Protective Cultures Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 477.67 Million |

| Market Size (2031) | USD 817.63 Million |

| Growth Rate (2026 - 2031) | 11.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Protective Cultures Market Analysis by Mordor Intelligence

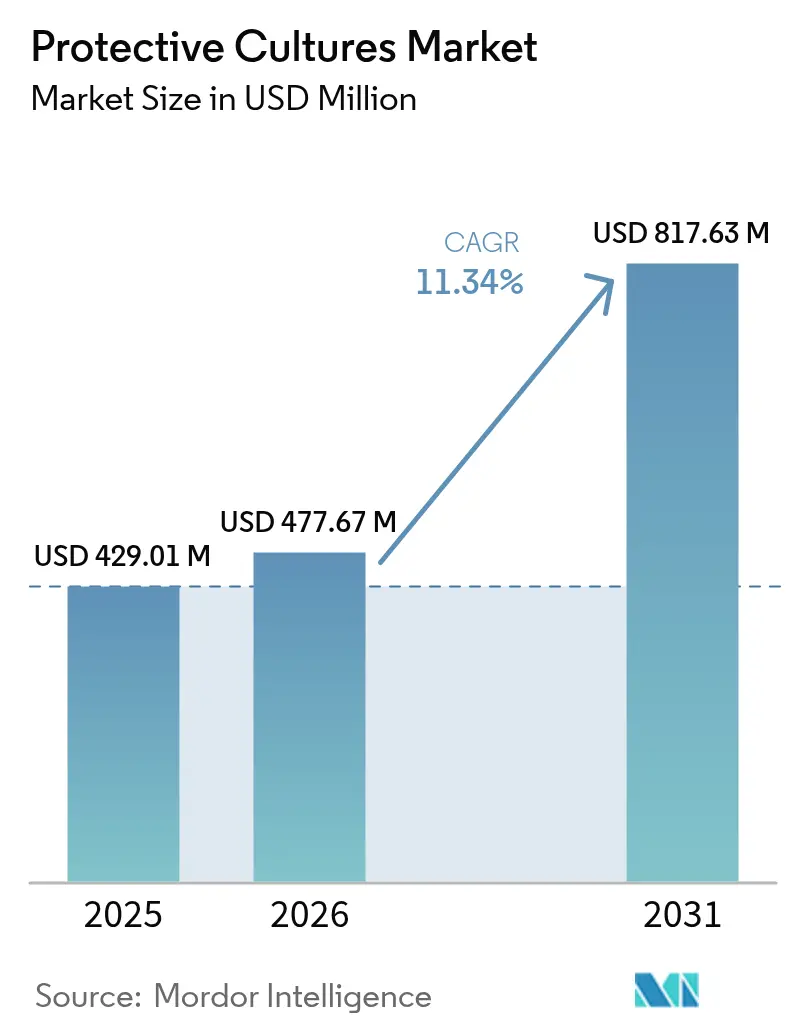

The protective cultures market size was valued at USD 429.01 million in 2025 and estimated to grow from USD 477.67 million in 2026 to reach USD 817.63 million by 2031, at a CAGR of 11.34% during the forecast period (2026-2031). This growth trajectory reflects the convergence of clean-label consumer demands, regulatory pressures for natural preservation, and technological advances in microbial stabilization methods. The rise in the protective cultures market size over the period highlights a structural pivot from synthetic preservatives to microbial bioprotection. Escalating demand for clean-label products, growing regulatory acceptance of natural antimicrobials and ongoing advances in strain stabilization technologies collectively underpin this expansion. Rapid formulation innovation, wider availability of regulatory-cleared strains and deeper penetration into emerging convenience-food segments further broaden addressable opportunities across both legacy and novel applications. The increasing consumer awareness about food safety and preservation has accelerated the adoption of protective cultures in various food products. Manufacturers are investing significantly in research and development to enhance the effectiveness and stability of protective culture strains. The rising focus on extending shelf life while maintaining product quality has made protective cultures an essential component in food preservation systems. The expansion of ready-to-eat food segments in developing markets has created additional growth opportunities for protective culture applications.

Key Report Takeaways

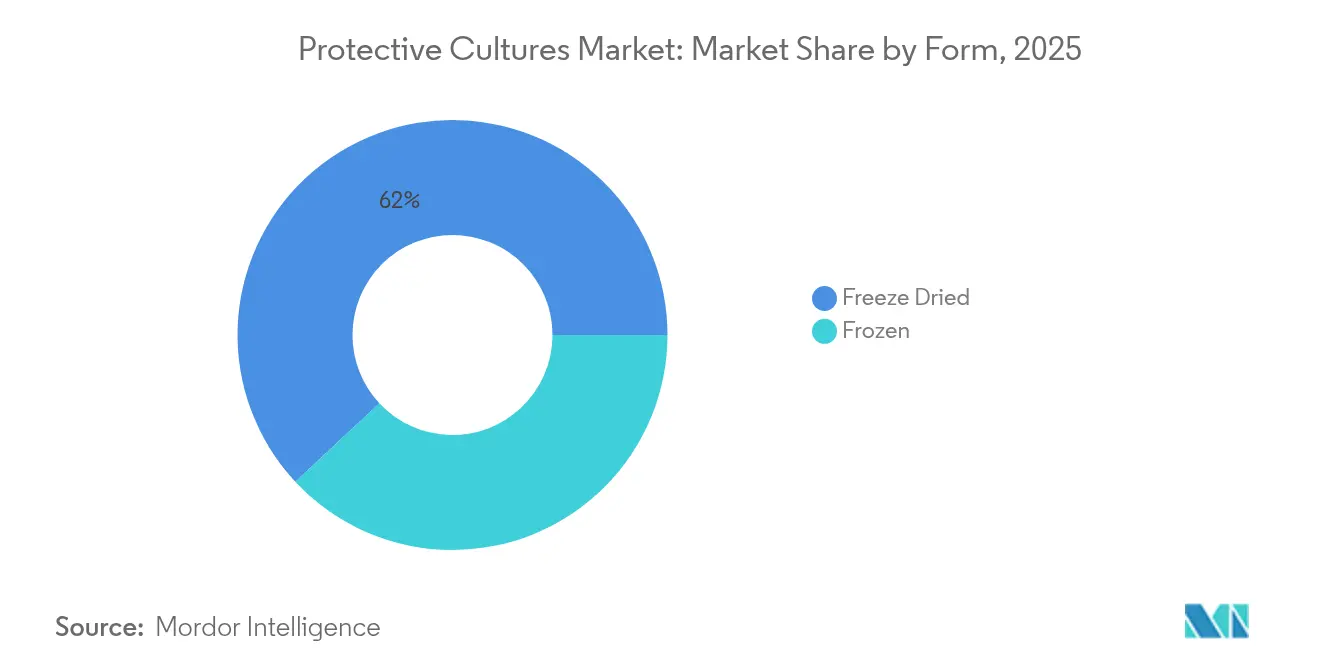

- By form, freeze-dried cultures led with 61.95% revenue share in 2025, whereas frozen cultures are projected to grow at 12.95% CAGR through 2031.

- By microorganism, bacterial strains accounted for 44.62% of the protective cultures market share in 2025; yeast cultures register the fastest forecast pace at 12.35% CAGR.

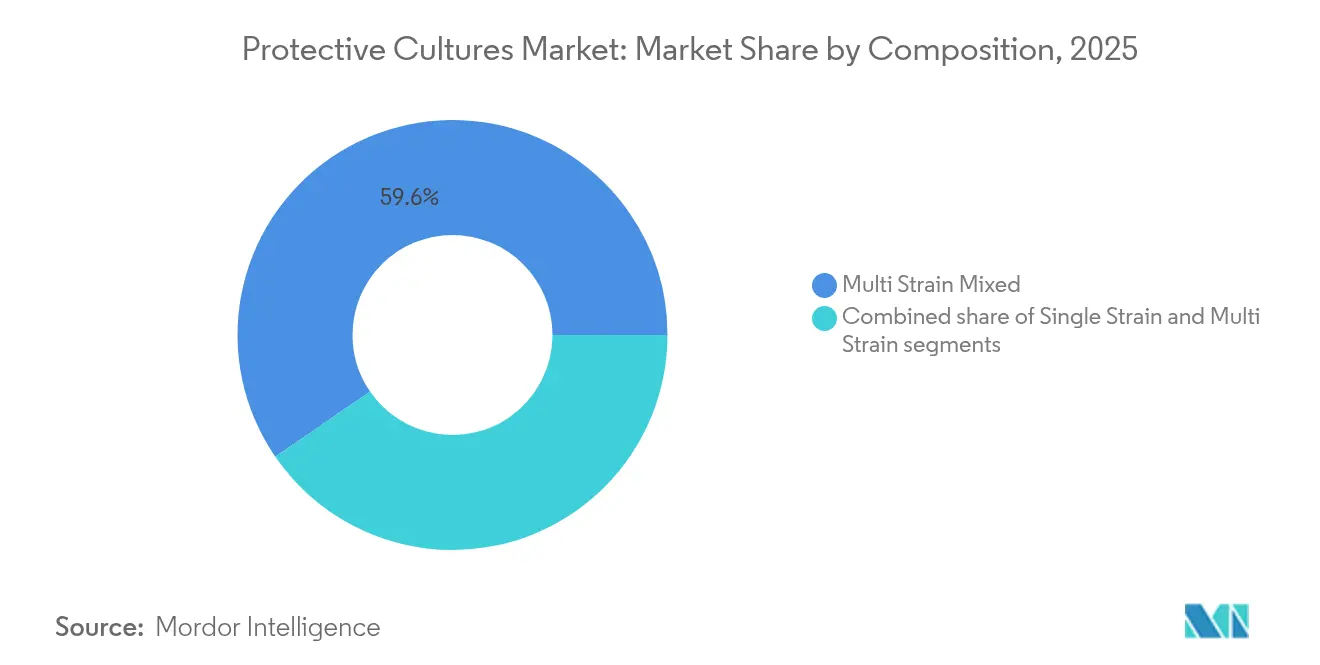

- By composition, multi-strain mixes commanded a 59.58% share in 2025 and are anticipated to rise at a 12.02% CAGR to 2031.

- By application, dairy products contributed 42.38% of revenue in 2025, while plant-based alternatives are set to expand 12.72% CAGR through 2031.

- By geography, North America captured a 32.05% share in 2025; Asia-Pacific represents the fastest regional trajectory at 12.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protective Cultures Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing demand for clean-label and natural preservation solutions | +2.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Expanding dairy production and need for extended shelf life | +2.1% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Expansion of ready-to-eat and convenience food markets | +1.9% | Global, with early gains in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Heightened consumer awareness of food safety and quality standards | +1.6% | Global | Medium term (2-4 years) |

| Rising popularity of fermented and functional foods | +1.4% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Growing focus on sustainable food production practices | +1.2% | Europe, North America, with expansion to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for clean-label and natural preservation solutions

Consumer rejection of synthetic additives drives protective cultures adoption, with consumers finding natural preservation ingredients acceptable despite concerns about shorter shelf life. This preference shift creates competitive advantages for manufacturers who successfully implement bioprotective solutions without compromising product quality or safety. Regulatory bodies increasingly support this transition, evidenced by the FDA's tolerance exemptions for multiple Bacillus strains, including B. subtilis CH4000 and B. licheniformis variants, eliminating regulatory barriers for natural preservation applications [1]Source: US Environmental Protection Agency, "Exempted several Bacillus species", www.epa.gov. The clean-label trend particularly benefits multi-strain formulations, which offer superior antimicrobial efficacy while maintaining ingredient transparency. Market leaders capitalize on this demand by developing culture blends that extend shelf life beyond conventional preservatives, addressing the fundamental consumer expectation for both naturalness and functionality. Advanced fermentation technologies enable producers to optimize strain combinations for specific food matrices, creating differentiated value propositions in competitive market segments.

Expanding dairy production and need for extended shelf life

Global dairy sector expansion necessitates innovative preservation solutions, particularly in emerging markets where cold-chain infrastructure limitations amplify spoilage risks. Queensland's dairy sector, contributing USD 13 billion to the regional economy with USD 4 billion farmgate value, exemplifies this challenge through innovations like Naturo's patented technology extending fresh milk shelf life to 60 days without heat treatment [2]Source: Queensland Government, "State-level initiatives highlighting technologies that stretch chilled milk life", www.qld.gov.au. This technological advancement demonstrates protective cultures' strategic importance in addressing supply chain inefficiencies and reducing food waste. IFF's HOLDBAC bioprotective cultures specifically target dairy applications, maintaining product freshness beyond traditional 'best before' dates while supporting manufacturers' sustainability objectives. In August 2024, the dairy industry's protective culture adoption accelerates through precision fermentation partnerships, exemplified by Fonterra's collaboration with Superbrewed Food to develop postbiotic protein ingredients with 85% protein content and enhanced stability. These developments position protective cultures as essential components in dairy value chain optimization, particularly for manufacturers targeting extended distribution networks and export markets.

Expansion of ready-to-eat and convenience food markets

Ready-to-eat meal segments drive protective culture innovation through complex preservation challenges involving multiple food components and varied storage conditions. This antimicrobial performance addresses critical food safety requirements for ready-to-eat products while supporting clean-label positioning. Convenience food manufacturers increasingly adopt multi-strain protective cultures to address diverse pathogen risks across product portfolios, leveraging technological advances in culture stability and cross-contamination prevention. The sector's growth correlates with urbanization trends and changing consumer lifestyles, creating sustained demand for preservation solutions that maintain product quality throughout extended distribution channels. Advanced packaging integration with protective cultures, including pH-sensitive indicators for real-time freshness monitoring, represents emerging technological convergence addressing convenience food safety challenges. These innovations position protective cultures as critical enablers for convenience food market expansion, particularly in emerging economies where cold-chain infrastructure development lags consumer demand growth.

Heightened consumer awareness of food safety and quality standards

Regulatory frameworks increasingly emphasize preventive food safety controls, creating market opportunities for protective culture applications that address hazard analysis and risk-based preventive controls. The FDA's extended comment period for preventive controls guidance reflects regulatory complexity surrounding food safety standards, impacting protective culture adoption strategies [3]Source: US Food and Drug Administration, "GRAS notices for novel strains", www.fda.gov . Consumer awareness drives demand for transparent preservation methods, with protective cultures offering verifiable antimicrobial mechanisms through competitive exclusion and metabolite production. China's comprehensive food safety standard updates, including 50 new or revised National Food Safety Standards, demonstrate global regulatory alignment supporting protective culture market expansion [4] Source: U.S Department of Agriculture,"50 updated National Food Safety Standards in 2025", www.usda.gov . Food safety consciousness particularly influences meat and seafood applications, where protective cultures address antibiotic-resistant pathogen concerns while maintaining product quality attributes.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High production costs of protective cultures | -1.8% | Global, with strongest impact in developing markets | Short term (≤ 2 years) |

| Challenges in maintaining culture stability and preventing cross-contamination | -1.4% | Global | Medium term (2-4 years) |

| Lengthy safety approvals for novel strains | -1.1% | Global, with regional variations | Long term (≥ 4 years) |

| Regulatory uncertainty or variation across regions | -0.9% | Global, with strongest impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs of protective cultures

Production cost pressures constrain protective culture adoption, particularly in price-sensitive market segments where synthetic preservatives maintain cost advantages. The requirement for specialized fermentation infrastructure, including controlled atmosphere conditions and contamination prevention systems, creates significant capital investment barriers for market entry. Advanced preservation technologies like flash freeze-drying reduce processing time and achieve maximum cell viability but require substantial equipment investments. Supercooling pretreatment methods enhance freeze-dried culture shelf life through exopolysaccharide thickness optimization and achieve high viability rates but add processing complexity and costs. These cost pressures particularly impact smaller manufacturers and emerging market applications, where price sensitivity limits premium preservation solution adoption. While strategic partnerships between culture producers and food manufacturers through precision fermentation collaborations offer potential cost mitigation via shared infrastructure investments and economies of scale, production cost challenges remain significant barriers to market penetration in cost-competitive food categories.

Challenges in maintaining culture stability and preventing cross-contamination

The protective cultures market faces distribution challenges due to the need to maintain culture stability across supply chains, which affects product effectiveness and market adoption. Quality control systems must prevent cross-contamination, especially in multi-strain formulations where preserving individual strain properties while preventing microbial interactions is crucial. While isochoric freezing technology helps maintain cellular structures by preventing ice crystal formation damage and preserves nutritional and sensory qualities while reducing microbial presence, it requires specialized equipment and process optimization. Market expansion in emerging economies remains limited due to stability issues in regions lacking proper cold-chain infrastructure. The European Food Safety Authority's Qualified Presumption of Safety framework provides stability assessment guidelines with updates every six months to reflect regulatory changes. Though advanced packaging and controlled atmosphere storage technologies could improve stability, high implementation costs and technical requirements restrict adoption, particularly among smaller market players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Freeze-Dried Dominance Faces Frozen Innovation

Freeze-dried cultures maintain market leadership with 61.95% share in 2025, reflecting established infrastructure and proven stability characteristics across diverse food applications. However, frozen cultures demonstrate superior growth potential at 12.95% CAGR through 2031, driven by technological advances in cryopreservation and reduced energy requirements. Flash freeze-drying innovations significantly reduce processing time while maintaining high cell viability, addressing traditional freeze-drying limitations of extended processing cycles and energy consumption. Supercooling pretreatment methods enhance freeze-dried culture longevity through protective protein expression and exopolysaccharide optimization, achieving viability rates during extended storage periods.

Frozen culture applications benefit from simplified handling requirements and reduced rehydration complexity, particularly advantageous for automated food processing systems. Isochoric freezing technology represents emerging preservation methods that maintain food quality without ice crystal damage, offering potential advantages for culture preservation applications. The form segmentation reflects broader industry trends toward processing efficiency and energy conservation, with frozen cultures positioned to capture market share through operational advantages and technological improvements. Distribution infrastructure considerations influence form selection, with freeze-dried cultures maintaining advantages in regions with limited cold-chain capabilities while frozen alternatives gain traction in developed markets with robust refrigeration networks.

By Microorganism Type: Bacterial Leadership Challenged by Yeast Innovation

Bacterial strains command 44.62% market share in 2025, leveraging established applications in dairy and meat preservation through lactic acid production and competitive exclusion mechanisms. Yeast-based cultures exhibit accelerated growth at 12.35% CAGR through 2031, driven by expanding applications in plant-based alternatives and fermented beverages. Bacillus species gained market acceptance through regulatory approvals, as several strains received FDA tolerance exemptions and GRAS status for food applications. Lactic acid bacteria remain the dominant choice due to their proven effectiveness against foodborne pathogens. For instance, Latilactobacillus sakei achieved more than 5-log reduction of Listeria monocytogenes under optimized conditions.

Mold applications remain specialized but demonstrate growth potential in specific fermented food categories, particularly in Asian markets where traditional fermentation practices drive acceptance. AB Mauri's acquisition of Omega Yeast Labs in August 2024 exemplifies strategic positioning in specialty yeast markets, combining global technology capabilities with innovative strain development. The microorganism segmentation reflects technological convergence between traditional fermentation applications and modern biopreservation requirements, with bacterial cultures maintaining established market positions while yeast innovations capture emerging application opportunities.

By Composition: Multi-Strain Formulations Drive Innovation

Multi-strain mixed compositions dominate with 59.58% market share in 2025 and maintain leadership through 12.02% CAGR growth, reflecting sophisticated formulation strategies that optimize antimicrobial efficacy across varied food matrices. Single strain applications serve specialized preservation requirements where specific pathogen targeting or regulatory constraints limit formulation complexity. Multi-strain formulations leverage synergistic antimicrobial mechanisms, combining organic acid production, competitive exclusion, and bacteriocin activity to achieve superior preservation performance compared to individual strain applications. DSM-Firmenich's Delvo Guard product line exemplifies multi-strain innovation, offering clean-label protective cultures specifically formulated for dairy applications with enhanced bioprotection capabilities.

Advanced strain selection methodologies enable precise formulation optimization for specific food categories, addressing diverse preservation challenges while maintaining product quality attributes. Multi-strain mixed compositions demonstrate particular advantages in complex food systems where multiple preservation mechanisms enhance overall antimicrobial efficacy and extend shelf life beyond single strain capabilities. The composition segmentation reflects industry maturation toward sophisticated biopreservation solutions that address diverse pathogen risks while supporting clean-label positioning. Regulatory acceptance of multi-strain formulations through EFSA's Qualified Presumption of Safety framework facilitates market expansion, with biannual updates reflecting ongoing safety assessment evolution. Strategic partnerships between culture producers and food manufacturers drive formulation innovation, leveraging combined expertise to develop application-specific solutions that optimize preservation performance while meeting regulatory requirements.

By Application: Dairy Dominance Meets Plant-Based Disruption

Traditional dairy applications maintain 42.38% market share in 2025, reflecting established preservation requirements and proven culture efficacy in milk, cheese, and yogurt production. Plant-based alternatives emerge as the fastest-growing segment at 12.72% CAGR through 2031, driven by expanding alternative protein markets and specialized preservation challenges. Fermentation technologies enhance plant-based product quality through improved digestibility, reduced anti-nutritional factors, and enhanced sensory characteristics, with lactic acid bacteria demonstrating particular effectiveness in legume-based applications. In May 2024 precision fermentation partnerships, exemplified by New Culture's collaboration with CJ CheilJedang for animal-free mozzarella production, demonstrate technological convergence supporting plant-based market expansion.

Meat, poultry, and seafood applications benefit from protective cultures' ability to address antibiotic-resistant pathogen concerns while maintaining product quality, with natural antimicrobial compounds like cowpea legumin extending beef shelf life from 6 to 12 days. Ready-to-eat meal segments drive innovation through complex preservation challenges involving multiple food components, with protective cultures offering solutions that address diverse pathogen risks while supporting convenience food market expansion. Other applications include fermented beverages, baked goods, and specialty foods, each presenting unique preservation requirements that drive specialized culture development.

Geography Analysis

North America commands 32.05% market share in 2025, leveraging established regulatory frameworks, advanced food processing infrastructure, and strong consumer acceptance of natural preservation solutions. The region benefits from comprehensive FDA guidance on protective culture applications and extensive GRAS recognition for bacterial strains, facilitating market development and product innovation. Asia-Pacific demonstrates the highest growth potential at 12.08% CAGR through 2031, driven by expanding food processing industries, urbanization trends, and increasing consumer awareness of food safety standards. China's comprehensive food safety standard updates, including new regulations for canned foods and food contact materials, create regulatory frameworks supporting protective culture adoption according to U.S. Department of Agriculture.

Europe maintains significant market presence through stringent food safety regulations and consumer preference for natural ingredients, with EFSA's Qualified Presumption of Safety framework providing regulatory clarity for protective culture applications. The region's robust dairy and meat processing sectors actively incorporate protective cultures to enhance product shelf life and safety. European food manufacturers increasingly adopt these solutions to meet clean-label requirements and reduce chemical preservative usage. The integration of protective cultures aligns with the region's focus on sustainable food production practices, supporting market growth through environmental and health considerations.

The geographic segmentation reflects varying regulatory maturity, infrastructure development, and consumer acceptance levels, with established markets providing stability while emerging regions offer growth opportunities. South America and Middle East and Africa demonstrate increasing adoption rates due to expanding food processing capabilities and modernizing preservation techniques. These regions show particular interest in protective cultures for traditional fermented foods and dairy products, driven by growing consumer awareness of food safety. The development of cold chain infrastructure and implementation of advanced food safety standards in these markets creates new opportunities for protective culture applications.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

The protective cultures market exhibits moderate consolidation, indicating established player dominance while maintaining opportunities for specialized entrants and technological innovators. Major players include Novo Holdings A/S, International Flavors & Fragrances Inc., DSM-Firmenich AG, and Lallemand Inc. Market leaders leverage comprehensive strain libraries, advanced fermentation capabilities, and global distribution networks to maintain competitive advantages across diverse application segments. The continuous investment in research and development enables companies to expand their strain collections. The implementation of high-throughput screening technologies accelerates the identification of novel protective strains. The establishment of regional innovation centers strengthens market presence and customer relationships.

Strategic positioning emphasizes technological differentiation through precision fermentation partnerships, exemplified by major collaborations between established food manufacturers and biotechnology companies for novel culture development. The integration of artificial intelligence enhances strain selection and optimization processes. The development of customized preservation solutions meets specific industry requirements. The formation of strategic alliances accelerates the commercialization of innovative protective culture solutions.

Emerging competitive dynamics include biotechnology startups introducing novel preservation mechanisms, such as Bountica's tasteless proteins, utilizing nutritional immunity principles to combat food pathogens. Technology adoption patterns emphasize automated culture production systems, advanced packaging integration, and real-time quality monitoring capabilities that enhance product efficacy and reduce contamination risks. Regulatory strategy becomes increasingly critical as companies navigate diverse approval requirements across global markets, with GRAS recognition and EFSA QPS status providing competitive advantages for market access and customer acceptance. Strategic acquisitions, exemplified by AB Mauri's purchase of Omega Yeast Labs, demonstrate consolidation trends targeting specialized capabilities and market access expansion.

Protective Cultures Industry Leaders

-

Novo Holdings A/S

-

International Flavors & Fragrances Inc.

-

DSM-Firmenich AG

-

Lallemand Inc.

-

Sacco System

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: China's National Health Commission and State Administration for Market Regulation released 50 new or updated National Food Safety Standards, including comprehensive regulations for canned foods and food contact materials, creating expanded regulatory frameworks for protective culture applications across diverse food categories.

- September 2024: Environmental Protection Agency established tolerance exemption for Bacillus licheniformis strain 414-01 in food commodities, eliminating regulatory barriers for agricultural and food processing applications when used according to label directions

- August 2024: AB Mauri North America acquired Omega Yeast Labs, a leading craft-brewing liquid yeast supplier, to enhance specialty yeast business capabilities and expand innovative strain offerings for diverse brewing applications.

- June 2024: Danone, Michelin, DMC Biotechnologies, and Crédit Agricole Centre France launched Biotech Open Platform with investment exceeding EUR 16 million to advance precision fermentation technologies for sustainable protein and enzyme production

Global Protective Cultures Market Report Scope

Global Protective Cultures Market is segmented by product form, microorganism type, application and geography. On the basis of product form, the market is segmented into freeze-dried and frozen. On the basis ofmicroorganism type, the market is segmented intoyeasts, molds, and bacteria. On the basis of application, the market is segmented into dairy products, meat, poultry and seafood products, ready to eat food products, and others. Also, the study provides an analysis of the protective culturesmarket in the emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

| Freeze-Dried |

| Frozen |

| Yeasts |

| Molds |

| Bacteria |

| Single Strain |

| Multi Strain |

| Multi Strain Mixed |

| Dairy Products |

| Meat, Poultry and Seafood |

| Ready-to-Eat Meals |

| Plant-based Alternatives |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Freeze-Dried | |

| Frozen | ||

| By Microorganism Type | Yeasts | |

| Molds | ||

| Bacteria | ||

| By Composition | Single Strain | |

| Multi Strain | ||

| Multi Strain Mixed | ||

| By Application | Dairy Products | |

| Meat, Poultry and Seafood | ||

| Ready-to-Eat Meals | ||

| Plant-based Alternatives | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected protective cultures market size by 2031?

The protective cultures market size is expected to reach USD 817.63 million by 2031, based on a 11.34% compound annual growth rate from 2026.

Which food applications benefit most from protective cultures?

Dairy products lead with 42.38% market share, followed by meat/poultry applications and plant-based alternatives.

How do freeze-dried and frozen protective cultures compare?

Freeze-dried cultures dominate with 61.95% market share due to ambient stability and established infrastructure, while frozen cultures are growing faster (12.95% CAGR) thanks to simplified handling, reduced rehydration complexity, and technological advances in cryopreservation.

Which regions show the strongest growth potential for protective cultures?

Asia-Pacific leads growth at 12.08% CAGR through 2031, driven by urbanization, expanding food processing industries, and increasing food safety awareness.

Page last updated on: