Refrigerator Compressor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.31 Billion |

| Market Size (2031) | USD 29.05 Billion |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

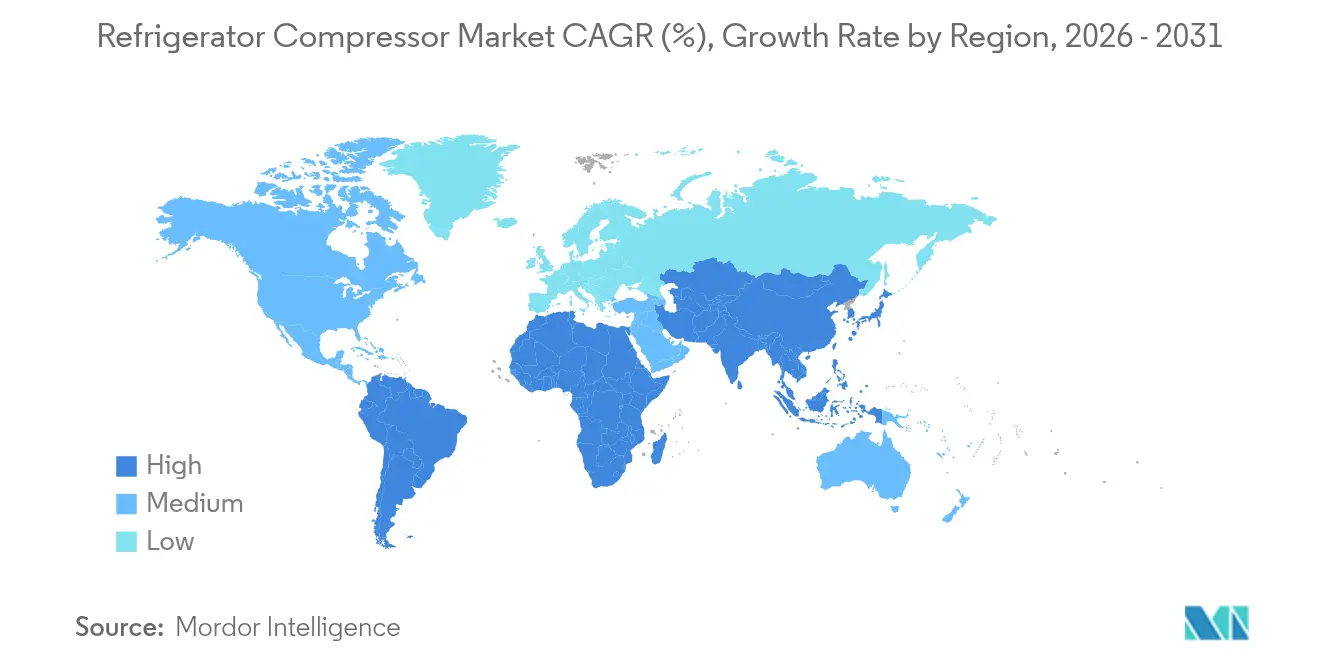

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

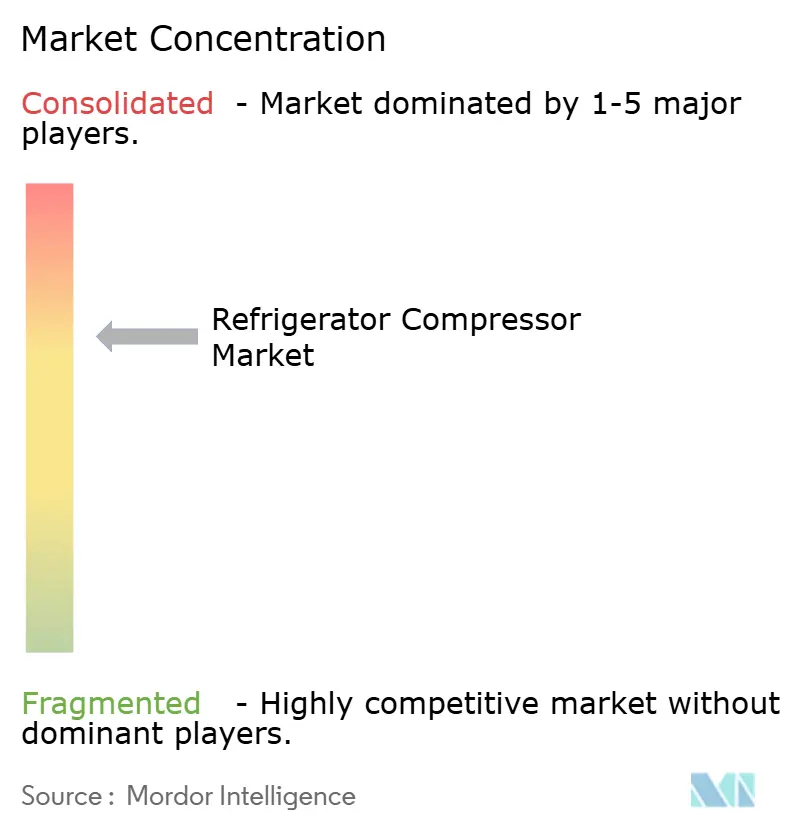

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Refrigerator Compressor Market Analysis by Mordor Intelligence

The Refrigerator Compressor Market size was valued at USD 22.31 billion in 2025 and estimated to grow from USD 23.31 billion in 2026 to reach USD 29.05 billion by 2031, at a CAGR of 4.50% during the forecast period (2026-2031).

The outlook is underpinned by regulatory mandates that favor high-efficiency technologies, the global expansion of the cold chain tied to e-commerce logistics, and aggressive capacity additions in the Asia-Pacific region. Variable-speed inverter compressors, which trim energy consumption by nearly 30%, are scaling quickly, while natural-refrigerant designs are gaining traction as high-GWP fluids are phased out. Large players are reshoring plants to North America and Europe to hedge supply-chain risk, yet copper and electrical-steel price spikes continue to squeeze bills of material. Mergers, such as Samsung’s USD 1.7 billion purchase of FläktGroup, confirm that strategic consolidation remains a key growth lever.[1]Samsung Newsroom, “Samsung to Acquire FläktGroup for USD 1.7 Billion,” samsung.com

Key Report Takeaways

- By product type, reciprocating compressors led the refrigerator compressor market with 68.90% of the market share in 2025; centrifugal designs are forecast to post the fastest growth of 10.3% CAGR through 2031.

- By refrigerant type, HFCs commanded 77.20% of the refrigerator compressor market size in 2025, while HFOs & blends are projected to expand at a 14.9% CAGR over the same period.

- By cooling capacity, the 1-15 kW band accounted for 48.30% of the refrigerator compressor market size in 2025 and is predicted to grow at a 5.2% CAGR to 2031.

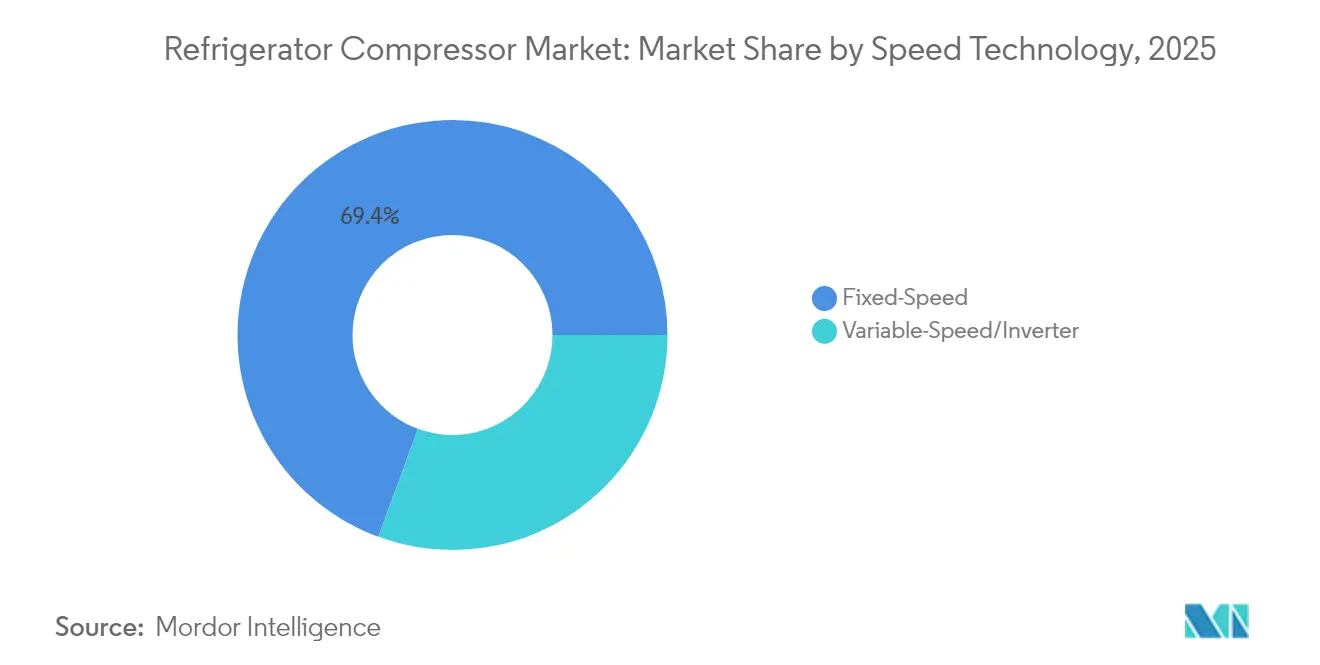

- By speed technology, fixed-speed units held 69.40% share of the refrigerator compressor market size in 2025, whereas inverter models are poised for a 6.85% CAGR through 2031.

- By application, residential refrigeration captured a 36.60% share in 2025; the healthcare cold-chain is set to log the quickest 6.1% CAGR up to 2031.

- By geography, the Asia-Pacific region dominated with a 42.80% share in 2025 and is also the fastest-growing region, with a 8.7% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Refrigerator Compressor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming e-commerce-driven cold-chain build-out | 1.0% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Stringent food-safety regulations in emerging markets | 0.7% | APAC emerging markets, Latin America, MEA | Short term (≤ 2 years) |

| Shift toward energy-efficient variable-speed (inverter) compressors | 0.6% | North America & EU regulatory push, APAC manufacturing scale | Long term (≥ 4 years) |

| Rapid electrification of last-mile refrigerated vans (plug-in hybrid cabinets) | 0.5% | Urban centers globally, EU and North America leading | Medium term (2-4 years) |

| Mandated global HFC phase-down accelerating low-GWP retrofit demand | 0.4% | EU and North America immediate, APAC gradual adoption | Short term (≤ 2 years) |

| AI-enabled predictive-maintenance services lowering total cost of ownership | 0.3% | Developed markets initially, expanding to emerging economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Cold-Chain Infrastructure Expansion Drives Compressor Demand

Explosive online grocery adoption is driving warehouse operators to build or retrofit cold storage at an unprecedented rate. Global cold storage revenues are on course to surpass USD 32 billion by 2030, registering a 13.6% CAGR.[2]Refrigerated & Frozen Foods, “Global Cold Storage Market Outlook,” rffmag.com Automation-ready micro-fulfillment hubs inside cities require compact, high-efficiency compressors that fit tight footprints. In the United States, cold storage spending is projected to increase from USD 43.2 billion in 2023 to USD 118.8 billion by 2031. Aging North-American facilities—many 20-30 years old—now face accelerated replacement cycles, giving variable-speed and low-GWP platforms a clear advantage. Speculative development is spreading to tier-2 Chinese cities, where startups are testing autonomous reefer vehicles equipped with ruggedized compressors that function at −40 °C ambient conditions. Together, these factors reinforce a robust long-run demand stream for the refrigerator compressor market.

Stringent Food-Safety Regulations Mandate Advanced Refrigeration Systems

Emerging-market governments are tightening temperature-control rules to curb food waste and safeguard exports. China’s trade-in subsidies revived refrigerator sales volume by 5.4% and value by 8.5% in 2024, illustrating how policy can spur rapid equipment turnover. New mandates often require onboard data logging, redundant cooling loops, and real-time alarms—all of which favor digitally controlled compressor platforms over legacy mechanical units. Comparable legislation in Brazil and Indonesia is widening the addressable base for premium products. Beyond storage, transport regulations now specify narrower temperature bands for seafood and pharmaceuticals, compelling fleet owners to upgrade to multi-zone inverter systems that maintain a precision of ±1 °C during long hauls.

Variable-Speed Compressor Technology Redefines Energy-Efficiency Standards

Variable-speed drives adjust capacity in real-time, reducing electricity use by nearly 30% compared to fixed-speed models.[3]ACHR News, “Variable-Speed Compressors Cut Energy Use by 30%,” achrnews.com The U.S. Department of Energy’s 2025 test procedure introduces SCORE and SHORE metrics that reward part-load performance.[4]U.S. Department of Energy, “Final Rule on CAC/HP Test Procedure 2025,” energy.gov Mitsubishi Electric is investing USD 143.5 million to build a Kentucky plant capable of producing 1 million twin-rotary variable-capacity compressors annually by 2027. Daikin and Copeland are jointly localizing inverter swing-rotary technology for U.S. residences, with production slated for mid-2025. Wider adoption hinges on technician training and affordable electronics; yet, cost curves continue to fall as APAC factories scale up their output.

Last-Mile Electrification Transforms Transportation Refrigeration

Cities are curbing diesel delivery vans, thereby accelerating demand for battery-electric refrigeration units. Hanon Systems opened a 900,000-unit electric-compressor line in Ontario in 2024 to serve North American vehicle makers. Electric architectures need lightweight compressors that draw minimal wattage without compromising pull-down speed. Plug-in hybrid cabinets, which switch to grid power during warehouse dwell time, are now logged as best practices in Europe. Component suppliers that master auto-grade quality, NVH mitigation, and CAN bus diagnostics are poised to capture a premium margin niche within the refrigerator compressor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost and financing gaps in developing economies | -0.7% | APAC emerging markets, MEA, Latin America | Medium term (2-4 years) |

| Volatile copper & electrical-steel prices inflating BoM costs | -0.5% | Global manufacturing, particularly China and APAC | Short term (≤ 2 years) |

| Shortage of technicians certified for flammable natural refrigerants | -0.3% | EU and North America transition regions | Medium term (2-4 years) |

| Cyber-security risks in IoT-connected compressor fleets | -0.2% | Developed markets with high connectivity adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital Cost Barriers Constrain Market Penetration in Emerging Economies

Variable-speed systems cost 40% more than fixed-speed units, stretching budgets in India, where domestic assembly meets only 6 million of the 15 million units demanded, leaving a 60-70% reliance on imports. Mitsubishi’s Kentucky plant price tag amounts to USD 143 per annual unit of capacity, underscoring the significant upfront investment required to localize production. Currency swings amplify the burden because most compressor components are dollar-denominated while local revenues are in a volatile domestic tender. Although India’s Production-Linked Incentive scheme offers partial relief, small firms still struggle to secure long-term financing.

Raw Material Price Volatility Pressures Manufacturing Economics

Copper reached record levels in July 2025 after a 50% U.S. import tariff announcement, highlighting supply risks for windings and tubing. The United States sources half of its copper abroad and cannot ramp up mining operations fast enough to offset curtailed imports. Climate-driven droughts threaten Chile's output, exacerbating the country's tightness. The International Energy Agency notes that clean-tech demand will triple metal needs by 2040, urging the adoption of circular-economy design. Compressor OEMs are redesigning motor stacks to save grams of copper, yet such engineering cycles lag commodity spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reciprocating Strength Meets Rising Centrifugal Demand

Reciprocating units accounted for 68.90% of the refrigerator compressor market size in 2025, due to their low cost and proven reliability in residential and light-commercial refrigerators. Continual line automation in China sustains its cost edge even as inverter controls lift seasonal efficiency. Centrifugal designs, although holding a modest share, are gaining at a 10.3% CAGR, thanks to data-center cooling, district-energy plants, and large food-processing sites that require more than 3,000 TR capacity. Variable-speed drives unlock smoother turndown ranges, making centrifugal machines attractive for partial-load operation. Scroll and rotary-screw models serve supermarket racks and ice-cream factories, while vane and linear technologies remain niche, reserved for low-noise or portable applications. Consolidation is evident: Atlas Copco’s acquisition of Kyungwon introduces oil-free screw technology, aligning with pharmaceutical purity standards. Integration of IoT sensors across all types indicates that mechanical layout is no longer the sole differentiator; lifecycle analytics is emerging as the new battleground within the refrigerator compressor market.

By Refrigerant Type: HFC Dominance Erodes Under Regulatory Pressure

HFC fluids still represented 77.20% of the refrigerator compressor market share in 2025, but their outlook is set to contract as quota cuts tighten. HFO blends are growing at the fastest rate, with a 14.9% CAGR, primarily in retrofit chiller projects where direct drop-in compatibility reduces service time. Hydrocarbons, such as R290, advance in plug-in retail cabinets, appreciated for their thermodynamic efficiency and minimal charge volumes. CO₂ trans-critical loops are climbing supermarket hilltops in Scandinavia and Japan, aided by ejector and parallel compression innovations that raise the coefficient of performance in hot climates. Panasonic’s 70-model portfolio launch in 2025 provides European OEMs with a ready supply of compressors factory-qualified for natural gas. Implementation hurdles include additional safety components—such as spark-proof relays and leak sensors—that increase the bill of materials, yet declining HFC quotas ensure a steady shift toward alternatives.

By Cooling Capacity: Mid-Range Sweet Spot Remains Unrivaled

The 1-15 kW bracket accounted for 48.30% of the refrigerator compressor market size in 2025 and is projected to grow at a 5.2% CAGR. Its versatility spans household fridge-freezers, beverage coolers, and small medical storage. Scale lets suppliers re-use stator tooling across dozens of models, slashing per-unit cost. Micro-compressors below 1 kW cater to portable coolers and e-grocery delivery boxes, but face volume volatility tied to discretionary spending. Above-15 kW behemoths power meat-packing plants and LNG boil-off recovery, yet grow more slowly because projects are lumpy and capital-heavy. Hanon’s Canadian plant, geared to EV thermal management, underscores how mid-range capacities will capture the pivot of transport refrigeration to electrification.

By Speed Technology: Inverter Uptake Outpaces Fixed-Speed Base

Fixed-speed machines retained a 69.40% share in 2025, but their volume edge belies a gradual substitution trend. Inverter units are forecast to rise ata 6.85% CAGR as policy ties incentives to seasonal efficiency and as smart-meter tariffs widen off-peak price spreads. Component costs continue to decline: IGBT modules are now 18% cheaper than in 2022, thanks to Chinese fab ramp-ups. Daikin-Copeland’s venture will localize swing-rotary inverters in Tennessee, shortening lead times for U.S. OEMs. Early-stage failure rates have declined following firmware-algorithm refinements, alleviating contractor concerns over complexity and paving the way for mainstream adoption across the refrigerator compressor market.

By Application: Residential Bedrock Supports Healthcare Upside

Residential refrigeration accounted for 36.60% of the 2025 demand, providing vendors with high-volume predictability. Still, the healthcare cold-chain is the fastest-growing sector at a 6.1% CAGR, as vaccine distribution centers and biologics plants proliferate worldwide. Commercial food retail continues to upgrade to embedded CO₂ racks that reduce leakage and lower energy bills, while industrial freezing remains essential for seafood and meat exports in Southeast Asia. Transportation refrigeration now spans road, rail, and marine segments, with each segment seeking lighter compressors to offset the mass of batteries or fuel penalties. Manufacturers are customizing firmware for these verticals, aiming to lock in service contracts that extend revenue beyond the initial sale.

Geography Analysis

Asia-Pacific controlled 42.80% of global shipments in 2025, powered by China’s full-stack supply chain and India’s widening demand gap. Chinese champion Midea accounts for 45% of the global home AC compressor output and 16% of refrigerators, with 41.9% of its revenue already generated offshore. India’s production shortfall leaves room for joint ventures and brownfield expansions encouraged by tax holidays. Japan and South Korea contribute high-end variable-speed IP; Samsung’s FläktGroup deal broadens its applied HVAC offering to serve hyperscale data centers, projected to grow at 18% annually.

North America is regaining strategic weight as firms hedge geopolitical and freight risks. Mitsubishi’s Kentucky retrofit is the first inverter compressor factory on U.S. soil, supported by USD 50 million in federal energy grants. LG added scroll-compressor lines in Mexico, leveraging USMCA rules to secure contracts for both the automotive and appliance sectors. Cold-chain construction is booming in the Sun Belt, mirroring the rapid influx of population and the increasing adoption of online grocery services.

Europe’s niche lies in stringent sustainability rules. Panasonic’s 70-model low-GWP rollout aligns with the 2027 quota cliff, ensuring local OEMs maintain continuity. EU manufacturers also lead in CO₂ ejector research, exporting their expertise to Middle East hotel chains seeking to decarbonize their chillers.

South America and MEA trail on value but show pockets of double-digit growth. Midea’s USD 122 million Brazilian fridge plant illustrates the race to secure local content advantages in Latin America’s largest white-goods market. Gulf-state datacenter builds, spurred by AI cloud demand, are opening high-capacity centrifugal opportunities that regional integrators cannot yet supply.

Competitive Landscape

Competitive intensity remains moderate, with the top five players accounting for roughly 68% of the revenue. Midea (GMCC-Welling) dominates the household segment, accounting for a 45% share of air-conditioning compressors and 16% of refrigerator units, generating USD 373.7 billion in revenue in 2023. Samsung’s USD 1.7 billion acquisition of FläktGroup positions it to capitalize on projected applied HVAC growth, which is expected to increase from USD 61 billion in 2024 to USD 99 billion in 2030, particularly in data-center cooling.

Technology differentiation pivots on efficiency, refrigerant flexibility, and digital services. Daikin-Copeland’s JV will blend Daikin inverter IP with Copeland distribution muscle, easing market entry barriers for swing-rotary designs in the United States. Atlas Copco’s Kyungwon deal enhances its oil-free screw offerings, which are vital for semiconductor fabs and pharmaceutical plants.

Manufacturers broaden revenue through predictive-maintenance platforms that sell analytics subscriptions. CAREL and SECO’s pending cloud toolkit underscores the shift toward service-led value capture. Meanwhile, commodity inflation is squeezing gross margins, pushing OEMs to insource stators or co-invest in copper recycling loops.

Refrigerator Compressor Industry Leaders

GMCC-Welling (Midea)

Nidec (Embraco)

Secop GmbH

Huayi Compressor (Highly)

Bitzer SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Samsung Electronics closed its USD 1.7 billion acquisition of FläktGroup to expand into the applied HVAC and data-center cooling markets, which are growing at an annual rate of 18%.

- June 2025: Panasonic launched 70 eco-friendly compressor models for Europe under iCORE (non-fluorinated) and iCOOL (inverter) banners.

- March 2025: Atlas Copco acquired Kyungwon Machinery Industry (USD 36 million 2024 revenue), adding oil-free screw technology and 126 employees.

- January 2025: Midea inaugurated a USD 122 million refrigerator plant in Pouso Alegre, Brazil, targeting the production of 1.3 million units annually.

Global Refrigerator Compressor Market Report Scope

Refrigeration compressors are an important part of every refrigeration system that employs a subcritical vapor-compression refrigeration cycle. They range in size from those utilized in refrigerated display cabinets in supermarkets and shops to those utilized in large industrial refrigeration systems in breweries.

The refrigerator compressor market is segmented by product type, application, and geography. By product type, the market is segmented by centrifugal, reciprocating, rotary screw, and others. By application, the market is segmented into residential, commercial, healthcare, industrial, and transportation. The report also covers the market size and forecasts for the refrigerator compressor market across the major regions. For each segment, the market size and forecasts have been done based on revenue (USD).

| Reciprocating |

| Scroll |

| Rotary Screw |

| Centrifugal |

| Others (Vane, Linear) |

| HFCs (R-134a, R-404A) |

| Natural: Hydrocarbons (R-290/600a) |

| Natural: CO₂ (R-744) |

| HFOs and Blends (A2L) |

| Up to 1 kW |

| 1 to 15 kW |

| Above 15 kW |

| Fixed-Speed |

| Variable-Speed/Inverter |

| Residential Refrigerators and Freezers |

| Commercial (Retail, Supermarkets, HoReCa) |

| Healthcare and Pharma Cold-Chain |

| Industrial Processing and Cold Storage |

| Transportation Refrigeration (Road, Marine, Rail) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Reciprocating | |

| Scroll | ||

| Rotary Screw | ||

| Centrifugal | ||

| Others (Vane, Linear) | ||

| By Refrigerant Type | HFCs (R-134a, R-404A) | |

| Natural: Hydrocarbons (R-290/600a) | ||

| Natural: CO₂ (R-744) | ||

| HFOs and Blends (A2L) | ||

| By Cooling Capacity | Up to 1 kW | |

| 1 to 15 kW | ||

| Above 15 kW | ||

| By Speed Technology | Fixed-Speed | |

| Variable-Speed/Inverter | ||

| By Application | Residential Refrigerators and Freezers | |

| Commercial (Retail, Supermarkets, HoReCa) | ||

| Healthcare and Pharma Cold-Chain | ||

| Industrial Processing and Cold Storage | ||

| Transportation Refrigeration (Road, Marine, Rail) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the refrigerator compressor market?

The refrigerator compressor market size reached USD 23.31 billion in 2026 and is projected to grow to USD 29.05 billion by 2031.

Which region leads the refrigerator compressor market?

Asia-Pacific held the largest 42.80% share in 2025 and is also the fastest-growing at 8.7% CAGR to 2031.

Why are variable-speed compressors gaining popularity?

Variable-speed technology adjusts capacity in real time, cutting energy consumption by about 30% and helping OEMs comply with stricter efficiency rules effective from 2025.

How is the HFC phase-down affecting compressor design?

Regulations such as the EU F-Gas quota cuts are accelerating the switch to natural refrigerants, pushing manufacturers to release R290, CO₂, and HFO-ready compressor lines.

What is driving demand in healthcare refrigeration?

Expansion of vaccine supply chains and biopharma logistics is lifting the healthcare segment, forecast to record the fastest 6.1% CAGR through 2031.

Page last updated on: