Procurement Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

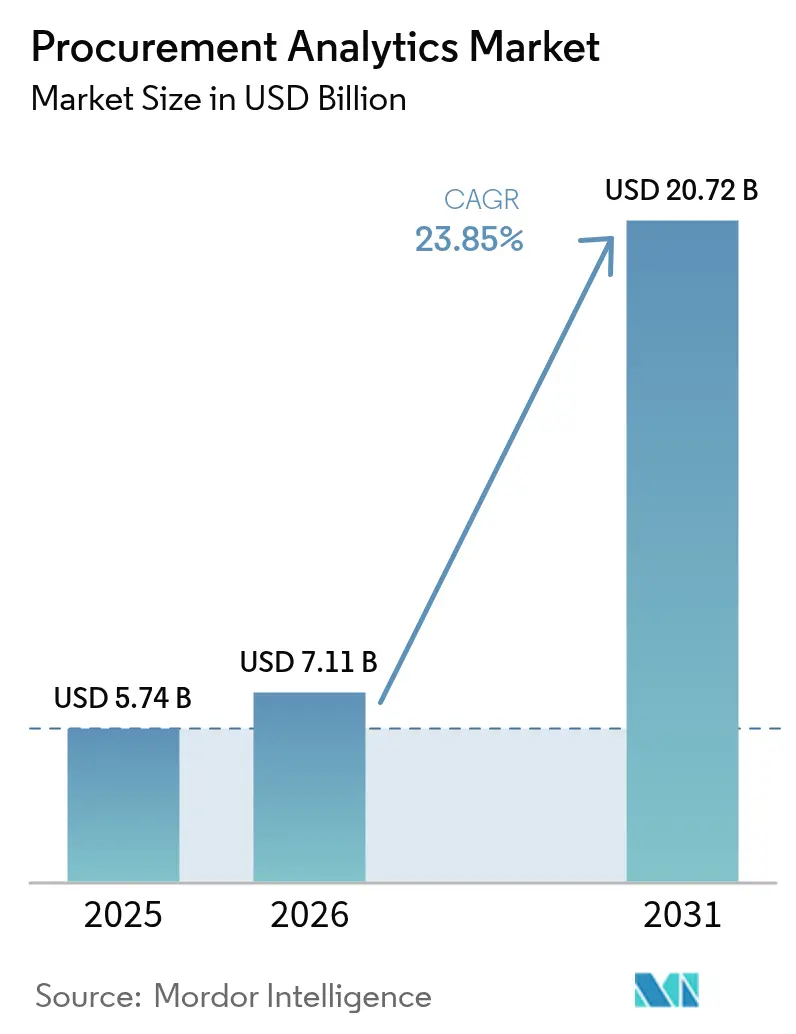

| Market Size (2026) | USD 7.11 Billion |

| Market Size (2031) | USD 20.72 Billion |

| Growth Rate (2026 - 2031) | 23.85% CAGR |

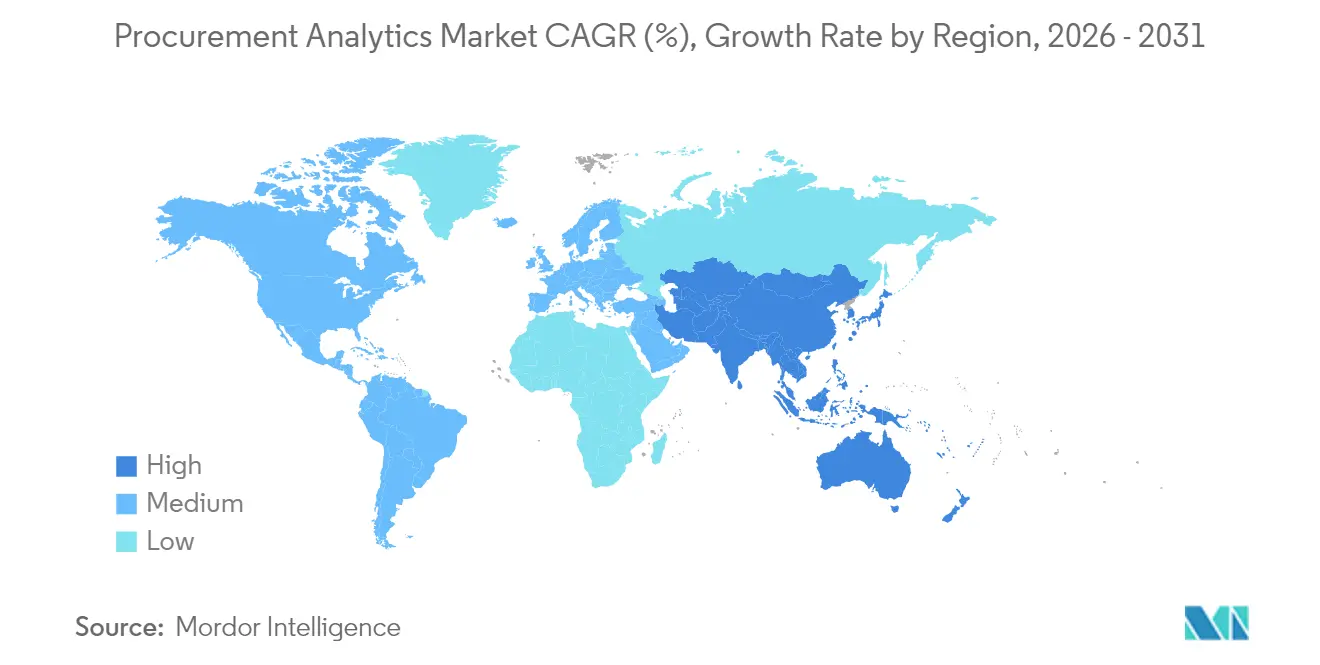

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Procurement Analytics Market Analysis by Mordor Intelligence

Procurement Analytics market size in 2026 is estimated at USD 7.11 billion, growing from 2025 value of USD 5.74 billion with 2031 projections showing USD 20.72 billion, growing at 23.85% CAGR over 2026-2031. Rapid cloud migration, the infusion of generative AI into source-to-pay workflows, and heightened attention to supply-chain resilience underpin the expansion of the procurement analytics market. Enterprises continue to replace disconnected legacy tools with unified analytics suites that elevate spend visibility, improve supplier performance, and automate tactical buying. Software remains the principal revenue generator, yet the steepest growth is shifting to services as organizations seek specialized expertise to integrate multi-tenant platforms with complex ERP landscapes. Adoption is accelerating among small and medium enterprises, whose cloud-native deployments bypass capital-intensive infrastructure while delivering enterprise-grade capabilities. Intensifying regulations—especially around ESG compliance and data sovereignty—are reshaping deployment decisions and prompting vendors to expand local hosting footprints.

Key Report Takeaways

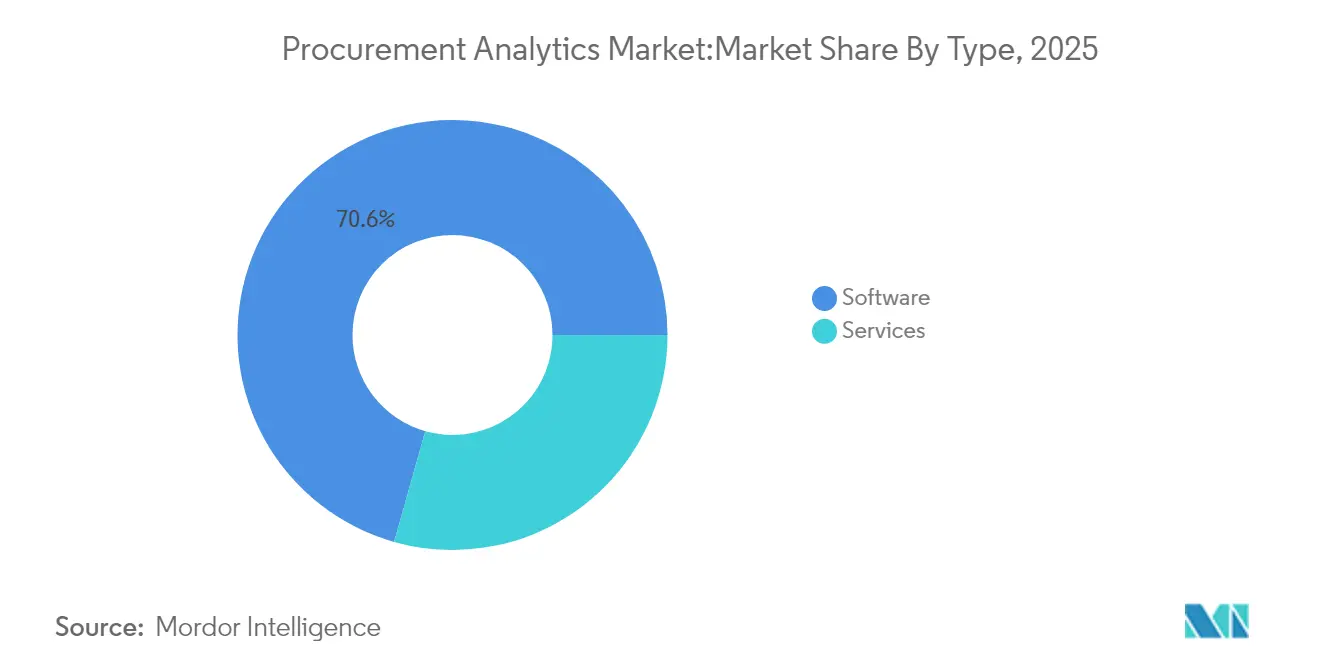

- By type, software held 70.62% of the procurement analytics market share in 2025, whereas services are projected to accelerate at 26.45% CAGR through 2031.

- By deployment, cloud models accounted for 64.35% of the procurement analytics market size in 2025 and will expand at a 25.15% CAGR to 2031.

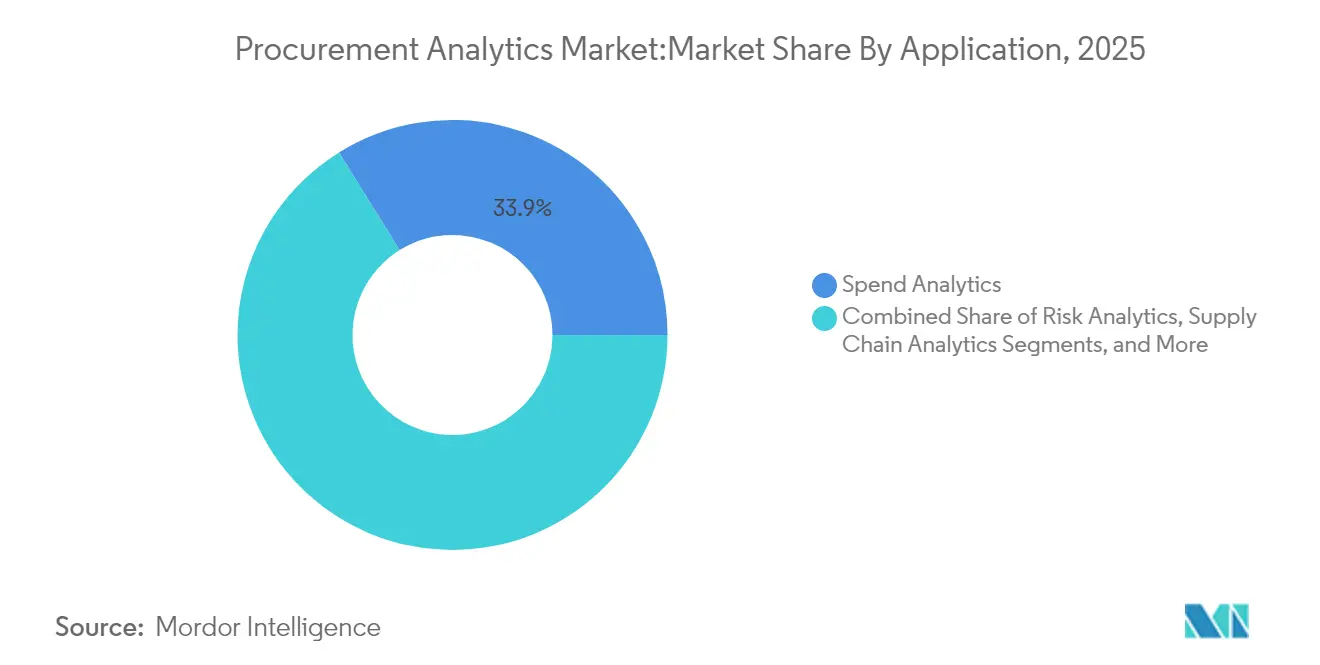

- By application, spend analytics led with 33.85% revenue share in 2025, while risk analytics is poised for the fastest 25.95% CAGR through 2031.

- By end-user industry, manufacturing commanded 26.74% of 2025 revenue; healthcare and life sciences is forecast to rise at a 25.80% CAGR to 2031.

- By organization size, large enterprises contributed 63.72% of 2025 revenue, though SME adoption is climbing at 26.70% CAGR.

- By geography, North America captured 36.95% of 2025 revenue; Asia-Pacific is the fastest-growing region at 26.10% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Procurement Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SaaS-first procurement-suite road-maps | +4.2% | Global; early uptake in North America and EU | Medium term (2-4 years) |

| Generative-AI copilots embedded in source-to-pay | +5.8% | North America and EU core; expanding to APAC | Short term (≤ 2 years) |

| Cloud-native TCO economics for mid-market buyers | +3.1% | Global; strong in APAC | Medium term (2-4 years) |

| ESG-linked supplier scoring mandates | +2.9% | EU and North America; expanding globally | Long term (≥ 4 years) |

| Predictive risk analytics for near-shoring strategies | +4.5% | Global; manufacturing hubs | Medium term (2-4 years) |

| Autonomous purchasing bots for tail-spend | +3.7% | North America and EU early adopters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

SaaS-first procurement-suite road-maps

Companies are retiring fragmented on-premise tools in favor of unified, cloud-native suites that scale on demand, enable organization-wide spend visibility, and accelerate analytics roll-out schedules. Adoption momentum is most evident among mid-market firms that lacked the capital for enterprise-grade infrastructure, yet now benefit from subscription pricing and automated updates. Once operational, these platforms consolidate disparate data sources, laying the groundwork for machine-learning models that optimize sourcing events and monitor compliance in real time. Vendors that bundle prebuilt connectors and low-code interfaces are gaining an edge because they shorten time-to-value and minimize reliance on scarce integration talent.

Generative-AI copilots embedded in source-to-pay

Generative AI modules embedded inside requisition, contract, and supplier-performance workflows are transforming procurement from reactive to insight-led operations. Fortune-500 adopters report double-digit cuts in processing time after letting AI draft sourcing documents, classify open-text spend, and surface negotiation levers. [1]Zycus, “GenAI Deployment within Fortune 500 Companies,” zycus.com Nevertheless, only a minority of enterprises allow unrestricted model access because sensitive commercial data requires rigorous governance. Vendors are responding by shipping policy-based access controls, localized language models, and in-platform redaction features that satisfy data-protection officers without stalling innovation.

Cloud-native TCO economics for mid-market buyers

Multi-tenant architectures erase capital outlays for hardware, routine maintenance, and disaster-recovery tooling. Mid-sized manufacturers using cloud suites report double-digit productivity gains and smoother upgrade cycles that free IT staff for value-added analytics projects. Enhanced elasticity also permits organizations to spin up sandboxed environments for AI model training without disrupting business-critical workloads, further lowering experimentation barriers.

ESG-linked supplier scoring mandates

Europe’s Supply Chain Due Diligence Directive and similar statutes in the United States are forcing buyers to embed environmental and social metrics into supplier evaluations. Platforms that integrate real-time emissions dashboards and diversity benchmarks are seeing uptake as procurement teams tie contract award criteria to carbon-footprint thresholds. [2]Supplier.io, “Beyond Good Intentions: The Tangible Business Case for ESG-Focused Procurement,” supplier.io Early adopters report tangible payoffs, including reduced risk of regulatory penalties and greater brand preference among sustainability-minded customers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of procurement-data engineers | −2.8% | Global; acute in North America and EU | Short term (≤ 2 years) |

| “Shadow IT” spend outside ERP integration | −1.9% | Global; higher in decentralized firms | Medium term (2-4 years) |

| Data-sovereignty regulations limiting cross-border hosting | −1.4% | EU and APAC; spreading globally | Long term (≥ 4 years) |

| Multi-tenant cost models pressured by Gen-AI GPU pricing | −1.1% | Global cloud deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of procurement-data engineers

Fifty-eight percent of enterprises struggle to recruit analytics talent who grasp both data-engineering principles and category-management nuances. The scarcity inflates wage bills and prolongs deployment cycles as over-extended teams juggle cleansing, normalization, and model-maintenance tasks. Some firms offset the gap by adopting low-code data-pipelines or outsourcing model-build projects to vendors, yet knowledge transfer remains a persistent bottleneck.

“Shadow IT” spend outside ERP integration

On average, enterprises run more than 1,000 cloud services, only a tenth of which are visible to central IT. Unregistered tools fracture spend data, hampering the end-to-end view that procurement analytics market solutions need to detect savings opportunities or policy violations. Education campaigns, sanctioned app-stores, and modern API hubs are emerging as preferred countermeasures, but governance programs still trail adoption velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services capture accelerating demand

Services held a comparatively small revenue base but are rising at 26.45% CAGR, outpacing platform growth as enterprises acknowledge that skilled implementation drives sustained outcomes. Advisory teams perform data-model tuning, supplier-onboarding, and change-management workshops that customers cannot replicate internally. Johnson Controls’ global roll-out, which linked 800 suppliers across 14 plants, underscored the scale of integration work required. The procurement analytics market size for services is therefore projected to expand rapidly, even though software retains a 70.62% share. Cross-training initiatives, best-practice libraries, and outcome-based pricing models are further boosting service uptake by aligning fees with realized savings.Platform providers continue reinforcing self-service configuration wizards, yet growing data-quality expectations keep professional services in demand. Vendors with embedded advisory arms can monetize both license and services streams, while pure-play consultancies specialize in complex ERP co-existence or multi-lingual supplier-enablement campaigns. As platform functionality standardizes, differentiation tilts toward implementation accelerators and domain-specific playbooks that cut time-to-value.

By Deployment: Cloud leadership intensifies

Cloud accounts for 64.35% of 2025 revenue, confirming its status as the dominant delivery model for the procurement analytics market. The economics improve when factoring in avoided hardware refreshes, automated patching, and usage-based scaling. Weinor’s adoption of a cloud suite trimmed requisition cycle times by up to 41%, equating to a full-time employee’s productivity gain. On-premise persists in regulated verticals that mandate local data residency, but even these buyers favor hybrid models that host sensitive records in private clouds while consuming AI engines from public clouds.Edge-ready architecture is emerging as a differentiator, enabling near-real-time analytics at factory sites with intermittent connectivity. Vendors that pre-certify with hyperscalers and colocation providers accelerate customer deployments while satisfying sovereignty constraints. Consequently, the procurement analytics market share of cloud deployments is set to widen further as smaller firms leapfrog on-premise generations altogether.

By Application: Risk analytics outpaces foundational spend analytics

Spend analytics remains the cornerstone, but the procurement analytics market size attributable to risk analytics is climbing fastest at 25.95% CAGR. The spike follows an uptick in disruptions ranging from raw-material shortages to geopolitical trade shifts, which exposed the limitations of rear-view dashboards. Platforms now ingest shipment trackers, macro-economic indicators, and supplier-financial scores to flag potential bottlenecks before they affect production. Semiconductor, medical-device, and food manufacturers increasingly rely on predictive alerts to justify buffer-stock or near-shoring strategies.Contract-lifecycle, supplier-performance, and demand-forecasting modules continue to expand in tandem, as organizations prefer suites that share a common data model. Vendors emphasize configurable risk-scoring engines so customers can weigh factors such as ESG performance or cyber-resilience alongside traditional lead-time metrics.

By End-user Industry: Healthcare accelerates, manufacturing dominates

Manufacturing held a 26.74% revenue share in 2025, leveraging analytics to orchestrate multi-tier supply chains and navigate volatile commodity pricing. Healthcare and life-sciences, however, is the standout growth engine at 25.80% CAGR, driven by stringent compliance reporting and pressure to lower procedure costs. Banner Health trimmed USD 3.2 million from surgical supplies by standardizing preference cards on an analytics platform. Similar momentum is unfolding in pharmaceuticals, where analytics track validated suppliers and monitor cold-chain integrity.Energy, transportation, and retail segments also intensify investment to counter inflation and boost ESG transparency. Multiple industries converge on one theme: analytics now influence not just unit price negotiations but broader resilience strategies, including dual-sourcing and capacity-buffer orchestration.

By Organization Size: SMEs embrace cloud-native simplicity

Large enterprises supplied 63.72% of 2025 revenue, yet SME subscriptions are growing at 26.70% CAGR as vendors roll out pay-as-you-grow tiers. Cloud deployment lowers the skill threshold, allowing lean teams to obtain AI-driven insights previously restricted to corporations with dedicated data-science groups. Provisur Technologies’ 20% spend reduction illustrates the magnitude of gains achievable when mid-market firms implement guided-sourcing analytics. To sustain traction, suppliers bundle pre-mapped commodity taxonomy, mobile approval workflows, and user-experience designs tuned for generalists.

Geography Analysis

North America led the procurement analytics market with 36.95% revenue in 2025. Mature cloud infrastructure, a dense ecosystem of specialized service providers, and continued tariff uncertainty encourage enterprises to invest in real-time cost-modeling engines. Universities and utilities confirm that more than 60% of their suppliers express tariff-related concerns, pushing buyers to deploy scenario-planning dashboards. Federal incentives for reshoring critical materials add another dimension, requiring analytics that integrate subsidy tracking and local-content thresholds.Asia-Pacific delivers 26.10% CAGR due to manufacturing-led digitization and supportive e-governance programs. Asia-Pacific posts the fastest growth. Government-led manufacturing 4.0 grants in China and South-East Asia subsidize automation that pairs machine-data streams with procurement KPIs. Multinational OEMs locate sourcing centers in Singapore to tap its cloud-first regulations, then extend shared services across ASEAN plants. Japanese conglomerates, historically cautious about public-cloud workloads, are adopting sovereign-cloud zones that satisfy domestic privacy statutes while enabling AI model training on multi-year purchasing archives.Europe ranks close behind North America in absolute spend. ESG compliance drives analytics to the boardroom, where supply-chain transparency becomes as strategic as price savings. France’s digital-sovereignty charter propels demand for regionally hosted suites, while the United Kingdom’s post-Brexit customs landscape amplifies the need for harmonized tariff-classification tools. Eastern European manufacturers, aiming to capture near-shoring contracts, invest in risk-analytics modules that quantify geopolitical exposure and logistics lead-time variability.

Competitive Landscape

The procurement analytics market remains moderately fragmented. ERP giants SAP, Oracle, and IBM leverage cross-selling access to large installed bases, bundling analytics into enterprise subscriptions that promise single-vendor simplicity. Best-of-breed vendors such as Coupa, Zycus, Jaggaer, and Sievo compete on rapid innovation cycles and vertical feature depth. Sievo’s in-platform AI assistant, for instance, auto-categorizes long-tail spend and recommends consolidation options.

Funding momentum signals continued disruption: LightSource secured USD 33 million to expand a supply-chain software suite designed to model tariff scenarios for US importers. Partnerships also matter. Johnson Controls and LeanDNA jointly built a digital thread spanning 800 suppliers, evidencing how integration specialists augment platform capabilities.

While consolidation activity intensifies as incumbents acquire AI startups to fast-track roadmap gaps, pure-play challengers differentiate through intuitive UX, preconfigured metrics, and industry-specific content packs. Data-sovereignty pressures compel all vendors to extend regional hosting and bring-your-own-key encryption, adding infrastructure complexity that favors scale players but allows niche providers to win in regulated pockets.

Procurement Analytics Industry Leaders

SAP SE

Oracle Corporation

IBM Corporation

SAS Institute Inc.

Coupa Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: LightSource raised USD 33 million to scale its tariff-scenario modeling platform, targeting manufacturers grappling with shifting trade policies.

- January 2025: SAP posted record Q1 2025 cloud revenue of EUR 4,993 million (USD 5,493 million), with cloud ERP modules—procurement analytics included—growing 34% year-over-year.

- December 2024: Zycus reported that 94% of procurement teams now employ generative-AI tools, up from 50% the prior year.

- November 2024: KNOLL Maschinenbau implemented Tacto’s platform to comply with Germany’s due diligence law while boosting spend transparency.

- July 2024: Flex paired with aPriori to introduce cost analytics that sharpen RFQ win rates, illustrating analytics’ role in competitive quoting.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the procurement analytics market as vendor-supplied software and related advisory services that transform spend, contract, supplier, and risk data into descriptive, diagnostic, and predictive insights that guide sourcing across direct and indirect categories. According to Mordor Intelligence, global license, subscription, and implementation revenues totaled USD 5.74 billion in 2025.

Scope exclusion: Hardware, stand-alone business intelligence tools, and internal analytics labor fall outside this assessment.

Segmentation Overview

- By Type

- Software

- Services

- By Deployment

- On-Premise

- Cloud

- By Application

- Spend Analytics

- Risk Analytics

- Supply Chain Analytics

- Contract Management

- Demand Forecasting

- Supplier Performance Management

- By End-user Industry

- Manufacturing

- Transportation and Logistics

- Retail and E-commerce

- BFSI

- IT and Telecommunication

- Healthcare and Life Sciences

- Energy and Utilities

- Other End-user Industries

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview procurement chiefs, category managers, and platform architects in North America, Europe, Asia-Pacific, and the Middle East. They then survey finance leaders in midsize firms. These exchanges validate savings targets, module penetration, and cloud price corridors flagged during secondary study.

Desk Research

We pull baseline signals from the US General Services Administration, the EU Open Data Portal, UN Comtrade, and the OECD e-procurement benchmark, which map digital adoption and trade flows. Our team then reviews company 10-Ks, investor decks, patent pulls via Questel, news on Dow Jones Factiva, and revenue splits from D&B Hoovers to size vendor footprints and average deal values. These sources are illustrative; many other public and paid references enrich the desk work.

A second pass lines up macro markers, national IT spend series, cloud migration statistics, and purchasing manager indexes so we can judge regional demand before numbers are frozen.

Market-Sizing & Forecasting

We rebuild enterprise software budgets from national IT spend totals, apply "spend under management" ratios, and cross-check outputs with selective bottom-up snapshots of vendor revenue and average contract value. Key drivers modeled include median indirect spend per employee, cloud deployment share, modules per customer, supplier portal usage, and currency shifts. A multivariate regression projects demand through 2030, while scenario analysis flexes uptake in manufacturing and healthcare cohorts.

Data Validation & Update Cycle

Outputs pass a three-layer review: junior analysts test formulas, senior peers probe anomalies, and principals sign off. Models refresh each year, with interim updates triggered by mergers, regulatory changes, or macro shocks.

Why Mordor's Procurement Analytics Baseline Earns Client Trust

Published estimates often diverge because firms select dissimilar application mixes, base years, and refresh cadences.

Our checks show others may omit services revenue or assume flat SaaS pricing, whereas we already see fees easing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.74 B (2025) | Mordor Intelligence | - |

| USD 4.86 B (2024) | Global Consultancy A | Narrower application scope and slower SaaS adoption assumption |

| USD 3.32 B (2022) | Industry Journal B | Outdated baseline and limited regional coverage |

These contrasts underline how our disciplined scope selection, timely validation, and clearly traceable variables give decision-makers a balanced, reproducible baseline.

Key Questions Answered in the Report

What is the current size of the procurement analytics market?

The procurement analytics market is valued at USD 7.11 billion in 2026 and is projected to reach USD 20.72 billion by 2031.

Which application segment is expanding fastest?

Risk analytics is the quickest-growing application, posting a 25.95% CAGR as firms prioritize supply-chain resilience.

Why are services growing faster than software?

Organizations increasingly need specialized expertise for data integration, AI model tuning, and change management, fueling a 26.45% services CAGR.

How are SMEs adopting procurement analytics solutions?

Cloud-native, pay-as-you-grow models eliminate heavy infrastructure costs, enabling SMEs to embrace analytics at a 26.70% CAGR.

Which region shows the strongest market growth?

Asia-Pacific leads in growth with a 26.10% CAGR, helped by manufacturing digitization programs and supportive government policies.

What role does ESG regulation play in procurement analytics adoption?

EU and North American due-diligence laws drive demand for platforms that embed supplier sustainability scoring, positioning analytics as a compliance essential.

Page last updated on: