Booster Compressor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

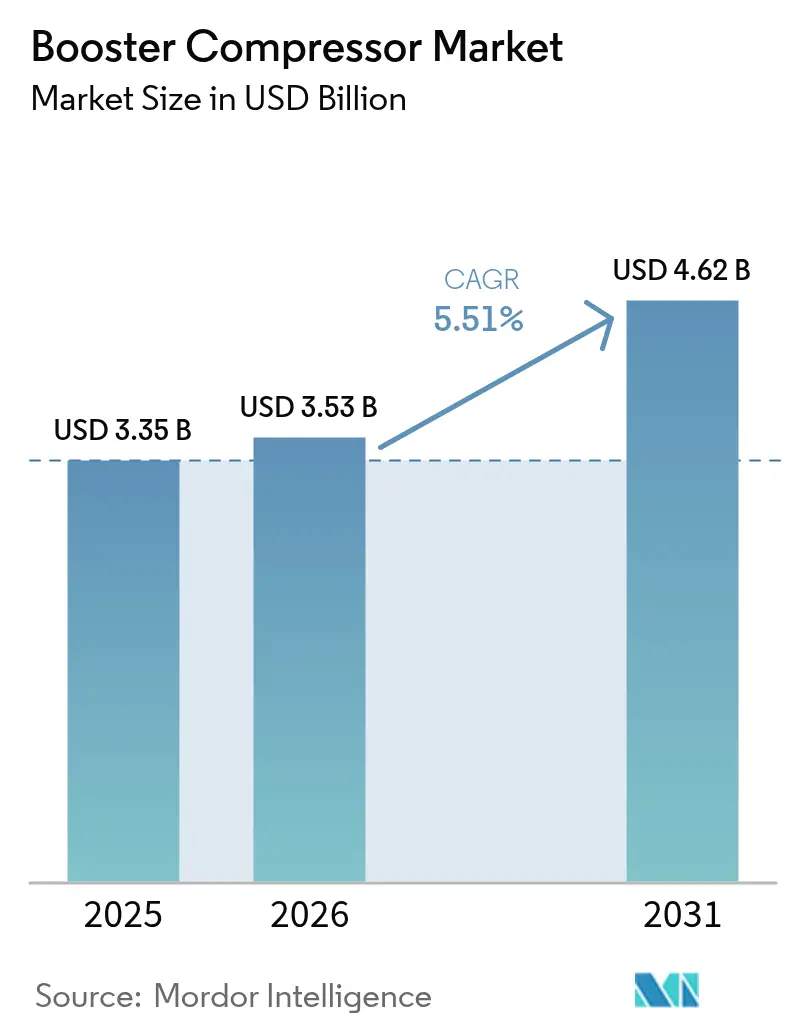

| Market Size (2026) | USD 3.53 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

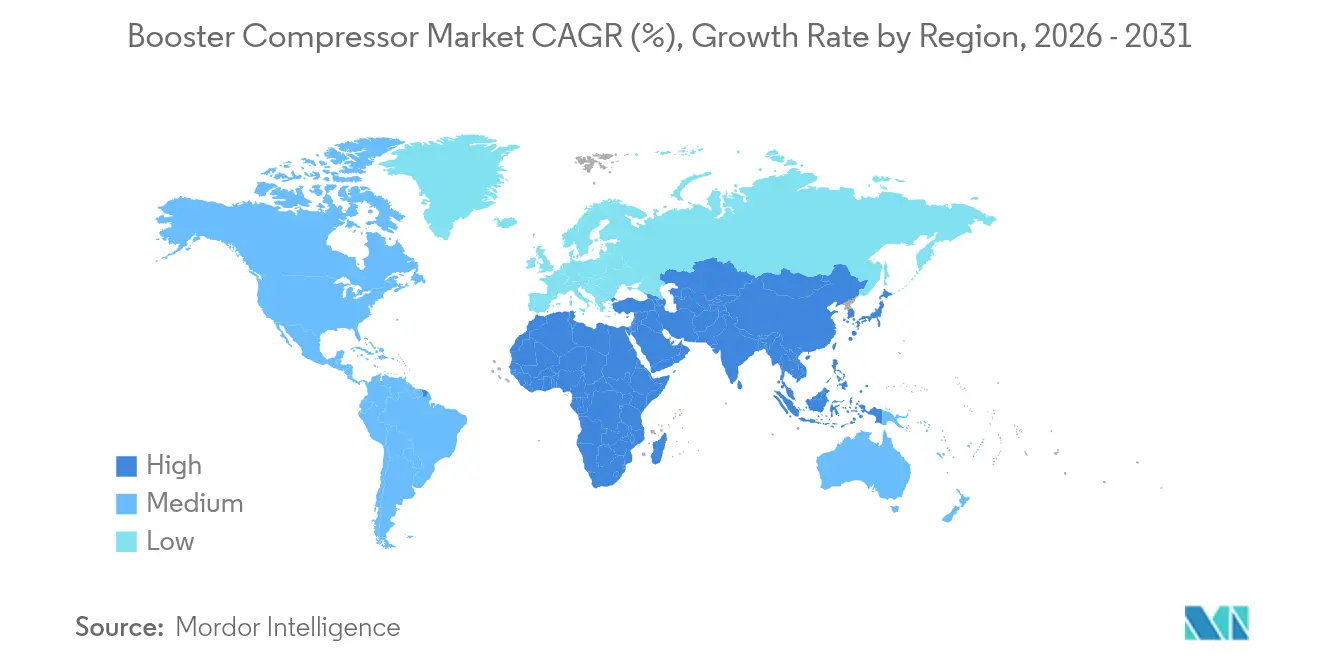

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

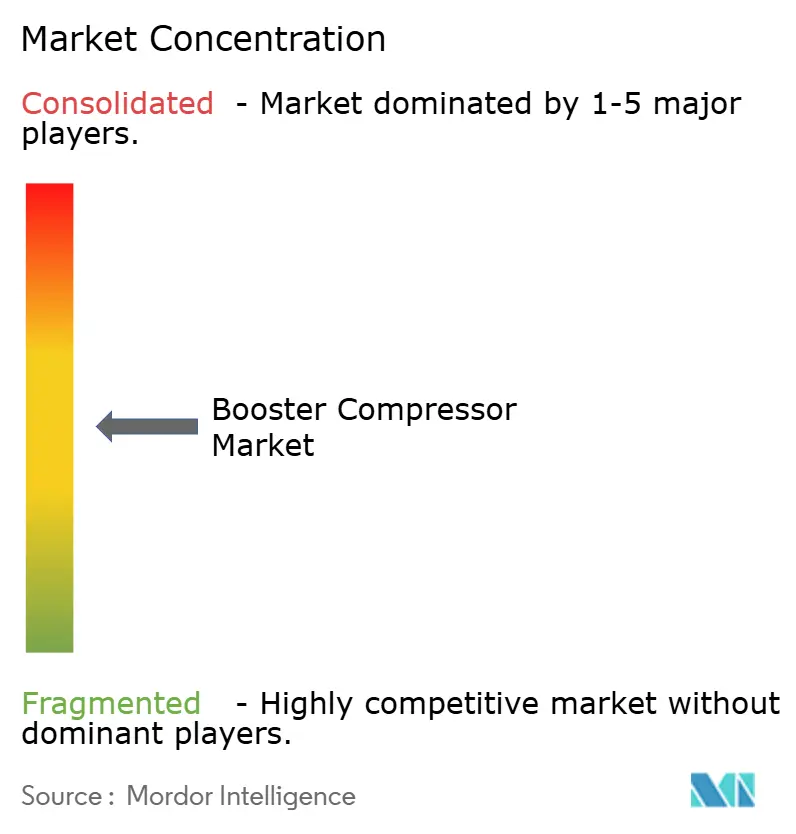

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Booster Compressor Market Analysis by Mordor Intelligence

The Booster Compressor Market size was valued at USD 3.35 billion in 2025 and estimated to grow from USD 3.53 billion in 2026 to reach USD 4.62 billion by 2031, at a CAGR of 5.51% during the forecast period (2026-2031).

The sustained expansion reflects steady capital spending on natural gas transmission upgrades, manufacturing automation, and early hydrogen fuel infrastructure. Strong policy support for energy-efficient equipment, wider adoption of variable-speed technologies, and rental platforms that lower entry barriers also underpin demand. Tightening federal standards in the United States, as well as parallel rules in Canada and the European Union, are accelerating replacement cycles toward designs with higher isentropic efficiency and lower emissions [1]U.S. Department of Energy, “Energy Conservation Program: Test Procedures for Compressors,” energy.gov. In parallel, the hydrogen economy’s push for 450-900 bar refueling systems is creating premium opportunities at the upper end of the pressure spectrum, while the Asia-Pacific region’s industrialization keeps volume demand high.

Key Report Takeaways

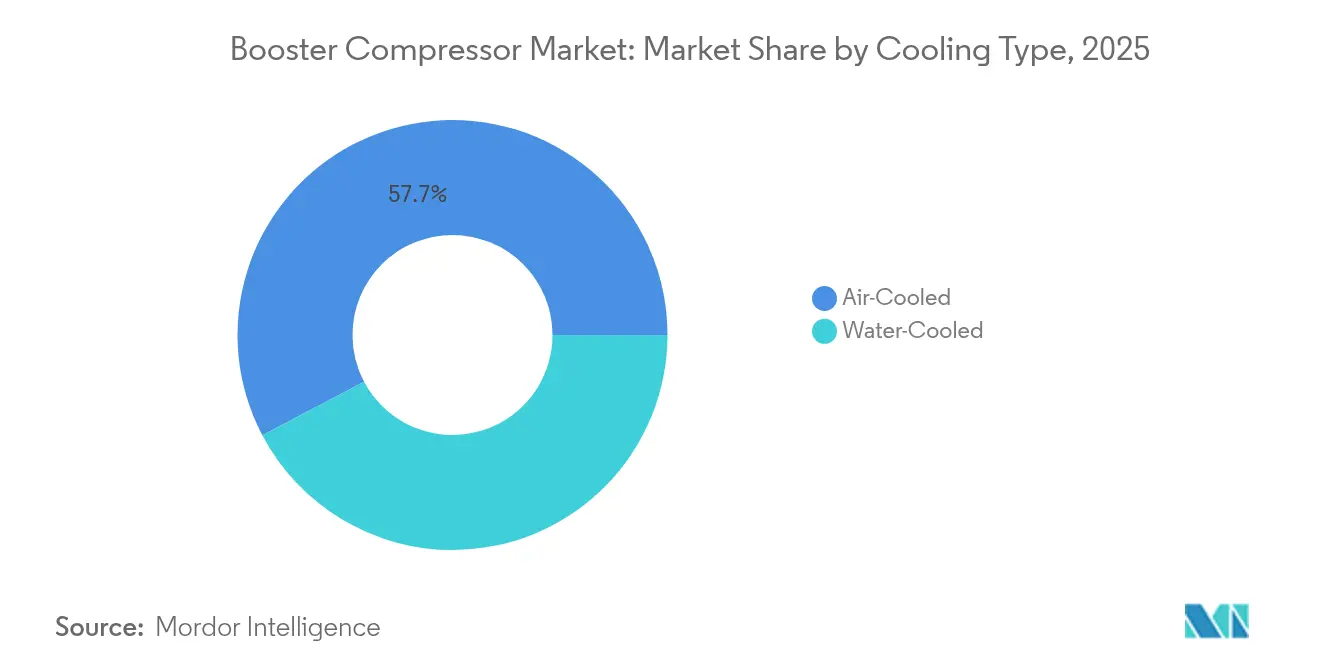

- By cooling type, air-cooled systems led with 57.72% revenue share in 2025; water-cooled designs are projected to expand at a 6.63% CAGR through 2031.

- By compression stage, single-stage units captured 50.35% of the booster compressor market share in 2025, whereas three-stage and above configurations are forecast to grow at a 7.08% CAGR.

- By lubrication type, oil-lubricated equipment accounted for 60.84% of the booster compressor market size in 2025; oil-free systems are projected to grow at a 6.86% CAGR through 2031.

- By pressure range, the 21–40 bar bracket commanded 43.55% share in 2025, while the 101–350 bar segment is advancing at 6.74% CAGR.

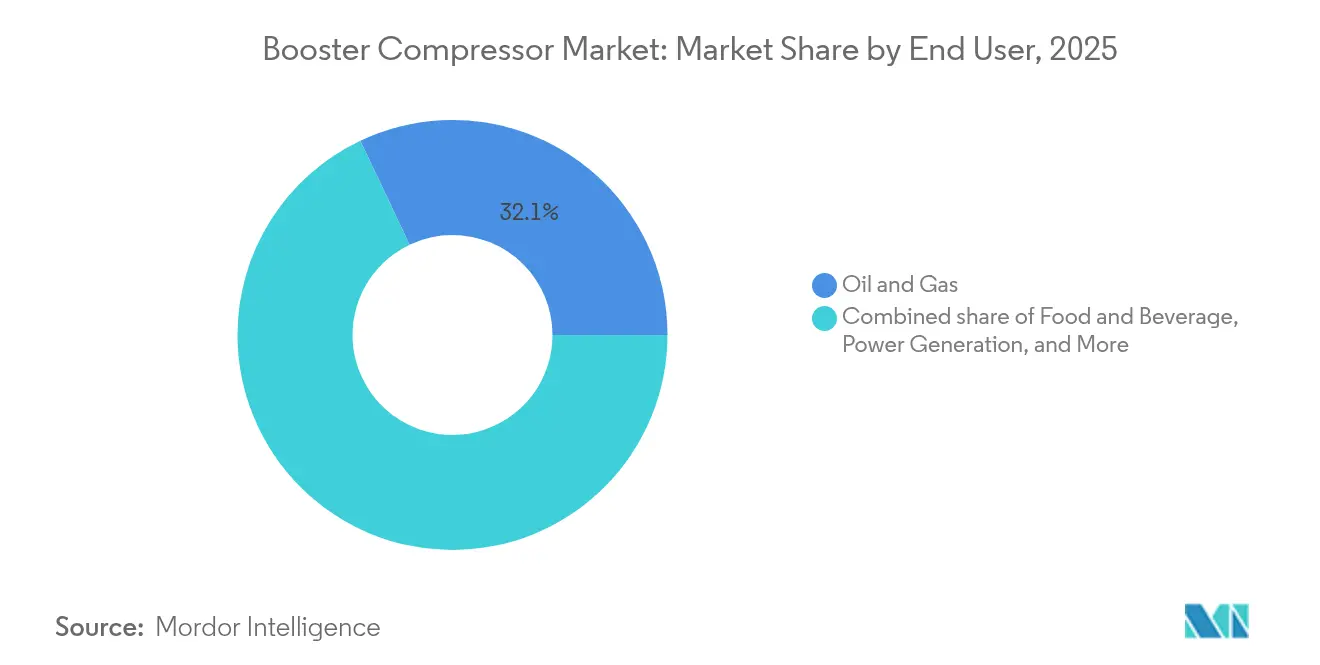

- By end user, the oil & gas sector accounted for a 32.05% share of the booster compressor market size in 2025, while the food & beverage sector is pacing the field at a 7.43% CAGR.

- By geography, the Asia-Pacific region dominated with a 39.45% revenue share in 2025 and is expected to continue posting the fastest regional growth at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Booster Compressor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising natural-gas pipeline pressure upgrade programs | 1.20% | North America & Europe, spill-over to APAC | Medium term (2-4 years) |

| Industrial demand for high-pressure compressed air | 1.00% | Global, concentrated in APAC manufacturing hubs | Long term (≥ 4 years) |

| Expansion of EOR & well-head compression in oil & gas | 0.80% | North America core, Middle East & North Africa | Short term (≤ 2 years) |

| Energy-efficiency mandates for compressed-air systems | 0.70% | North America & EU regulatory leadership | Medium term (2-4 years) |

| Hydrogen refueling stations requiring 450-bar boosters | 0.60% | Europe & APAC early adoption, North America following | Long term (≥ 4 years) |

| “Compressed-air-as-a-service” rental platforms | 0.40% | Global, with early gains in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Natural Gas Pipeline Pressure Upgrade Programs

Major transmission operators are modernizing aging lines to meet higher throughput targets and tighter emission limits. In 2024-2025, the Federal Energy Regulatory Commission cleared expansions, including the South System Expansion 4 project, which added 1.3 million Dth/d via new loops and 13 station upgrades.[2]Federal Energy Regulatory Commission, “Order Granting Certificate for South System Expansion 4,” ferc.gov Similar replacements by Consumers Energy in Michigan and Northwest Pipeline in Wyoming feature advanced boosters that reduce NOx emissions by 93% and methane emissions by 89%.[3][4]Consumers Energy, “Four Cities Metro Pipeline Project Overview,” consumersenergy.com Northwest Pipeline LLC, “Kemmerer Replacement Environmental Report,” nwpipeline.com Higher operating pressures require multi-stage reciprocating or integrally geared centrifugal designs that can maintain flow efficiency across varying load profiles. Vendors that can bundle equipment with turnkey installation and remote monitoring win orders because operators prefer single-point accountability for these capital-intensive projects.

Industrial Demand for High-Pressure Compressed Air

Precision manufacturing segments—such as laser cutting, PET bottle blowing, and semiconductor cleaning—now specify base pressures of 30-40 bar, rather than the legacy 7-13 bar range. The U.S. Department of Energy’s 2025 efficiency rule compels OEMs to raise minimum isentropic performance, pushing factories to retire legacy plants early. Asia-Pacific’s production-linked incentive schemes in India, along with the “Making Indonesia 4.0” roadmap, are increasing the installed base of automated lines that operate on oil-free, high-pressure air. Variable-speed drives improve part-load efficiency by up to 35%, making three-stage packages economical for mid-sized job shops. As a result, the booster compressor market is experiencing a structural shift toward equipment that balances pressure stability, energy consumption, and air purity.

Expansion of EOR & Well-Head Compression in Oil & Gas

Operators continue to extract incremental value from mature oil and gas reservoirs. Field trials show down-hole boosters can lift production by 32-41%, equivalent to 14-20 Bcf extra per well over five years. Projects such as the UAE’s Sajaa gas field have installed 12 surface boosters, totaling 18,600 HP, to counter declining formation pressure. Subsea compression is also scaling; Chevron’s USD 4 billion Jansz-Io project and Equinor’s Åsgard upgrades testify to the payoff in large gas provinces. These applications favor oil-free, three-stage and above units with magnetic bearings that reduce maintenance windows—a feature increasingly requested in tenders.

Energy-Efficiency Mandates for Compressed-Air Systems

Policy makers are turning the screw on industrial energy use. California’s Energy Commission enforces state-level compressor standards projected to save consumers USD 22 million per year. Natural Resources Canada adopts equivalent regulations for units manufactured after January 2025. OEMs are therefore redesigning packages with intercoolers, heat-recovery loops, and smart controllers that trim annual electricity bills by 20% in food-grade applications. In procurement, buyers now score bids on specific power (kW/m³/min) rather than headline horsepower, re-shaping competitive positioning within the booster compressor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance expenditure | -0.90% | Global, particularly affecting smaller operators | Long term (≥ 4 years) |

| Volatile upstream CAPEX cycles | -0.70% | North America shale regions, global offshore | Short term (≤ 2 years) |

| Shortage of certified high-pressure technicians | -0.50% | North America & Europe acute, APAC emerging | Medium term (2-4 years) |

| Price erosion from VSD centrifugal alternatives | -0.40% | Global industrial applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Expenditure

Multi-stage boosters rated above 350 bar can cost three times a standard plant air unit and require specialized alloys, precision components, and explosion-proof enclosures. Lifecycle studies indicate that service accounts for 15-25% of total ownership cost, a burden that deters smaller processors from upgrading. The global HVACR sector reports 80,000 open technician positions in North America, inflating labor rates and lengthening downtime. Manufacturers respond with ten-year service-interval designs that utilize magnetic bearings, eliminating the need for oil circuits, as seen in Baker Hughes’ Integrated Compressor Line. Even so, sticker shock slows adoption for cash-constrained buyers in emerging economies.

Volatile Upstream CAPEX Cycles

Oil-company budgets remain cyclical. U.S. independents trimmed spending to USD 61.7-65.4 billion in 2024 despite higher benchmark prices, reflecting shareholder pressure for capital discipline. Exploration’s share of global upstream capex slipped to 8%, curbing new gas-gathering compressor orders. While selective investments still flow to projects with rapid payback or ESG advantages, the booster compressor market experiences quarter-on-quarter order volatility. Suppliers therefore diversify into midstream and industrial segments to buffer revenue swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Type: Water-Cooled Systems Drive Efficiency Gains

Water-cooled boosters delivered the fastest revenue growth, although air-cooled models still dominated the booster compressor market size. Water-based intercooling dissipates heat more effectively across three-stage trains, trimming motor kW by up to 8% in 350-bar hydrogen service. Demand is strongest in food-grade and high-duty petrochemical plants where continuous operation justifies higher installation costs. OEMs tout heat-recovery kits that repurpose rejected thermal energy to power building hot-water systems, thereby improving overall facility efficiency. In contrast, air-cooled units remain the preferred choice for construction sites, containerized rigs, and regions facing water scarcity regulations. Their rugged design, minimal auxiliary hardware, and simpler maintenance keep them central to rental fleets that underpin the booster compressor market.

Second-generation water-cooled designs now feature stainless-steel tube bundles and fully welded plates to resist scaling in variable water quality. Operators running hydrogen stations report discharge-temperature reductions of 15°C and valve life extensions of 30% after switching from air to water cooling. While capital outlay is higher, plant managers recoup their investment through lower electricity bills and reduced unscheduled shutdowns. Consequently, water-cooled share is expected to chip steadily at the dominance of air-cooled systems over the forecast period.

By Compression Stage: Multi-Stage Configurations Gain Momentum

Single-stage boosters maintain a 50.35% share of the booster compressor market for pressures up to 100 bar due to their compact footprint and low part count. However, as hydrogen, laser-cutting, and PET lines migrate toward 350 bar requirements, three-stage and above packages log the fastest uptake. Multi-stage compression spreads pressure ratio across cylinders, cutting discharge temperature and valve stress, which in turn extends overhaul intervals. Energy audits in Asia-Pacific’s beverage plants show that three-stage machines save 12% in specific power compared to retrofitted two-stage sets.

Technological advances, such as active electronically controlled intercoolers and variable clearance pockets, further enhance multi-stage efficiency. High-pressure OEMs integrate magnetic-bearing crankcases that enable oil-free operation at 1,500 rpm, while maintaining vibration levels below API 618 thresholds. Engineering, procurement, and construction firms favor such integrated solutions because they simplify compliance with specifications in turnkey hydrogen stations. In parallel, two-stage units occupy a mid-range niche for users upgrading from plant air to 40-100 bar service yet lacking the budget or need for full three-stage performance.

By Lubrication Type: Oil-Free Technology Addresses Contamination Concerns

Heightened scrutiny of food-grade safety and pharmaceutical purity is steering purchases toward Class 0 certified oil-free boosters. These designs employ high-temperature non-stick coatings, labyrinth seals, and, in some cases, water-injected compression to remove hydrocarbon risk. The extra investment—often 20-30% over oil-lubricated peers—is justified by avoiding product recalls and simplifying ISO 8573-1 compliance audits. Electronics fabs likewise adopt oil-free systems to prevent downstream contamination on wafer lines. As a result, the oil-free booster compressor industry is expected to see a CAGR outpacing the overall market through 2031.

Oil-lubricated boosters continue to dominate high-horsepower, EOR duty because the lubricant film dampens piston slap and facilitates heat dissipation in sour-gas service. Contemporary filtration systems achieve 0.01-micron particle removal, making them suitable for many industrial applications where absolute oil-free air is not critical. Aftermarket vendors market synthetic PAO oils that extend oil-change intervals to 8,000 hours, thereby lowering downtime. Therefore, while oil-free units grow the fastest, the absolute installed base of oil-lubricated machines remains large, especially in the heavy industry sector, supporting a healthy spare parts and service economy within the booster compressor market.

By Pressure Range: High-Pressure Applications Accelerate Growth

Systems rated 101-350 bar are the breakout segment because they enable premium processes such as high-definition laser cutting, PET preform blowing, and pressure testing of carbon-fiber pressure vessels. The booster compressor market size for this band recorded a 6.74% CAGR, driven by the expansion of fleets of laser cutters in metal fabrication hubs across China, Vietnam, and Mexico. OEM field data show a 100-bar laser-assist gas can cut stainless steel 20% faster, offsetting higher utility costs. Meanwhile, base-load plant air in the 21-40 bar range continues to anchor volume shipments to general manufacturing and mining.

Above 350 bar boosters, though niche, command the highest unit prices. Hydrogen hubs in Germany and South Korea specify a discharge pressure of 700-900 bar for heavy-duty truck dispensing, generating premium margins for diaphragm or compound piston designs. Exploratory CCS projects also require CO₂ compression above 200 bar for pipeline injection. As governments roll out net-zero roadmaps, vendors with proven ultra-high-pressure references are poised to capture a disproportionate share of the profit.

By End User: Food & Beverage Sector Leads Growth

Food & beverage processors are automating to boost throughput and comply with Hazard Analysis and Critical Control Point protocols, creating upsized demand for clean, dry, high-pressure air. Class 0 oil-free boosters now power blow-molding, mixing, and packaging lines that run 24/7. Global bottlers report energy savings of 12% after switching to variable-speed, three-stage units paired with heat recovery for pasteurization water. Although oil & gas still account for 32.05% of current revenue, its growth track is slower due to cautious upstream capital expenditures. Chemical and petrochemical sites maintain steady replacement demand, while metals, automotive, and electronics plants broaden the customer base in the Asia-Pacific.

Global quick-service restaurant chains are pressuring suppliers to certify the quality of compressed air across their entire cold-chain network. That requirement trickles down the value chain to packaging converters and logistics firms, further enlarging the addressable pool for oil-free boosters. Net result: the food & beverage segment is the clear growth engine within the booster compressor market through 2031.

Geography Analysis

Asia-Pacific remains the cornerstone of booster compressor demand. China, India, and ASEAN account for nearly 39.45% of 2025 sales, a share expected to edge up as new electronics fabs and vehicle plants break ground under national manufacturing roadmaps. Although China’s export share in low-value goods slipped, its higher value-added output still uses more compressed air per unit of GDP. India’s incentive scheme channels tax benefits to producers of mobile phones, solar modules, and specialty chemicals, each of which requires oil-free, high-pressure air systems. Southeast Asia’s greenfield plants often bypass legacy two-stage machines and order three-stage packages with digital controllers from the outset, accelerating the diffusion of technology.

North America ranks second, thanks to upgrades in shale gas infrastructure. The U.S. Department of Energy’s new compressor standards, effective January 2025, are prompting early replacements, while FERC-approved pipeline extensions require modern boosters equipped with methane leak detection. Modular hydrogen stations in California and Texas add a small but fast-growing volume. Europe shows steady replacement demand, particularly in Germany, France, and the Nordics, where automotive, food, and green hydrogen projects converge. The EU policy, which requires public hydrogen stations every 200 km along core corridors by 2030 under the Alternative Fuels Infrastructure Regulation, directly lifts ultra-high-pressure orders.

South America and the Middle East & Africa form the long-term frontier. Brazil’s pre-salt developments and Saudi Arabia’s push into non-oil industries provide anchor projects; however, political and logistical risks temper near-term volumes. Nonetheless, vendors focused on service quality and financing packages can win outsized shares as these regions diversify their industrial bases.

Mordor Intelligence provides coverage of the booster compressor market across other key regional markets, including Middle East and Africa and Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The booster compressor market is moderately concentrated, with the top five vendors controlling a combined 55-60% of global revenue. Atlas Copco, Ingersoll Rand, and Baker Hughes rank at the front, and all three continued bolt-on acquisitions to deepen product portfolios. Atlas Copco’s purchase of Kyungwon Machinery adds local Korean manufacturing and 126 staff, strengthening service proximity in Asia-Pacific. Honeywell’s USD 2.16 billion deal for Sundyne broadens reach into integrally geared packages for clean-fuel complexes. These moves illustrate a pivot toward higher-pressure, higher-value machines that align with hydrogen and carbon-capture megatrends.

Technology boundaries are blurring. Variable-speed centrifugal systems now overlap reciprocating designs up to 150 bar, forcing piston OEMs to innovate oil-free cylinders and smart unloaders. Digital twins embedded in control software predict bearing wear and optimize valve timing, trimming energy use by 5-7% in refinery service. Smaller specialists—Burckhardt Compression, Howden, and Ariel—leverage deep engineering competence in ultra-high-pressure or process-gas niches to defend margins. Meanwhile, distributors such as Hitachi Global Air Power’s newly acquired dealers in Texas integrate parts, rental, and condition-monitoring services to secure annuity revenue.

White-space opportunities arise in service-based models. Customers increasingly request guaranteed compressed-air supply rather than equipment ownership, leading major players to scale “air-as-a-service” contracts with IoT dashboards. Rental fleets also become a pathway for rapid adoption of energy-efficient units because pay-back risk shifts to the provider. The net result is intensifying competition not only on hardware capabilities but on financing, digital services, and sustainability credentials.

Booster Compressor Industry Leaders

Ingersoll-Rand plc

Atlas Copco AB

Baker Hughes Company

Siemens Energy AG

Gardner Denver Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Honeywell completed acquisition of Sundyne for USD 2.16 billion, bolstering its integrally geared compressor portfolio for refining and clean fuels markets.

- March 2025: Atlas Copco agreed to acquire Korea-based Kyungwon Machinery for SEK 465 million, extending regional manufacturing and medical-gas expertise.

- February 2025: FERC issued an environmental assessment for Florida Gas Transmission’s South Central Louisiana project, including new 4,500 HP booster units to add 75,000 MMBtu/d capacity.

- January 2025: The U.S. DOE implemented revised compressor test procedures; compliance becomes mandatory on Jul 16 2025.

Global Booster Compressor Market Report Scope

The booster compressor market report includes:

| Air-Cooled |

| Water-Cooled |

| Single-Stage |

| Two-Stage |

| Three-Stage and Above |

| Oil-Lubricated |

| Oil-Free |

| 21 to 40 bar |

| 41 to 100 bar |

| 101 to 350 bar |

| Above 350 bar |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Power Generation |

| Manufacturing |

| Food and Beverage |

| Other Process Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Cooling Type | Air-Cooled | |

| Water-Cooled | ||

| By Compression Stage | Single-Stage | |

| Two-Stage | ||

| Three-Stage and Above | ||

| By Lubrication Type | Oil-Lubricated | |

| Oil-Free | ||

| By Pressure Range | 21 to 40 bar | |

| 41 to 100 bar | ||

| 101 to 350 bar | ||

| Above 350 bar | ||

| By End User | Oil and Gas | |

| Chemicals and Petrochemicals | ||

| Power Generation | ||

| Manufacturing | ||

| Food and Beverage | ||

| Other Process Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the booster compressor market?

The booster compressor market size stands at USD 3.53 billion in 2026 and is projected to reach USD 4.62 billion by 2031.

Which region leads the booster compressor market?

Asia-Pacific holds 39.45% of global revenue and also records the fastest 6.78% CAGR through 2031.

Why are water-cooled booster compressors gaining traction?

Water-cooled designs dissipate heat more efficiently, enabling continuous 350-bar duty while lowering specific power, making them attractive for hydrogen stations and high-duty food plants.

How will DOE efficiency rules affect the market?

Mandatory test procedures effective July 2025 push buyers toward higher-isentropic efficiency models, stimulating replacement demand for compliant boosters.

Which end-use sector is expanding the fastest?

Food & beverage applications grow at a 7.43% CAGR as factories automate and adopt Class 0 oil-free air to meet stringent contamination standards.

What technology trend is reshaping competitive dynamics?

Variable-speed drive centrifugal packages now rival reciprocating boosters up to 150 bar, pressuring traditional suppliers to add smart control and hybrid designs.

Page last updated on: