Market Overview

| Study Period | 2021 - 2031 |

|---|---|

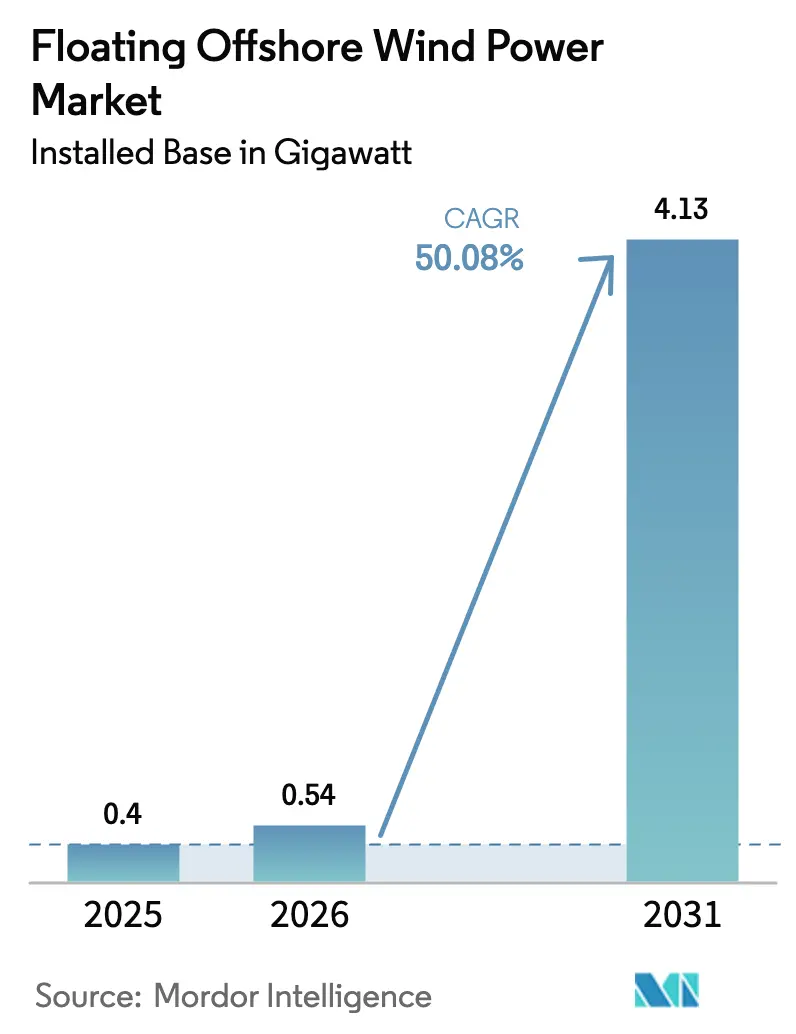

| Market Volume (2026) | 0.54 gigawatt |

| Market Volume (2031) | 4.13 gigawatt |

| Growth Rate (2026 - 2031) | 50.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Floating Offshore Wind Power Market Analysis by Mordor Intelligence

The Floating Offshore Wind Power Market size in terms of installed base is projected to expand from 0.4 gigawatt in 2025 and 0.54 gigawatt in 2026 to 4.13 gigawatt by 2031, registering a CAGR of 50.08% between 2026 to 2031.

This growth comes from the transition into deep-water zones that hold roughly 80% of global offshore wind potential and from continuous turbine upsizing that lowers the levelized cost of energy. Transitional depths of 30-60 m still dominate installations, yet ultra-deep sites beyond 60 m are accelerating as regulators unlock leases off California, Japan, and South Korea. Semi-submersible platforms maintain the lead because they suit modular fabrication, while Spar-buoy concepts advance quickly as Asian yards perfect steel-intensive hulls for typhoon conditions. Reforms to contracts for difference (CfDs) in the United Kingdom and France increase bankability, and national hydrogen roadmaps enhance revenue certainty by pairing electricity sales with green-hydrogen offtake. At the same time, shortages of installation vessels and dynamic-cable reliability issues pressure near-term schedules and margins.

Key Report Takeaways

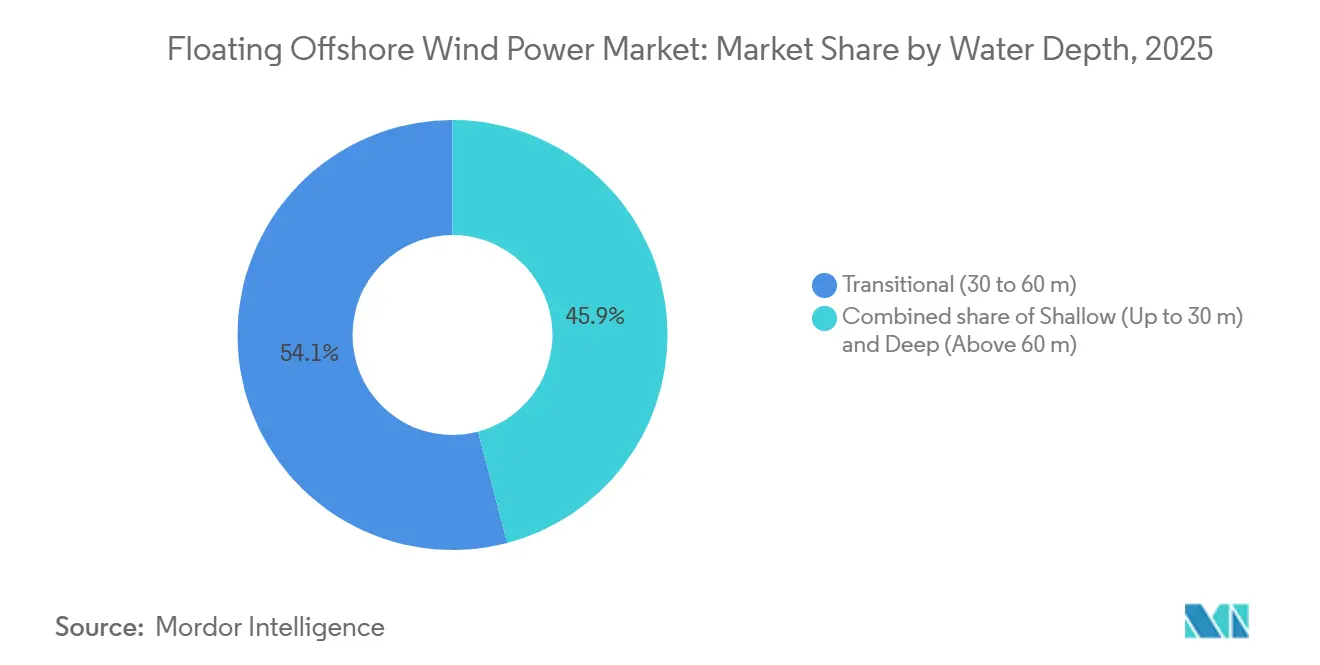

- By water depth, Transitional depths captured 54.1% share in 2025; Deep-water zones above 60 m are forecasted to have a 58.2% CAGR through 2031.

- By platform type, semi-submersibles held 55.8% of the Floating Offshore Wind Power market share in 2025, while Spar-buoy designs are pacing at a 55.3% CAGR to 2031.

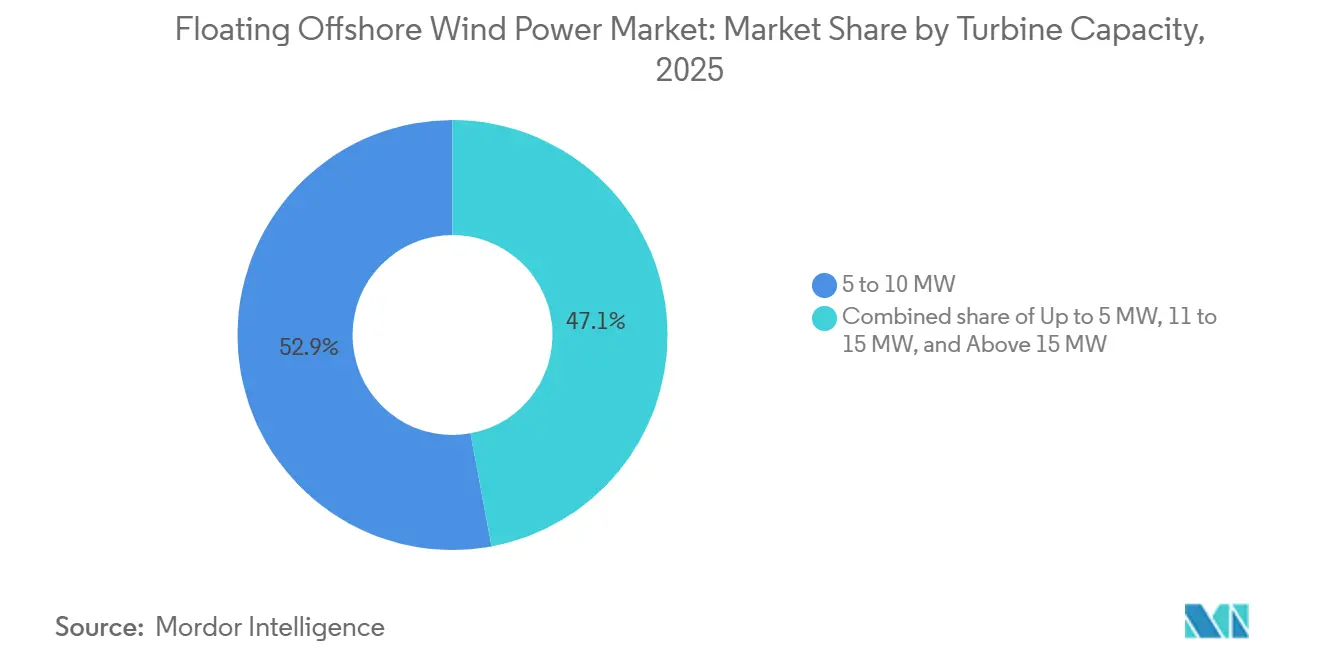

- By turbine class, 5-10 MW machines accounted for 52.9% of the Floating Offshore Wind Power market in 2025; units above 15 MW are advancing at a 56.1% CAGR through 2031.

- By the application stage, pre-commercial pilots dominated 65.3% of capacity in 2025, whereas commercial utility-scale arrays are poised for a 61.5% CAGR to 2031.

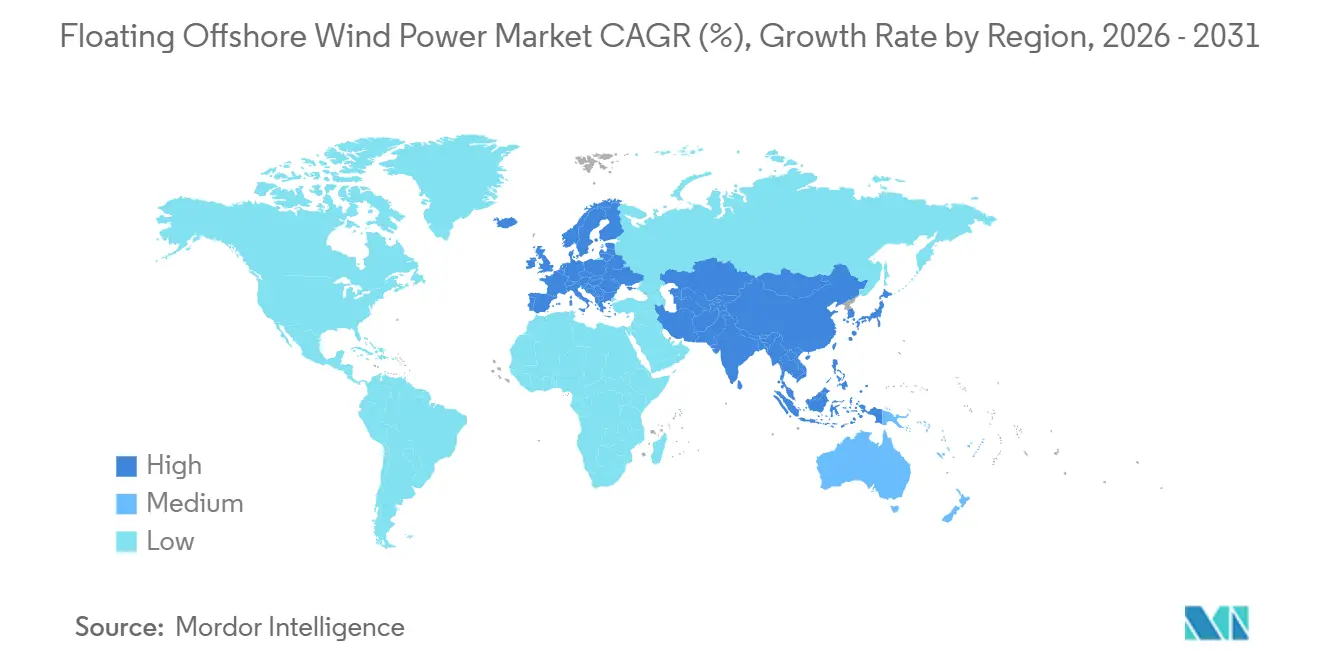

- By geography, Europe retained 53.6% capacity in 2025; Asia-Pacific is the fastest region, tracking a 53.3% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Floating Offshore Wind Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Lease Awards in U.S. & APAC Deep-Water Zones | 8.5% | North America (California, Oregon, Gulf of Mexico), Asia-Pacific (Japan, South Korea, Taiwan, China) | Medium term (2-4 years) |

| Rapid Turbine Upsizing to 15-20 MW Class Reducing LCOE | 9.2% | Global, with early adoption in Europe (UK, Norway) and Asia-Pacific (China, Japan) | Short term (≤ 2 years) |

| Oil & Gas Platform Conversions Unlocking Gulf of Mexico Supply Chain | 6.8% | North America (Gulf of Mexico), with spillover to Brazil and West Africa | Medium term (2-4 years) |

| EU & UK CfD Reform Boosting Bankability | 7.5% | Europe (UK, France, Spain, Italy, Nordic countries) | Short term (≤ 2 years) |

| National Hydrogen Roadmaps Creating Co-location Demand | 5.3% | Europe (Germany, Netherlands, Norway), Asia-Pacific (Japan, South Korea, Australia) | Long term (≥ 4 years) |

| Asian Cable-Vessel Build-out Shortening Installation Schedules | 4.9% | Asia-Pacific core (China, Japan, South Korea), with spillover to Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Lease Awards in U.S. & APAC Deep-Water Zones

The Bureau of Ocean Energy Management’s award of 4.6 GW of leases off California and Oregon in 2024 moved investment toward mooring systems able to withstand 1,200 m depths and seismic loads. Japan’s Ministry of Economy, Trade and Industry followed with 1.8 GW of Round 2 zones that impose typhoon-resilient design and 40% local-content rules.[1]Ministry of Economy Trade and Industry, “Round 2 Offshore Wind Bid Results,” meti.go.jp South Korea’s 8th power-supply plan sets a 6 GW floating target for 2030, steering capital to Ulsan and Jeju, where 150-m depths preclude monopiles. Taiwan’s 2026 allocation earmarks 3 GW for floating projects, incentivizing tension-leg pilots. Lease awards de-risk permitting, yet California’s interconnection queue stretches to 2029 because of congestion around Moss Landing and Diablo Canyon substations.

Rapid Turbine Upsizing to 15-20 MW Class Reducing LCOE

Serial production of Siemens Gamesa’s 15 MW SG 14-236 DD and Vestas’ V236-15 MW turbines began in 2025, each cutting foundation costs for 1 GW projects by nearly half and slicing balance-of-plant expenses by USD 180 million. GE Vernova’s 14 MW Haliade-X variant optimized for low-wind regimes enlarges viable lease zones in New York State. MingYang and Goldwind achieved 16 MW prototypes, validating two-piece blades, rail transport, and extended service intervals. Capex per installed megawatt is tracking from USD 4.2 million in 2024 toward USD 3.1 million by 2028.

Oil & Gas Platform Conversions Unlocking Gulf of Mexico Supply Chain

Shell’s Vito decommissioning plan repurposes a tension-leg structure for 200 MW of floating turbines 150 km south of Louisiana, leveraging existing export cables and crew quarters to trim greenfield costs by 35%. TotalEnergies and Aker Solutions are assessing 12 semi-submersible rigs for wind retrofits, activating dormant fabrication yards in Brownsville and Corpus Christi. The U.S. Department of Energy allocated USD 50 million to demonstrate mooring interoperability, aiming to charter idle pipelay barges and ease vessel constraints.

EU & UK CfD Reform Boosting Bankability

Allocation Round 6 in the United Kingdom introduced inflation-indexed strike prices of GBP 176/MWh, which lower debt-service coverage ratios and court pension funds. France’s CRE awarded 15-year CfDs at EUR 120/MWh for the Golfe du Lion array, offering local-content bonuses. Spain extended contract tenors to 25 years, balancing lower tariffs with longer cash flows. Italy adopted a two-way tariff that shields developers when merchant prices drop, while Equinor secured a 25-year corporate offtake for Hywind Tampen with Norsk Hydro.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| WTIV & FIV Vessel Shortage Driving Day-rates > USD 450k | -3.8% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| High-Voltage Dynamic Cable Failures in 50-100 m Depth Pilots | -2.9% | Europe (North Sea, Celtic Sea), Asia-Pacific (Japan, Taiwan) | Medium term (2-4 years) |

| California ESA Right-Whale Constraints Slowing BOEM Permits | -1.6% | North America (California, Oregon) | Medium term (2-4 years) |

| Spot Steel Price Volatility (> USD 950/t) Disrupting Floater Yards | -3.2% | Global, with acute impact in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

WTIV & FIV Vessel Shortage Driving Day Rates Above USD 450k

Only 23 wind-turbine installation vessels (WTIVs) can handle 15 MW machines in 2025, yet 47 GW of projects need lifting through 2028. As utilization exceeds 95%, charter prices rose to USD 485,000 per day, postponing California’s Morro Bay array by two years and inflating a 500 MW project’s vessel bill to USD 87 million.[2]Bureau of Ocean Energy Management, “California Offshore Wind Leases: ESA Review,” boem.gov Shipyards are building 14 new WTIVs for 2026-27 delivery, but supply relief before 2027 remains limited.

High-Voltage Dynamic Cable Failures in 50-100 m Depth Pilots

Scotland’s Kincardine farm suffered a six-month outage in 2024 after bending-radius violations damaged 66 kV cables during 12-m wave events. Revised IEC 61400-3-2 standards now mandate tighter fatigue margins, and insurers require redundancy plus strain monitoring. Prysmian’s helically armored cable, released in 2025, meets those criteria but costs EUR 2.8 million per km, adding USD 90 million to a 1 GW project.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Water Depth: Deep Zones Redefine Lease Economics

Transitional depths of 30-60 m represented 54.1% of global installations in 2025, largely around the North Sea, where hybrid gravity anchors lower mooring costs. Deep-water sites beyond 60 m are on pace for a 58.2% CAGR, unlocking the vast technical potential off California, Japan, and Norway. The Floating Offshore Wind Power market size for the Deep segment is projected to reach 2,900 MW by 2031. California’s Morro Bay area highlights the economics: suction anchors rated for 1,000-m depths lift capital expense to USD 4.1 million per MW, yet access to 25 GW of wind resource offsets that premium. Japan’s Goto leases and South Korea’s Ulsan sites confirm similar depth-driven economics.

Shallow settings under 30 m captured only demonstration activity. Several European pilots used benign waters to test platform behavior before scaling to harsher seas. Meanwhile, Deep-water adoption relies on mooring innovation such as Vryhof’s STEVMANTA suction anchor, which reduces anchor count from four to three and slashes installation time by 25%.

By Floating Platform Type: Semi-Submersibles Dominate, Spar-Buoys Rise

Semi-submersibles contributed 55.8% of 2025 capacity, thanks to modular fabrication and compatibility with 15-20 MW turbines. Principle Power’s WindFloat platform can be towed out from quays with only a 4 m draft and then ballasted in place.[3]Principle Power, “WindFloat Atlantic Performance Update 2025,” principlepower.com Spar-buoys show the fastest ascent with a 55.3% CAGR as Asian yards employ high-volume steel roll-forming and demonstrate remarkable pitch stability in typhoon seas. The Floating Offshore Wind Power market share of Spar-buoys is therefore set to expand sharply through 2031.

Tension-leg platforms hold a niche 12% share, appearing where firm seabed clay enables vertical tethers that minimize heave. Hybrid barge ideas like BW Ideol’s Damping Pool or Hexicon’s TwinWind duet aim to trim anchor costs by sharing moorings but remain at pilot scale.

By Turbine Capacity: Gigawatt-Class Machines Reshape Economics

Turbines rated 5-10 MW still formed 52.9% of 2025 deployments, yet serial production of 15-16 MW units is tilting the economics decisively. The Floating Offshore Wind Power market size for machines above 15 MW is expected to expand at a 56.1% CAGR, aided by Siemens Gamesa’s SG 14-236 DD and Vestas’ V236-15.0 MW products. A 1 GW farm now needs 63 turbines instead of 125, cutting cable runs by 40%. Goldwind’s direct-drive 16 MW rotor reduces gearbox maintenance and extends service intervals to 18 months.

Smaller turbines remain configured for older pilots and typhoon-constrained regions. Doosan’s 8 MW platform continues to serve South Korean demos, yet its announced 12 MW variant shows the convergence toward global sizing norms.

By Application Stage: Pilots Yield to Utility-Scale Arrays

Pilots occupied 65.3% of installed capacity in 2025, virtually all funded by demonstration grants or transitional tariffs. Utility-scale arrays now line up financing as CfD reforms lower the weighted average cost of capital to 6.2% and insurers offer premiums of 1.8% of the installed cost. The Floating Offshore Wind Power market size for utility-scale projects is projected to overtake pilot capacity in 2028.

Hybrid wind-to-hydrogen projects already account for 8% of deployments. Germany’s AquaVentus and Japan’s Fukushima Forward pilots confirm that pairing wind with electrolyzers boosts equity returns by 150 bps, although electrolyzer capex of USD 800/kW still weighs on scalability.

Geography Analysis

Europe maintained 53.6% of installations in 2025, supported by the United Kingdom’s ScotWind leases, France’s Golfe du Lion tender, and Norway’s oil-platform decarbonization schemes. The Floating Offshore Wind Power market size in Europe is expected to pass 2,000 MW by 2031. United Kingdom policy mandates 25% local content, prompting port upgrades at Aberdeen and Inverness and sustaining semi-submersible fabrication.[4]Crown Estate Scotland, “ScotWind Leasing Round Outcomes,” crownestatescotland.com France’s 15-year CfDs at EUR 120/MWh and Mediterranean barge deployments provide predictable revenue and regional yard work. Spain, Italy, and Nordic nations follow with smaller yet fast-moving allocations that embed aquaculture or desalination co-use.

Asia-Pacific shows the strongest growth trajectory with a 53.3% CAGR. China’s Guangdong and Fujian provinces target 5 GW under the 14th Five-Year Plan, deploying MingYang and Goldwind 16 MW turbines. Japan’s 1.8 GW Round 2 leases include mandatory green-ammonia synthesis, while South Korea’s Ulsan Hydrogen City connects 500 MW of wind to 200 MW of PEM electrolyzers. Taiwan’s 2026 round reserves 3 GW for floating projects with 60% local content to develop domestic cable and mooring suppliers.

North America secured 4.6 GW of leases off California and Oregon, but ESA consultations for the North Pacific right whale extend permitting by 18 months. Developers now fund passive-acoustic monitoring and seasonal work restrictions, pushing the first power to 2030. Meanwhile, Gulf of Mexico platform conversions tap idle rigs and established subsea infrastructure to curb capex by 35%. South America and the Middle East & Africa remain nascent. Petrobras studies a 150 MW conversion off Rio de Janeiro, and the United Arab Emirates assesses 200 MW near Abu Dhabi for green-hydrogen export.

Competitive Landscape

The sector shows moderate concentration. The five largest turbine makers, Siemens Gamesa, Vestas, GE Vernova, MingYang, and Goldwind, deliver 68% of nacelle supply, while platform intellectual-property holders Principle Power, BW Ideol, Aker Solutions, and Hexicon license designs that regional yards fabricate. Developers with oil-and-gas pedigrees such as Equinor, TotalEnergies, Shell, and Ørsted exploit subsea-engineering know-how to defend margins. Emerging Chinese players compress costs through vertical integration, exerting pricing pressure on European OEMs.

Technology competition centers on moorings and dynamic cables. Vryhof’s STEVMANTA suction anchor reduces anchor count, trimming a 1 GW farm’s balance-of-plant cost by USD 40 million. Prysmian’s 66 kV helically armored cable mitigates fatigue but raises capex. Strategic deals in 2025 include Equinor and RWE’s USD 9.2 billion commitment for 3 GW at Morro Bay and Ocean Winds’ USD 4.5 billion partnership with Copenhagen Infrastructure Partners for 2.5 GW in Scotland, each leveraging indexed tariffs and EIB debt to close financing.

Patent filings under WIPO IPC F03D13/25 rose 42% in 2024, led by Equinor’s shared-mooring patterns and Hexicon’s dual-turbine barge, suggesting intensifying intellectual-property rivalry. Supply-chain scarcities persist, particularly WTIV availability and heavy-lift cranes, but 14 units now under construction in Korean and Chinese yards should come online between 2026-2027 to alleviate bottlenecks.

Floating Offshore Wind Power Industry Leaders

General Electric Company

Vestas Wind Systems A/S

Siemens Gamesa Renewable Energy, S.A

BW Ideol AS

Equinor ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DNV, a global leader in wind energy technology certification, has signed a memorandum of understanding (MoU) with Japan's Floating Offshore Wind Technology Research Association (FLOWRA) to explore collaborative opportunities in the development of floating wind technology.

- April 2025: The UK government announced a GBP 300 million package for domestic offshore wind supply chains, spanning turbine components, floating platforms, and subsea cables.

- April 2025: China Power, Tokyu Land Corporation, and Renewable Japan commenced commercial operation of the 3 MW Hibiki-nada barge-type floating wind plant, Japan’s first of its kind.

- March 2025: The UK government has allocated more than GBP 55 million for Port of Cromarty Firth upgrades, enabling the serial production of floating turbines and creating up to 1,000 skilled jobs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the floating offshore wind power market as all grid-connected wind turbines installed on buoyant, moored platforms that operate in waters deeper than thirty meters, with market size measured in commissioned capacity (MW) as well as their associated revenue pools.

Scope Exclusion: Near-shore fixed-foundation projects in depths below thirty meters are excluded.

Segmentation Overview

- By Water Depth

- Shallow (Up to 30 m)

- Transitional (30 to 60 m)

- Deep (Above 60 m)

- By Floating Platform Type

- Semi-Submersible

- Spar-Buoy

- Tension-Leg Platform (TLP)

- Barge & Hybrid Concepts

- By Turbine Capacity

- Up to 5 MW

- 5 to 10 MW

- 11 to 15 MW

- Above 15 MW

- By Application Stage

- Pre-Commercial Pilot

- Commercial Utility-Scale

- Hybrid Wind-to-X (Hydrogen, Desalination)

- By Geography

- North America

- United States

- Rest of North America

- Europe

- France

- United Kingdom

- Spain

- Nordic Countries

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

During 2025, we interviewed turbine OEM engineers, mooring contractors, port managers, and power-offtake planners across Europe, Asia-Pacific, and North America. Their insights helped us confirm average turbine ratings, commissioning lags, and achievable load factors, which we then used to temper aspirational project schedules published online.

Desk Research

Mordor analysts first gather foundational numbers from open datasets such as IRENA, GWEC annual capacity tallies, Eurostat renewable statistics, and U.S. DOE offshore wind market reports, which outline national pipelines, auction results, and commissioning dates. Policy documents by the European Commission, the UK Crown Estate, and BOEM supply target trajectories and lease specifics that anchor the capacity build-out curves. Industry journals and port authority cargo logs help us approximate nacelle movements and blade exports that signal actual installations. We layer this with paywalled intelligence pulled from D&B Hoovers for company financials and Dow Jones Factiva for investment announcements to cross-check project valuations. The sources listed are illustrative; many additional publications and datasets inform the desk phase.

A second pass mines patent filings via Questel and shipment traces from Volza to validate technology diffusion and hardware flow, letting us isolate genuine turbine deployments from mere press releases. Where gaps persist, we consult Aviation Week and IMTMA libraries for steel and composite cost indices used to sanity-check capex assumptions.

Market-Sizing & Forecasting

A top-down installed-capacity reconstruction is built from government targets and announced project pipelines, which are then stress-tested with selective bottom-up supplier roll-ups for the five largest arrays. Drivers such as average turbine rating, water-depth mix, floating platform choice, capacity factor progression, steel price trends, and lease-to-COD cycle length feed a multivariate regression that projects capacity through 2030. Missing sub-municipal data, when encountered, is bridged using regional penetration ratios benchmarked against analogous fixed-bottom builds.

Data Validation & Update Cycle

Outputs run through variance checks against IRENA and GWEC time-series, after which a senior reviewer challenges anomalies. Models refresh annually, with off-cycle updates triggered by final investment decisions, turbine order backlogs, or policy shifts. Just before publication, an analyst reruns the latest numbers so clients receive a current snapshot.

Why Mordor's Floating Offshore Wind Power Baseline Earns Trust

Published figures for this young sector often diverge because providers mix revenue and capacity metrics, bundle fixed-bottom assets, or apply aggressive learning-curve multipliers. Our team anchors estimates to physically installed megawatts and moderates long-range growth using country-specific supply-chain constraints, which makes Mordor's view naturally more conservative yet dependable for planning.

Key gap drivers include: a) differing unit of account (capacity versus dollar value), b) inclusion of speculative license areas that lack grid agreements, and c) currency and inflation adjustments applied inconsistently across multiyear models.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 0.39 GW (2025) | Mordor Intelligence | - |

| USD 1.7 B (2025) | Global Consultancy A | Mixes revenue of component vendors with capacity, lacks deployment cut-off date |

| USD 0.37 B (2024) | Trade Journal B | Counts prototypes and optioned leases, excludes Asia-Pacific cost inflation |

In short, Mordor's stepwise capacity tracking, tempered assumptions, and annual refresh cadence supply decision-makers with a transparent baseline that links directly to verifiable turbines in the water.

Key Questions Answered in the Report

What is the projected capacity for floating offshore wind by 2031?

Installed capacity is expected to reach 4,130.80 MW by 2031, driven by a 50.08% CAGR.

How do deep-water sites impact project economics?

Depths beyond 60 m unlock larger wind resources but add mooring costs, lifting capex toward USD 4.1 million/MW yet enabling higher capacity factors.

Which turbine rating now sets the benchmark for commercial arrays?

Serial-production 15-16 MW machines now dominate new contracts because they cut foundation counts and balance-of-plant costs.

Why are semi-submersible platforms still favored?

They allow modular yard fabrication, shallow-draft tow-out, and compatibility with turbines up to 20 MW, keeping installed costs competitive.

What policy reforms have improved bankability?

Inflation-indexed CfDs in the United Kingdom and 15-year fixed tariffs in France lower weighted average cost of capital to roughly 6.2%.

How does hydrogen co-location influence returns?

Pairing floating wind with offshore electrolyzers adds a second revenue stream that can lift equity returns by about 150 bps.

Page last updated on: