Purging Compound Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

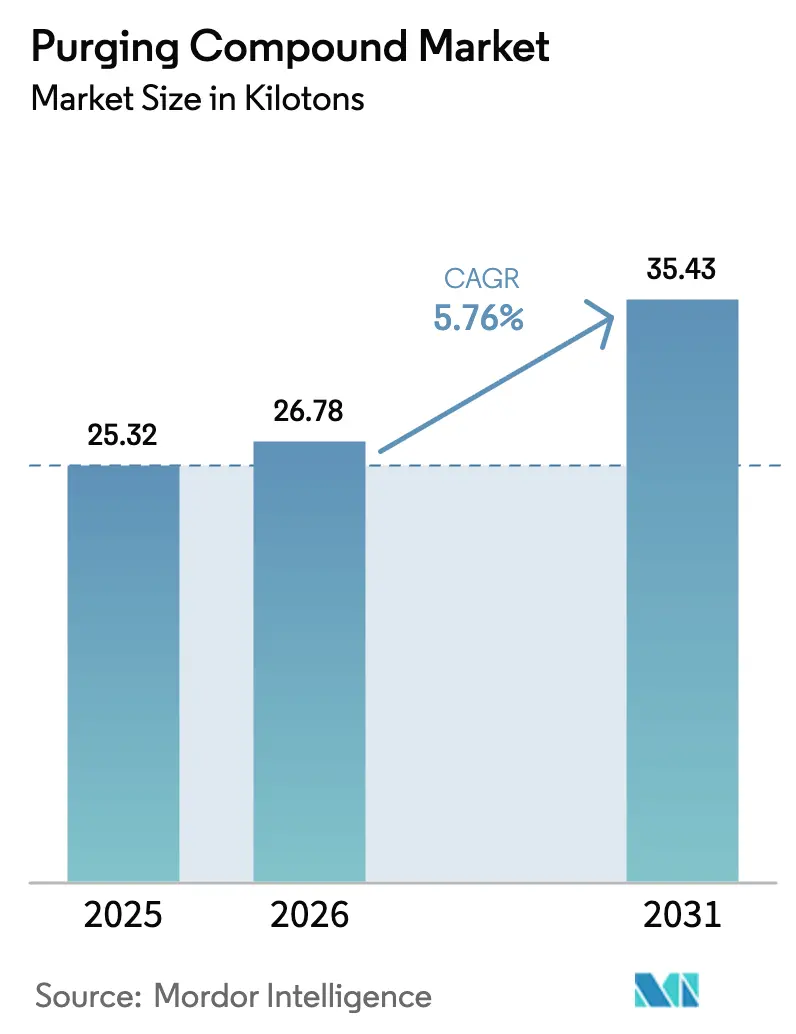

| Market Volume (2026) | 26.78 kilotons |

| Market Volume (2031) | 35.43 kilotons |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

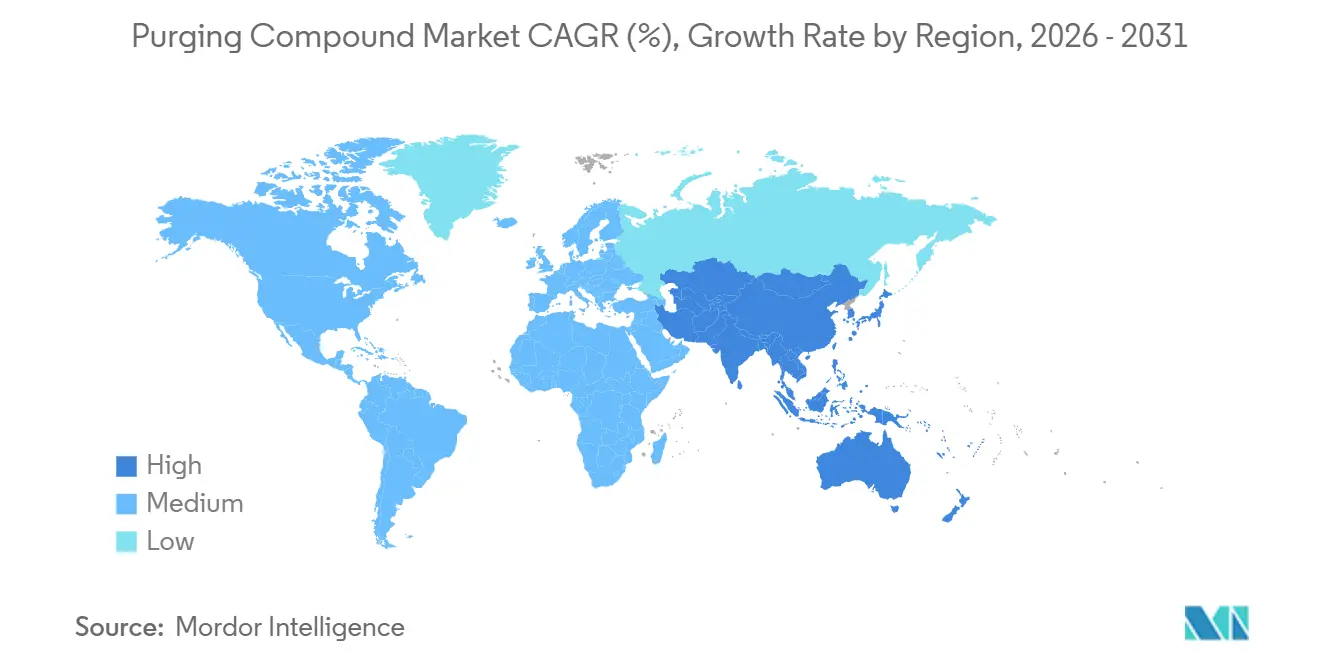

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

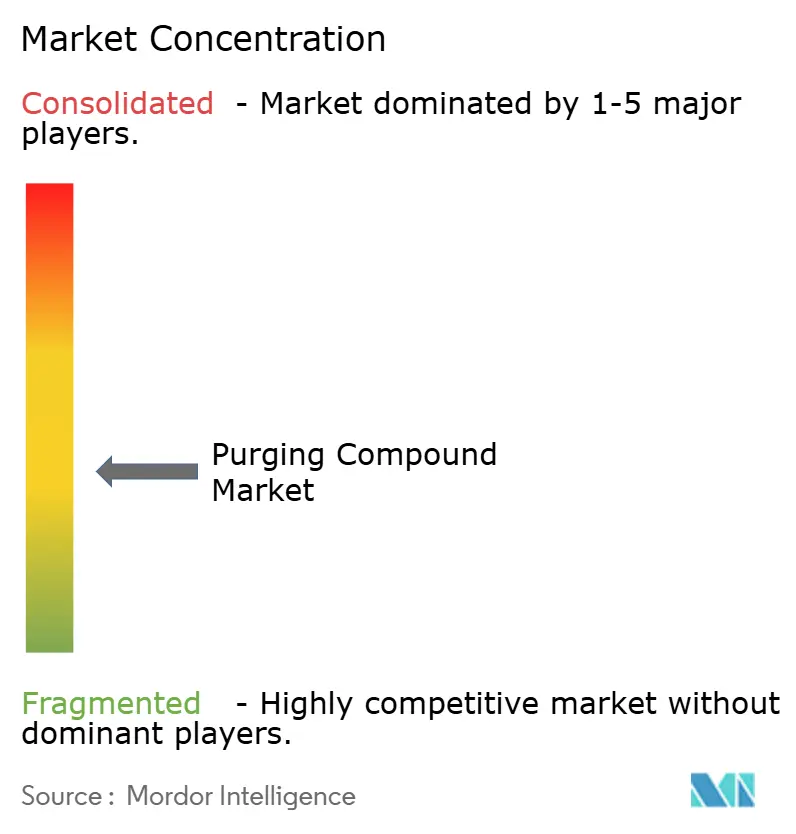

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Purging Compound Market Analysis by Mordor Intelligence

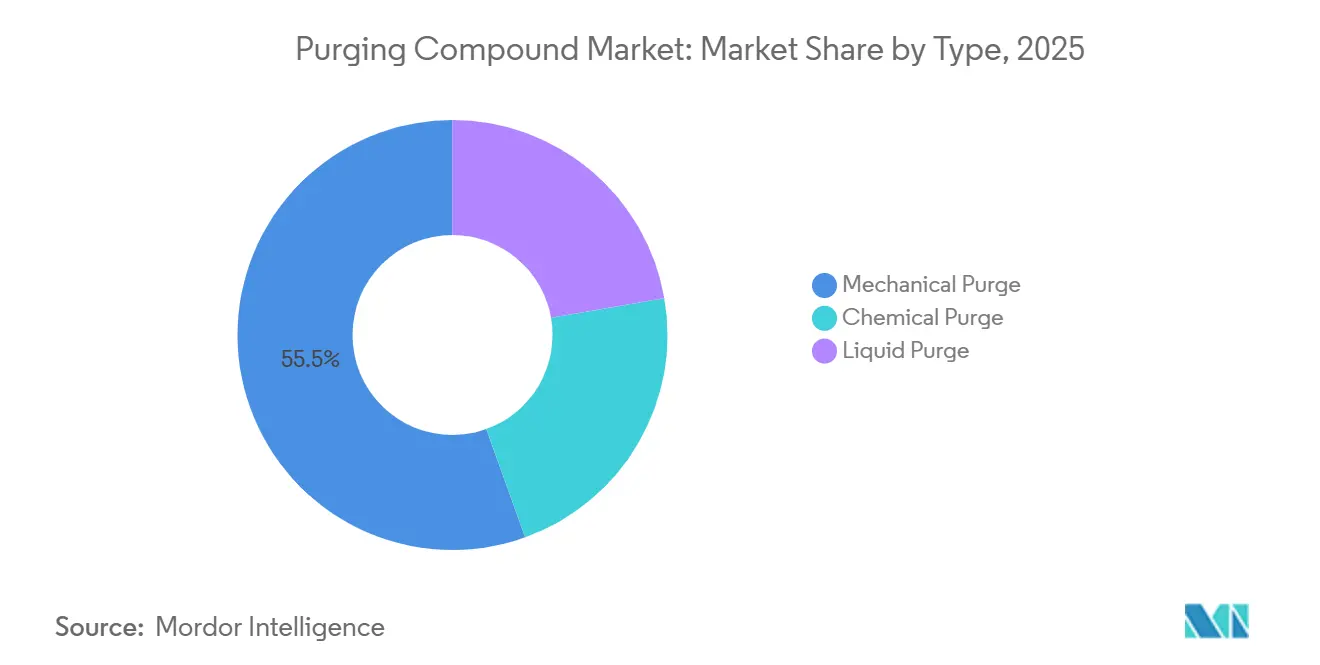

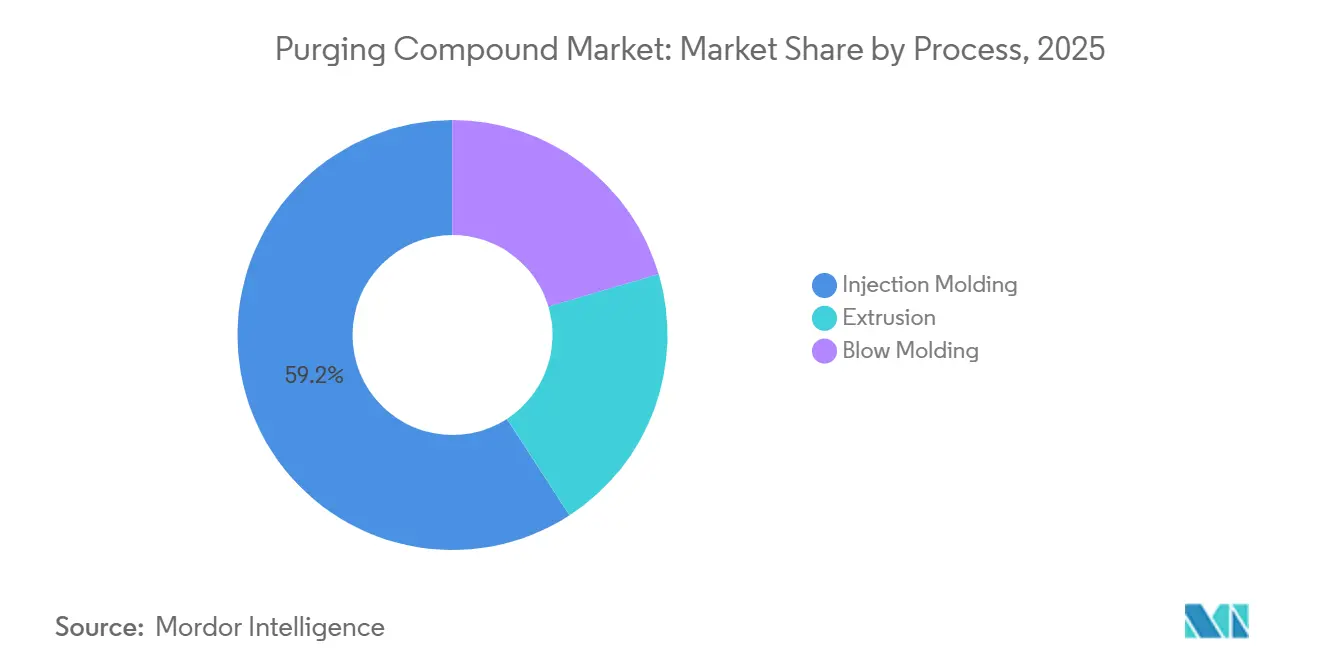

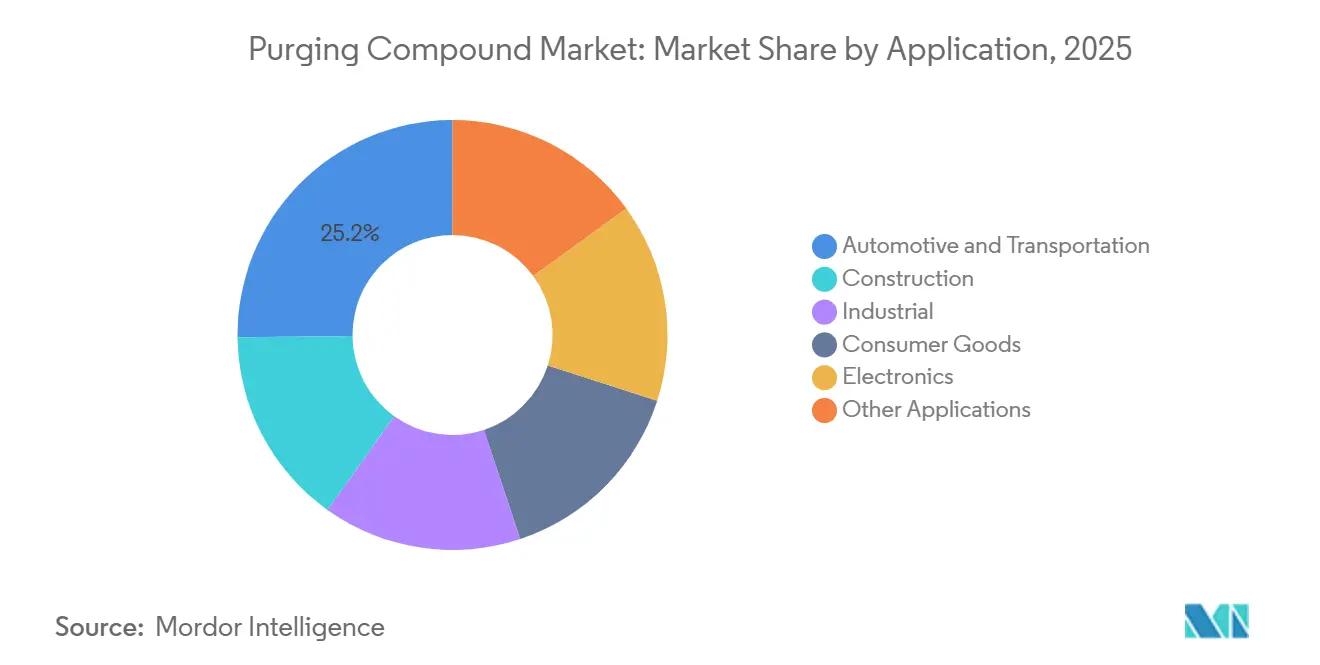

The Purging Compound Market size is projected to expand from 25.32 kilotons in 2025 and 26.78 kilotons in 2026 to 35.43 kilotons by 2031, registering a CAGR of 5.76% between 2026 to 2031. Growth is propelled by rapid adoption of high-temperature engineering polymers, shorter change-over intervals in Industry 4.0 plants, and rising regulatory pressure to curb microplastic abrasion. North America accounted for a dominant 50.12% purging compound market share in 2025, yet Asia-Pacific is the fastest-growing region at a 6.18% CAGR, supported by China’s surge in electric-vehicle production. Mechanical purge products led with 55.49% volume share in 2025 and are expanding at 6.08% CAGR, while injection molding represents 59.16% of volume on the back of frequent color and resin transitions. Automotive and transportation applications captured 25.16% share in 2025 and continue to benefit from zero-defect mandates on battery enclosures and structural parts. Competitive intensity remains moderate because integrated chemical majors bundle purging compounds with engineering resins, whereas niche suppliers focus on application-specific formulations that yield up to 85% scrap reduction.

Key Report Takeaways

- By type, mechanical purge held 55.49% of the purging compound market size in 2025 and is forecast to post the quickest 6.08% CAGR through 2031.

- By process, injection molding commanded 59.16% share of the purging compound market size in 2025 and exhibits the fastest 6.10% CAGR to 2031.

- By application, automotive and transportation led with 25.16% share of the purging compound market size in 2025 and is projected to expand at the highest 5.95% CAGR through 2031.

- By geography, North America retained 50.12% purging compound market share in 2025, yet Asia-Pacific is growing at a robust 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Purging Compound Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of High-Temperature Engineering Polymers | +1.2% | Global, with concentration in North America, Europe, and APAC manufacturing hubs | Medium term (2-4 years) |

| Shorter Color and Resin Change-Over Intervals in Industry 4.0 Plants | +1.5% | North America and Europe, expanding to APAC smart factories | Short term (≤ 2 years) |

| Rising Demand for Bio-Based / Low-VOC Purging Chemistries | +0.8% | Europe and North America, driven by sustainability mandates | Long term (≥ 4 years) |

| Surge in Micro-Lot Packaging and Medical Disposables | +1.1% | Global, with peak demand in North America and Europe healthcare sectors | Medium term (2-4 years) |

| OEM Qualification Norms for E-Mobility Parts | +1.0% | APAC core (China, South Korea, Japan), spill-over to North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of High-Temperature Engineering Polymers

Processing temperatures above 350 °C for polyetherimide, polyphenylene sulfide, and polyethersulfone accelerate polymer degradation that standard purges cannot remove. BASF’s Ultrason PESU lowered processing temperature requirements by about 12.5% in 2024, yet flame-retardant polyamides and polycarbonates still leave carbonized residues on screw flights. Battery enclosures molded under IEC 62660-3 safety norms demand contamination-free conditions to avoid electrical shorts. Processors note purge cycles are 20% longer for these polymers, which lifts volumetric demand. SABIC’s USD 220 million ULTEM facility in Singapore added 50% capacity in 2024, enhancing regional availability and stimulating the purging compound market.

Shorter Color and Resin Change-Over Intervals

Industry 4.0 platforms compress change-over windows from hours to minutes, requiring purging compounds capable of cleaning in fewer screw rotations. Asaclean field trials in 2024 demonstrated 47% faster color changes and 67% scrap savings when compared with virgin-resin flushing. Engel’s e-victory electric molding machines embed automated purge programs that inject compounds at preset temperature thresholds, reducing operator error. Tier 1 suppliers molding 15-20 color variants per shift gain economic leverage, which in turn enlarges the purging compound market.

Rising Demand for Bio-Based / Low-VOC Purging Chemistries

European directives seeking 55% recycling of plastic packaging by 2030 and the upcoming PFAS limits are encouraging adoption of bio-attributed formulations. BASF’s biomass-balanced Ultrason PESU launched in 2025 enables sustainability claims without process changes. Premix introduced PRE-PRG, a natural-fiber compound exceeding 50% bio-based content, aimed at medical and food-contact processors. Clariant’s bio-surfactant packages cut hazardous air pollutants by 30%, meeting California Air Resources Board caps. Although unit prices sit 15%-25% higher than conventional products, brand owners with explicit environmental mandates remain early adopters.

Surge in Micro-Lot Packaging and Medical Disposables

Single-use medical devices and personalized packaging require frequent resin changes that magnify purging-compound consumption. Chem-Trend’s Ultra Purge 3615 achieved 85% scrap reduction and 69% downtime savings in 2024 medical-molding trials. Europe generated 900,000 metric tons of healthcare plastics waste in 2023, of which single-use items formed 60%, underlining the volume effect on the purging compound market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Prices of Specialty Resins and Additives | -0.9% | Global, with acute impact in regions dependent on imported feedstocks | Short term (≤ 2 years) |

| High Unit Price Versus Re-Grind/Virgin Resin | -0.7% | Price-sensitive markets in South America, MEA, and ASEAN | Medium term (2-4 years) |

| Regulatory Scrutiny on Micro-Plastic Abrasion | -0.5% | Europe and North America, with emerging pressure in APAC coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Specialty Resins and Additives

Price spikes for carrier resins and antioxidant packages compress margins and discourage inventory build-up. BASF lifted Ultraform polyoxymethylene prices by USD 350 per ton in March 2025 amid feedstock inflation[1]BASF, “Price Adjustment for Ultraform POM,” basf.com . Antioxidant costs rose 10% in March 2024 following outages at Asian suppliers, while the U.S. Producer Price Index for plastic resins logged a negative 1.1% twelve-month change in September 2025, highlighting volatility. Converters in currency-depreciating regions often extend purge intervals or revert to re-grind, dampening short-term demand.

High Unit Price Versus Re-Grind / Virgin Resin

Mechanical purges cost USD 4-8 per kilogram, a 300% premium over post-industrial re-grind, prompting commodity processors to tolerate minor contamination. Chem-Trend data show that Ultra Purge 3615 can yield payback in as little as four weeks through scrap and downtime savings, yet many small processors in ASEAN and South America lack tools to quantify total cost of ownership. This price sensitivity slows adoption, especially where labor costs are low and throughput trumps efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mechanical Purge Dominates Through Abrasive Efficiency

Mechanical purges accounted for 55.49% of the purging compound market size in 2025 and are set to expand at a 6.08% CAGR through 2031. Their blend of carrier resin and mineral fillers forms an abrasive slurry that detaches carbonized deposits even at processing temperatures above 300 °C. Chem-Trend’s Ultra Purge 3615 demonstrated 85% scrap reduction in 2024 field trials, reinforcing the performance advantage over passive flushing. Chemical purges, though gaining ground where mold-surface integrity is critical, currently hold just under one-third of demand. Liquid purges occupy a niche in hot-runner systems with narrow channels. European sustainability rules are nudging suppliers to replace petro-based carriers with bio-attributed resins, a pivot led by BASF’s biomass-balanced Ultrason PESU. The push for low-VOC plants further favors mechanical purges with minimal solvent content, positioning them to defend leadership even as alternative chemistries mature.

Demand differentials arise from process temperature, residue tenacity, and change-over frequency. Injection-molding lines running high-temperature polyamides favor mechanical grades because chemical foaming agents can leave gas pockets inside manifolds. Extrusion processors shift toward chemical grades during long runs to avoid abrasive barrel wear, yet still maintain mechanical products for transition between dark and light colors. Market entrants focusing on bio-based abrasive fillers promise 30% carbon-footprint savings, although price premiums of 15% mean penetration will stay limited to brand owners with explicit climate targets.

By Process: Injection Molding Leads on Frequent Changeovers

Injection molding seized 59.16% of the purging compound market size in 2025 and is forecast to grow at a 6.10% CAGR through 2031, reflecting its high-mix, low-volume production model. Instrument panels, battery enclosures, and diagnostic housings each require resin or color switches several times per shift. Engel’s e-victory machines automatically trigger purge sequences, cutting operator-driven variability. Extrusion stands second due to sheer throughput, yet fewer changeovers translate to lower usage intensity on a per-kilogram basis. Blow molding, though smallest, is accelerating as pharmaceutical vials and single-dose bottles command contamination-free standards. Asaclean reported 67% scrap savings and 47% faster color transitions in 2024 extrusion trials, illustrating tangible paybacks.

Automation amplifies demand by shortening idle periods between runs, yet it also raises expectations for purge effectiveness on the first attempt. Processors integrating real-time quality monitoring reject even faint streaks, forcing full purges rather than partial pushes with virgin resin. New vanguard machines feature closed-loop screw-position feedback that flags contamination early, creating another trigger for compound use. Extrusion processors dealing with multilayer film increasingly purge each layer separately, doubling consumption relative to monolayer lines. Although blow-molding volumes lag, rising use of high-viscosity polyester for medical containers necessitates specialized liquid or chemical purges that can negotiate narrow parison heads.

By Application: Automotive Leads, Electronics Accelerates

Automotive and transportation held 25.16% of the purging compound market size in 2025 and will continue at a healthy 5.95% CAGR through 2031. Mandatory zero-defect thresholds on surface finish, coupled with the IEC 62660-3 battery-safety standard, push Tier 1 suppliers to purge thoroughly between each molding batch. Electric-vehicle growth in China remains a prime volume driver, as 9.59 million units rolled off assembly lines in 2023. Electronics displays the fastest momentum as shrinking component dimensions make even microscopic residue unacceptable. SEMI recorded USD 109 billion in semiconductor equipment sales during 2024, illustrating the scale of plastics integration into chip packaging.

Construction and consumer goods generate stable if slower growth, given their longer production runs which dilute per-unit purge usage. Still, window-profile lines switching from PVC to ASA color variants rely on purging compounds to avoid streaking. The medical segment benefits from soaring demand for single-use devices; American Chemistry Council data peg medical-device reprocessing at a 16.2% CAGR through 2032, indirectly lifting purging volumes. Appliance makers in Asia-Pacific are adopting anti-bacterial resin grades that need separate purge regimes, while industrial machinery suppliers stipulate contamination control in warranty clauses, adding a downstream pull on demand.

Geography Analysis

North America maintained a commanding 50.12% purging compound market share in 2025, thanks to its concentration of advanced automotive and medical molding hubs that value quality over cost. Formosa Plastics’ 249,000 ton polypropylene plant started in Texas during Q3 2024, boosting regional resin availability and directly increasing compound use during qualification trials. United States processors comply with FDA biocompatibility rules and EPA air-quality standards that encourage low-VOC purges, whereas Canadian suppliers of surgical disposables echo similar contamination tolerances. Mexico’s automotive clusters serving Ford, General Motors, and Volkswagen rely on purging compounds to minimize cosmetic rejects in instrument panels.

Asia-Pacific represents the fastest-growing node with a 6.18% CAGR through 2031, driven by Chinese electric-vehicle momentum, India’s USD 2.4 billion advanced chemistry cell incentive, and ASEAN contract manufacturing for electronics. BASF’s Zhanjiang Verbund site moved a 1 million-ton ethylene cracker online in November 2025, enlarging downstream polyethylene streams and spurring regional demand for compatible purging compounds. Japan’s precision molding sector demands liquid purges suitable for narrow hot-runner channels, while South Korea’s share of global semiconductor equipment sales ensures continuous use of chemical purges in chip-packaging injection systems. In India, price sensitivity limits premium adoption, yet exporters to Europe must demonstrate compliance with EU microplastic rules, stimulating gradual uptake.

In Europe, Germany, France, and Italy together molded over half of the region’s 52.8 million-ton plastics output in 2023. The EU REACH Regulation 2023/2055 accelerates transition from abrasive mechanical grades to chemical variants that dissolve residues without generating particulate emissions. South America and the Middle East and Africa remain emerging markets for the purging compound market, with Brazil’s Braskem and Saudi Arabia’s SABIC bundling compounds alongside resins, though lower contamination standards and higher price sensitivity slow progress. IMCD Group’s 2024 acquisition of Protea Chemicals expanded technical support in sub-Saharan Africa, hinting at gradual penetration.

Competitive Landscape

The purging compound market shows moderate concentration because integrated majors such as BASF, Dow, and Clariant leverage upstream resin production to bundle purge grades, while specialists like Chem-Trend capture value through tailored formulations. BASF’s March 2025 price increase of USD 350 per ton on Ultraform polyoxymethylene highlighted feedstock volatility that squeezes independent suppliers who buy open-market resins. Chem-Trend’s Ultra Purge 3615 recorded up to 69% downtime savings in 2024 field evaluations, setting performance benchmarks for mechanical grades. Clariant advances bio-surfactant systems compatible with EU VOC caps, while Dow scales advanced recycling to supply post-consumer carriers at competitive cost[2]Dow, “Advanced Recycling Expansion in Texas,” dow.com .

Strategic differentiators fall along three axes, namely thermal-stability enhancements permitting safe purging above 350 °C, bio-based content to satisfy circular-economy mandates, and digital service integrations linking purge sequences with PLC control. North American and European converters lead on digital adoption, embedding Siemens or Rockwell Automation modules that auto-dose compounds. Asia-Pacific processors emphasize cost efficiency, often selecting high-abrasive mechanical purges that work without additional infrastructure. Patent activity recorded during 2024-2025 focuses on foaming agents that expand within barrel cavities and bio-attributed carriers made from waste cooking oil, targeting 30% lower carbon footprints.

Distribution partnerships influence regional reach. IMCD’s takeover of Protea Chemicals in 2024 widened VELOX purging compound access across southern Africa, while Calsak Corporation expanded Chem-Trend distribution in Western U.S. states. Emerging disruptors market compounds using post-consumer recycled carriers, claiming 10%-15% price discounts compared with virgin-based incumbents. While uptake remains limited, these offerings align with voluntary scope-3 emission targets set by global brand owners, creating a niche yet expanding revenue pool.

Purging Compound Industry Leaders

Chem-Trend L.P.

Asahi Kasei Corporation

Shuman Plastics, Inc.

CLARIANT

Daicel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BASF commissioned a 1 million-ton ethylene cracker and a 500,000-ton HDPE unit in Zhanjiang, China, enhancing regional resin self-sufficiency. This development is expected to drive demand for purging compounds in downstream applications.

- October 2025: Asahi Kasei Corporation introduced new Asaclean R-Series purging compounds in Europe. This development is expected to impact the purging compounds market by offering enhanced solutions for universal, time-optimized, and quick material changeover applications.

Global Purging Compound Market Report Scope

Purging compounds cleans and preserves thermoplastics production machinery. They dissolve leftover material and contaminants in equipment. In the automotive and aerospace industries, purging chemicals are used to clean and maintain processing equipment to make sure that parts are consistent and of good quality.

The purging compound market is segmented by type, process, application, and geography. By type, the market is segmented into mechanical purge, chemical purge, and liquid purge. By process, the market is segmented into injection molding, extrusion, and blow molding. By application, the market is segmented into automotive and transportation, construction, industrial, consumer goods, electronics, and other applications. The report also covers the market size and forecast for the purging compound in 17 countries across major regions. For each segment, market sizing and forecasts have been on the basis of volume (tons).

| Mechanincal Purge |

| Chemcial Purge |

| Liquid Purge |

| Injection Molding |

| Extrusion |

| Blow Molding |

| Automotive and Transportation |

| Construction |

| Industrial |

| Consumer Goods |

| Electronics |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Mechanincal Purge | |

| Chemcial Purge | ||

| Liquid Purge | ||

| By Process | Injection Molding | |

| Extrusion | ||

| Blow Molding | ||

| By Application | Automotive and Transportation | |

| Construction | ||

| Industrial | ||

| Consumer Goods | ||

| Electronics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current volume of the purging compound market?

The purging compound market size is 26.78 kilotons in 2026 and is projected to reach 35.43 kilotons by 2031.

Which process segment leads demand for purging compounds?

Injection molding holds 59.16% of volume and grows at a 6.10% CAGR because frequent color and resin changes require rapid cleaning.

Why are mechanical purge compounds dominant?

Mechanical grades secure 55.49% share due to abrasive fillers that effectively remove carbonized residues during high-temperature transitions.

Which region is expanding fastest?

Asia-Pacific records the highest 6.18% CAGR through 2031, driven by rapid electric-vehicle and electronics manufacturing expansion.

Page last updated on: