Extracorporeal Membrane Oxygenation (ECMO) System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

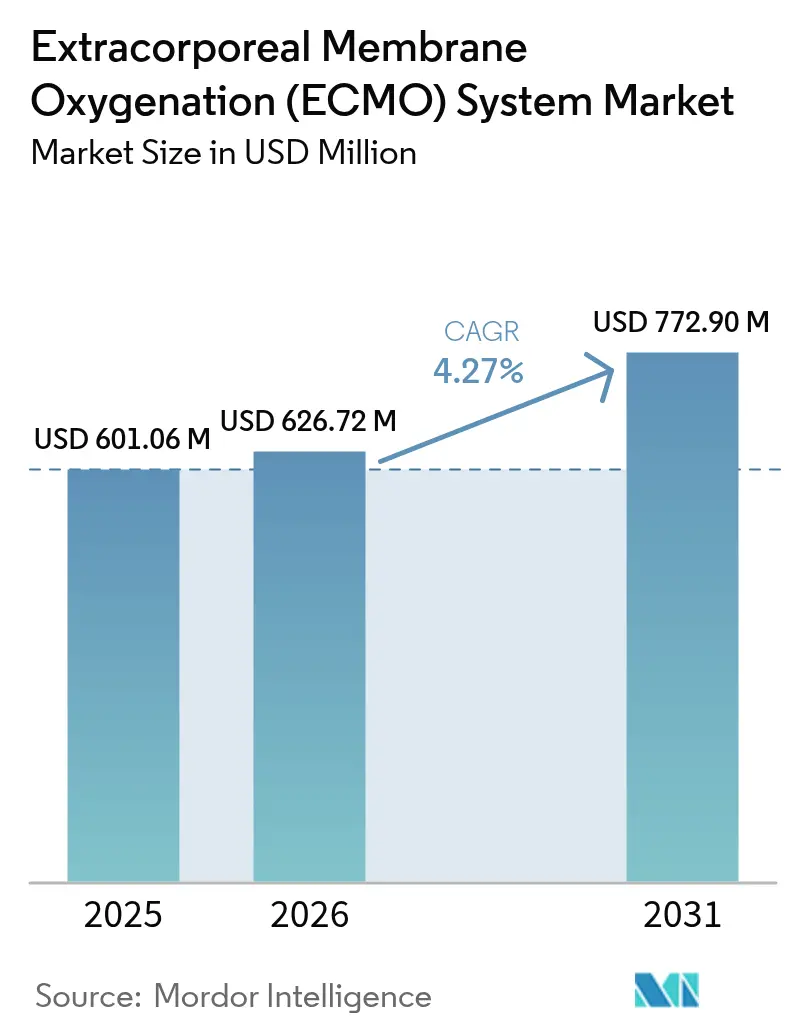

| Market Size (2026) | USD 626.72 Million |

| Market Size (2031) | USD 772.90 Million |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extracorporeal Membrane Oxygenation (ECMO) System Market Analysis by Mordor Intelligence

The extracorporeal membrane oxygenation system market size is expected to grow from USD 601.06 million in 2025 to USD 626.72 million in 2026 and is forecast to reach USD 772.9 million by 2031 at 4.27% CAGR over 2026-2031. Demand remains resilient because ECMO fills the critical gap between conventional ventilation or cardiopulmonary bypass and definitive recovery or transplant. The recent shift from bulky consoles to lightweight, transport-ready units has widened the clinical window for support, allowing more centers to mobilize ECMO teams within emergency and perioperative settings. Rising survival evidence in adult respiratory distress syndrome, the success of extracorporeal cardiopulmonary resuscitation (ECPR), and maturing reimbursement rules in high-income countries underpin predictable revenue growth. In parallel, emerging economies are building modern ICUs at record speed, a trend that lifts procedure volumes and accelerates local manufacturing partnerships.

Key Report Takeaways

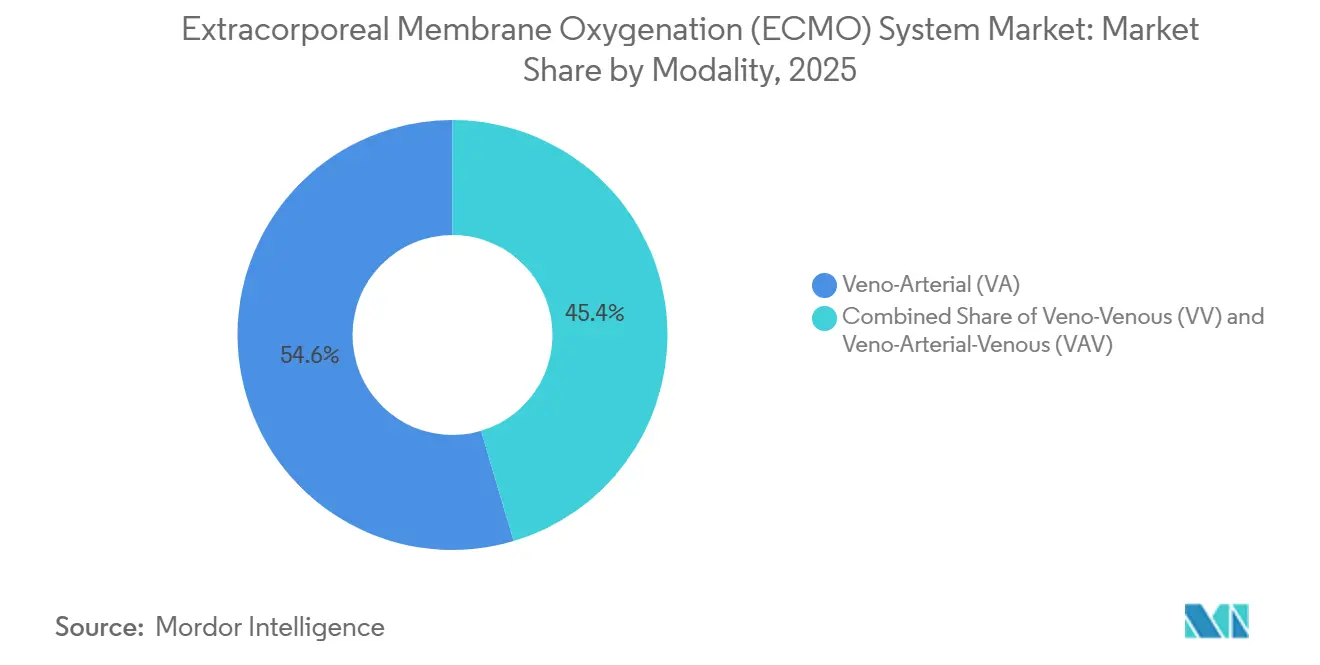

- By modality, veno-arterial ECMO held 54.60% of the extracorporeal membrane oxygenation system market share in 2025, while veno-venous ECMO is set to log a 10.40% CAGR to 2031.

- By component, oxygenators captured 29.60% of the extracorporeal membrane oxygenation system market size in 2025; console and pump platforms are projected to expand at a 11.80% CAGR through 2031.

- By application, respiratory failure accounted for 43.20% of the extracorporeal membrane oxygenation system market size in 2025, yet ECPR is the fastest-growing use case at 13.40% CAGR to 2031.

- By end user, tertiary care hospitals dominated with 80.30% revenue share in 2025, whereas specialty and cardio-thoracic clinics are forecast to post a 12.30% CAGR over the same horizon.

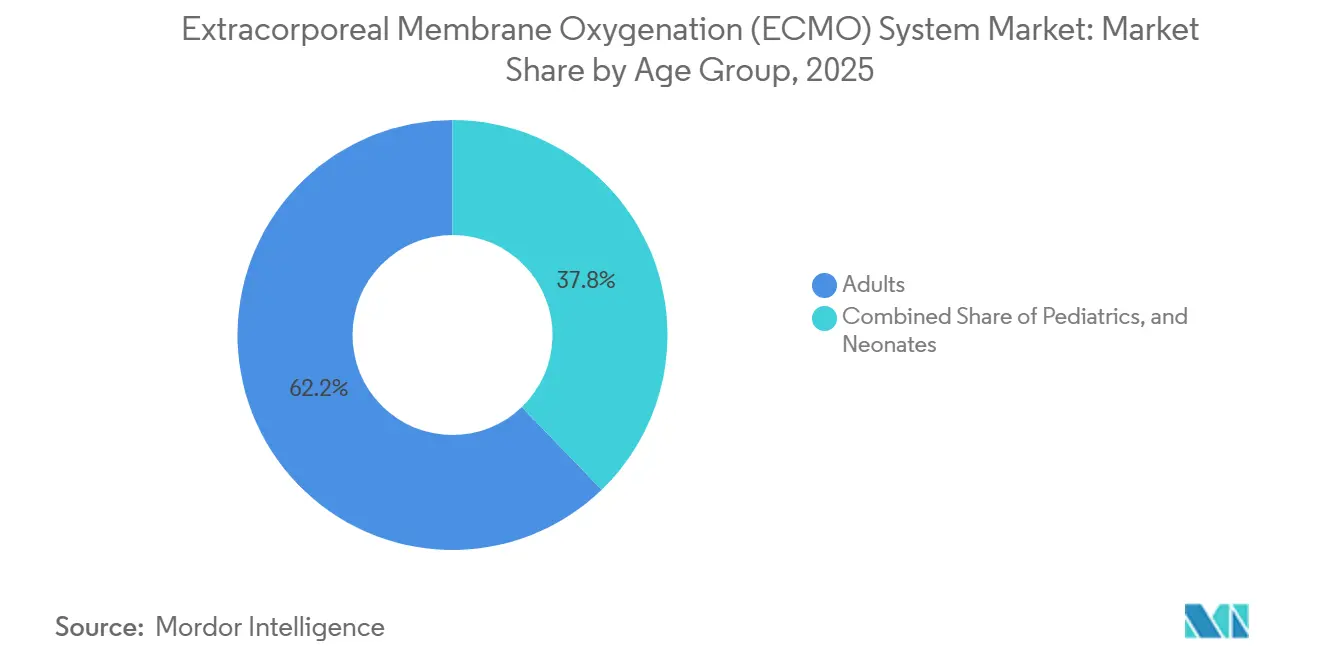

- By age group, adults represented 62.20% of the extracorporeal membrane oxygenation system market share in 2025, while the pediatric cohort is forecast to grow at an 11.00% CAGR to 2031.

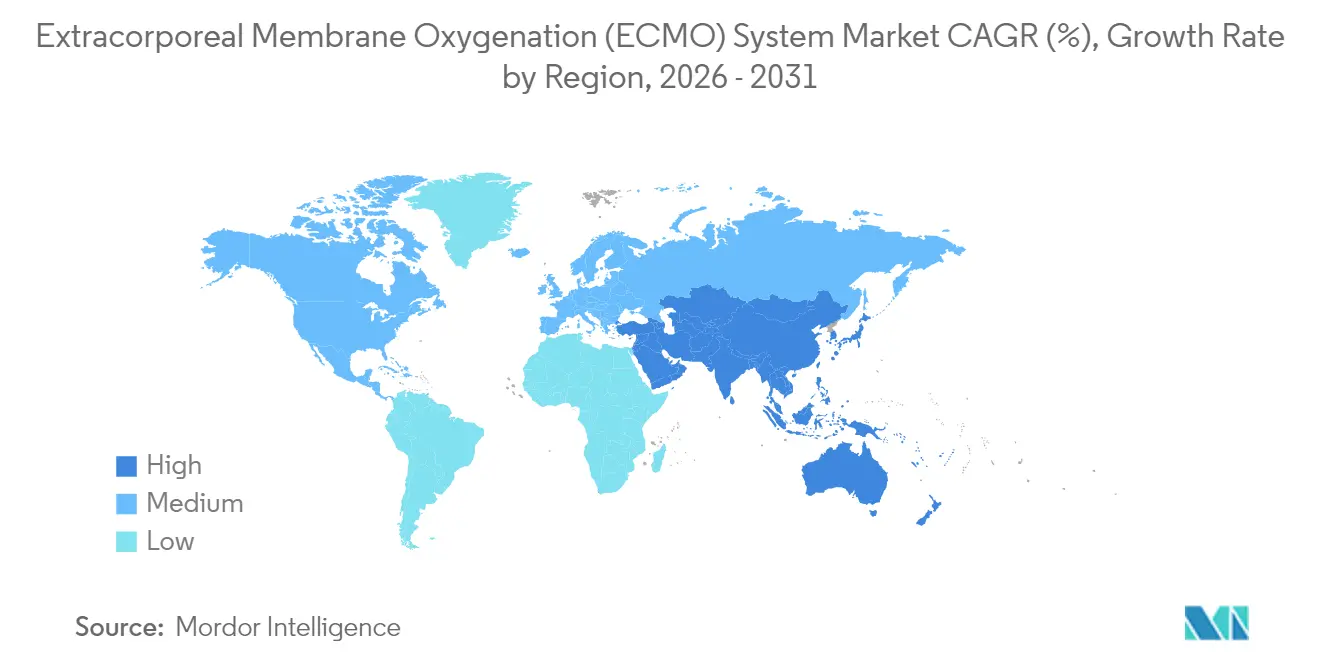

- By geography, North America led with 38.40% revenue share in 2025; Asia-Pacific is projected to grow the quickest with a 10.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Extracorporeal Membrane Oxygenation (ECMO) System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global incidence of severe acute cardio-pulmonary failure | +1.2% | Global, higher in aging populations | Medium term (2-4 years) |

| Continuous technological innovations delivering compact, integrated ECMO platforms | +0.8% | North America & EU lead, APAC adoption | Long term (≥4 years) |

| Expansion of reimbursement & funding mechanisms across developed markets | +0.6% | North America & EU, selective APAC | Short term (≤2 years) |

| Rapid growth of advanced ICU infrastructure in high-population emerging economies | +0.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Increasing evidence base demonstrating improved survival & cost-effectiveness | +0.5% | Global, evidence-driven first | Long term (≥4 years) |

| Formal inclusion of ECMO in critical-care guidelines | +0.4% | Global, guideline-driven markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Incidence of Severe Acute Cardio-Pulmonary Failure

Aging societies, sedentary lifestyles, and higher chronic disease prevalence create a steady flow of patients who progress to refractory heart or lung failure despite optimized conventional care. COVID-19 highlighted ECMO’s role when ventilatory strategies reached physiological limits, and registries continue to report sustained ARDS caseloads that require extracorporeal support. Concurrently, more centers are deploying veno-arterial circuits for cardiogenic shock following myocardial infarction, further boosting utilization in both developed and developing regions.

Continuous Technological Innovations Delivering Compact, Integrated ECMO Platforms

Modern devices integrate pumps, sensors, and touchscreen interfaces into slimline carts that fit bedside or ambulance footprints. Medtronic’s VitalFlow system runs on only 40 mL priming volume yet delivers full adult flows and integrated gas exchange monitoring. Magnetically levitated pumps minimize hemolysis, while AI-based dashboards predict clot formation and neurological events with high accuracy. These advances shrink the learning curve and make inter-facility transport safer, broadening the extracorporeal membrane oxygenation system market.

Expansion of Reimbursement & Funding Mechanisms Across Developed Markets

Clearer coding and bundled payments now exist for inpatient ECMO in the United States (MS-DRG-003 national rate USD 152,947)[1]Centers for Medicare & Medicaid Services, “FY 2024 IPPS Final Rule,” cms.gov. Several European payers have since aligned tariff schedules, while Japan and South Korea include ECMO under national catastrophic illness funds. Predictable reimbursement lowers financial risk for hospitals, catalyzing capital purchases and staff hiring.

Rapid Growth of Advanced ICU Infrastructure In High-Population Emerging Economies

China, India, Indonesia, and Saudi Arabia are building negative-pressure rooms and ECMO-capable ICUs inside new tertiary hospitals financed by public–private partnerships. Governments prioritize technology transfer, encouraging vendors to localize tubing sets and service hubs, cutting downtime and import duties. The extracorporeal membrane oxygenation system market therefore benefits from dual demand: procedure growth and equipment localization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortage of trained perfusion and critical-care personnel | −1.1% | Global, acute in emerging markets | Short term (≤2 years) |

| Complex, lengthy regulatory compliance for Class III devices | −0.8% | Global, stringent in North America & EU | Medium term (2-4 years) |

| Clinical complications and medicolegal risks | −0.6% | Litigation-prone markets, chiefly North America | Long term (≥4 years) |

| High capital, consumables and lifecycle costs | −0.7% | Cost-sensitive settings, especially lower-income APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Trained Perfusion And Critical-Care Personnel

Worldwide nursing deficits reached 5.9 million positions in 2025, and the pipeline for ECMO specialists is even tighter because certification demands at least 2 years of ICU experience[3]International Council of Nurses, “2025 State of the World’s Nursing,” icn.ch. Simulation-based curricula shorten upskilling, yet emerging markets still struggle to attract or retain talent. Nurse-led ECMO programs have trimmed staffing budgets by 52% in some U.S. centers but depend on robust institutional support.

Clinical Complications And Medicolegal Risks

Bleeding, thrombosis, stroke, and infection continue to pose challenges, driving malpractice premiums higher in North America and prompting defensive practice. AI-driven early warning modules may mitigate hazard rates, yet litigation costs still deter smaller hospitals from starting programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Rapid Respiratory Focus Widens Case Mix

Veno-arterial ECMO retained 54.60% of the extracorporeal membrane oxygenation system market in 2025, reflecting its dual heart-lung support versatility. Procedure volumes rise steadily in shock and surgical weaning scenarios, yet the 10.40% CAGR expected for veno-venous configurations signals a pivot toward pure respiratory rescue. The extracorporeal membrane oxygenation system market size for veno-venous circuits is projected to hit USD 358.7 million by 2031 as evidence from COVID-19 resets ARDS treatment algorithms. Centers now employ “awake ECMO” to keep patients mobilized and extubated, reducing ventilator-associated pneumonia risk while shortening ICU stays.

Veno-arterial-venous (VAV) hybrids treat complex mixed failures but remain niche because cannulation is intricate and monitoring demands are high. Registry analyses question if additional survival gains justify the higher bleeding risks, a debate likely to temper near-term adoption. Nonetheless, innovation in dual-lumen cannulas and left-ventricular unloading may refresh VA-ECMO growth by easing hemodynamic management.

By Component: Integration Lifts Pump-Console Revenues

Oxygenators locked in a 29.60% revenue share in 2025 due to recurring replacements every 5–7 days, but consoles and centrifugal pumps are forecast to expand at 11.80% CAGR as hospitals upgrade to all-in-one workstations. Vendors now integrate gas mixers, thermal control, and hemodynamic dashboards, effectively upselling replacement cycles. The extracorporeal membrane oxygenation system market size for pumps is estimated to reach USD 282.3 million by 2031, with magnetically levitated impellers reducing hemolysis and maintenance downtime.

Novel dual-chamber gas exchangers that forgo wall oxygen lines could cut ICU infrastructure costs, opening low-resource settings. Biocompatible polymer coatings diminish platelet activation, extending oxygenator life and lowering consumable costs, a shift that may slightly erode aftermarket revenues but boost overall adoption.

By Application: ECPR Climbs Fastest

Respiratory failure represented 43.20% of total procedures in 2025, anchored by established ARDS protocols. Yet, extracorporeal cardiopulmonary resuscitation is rising 13.40% annually as urban EMS teams trial mobile ECMO carts that initiate flows within 60 minutes of collapse. The extracorporeal membrane oxygenation system market share tied to ECPR could top 15.80% by 2031 if survival gains observed in pilot studies hold across multicenter trials.

Cardiac failure use cases remain steady in bridge-to-transplant and post-cardiotomy settings, maintaining 32.70% of revenue. Combined organ-support strategies that link ECMO with continuous renal replacement therapy are gaining attention as multi-organ failure prevalence grows.

By Age Group: Pediatric Growth Accelerates

Adult cases still make up 62.20% of total usage; however, pediatric and neonatal demand is rising at 11.00% CAGR as purpose-built mini circuits with 15 mL priming volumes enter the market. Predictive AI modules tuned for neuro-developmental risk help clinicians titrate flows and anticoagulation in children. National pediatric ECMO guidelines published in 2024 helped unify cannulation protocols, and regional transport teams enable rural referrals without delaying initiation.

Long-term follow-ups now track neurocognitive outcomes up to five years, generating evidence that supports earlier intervention in congenital heart disease. These data bolster parental consent rates and encourage donors to fund specialized pediatric ECMO beds.

By End User: Specialized Centers Drive Efficiency

Tertiary hospitals commanded 80.30% of revenue in 2025 because multidisciplinary teams and 24/7 perfusion coverage are prerequisites for safe ECMO. Clinical volume–outcome studies confirm mortality drops when centers exceed 30 runs per year, reinforcing centralization. Specialty cardio-thoracic clinics, though smaller, are growing 12.30% a year by carving out elective elective transplant and ventricular-assist device weaning niches.

Emergency departments now trial veno-venous ECMO cannulation under ultrasound, aiming for door-to-flow times below 40 minutes. Such protocols could disperse procedures across more facilities once staff shortages ease, softening tertiary dominance in the later years of the forecast.

Geography Analysis

North America held 38.40% of the extracorporeal membrane oxygenation system market in 2025, buoyed by robust reimbursement, a mature organ-transplant ecosystem, and more than 250 ELSO-registered centers. U.S. hospitals enjoy clear Medicare billing codes, giving administrators confidence to fund additional circuits and specialized staff. Canadian provinces follow a hub-and-spoke model that dispatches mobile teams to regional ICUs, optimizing asset utilization and maintaining equitable access.

Asia-Pacific is the fastest-growing region with a projected 10.30% CAGR through 2031. China deployed thousands of units during COVID-19, sparking domestic manufacturing that now supplies peripheral markets in Southeast Asia. India’s private hospital chains treat an expanding middle-class cardiac cohort, and favorable taxation on imported life-support equipment shortens replacement cycles. Japanese aging demographics and universal coverage encourage adoption, though budgets emphasize evidence-driven indications, keeping volume growth disciplined.

Europe posted steady mid-single-digit growth as national health services refine patient selection to cap costs. Germany operates 100-plus ECMO hubs, while the United Kingdom consolidated caseloads into five high-volume centers that report 55% survival in viral ARDS. Middle East adoption clusters in United Arab Emirates and Saudi Arabia, where sovereign wealth funds finance advanced cardiac institutes. Latin America shows pockets of uptake in Brazil and Argentina, although currency volatility and import tariffs temper growth. Africa’s adoption remains nascent outside South Africa and Egypt, limited by capital costs and perfusionist scarcity.

Competitive Landscape

The extracorporeal membrane oxygenation system market features a moderate concentration with top five players controlling around half of the revenue. Getinge’s Cardiohelp, Medtronic’s VitalFlow, and LivaNova’s TandemLife platforms dominate hospital tenders due to broad regulatory footprints and bundled training programs. Getinge continues to refresh oxygenator membranes with heparin-coated polymer that extends run time, while LivaNova integrates cloud telemetry into its new hardware revision, permitting remote troubleshooting.

Strategic acquisitions remain a core growth lever. Medtronic absorbed MC3 Cardiopulmonary to secure next-generation oxygenator IP and accelerate VitalFlow’s U.S. launch. Eurosets positions its 7 kg Colibrì system as the lightest adult ECLS platform, targeting retrieval services; the firm leverages modular disposables to lock in follow-on sales. Abbott broadened CentriMag’s indication window after FDA clearance for longer-term use, strengthening its bridge-to-decision portfolio.

Price competition is tempered by stringent regulatory and service requirements, leading vendors to differentiate via comprehensive clinical-support packages rather than discounting. Outsourced perfusion staffing, remote monitoring, and risk-sharing uptime guarantees are bundled into multi-year supply agreements. Start-ups such as Hemovent, with its portable MobyBox, pursue CE-only markets first to gather data before tackling FDA pathways. Meanwhile, component suppliers, membrane manufacturers, pump motor makers, and sensor specialists, are increasingly integrated in forward buyouts, tightening control over critical parts and safeguarding margins.

Extracorporeal Membrane Oxygenation (ECMO) System Industry Leaders

Getinge AB

Medtronic plc

LivaNova PLC

Terumo Corporation

Fresenius Medical Care (Xenios)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Medtronic launched VitalFlow, an all-in-one ECMO system designed for intuitive bedside operation in Europe.

- September 2024: AIIMS Bhubaneswar saved a critically ill woman using ECMO therapy, underscoring domestic skill growth in India.

- August 2024: Tampa General Hospital’s ECMO program received a Gold Level Center of Excellence designation from ELSO.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Extracorporeal Membrane Oxygenation (ECMO) system market as the installed consoles, pumps, oxygenators, heat exchangers, cannula sets, and integrated sensors that deliver prolonged cardiac or respiratory support in VA, VV, or VAV modes within critical-care settings.

Scope exclusion: Stand-alone cardiopulmonary bypass circuits used only for short surgical procedures are not counted.

Segmentation Overview

- By Modality

- Veno-Arterial (VA)

- Veno-Venous (VV)

- Veno-Arterial-Venous (VAV)

- By Component

- Console / Pump

- Oxygenator

- Heat Exchanger

- Cannulae & Tubing Sets

- Sensors & Controllers

- By Application

- Respiratory Failure

- Cardiac Failure

- Extracorporeal CPR (ECPR)

- By Age Group

- Neonates

- Pediatrics

- Adults

- By End User

- Tertiary Care Hospitals

- Specialty & Cardio-Thoracic Clinics

- Emergency Care Units

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with intensivists, perfusionists, biomedical engineers, and supply-chain managers across North America, Europe, and Asia filled incidence gaps, validated pricing corridors, and confirmed typical ECMO run durations that our desk work could only approximate.

Desk Research

We collected baseline data from tier-one public sources such as the World Health Organization, the Extracorporeal Life Support Organization registry, United Nations Comtrade shipment codes, Eurostat hospital statistics, and peer-reviewed journals (Critical Care, JAMA). Company 10-Ks, FDA device approvals, and association portals for perfusionists and transplant centers enriched usage metrics. Paid repositories including D&B Hoovers for supplier revenues and Questel for patent filing trends helped us size competitive presence and innovation intensity. This list is illustrative; many other documents informed data gathering, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with critical-care admissions for severe respiratory or cardiac failure, prevalence-to-treatment ratios, and average ECMO use per 100 qualified cases, which are then multiplied by mean procedure disposables and capital replacement cycles. Select bottom-up roll-ups of leading supplier revenues and sampled ASP × unit volumes ground the totals and highlight variance pockets. Key model drivers include global ARDS incidence, cardiogenic shock rates, transplant volumes, installed-base obsolescence, and reimbursement uptakes. Multivariate regression, supported by expert consensus on each driver's trajectory, projects values through 2030; missing country splits are resolved by weighted regional proxies.

Data Validation & Update Cycle

Outputs pass anomaly scans against independent indicators such as oxygenator import values and ELSO center additions. Senior analysts review flagged variances before sign-off. Reports refresh annually, with interim updates when regulatory approvals or major recalls shift demand. A final pre-delivery sweep ensures clients receive the most current baseline.

Why Mordor's ECMO System Baseline Commands Confidence

Published ECMO figures often differ because firms mix device scopes, assume contrasting ASP erosion paths, or refresh models on uneven cycles. Our disciplined variables, clear inclusions, and yearly updates reduce such drift.

Typical gap drivers include: some publishers track console sales only, others apply aggressive global price deflation, and many leave out single-use tubing revenues that Mordor Intelligence includes for a fuller market view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 601.06 Mn (2025) | Mordor Intelligence | |

| USD 532.3 Mn (2024) | Global Consultancy A | Counts machines but excludes consumables and service income; narrower regional coverage |

| USD 322.9 Mn (2024) | Sectoral Publisher B | Relies on discharge sample extrapolation and steep ASP deflation; model refreshed every two years |

In short, our balanced mix of hospital-level demand metrics, supplier checks, and annual revisions equips decision-makers with a dependable, transparent baseline that can be retraced to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current ECMO system market size?

The global ECMO system market is valued at around USD 626.72 million in 2026 and is projected to exceed USD 772.9 million by 2031.

Which ECMO modality is growing the fastest?

Veno-Venous (VV) ECMO is the fastest-growing modality, expanding at an estimated 10.40% CAGR between 2026 and 2031.

How are CMS reimbursement changes impacting hospitals?

CMS reclassification has lowered payments for peripheral ECMO by 40-80 %, prompting hospitals to redesign cannulation workflows and emphasize value-based outcome contracts.

Why is Asia-Pacific considered a high-growth region for ECMO?

Rapid ICU infrastructure expansion, local manufacturing approvals, and large patient populations in China and India are propelling Asia-Pacific ECMO demand at about 10.30 % CAGR.

What personnel challenges does ECMO adoption face?

A global shortage of perfusionists and ECMO-trained critical-care staff limits capacity; hospitals are investing in automation and tele-supervision to mitigate this constraint.

Which component holds the largest share of the ECMO system market?

Oxygenators account for roughly 29.60 % of total ECMO system revenue, reflecting their pivotal role in gas exchange performance.

Page last updated on: