Rail Asset Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

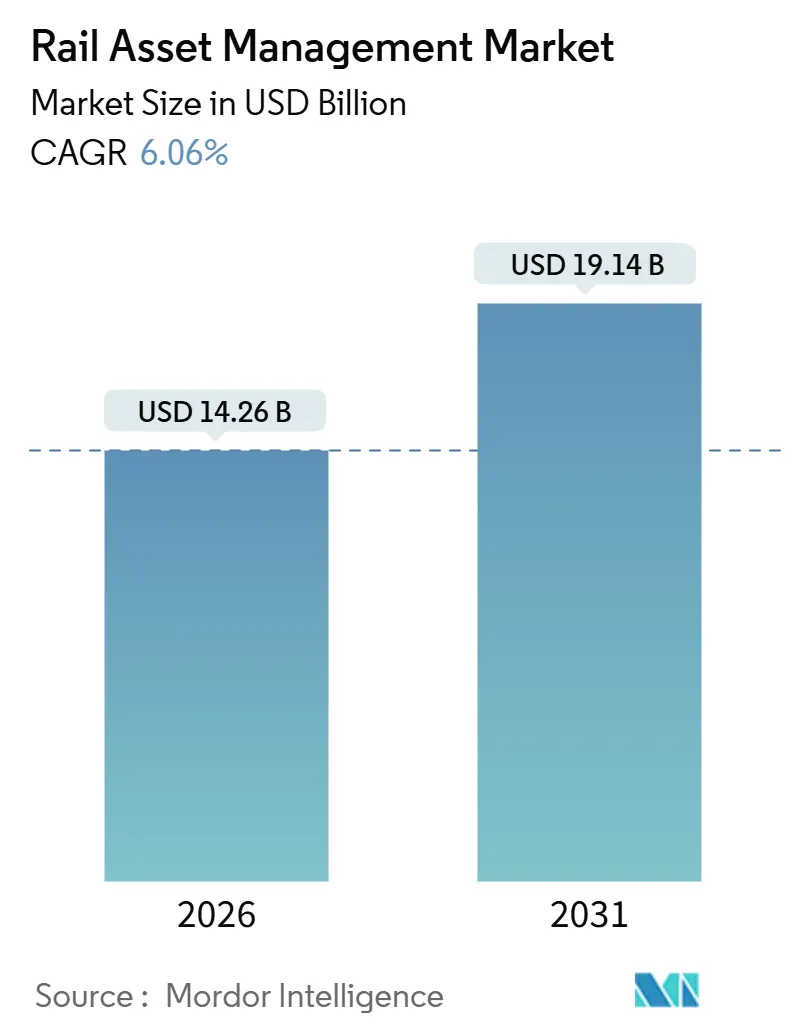

| Market Size (2026) | USD 14.26 Billion |

| Market Size (2031) | USD 19.14 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

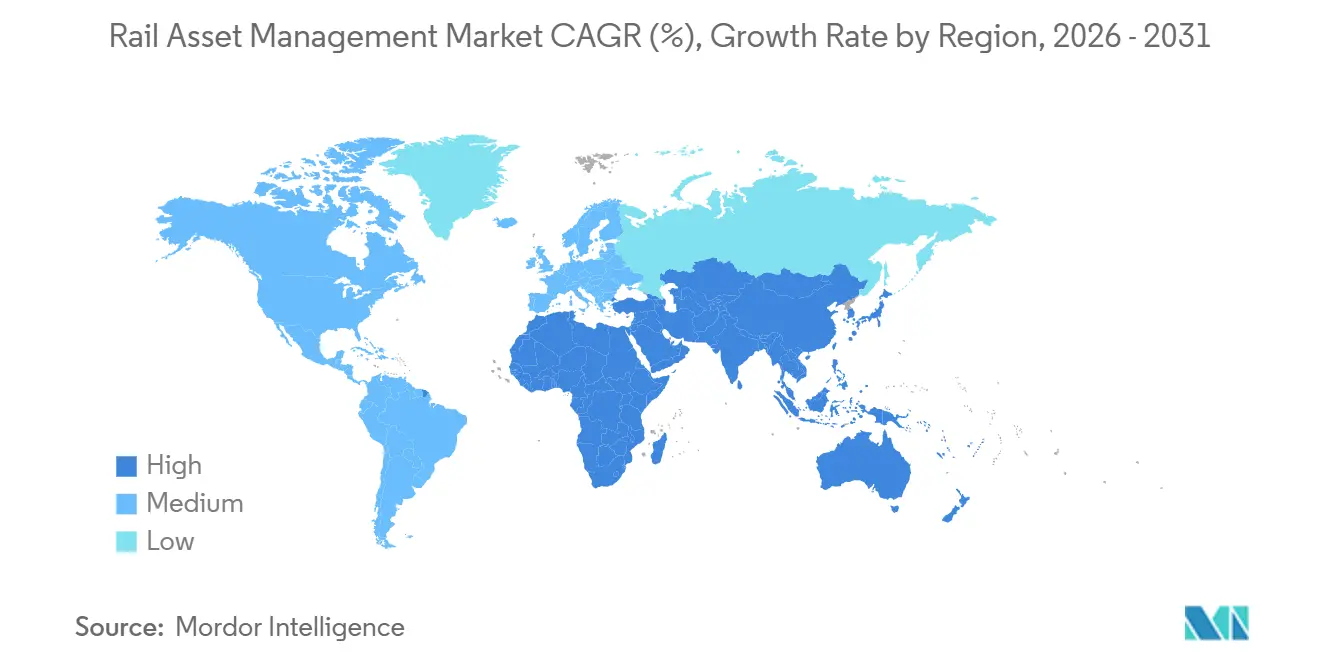

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

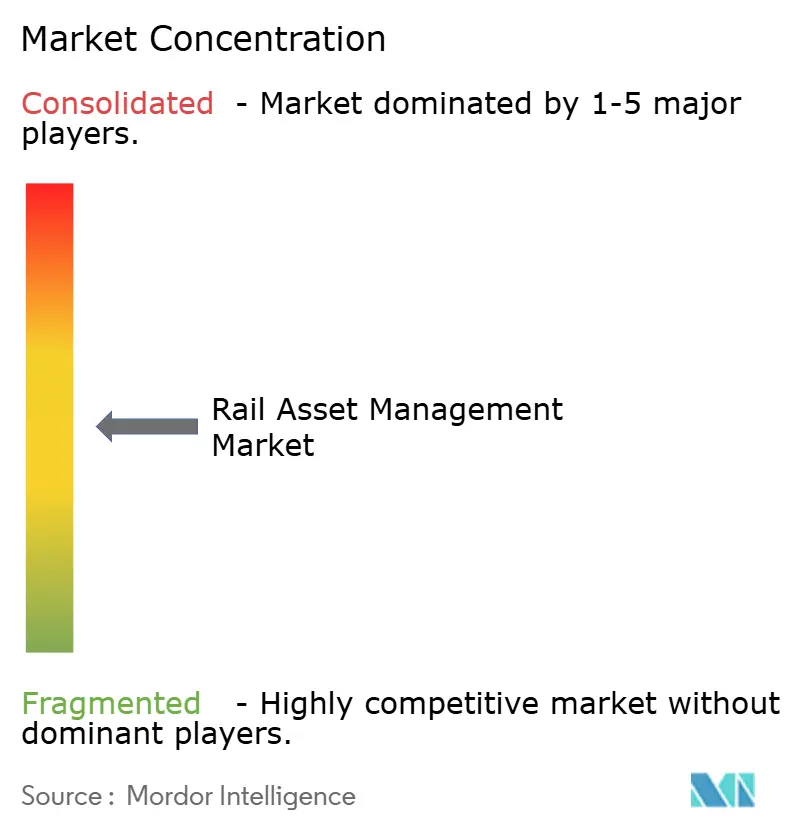

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rail Asset Management Market Analysis by Mordor Intelligence

The rail asset management market size is valued at USD 14.26 billion in 2026 and is projected to reach USD 19.14 billion by 2031, advancing at a 6.06% CAGR across the forecast window. This healthy trajectory reflects a decisive shift from reactive repair to data-driven lifecycle optimization that lowers unplanned downtime, stretches capital budgets, and improves schedule adherence. Large railroads and metro operators are expanding pilot programs that combine IoT sensors, machine-learning diagnostics, and digital twin models, while governments are linking funding eligibility to formal asset-management plans. Competitive intensity is building as rolling-stock OEMs bundle software with equipment deliveries and enterprise IT vendors press their way into the procurement cycle. In parallel, managed-service providers are scaling outcome-based contracts that appeal to mid-sized operators unable to recruit rail-savvy data scientists. Cyber-security mandates, climate-resilience criteria, and talent shortages complicate adoption, yet evidence from early movers shows that predictive analytics can cut delay minutes, derailment risk, and maintenance spend enough to justify investment.

Key Report Takeaways

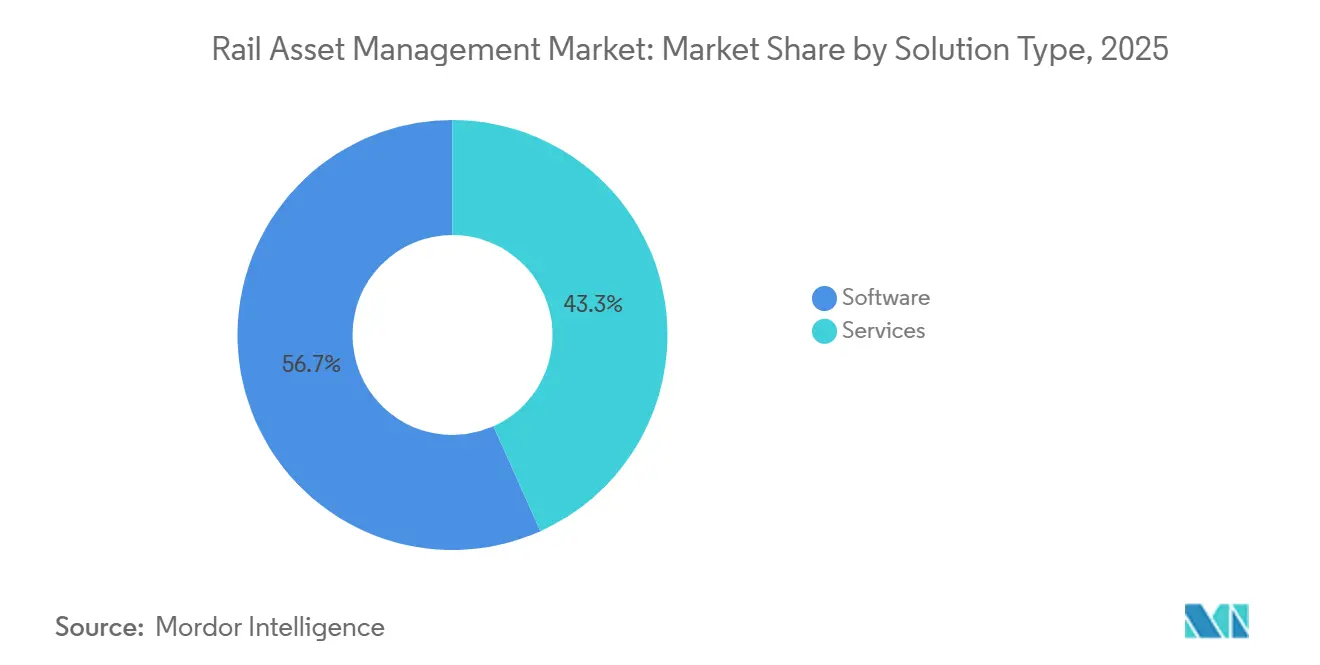

- By solution type, software platforms led with 56.71% revenue share in 2025, while services are forecast to expand at a 6.23% CAGR through 2031.

- By deployment, on-premises installations held a 63.13% share in 2025, whereas cloud solutions are projected to grow at a 6.29% CAGR to 2031.

- By asset type, rolling stock accounted for 66.89% of the rail asset management market share in 2025, while infrastructure assets are expected to grow at a 6.33% CAGR over the forecast period.

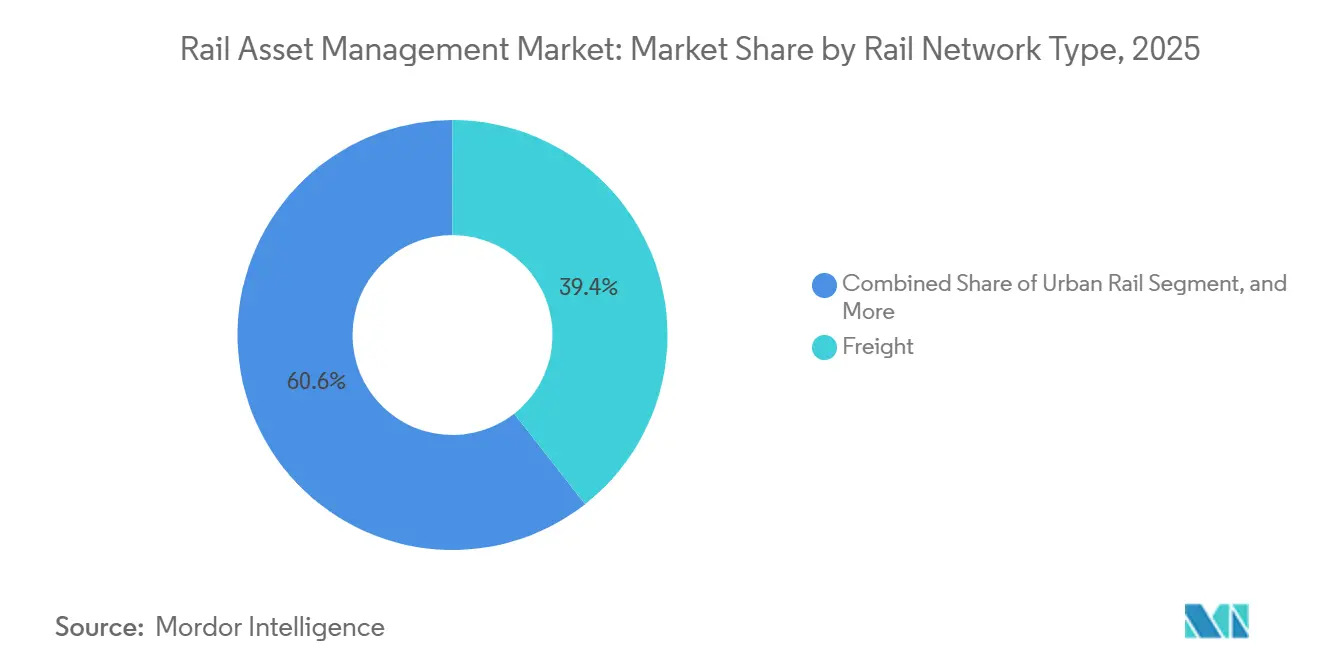

- By rail network type, freight networks commanded a 39.41% share in 2025, whereas urban rail is poised for the fastest rise at a 6.51% CAGR through 2031.

- By end-user, rail operators captured 72.78% of 2025 expenditure, while infrastructure maintenance contractors are projected to register the highest CAGR of 6.78%.

- By geography, Asia-Pacific dominated with 38.27% revenue share in 2025, while the Middle East is set to log the quickest regional expansion at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rail Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Effective Rail Operations | +1.2% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Increase in Government Initiatives and Public-Private Partnerships | +0.9% | Middle East, South America, Asia-Pacific | Long term (≥ 4 years) |

| Rapid Urbanization in Developing Countries | +0.8% | Asia-Pacific, Middle East, Africa | Long term (≥ 4 years) |

| Adoption of Condition-Based and Predictive Maintenance Analytics | +1.3% | Global, early adoption in Europe and North America | Short term (≤ 2 years) |

| Digital Twin Integration for Lifecycle Cost Optimization | +1.0% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Climate-Resilient Rail Infrastructure Investments | +0.7% | Europe, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of Condition-Based and Predictive Maintenance Analytics

Railroads and metro systems are shifting from fixed-interval overhauls to sensor-guided interventions that spot faults weeks in advance, trimming work orders and letting crews plan outages when capacity is available.[1]Swiss Federal Railways, “Track Defect Reduction Through Acoustic Sensors,” sbb.ch Swiss Federal Railways logged a 68% drop in track defects and a 21% cut in maintenance tasks after instrumenting 1,200 km of mainline with acoustic and vibration sensors in 2024. BNSF Railway used wheel-impact data and thermal imaging to flag 12,000 railcar defects in 2025, avoiding an estimated USD 45 million in derailment costs. Falling hardware prices mean industrial IoT nodes now sell for under USD 150, making it economical to monitor secondary lines and mid-life rolling stock, broadening the addressable fleet. Public grant programs increasingly reward proposals that embed predictive analytics, accelerating diffusion across both freight and passenger operators.

Growing Demand for Effective Rail Operations

Passenger ridership and freight volumes rebounded in 2025, pushing operators to raise on-time performance and asset utilization targets.[2]Deutsche Bahn, “AI-Driven Predictive Maintenance Reduces Delays,” deutschebahn.com Deutsche Bahn applied AI diagnostics across 33,000 km of network and cut delay minutes by 20% in the same year. Union Pacific’s digital twin of wheel bearings and rail joints deferred USD 200 million in unscheduled locomotive work, demonstrating how maintenance analytics directly drive financial upside. A derailment still costs USD 1-3 million in track repairs, cargo claims, and fines, so executives now link bonuses to asset-reliability metrics. As performance stakes climb, predictive maintenance moves from tactical pilot to core operating discipline across long-haul freight, high-speed passenger, and metro lines.

Digital Twin Integration for Lifecycle Cost Optimization

Virtual replicas of bridges, tunnels, rolling stock, and power assets let engineers test degradation scenarios without interrupting service, driving measurable savings. Network Rail’s Control Period 7 budget funds digital twins for 20,000 bridges and 40,000 switches, aiming to shave inspection time and extend asset life. Siemens Mobility’s Railigent couples live sensor feeds with simulation models and has reduced track possession windows by up to 15% for European clients. The U.K. Department for Transport found operators can capture 10-15% lifecycle savings when digital twins connect procurement, inventory, and scheduling systems. Hitachi’s 2025 purchase of Thales’ ground-transport unit merges IoT analytics with signaling expertise, expanding twin capabilities into new regions.[3]Hitachi Rail, “Lumada Integration Post-Acquisition,” hitachirail.com

Increase in Government Initiatives and Public-Private Partnerships

Mega-projects in the Middle East, North America, and Asia-Pacific now require formal asset-management plans as a funding precondition, ensuring steady demand for software and services. Saudi Arabia’s USD 22.5 billion Riyadh Metro and the UAE’s USD 11 billion Etihad Rail backbone both bundled predictive-maintenance platforms into initial contracts. The U.S. Federal Railroad Administration earmarked USD 8 billion from its broader rail allocation for digital inspection and asset-health technologies, boosting adoption among intercity and commuter operators. Brazil’s privatization wave builds condition-based maintenance benchmarks into lease tenders, rewarding bidders that commit to sensor coverage and analytics reporting. Such policies lower technology risk perceptions and shorten payback periods, especially for mid-sized or publicly funded railroads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Deployment Costs | -0.8% | Global, acute in South America and Africa | Short term (≤ 2 years) |

| Difficulties with Legacy Infrastructure Integration | -0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Cyber-security and Data-Privacy Concerns in Connected Rail Assets | -0.7% | Global, heightened in North America and Europe | Short term (≤ 2 years) |

| Shortage of Rail-Specific Data Science Talent | -0.5% | Global, severe in Australia and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Deployment Costs

Retrofitting 1,000 km of mainline with sensors, edge compute, and communications can demand USD 15-25 million before licenses and integration, a hurdle for agencies with tight capital envelopes. Argentina paused a USD 120 million upgrade in 2024, opting for incremental pilots on high-traffic corridors because full funding was unavailable. Smaller U.S. regional railroads account for 40% of network mileage but only 10% of revenue, making it hard to amortize fixed costs without outside assistance. Contractors such as SNC-Lavalin pool assets across multiple clients to cut per-operator software fees by 60%, but some markets still await subsidy reform to unlock larger programs. Until costs fall further or financing models evolve, deployment pace will vary widely by region and operator size.

Cyber-Security and Data-Privacy Concerns in Connected Rail Assets

The European Union Agency for Railways logged a 220% rise in cyber incidents against operators between 2020 and 2024, spanning ransomware and denial-of-service attacks on ticketing and control networks. U.S. TSA Directive 1580-21-01 obliges freight and high-risk passenger carriers to report incidents within 24 hours and keep recovery plans current, adding compliance costs that can exceed USD 5 million annually for mid-sized railroads. Recommended safeguards, such as network segmentation, data encryption, and routine penetration testing, increase total ownership costs by 10-15% for connected asset-management systems. Operators in Europe must also anonymize location data to satisfy GDPR, complicating algorithms that rely on granular tracking for predictive accuracy. These factors elevate security credentials to a primary vendor-selection criterion and occasionally delay rollouts until in-house teams or partners can guarantee compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Services Gain as Implementation Complexity Rises

Spending on software platforms accounted for 56.71% of the rail asset management market in 2025, underlining the foundational role of enterprise asset management suites, computerized maintenance systems, and digital twins. Services consulting, integration, managed analytics, and training, however, are expected to register a 6.23% CAGR and steadily narrow the gap. Complex integrations that link IoT sensors with legacy supervisory control systems, enterprise resource planning systems, and geospatial databases require specialized domain knowledge that few operators retain in-house. A typical IBM Maximo rollout tailored for rail operations runs 18 months and costs USD 10-20 million in professional services before the first algorithm reaches production. Similar patterns are evident in Europe and the Asia-Pacific with SAP S/4HANA.

Rising complexity pushes railroads and transit authorities to outsource risk. Capgemini reported a 35% jump in its rail digitalization backlog during 2025 as operators leaned on systems integrators to conduct data cleansing, model calibration, and crew change-management programs. Managed-service contracts, such as Accenture’s analytics-as-a-service offering for three European metros, shift expenditure from capex to opex, tying payments to uptime or cost-reduction targets. This structure appeals to mid-sized agencies facing talent shortages and rigorous performance targets, ensuring that the rail asset management market continues to tilt toward service-rich engagements.

By Deployment: Cloud Gains Traction Despite Security Concerns

On-premises solutions represented 63.13% of global spend in 2025, a legacy preference rooted in direct system control and perceived regulatory certainty. Cloud solutions are projected to grow 6.29% per year as hyperscalers demonstrate lower total cost of ownership and faster upgrade cycles. A 2024 AWS case study showed that operators shifting asset-management workloads to the cloud realized 31% lower operating costs, 45% fewer security incidents, and a 54% drop in outages compared with similar on-premises estates. Hybrid architectures are emerging as a middle ground: Network Rail keeps mission-critical signaling data on private servers while running asset-health analytics on Microsoft Azure to meet U.K. security standards.

Despite benefits, migration hesitancy persists where national cyber agencies impose stringent certification hurdles. New guidance from the European Union Agency for Railways in 2024 clarifies encryption and segmentation requirements, removing some uncertainty but adding overhead. Smaller operators with limited capital favor fully managed, cloud-native platforms that provide built-in disaster recovery and globe-spanning redundancy. As reference deployments expand, decision makers increasingly weigh the productivity boost against the incremental security measures now regarded as standard practice.

By Asset Type: Infrastructure Gains as Track and Signaling Digitalize

Rolling stock accounted for 66.89% of 2025 outlays, reflecting the high ticket price of locomotives, coaches, and railcars, as well as their visibility to passengers and shippers. Infrastructure assets, including bridges, tunnels, signaling, and electrification, are forecast to notch a 6.33% CAGR as operators confront systemic risk tied to aging civil works. A 2024 report by the U.K. Rail Safety and Standards Board found that track faults accounted for 42% of service disruptions but received only 28% of maintenance budgets. Deutsche Bahn reacted by allocating EUR 3.2 billion (USD 3.62 billion) to digital inspections of switches and catenary in 2025, up 40% year-on-year.

Sensors that detect acoustic anomalies, ground-penetrating radar that maps ballast voids, and drones that survey bridge corrosion now complement traditional geometry cars. Signaling modernization reinforces the trend: communications-based train control embeds self-diagnostic features that feed asset-health dashboards in real time. Electrification programs aimed at decarbonization add substations, feeders, and wayside batteries, all of which require monitoring. Collectively, these shifts close the historical budget gap between rolling stock and infrastructure, sustaining infrastructure’s faster growth lane in the rail asset management market.

By Rail Network Type: Urban Rail Surges on Metro Expansions

Freight networks produced the lion’s share of revenue, 39.41% in 2025, on sheer asset-mass and route-mile exposure. Urban rail, however, is slated to record a 6.51% CAGR, the swiftest among network types, as megacities tackle congestion and air-quality mandates. India extended metro corridors from 700 km in 2020 to 1,100 km in 2025, embedding predictive maintenance into new rolling stock and traction power at the tender stage. Riyadh Metro launched 176 km of fully automated lines in 2024 with Siemens and Alstom platforms monitoring 470 trains and 85 stations from day one.

High-speed and intercity passenger services occupy the middle ground, benefiting from government subsidies tied to safety metrics. Freight railroads, although cash generative, must justify technology spending against tight operating ratios; they prioritize projects with payback periods of under 3 years. Urban rail agencies, often publicly owned, accept longer payback horizons because service reliability directly influences economic output. This dichotomy underpins divergent growth arcs inside the rail asset management market.

By End-User: Maintenance Contractors Emerge as Growth Leaders

Rail operators accounted for 72.78% of 2025 spending through asset ownership and regulatory accountability. Infrastructure maintenance contractors are on course for the fastest expansion, growing at a 6.78% CAGR as agencies outsource condition-based maintenance. SNC-Lavalin rolled out a shared asset-management platform in 2024 that now serves 12 clients, trimming per-operator software charges by 60%. Contractors gain economies of scale in sensor procurement and data-science staffing that single operators struggle to replicate.

Government transport authorities require standardized reporting under rules such as the U.S. Transit Asset Management regulation, pulling in software capable of aggregating multi-operator feeds. Rolling-stock leasing firms, notably GATX, are installing telemetry across thousands of cars to protect residual values and offer value-added services. Together, these shifts diversify the buying centers in the rail asset management market, compelling vendors to tailor their commercial models to each stakeholder tier.

Geography Analysis

Asia-Pacific held 38.27% of the rail asset management market in 2025, anchored by China’s CNY 80 billion (USD 11.2 billion) push for smart railways under the 14th Five-Year Plan and India’s surge in metro mileage across 20 cities. East Japan Railway applied digital twins to its Shinkansen fleet in 2025, lowering unscheduled maintenance by 18% and extending overhaul intervals to 1.8 million km. Australia, facing a shortfall of 16,590 rail workers by 2032, accelerated the adoption of automated inspection drones to mitigate labor risk.

The Middle East is forecast to post the fastest regional CAGR of 7.11% through 2031. Saudi Arabia’s USD 22.5 billion Riyadh Metro and the UAE’s USD 11 billion Etihad Rail backbone embed Siemens Railigent and Alstom HealthHub systems, ensuring predictive maintenance from day one. Gulf Cooperation Council plans to link 2,200 km of cross-border track by 2030, all designed with twin-ready BIM models, thereby sidestepping costly retrofits.

North America is in consolidation mode following Union Pacific’s USD 85 billion takeover of Norfolk Southern in July 2025, creating a 50,000-mile transcontinental carrier committed to standardizing digital twins across its estate. U.S. federal infrastructure appropriations allocate USD 66 billion to passenger rail, including USD 8 billion earmarked for asset-management technology. Canada awarded a CAD 3.9 billion (USD 3.04 billion) design-build-maintain package for a Toronto-Montreal high-speed line, which locks in a 30-year service agreement, illustrating the growing prevalence of contracts that bundle construction with lifecycle oversight.

Europe’s mature networks funnel money toward optimization and climate resilience rather than raw expansion. Deutsche Bahn plans to spend EUR 22.15 billion on infrastructure in 2025, with EUR 3.62 billion allocated to digital condition monitoring, up 40% from 2024 allocations. Network Rail’s GBP 55.63 billion Control Period 7 budget likewise prioritizes digital twins and inspection automation. South America and Africa remain nascent markets: fiscal stress delayed Argentina’s USD 120 million system upgrade, while South Africa and Egypt continue to rely on time-based maintenance, offering white space for vendors as macro conditions improve.

Competitive Landscape

The rail asset management market features moderate concentration: the ten largest suppliers accounted for roughly 55-60% of 2025 revenue, yet rivalry is sharpening as incumbents and newcomers converge on the same digital opportunity. Siemens Mobility, Alstom, Hitachi Rail, and Wabtec leverage installed fleets and signaling footprints to lock clients into end-to-end ecosystems that package sensors, software, and services. IBM, SAP, and Cisco position themselves as vendor-agnostic integrators, appealing to operators wary of proprietary lock-in and keen on multi-vendor interoperability.

Vertical integration continues to reshape vendor maps. Hitachi Rail closed its purchase of Thales’ ground transportation unit in May 2025, merging Lumada IoT analytics with mission-critical signaling to deliver a full-stack proposition. Siemens and Alstom announced plans to merge rail operations in January 2025, a deal that, pending approvals, would combine the Railigent and HealthHub platforms into a unified suite with annual revenue exceeding EUR 33.9 billion (USD 33.9 billion). Patent filings on AI-based diagnostics and digital twin engines are accelerating; Siemens, Alstom, and Wabtec lodged 120 rail-specific AI patents between 2024 and 2025, signaling intent to erect IP barriers.

Smaller disruptors fill gaps with modular, low-cost offerings. KONUX sells plug-and-play sensor kits for under USD 10,000 per turnout segment, enabling operators without deep IT budgets to pilot predictive maintenance. Eke-Electronics and Beena Vision focus on niche applications such as smart HVAC monitoring and automated wheel inspection, often out-innovating larger rivals on cycle time. Managed-service providers, typified by Capgemini and Accenture, are capturing a growing slice of contract value by wrapping cloud hosting, data analytics, and performance guarantees around third-party platforms. This mosaic keeps pricing keen and fuels rapid capability upgrades, ensuring that competitive stakes remain high through the outlook period.

Rail Asset Management Industry Leaders

Siemens AG

Hitachi Ltd.

IBM Corporation

SAP SE

Huawei Technologies Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Union Pacific completed its USD 85 billion acquisition of Norfolk Southern, creating the first coast-to-coast Class I freight railroad in the United States with projected USD 2.75 billion in annual synergies.

- May 2025: GATX and Brookfield finalized a USD 4.4 billion joint venture to purchase about 105,000 railcars from Wells Fargo Rail, accelerating telematics deployment across the fleet.

- May 2025: Hitachi Rail closed its acquisition of Thales’ ground transportation business, combining Lumada analytics with advanced signaling to form a full-stack asset-management suite.

- February 2025: Canada awarded a CAD 3.9 billion (USD 3.04 billion) design-build-maintain contract for the Toronto–Ottawa–Montreal high-speed corridor to a Siemens Mobility and SNC-Lavalin consortium, including a 30-year asset-management commitment.

Global Rail Asset Management Market Report Scope

The Rail Asset Management Market Report is Segmented by Solution Type (Software, and Services), Deployment (On-Premises, and Cloud), Asset Type (Rolling Stock, and Infrastructure), Rail Network Type (Urban Rail, Mainline Passenger, Freight), End-User (Rail Operators, Government Transport Agencies, Infrastructure Maintenance Contractors, Rolling Stock Leasing Firms), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-Premises |

| Cloud |

| Rolling Stock |

| Infrastructure |

| Urban Rail |

| Mainline Passenger |

| Freight |

| Rail Operators |

| Government Transport Agencies |

| Infrastructure Maintenance Contractors |

| Rolling Stock Leasing Firms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Solution Type | Software | ||

| Services | |||

| By Deployment | On-Premises | ||

| Cloud | |||

| By Asset Type | Rolling Stock | ||

| Infrastructure | |||

| By Rail Network Type | Urban Rail | ||

| Mainline Passenger | |||

| Freight | |||

| By End-User | Rail Operators | ||

| Government Transport Agencies | |||

| Infrastructure Maintenance Contractors | |||

| Rolling Stock Leasing Firms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value and projected growth of the rail asset management market?

The rail asset management market size stands at USD 14.26 billion in 2026 and is forecast to reach USD 19.14 billion by 2031, translating into a 6.06% CAGR.

Which solution category is expanding the fastest?

Services, covering consulting, integration, and managed analytics, are expected to grow at a 6.23% CAGR as operators seek external expertise to handle complex deployments.

Why are urban rail systems adopting asset-management technology rapidly?

Metro operators prioritize reliability and headway optimization; predictive maintenance enables sub-90-second intervals and reduces passenger disruptions, supporting a 6.51% CAGR for urban rail.

How are cloud deployments influencing cost structures?

Operators migrating to cloud platforms have recorded 31% lower total cost of ownership and fewer outages, prompting a regional pivot toward hybrid or full cloud implementations.

What role do maintenance contractors play in market growth?

Outsourcing to specialized contractors allows public agencies to spread sensor and analytics costs across multiple clients, driving a 6.78% CAGR in contractor spending.

Which region is expected to grow the quickest through 2031?

The Middle East leads with a projected 7.11% CAGR, underpinned by mega-projects such as Riyadh Metro and Etihad Rail that embed digital asset-management from inception.

Page last updated on: