Road Safety Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

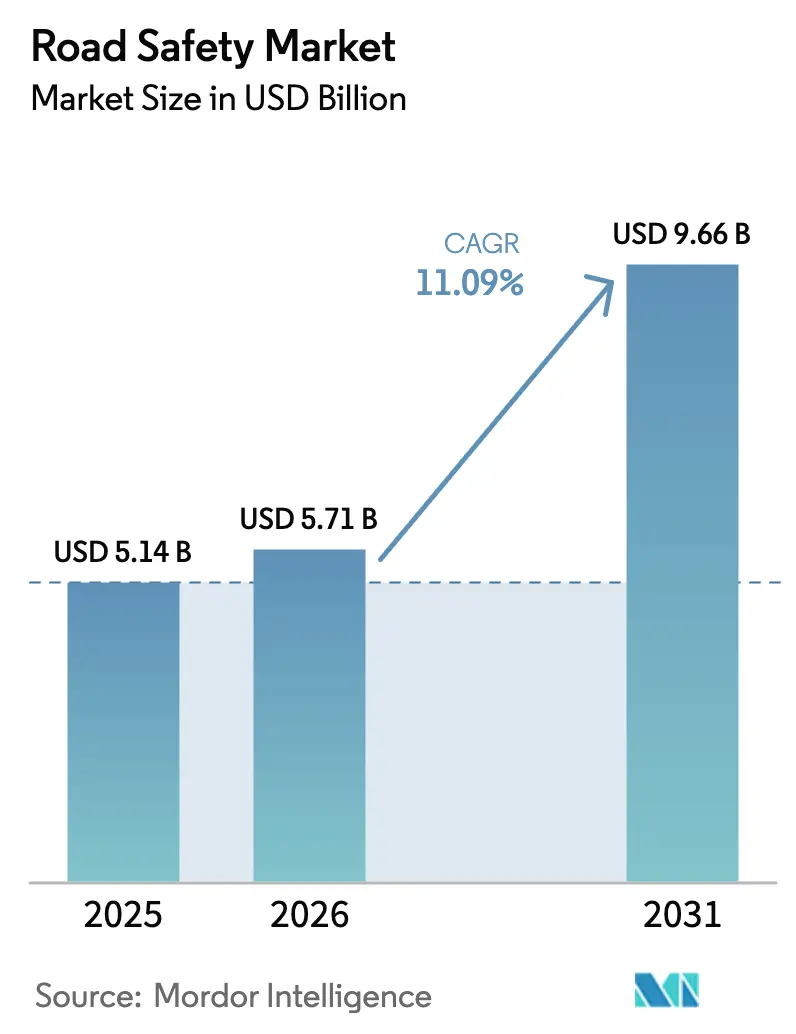

| Market Size (2026) | USD 5.71 Billion |

| Market Size (2031) | USD 9.66 Billion |

| Growth Rate (2026 - 2031) | 11.09% CAGR |

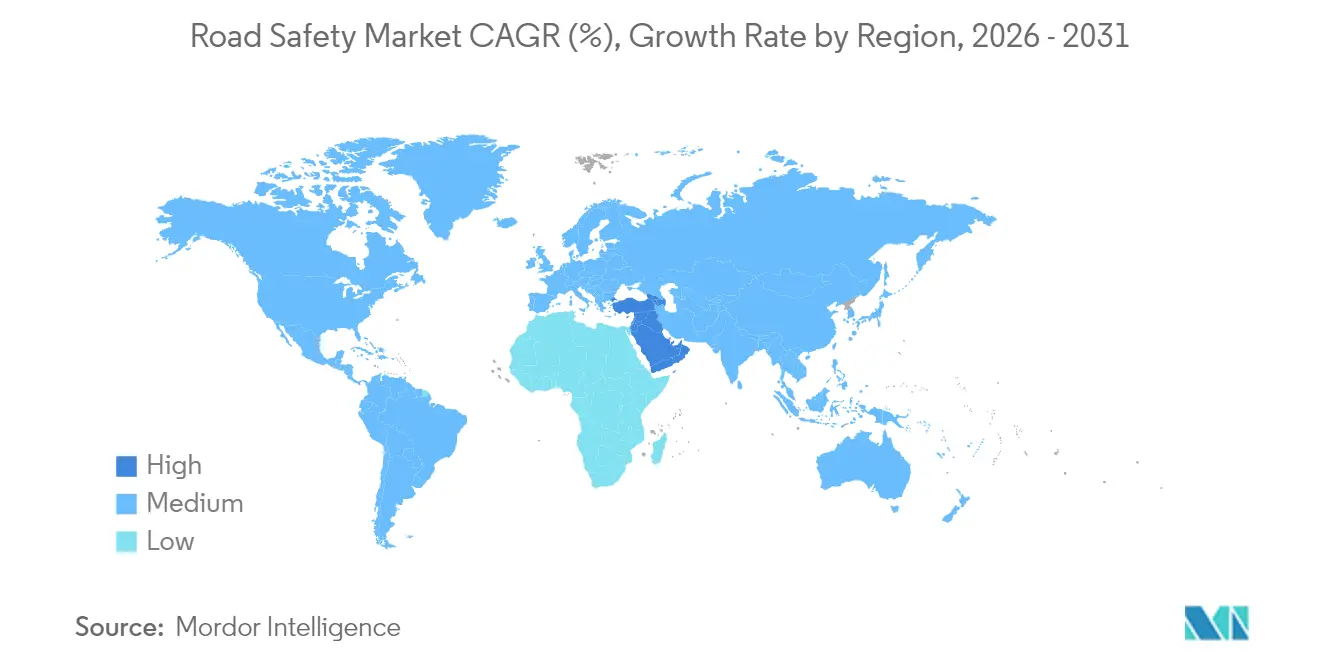

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

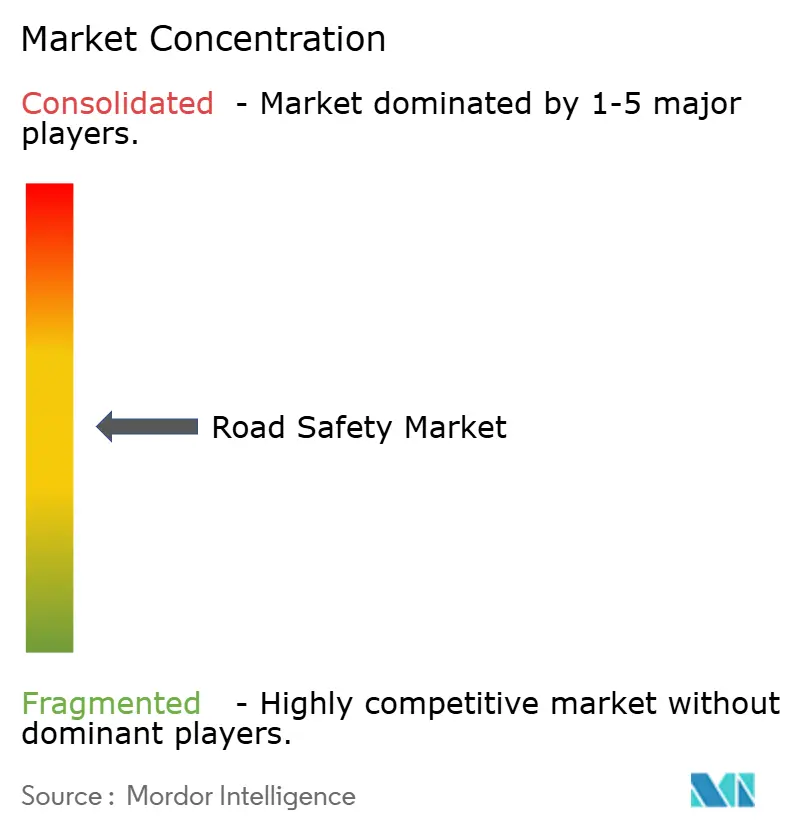

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Road Safety Market Analysis by Mordor Intelligence

The road safety market size is expected to grow from USD 5.14 billion in 2025 to USD 5.71 billion in 2026 and is forecast to reach USD 9.66 billion by 2031 at 11.09% CAGR over 2026-2031. Investments linked to the EU Regulation 2019/2144, Vision Zero programs in the United States, and state-sponsored ITS funds in Asia have created synchronized demand cycles across hardware, software, and services. Red-light and speed-enforcement upgrades remain the revenue backbone, yet corridor-based monitoring, AI analytics, and V2X integration are redefining procurement specifications. North America’s performance-based contracts and Europe’s privacy-centric architectures are shaping vendor strategies, while Middle East smart-city projects and African corridor modernizations broaden the geographic addressable base. Against this backdrop, hardware refreshes are evolving into data-service annuities, tilting competitive advantage toward suppliers that can wrap analytics and compliance modules around deployed assets.

Key Report Takeaways

- By solution, Section/Average-Speed Enforcement is expanding at a 12.35% CAGR through 2031; red-light systems retained 29.65% road safety market share in 2025.

- By component, software captured 10.8% CAGR during 2025-2026, whereas hardware still held 54.85% of the road safety market size in 2025.

- By enforcement type, fixed installations contributed 61.35% of the road safety market size in 2025; mobile/in-vehicle platforms are growing at 12.1% CAGR.

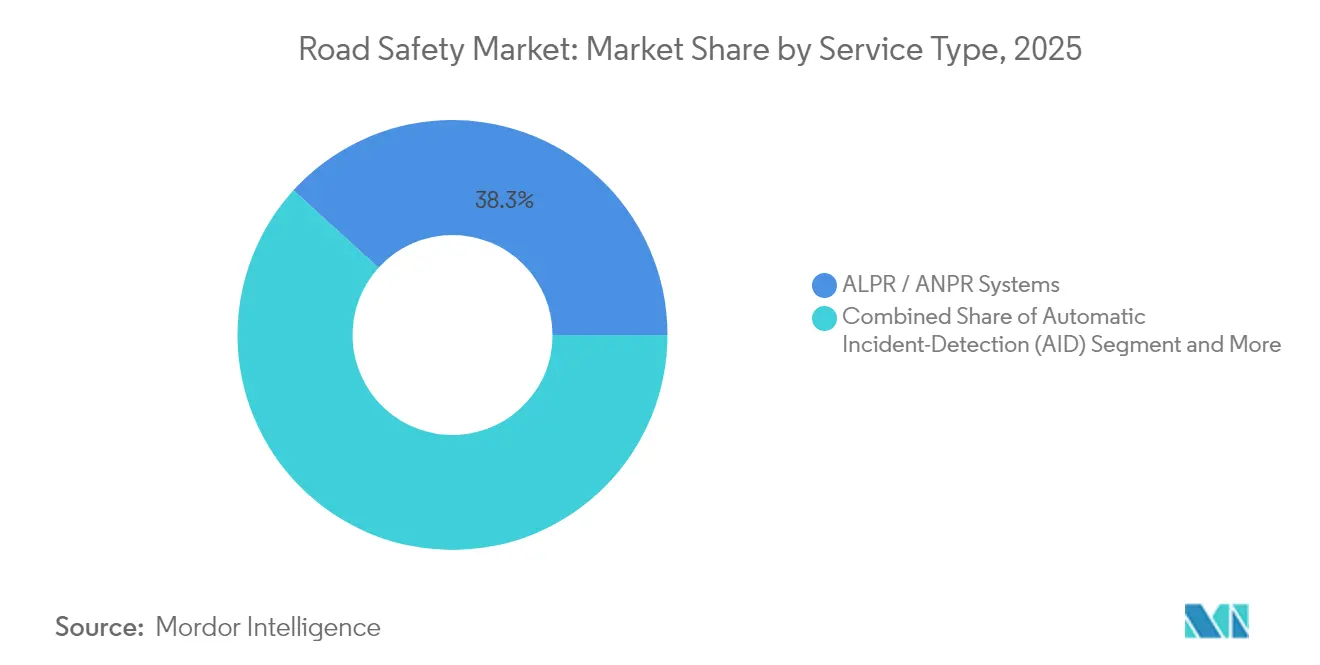

- By system type, ALPR/ANPR solutions commanded 38.25% road safety market share in 2025; automatic incident detection leads growth at 12.75% CAGR.

- By end-user, municipal and urban road authorities accounted for 45.85% of 2025 spend; commercial fleets are advancing at a 12.6% CAGR.

- Geography-wise, North America generated 38.55% of 2025 revenue, while the Middle East and Africa post a 12.3% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Road Safety Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU 2030 enforcement-camera mandates drive equipment refresh | +2.1% | Europe, spillover to North America | Medium term (2-4 years) |

| Vision Zero plans propel U.S. speed-management budgets | +1.8% | United States | Short term (≤ 2 years) |

| China ITS upgrade fund accelerates ANPR rollout | +1.6% | China | Medium term (2-4 years) |

| India Bharatmala II highway safety corridors | +1.4% | India | Long term (≥ 4 years) |

| Smart-city mega-projects adopt AI road-safety analytics | +1.2% | Middle East focus | Medium term (2-4 years) |

| Insurance-telematics partnerships boost video analytics | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU 2030 enforcement-camera mandates drive equipment refresh

Mandatory advanced safety provisions effective July 2024 have forced European municipalities to overhaul legacy cameras and connect them with intelligent speed assistance and emergency-braking systems. Prague’s AI-enabled traffic control rollout by Yunex Traffic shows how enforcement assets migrate toward platform-based, predictive ecosystems.[1]Yunex Traffic, “Prague AI-Enabled Traffic Control System Implementation,” yunextraffic.com Cross-border suppliers have standardized on EU-compliant firmware, pushing similar refresh programs into export markets. Contract structures are shifting from one-off hardware sales to 7- to 10-year managed-service agreements that lock in analytics subscriptions and cybersecurity updates

Vision Zero plans propel U.S. speed-management budgets

The USD 5 billion Safe Streets and Roads for All grant and USD 96 million in advanced technology awards have re-directed city budgets from reactive citation models to data-driven speed management. [2]U.S. Department of Transportation, “USDOT Awards Nearly $60 Million in Advanced Vehicle Technology Grants,” highways.dot.gov Oakland, San Francisco, and New York City have contracted Verra Mobility for turnkey speed-safety programs, specifying performance clauses tied to collision-reduction metrics. This guaranteed outcome model incentivizes vendors to bundle AI analytics, sensor calibration, and cloud evidence management in a single service stack.

China ITS upgrade fund accelerates ANPR rollout

Beijing’s coordinated funding for V2X and ANPR targets the addition of 30 million connected vehicles annually by 2034, establishing a laboratory for predictive violation prevention. Unit economics benefit as domestic production scales, compressing global hardware prices and exporting Chinese protocol standards. Hikvision and Dahua now bid competitively in Latin American and African procurements that historically defaulted to European brands.

India Bharatmala II highway safety corridors

Bharatmala II weaves AI monitoring into greenfield highway construction, proven by Bengaluru’s 165-junction adaptive control network.[3]IndiaAI, “AI and Traffic Control in India: Revolutionizing Road Management,” indiaai.gov.in Embedding safety sensors at the planning stage shortens payback cycles and creates predictable upgrade paths aligned with pavement life-cycle schedules. Vendors able to integrate urban smart-city modules with national corridor projects strengthen cross-domain credibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR and CCPA data-retention limits on enforcement cameras | -1.5% | Europe and North America | Short term (≤ 2 years) |

| High capex for AI multi-sensor systems in LMICs | -1.1% | Asia-Pacific, MEA | Medium term (2-4 years) |

| Litigation push-back on automated speed enforcement | -0.8% | United States, spillover to Europe | Medium term (2-4 years) |

| Cyber-vulnerability in roadside IoT sensors | -0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR and CCPA data-retention limits on enforcement cameras

Meta’s EUR 1.2 billion (USD 1.296 billion) fine in 2025 underscored regulatory willingness to penalize non-compliance. Road safety operators must now build local processing nodes, avoid cross-border evidence storage, and automate deletion routines that sometimes conflict with evidentiary-chain rules. Compliance overhead tilts the playing field toward multinationals with in-house legal, security, and DevSecOps resources.

High capex for AI multi-sensor systems in LMICs

Intersection-level investments of USD 50,000–100,000 exceed tax revenues in many emerging municipalities. Concessional finance and revenue-share models exist but lengthen procurement cycles, delaying safety benefits. Vendors offering modular, upgrade-ready kits can unlock latent demand without compromising forecasting accuracy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Corridor monitoring accelerates safety outcomes

Red-light systems retained a 29.65% road safety market share in 2025, indicating that intersection protection remains foundational to municipal safety strategies. However, the corridor-based approach propelled Section/Average-Speed Enforcement to a 12.35% CAGR, demonstrating that continuous driver behavior modulation outperforms point-specific deterrence. That momentum is reinforced by national speed-harm studies feeding Vision Zero dashboards in the United States and speed-camera networks in France. The road safety market size attached to corridor monitoring is projected to expand faster than legacy intersection programs, incentivizing suppliers to bundle radar, lidar, and ALPR across contiguous segments.

The pivot from reactive ticketing to proactive analytics is reshaping revenue mechanics. Agencies now score bidders on crash-reduction forecasts, demanding configurable AI models that adapt to evolving traffic patterns. Vendors capable of integrating violation, congestion, and green-wave metrics into unified dashboards secure higher recurring fees and longer support contracts, mitigating lump-sum hardware margins.

By Component: Software intelligence transforms asset value

Hardware still dominated 54.85% of the road safety market size in 2025 due to camera, radar, and sensor procurement cycles. Yet software’s 10.8% CAGR signals that analytic layers, not steel and silicon, now dictate competitive differentiation. Cloud-native modules provide real-time edge processing, video redaction for GDPR, and fleet-operator APIs, enabling cities to pivot swiftly when grant stipulations evolve. ISS’s IntelliSection embeds computer-vision algorithms that triage intersection conflicts and recommend optimal phasing without civil-works upgrades.

Services revenue, anchored by 24×7 monitoring and KPI compliance reporting, climbs steadily as agencies outsource upkeep to contain payroll overhead. This services glide path erodes traditional pay-per-citation dependencies and drives multipliers on installed base valuation during M&A due diligence.

By Enforcement Type: Mobile versatility unlocks fleet demand

Fixed cabinets recorded 61.35% of the 2025 deployment value, but fleet-integrated mobile platforms are trending at 12.1% CAGR, mirroring the insurance-telematics driver. Mobile units embedded in police cruisers or commercial vehicles extend enforcement coverage without expensive civil works, and AI object detection eliminates the need for operator judgment. Portable tripod kits remain the entry point for small towns and construction-zone projects where permanent fixtures lack ROI.

Commercial fleets see ROI through lower insurance deductibles and reduced litigation exposure. Verra Mobility’s in-vehicle enforcement suite illustrates how OEM-agnostic sensors and cloud analytics lower installation friction, nudging procurement toward subscription models

By System Type: AI detection elevates situational awareness

ALPR/ANPR platforms held 38.25% road safety market share in 2025, validating plate recognition as a mature baseline for tolling and enforcement. However, AI-driven incident detection is scaling at 12.75% CAGR as agencies deploy computer vision to pre-empt collisions and trigger dynamic lane controls. Currux Vision’s San José rollout outperformed legacy systems by delivering 90%+ violation detection accuracy and real-time alerting.

Variable message signs and intersection-safety cameras increasingly integrate with AI modules that feed alerts into traffic management centers, linking enforcement with flow optimization. Suppliers conversant with both computer-vision pipelines and secure V2X protocols gain a defensible edge as standards coalesce.

By End-User: Private-sector adoption rewrites sales funnels

Municipal and urban road authorities accounted for 45.85% of 2025 spending, but commercial fleets are posting a 12.6% CAGR through 2031. Liability-averse operators install driver-monitoring cameras and forward-collision sensors to unlock premium discounts and mitigate nuclear verdict risks. National highway agencies allocate capital toward corridor programs that sync with tolling and weigh-in-motion upgrades, while toll-road concessionaires embed enforcement within revenue-collection architecture to improve investor IRR profiles.

Vendor roadmaps increasingly feature enterprise-grade APIs and unified asset dashboards, allowing fleet managers to align compliance data with logistics platforms. The resulting stickiness drives multi-year license commitments, converting one-time hardware deals into recurring ARR.

Geography Analysis

North America generated 38.55% of 2025 revenue, buoyed by Vision Zero mandates and USD 60 million worth of federal V2X grants across Arizona, Texas, and Utah highways. The region continues to favor outcome-based procurements, forcing vendors to underwrite performance guarantees and embed continuous-improvement provisions in service-level agreements. Canada’s ITS-focused infrastructure bank and Mexico’s highway modernization targets extend addressable demand, with NAFTA-wide interoperability requirements driving standards harmonization.

Europe’s trajectory remains steady as the 2019/2144 regulation orchestrates synchronized refresh cycles. Privacy and cybersecurity directives are stringent, but they also create export-ready compliance frameworks adopted by Asia and Latin America. Consolidation is accelerating; SWARCO’s Elmore Group purchase and Lacroix bid deepen supply-chain verticalization and broaden software stacks. Eastern Europe benefits from EU-funded smart-mobility corridors, expanding TAM without commensurate competitive intensity.

The Middle East and Africa deliver a 12.3% CAGR, the fastest worldwide. Saudi Arabia’s NEOM blueprint and UAE’s ITS Master Plan roll out smart-city infrastructure unconstrained by legacy assets, letting AI-native platforms leapfrog older systems. African Union safety corridors—such as Kenya’s Road Safety Action Plan—attract blended-finance packages that reduce sovereign debt burden, creating predictable pipelines for mid-tier suppliers.

Competitive Landscape

The road safety industry is moderately fragmented, . Kapsch TrafficCom booked EUR 539 million (USD 582.1 million) revenue and secured a USD 1.4 million Hawaii tunnel contract, capitalizing on referenceability within North America. Jenoptik leverages lidar IP for hybrid lidar-radar cameras, while Sensys Gatso pushes subscription pricing via managed-service contracts. SWARCO’s inorganic push—ten acquisitions since 2022—builds a diversified traffic technology stack spanning controllers, V2X radios, and analytics.

AI-native challengers such as Currux Vision, Omnisight, and Derq differentiate on computer-vision accuracy and cloud-agnostic deployment. Thales’s partnership with Cubic to launch eSIM vehicle connectivity extends aerospace-grade security into roadside domains. Established incumbents respond by embedding AI modules via internal R&D or bolt-on acquisitions and by creating venture funds to accelerate ecosystem participation.

Road Safety Industry Leaders

Kapsch TrafficCom AG

Jenoptik AG

Sensys Gatso Group AB

SWARCO AG

Verra Mobility Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thales and Cubic unveiled eSIM-enabled connected-vehicle solutions, positioning the duo to capture V2X-linked enforcement and authentication revenues.

- February 2025: Siemens Mobility clinched a EUR 2.8 billion (USD 3.024 billion) Deutsche Bahn control-and-safety deal, demonstrating cross-modal platform convergence.

- January 2025: ISS debuted IntelliSection to automate intersection safety analytics, reinforcing software-first differentiation.

Global Road Safety Market Report Scope

The road safety market relates to the safety and protection of passengers, vehicles, drivers, and pedestrians while driving. The study covers important market parameters, underlying growth influencers, and major industry vendors that support road safety market estimations and growth rates during the forecast period. The research examines COVID-19's overall impact on the road safety system market.

The road safety market is segmented by solution (red light enforcement, speed enforcement, bus lane enforcement, and section enforcement, automatic license plate recognition/automatic number plate recognition (ALPR/ANPR), incident detection and response), by services (consulting, support, and maintenance, integration and deployment), and by geography.

| Red-Light Enforcement |

| Speed Enforcement |

| Section / Average-Speed Enforcement |

| Bus-Lane Enforcement |

| Incident Detection and Response |

| Hardware |

| Software |

| Services |

| Fixed Systems |

| Mobile / In-Vehicle Systems |

| Portable / Tripod Systems |

| ALPR / ANPR Systems |

| Automatic Incident-Detection (AID) |

| Intersection-Safety Cameras |

| Variable Message / Warning Signs |

| Municipal and Urban Road Authorities |

| National Highway Agencies |

| Law-Enforcement and Police Departments |

| Toll-Road / Concession Operators |

| Commercial Fleet Operators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Solution | Red-Light Enforcement | ||

| Speed Enforcement | |||

| Section / Average-Speed Enforcement | |||

| Bus-Lane Enforcement | |||

| Incident Detection and Response | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Enforcement Type | Fixed Systems | ||

| Mobile / In-Vehicle Systems | |||

| Portable / Tripod Systems | |||

| By System Type | ALPR / ANPR Systems | ||

| Automatic Incident-Detection (AID) | |||

| Intersection-Safety Cameras | |||

| Variable Message / Warning Signs | |||

| By End-User | Municipal and Urban Road Authorities | ||

| National Highway Agencies | |||

| Law-Enforcement and Police Departments | |||

| Toll-Road / Concession Operators | |||

| Commercial Fleet Operators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the road safety market and how fast is it growing?

The market is worth USD 5.71 billion in 2026 and is forecast to expand to USD 9.66 billion by 2031, reflecting an 11.09% CAGR.

Which geographic region leads road-safety spending today?

North America holds 38.55% of global revenue, supported by Vision Zero programs and federal V2X grants.

Which solution category is expanding the fastest?

Section/Average-Speed Enforcement systems post a 12.35% CAGR through 2031 as agencies shift toward corridor-based monitoring.

How important is software in future procurement cycles?

Software revenues are growing at 10.8% CAGR, signaling a pivot from camera hardware to AI-driven analytics subscriptions.

Page last updated on: