Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

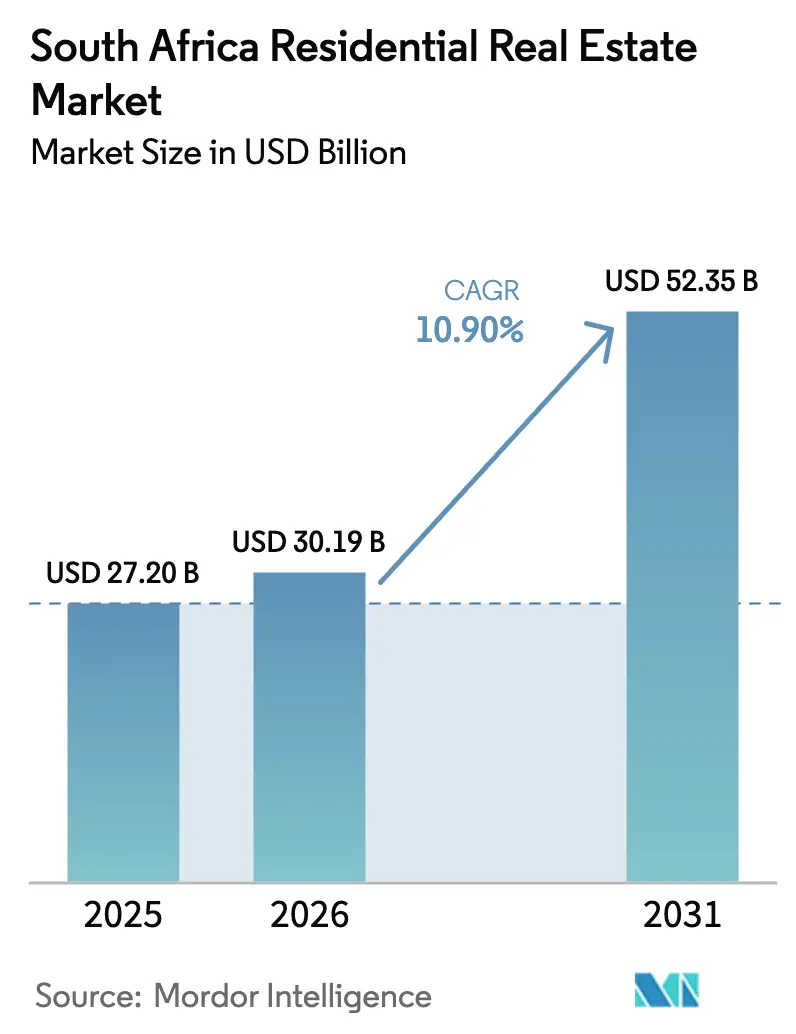

| Base Year Market Size (2025) | USD 27.20 Billion |

| Market Size (2026) | USD 30.19 Billion |

| Market Size (2031) | USD 52.35 Billion |

| Growth Rate (2026 - 2031) | 10.90% CAGR |

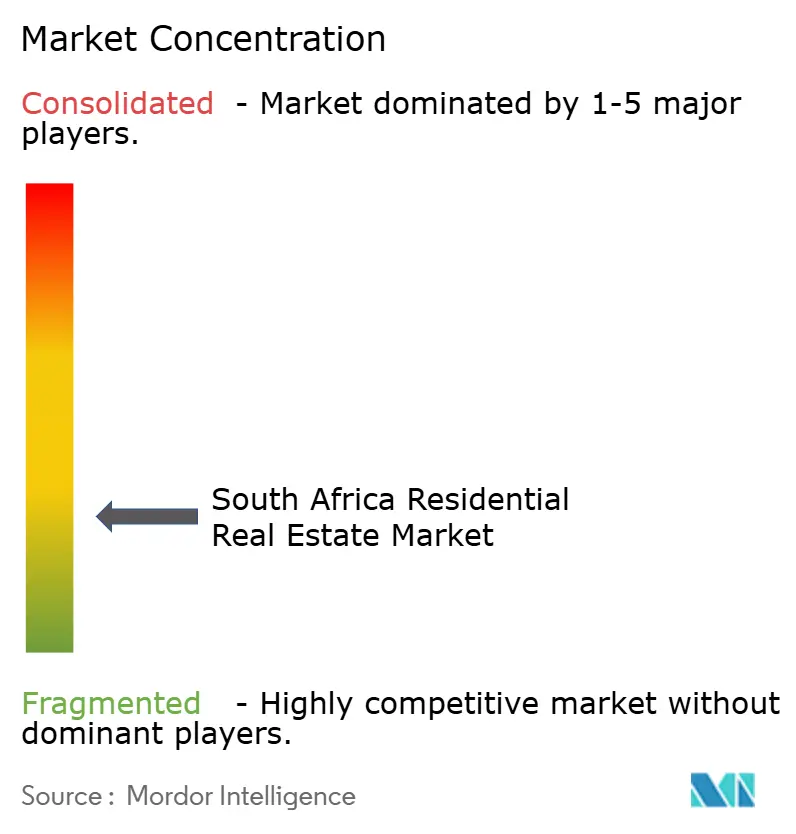

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Residential Real Estate Market Analysis by Mordor Intelligence

The South Africa residential real estate market is estimated at USD 30.19 billion in 2026, and is expected to reach USD 52.35 billion by 2031, at a CAGR of 10.9% during the forecast period (2026 - 2031). This vigorous pace results from easier monetary conditions, the nationwide rollout of the Electronic Deeds Registration System, and sizable pent-up demand in both affordable and coastal lifestyle segments. Momentum continues even while national GDP grew just 0.6% in 2024 and 1.8% in 2025, showing that housing demand operates on drivers largely detached from near-term macro volatility[1]https://www.statssa.gov.za/. First-time buyers draw on expanded FLISP subsidies, while higher-income households relocate from Gauteng to the Western Cape, KwaZulu-Natal, and Eastern Cape, spurring double-digit price expansion in secondary coastal metros. The investment community is also repositioning toward income-producing rental stock as interest-rate cuts widen the spread between gross yields and ten-year sovereign bonds.

Key Report Takeaways

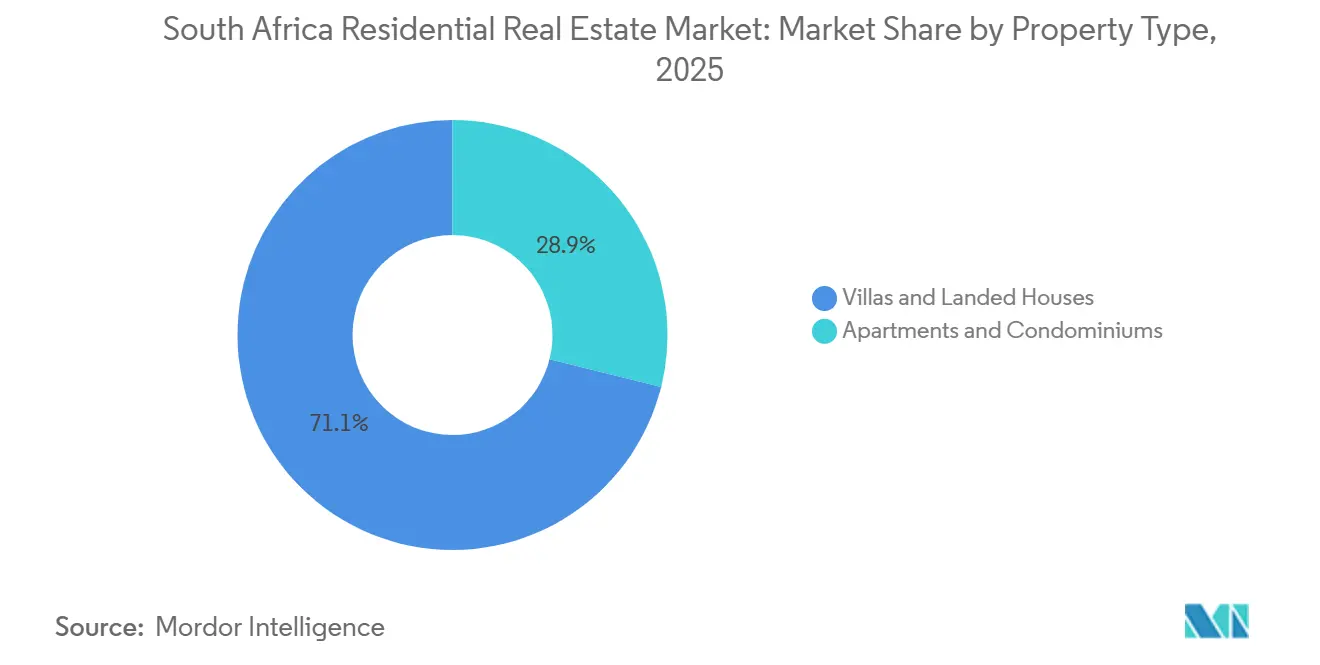

- By property type, villas and landed houses held 71.1% of the South Africa residential real estate market share in 2025, while apartments and condominiums are forecast to post an 11.4% CAGR through 2031.

- By price band, affordable units captured 45.3% of the 2025 value, yet luxury homes priced above USD 273,000 are set to expand at an 11.5% CAGR through 2031.

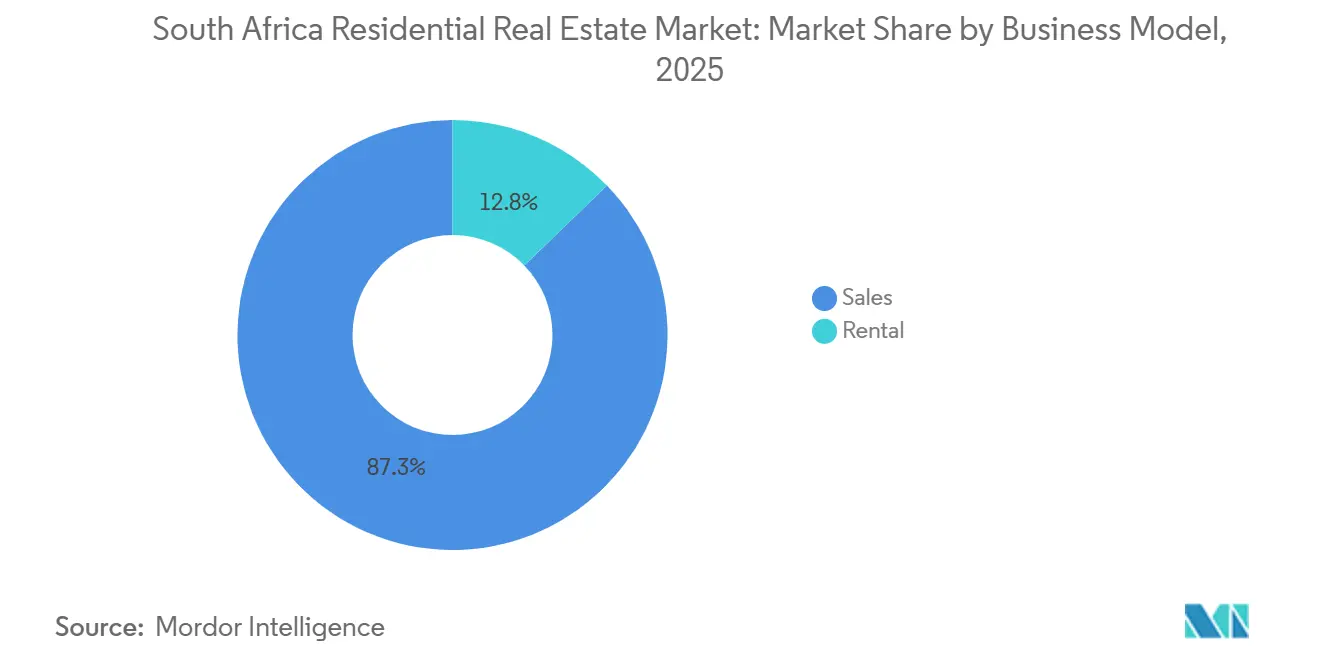

- By business model, sales transactions dominated with an 87.3% share in 2025, whereas rental activity is projected to rise at a 12.2% CAGR over the outlook period.

- By mode of sale, secondary transactions made up 67.9% of value in 2025, and primary new-build sales are expected to grow fastest at 12.4% CAGR to 2031.

- By key cities, Cape Town commanded 23.4% of value in 2025, and Bloemfontein is positioned for the quickest advance at an 11.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural undersupply of affordable housing amid urbanization | +2.8% | Gauteng, Western Cape, KwaZulu-Natal | Long term (≥ 4 years) |

| Expansion of FLISP subsidy and securitization boosting first-time buyers | +2.1% | National | Medium term (2-4 years) |

| Remote-working professionals driving semigration to coastal secondary cities | +1.6% | Western Cape, KwaZulu-Natal, Eastern Cape | Medium term (2-4 years) |

| Buy-to-let investment surge via REIT conversion of sectional-title stock | +1.4% | Major metros | Medium term (2-4 years) |

| Protech-enabled digital transactions accelerating sales velocity | +1.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Structural Undersupply of Affordable Housing Amid Urbanization in Gauteng and Western Cape

Affordable housing stock lags demand by more than 1.6 million units in the two provinces that host the bulk of population inflows[2]https://www.capetown.gov.za/. Waiting lists reached 375,000 households in Cape Town and 1.3 million in Johannesburg during 2024, a gap that widens each year because land release and municipal approvals move slowly. Even though the housing ministry earmarks USD 656 million per year for subsidized build programs, rezoning delays often stretch to 24 months, prompting private developers to focus on pre-serviced corridors such as Midrand Waterfall. Land prices in these nodes exceeded USD 46,500 per plot in 2025, putting pressure on entry-level budgets despite rising subsidies. The imbalance keeps the affordable segment firmly in control of volume growth and underpins steady price inflation even in higher-rate environments.

Expansion of FLISP Subsidy and Securitization Boosting First-Time Buyers

FLISP now covers deposits between USD 2,100 and USD 9,100, which closes the upfront funding gap for households earning up to USD 1,200 monthly. Coupled with a 125-basis-point prime-rate decline that trimmed monthly payments on a USD 55,000 mortgage by USD 66, affordability improved measurably in 2025. New securitization rules allow banks to bundle these loans, lowering origination costs by as much as 75 basis points and lifting approval rates to 68% in 2024. BetterBond and ooba Home Loans processed 22% more FLISP-backed applications year over year, channeling additional liquidity toward the affordable tier. Regional skew persists because Gauteng and Western Cape together still collect 62% of total disbursements.

Remote-Working Professionals Driving Semigration to Coastal Secondary Cities

Remote work settled at 28% of white-collar roles in 2024, giving professionals freedom to leave Gauteng for seaside towns that offer lifestyle benefits and lower home prices. The Western Cape absorbed 32.4% of net inter-provincial moves, and the trend raised median transaction values in Hermanus, Ballito, and Knysna by 3.8% to 4.2% in 2025 [3]https://www.fnb.co.za/. Most migrants are 36-49 years old and purchase properties in the USD 137,000–USD 273,000 band, fuelling new mixed-use estates that integrate coworking hubs. Environmental clearances lasting up to 36 months constrain near-term supply, and that tightness lifts price growth ahead of inland averages. The semigration wave creates a bifurcated trajectory where coastal nodes outpace core Gauteng metros.

Buy-to-Let Investment Surge via REIT Conversion of Sectional-Title Stock

South Africa’s REIT rules incentivize rental-income distribution and limit gearing, attracting yield-seeking investors into sectional-title portfolios. Developers delivered 4,866 sectional units in 2025, up 13.5% year to date, despite a 21.2% slide in municipal approvals, indicating a tilt toward higher-density formats that can be packaged for REIT holdings. Residential penetration inside listed REITs remains under 5%, yet smaller private syndicates stepped in where incumbents Growthpoint and Redefine keep minimal housing exposure. Conversion costs of USD 2,700–USD 8,200 per unit remain a hurdle, but steady rental yields of 6%–8% and faster electronic registration speed strengthen the case. Pension funds that integrate ESG metrics increasingly direct allocations toward affordable rental blocks, giving the segment a longer runway.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prime lending rate above 11% squeezing mortgage affordability | -1.8% | National, with acute impact in Gauteng, Western Cape, and KwaZulu-Natal | Short term (≤ 2 years) |

| Persistent load-shedding inflating build costs & dampening sentiment | -1.3% | National, with severe impact in Gauteng, Western Cape, and KwaZulu-Natal metros | Medium term (2-4 years) |

| Municipal service backlogs delaying plan approvals | -1.1% | Johannesburg, Tshwane, eThekwini, with spillover to secondary metros | Long term (≥ 4 years) |

| Reduced foreign-buyer demand from tighter exchange-control & visa rules | -0.7% | Cape Town (Atlantic Seaboard), Johannesburg (Sandton), Durban (Umhlanga) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prime Lending Rate Above 11% Squeezing Mortgage Affordability

Even after three consecutive rate cuts, the prime rate stood at 10.5% in July 2025, roughly 325 basis points above the 2019 average. Monthly payments on a USD 55,000 loan consume 34% of the median Gauteng household income, breaching the 30% affordability ceiling promoted by the National Credit Regulator. Bond approval rates for non-subsidized applicants slipped to 52% in 2024 as banks tightened debt-service ratio thresholds. Developers acknowledged the strain; Balwin’s mid-2025 unit sales fell 16% year on year, pushing the firm further toward entry-level product lines. A deeper rate-cutting cycle would clearly lift sentiment, but it remains contingent on disinflation that is not yet fully embedded.

Persistent Load-Shedding Inflating Build Costs and Dampening Sentiment

Although Eskom suspended outages after March 2024, developers still carry the cost of backup systems installed during 2022–2023, increasing construction budgets by roughly 10%. Survey data show that 43% of prospective buyers rank reliable power as a decisive factor, especially in Johannesburg and Cape Town. Solar and battery packages add USD 8,200–USD 13,700 per unit, pushing certain affordable products above subsidy thresholds. Treasury’s infrastructure pipeline reaches 2030, so the risk of renewed blackouts still weighs on confidence. As long as sentiment remains fragile, discretionary upgrades and second-home purchases stay below their potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Villa dominance and apartment ascent

Villas and landed houses commanded a 71.12% South Africa real estate market share in 2025, reflecting entrenched preferences for private outdoor space and gated security. Transaction volumes surged in semigration hot-spots where larger erven remain attainable, reinforcing the segment’s leadership. Yet urban land scarcity and rising construction costs encourage compact layouts, nudging developers to consider modular designs and off-site fabrication. Institutional landlords are also re-entering the mid-income freehold segment, bundling scattered homes into rental portfolios to capture yield stability.

Apartments and condominiums represent the fastest-growing slice, expanding at an 11.4% CAGR toward 2031. Developers leverage sectional title legislation to pre-sell units, which eases project financing and de-risks balance sheets. Mixed-use precincts in Cape Town’s Longkloof or Johannesburg’s Sandton nodes blend residential, retail, and flexible offices, appealing to professionals who value proximity over plot size. Smart-home features and green building ratings amplify tenant appeal, while short-stay platforms create ancillary income streams that bolster underwriting assumptions.

By Price Band: Affordable leadership with luxury surge

Affordable homes priced at or below USD 82,000 claimed a commanding 45.3% of the 2025 value, thanks to the widened FLISP bracket and securitized mortgage funding. In parallel, luxury stock above USD 273,000 enjoys the fastest expected advance at 11.5% CAGR, reflecting continued semigration from Gauteng and the inflow of international retirees. The dual-track pattern keeps median effective price increases modest in mid-market bands where interest-rate sensitivity is highest. Cape Town’s Atlantic Seaboard saw luxury transactions eclipse 14% year-on-year in 2024, although the same geography supports only slow affordable activity because median land costs run far beyond subsidy coverage.

FLISP expansion narrowed deposit gaps for thousands of entry-level families, but the programme’s USD 82,000 ceiling excludes core Atlantic Seaboard and Sandton addresses. Consequently, Bloemfontein, Gqeberha, and Polokwane register disproportionate take-up. Luxury buyers, meanwhile, remain less rate-conscious and prioritize security, proximity to beaches, and immediate access to backup power. Developers balance the portfolio by rolling out mixed-product estates that slot high-end detached homes beside mid-rise affordable blocks, an approach evident in Balwin’s Ballito Hills project. The strategy hedges against cyclical swings and anchors stable cash flow under varying credit conditions.

By Business Model: Ownership tradition meets rental momentum

Sales still accounted for 87.3% of 2025 turnover, but the rental slice is poised for a 12.2% CAGR to 2031, outstripping sales growth of 10.6%. Gross yields of 6%–8% exceed inflation by roughly 200 basis points and, once leverage is applied, generate attractive cash-on-cash returns for REIT and private-equity players. Electronic registration boosts liquidity, which shortens the cash conversion cycle for professional landlords. For end-users, elevated interest rates delay ownership and intensify rental demand, especially among the 25–34 age cohort in Cape Town and Johannesburg.

Residential REIT penetration remains low at under 5%, yet conversion momentum is building as pension funds seek alternatives to volatile equity dividends. High vacancy in older Johannesburg CBD towers is driving share-block-to-sectional shift because fresh capital is more willing to underwrite refurbishments once ownership is simplified. Longer term, rising institutional interest should narrow the pricing gap between commercial and residential cap rates, making the sector structurally more investable for global capital.

By Mode of Sale: New-Build Momentum Defies Approval Bottlenecks

Secondary transactions comprised 67.9% of market value in 2025, reflecting the dominance of South Africa’s mature housing stock. Nonetheless, primary new-builds carry the highest outlook at 12.4% CAGR as developers preload pipelines with land already cleared for infrastructure. Affordable-focused Calgro M3 delivered 1,650 units in 2024 and maintains a queue of 25,000 plots, illustrating how deep land banks offset municipal bottlenecks. Buyers gravitate toward energy-efficient new stock that sharply lowers running costs, a factor that existing-home sellers struggle to match without costly retrofits.

The Electronic Deeds Registration System cuts title lag, which used to create a mismatch between developer outflows and inflows. That improvement reduces financing costs and lowers the minimum viable scale for boutique builders. However, mid-market price points still face shortages because land inside established metros remains costly and scarce. Unless service-delivery backlogs improve, most short-term volume gains will come from projects adjacent to already serviced corridors.

Geography Analysis

Cape Town maintained a 23.4% slice of the South Africa residential real estate market in 2025 and achieved enduring premiums because a 375,000-unit waiting list keeps formal stock undersupplied. The city’s Atlantic Seaboard trades at average prices above USD 547,000, attracting both domestic semigrants and a stable pool of foreign buyers, though recent visa tightening added friction to offshore demand. Transaction values continue to rise even while municipal approvals contracted 21.2% in 2025, underscoring structural supply limits.

Johannesburg houses the nation’s largest urban economy, yet a 40% non-compliance rate across 3,000 buildings chokes fresh inventory, pushing up prices in Sandton and Rosebank well ahead of broader Gauteng averages. Remote workers relocating to the Western Cape and KwaZulu-Natal temper local absorption, yet Johannesburg still seeds liquidity into secondary nodes when owners dispose of high-value assets to fund coastal purchases. Durban’s eThekwini municipality faces a 60% compliance backlog, but Umhlanga and Ballito outperform on the back of strong in-migration and corporate relocations linked to the Dube TradePort.

Bloemfontein posts the fastest growth trajectory at 11.8% CAGR to 2031 because USD 52,000 median pricing sits squarely within FLISP eligibility, boosting first-time ownership. Pretoria sustains a moderate 3.5% annual appreciation by leveraging its public-sector employment base. Port Elizabeth trails coastal peers due to auto-sector volatility, yet new logistic corridors could revive sentiment beyond 2026. Outlying metros and rural nodes hold roughly one-third of national value and will keep expanding in line with broader semigration patterns as connectivity and remote-work tools improve.

Value Chain Analysis

South Africa's residential real estate value chain starts with land assembly and entitlements (municipal zoning, plan approvals, and environmental clearances), moves through project financing and construction (developers, contractors, and materials supply), then to distribution (broker networks and digital lead platforms), and ends with transaction finalization (bond origination, conveyancing, and deeds registration) and ongoing operations (property management, utilities, and municipal rates). The rollout of the Electronic Deeds Registration System and the growth of mortgage intermediaries such as BetterBond and ooba increase transaction throughput by tightening the handoff between banks, conveyancers, and the deeds office, while brokers (Pam Golding, Seeff, RE/MAX) increasingly package sales with virtual viewings and data-enabled pricing support.

The main friction points sit upstream in approvals, infrastructure readiness, and build-cost volatility. In 2026, contractors reported applying conflict-related surcharges of about 10% to 15% on new builds alongside longer lead times from shipping reroutes, pushing developers toward local-first sourcing and alternative building technologies supported by the National Home Builders Registration Council. On the demand-to-close side, affordability pressures cascade through the chain, as higher deposit requirements reported by BetterBond in April 2026 and elevated municipal charges in large metros increase the all-in cost of ownership for end buyers and landlords, influencing product design (smaller units, sectional title) and investor underwriting for rental blocks.

Competitive Landscape

The South Africa residential real estate market is considered to be highly fragmented. Developers Balwin Properties and Calgro M3 dominate the affordable-to-mid-market band, but both reported margin compression after backup-power investments lifted build costs by about 10% during the 2022–2023 blackout period. Balwin’s revenue fell to USD 145 million in the half year to August 2024, prompting a pivot toward products priced below USD 82,000, while Calgro sustained positive growth through disciplined land banking and phased rollouts.

Brokerage rivals Pam Golding, Seeff, and RE/MAX differentiate via digital platforms that integrate electronic deeds registration, 3D walk-throughs, and chatbot lead capture. Pam Golding executed more than 15,000 transactions in FY 2024 and saw rental revenue climb 12% as investors chased high gross yields. RE/MAX leverages a 2,500-agent footprint to deepen reach in secondary metros such as Bloemfontein and Nelspruit, while Seeff capitalizes on early solar-ready listing certification to appeal to power-conscious buyers.

PropTech originators BetterBond and ooba process over 40% of new mortgages and have built machine-learning scorecards that compress decision cycles. On the institutional side, listed REITs Growthpoint and Redefine remain under-weight residential, although smaller private vehicles accelerate conversion pipelines for sectional-title blocks. ESG-aligned pension funding is emerging as a potent force in green affordable projects and could reshape competitive dynamics once scalable structures reach full proof of concept.

South Africa Residential Real Estate Industry Leaders

Pam Golding Properties

Seeff Property Group

RE/MAX of Southern Africa

Rawson Property Group

Chas Everitt International

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Market whitespace is most visible in delivery models that bridge the affordable and "missing middle" bands while working around municipal capacity constraints. National government flagged 212 stalled housing projects in March 2026 and put a formal process in place to categorize and unblock them using earmarked funding, which creates actionable scope for contractors, developers, and project managers that can remediate partially completed sites, re-scope services, and bring units to transfer rather than relying only on greenfield approvals. In the Western Cape, the Department of Infrastructure introduced an Instalment Sale Agreement model at the Mountain View development in Mossel Bay in July 2026, providing a template for rent-to-own or instalment-based ownership that developers and financiers can replicate in other fast-inmigration nodes.

Digitization across valuation, underwriting, and construction execution opens another opportunity lane, particularly where deeds and municipal data can be converted into bankable decision tools. Lightstone Property introduced AI-driven valuation models in May 2026 that integrate deeds, cadastral, and municipal datasets, supporting faster and more consistent pricing, which benefits brokers, lenders, and institutional buyers assembling rental portfolios. In parallel, construction firms are standardizing cloud collaboration and estimating workflows, which aligns with the need to control cost swings linked to imported materials and logistics; combined with tighter safety oversight signaled by Public Works and Infrastructure in July 2026 through a national built-environment and construction safety framework, the market favors developers and contractors that can document compliance and provide auditable project controls.

Recent Industry Developments

- July 2026: The Western Cape Department of Infrastructure introduced an Instalment Sale Agreement model at the Mountain View development in Mossel Bay to help the missing middle access home ownership. By formalizing an alternative path to ownership outside traditional mortgages, it broadens the addressable buyer pool for developers active in coastal and secondary metros.

- April 2026: BetterBond reported a quarter-on-quarter increase in deposit requirements across buyers, tightening upfront affordability even as rate conditions eased from earlier peaks. The shift changes conversion rates from viewing to bond approval and pushes developers and brokers to reconfigure product and pricing toward subsidy-linked and lower-ticket stock.

- April 2025: The Deeds Office deployed the Electronic Deeds Registration System, reducing transfer timelines to around three weeks and shortening the cash-conversion cycle from offer to registration. Faster registration improves liquidity for investors and supports higher transaction velocity for brokers, conveyancers, and developers selling primary stock.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the annual value of residential property activity in South Africa, covering homes that are formally built, legally zoned, and traded or leased through recognized channels, with values captured in USD.

Scope exclusions: Informal backyard dwellings and unregistered rural homesteads are excluded because they do not consistently show up in formal transaction or lease records.

Segmentation Overview

- Sales

- Rental

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by pulling the most repeatable public signals on housing demand, affordability, and formal supply. We rely on sources such as Statistics South Africa releases, the South African Reserve Bank macro series, and the National Treasury budget documents to anchor income, inflation, and credit direction. Property and transaction signals are then cross-checked using sources such as Deeds Registry style transaction aggregates, municipal planning and building permit publications, and central bank or regulator releases tied to mortgage activity.

To tighten the model inputs, we also review company filings and investor presentations from listed real estate related groups, along with industry association updates and trusted press coverage on rate moves and housing policy. In a few places, paid subscriptions are used to speed up company financials and intelligence screening, plus patent databases when PropTech adoption signals are relevant to transaction efficiency. The sources listed here are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys with developers, brokers, lenders, property managers, and local specialists who track pricing and absorption at the city level. Since this is a single-country market, the discussions are balanced across key metros and secondary coastal areas so that unit trends, mortgage appetite, and rental tightness can be tested before assumptions are locked. We also revisit respondents when desk signals move sharply, like an unexpected rate shift or a policy change affecting first time buyers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | |

| Mid tier: 46% | Functional/Unit leaders: 38% | |

| Smaller Players: 19% | Managers: 50% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where demand and value are reconstructed from housing transaction and mortgage related indicators, and then aligned to formal rental activity trends. The model is further checked using selective bottom-up approximations like sampled price per square meter ranges by city, observed transaction volumes by property category, and channel checks with brokers and property managers.

Key inputs that shape the annual totals include residential mortgage rate direction, household formation and urban migration signals, new housing completions and permit activity, deed registration and transfer timing, and rental vacancy and escalation patterns. When any one indicator is incomplete for a period, we fill gaps by using nearby time series behavior and then validate the effect with interview feedback so we do not overstate short-term swings.

For forecasting, scenario analysis is used around interest rate paths and affordability, and the base case is then smoothed using a simple multivariate regression that links value growth to rates, inflation, and housing supply momentum. The final curve is adjusted only after it stays consistent with practical market checks, like absorption speed in active metros and typical down-payment behavior discussed by lenders.

Data Validation & Update Cycle

Validation is handled through a clear set of cross-checks where model outputs are compared with independent signals such as mortgage growth direction, deed activity trends, and observed pricing changes in major metros. Outliers are flagged early, and the assumptions behind them are reviewed in steps, first by the analyst building the model and then through an internal review before sign-off.

When variances widen beyond what the real-world indicators support, respondents are re-contacted to confirm whether the shift is structural or temporary (for example, a rate cut cycle starting sooner than expected). Reports are refreshed annually, and interim updates are made if a material event changes demand or pricing behavior. Before delivery, a fresh pass is completed so the latest releases and market developments are reflected in the final numbers.

Mordor Intelligence's South Africa Residential Real Estate Market Size Versus Other Published Estimates

Published market sizes for South Africa residential real estate can look far apart, even when they talk about similar years, because the underlying scope and the way values are counted are not always the same. Differences usually come from what gets included as residential activity, how rentals are treated, and whether the estimate is tied back to formal transaction evidence or mainly to macro growth assumptions.

The main gap comes from whether informal and unregistered housing activity is counted, where Mordor Intelligence keeps the sizing tied to formally traded or formally leased homes that show up in deed based and recognized lease signals, which tends to avoid inflating value with hard to verify volumes. Some publishers also publish an all-real-estate number and then label it as residential in summaries, and that alone can lift the total because commercial property cycles and pricing behave differently. Currency timing and the assumed speed of price growth also matter, especially when a source uses a conservative rate path versus a faster easing path and then applies it directly to home values.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 27.20 B (2025) | |

| Industry Press Release A | USD 51.69 B (2024) | Uses a broad South Africa real estate scope that can blend residential and commercial activity, and it does not clearly separate formal home transactions and rentals from the wider property value pool. |

| Industry Listing Platform B | USD 30.19 B (2025) | Quotes a single year value but the study window and inclusions are not fully transparent, so rentals, new-build versus resale treatment, and currency conversion timing may not match a consistent annual value model. |

Taken together, the spread is explained mostly by scope and counting rules rather than by a simple disagreement on growth. Our approach stays traceable to observable housing signals, and the assumptions are checked with market participants so the final value is easier to reproduce and update.

Key Questions Answered in the Report

How large is the South Africa residential real estate market today?

The South Africa residential real estate market size is USD 30.19 billion in 2026 and is forecast to exceed USD 52 billion by 2031.

Which segment holds the biggest share of value?

Villas & landed houses lead with 71.1% of 2025 transaction value, reflecting a long-standing consumer preference for freestanding properties.

What is driving the sharp rise in sectional-title apartments?

Developers favor high-density formats on scarce urban land, and faster digital deeds transfer improves liquidity for investors, resulting in an 11.4% CAGR outlook for apartments to 2031.

Why is Cape Town consistently the most expensive metro?

A chronic undersupply, strong lifestyle appeal and steady inflow of high-net-worth semigrants push Cape Town prices well above other metros.

How are interest-rate trends affecting first-time buyers?

A 125-basis-point drop in prime rate since 2024 trims monthly payments, while FLISP subsidies narrow deposit gaps, lifting approval rates for entry-level borrowers.

What makes Bloemfontein the fastest-growing city market?

Affordability around USD 52,000, combined with lower municipal bottlenecks, positions Bloemfontein for an 11.8% CAGR through 2031.

Page last updated on: