Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

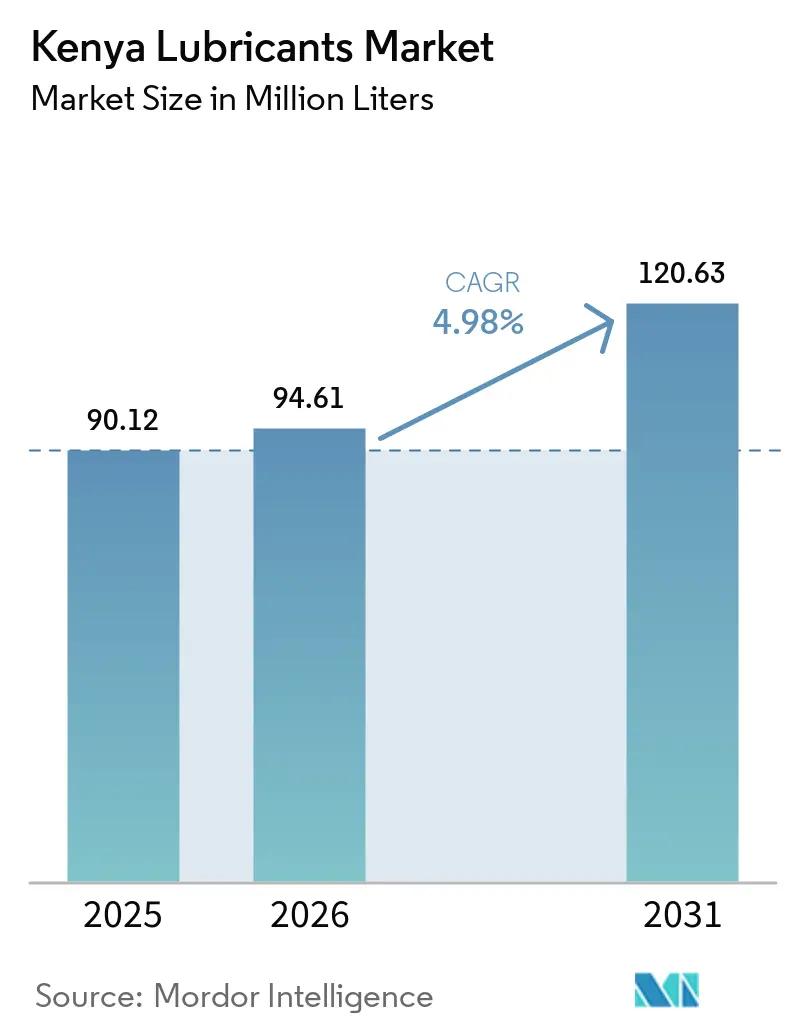

| Base Year Market Size (2025) | 90.12 Million liters |

| Market Volume (2026) | 94.61 Million liters |

| Market Volume (2031) | 120.63 Million liters |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

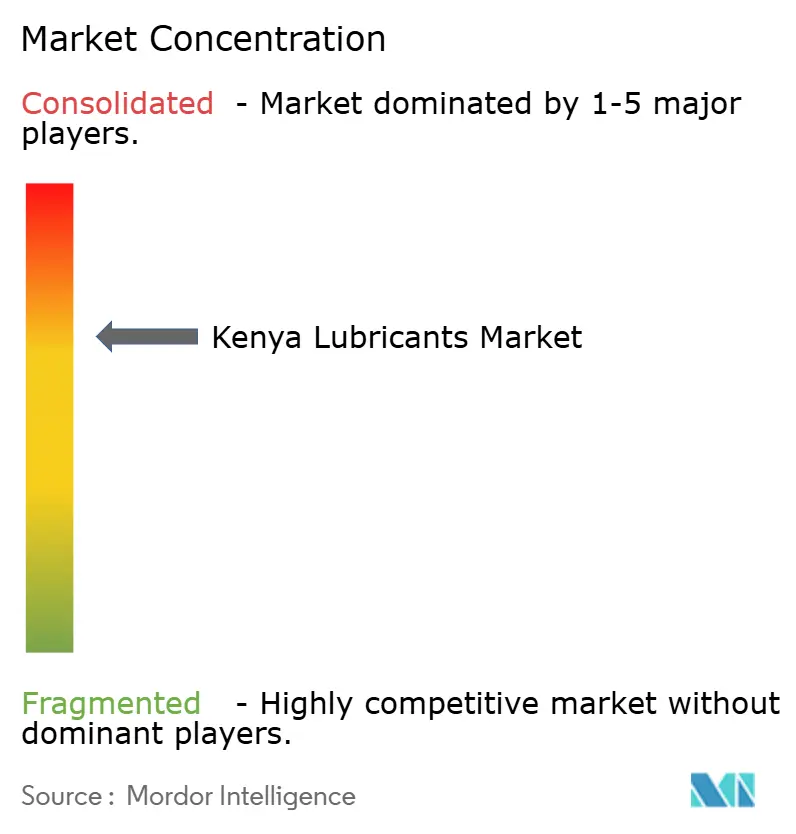

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Lubricants Market Analysis by Mordor Intelligence

The Kenya Lubricants Market size is expected to increase from 90.12 million liters in 2025 to 94.61 million liters in 2026 and reach 120.63 million liters by 2031, growing at a CAGR of 4.98% over 2026-2031. Infrastructure-led industrial expansion, a recovering vehicle parc, and rising logistics throughput along the Nairobi-Mombasa corridor continue to anchor demand. However, crude-linked base-oil volatility and an evolving electric-mobility policy framework complicate margins. Rapid construction activity, geothermal power investments, and county-level road works are intensifying the consumption of hydraulic fluids and grease. Meanwhile, the surging boda-boda segment is pushing small-engine synthetics into the mainstream. Policy-driven electrification and a higher excise on finished-lube imports are accelerating the business case for local blending. This shift is prompting both multinationals and regional independents to expand domestic capacity. Competitive intensity remains moderate, as the three largest oil-marketing companies (OMCs) jointly hold a significant share of petroleum volumes. Additionally, quality-assurance platforms, predictive-maintenance services, and loyalty programs are emerging as key differentiators across both formal and informal retail channels.

Key Report Takeaways

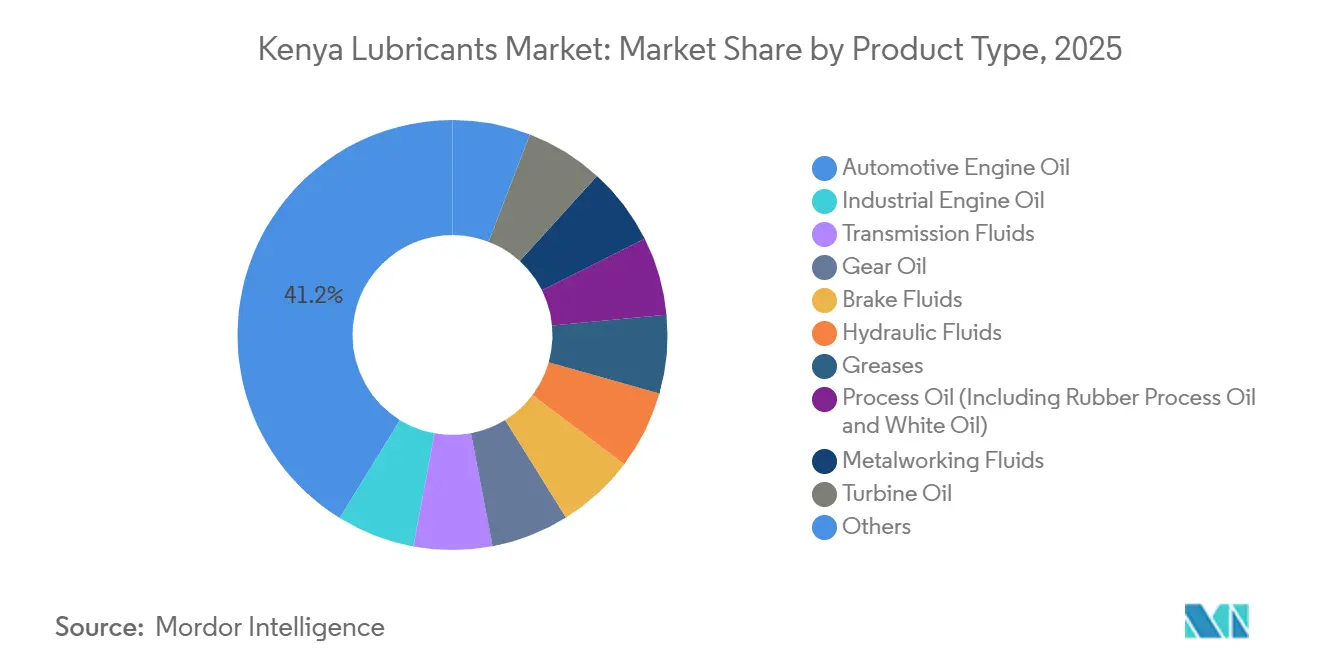

- By product type, automotive engine oil held 41.22% of the Kenya lubricants market share in 2025, while grease is projected to expand at a 5.68% CAGR through 2031.

- By end-user, the automotive segment accounted for 55.23% of 2025 volume; the industrial segment is set to grow at a 5.55% CAGR over 2026-2031.

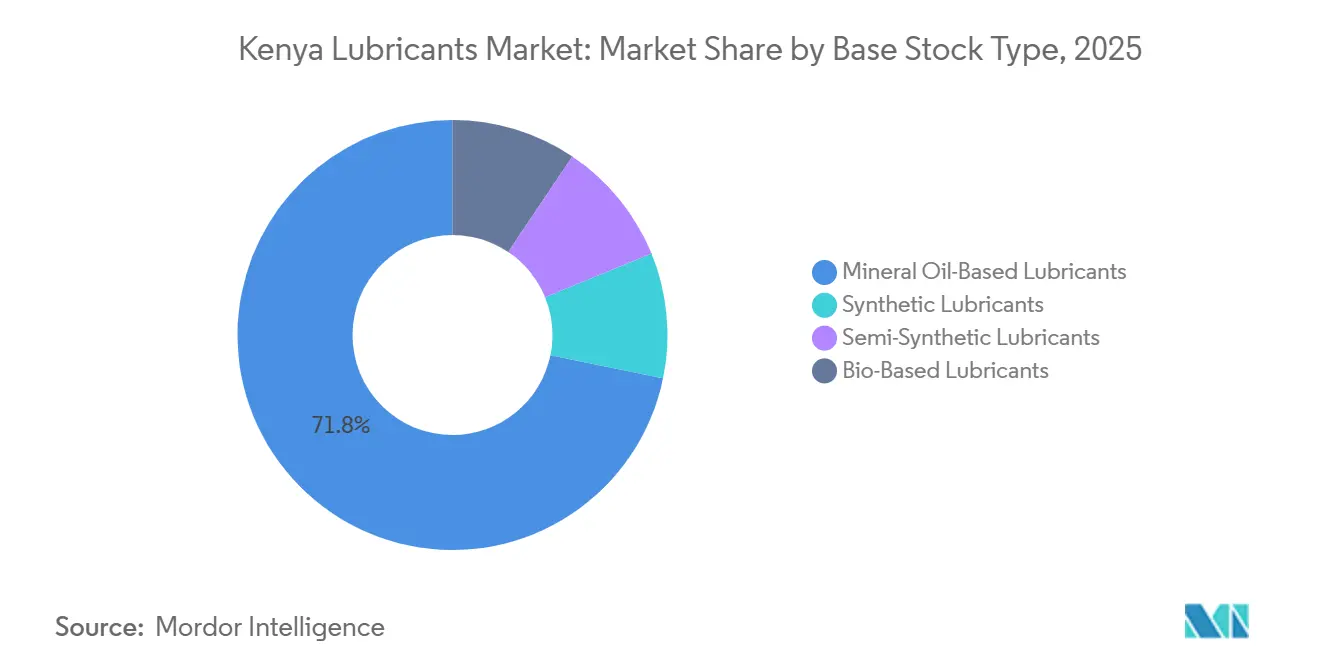

- By base stock type, mineral oil-based lubricants commanded 71.77% of 2025 demand, yet synthetic lubricants are advancing at a 5.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kenya Lubricants Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid expansion of construction and industrial CAPEX | +1.20% | Nairobi, Mombasa, Kwale | Medium term (2-4 years) |

| Growing on-road vehicle parc and ageing fleet | +1.50% | National, highest density Nairobi and Central Kenya | Short term (≤ 2 years) |

| Increasing investments in thermal and geothermal power plants | +0.80% | Rift Valley and national grid nodes | Long term (≥ 4 years) |

| Nairobi-Mombasa logistics corridor accelerating heavy-duty lube demand | +0.90% | A109 corridor and SGR freight routes | Medium term (2-4 years) |

| Surging motorcycle ride-hailing fueling demand for small-engine synthetics | +1.00% | Urban and peri-urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Construction and Industrial CAPEX

Capital investments in roads, water projects, and manufacturing plants are boosting the consumption of hydraulic fluids, gear oils, and extreme-pressure greases. The 2026 Manufacturing Priority Agenda underscores the pivotal role of manufacturing in economic transformation. A surge in cement output signals ongoing infrastructure activities. County budgets, such as Kwale’s allocation for machinery fuel and lubricants, underscore how devolved funding directly elevates the demand for heavy-equipment lubricants. Suppliers providing bundled services - such as oil analysis, contamination control, and predictive maintenance - are locking in multiyear contracts, insulating themselves from spot-price volatility. These contracts enhance the perception of the Kenyan lubricants market as a stable revenue stream for vendors adhering to ISO and KEBS standards. In summary, construction and industrial capital expenditures are the main catalysts for medium-term growth during the forecast period of 2026-2031.

Growing On-Road Vehicle Parc and Ageing Fleet

Vehicle registrations hit a record high, marking a year-on-year uptick. The robustness of commercial vehicles is driving demand for heavy-duty diesel engine oil and transmission fluid. While Kenya predominantly has a second-hand vehicle fleet, imports are entering service at seven to eight years old, just shy of a stricter age cutoff. These mature engines require shorter drain intervals and a diverse viscosity range, fostering a preference for mineral oils and economy multigrades, which are easily accessible at independent workshops. This pattern guarantees a consistent rise in lubricant volumes, even as urban areas witness a surge in electric vehicle adoption, highlighting the Kenya lubricants market's near-term resilience.

Increasing Investments in Thermal and Geothermal Power Plants

Kenya's power capacity is on the rise, with aspirations to hit even loftier targets by 2030. The Olkaria expansion, focusing on geothermal and thermal projects, is poised to play a pivotal role. Every megawatt generated leads to steady purchases of turbine oils, transformer oils, and drilling-rig hydraulics - all of which are vital for utility operations. KETRACO’s blueprint for new transmission lines is set to heighten the demand for transformer oil, particularly for IEC/ISO compliant brands. With significant penalties tied to power-plant downtimes, utilities are willing to invest in premium, traceable, lab-tested fluids, bolstering the high-margin segments of the Kenyan lubricants market.

Nairobi-Mombasa Logistics Corridor Accelerating Heavy-Duty Lube Demand

The Port of Mombasa celebrated a significant cargo-handling milestone[1]Kenya Ports Authority, “2025 Cargo Throughput Statistics,” kpa.co.ke . Moreover, transit freight to neighboring land-locked countries experienced a notable uptick. Heavy-duty trucks, making long hauls on the A109 highway, frequently undergo oil changes, consuming considerable engine oil with each service. This highway traffic not only broadens the reach of the Kenyan lubricants market but also draws in operators from Uganda and Rwanda. These operators often stock up in Mombasa or Nairobi, avoiding potential shortages back home. Local distributors, with depots along the corridor and mobile service trucks, are strategically positioned to seize these regional opportunities and cultivate cross-border loyalty.

Restraints Impact Analysis*

| RESTRAINT | % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Crude-price linked base-oil cost volatility | -0.70% | Nationwide import exposure via Mombasa | Short term (≤ 2 years) |

| Planned excise duty on finished-lube imports | -0.50% | National | Medium term (2-4 years) |

| Early-stage EV and hybrid roadmap dampening long-term volume outlook | -0.30% | Urban EV hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Linked Base-Oil Cost Volatility

Fluctuations in Brent prices have a direct bearing on the landed costs of imported base oils. In November 2025, diesel landed prices increased, whereas super-petrol prices decreased, underscoring an asymmetric price pass-through. A four-month freeze on pump prices led to inventory losses for Oil Marketing Companies (OMCs), putting a strain on their lubricant working capital. Distributors, bound by fleet contracts of 90 to 180 days, face a mismatch risk, given their overseas suppliers operate on 30-day quoting terms. As crude prices remain elevated, there is a noticeable shift toward extended-drain synthetics and bio-based alternatives. This evolving preference is exerting pressure on the volumes of mineral oils, which currently dominate Kenya's lubricant market.

Planned Excise Duty on Finished-Lube Imports

The Finance Act 2025 increased the VAT on lubricant supplies funded by aid and raised the excise on plastic packaging, thereby inflating the landed import costs[2]Kenya Revenue Authority, “Finance Act 2025,” kra.go.ke . The mandate for certificates of origin has introduced delays in port clearances. Moreover, a recent tribunal ruling underscored the significant effect of reclassification on duty rates. These challenges have catalyzed a surge in investments toward domestic blending lines. A case in point is Kenol Kobil's collaboration with Castrol, emphasizing this trend. By opting for local blending, they avoid tariffs on finished goods and secure a margin advantage. As domestic blending capacity expands, it is also reshaping the sourcing landscape of Kenya's lubricant sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automotive Engine Oil Dominance Meets Grease Acceleration

In 2025, automotive engine oil secured a dominant 41.22% share of the volume, solidifying its status as a pivotal segment. Grease, fueled by the demands of construction machinery and mining equipment, is projected to outpace all other product types, boasting a 5.68% CAGR through the forecast period of 2026-2031.

Demand for industrial engine oil mirrors the growth in backup power capacities. Meanwhile, transmission fluids and gear oils are reaping the rewards of a resurgence in commercial vehicle registrations. The consumption of brake and hydraulic fluids is closely tied to periodic vehicle inspections and county-level road construction activities. Turbine and transformer oils, though niche, are capitalizing on KETRACO’s grid expansion. While process oils, metalworking fluids, and other specialty lubricants maintain a modest market size, they are witnessing a steady uptick in demand, thanks to local OEM assembly lines and fabrication shops in Kenya.

By End-User Industry: Automotive Leadership, Industrial Acceleration

In 2025, the automotive sector accounted for a substantial 55.23% of the overall demand. This consumption was spread across passenger vehicles, commercial vehicles, and a swiftly expanding base of two-wheelers. Boda-boda riders, who often schedule multiple oil changes each month, present a lucrative opportunity for distributors, especially those forging direct ties with fleet managers.

Industrial sectors, such as power generation, metalworking, textiles, and cement, are poised for a 5.55% CAGR growth during the forecast period of 2026-2031. This growth is largely attributed to the expansion of geothermal energy and manufacturing. While marine and aerospace applications are predominantly confined to coastal shipping and major airports, heavy equipment users in construction, mining, and agriculture are increasingly seizing a larger slice of the Kenyan lubricants market, especially in grease and hydraulic fluids.

By Base Stock Type: Mineral Incumbency, Synthetic Ascent

In 2025, mineral oil dominated the landscape, accounting for a significant 71.77% of consumption. This dominance highlights the price sensitivity of consumers and the adaptability of an aging vehicle fleet to a range of viscosity bands. However, synthetic oils are growing at a notable 5.26% CAGR during the forecast period of 2026-2031. This surge is driven by fleets seeking extended drain intervals and OEMs imposing stricter warranty specifications.

Semi-synthetic oils, which combine Group III or PAO base stocks with mineral formulations, are becoming increasingly popular among budget-conscious workshop owners. While bio-based lubricants are still in their nascent stages, they could gain momentum with potential policy support, especially as Kenya intensifies its biofuel crop production efforts. This trend suggests a possible transformation in the future dynamics of the Kenyan lubricants market.

Geography Analysis

Nairobi and its neighboring counties has taken the center stage in Kenya's lubricant market, driven by a thriving vehicle parc and bolstered by active corporate fleets, ride-hailing services, and independent garages. Mombasa, home to two major blending plants and recognized as East-African's busiest port, serves as both the primary import gateway and a coastal hub for demand. The 480-km corridor that links Nairobi and Mombasa not only bridges the two cities but also expands the market size, facilitating the transit of regional cargo to destinations such as Uganda, Tanzania, and Rwanda.

While the geothermal hubs in the Rift Valley lean towards high-spec turbine and transformer oils, Western Kenya reaps the benefits of agricultural mechanization and cross-border trade. Nationwide, retail fuel stations act as key distribution points for packaged lubricants. Furthermore, with devolved budgets channeling funds towards road graders, drilling rigs, and health-sector generators, county procurement offices are gaining prominence. Suppliers are cementing their foothold in Kenya's diverse consumption hotspots by establishing multi-county depot networks, ensuring compliance with KEBS packaging standards, and forming rapid-response technical teams.

Competitive Landscape

The Kenya lubricants market is moderately consolidated. Vivo, with its blending plant in Mombasa, has rolled out a USSD anti-counterfeit platform, promoting verified purchases to enhance brand trust in informal markets. TotalEnergies operates the region's largest ISO 9001-certified blending facility, exporting to six neighboring nations and establishing Kenya as a crucial regional hub. Rubis, in collaboration with state-owned NOCK, is revitalizing retail outlets and sharing profits, solidifying its national footprint.

Yet, the landscape is shifting with the entry of new players. Saudi Aramco's green light to acquire Valvoline's local assets hints at ambitions that extend beyond lubricants, eyeing fuel imports as well. Local entities like Yana Oil, backed by Bureau Veritas laboratory management, are distinguishing themselves with tailored formulations and prompt deliveries. As the market contends with counterfeiting challenges, suppliers are leveraging technology-driven promotions, predictive maintenance packages, and mechanic loyalty programs to enhance their foothold in Kenya's lubricant sector.

Kenya Lubricants Industry Leaders

Hass Petroleum

OLA Energy

Rubis Energy Kenya

TotalEnergies Marketing Kenya PLC

Vivo Energy (Shell)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Gulf Energy E&P BV had secured a USD 15 million onshore drilling rig from the UAE to expedite Kenya's first commercial oil production in the South Lokichar Basin, targeting a December 1, 2026, commencement. This development is expected to impact the demand for lubricants in Kenya by driving demand for specialized lubricants used in drilling and oil production processes.

- July 2025: Vivo Energy Kenya, the official distributor and marketer of Shell products and services in the country, has announced the opening of its 336th Shell service station. The newly launched Shell Imara Daima service station is conveniently located in Nairobi along Mombasa Road.

Kenya Lubricants Market Report Scope

Lubricants are fluids designed to minimize friction between surfaces, thereby preventing wear and tear. Tailored for specific end users, these lubricants are crafted using distinct additives and base oils. Typically, base oils comprise 75% to 90% of a lubricant's formulation, imparting the final product with its essential lubricating properties.

The lubricants market is segmented by product type, end-user industry, and base stock type. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil, metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

How fast will lubricant demand rise in Kenya between 2026 and 2031?

The Kenya lubricants market size stands at 94.61 million liters in 2026, and it is projected to reach 120.63 million liters by 2031 at a 4.98% CAGR.

Which product line is expanding quickest?

Grease leads growth at a projected 5.68% CAGR thanks to heavy-equipment deployments in construction and mining.

What proportion of sales does automotive use represent?

Automotive accounted for 55.23% of 2025 volume and remains the single largest end-user block.

Are synthetics gaining ground over mineral oils?

Yes, although mineral grades still hold 71.77% share, synthetics are advancing at 5.26% CAGR as fleets chase longer drain intervals.

What policy shifts could disrupt future lubricant demand?

The National Electric Mobility Policy aims for 5% EV penetration of new registrations, gradually redirecting demand toward greases, e-gear oils and thermal fluids.

Page last updated on: