Railway Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

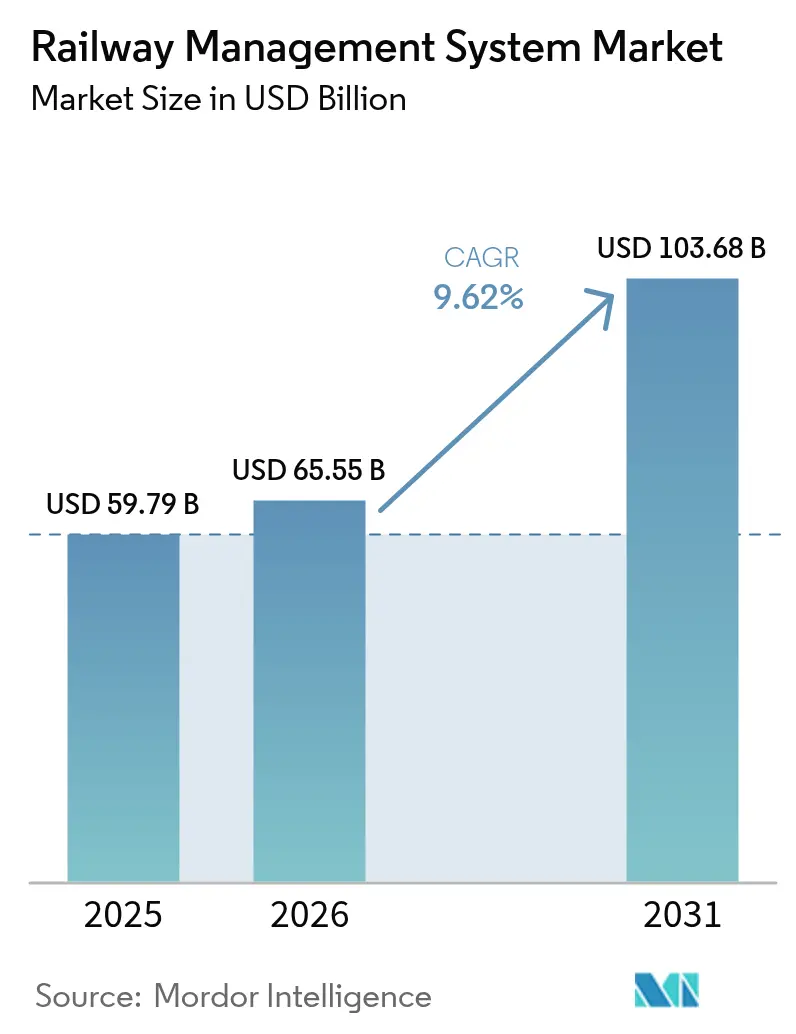

| Market Size (2026) | USD 65.55 Billion |

| Market Size (2031) | USD 103.68 Billion |

| Growth Rate (2026 - 2031) | 9.62% CAGR |

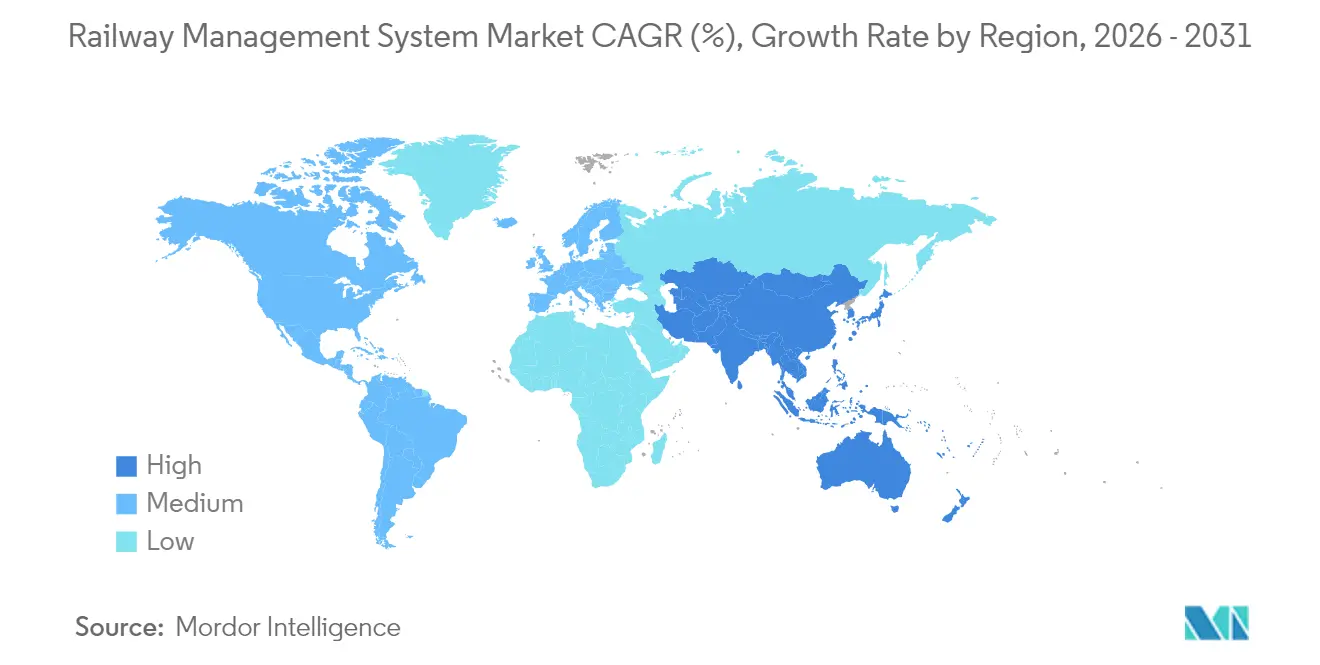

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Railway Management System Market Analysis by Mordor Intelligence

Railway Management System Market size market size in 2026 is estimated at USD 65.55 billion, growing from 2025 value of USD 59.79 billion with 2031 projections showing USD 103.68 billion, growing at 9.62% CAGR over 2026-2031.

Continuous regulatory pressure for digital-first rail operations, swelling cybersecurity budgets, and rising investments in predictive maintenance collectively underpin this expansion. Mandated interoperability programs such as the EU’s ERTMS Baseline 3, large-scale AI roll-outs on Asian high-speed lines, and federal decarbonization roadmaps in North America reinforce operator appetite for platform-level upgrades across the railway management system market transport[1]European Commission, “ERTMS: State of Play,” transport.ec.europa.eu. Solutions outpace services in absolute revenue terms, yet managed services record the quickest slope of growth as operators pivot to outcome-based contracting for risk transfer and skills access. At the same time, freight-focused visibility initiatives, exemplified by RailPulse telematics and Union Pacific’s API ecosystem, improve operational resilience and spur fresh demand for data-rich control architectures across the railway management system market.

Second-order headwinds also shape strategy. Volatile steel prices inflate track-related capex, fiber-backhaul scarcity slows digital transformation in parts of Sub-Saharan Africa, and legacy signaling interfaces raise integration risk, factors that intensify vendor screening and strengthen the business case for turnkey offerings. Nevertheless, government decarbonization funds, such as the U.S. Action Plan for Rail Energy and Emissions Innovation, continue to unlock procurement budgets for energy-optimization modules and zero-emission propulsion, lifting medium-term upside for the railway management system market [2]U.S. Department of Energy, “Rail Energy and Emissions Innovation Action Plan,” energy.gov.

Key Report Takeaways

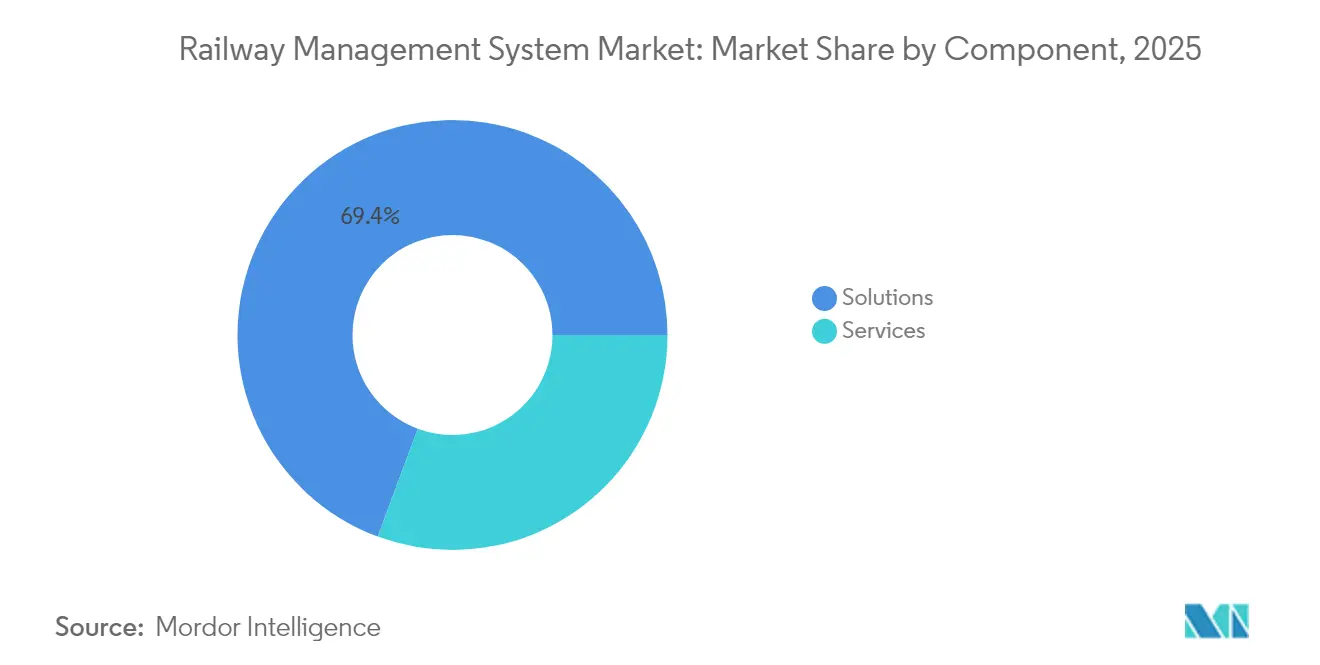

- By component, solutions commanded 69.35% of the railway management system market share in 2025, while managed services delivered the fastest 9.8% CAGR outlook to 2031.

- By rail type, passenger rail led with a 54.25% revenue share of the railway management system market size in 2025, whereas freight rail is projected to expand at a strong 10.04% CAGR through 2031.

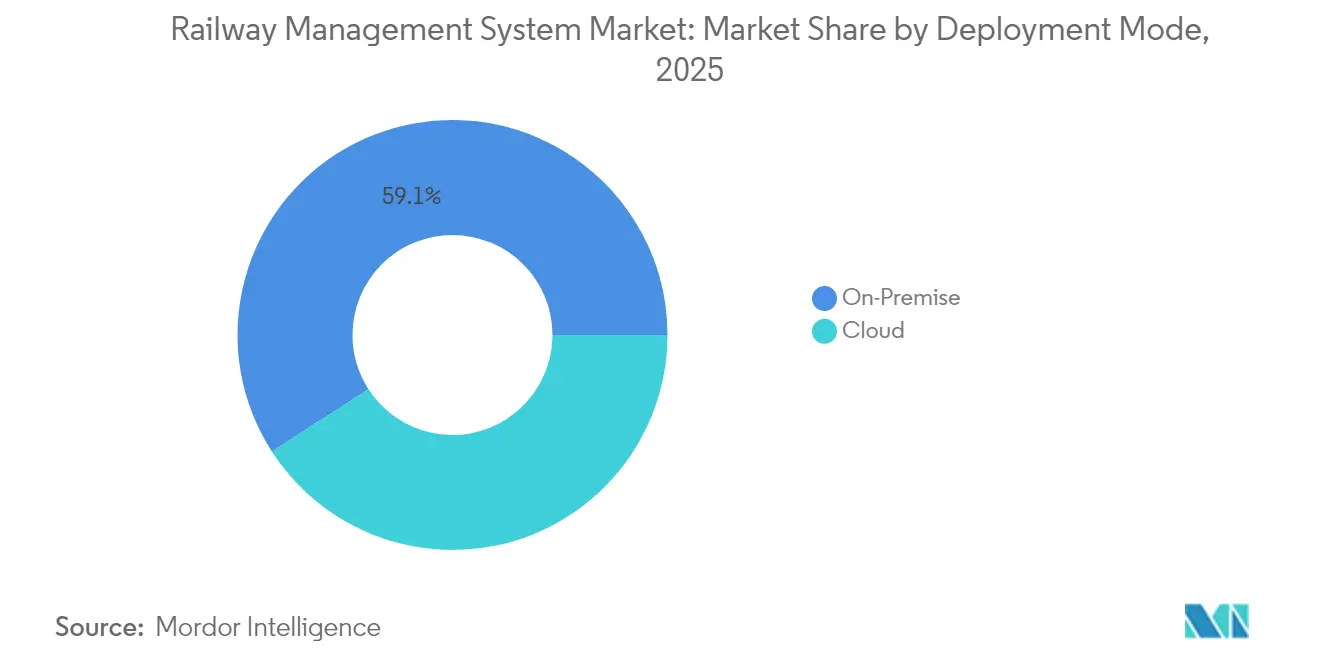

- By deployment mode, on-premise installations retained 59.12% of the 2025 railway management system market size, yet cloud deployments are forecast to grow at 10.12% CAGR to 2031.

- By geography, Europe held 31.45% of the 2025 railway management system market share, but Asia offers the quickest 9.96% CAGR over the forecast window.

- Hitachi Rail, Thales, Siemens Mobility, and Alstom together accounted for roughly 43% of the global railway management system market share in 2024, pointing to a moderately consolidated playing field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Railway Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated ERTMS Baseline 3 adoption across core EU corridors by 2030 | +2.1% | Europe with spillover to APAC | Medium term (2-4 years) |

| Digital-twin-enabled predictive maintenance roll-outs on Asian high-speed lines | +1.8% | APAC core, expanding to North America | Long term (≥ 4 years) |

| Government decarbonization stimulus boosting energy-optimization modules | +1.5% | Global, early uptake in EU & North America | Medium term (2-4 years) |

| Rapid CBTC deployment in GCC urban networks | +0.9% | Middle East, tech transfer to emerging markets | Short term (≤ 2 years) |

| North American freight rail demand for end-to-end visibility | +1.2% | North America, influencing global freight standards | Medium term (2-4 years) |

| Escalating ransomware threats driving cyber-secure rail control investments | +1.7% | Global critical-infrastructure regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandated ERTMS Baseline 3 Adoption Across Core EU Corridors by 2030

Regulation-driven adoption of ERTMS Baseline 3 across the Trans-European Network has become the strongest systemic catalyst for the railway management system market. By early 2023, 52% of the 59,055 km core network had migrated, and 21,744 rolling-stock units are due for ETCS upgrades by 2030. The mandate sparks a worldwide cascade effect because suppliers must deliver interoperable software stacks ready for multi-region deployment. Hitachi Rail’s EUR 1.66 billion (USD 1.8 billion) purchase of Thales’ Ground Transportation Systems signals early-stage consolidation aimed at vertically unifying digital signaling IP. As implementation costs have doubled since 2018, network owners increasingly favor single-platform vendors to ease budget pressure and compress delivery risk.

Digital-Twin-Enabled Predictive Maintenance Roll-outs on Asian High-Speed Lines

China now operates more than 48,000 km of high-speed track using AI-imbued digital twins capable of processing 200 terabytes within 40 minutes, achieving 95% alert accuracy and cutting minor track faults by 80%. Coupled with LTE-M-supported CBTC networks in cities such as Shenyang, this shift moves maintenance strategy from reactive to predictive, slashing unplanned downtime and labor overhead [3]Huawei, “Shenyang Metro LTE-M case study,” huawei.com. These gains place competitive pressure on Western incumbents and embed predictive analytics as a baseline requirement across the railway management system market.

Government Decarbonization Stimulus Boosting Energy-Optimization Modules

Net-zero targets translate into monetizable demand for electrification, hydrogen traction, and advanced energy-management software. The U.S. Action Plan prioritizes catenary extension, battery-electric consist pilots, and hydrogen locomotives under a 2050 target date[4]U.S. Department of Energy, “Rail Energy and Emissions Innovation Action Plan,” energy.gov. The United Kingdom’s GBP 120 million (USD 152 million) investment in Scottish feeder stations underscores the scale of mid-voltage reinforcement needed for full network electrification. Peer-reviewed research demonstrates that hybrid trains can cut fuel use and CO2 by 34% when batteries are optimally sized, hard-coding energy optimization modules into operator procurement checklists.

Rapid CBTC Deployment in GCC Urban Networks

Saudi Arabia’s 176 km Riyadh Metro is now the world’s longest driverless network, while Dubai and Doha race to extend fully automated lines. Greenfield nature and sovereign funding deliver accelerated deployment schedules and clean systems architectures, making GCC projects a live testbed for high-throughput CBTC, 5G trackside connectivity, and compartmentalized cybersecurity. Vendors gain economies of scale, enabling faster innovation cycles that ultimately radiate into emerging markets in Africa and Southeast Asia.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy signaling interfaces hindering full-stack integration | –1.4% | Global, acute in mature networks | Long term (≥ 4 years) |

| Budget overruns delaying software refresh cycles | –0.8% | Europe & North America | Medium term (2-4 years) |

| Inter-vendor OT-IT interoperability challenges | –0.7% | Global multi-vendor environments | Medium term (2-4 years) |

| Fibre-backhaul scarcity in Sub-Saharan corridors | –0.5% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Signaling Interfaces Hindering Full-Stack Integration

London’s Crossrail recorded GBP 2–3 billion overruns after complex handoffs between ERTMS, CBTC, and vintage TPWS hardware delayed commissioning. Similar PTC interoperability issues in the U.S. expose knowledge gaps, widen project timelines, and entrench incumbents. These friction points elevate integration services cost curves across the railway management system market.

Budget Overruns Delaying Software Refresh Cycles

Peer-reviewed analysis of 63 global rail projects places mean cost overrun at 44.7%, with software integration as a primary contributor. Isle of Wight’s GBP 26 million upgrade slipped four months on account of flawed software interfaces, underscoring how budget blowouts prolong the useful life of obsolete systems and slow technology absorption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate Through Integration Complexity

Solutions carved out 69.35% of the 2025 railway management system market, underscoring operator reliance on unified application suites amid rising digital complexity. Revenue growth is anchored in rail traffic management platforms, asset management engines, and control systems optimized for ERTMS roll-outs. In parallel, the managed-services niche is forecast to expand at 9.8% CAGR between 2026-2031, as operators externalize lifecycle risk to specialists, often under availability-based arrangements embedded in concession agreements. Training and consulting grow steadily, driven by workforce skills gaps around AI analytics and cybersecurity protocols.

Services strength mirrors a structural tilt toward outcome-based relationships, where performance KPIs replace one-off hardware sales. System integrators monetize cross-vendor complexity, and managed-service partners embed continuous improvement charters into multi-year SLAs. Regulatory audits around cyber, safety, and signaling drive demand for niche advisory capabilities, allowing professional services teams to wield premium hourly rates or subscription models. Together, these forces reinforce the solutions-as-a-service paradigm, cementing solutions at the core of the railway management system market.

By Rail Type: Freight Digitalization Drives Growth Momentum

Passenger rail currently represents the largest slice of the railway management system market size, with a 54.25% share in 2025, propelled by high-speed and urban mobility projects in Europe and Asia. Freight rail, however, delivers the sharper 10.04% CAGR trajectory to 2031, reflecting urgent shipper demand for predictive asset monitoring, real-time ETAs, and emissions reporting. High-speed and inter-city applications ride on sustained state funding for capacity upgrades, while light-rail corridors in GCC capitals leverage greenfield CBTC roll-outs to compress implementation cycles.

North American freight digitalization illustrates the upside: Union Pacific’s open API suite enables real-time status calls for 30,000 customers, and RailPulse fuses GPS, accelerometer, and impact sensors across fleet operators. Asset-heavy bulk carriers can thus shrink dwell, improve wagon turn, and solidify case studies that accelerate copycat adoption in Brazil, South Africa, and India, bolstering long-run demand in the railway management system market.

By Deployment Mode: Cloud Transformation Accelerates Despite Security Concerns

On-premise configurations still hold 59.12% revenue but cloud solutions claim the steeper 10.12% CAGR path, fueled by elastic compute, embedded AI frameworks, and pay-per-use pricing. Deutsche Bahn already pipes terabytes of sensor data through a cloud-native analytics layer, shrinking prediction runtimes for asset health diagnostics. Smaller operators embrace cloud to bypass heavy capital formation, whereas cybersecurity mandates in Europe promote hybrid architectures combining edge-certified servers with sovereign cloud storage. In effect, cloud’s structural scalability will chip away at on-premise share, further widening addressable revenue inside the railway management system market.

By End-User: Infrastructure Managers Lead Technology Adoption

Infrastructure managers entities responsible for right-of-way, power, and signaling—have emerged as the highest velocity adopters because they must satisfy network-wide safety mandates. Deutsche Bahn’s USD 5.1 billion Digital Rail roadmap demonstrates how owner-operators can embed ETCS Level 3, automatic train operation (ATO), and cloud analytics to lift capacity by up to 35%. Station managers focus on passenger information and CCTV analytics, while freight service providers channel capex toward telemetry and yard automation. The blurred boundaries of public-private consortiums spur hybrid governance models that use common data lakes and shared control centers, reinforcing the platform play across the railway management system market.

Geography Analysis

Europe retained 31.45% of 2025 revenue in the railway management system market, reflecting robust public funding and the legislative power of ERTMS Baseline 3. Germany alone will invest EUR 4.7 billion (USD 5.1 billion) by 2030 to unlock 35% capacity gains through digital signaling and automated operations. Siemens Mobility’s EUR 2.8 billion (USD 3.0 billion) framework with Deutsche Bahn further illustrates the scale of multi-year digitalization envelopes. Although Europe hosts dense legacy networks, vendors that master interface orchestration capture recurring upgrade fees, reinforcing Europe’s anchor position in the railway management system market.

Asia stands as the fastest expanding geography at a 9.96% CAGR through 2031. China has lengthened its rail footprint to 162,000 km, including 48,000 km high-speed, and plans CNY 590 billion (USD 81 billion) of 2025 investments. AI-based predictive maintenance combined with government-backed capacity additions fosters a broad market for digital twins and cloud analytics. India complements the growth narrative with a USD 30 billion budget committed to high-speed corridors and signaling upgrades, catalyzing supplier entry and value-chain localization. Collectively, these factors elevate Asia as the most attractive near-term volume prize in the railway management system market.

North America provides a stable but lower-beta trajectory compared to Asia. Federal decarbonization incentives and demand for freight visibility raise per-route digital spend, while BNSF’s USD 3.8 billion capex plan demonstrates Class I appetite for track and technology investment. The Middle East, anchored by the GCC’s metro pipelines, and Africa, constrained by fiber scarcity yet buoyed by pan-continental rail corridors, contribute emerging-market upside to the railway management system market. Here, turnkey vendors secure project wins by bundling private wireless, CBTC, and cyber-secure cloud to fill capability gaps.

Regulatory Landscape

Railway management system deployments are increasingly shaped by cybersecurity, safety, and interoperability requirements across major rail geographies. In the United States, TSA Security Directive 1580-21-01E took effect on January 16, 2026, requiring freight railroad owner-operators to maintain TSA-aligned cybersecurity implementation planning, including controls such as segmentation, access control, and continuous monitoring. This has heightened demand for secure-by-design traffic management, control, and data platforms.

In Europe, interoperability rules administered through the European Union Agency for Railways (ERA) continue to drive procurement requirements via CCS/Telematics TSIs. Product-security obligations are also tightening under the EU Cyber Resilience Act, including active reporting of exploited vulnerabilities starting September 11, 2026. In North America, rail security compliance extends to passenger operations, including Canada’s Passenger Rail Transportation Security Regulations that require at least annual security risk assessments, which reinforces the need for vendors with lifecycle governance tooling and managed security capabilities.

Value Chain Analysis

The value chain covers component suppliers (sensors, communications modules, semiconductors, and edge compute), platform and application developers (traffic management, asset and maintenance management, passenger information, ticketing, and security), and prime contractors or system integrators that combine signaling, telecom, cybersecurity, and control-center software into certified solutions for railway operators and infrastructure managers. Large OEMs and technology vendors such as Alstom, Siemens Mobility, Hitachi Rail, Thales, Wabtec, Cisco, and Nokia participate across multiple layers, while testing, certification, cybersecurity hardening, and safety case management represent a high-value share of delivery.

Downstream, long-term frameworks and programmatic modernization are becoming more common, shifting revenue toward multi-year integration, support, and managed services rather than one-off deployments. Interoperability requirements, particularly in multi-vendor environments, can bottleneck progress around legacy interfaces and standards conformance, which raises the value of platforms that expose open APIs and can align to European TSI-driven telematics architectures, including the updated TAP/TAF TSI adopted in 2026. Vendors able to coordinate OT-IT integration across signaling, private wireless, cloud analytics, and cybersecurity controls under outcome-based SLAs benefit most from this shift.

Competitive Landscape

Competitive intensity sits at the nexus of legacy hardware incumbency and software-driven value migration. Hitachi Rail’s EUR 1.66 billion (USD 1.8 billion) acquisition of Thales’ Ground Transportation Systems, creating a EUR 7.3 billion (USD 7.9 billion) revenue unit across 51 countries, demonstrates momentum toward scale-driven solution portfolios. Siemens, Alstom, ABB, and Wabtec protect sizeable installed bases, yet face encroachment from Cisco, Huawei, IBM, and hyperscalers offering cloud-native AI stacks.

Strategic contracting is tilting to decade-plus frameworks that lock vendors into joint innovation roadmaps and shared risk pools. Alstom’s EUR 600 million (USD 681 million) interlocking deal with Deutsche Bahn through 2032 exemplifies the governance shift toward outcome-oriented alliances. White-space battlegrounds include zero-trust OT networks, hydrogen traction battery management software, and obstacle detection algorithms—areas in which emerging specialists can capture defensible niches. Patent filings surged in 2024 around virtual block and sensor-fusion vision systems, such as Rail Vision’s U.S. grant for AI obstacle detection, verifying the race to anchor next-gen safety IP within the railway management system market.

Vendor scorecards now integrate cybersecurity maturity, cloud-readiness, and carbon-footprint transparency. Operators favor platforms equipped to orchestrate multi-vendor ecosystems and furnish open APIs. Consequently, ecosystem partnerships outpace isolated product launches, making integration competence the pivotal battleground within the railway management system market.

Railway Management System Industry Leaders

General Electric Company

ABB limited

Alstom SA

Cisco Systems Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-led standardization and security obligations create clear whitespace for vendors that can combine interoperability, telematics data exchange, and cyber-by-design workflows into upgradeable platforms. In Europe, the adoption of Regulation (EU) 2026/253 integrating telematics applications for passenger and freight services supports demand for common data architectures and compliance-ready interfaces, particularly for operators and infrastructure managers operating across borders and multi-vendor estates.

A second opportunity centers on enabling infrastructure for AI, automation, and modern signaling, especially fiber backhaul and IP networking, which can expand cloud analytics and video or security use cases. Network Rail’s Visual Safety and Security Systems Strategy released in April 2026 targets integration of disparate camera and analytics systems, supporting demand for unified command-and-control software, asset management integration, and cybersecurity. In Asia, Indian Railways program approvals during 2026 covering fiber rollout, electronic interlocking, station networking, and Kavach ATP expansion indicate ongoing budget allocation toward communications backbone and digital control layers, favoring suppliers that can deliver end-to-end integration across edge, network, applications, and lifecycle services on large distributed networks.

Recent Industry Developments

- June 2026: Alstom signed contracts totaling around EUR 690 million with Egyptian National Railways to modernize strategic corridors, including ETCS Level 1 signaling and digital operations control capabilities. The scale of this program reinforces demand for integrated traffic management, control-center software, and certified signaling ecosystems rather than standalone point solutions.

- June 2025: Network Rail and partners launched Project Reach to install 1,000 km of fiber along major UK routes to address coverage gaps and improve backhaul for digital applications. Expanded fiber capacity supports cloud-connected asset monitoring, video security, and real-time operational management modules that rely on resilient trackside-to-core connectivity.

- February 2024: Siemens Mobility and Leonhard Weiss won a EUR 2.8 billion multi-year control-and-safety framework with Deutsche Bahn. The long-duration framework structure signals continued procurement preference for platform roadmaps and integrated delivery models spanning deployment, upgrades, and lifecycle support.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the railway management system market covers software and related services that support planning, control, monitoring, and optimization of rail operations, traffic, assets, maintenance, and passenger information across rail networks.

Scope exclusions: Pure rail infrastructure civil works and standalone rolling stock manufacturing revenues are not counted unless they are bundled as part of a management-system contract.

Segmentation Overview

- By Component

- Solutions

- Rail Asset Management System

- Rail Traffic Management System

- Rail Operation Management System

- Rail Control System

- Rail Maintenance Management System

- Passenger Information System

- Rail Security and Safety

- Revenue Management and Ticketing

- Services

- Training and Consulting

- System Integration and Deployment

- Support and Maintenance Service

- Managed Service

- Professional Service

- Solutions

- By Rail Type

- Passenger Rail

- Freight Rail

- High-Speed / Inter-city Rail

- Urban and Light Rail

- By Deployment Mode

- On-Premises

- Cloud

- By End-User

- Railway Operators

- Infrastructure Managers

- Station Managers

- Freight Service Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped set the market boundary and build the first demand map by region. We relied on public transport and rail network statistics, plus policy direction from sources such as the World Bank, OECD transport data, the International Union of Railways (UIC), national transport ministries, and rail regulator publications. These inputs were then aligned with procurement and project information available in the public domain.

To keep the model grounded in actual spending patterns, we reviewed annual reports, investor presentations, and contract announcements from rail operators, integrators, and technology suppliers. We also used paid subscriptions for company financials and news intelligence, and a global contracts and tenders database to cross-check project timing and typical scope language. These desk sources are not exhaustive, and we also used other public documents to clarify definitions, validate assumptions, and resolve data gaps.

Primary Interviews and Surveys

Primary work focused on confirming what is budgeted and delivered under railway management programs, and how pricing shifts with cloud adoption, upgrades, and multi-year service terms. We spoke with rail operators, public authorities, system integrators, and niche software specialists across key geographies. That respondent input was then used to confirm adoption rates, replacement cycles, and the structure of typical deal terms.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 45% |

| Mid tier: 58% | Functional/Unit leaders: 26% | EMEA: 30% |

| Smaller Players: 15% | Managers: 59% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where rail network activity and investment signals are used to reconstruct the addressable spend on management systems by region and rail type. Inputs that commonly matter include rail route kilometers and traffic intensity, urban transit and mainline modernization programs, digital signaling and control rollouts, the mix of greenfield versus upgrade projects, and the share of contracts that include multi-year software and support.

Once the demand pool is formed, the total is corroborated with selective bottom-up approximations, such as sampled deal values from tenders, typical software and services splits, and ASP by deployment (on-premises versus cloud) where evidence exists. Where bottom-up evidence is thin, gaps are handled using comparable project archetypes, then stress-testing the assumption with operator and integrator feedback.

For forecasting, we use scenario analysis driven by a multivariate view of factors such as public rail capex direction, digitalization mandates, and expected refresh cycles for operations and maintenance platforms. The final outlook is adjusted only after the assumptions are checked against pipeline timing and renewal behavior provided by interviewees, and then reflected in yearly growth paths.

Data Validation & Update Cycle

Validation is done through checks that compare model totals with independent signals, such as public rail investment programs, awarded contract values, and region-level deployment momentum. When an anomaly shows up, such as a sudden jump that cannot be explained by project timing or price movement, it is flagged for analyst review and, when needed, clarified through follow-up outreach.

Before sign-off, assumptions and calculations go through multi-step reviews so the logic can be traced from drivers to totals. Reports are refreshed annually, and interim updates are triggered when material events occur, such as policy changes, major project delays, or sharp currency moves. Right before delivery, a fresh review pass is completed so clients receive the most current view available.

Mordor Intelligence's Railway Management System Market Size Compared With Other Published Estimates

Published market sizes for railway management systems can differ even when the topic name looks the same, because the counted revenue streams and timing choices are not always aligned. Differences usually come from what gets treated as software versus broader rail digitalization, the year used for currency conversion, and how multi-year service revenue is recognized.

In a refresh-led build, the biggest gap drivers are often the update cadence of project pipelines, the way ASP changes are carried into the next year, and whether tender-award delays are reflected quickly or averaged out. By updating currency timing and re-checking contract scope language through recent awards and operator feedback, Mordor Intelligence keeps the total tied to delivered management-system revenue rather than wider signaling or infrastructure spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 65.55 B (2026) | |

| Global Consultancy A | USD 57.10 B (2024) | Uses an earlier pricing and currency window, and may smooth ASP progression across upgrades, which can miss the step-change effect of newer digital control rollouts and higher service attach rates. |

| Trade Journal B | USD 27.90 B (2028) | Often reports a narrower software-only subset or a partial regional roll-up, and the refresh cadence can lag recent tender awards and go-live delays that change the revenue recognized in a given year. |

The spread is easier to interpret once the year label and what counts as revenue are made consistent, because some figures lean on earlier-year price points or partial scope coverage. Our approach stays repeatable by tying totals to observable demand signals (tenders, upgrade cycles, and operator budgets) and then revising assumptions when timing and currency conditions change.

Key Questions Answered in the Report

What is the current Railway Management System Market size?

The Railway Management System Market size is estimated at USD 65.55 billion in 2026 and is projected to grow at a CAGR of 9.62% during the forecast period (2026-2031).

Who are the key players in Railway Management System Market?

General Electric Company, ABB limited, Alstom SA, Cisco Systems Inc. and IBM Corporation are the major companies operating in the Railway Management System Market.

Which is the fastest growing region in Railway Management System Market?

Asia is estimated to grow at the highest 9.96% CAGR over the forecast period (2026-2031).

Which region has the biggest share in Railway Management System Market?

In 2025, Europe accounts for the largest 31.45% market share in Railway Management System Market.

Page last updated on: