Regulatory Reporting And Compliance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.7 Billion |

| Market Size (2031) | USD 7.24 Billion |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Regulatory Reporting And Compliance Market Analysis by Mordor Intelligence

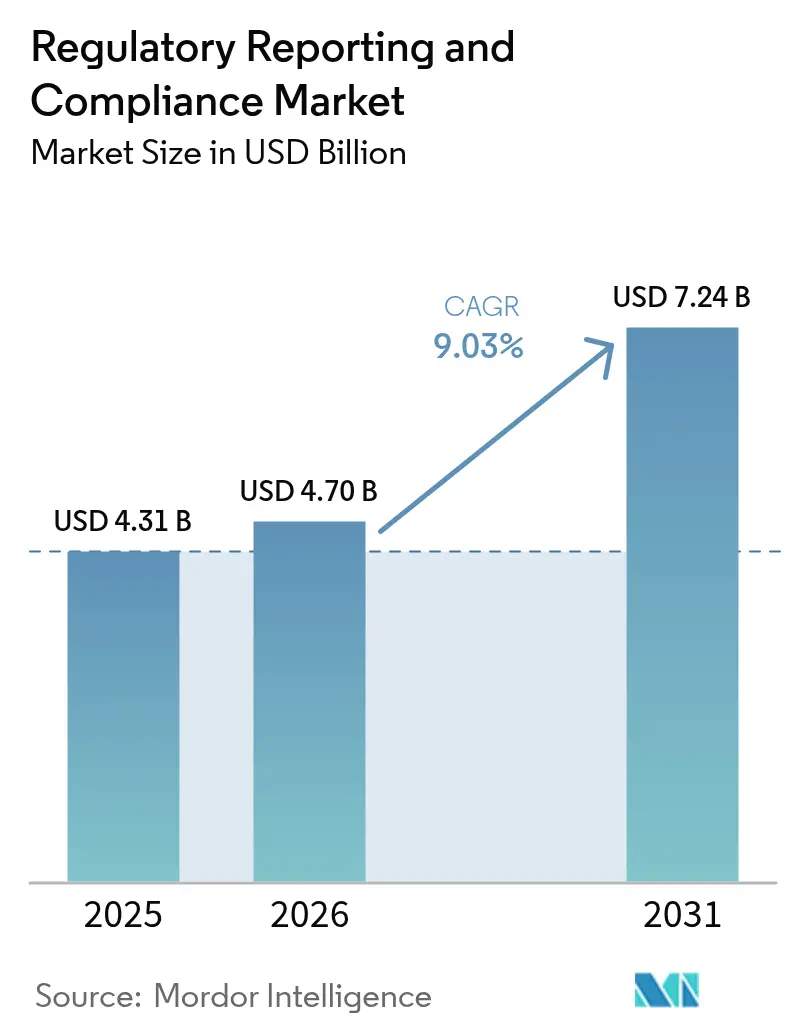

The regulatory reporting and compliance market size in 2026 is estimated at USD 4.70 billion, growing from 2025 value of USD 4.31 billion with 2031 projections showing USD 7.24 billion, growing at 9.03% CAGR over 2026-2031. Market expansion is driven by harmonized guidelines from the International Council for Harmonisation (ICH), the U.S. Food and Drug Administration’s (FDA) stricter data integrity rules, and the European Medicines Agency’s (EMA) digital submission mandates. Heightened demand for rapid dossier approval, widespread adoption of electronic Common Technical Document (eCTD) formats, and the increasing prevalence of multi-regional clinical trials underscore the need for a sophisticated compliance infrastructure. Biotechnology pipelines, breakthroughs in gene and cell therapy, and the rise of artificial-intelligence (AI)–enabled regulatory platforms further accelerate spending. Vendors capable of pairing deep domain expertise with cloud-native, data-driven technologies are gaining competitive traction, reshaping service delivery models across the pharmaceutical, biotechnology, and medical device segments.

Key Report Takeaways

- By service type, consulting led with 28.10% of the regulatory reporting and compliance market share in 2025, whereas regulatory writing and publishing is poised for an 11.10% CAGR through 2031.

- By service provider type, in-house teams held 63.65% of the regulatory reporting and compliance market share in 2025, while outsourced models are expected to expand at a 10.75% CAGR over 2026-2031.

- By end user, pharmaceutical firms captured 34.80% share of the regulatory reporting and compliance market size in 2025, yet biotechnology companies record the fastest 12.10% CAGR to 2031.

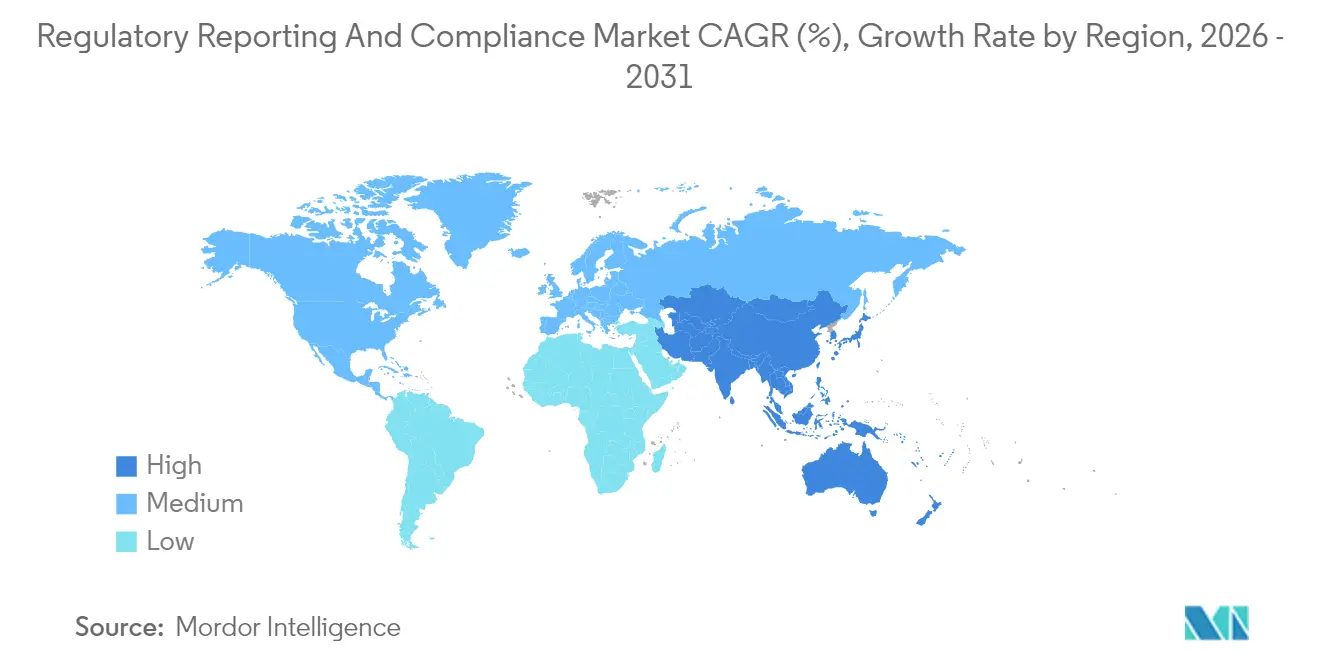

- By geography, North America dominated with 41.10% share in 2025; Asia-Pacific advances at a 10.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Regulatory Reporting And Compliance Market Trends and Insights

Drivers Impact Analysis*

| Driver | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Faster Approval Process | +2.1% | Global, highest in North America & Europe | Short term (≤ 2 years) |

| Continuously Changing Regulatory Landscape | +1.8% | Global, notably APAC emerging markets | Medium term (2–4 years) |

| Digitalization of Regulatory Processes | +2.3% | North America & EU core, spill-over to APAC | Medium term (2–4 years) |

| Increasing Complexity of Multi-Region Clinical Trials | +1.6% | Global, concentrated in major pharma hubs | Long term (≥ 4 years) |

| AI-Enabled Regulatory-Intelligence Platforms Shorten Dossier Cycles | +1.4% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| ESG-Driven Disclosure Mandates Expand Compliance Scope | +0.8% | Europe & North America, emerging in APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Faster Approval Process

Breakthrough therapy designation halves FDA review timelines, creating premium demand for advisory services that compress submissions without compromising rigor[1]U.S. Food and Drug Administration, “Breakthrough Therapy Program Performance Report,” fda.gov. Specialized regulatory writers now command 40% price premiums for expedited dossiers. Real-world evidence (RWE) guidelines, updated in 2024, open new acceleration avenues yet require advanced analytics unavailable in most in-house teams. As sponsors harness RWE, external partners with robust data-science capabilities help navigate evolving evidence standards. This emphasis on speed sustains above-market fee structures and cements deep vendor-client collaboration. Competitive pressure to reduce launch gaps reinforces the regulatory reporting and compliance market’s strategic value proposition.

Continuously Changing Regulatory Landscape

In 2024, regulators issued more than 200 substantive guideline updates, forcing companies to maintain continuous surveillance. China’s National Medical Products Administration released 15 new technical guidelines, reshaping dossier formats and safety-reporting thresholds. Timely interpretation of overlapping national and ICH frameworks now exceeds the capacity of many internal teams. Hybrid models blend core expertise with specialized consultants for jurisdiction-specific compliance, enabling flexible resource allocation. While global harmonization holds long-term promise, near-term complexity keeps external advisory services indispensable. Companies allocating higher budgets for horizon-scanning tools illustrate the regulatory reporting and compliance market’s resilience.

Digitalization of Regulatory Processes

Electronic submissions represent 85% of FDA filings, up from 45% in 2019. EMA’s IRIS pilot cut first-cycle assessment times by 30%. Structured Product Labeling (SPL) upgrades mandate machine-readable formats, compelling sponsors to adopt cloud-native regulatory information management systems. Consultancy demand spans platform selection, data migration, and user training. Vendors offering turnkey implementation solutions report 40% efficiency gains for clients. As agencies increasingly employ AI-driven document screening, service providers with natural-language processing tools strengthen competitive edges.

Increasing Complexity of Multi-Region Clinical Trials

Global trials now span an average of 12 jurisdictions, each enforcing distinct data standards. WHO’s registry logged 25% more multi-regional trials in 2024, reflecting decentralization strategies[2]World Health Organization, “International Clinical Trials Registry Platform Annual Report 2024,” who.int. Divergence between EU and post-Brexit UK rules adds dual-compliance burdens, while rare-disease programs necessitate compassionate-use protocols across regions. Consultants skilled in FDA, EMA, PMDA, and NMPA nuances command premium fees. Digital trial-master-file solutions and cross-jurisdictional harmonization frameworks create new service niches. Complexity extends engagement cycles, supporting sustained growth in the regulatory reporting and compliance market.

Restraints Impact Analysis*

| Restraint | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Technologically Advanced Infrastructure in Developing Nations | −1.2% | APAC emerging markets, MEA, Latin America | Medium term (2–4 years) |

| Complicated Local and Global Regulatory Norms | −1.5% | Global, most acute in multi-jurisdiction filings | Short term (≤ 2 years) |

| Shortage of Skilled Regulatory-Affairs Professionals | −1.8% | Global, most acute in North America & Europe | Long term (≥ 4 years) |

| Cyber-Security & Data-Residency Hurdles for Cloud Compliance Tools | −1.1% | Europe, North America, data-sovereignty focused regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lack of Technologically Advanced Infrastructure in Developing Nations

Paper-based processes persist in India, Brazil, and parts of Africa, forcing multinational sponsors to run parallel paper and electronic workflows, inflating compliance costs by up to 30%. Government-funded upgrades progress unevenly, leaving implementation gaps that hamper cloud-based submissions. Vendors address the divide through hybrid solutions combining low-bandwidth portals with on-site scanning hubs. Nonetheless, slow modernization tempers adoption of advanced AI-driven tools, moderating the regulatory reporting and compliance market’s broader CAGR.

Shortage of Skilled Regulatory-Affairs Professionals

Industry surveys show 40% of firms struggle to fill senior roles, particularly in AI-centric dossier strategy[3]Regulatory Affairs Professionals Society, “2024 Global Regulatory Workforce Trends Survey,” raps.org. Salary premiums surpass 60% for cross-jurisdictional experts. Universities lag in offering curricula covering digital submissions and real-world data analytics. The impending retirement of one-third of senior practitioners risks institutional knowledge drain. Consulting firms counter talent scarcity through accelerated training academies and global talent hubs, yet supply gaps persist, capping near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Consulting Dominance Faces Digital Disruption

Consulting captured 28.10% of the regulatory reporting and compliance market share in 2025 on the strength of expertise in navigating complex submission pathways. Regulatory writing and publishing is accelerating at an 11.10% CAGR, supported by the FDA’s enhanced eCTD and the EMA’s structured-data mandates. This rise in automation, artificial-intelligence content generation, and cloud-enabled template libraries reshapes resource allocation, prompting consultants to integrate technology partnerships. As sponsors prioritize speed, specialized writing teams deliver machine-readable dossiers that satisfy global agencies’ evolving technical standards. Meanwhile, legal-representation services grow steadily due to increased FDA warning-letter activity, and pharmacovigilance consulting gains momentum amid expanded post-market safety requirements.

Digitization casts consulting firms as technology orchestrators rather than pure advisory bodies. To protect margins, incumbents embed proprietary natural-language processing engines that auto-populate Module 3 and 5 components. This integration repositions human experts toward high-value strategic content. Consulting’s incumbency remains resilient, yet providers without technology roadmaps risk commoditization. Over the forecast period, the regulatory reporting and compliance market will witness convergence between content generation, data-engineering, and strategic advisory as clients demand unified, technology-enabled service suites.

By Service Provider Type: Outsourcing Accelerates Despite In-House Preference

Although in-house teams controlled 63.65% of the regulatory reporting and compliance market size in 2025, outsourced models are advancing at a 10.75% CAGR on cost and expertise advantages. Remote-work normalization dissolved geographic barriers, enabling sponsors to engage global talent pools. Outsourcing firms leverage economies of scale, offering turnkey regulatory information management systems and 24/7 monitoring services. Hybrid strategies now dominate: core regulatory strategy remains internal, while dossier authoring, horizon scanning, and multi-jurisdictional intelligence shift externally.

To capture premium engagements, providers invest in AI-based knowledge graphs that map historical agency queries to predictive response templates. These innovations drive first-cycle approval rates higher, appealing to cash-constrained biotech clients. Nevertheless, intellectual-property security and cultural alignment remain board-level concerns, prompting rigorous vendor due-diligence processes. The regulatory reporting and compliance market’s competitive intensity rises as full-service CROs, specialized boutiques, and RegTech startups vie for share through differentiated technology stacks.

By End User: Biotechnology Innovation Drives Premium Services

Pharmaceutical companies maintained 34.80% revenue share in 2025, yet biotechnology sponsors spearhead growth with a 12.10% CAGR. Rapid gene and cell therapy development introduces complex CMC (chemistry, manufacturing, and controls) data packages and heightened post-market commitments, stretching biotech in-house resources. Consultants capable of orchestrating accelerated approval pathways command 50% fee premiums. Meanwhile, medical-device firms rely on specialized advisors for EMA Medical Device Regulation (MDR) dossiers and the FDA’s evolving AI/ML product guidelines.

As convergence blurs lines between pharmaceuticals, biologics, and devices, service providers must integrate multidisciplinary expertise. Sponsors increasingly request platform-agnostic regulatory strategies covering gene editing, digital therapeutics, and combination products. This breadth reinforces the value proposition of end-to-end advisory firms. Over the forecast horizon, biotech’s share of the regulatory reporting and compliance market will continue expanding as venture investment funds scientific breakthroughs, keeping compliance consultancies central to commercialization success.

Geography Analysis

North America controlled 41.10% of the regulatory reporting and compliance market size in 2025, anchored by stringent FDA standards and a high concentration of large pharmaceutical sponsors. The agency’s adoption of AI-assisted review tools elevates technical-compliance requirements, channeling demand toward consultants adept in machine-readable submissions. Canada’s participation in Project Orbis and alignment with FDA oncology frameworks further sparks cross-border advisory engagements. Intellectual-property protection and strong venture funding amplify the region’s outsourcing budgets, sustaining above-average service pricing.

Asia-Pacific is the fastest-growing region at a 10.15% CAGR through 2031, powered by China’s regulatory reform agenda, Japan’s PMDA consultation enhancements, and India’s digital-submission pilot programs. Diversity of regulatory maturity creates fragmented demand patterns: global firms need local partners to interpret country-specific rules, while indigenous manufacturers seek expertise to meet FDA and EMA export requirements. Vendors that establish regional centers with bilingual teams and real-time intelligence platforms capture early-mover advantages in the regulatory reporting and compliance market.

Europe remains a mature but evolving arena. EMA’s ongoing digital-transformation roadmap and the UK MHRA’s post-Brexit divergence introduce complexity that bolsters advisory fees. Sustainability-related disclosure obligations broaden the compliance remit, creating opportunities for ESG-focused consultants. Northern and Western Europe lead digital adoption, whereas Central and Eastern sub-regions lag, opening niche engagements for infrastructure modernization. Elsewhere, Latin America, the Middle East, and Africa register slower uptake due to limited technical infrastructure but represent long-term opportunities as multinationals expand trials and manufacturing footprints. Targeted capacity-building initiatives by global health agencies gradually unlock new consulting revenue streams.

Competitive Landscape

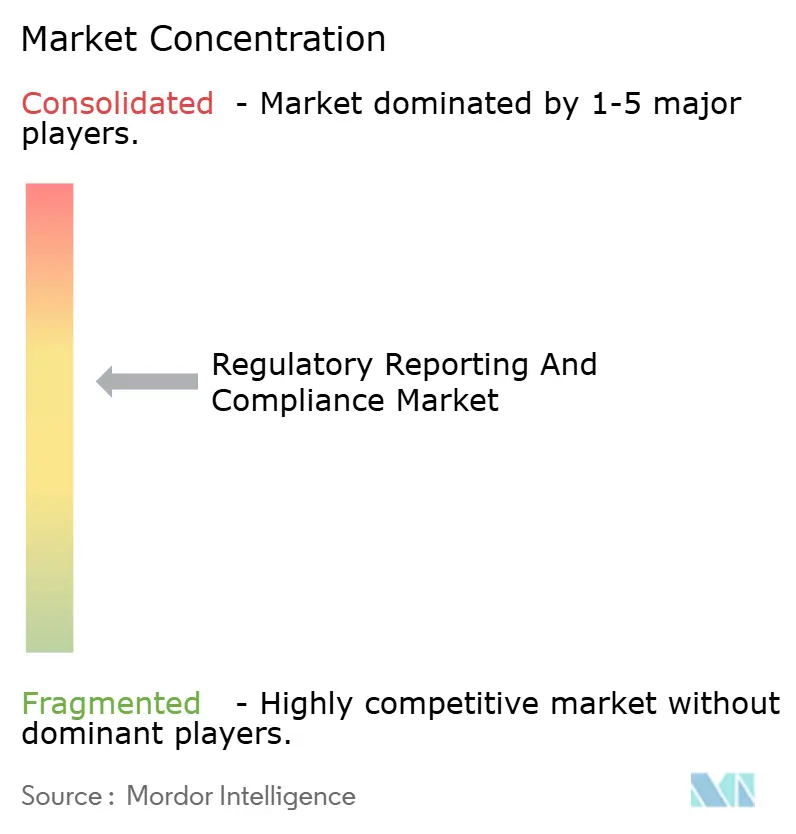

The regulatory reporting and compliance market is moderately fragmented, with top players comprising a combined 40-45% revenue share. Global leaders IQVIA, Syneos Health, and Parexel integrate scale, therapeutic breadth, and proprietary technology to defend positions. They invest heavily in machine-learning engines that predict approval timelines and auto-curate global regulatory changes. Mid-tier firms differentiate through deep expertise in specific therapeutic areas, such as rare diseases or advanced biologics, while RegTech startups focus on platform-based automation.

Consolidation accelerated in 2024 as strategic acquisitions filled technology gaps and expanded geographic reach. Syneos Health acquired Endpoint Clinical to strengthen rare-disease and breakthrough-therapy capabilities. Parexel established an APAC regulatory intelligence center in Singapore, reflecting geographic diversification strategies. Traditional contract research organizations integrate end-to-end regulatory offerings, challenging pure-play consultancies. Meanwhile, cloud-native platforms offer subscription access, pressuring hourly billing models.

Competitive success increasingly hinges on AI, data analytics, and interoperability with sponsor ecosystems. Firms embracing outcome-based pricing—tying fees to approval timelines or first-cycle success—gain traction. The competitive frontier now pivots on intellectual-property protection, data-security certifications, and the ability to deliver seamless hybrid on-shore/off-shore service models. As sponsors expect integrated solutions covering strategy, submission, and post-market surveillance, providers unable to combine domain expertise with technology at scale risk marginalization.

Regulatory Reporting And Compliance Industry Leaders

Genpact Ltd

IQVIA Holdings Inc

Certara, L.P.

Pharmaceutical Product Development, LLC (PPD)

Charles River Laboratories International, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: IQVIA committed USD 150 million to enhance its regulatory-intelligence platform, embedding machine-learning models that forecast approval timelines

- October 2024: Syneos Health closed the USD 85 million purchase of Endpoint Clinical, adding rare-disease regulatory expertise to its portfolio

Global Regulatory Reporting And Compliance Market Report Scope

As per the scope of the report, regulatory reporting and compliance refers to the processes and procedures organizations follow to adhere to legal and regulatory requirements set by government agencies and industry standards. It involves accurately documenting, reporting, and maintaining records of activities, safety, and quality measures to ensure transparency, accountability, and adherence to regulatory guidelines. Compliance helps ensure products and services meet safety, efficacy, and quality standards.

The regulatory reporting and compliance market are segmented by service type (regulatory consulting, product registration & clinical trial applications, legal representation, regulatory writing & publishing, and other regulatory services), service provider type (in-house and outsourcing), end user (pharmaceutical companies, medical device companies, and biotechnology companies), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America).

| Regulatory Consulting |

| Product Registration & Clinical Trial Applications |

| Legal Representation |

| Regulatory Writing & Publishing |

| Other Regulatory Services |

| In-House |

| Outsourcing |

| Pharmaceutical Companies |

| Medical Device Companies |

| Biotechnology Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Brazil | |

| Argentina | |

| Rest of South America |

| By Service Type | Regulatory Consulting | |

| Product Registration & Clinical Trial Applications | ||

| Legal Representation | ||

| Regulatory Writing & Publishing | ||

| Other Regulatory Services | ||

| By Service Provider Type | In-House | |

| Outsourcing | ||

| By End User | Pharmaceutical Companies | |

| Medical Device Companies | ||

| Biotechnology Companies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Brazil | ||

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the regulatory reporting and compliance market?

The regulatory reporting and compliance market size is USD 4.70 billion in 2026.

How fast is the market expected to grow?

The market is forecast to expand at a 9.03% CAGR, reaching USD 7.24 billion by 2031.

Which region leads in spending on regulatory compliance services?

North America holds the largest share at 41.10% as of 2025.

Which service type is growing the quickest?

Regulatory writing and publishing services are expanding at an 11.10% CAGR through 2031.

Why are biotechnology firms key to future growth?

Biotech sponsors face complex, accelerated approval pathways, driving a 12.10% CAGR demand for premium compliance support.

How does AI affect regulatory consulting?

AI-enabled intelligence platforms shorten dossier cycles, improve first-cycle approval odds, and differentiate service providers.

Page last updated on: