Recreational Vehicle Financing Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

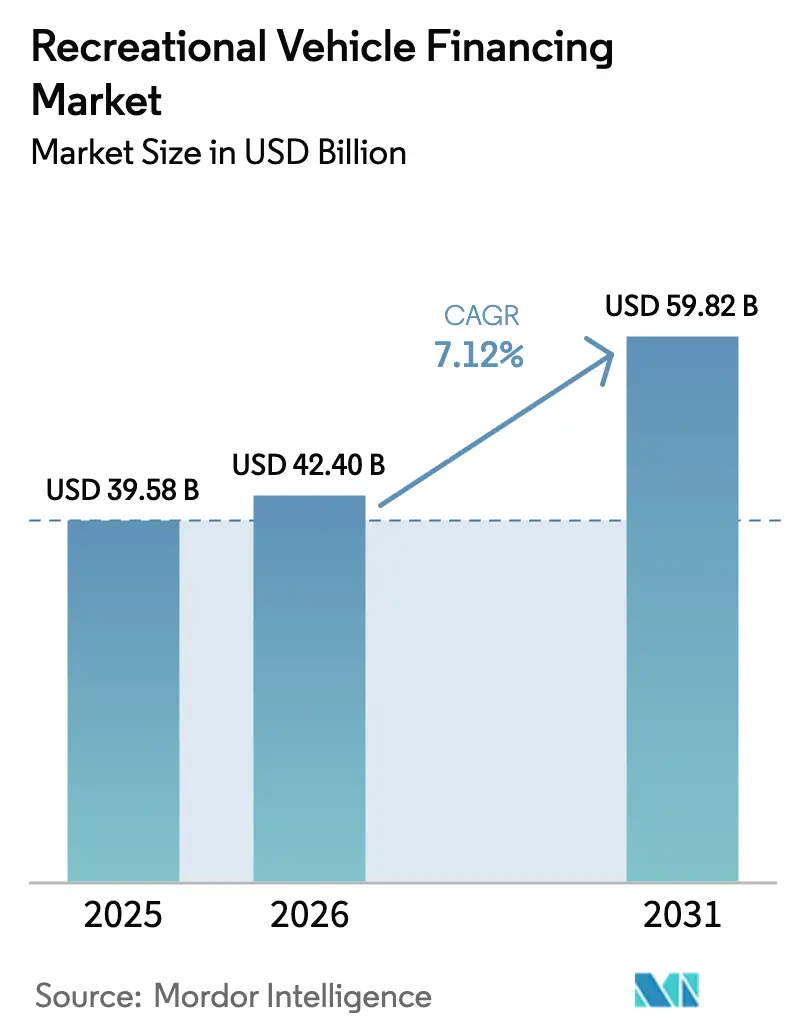

| Market Size (2026) | USD 42.4 Billion |

| Market Size (2031) | USD 59.82 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

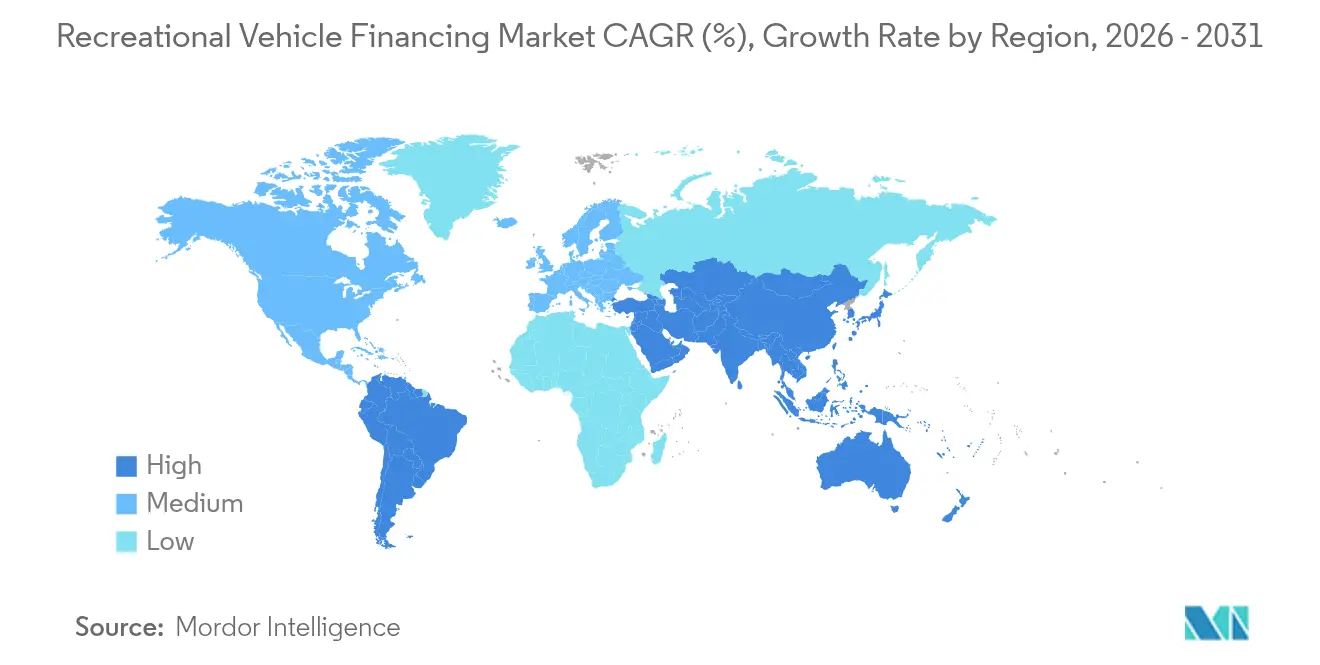

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recreational Vehicle Financing Market Analysis by Mordor Intelligence

The Recreational Vehicle (RV) Financing Market size is expected to grow from USD 39.58 billion in 2025 to USD 42.4 billion in 2026 and is forecast to reach USD 59.82 billion by 2031 at 7.12% CAGR over 2026-2031. The current expansion reflects the normalization of remote work, an accommodative lending climate, and sophisticated risk-based pricing models that broaden borrower eligibility. Within the RV financing market, purchase demand now blends leisure and full-time residency needs, especially among digital nomads who treat motorhomes as primary dwellings. Low interest rates and lengthening loan tenors, often extending to 240 months, have smoothed monthly payments, while telematics-enabled underwriting lowers loss severity and supports lender margins. Competitive pressures intensify as fintech entrants scale digital origination platforms, prompting traditional banks to refine customer experience and diversify product suites. Regionally, the United States anchors overall volumes, yet middle-income growth in Asia-Pacific signals a pivotal contribution to long-term demand. The RV financing market thus transitions from episodic holiday lending toward a resilient mobility-solutions ecosystem[1]“Survey of Lenders' Experiences,” RV Industry Association, rvia.org.

Key Report Takeaways

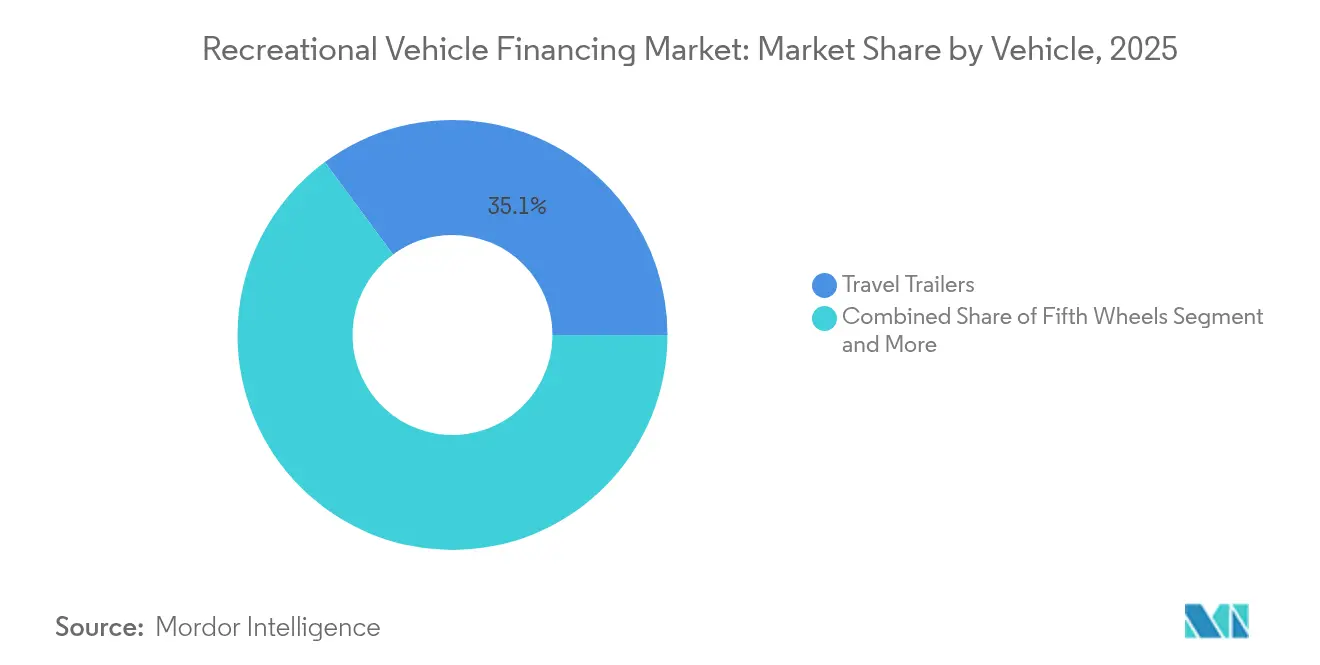

- By vehicle, travel trailers led with 35.12% of the Recreational Vehicle (RV) Financing Market share in 2025, whereas Class B motorhomes are forecast to grow at an 8.42% CAGR by 2031.

- By financing source, banks and credit unions held 47.05% of the Recreational Vehicle (RV) Financing Market share in 2025, while online fintech lenders are projected to advance at a 15.02% CAGR through 2031.

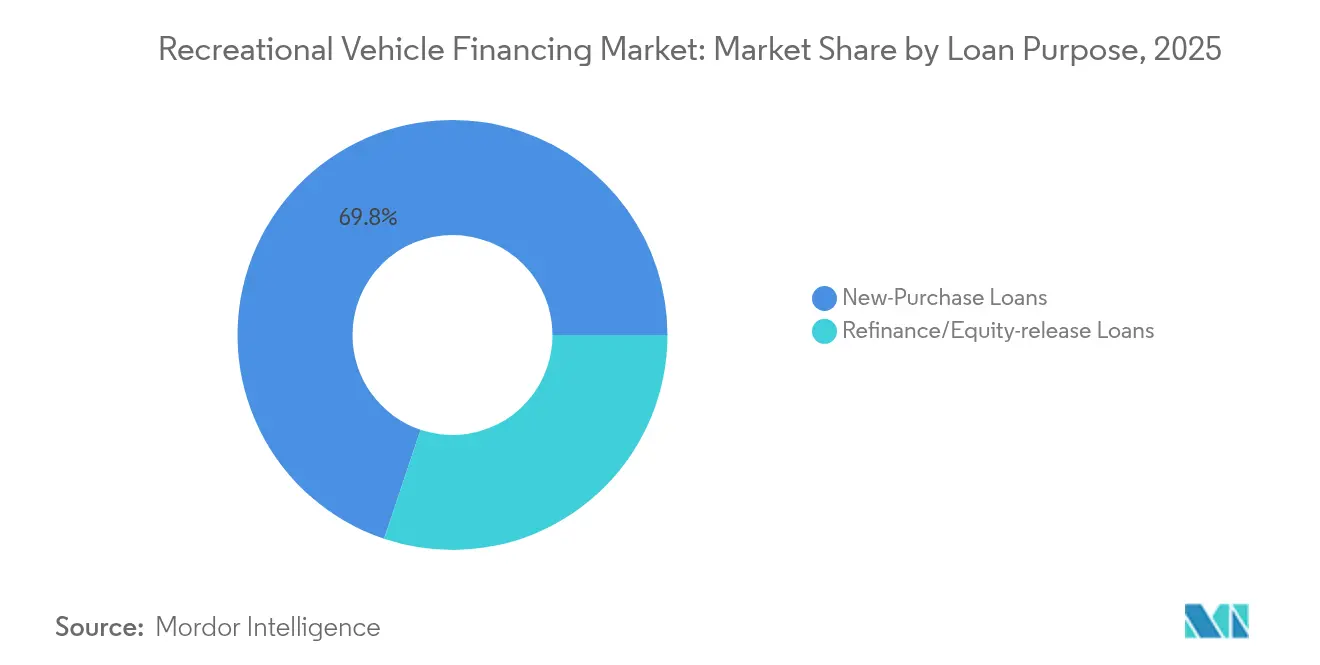

- By loan purpose, new-purchase contracts accounted for 69.84% of the RV financing market size in 2025; refinance and equity-release loans are expanding at 9.21% CAGR to 2031.

- By borrower credit tier, prime applicants captured 54.26% of the Recreational Vehicle (RV) Financing Market share in 2025, but sub-prime originations show the fastest 11.75% CAGR to 2031.

- By geography, North America commanded 60.88% of the Recreational Vehicle (RV) Financing Market share in 2025, whereas Asia-Pacific is set to deliver a 9.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Recreational Vehicle Financing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income and Favourable Rates | +2.1% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Remote-Work Adoption Enabling Mobile Lifestyles | +1.8% | North America & Europe core, spill-over to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Expansion Of Captive (OEM And Dealer) Financing | +1.4% | Global, with early gains in North America, Europe, Australia | Medium term (2-4 years) |

| Telematics-Driven Risk-Based Pricing | +1.2% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Peer-To-Peer RV Rental Platforms Lift Residual-Value | +0.9% | North America core, selective expansion to Europe & Asia-Pacific | Medium term (2-4 years) |

| ESG-Linked ABS Structures Reducing Lenders' Cost | +0.7% | Europe & North America, limited Asia-Pacific adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income and Favorable Interest-Rate Environment

Household wage gains and accommodative monetary policy have widened credit availability, driving a 23% year-over-year improvement in RV loan approvals among near-prime borrowers in 2025[2]“Truth in Lending (Regulation Z),” Consumer Financial Protection Bureau, federalregister.gov. Extended 240-month tenors are commonplace for high-ticket Class A units, cushioning monthly payments and attracting buyers migrating from high-cost housing markets. Lenders maintain portfolio health through variable-rate structures linked to telematics-derived usage scores, aligning risk and pricing dynamically. For many households, an RV now represents a cost-efficient hybrid of housing and transport, reinforcing structural growth in the RV financing market.

Surging Remote-Work Adoption Enabling Mobile Lifestyles

Remote-work normalization converts recreational vehicles into year-round residences, shifting underwriting toward models that recognize location-independent earnings and non-traditional address verification. The RV financing market benefits as borrowers with higher credit profiles seek flexible domiciles without fixed property taxes. Regulatory nuances around Truth-in-Lending dwelling status add compliance cost but also catalyze innovation in loan design. Demand concentrates among technology professionals utilizing RV mobility to arbitrage living costs while maintaining metropolitan salaries.

Expansion of Captive OEM and Dealer Financing Programs

Manufacturers and dealers progressively house financing inside the sales channel, offering promotional rates that undercut external lenders. Captive programs leverage rebate structures to accelerate new-model turnover and lift ancillary parts revenue. The approach secures brand loyalty while allowing OEMs to monetize financing margins. However, increased balance-sheet exposure obliges close liquidity surveillance during cyclical downturns. For borrowers, integrated financing shortens purchase cycles and supports the overall RV financing market trajectory.

Telematics-Driven Risk-Based Pricing Lowers Default Rates

Advanced telematics solutions supply granular data on mileage, maintenance adherence, and geolocation, enabling lenders to adjust rates in real time. Early adopters report up to 20% lower default incidence relative to traditional score-only underwriting, which in turn reduces capital charges and supports competitive APRs. Borrowers with sparse credit history but sound operating behavior benefit from better pricing, broadening participation in the RV financing market and reinforcing inclusive growth dynamics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront RV Costs and Rate Volatility | -1.9% | Global, with strongest impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Rapid Depreciation and High Insurance Premia | -1.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| TILA/"Dwelling" Classification Raising Compliance Costs | -1.1% | North America regulatory focus, limited global impact | Long term (≥ 4 years) |

| Climate-Driven Catastrophe Risk in Key Regions | -0.8% | Western North America, Southern Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront RV Costs and Rate Volatility

The average amount financed climbed to USD 67,216 in 2024, stretching affordability even with lengthened amortization schedules. Rate fluctuations elevate payment uncertainty on long-term notes, dampening entry-level demand despite product innovation. Lenders now package rate-cap options that transfer interest-rate risk, yet such hedges raise the effective cost of credit. The tension between affordability and yield will continue to temper near-term expansion in the RV financing market.

Rapid Depreciation and High Insurance Premia

RVs depreciate faster than passenger cars, creating negative equity exposure that complicates refinance exits. Insurance premiums have risen 25-30% annually in regions prone to climate-related events, forcing lenders to set conservative loan-to-value thresholds. Gap coverage and residual-value guarantees are emerging but add incremental cost, particularly for Class A motorhomes. Higher all-in ownership expenses pose a persistent brake on the RV financing market outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle: Towables Drive Market Volume

Travel trailers led the RV financing market size for vehicle types by capturing 35.12% of 2025 originations, owing to lower acquisition costs and compatibility with existing tow vehicles. The segment’s financing tenors seldom exceed 180 months, keeping portfolio duration manageable for lenders. Though smaller in volume, motorhomes are forecast to expand financing originations at an 8.42% CAGR to 2031 as remote workers favor compact mobile offices. Fifth-wheel units and toy haulers serve specialty niches, often bundling lifestyle accessories that increase loan amounts and necessitate higher down payments. Pop-up and folding trailers face consumer preference headwinds; however, seasonal renters occasionally convert to owners, creating episodic spikes in applications.

Motorhome sub-segments exhibit distinct borrower profiles. Class A buyers typically leverage higher loan limits and extended maturities reflective of luxury fit-outs. Class C units attract families, balancing amenity needs and budget constraints. Truck campers secure financing via shorter terms and elevated interest spreads, reflecting collateral portability and residual-value uncertainty. Variations in repayment tenure and collateral valuation illuminate why lenders segment risk within the broader RV financing market.

By Financing Source: Traditional Banks Face Digital Disruption

Banks and credit unions dominate the recreational vehicle financing market by commanding a 47.05% share of 2025 originations, benefitting from deposit-funded cost advantages and mature dealer ties. The RV financing market is nonetheless witnessing accelerated share capture by fintech lenders, whose 15.02% CAGR forecast rests on automated underwriting and instant decision portals. Dealer and OEM captives leverage promotional APRs to synchronize inventory clearance with financing uptake, particularly effective during model-year transitions. Government-backed programs remain marginal but provide critical liquidity in rural areas by treating certain RVs as manufactured housing. Peer-to-peer platforms, while nascent, signal a future avenue for risk-tiered investor participation in the RV financing industry.

The competitive re-ordering pressures incumbents to digitize origination pipelines, integrate e-signatures, and adopt alternative data scoring. Credit unions counter by bundling ancillary services, insurance, and membership perks to preserve loyalty. Ultimately, differentiated customer experience and funding cost arbitrage will dictate future share shifts across financing sources within the RV financing market.

By Loan Purpose: Refinancing Gains Momentum

New-purchase contracts represented 69.84% of the RV financing market share in 2025, reaffirming acquisition-centric borrower motivations. However, equity-release and refinance volumes are projected to climb 9.21% CAGR through 2031 as borrowers extract collateral value to consolidate debt or upgrade units. Rate volatility incentivizes seasoned owners to restructure terms when yield curves invert, sustaining secondary-market demand for seasoned RV paper. Equity-release loans often support non-recreational goals, home improvements, and education expenses, indicating the blurring of asset-specific and general-purpose financing within the RV financing market.

For lenders, refinance pipelines offer lower acquisition costs than new-buyer marketing and may exhibit stronger performance due to established payment history. Still, the rising share of cash-out refinances heightens loan-to-value ratios, requiring robust collateral valuation and insurance coverage to manage downside risk.

By Borrower Credit Tier: Prime Dominance with Sub-Prime Upside

Prime borrowers (FICO above 720) captured 54.26% of 2025 originations, reflecting the discretionary nature of RV purchases and the underwriting preference for low-risk profiles. Advances in AI-enabled scoring models permit deeper penetration of subprime tiers, which are now expanding at a 11.75% CAGR to 2031. Near-prime applicants mitigate pricing premiums via higher down payments or collateral add-ons such as extended warranties. Expanded credit-tier diversity broadens the RV financing market but demands calibrated risk-based pricing and robust asset-tracking tools.

Alternative data feeds machine-learning algorithms that challenge FICO's supremacy, including gig economy income stability and utility-payment histories. For lenders, balanced portfolio construction across credit tiers remains essential to optimize yield without compromising delinquency targets in the RV financing industry.

Geography Analysis

North America remains the principal region for the RV financing market, holding 60.88% of 2025 revenue. Mature dealer networks, competitive funding costs, and accommodating Regulation Z guidelines underpin a projected 6.35% CAGR through 2031. Shifts toward younger, ethnically diverse buyers introduce fresh demand, while regulation on dwelling classification compels lenders to refine compliance workflows.

Asia-Pacific is the fastest-growing geography, forecast at a 9.22% CAGR. Rising middle-class incomes, domestic tourism promotion, and growing acceptance of flexible living catalyze originations despite less-developed lending infrastructures. International banks and fintech companies increasingly collaborate with local dealers to standardize title, insurance, and servicing frameworks, laying the groundwork for scalable growth across the RV financing market.

Europe presents a mature yet fragmented landscape shaped by diverse regulatory regimes and limited campsite density. Demand centers on sustainable drivetrains and lightweight designs, prompting lenders to explore green-loan structures and ESG-linked asset-backed securities. South America, led by Brazil and Argentina, follows with a 7.45% CAGR outlook, though currency fluctuations and political volatility temper risk appetite.

In the Middle East and Africa, the RV financing market remains nascent, but affluent customers in the United Arab Emirates and South Africa exhibit rising interest in luxury motorhomes, hinting at long-term potential.

Competitive Landscape

The RV financing market demonstrates a degree of concentration. The top lenders in this market collectively hold a significant portion of the originations. The top five lenders in the RV financing market control a substantial portion of the market's originations in 2025. Bank of America is a leading player in the RV financing market. Scale allows access to low-cost wholesale funding and extensive dealer floor-plan relationships[3]“RV Loans & Financing Available Through Our Dealer Network,” Bank of America, dealer-network.bankofamerica.com . Wells Fargo is another significant lender, having enhanced its digital onboarding processes and established co-branded credit partnerships.

Captive finance divisions of major OEMs broaden reach by bundling promotional APRs with warranty programs, locking in customers and capturing incremental service revenue. Digitally native lenders employ AI-driven underwriting and instantaneous funding to win borrowers valuing speed and transparency. Synchrony’s expansion into trailer loans via strategic alliances illustrates how specialized financiers exploit product adjacencies to gain share.

Competitive intensity escalates as ESG-linked securitizations lower capital costs for lenders able to quantify environmental benefits, such as solar-equipped motorhomes. Players pioneering telematics-based pricing achieve portfolio loss advantages, which they reinvest in rate discounts. The strategic battlefield now spans cost of funds, customer experience, and data analytics capability, ensuring ongoing dynamism in the RV financing market.

Recreational Vehicle Financing Industry Leaders

Bank of America

Wells Fargo

JPMorgan Chase

Truist Bank (incl. LightStream)

U.S. Bank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: In collaboration with Epic Finance, AEONrv introduced a national financing program covering Class B and Class C motorhomes.

- April 2025: The RV Industry Association advanced the bipartisan Travel Trailer and Camper Tax Parity Act (H.R. 332) to allow dealers full deduction of interest on floor-plan loans for non-motorized towables units that represent 88% of RV sales.

Global Recreational Vehicle Financing Market Report Scope

Recreational vehicle financing refers to the process of obtaining loans or payment plans to purchase motorhomes, trailers, and other leisure vehicles. This financial service allows individuals and families to afford RVs by offering flexible repayment options, competitive interest rates, and various loan structures, catering to the growing demand for domestic travel and outdoor experiences.

The recreational vehicle financing market is segmented into vehicle type, financing sources, and geography. Based on vehicles, motorhomes (class a, class b, class c), caravans (travel trailers, fifth wheels, toy haulers, truck campers, pop-up trailers, folding camping trailers), based on financing sources (banks and credit unions, RV dealership financing, manufacturer financing, online lenders, government-backed loans). The market is segmented based on geography into North America, Europe, Asia-Pacific, and the rest of the world.

For each segment, the market size and forecast were based on the value of USD.

| Motorhomes | Class A |

| Class B (Van Conversions) | |

| Class C | |

| Towable RVs / Caravans | Travel Trailers |

| Fifth Wheels | |

| Toy Haulers | |

| Truck Campers | |

| Pop-up / Folding Trailers |

| Banks and Credit Unions |

| Dealer/OEM Captive Financing |

| Manufacturer-backed Programs |

| Online / FinTech Lenders |

| Peer-to-Peer and Marketplace Lending |

| Government-backed Loans |

| New Purchase Loans |

| Refinance / Equity-release Loans |

| Prime (FICO Above 720) |

| Near-Prime (660 to 719) |

| Sub-Prime (Below 660) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle | Motorhomes | Class A |

| Class B (Van Conversions) | ||

| Class C | ||

| Towable RVs / Caravans | Travel Trailers | |

| Fifth Wheels | ||

| Toy Haulers | ||

| Truck Campers | ||

| Pop-up / Folding Trailers | ||

| By Financing Source | Banks and Credit Unions | |

| Dealer/OEM Captive Financing | ||

| Manufacturer-backed Programs | ||

| Online / FinTech Lenders | ||

| Peer-to-Peer and Marketplace Lending | ||

| Government-backed Loans | ||

| By Loan Purpose | New Purchase Loans | |

| Refinance / Equity-release Loans | ||

| By Borrower Credit Tier | Prime (FICO Above 720) | |

| Near-Prime (660 to 719) | ||

| Sub-Prime (Below 660) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Recreational Vehicle Financing market?

The recreational vehicle financing market stands at USD 42.4 billion in 2026 and is forecast to reach USD 59.82 billion by 2031.

Which vehicle segment dominates loan originations?

Travel trailers within the towable category led with 35.12% of 2025 volume.

How fast are fintech lenders growing in this space?

Online and fintech originators are projected to expand at a 15.02% CAGR through 2031.

Why are remote workers influencing demand?

Remote professionals use RVs as full-time residences, generating year-round financing demand and longer loan terms.

What restrains market growth despite favorable rates?

High upfront vehicle prices, rapid depreciation, and rising insurance costs compress affordability and refinancing options.

Which region is expected to grow the fastest?

Asia-Pacific is projected to grow at a 9.22% CAGR as middle-class leisure spending accelerates.

Page last updated on: