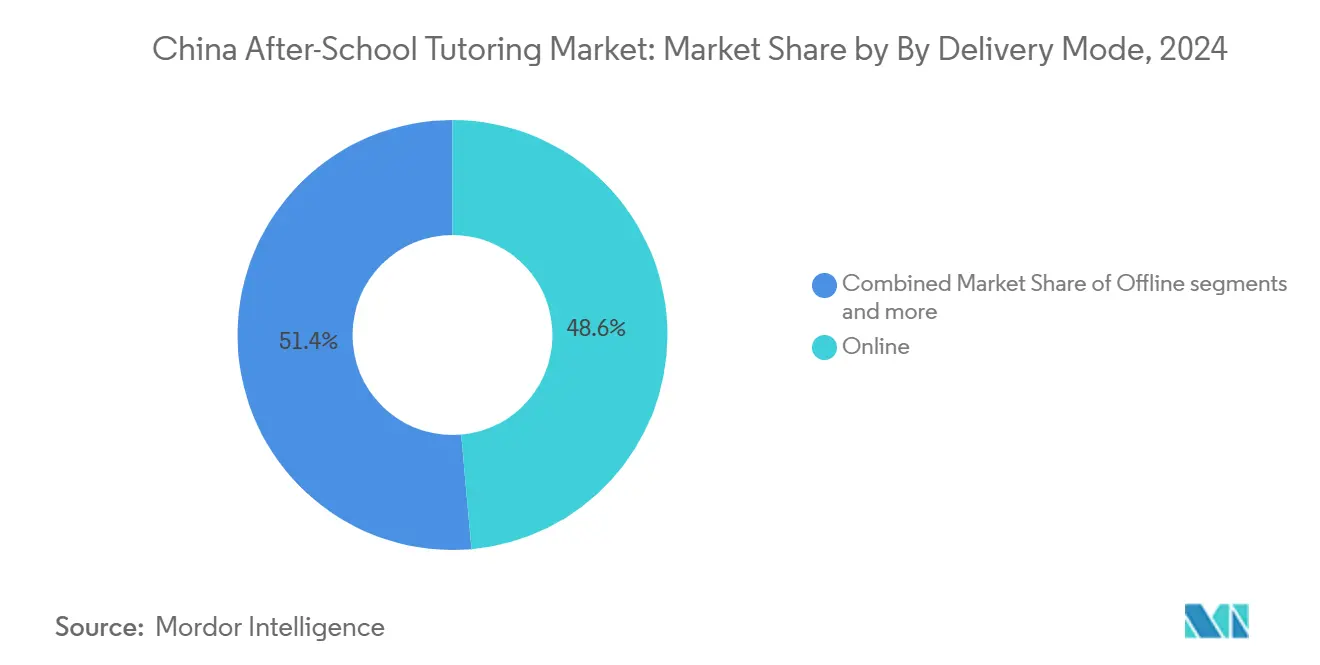

- By delivery mode, online tutoring led with 48.60% of the China after-school tutoring market share in 2024 and is forecast to post an 8.20% CAGR through 2030.

- By subject category, core academics accounted for 60.23% of the China after-school tutoring market size in 2024, while STEM enrichment is advancing at a 7.65% CAGR to 2030.

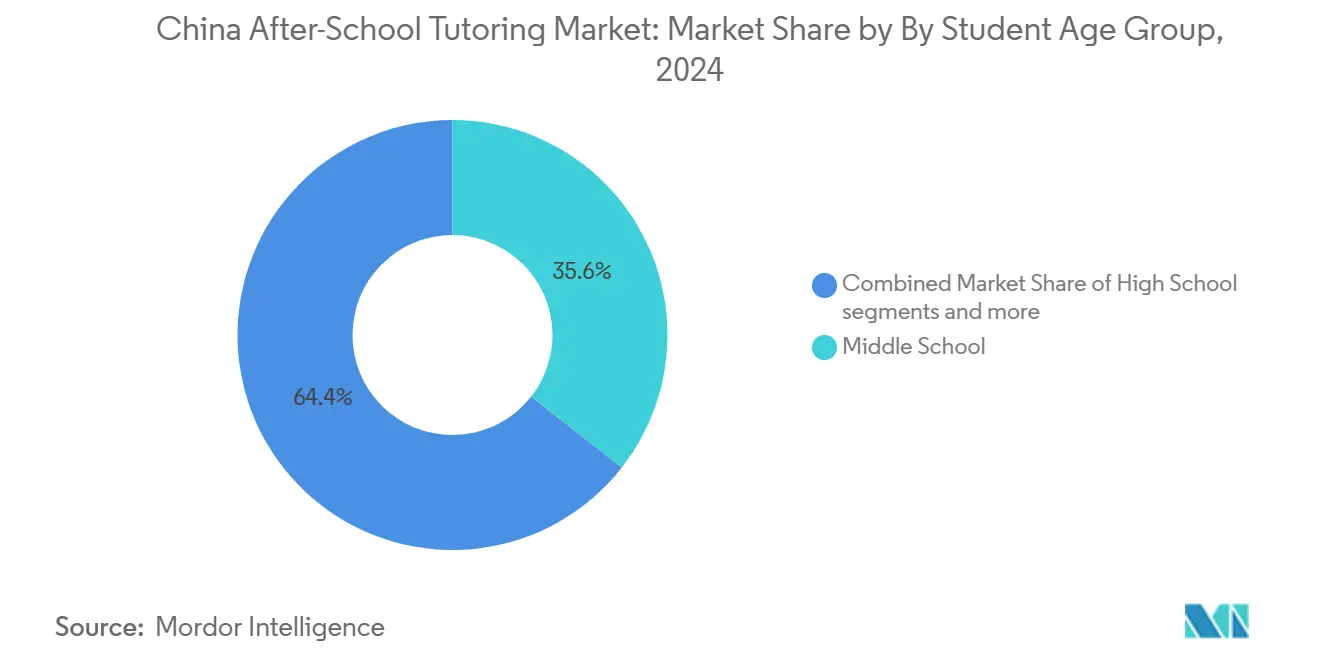

- By student age group, middle school students represented 39.12% of the China after-school tutoring market in 2024; high school students exhibit the fastest 9.84% CAGR through 2030.

- By region, East China held 45.12% revenue share of the China after-school tutoring market in 2024, whereas the rest-of-China cluster is projected to expand at a 10.11% CAGR to 2030.

China After-School Tutoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Entrenched exam-oriented culture & Gaokao pressure | +2.8% | National, with highest intensity in East and North China | Long term (≥ 4 years) |

| Rapid penetration of AI-powered adaptive learning platforms | +2.1% | National, with early adoption in Tier 1 cities | Medium term (2-4 years) |

| Rising disposable income & willingness to spend in lower-tier cities | +1.9% | Rest of China regions, spill-over to South-Central China | Medium term (2-4 years) |

| Expansion of non-academic "quality-oriented" tutoring after Double-Reduction | +1.7% | National, with regulatory compliance focus | Short term (≤ 2 years) |

| WeChat private-domain ecosystems lowering CAC for micro-tutoring studios | +1.4% | National, with higher penetration in urban areas | Short term (≤ 2 years) |

| Government incentives for STEM skills (coding, robotics) | +1.3% | National, with pilot programs in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Entrenched Exam-Oriented Culture & Gaokao Pressure

The Gaokao remains the decisive gateway to higher education and social mobility, so families continue funneling resources toward supplemental study despite tighter rules. Demand even intensified during 2021-2023 enforcement, with underground and cross-border solutions filling gaps until compliant channels re-emerged. Tutors that bundle critical-thinking modules with traditional academics now satisfy both exam rigor and modern competency goals. Regulatory messaging has subtly shifted toward managed coexistence, implicitly accepting that abolishing tutoring is impractical. Consequently, premium, regulation-aligned offerings are commanding higher prices while sustaining volume growth.

Rapid Penetration of AI-Powered Adaptive Learning Platforms

Platforms such as Squirrel AI and TAL’s Genius Tutor use GPT-4-based engines to diagnose learning gaps and curate real-time lesson paths, delivering measurable efficiency gains. The technology scales personalized attention to millions of students, cutting routine tutor workload and letting staff focus on high-value mentoring. Cost-effective models like DeepSeek-R1 have lowered entry barriers, letting mid-sized firms deploy advanced AI without prohibitive R&D budgets [1]Staff Writer, “DeepSeek-R1 Model Revolutionizes AI in Education,” Nasdaq, nasdaq.com . Competitive advantage now hinges on data-rich algorithms that refine with every session, raising performance benchmarks sector-wide. Parents view AI dashboards as credible proof of progress, accelerating preference migration from static video courses to adaptive ecosystems.

Rising Disposable Income & Willingness to Spend in Lower-Tier Cities

Disposable income growth outside Tier 1 hubs broadened the addressable base, as families in Northeast, Southwest, and Northwest provinces increased educational outlays. New Oriental’s network of 1,089 schools illustrates how incumbents scale into these cost-effective markets while maintaining margins [2]New Oriental Education and Technology Group, “New Oriental Announces Results for the First Fiscal Quarter Ended August 31, 2024,” neworientaleducationandtechnologygroupinc.gcs-web.com . Hybrid formats that blend live streaming with periodic on-site mentoring resonate because they balance affordability and personal touch. Government consumption boosters and infrastructure upgrades further spur enrollment uptakes. Early movers are locking in loyalty through localized content and alumni referral programs that exploit community trust.

WeChat Private-Domain Ecosystems Lowering CAC for Micro-Tutoring Studios

WeChat’s private domain lets tutors cultivate persistent parent groups, push homework reminders, and collect payments without large advertising budgets [3]Staff Writer, “《视频号橱窗 教育培训 类目管理规则》,” Tencent, channels.weixin.qq.com . Two-way communication fosters trust, translating into higher renewal rates and word-of-mouth referrals. Integrated scheduling and mini-program content reduce administrative overheads, enabling one-person studios to scale to hundreds of students. Large institutions mirror the approach through dedicated service accounts that personalize outreach at scale. Continuous platform rule updates clarify compliance requirements, encouraging further capitalization on low-cost acquisitions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| "Double-Reduction" policy capping for-profit K-12 academic tutoring | -3.2% | National, with stricter enforcement in Tier 1 cities | Long term (≥ 4 years) |

| Shrinking school-age population (falling births since 2016) | -1.8% | National, with acute impact in urban areas | Long term (≥ 4 years) |

| Tutor talent drain amid sectoral uncertainty | -1.1% | National, with higher impact in competitive markets | Medium term (2-4 years) |

| Stricter data-privacy & algorithm governance rules for EdTech | -0.9% | National, with focus on AI-powered platforms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

“Double-Reduction” Policy Capping For-Profit K-12 Academic Tutoring

The 2021 regulatory policy prohibited academic tutoring during weekends and holidays, introduced stringent licensing requirements, and mandated the conversion of K-12 academic institutions into non-profit entities, significantly altering the operational landscape. The resulting compliance costs led to widespread closures, revenue declines, and a strategic pivot toward enrichment programs and international markets as firms sought alternative growth avenues. Although enforcement measures showed slight relaxation in 2024, the prevailing regulatory uncertainty has compelled businesses to adopt conservative approaches to expanding their academic services. Emerging innovations, such as AI-powered study rooms, underscore the enduring demand for academic support but simultaneously expose firms to potential regulatory penalties. Navigating the complexities of this policy framework remains a critical strategic challenge for businesses, shaping their operational and growth strategies through 2030.

Shrinking School-Age Population (Falling Births Since 2016)

Declining birth rates are driving reductions in enrollment cohorts, with urban districts experiencing the most pronounced impact due to significant fertility rate contractions. In response, education service providers are focusing on premiumizing their offerings to enhance revenue per student while strategically expanding into adult education and test preparation segments to diversify revenue streams. The market is witnessing increased consolidation pressures as weaker players struggle to maintain class occupancy, leading to a rise in acquisitions and market exits. At the same time, parents with single children are allocating higher expenditures toward education, which partially mitigates the impact of declining enrollment volumes. Nevertheless, demographic challenges are anticipated to limit overall market growth if per-pupil spending reaches a plateau.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Mode: Online Dominance Drives Digital Transformation

Online tutoring controlled 48.60% of the China after-school tutoring market share in 2024 and is tracking an 8.20% CAGR to 2030, showcasing a structural consumer pivot toward digital convenience. Cost efficiency, nationwide reach, and AI-driven personalization underpin this strength, while hybrid models use local centers as trust anchors to improve retention. The China after-school tutoring market size for hybrid formats is projected to widen quickly as parents seek a balance between screen learning and supervised practice. Offline centers remain vital for younger learners needing hands-on guidance, but they increasingly embed livestream classrooms to cut fixed costs. Competitive intensity rests on algorithm quality, session interactivity, and integrated WeChat communities that keep acquisition costs low.

At the product level, question-scanning and instant answer apps such as Zuoyebang’s Question.AI rank among top global AI downloads, reflecting tech leadership. Providers battle over latency, accuracy, and gamification features that sustain student engagement. WeChat mini-apps power micro-studio growth by combining course delivery, homework uploads, and payment in a single interface, lowering entry barriers. Large players partner with telecom carriers to preload tutoring apps on low-cost tablets, deepening rural penetration. As regulatory clarity around data governance tightens, audit-ready AI architectures become decisive trust factors.

By Subject Category: STEM Enrichment Challenges Academic Dominance

Core academics kept 60.23% of the Chinese after-school tutoring market in 2024, yet STEM enrichment courses post the fastest 7.65% CAGR thanks to coding and robotics enthusiasm. Government policy alignment, international competition narratives, and visible career outcomes fuel this pivot. The China after-school tutoring market size for coding programs is scaling as EdTech firms gamify Python and Arduino curricula to suit primary-grade attention spans. Foreign language diversification beyond English gains traction among parents anticipating globalized job markets, while arts and sports courses benefit from policy incentives for holistic education. Providers that cross-bundle mathematics logic with coding practice create differentiated value propositions difficult to copy.

Market leadership in STEM remains fluid as start-ups leverage rapid AI prototyping to iterate courseware quickly. Incumbents license branded robotics kits to enrich hands-on labs, driving hardware-plus-software revenue models. Academic subjects still command premium pricing for Gaokao relevance, but price elasticity is rising because parents can compare AI-enhanced platforms more easily. Niche players offering debate or creative writing see steady demand, especially as universities broaden admissions criteria. Future growth depends on producing demonstrable skill certifications that universities and employers recognize.

By Student Age Group: High School Acceleration Reflects Gaokao Intensity

Middle schoolers formed the largest 39.12% tranche of the China after-school tutoring market share in 2024, underpinning continued mass-market stability. High school cohorts, however, will deliver a 9.84% CAGR through 2030 as Gaokao stakes intensify and regulatory loophole tutoring formats mature. The China after-school tutoring market size for high school AI-powered test prep platforms is expanding because digital natives value interactive analytics. Primary grades maintain solid growth in STEM and quality-oriented modules focused on creativity and motor skills.

High school demand concentrates on adaptive mock-exam engines and essay-grading AI that provide rapid feedback, shortening study cycles. Providers add mental-health counseling and time-management workshops, responding to parental concerns about burnout. Middle school services now integrate foundational coding to smooth transition into advanced STEM curricula. Primary-age offerings emphasize immersive story-based learning and parent-child co-creation workshops delivered via weekend micro-camps. Across cohorts, community-driven WeChat groups cultivate peer competition that boosts completion rates.

Geography Analysis

East China’s longstanding dominance arises from dense wealth, top-tier infrastructure, and cultural emphasis on educational achievement, fostering sophisticated consumers willing to pay for AI-enhanced personalization. Providers pilot regulatory-compliant models in Shanghai and Hangzhou, refining offerings before scaling nationally. Strict enforcement drives competitive innovation, rewarding firms that can integrate certified teachers, adaptive algorithms, and parental dashboards within permitted operating windows. Despite maturity, incremental growth stems from upselling enrichment bundles to households already committed to academic tutoring. The region’s premium prices subsidize R&D, benefiting expansion elsewhere.

North China and South-Central China form sizable, differentiated arenas shaped by economic composition and educational emphasis. North China’s proximity to policymakers facilitates rapid interpretation of new guidelines, giving compliant vendors a head start. South-Central’s manufacturing base values problem-solving and technical literacy, expanding demand for vocational-adjacent tutoring alongside academics. Both areas display a heightened appetite for hybrid offerings that deliver personalized learning yet preserve local teacher relationships. Competitive intensity rose after 2021, as displaced East-China operators sought new revenue pools, accelerating service quality convergence across regions.

Rest-of-China clusters—Northeast, Southwest, Northwest—now deliver the fastest growth, propelled by disposable-income gains and government programs targeting equity. Lower operational costs allow profitable pricing below Tier 1 averages, widening access to tutoring among emerging middle-class families. Providers typically adopt hub-and-spoke models: centralized digital lesson creation with localized mentor support to maintain parent trust. Improved broadband coverage narrows experience gaps, letting AI platforms perform effectively even in remote counties. State Council directives that encourage private education investment deepen the funding pool, enticing national brands to accelerate rollout schedules across these areas.

Competitive Landscape

The after-school tutoring market in China remains highly fragmented in 2024, with the top five companies collectively capturing only a small portion of the total revenue. New Oriental and TAL Education rely on brand equity and cash reserves to diversify into enrichment and go overseas, buffering policy risk. Technology-centric firms like Squirrel AI and Zuoyebang emphasize algorithmic superiority and platform scalability, vying for digital mindshare. Thousands of micro-studios leverage WeChat private domains to cultivate niche communities, achieving defensible personalization and low customer-acquisition costs. STEM specialists exploit policy tailwinds to capture white-space demand, competing on certified curricula and proprietary robot-kit ecosystems.

Strategic initiatives vary: TAL’s Genius Tutor integrates GPT-4o to deliver real-time feedback, lifting engagement metrics, while New Oriental’s enrichment pivot saw 30.5% revenue growth in fiscal Q1 2025 [4]Equity Research, “TAL Education Group: Expansion of Enrichment Learning Programs,” Smartkarma.com, smartkarma.com . Zuoyebang’s confidential U.S. IPO filing signals investor appetite for EdTech platforms as regulatory pressure eases. Four Seasons Education reported a 118% revenue surge upon expanding into tourism-education hybrids, illustrating creative diversification. Venture-backed start-ups like Conan AI target hardware-plus-software bundles for younger learners, receiving angel rounds to accelerate go-to-market.

Competitive success increasingly depends on AI transparency, data-privacy compliance, and multi-scenario content that satisfies both academic and holistic ambitions. Firms incorporating mental-wellness coaching and peer-collaboration tools differentiate beyond pure curriculum delivery. Cross-border expansion into Southeast Asia and online Mandarin-learning markets offers new revenue pillars for scaled Chinese brands. However, talent retention remains challenging as experienced tutors pursue entrepreneurial paths or shift to public schools for stability. Overall, a fragmented, innovation-intensive environment favors agile operators with strong compliance governance and adaptive technology stacks.

China After-School Tutoring Industry Leaders

New Oriental Education & Technology Group

TAL Education Group (Xueersi)

Gaotu Techedu (Gaotu)

Offcn Education

Yuanfudao /Ape Tutoring

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Yuanfudao unveiled the Xiaoyuan AI Learning Machine, an at-home tutoring device with an adjustable camera base and built-in printer that personalizes coursework for K-12 users.

- February 2025: Sunlands Technology Group launched an upgraded adult-learning platform powered by the DeepSeek AI model, adding 24/7 adaptive tutoring features aimed at the USD 788 billion domestic lifelong-education segment.

- January 2025: TAL Education introduced Genius Tutor, an AI system built on Microsoft Azure OpenAI GPT-4o that delivers real-time math, reading, and writing assistance to students nationwide.

- October 2024: New Oriental opened additional schools and learning centers, reaching 1,089 locations, while simultaneously adding new non-academic courses that helped revenue rise 30.5% in Q1 FY25.

China After-School Tutoring Market Report Scope

| Online |

| Offline |

| Hybrid |

| Core Academics (Math, Chinese, English) |

| STEM Enrichment (Coding & Robotics) |

| Foreign Languages (Non-English) |

| Arts & Sports |

| Primary School |

| Middle School (Junior High) |

| High School |

| East China |

| North China |

| South-Central China |

| Rest Of China (Northeast, Southwest, Northwest) |

| By Delivery Mode | Online |

| Offline | |

| Hybrid | |

| By Subject Category | Core Academics (Math, Chinese, English) |

| STEM Enrichment (Coding & Robotics) | |

| Foreign Languages (Non-English) | |

| Arts & Sports | |

| By Student Age Group | Primary School |

| Middle School (Junior High) | |

| High School | |

| By Region | East China |

| North China | |

| South-Central China | |

| Rest Of China (Northeast, Southwest, Northwest) |

Key Questions Answered in the Report

How large is the China after-school tutoring sector in 2025?

The market stands at USD 99.30 billion and is projected to grow to USD 168.87 billion by 2030.

Which delivery channel is growing fastest among tutoring providers?

Online formats post an 8.20% CAGR through 2030, powered by AI personalization and nationwide reach.

What segment shows the strongest subject-level expansion?

STEM enrichment, especially coding and robotics, is advancing at a 7.65% CAGR under government incentives.

Why are lower-tier cities pivotal for future growth?

Rising disposable income and government equity programs push a 10.11% CAGR in the rest-of-China regions.

How fragmented is the competitive landscape?

The market remains fragmented, as the top five firms account for only a small portion of the revenue, allowing regional players significant opportunities for growth.

How has the Double-Reduction policy altered business models?

Firms shifted from weekend academic tutoring to enrichment, hybrid delivery, and AI platforms while ensuring regulatory compliance.

Page last updated on: