Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

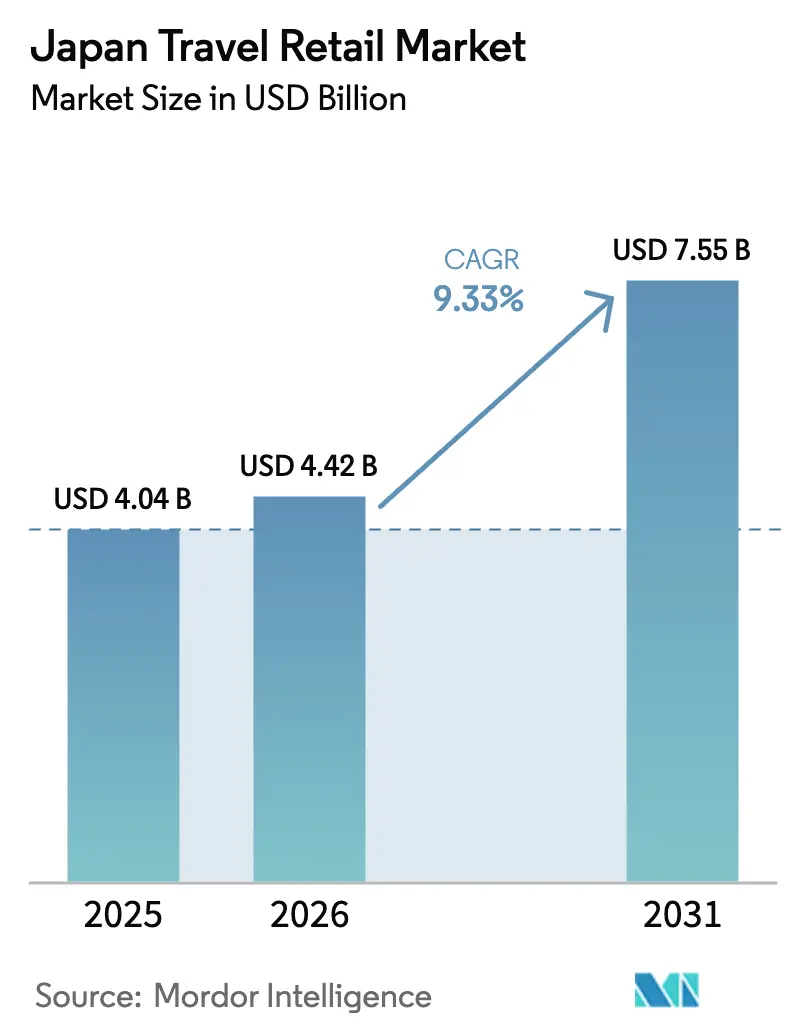

| Base Year Market Size (2025) | USD 4.04 Billion |

| Market Size (2026) | USD 4.42 Billion |

| Market Size (2031) | USD 7.55 Billion |

| Growth Rate (2025 - 2031) | 9.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Travel Retail Market Analysis by Mordor Intelligence

The Japan Travel Retail Market size is projected to expand from USD 4.04 billion in 2025 and USD 4.42 billion in 2026 to USD 7.55 billion by 2031, registering a CAGR of 9.33% between 2026 to 2031.

The growth path is supported by expanded duty-free floor space at Haneda and Narita and by Kansai International Airport’s completed Terminal 1 renovation, which increases the commercial mix and throughput capacity[1]Tokyo International Air Terminal, “Terminal Information and Services,” Haneda Airport, haneda-airport.jp. Inbound demand accelerated in 2025 as arrivals and per capita spending strengthened, while operators recalibrated assortments toward high-margin exclusives to hedge currency and mix shifts[2]Japan Tourism Agency, “Tourism Policy and Statistics,” MLIT, mlit.go.jp. Regulatory changes will reframe checkout and customs in November 2026 as Japan moves to an airport refund tax-free model, removing packaging rules and purchase caps for consumables while adding validation steps at exit points. Channel control remains central because airports concentrate traffic and still handle the bulk of high-value transactions in the Japan travel retail market.

Key Report Takeaways

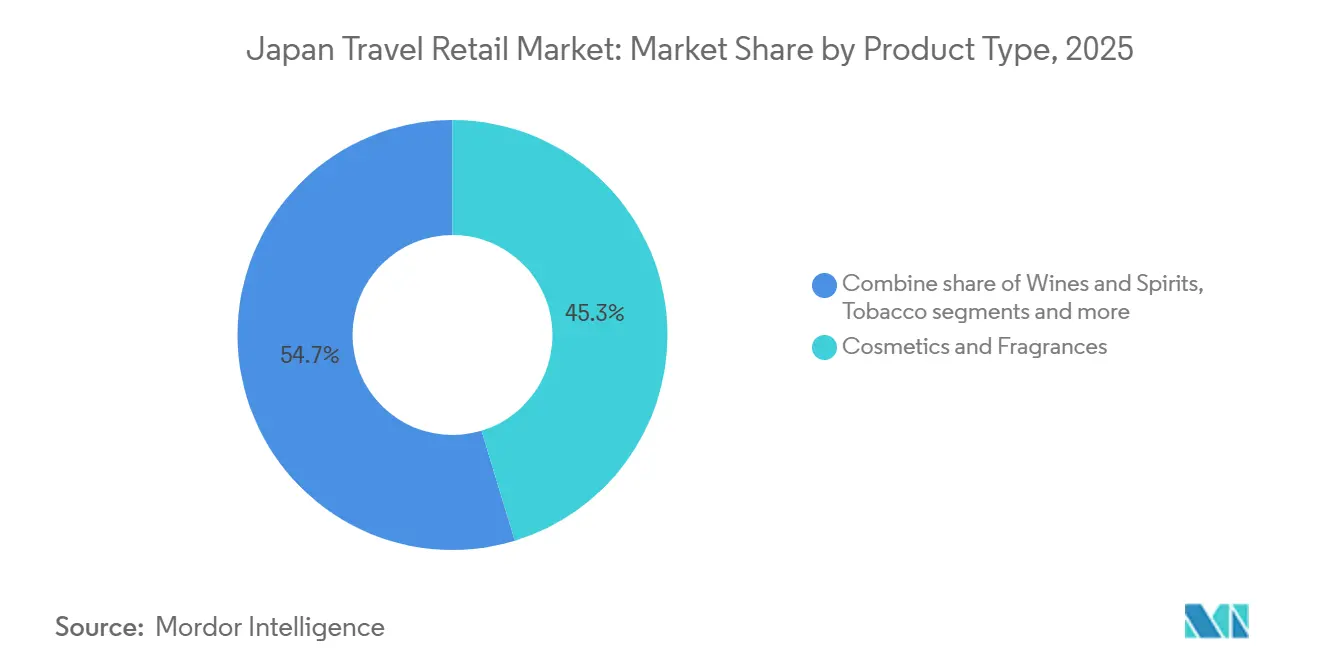

- By product type, cosmetics and fragrances led with 45.31% revenue share in 2025, while wines and spirits are forecast to expand at an 11.12% CAGR through 2031.

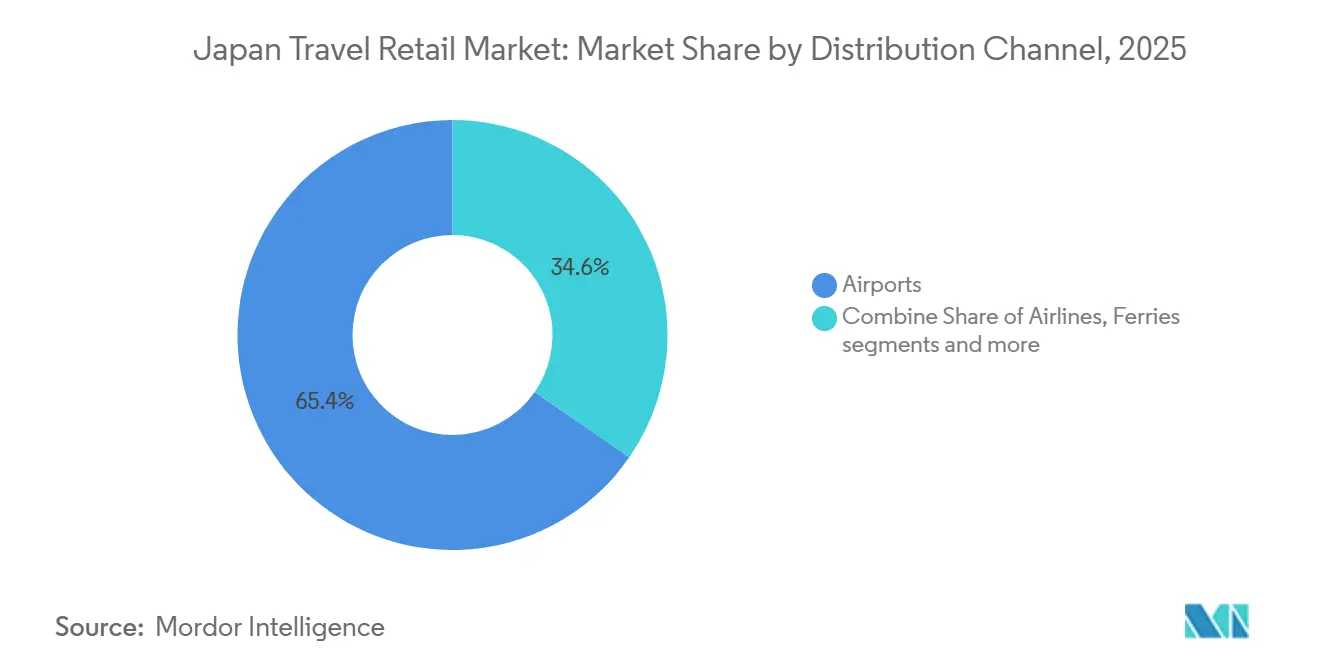

- By distribution channel, the airports segment held 65.35% of the Japan travel retail market share in 2025, while airports are projected to grow at a 10.58% CAGR to 2031.

- By geography, Kanto accounted for 53.31% of market value in 2025, while Kansai or Kinki is projected to post the fastest growth at a 9.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Travel Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| World-leading luxury brand store openings in Japan | 1.8% | Global, with spillover to Kanto (Tokyo Ginza), Kansai (Osaka), and airport gateways (Haneda T2/T3, KIX T1) | Medium term (2–4 years) |

| Rising duty-free spend by Chinese & Korean travellers | 2.5% | National, with the highest gains in Kanto (Haneda), Kansai (KIX, Expo corridor), and Kyushu (Fukuoka proximity) | Short term (≤ 2 years) |

| Airport retail-space expansion & refurbishment at Haneda, Narita, Kansai | 2.2% | Asia-Pacific core, with primary concentration in Kanto (Haneda/Narita catchment) and Kansai (KIX Expo preparation) | Medium term (2–4 years) |

| Digital tax-refund kiosks & cash-less payments are boosting conversion | 1.3% | National rollout; early gains concentrated in metropolitan gateways (Tokyo, Osaka, Nagoya Centrair) | Short term (≤ 2 years) |

| Limited-edition Japanese whisky boom in global collector circles | 1.0% | Global export markets (United States, China, France); domestic airport duty-free (Narita, Haneda, KIX) capture secondary premiums | Long term (≥ 4 years) |

| Osaka–Kansai Expo 2025 and other mega-events are driving one-off visitor spikes | 0.6% | Kansai/Kinki epicentre; secondary dispersion to Chugoku (Hiroshima), Chubu (Nagoya), and Tokyo metropolitan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

World-leading luxury brand store openings in Japan

Global operators expanded in 2025 as Avolta entered Japan with a 500 square meter food and beverage concession at Kansai International Airport, which adds recognized culinary brands and strengthens cross-channel engagement. Kansai’s Terminal 1 program continues into summer 2026 with a planned slate of 23 stores that includes first airport boutiques for Gentle Monster and Moncler, which target premium traffic around Expo 2025[3]Kansai Airports, “Walk-Through Duty Free and Capacity Upgrade,” Kansai Airports, kansai-airports.co.jp. Lotte Duty Free renovated its Tokyo Ginza flagship in October 2024 and introduced a Korean fashion zone and a curated House of Suntory whisky offering by allocation, which aligns with demographic shifts toward younger and digitally engaged shoppers[4]Lotte Duty Free Newsroom, “Tokyo Ginza Renewal and Category Expansion,” Lotte Duty Free, lottedfs.com.. Airport landlords deepen ties with luxury brands through co-financed boutique buildouts and exclusive placements that create scarcity and commit prime frontage to select operators for long leases. This clustering effect concentrates ultra-high net worth spending in priority terminals and elevates the role of airports within the Japan travel retail market.

Rising duty-free spend by Chinese & Korean travellers

South Korean arrivals led in 2024 and recorded year-on-year growth that changed the mix at key gateways, which raised demand for value-focused products and Korean language services at retail touchpoints. Korean card spending in Japan expanded through 2025, with department stores and duty-free clusters targeting this cohort with tailored counters and curated assortments to support higher frequency trips. Chinese demand turned more volatile in late 2025 as a travel advisory and currency pressure weighed on per-transaction spending and reduced luxury basket sizes at select hubs. Operators pivoted with localized experiences and more consumables to preserve conversion while strengthening their focus on United States and European high-value travelers to diversify exposure. This rebalancing helps stabilize performance in the Japan travel retail market as visitor flows shift and as traffic patterns favor independent travelers over large tour groups.

Airport retail-space expansion & refurbishment at Haneda, Narita, Kansai

Narita advanced a multiyear consolidation that will raise gate counts and drive capacity toward 75 million passengers in the early 2030s, which supports long-term retail intensification on the landside and airside. Haneda added gates and commercial space in 2026 to reduce congestion around Terminal 3 and continues to evaluate processing improvements that enable late-night services and better dwell capture. Kansai completed a major renovation in March 2025 that expanded international capacity and installed a large walk-through duty-free zone, which validated higher revenue capture through improved passenger flow. Automation in registers and backroom replenishment improved speed to shelf and reduced stockouts, which lifted both conversion and average ticket for targeted categories. These changes improve yield per square meter and reinforce the airports’ primacy within the Japan travel retail market.

Digital tax-refund kiosks & cashless payments are boosting conversion

Digital refund workflows and cashless payment acceptance improve throughput at peak times and reduce cashier workload, which helps move high-intent travelers through checkout with fewer delays. Airports rolled out contactless pickup features that integrate with pre-order platforms and mobile wallets, which increased convenience for Chinese and Korean travelers who prefer app-based journeys. Broad acceptance of Alipay and WeChat Pay complements card rails and draws spend from mobile-first customers who often plan purchases before arrival. The November 2026 shift to an airport refund model will standardize the refund point at the exit border and reduce paperwork in stores, which can reallocate staff time to selling and clienteling. These steps enhance conversion in the Japan travel retail market and support consistent execution across terminals that handle late-night and irregular operations.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yen volatility is squeezing margins on imported inventory | -1.5% | National, with acute pressure on luxury-brand sourcing (Kanto metros, Kansai KIX) and duty-free operators holding EUR/USD inventory | Short term (≤ 2 years) |

| Strict customs allowances on alcohol & tobacco purchases | -0.9% | Global compliance (all airports); enforcement concentrated at Narita, Haneda departure gates, and maritime entry points | Long term (≥ 4 years) |

| Acute airport-retail labour shortages are curbing store hours | -1.2% | National crisis, most severe at Narita (16% workforce decline), Haneda Terminal 3, and regional airports (Hokkaido, Kyushu) | Medium term (2-4 years) |

| Grey-market price arbitrage is eroding brand price integrity | -0.7% | Global (daigou networks); domestic concentration in Tokyo Ginza, Osaka Shinsaibashi, and online resale platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Yen volatility is squeezing margins on imported inventory.

Exchange rate swings tightened gross margins for operators carrying imported luxury inventory that had been purchased at prior currency levels, which forced shifts toward more resilient consumables. Haneda reported a lower luxury share through late 2025 that reflected price sensitivity and allocation discipline by brands to manage gray market risks. Some boutiques deferred fit-out expansions as the arbitrage gap to Europe and the United States narrowed, which diluted impulse splurges by price-aware travelers. Payment cost structures added to pressure as cross-border card fees compounded discounts and promotions that retailers used to keep traffic moving. Operators responded by emphasizing bundled sets and airport exclusives in categories like cosmetics to defend volume while accepting lower average transaction values in the near term.

Strict customs allowances on alcohol & tobacco purchases

Japan limits duty-free alcohol to three 760 milliliter bottles and tobacco to 200 cigarettes, which caps bulk buying and pushes high-frequency shoppers to distribute purchases across trips. The general goods threshold triggers duties and consumption tax on overage, which can redirect luxury splurges to downtown boutiques where sales staff guide refund procedures in calmer settings. Enforcement tightened with stronger penalties for false declarations and stepped up inspections that created friction during peak departures. Differences with other hubs like Incheon and Changi influence route shopping as some travelers plan large liquor and tobacco purchases in markets with more accommodating limits. The 2026 switch to an airport refund model will standardize validation at exit points, which may reduce downtown speed advantages and consolidate spirits purchases airside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premiumization rewrites the spirits playbook

Cosmetics and fragrances captured 45.31% of 2025 product revenue and remained the anchor category for frequent buyers, while wines and spirits are forecast to grow at an 11.12% CAGR through 2031 as premiumization deepens. Airport operators raised the visibility of curated whisky and high-end spirits with allocation-based counters and education-led displays that translate scarcity into full price sell-through. The cosmetics mix leaned into airport-exclusive sets and giftable formats that raise average tickets while sustaining a broad penetration rate among shoppers from China and South Korea. Jewelry and watches faced tighter allocations from select brands, which pushed some buyers toward daily queues and reshaped spend toward accessories and footwear within budget thresholds. The Japan travel retail market benefits from this spread of premium and entry options because it supports conversion across diverse spending profiles and trip purposes.

The Japan travel retail market size for wines and spirits is projected to expand at an 11.12% CAGR between 2026 and 2031, which is driven by collector demand and brand storytelling that reward limited releases. Duty-free teams rely on lotteries, pre-order windows, and pick-up lockers to manage high-demand bottles while preserving fairness and regulating crowds near gates. Cosmetics and fragrances continue to anchor volume with sets designed for gifting and self-care, which helps offset volatility in large-ticket luxury when currency or policy shifts weigh on value perception. Food and confectionery sustain high purchase frequency and deliver predictable throughput that supports inventory turns in late-night operations, even if revenue contribution trails premium categories. This product mix helps the Japan travel retail industry balance margin and volume while protecting unit economics through cycles.

By Distribution Channel: Airports entrench dominance, yet downtown duty-free tests limits

Airports commanded 65.35% of channel share in 2025 and are forecast to grow at a 10.58% CAGR through 2031, underpinned by throughput gains and more efficient layouts that steer all passengers past core retail. Haneda set new records for international passengers in 2025, which reinforced airside dominance for liquor, tobacco, and luxury categories where duty exemption and convenience matter most. Kansai’s walk-through flagship raised sales after its renovation due to improved queue management, faster scanning, and better adjacencies that encourage last-minute purchases. Airlines complement ground retail through pre-order exclusives and in-flight allocations that offer premium and collaboration items to captive premium cabins. These factors help consolidate spending in the Japan travel retail market within airport territories and reduce leakage to off-airport locations.

The Japan travel retail market size for airports is projected to expand at a 10.58% CAGR between 2026 and 2031 as operators scale digital pre-order and locker pickup for time-sensitive travelers. Downtown duty-free will shift under the 2026 airport refund regime since cash refunds at the counter will give way to customs validation at departure, which erodes speed advantages for city stores. Ferries and rail-linked convenience concepts add incremental channels but remain constrained by customs procedures, floor space, and lower high-ticket conversion compared with airside. Vertical integrations by airport affiliates that wholesale and retail across multiple airports capture margin at several points and translate loyalty programs into higher repeat purchase rates. These moves reinforce the central role of airports in the Japan travel retail industry while other channels adapt to the refund shift and ongoing staffing constraints.

Geography Analysis

Kanto accounted for 53.31% of the 2025 market value as Haneda and Narita together concentrated international flows, which positioned the region for sustained retail capture despite slot ceilings. The area benefits from dense downtown duty-free clusters that funnel tourists between city shopping and airport pickup options that are synchronized with flight schedules. Visitor profiles now include more repeat travelers who pair Tokyo with regional circuits, which broadens spend beyond the capital while keeping airside purchases strong. The November 2026 refund system may redirect some downtown transactions back toward airside, which supports core categories that retain duty exemption in airports. These changes keep Kanto at the center of the Japan travel retail market while the mix of travelers evolves.

Kansai or Kinki is projected to be the fastest growing region at a 9.82% CAGR through 2031 as the renovated Kansai International Airport and Expo 2025 lift throughput and command attention from global brands. The region’s airport added walk-through formats and upgraded services that support late-night operations and smooth departure peaks during event windows. Department stores and downtown boutiques collaborate with airports by aligning launches and exclusives that keep visitors engaged across the trip lifecycle. Kyushu and Okinawa capture short break traffic from South Korea and leverage ferry links, which supplement airside sales with maritime routes and offshore duty-free operations. This spread channels new and repeat travelers into the Japan travel retail market across multiple gateway types in western Japan.

Hokkaido, Chubu, and other regions add diversity to itineraries as seasonal events and outdoor attractions bring more winter and shoulder season traffic that engages local retail formats. Regional airports and rail networks enhance access and support pop-up retail partnerships that tie into local specialties and craft beverage brands. Duty-free operators tailor inventory to seasonal profiles to reduce stockouts and align shelf space with time-sensitive categories. The Japan travel retail market benefits as travelers spend more time in secondary cities and then complete big-ticket purchases at departure hubs. This pattern reduces concentration risk and supports a more even distribution of retail revenue across the country’s tourism map.

Competitive Landscape

The Japan travel retail market features moderate fragmentation with no single operator above 15% share, which encourages partnerships between airport companies and global travel retailers to secure brand allocations. Kansai Airports worked with Lagardère Travel Retail to deliver a large walk-through duty-free concept that brings multi-category depth and consistent merchandising in a single path. Avolta entered the market in 2025 with a food and beverage footprint that leverages the company’s digital platforms and loyalty to engage travelers who pre-plan purchases and dining. Japan Airport Terminal expanded wholesale and retail links across multiple airports to drive scale benefits and coordinate assortments with operational innovations like robotized replenishment. These moves increase bargaining power with luxury houses and help accelerate rollouts that anchor premium experiences across the Japan travel retail market.

Lotte Duty Free’s Tokyo Ginza store upgraded its floors to balance domestic and inbound demand with Korean fashion and whisky curation that maps to younger and high-intent shopper profiles. DFS Group concentrated on Okinawa’s offshore model and invested in luxury brand spaces that suit the island's shopper needs and align with tourist flows. Airlines amplified retail access through pre-order for allocation of bottles and collaboration goods that can be collected airside or onboard for premium cabins. Technology adoption enabled rapid replenishment and improved availability, which cut lost sales and increased conversion across categories that drive margins. Environmental credentials influence tenders as airport groups highlight carbon accreditation tiers, which carry weight for investors and brand partners.

The portfolio breadth of leading operators provides resilience across cycles as food and beverage, convenience, and luxury cross-subsidize each other under single concession frameworks. Operators that run loyalty ecosystems and own wholesale channels capture data and margin at multiple points, which feeds better category planning and tailored promotions. Staffing tightness remained a constraint, which accelerated trials of low-touch formats that simplify souvenir and essentials sales while preserving service in premium departments. These dynamics point to steady competitive intensity and a premium leaning assortment strategy that aligns with international traffic trends. The net result is a contest for space, brand exclusivity, and digital convenience that defines leadership in the Japan travel retail market.

Japan Travel Retail Industry Leaders

Japan Airport Terminal Co. Ltd.

NAA Retailing (Fa-So-La)

JALUX Inc.

ANA Trading Duty Free

DFS Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Japan Airport Terminal opened HANEDA STAR & LUXE, a high-value gift boutique in Terminal 2 featuring airport-exclusive brands and premium confectionery, targeting business travellers and domestic shoppers seeking prestige souvenirs.

- March 2025: Kansai International Airport completed the grand opening of Terminal 1's full renovation (Phases 1–3), expanding international capacity by 60% and unveiling Japan's largest walk-through duty-free zone (2,500 m²) ahead of Expo 2025.

- January 2025: Japan Tourism Agency launched nationwide explanatory meetings (January 27 – February 24, 2026) to prepare duty-free retailers for the November 2026 refund method transition, emphasising system upgrades and compliance with new customs approval workflows.

- June 2024: Nikka Whisky announced a YEN 6 billion ($38 million) investment to expand storage capacity by 10%, aiming to meet surging international demand and bolster exports as Japanese whisky's global footprint widens.

Japan Travel Retail Market Report Scope

Travel Retail is commonly used to describe the duty-free retail industry, in addition to all retail activities dedicated to travelers and tourists. A complete background analysis of the Japanese Travel Retail Market includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the Market, market dynamics, and key company profiles covered in the report. The Market is segmented by Product Type (Fashion and Accessories, Wine and spirits, Tobacco, Food and confectionary, Fragrances and Cosmetics, and Other Product Types) and by Distribution Channel (Airports, Airlines, Ferries, and Other Distribution Channels). The report offers market size and forecasts for the Japan Travel Retail Market in terms of value (USD) for all the above segments.

By Product Type

| Fashion & Accessories |

| Jewelry & Watches |

| Wines & Spirits |

| Food & Confectionery |

| Cosmetics & Fragrances |

| Tobacco |

| Other Product Types (Stationery, Electronics, etc.) |

By Distribution Channel

| Airports |

| Airlines |

| Ferries |

| Other Channels (Railway Stations, Border Shops, Downtown) |

By Geography

| Hokkaido |

| Tohoku |

| Kanto |

| Chubu |

| Kansai/Kinki |

| Chugoku |

| Shikoku |

| Kyushu & Okinawa |

| By Product Type | Fashion & Accessories |

| Jewelry & Watches | |

| Wines & Spirits | |

| Food & Confectionery | |

| Cosmetics & Fragrances | |

| Tobacco | |

| Other Product Types (Stationery, Electronics, etc.) | |

| By Distribution Channel | Airports |

| Airlines | |

| Ferries | |

| Other Channels (Railway Stations, Border Shops, Downtown) | |

| By Geography | Hokkaido |

| Tohoku | |

| Kanto | |

| Chubu | |

| Kansai/Kinki | |

| Chugoku | |

| Shikoku | |

| Kyushu & Okinawa |

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan travel retail market?

The Japan travel retail market size is USD 4.42 billion in 2026 and is projected to reach USD 7.55 billion by 2031 at a 9.33% CAGR.

Which product categories are leading and growing fastest in Japan travel retail?

Cosmetics and fragrances led with a 45.31% share in 2025, while wines and spirits are forecast to grow at an 11.12% CAGR through 2031.

How dominant are airports in Japan’s travel retail sales?

Airports held 65.35% of sales in 2025 and are projected to grow at a 10.58% CAGR to 2031, supported by terminal upgrades and walk-through formats.

Which regions are most important for Japan travel retail performance?

Kanto accounted for 53.31% of the value in 2025, while Kansai or Kinki is projected to be the fastest-growing region at a 9.82% CAGR through 2031.

How will the 2026 airport refund model affect Japan travel retail?

The November 2026 transition centralizes tax refund validation at the airport and removes packaging rules and purchase caps for consumables while adding new exit confirmation steps.

Page last updated on: