Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.47 Billion |

| Market Size (2031) | USD 14.5 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fetal And Neonatal Monitoring Market Analysis by Mordor Intelligence

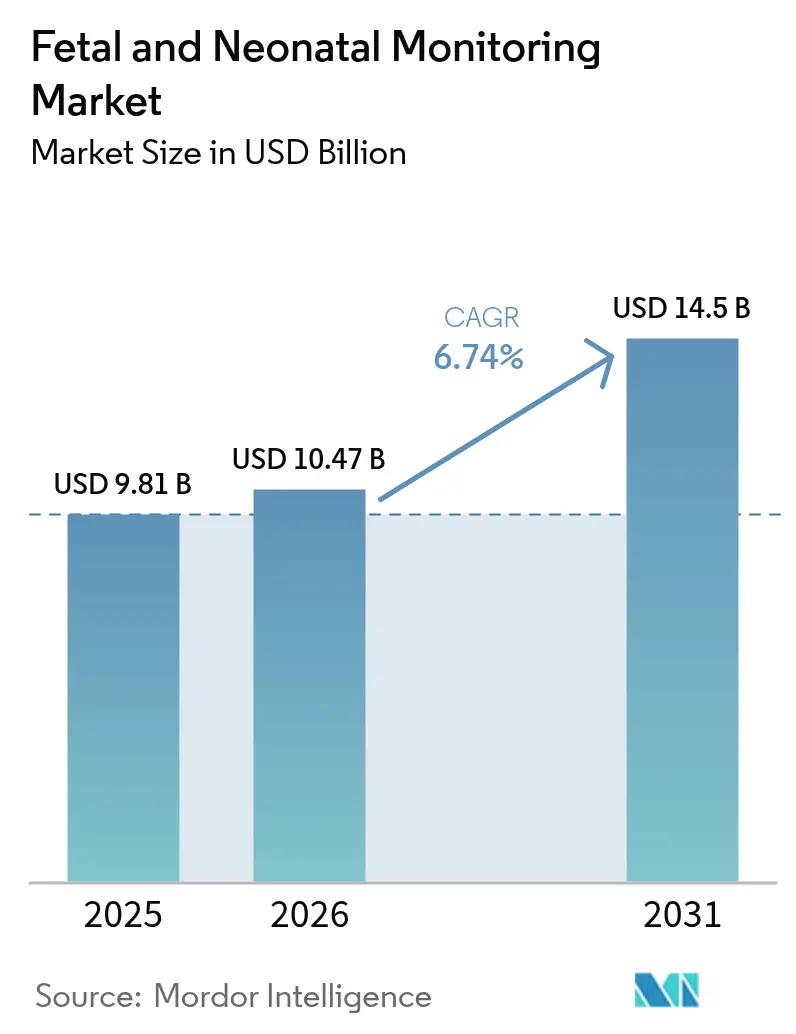

The Fetal And Neonatal Monitoring Market size is projected to be USD 9.81 billion in 2025, USD 10.47 billion in 2026, and reach USD 14.5 billion by 2031, growing at a CAGR of 6.74% from 2026 to 2031.

Demand escalates as pre-term deliveries climb, private hospitals in emerging economies add Level III and Level IV neonatal intensive-care beds, and artificial-intelligence modules are embedded in cardiotocography (CTG) and multiparameter platforms. Portable, battery-powered monitors are gaining traction in maternity-care deserts, helped by permanent U.S. reimbursement codes for remote patient monitoring. Meanwhile, the FDA’s cybersecurity rule, enforced from October 2024, marginally increases compliance costs yet catalyzes vendor consolidation, tilting share toward companies able to sustain ISO 27001 programs. Across regions, China’s three-child policy and India’s LaQshya quality mandate together underpin device procurement pipelines that run through 2031.

Key Report Takeaways

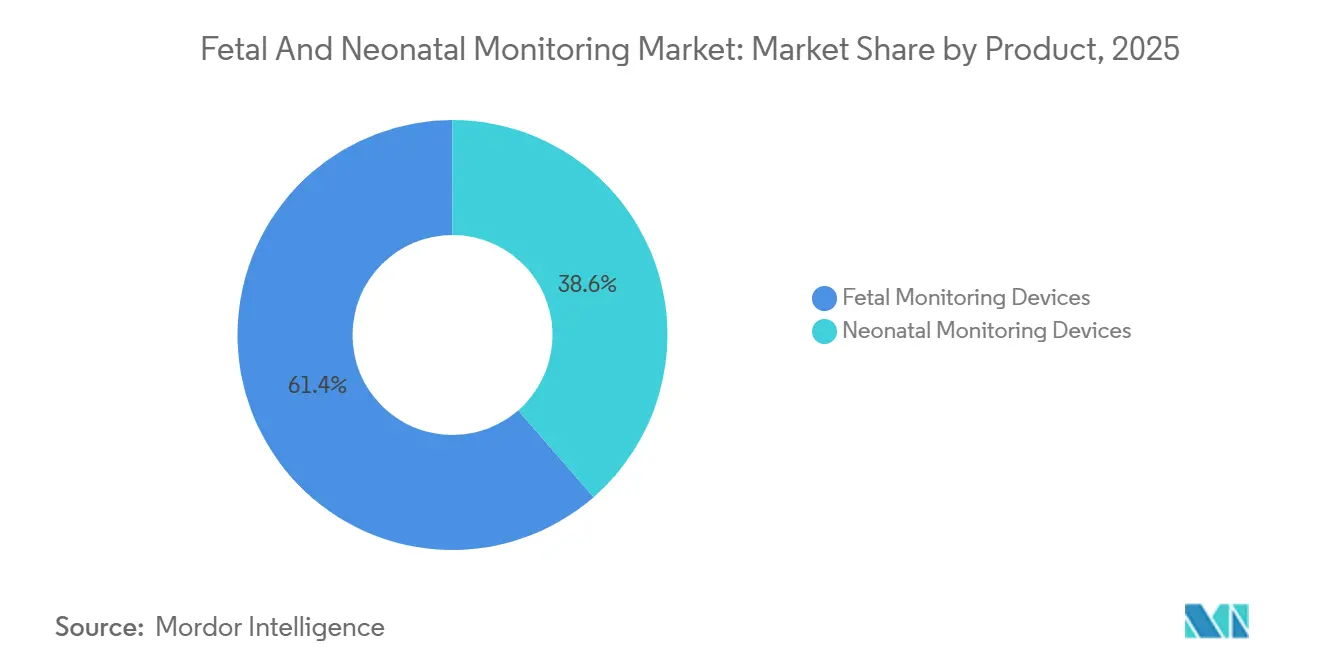

- By product category, fetal monitoring devices accounted for 61.45% of the fetal and neonatal monitoring market share in 2025, whereas neonatal monitoring devices are forecast to advance at a 7.43% CAGR through 2031.

- By method, non-invasive techniques dominated with 69.98% revenue in 2025; non-invasive techniques also regestered fastest growth with 7.65% CAGR through 2031.

- By portability, portable systems—though starting from a smaller base—are projected to grow at 8.23% a year, supported by maturing home-care reimbursement and FDA-cleared wireless patches.

- By end user, hospitals retained 53.12% spending in 2025, but standalone neonatal care centers are growing at 7.23% as payers steer extreme-prematurity cases into specialized, lower-cost facilities.

- By geography, North America led with 45.3% of 2025 revenue; Asia-Pacific is on track to post an 8.11% CAGR, buoyed by China’s maternal-health subsidies and India’s NICU build-outs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fetal And Neonatal Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pre-Term & Low-Birth-Weight Deliveries | +1.2% | Global, with highest incidence in Sub-Saharan Africa and South Asia | Medium term (2-4 years) |

| Government Maternity-Care Initiatives in Emerging Economies | +1.5% | APAC core (India, China, Indonesia), spill-over to MEA | Long term (≥ 4 years) |

| Expanding NICU Capacity Across Private Hospital Chains | +1.3% | APAC (India, China), Middle East GCC, select Latin America metros | Medium term (2-4 years) |

| Increasing Adoption of Advanced CTG & Ultrasound Systems | +0.9% | North America, Europe, urban APAC | Short term (≤ 2 years) |

| Integration of Maternal-Fetal Big-Data Platforms with Hospital Command Centers | +0.8% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Insurance-Reimbursement Shifts Favoring Remote Fetal Telemetry | +1.0% | United States (CMS coverage), select European payers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Pre-Term & Low-Birth-Weight Deliveries

The U.S. pre-term rate climbed to 10.41% in 2024 [1]March of Dimes "A profile of prematurity in United States" marchofdimes.org. Hospitals respond by deploying continuous electronic fetal monitoring in labor suites and stocking Level III NICUs with multiparameter devices that track heart rate, oxygen saturation, and transcutaneous carbon dioxide. Demand is also shifting to wireless Doppler patches for high-risk pregnancies managed at home, a segment enabled by permanent U.S. telehealth codes. Portable monitors compliant with ISO 80601-2-85 remain essential in rural Africa and South Asia, where mains power is unreliable. Collectively, these dynamics lift unit volumes faster than population growth, sustaining the fetal and neonatal monitoring market even in low-birth-rate economies.

Government Maternity-Care Initiatives in Emerging Economies

Between 2020 and 2025, India’s Janani Suraksha Yojana distributed cash incentives to 30 million mothers, channeling deliveries toward accredited facilities equipped with fetal monitors. China’s provinces have earmarked more than CNY 2 billion (USD 280 million) in 2024 for NICU upgrades under the three-child policy [2]National Health Commission of China, “Health Statistics Yearbook 2024,” nhc.gov.cn. Ethiopia, after equipping 500 health centers with handheld Dopplers, recorded an 18% stillbirth reduction in two years. These policies converge on low-cost, non-invasive devices, accelerating external Doppler and handheld ultrasound sales. Faster regulatory acceptance, with many ministries accepting FDA or CE clearances without in-country trials, condenses vendor entry times to under nine months, widening geographic reach for the fetal and neonatal monitoring market.

Expanding NICU Capacity Across Private Hospital Chains

Rainbow Children’s, Motherhood Hospitals and Aster DM collectively added 1,200 NICU beds in India during 2024, each ordering Mindray BeneVision monitors and Dräger Babylog ventilators. Similar expansions are under way in China and the Gulf Cooperation Council, creating a replacement cycle for analog monitors installed a decade ago. Stand-alone neonatal centers already account for 12% of new NICU beds and should reach 15% by 2028, reshaping procurement toward modular, cloud-connectable platforms. As capacity scales, service contracts bundled with software upgrades become a decisive revenue stream for vendors, reinforcing recurring value in the fetal and neonatal monitoring market.

Increasing Adoption of Advanced CTG & Ultrasound Systems

The FDA cleared the Dawes-Redman computerized CTG algorithm in March 2025, making automated interpretation mainstream and cutting observer variability by 30% [3]U.S. Food and Drug Administration, “510(k) Database,” fda.gov. Philips’ Avalon CL adds AI modules that push smartphone alerts, while handheld ultrasound probes priced under USD 5,000 proliferate in rural clinics. Regulatory pathways remain efficient, most devices stay in Class II—so innovation cycles shorten. Consequently, next-generation CTG and low-cost ultrasound together add fresh avenues for revenue diversification within the fetal and neonatal monitoring market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Device Accessibility in Rural LMIC Facilities | -0.7% | Sub-Saharan Africa, rural South Asia, Andean Latin America | Long term (≥ 4 years) |

| Lengthy 510(k)/CE Approval Timelines | -0.5% | United States, European Union | Medium term (2-4 years) |

| Rising Cyber-Security Insurance Premiums | -0.4% | North America, Western Europe | Short term (≤ 2 years) |

| Consumer Data-Privacy Concerns | -0.3% | EU, United States, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Device Accessibility in Rural LMIC Facilities

A 2024 World Bank audit revealed that 43% of primary health centers in Kenya, Tanzania and Uganda face daily power outages over four hours, hampering mains-powered CTG deployment. Consumable spoilage rates exceed 15% in tropical climates, inflating per-use costs. As a result, handheld Dopplers priced below USD 300 dominate, yet lack continuous waveforms needed for quality audits. Stillbirth rates remain stubbornly high—21 per 1,000 in sub-Saharan Africa—highlighting that hardware alone cannot offset workforce and infrastructure gaps. These factors collectively subtract 0.7 percentage points from the long-term CAGR of the fetal and neonatal monitoring market.

Lengthy 510(k)/CE Approval Timelines

Median U.S. 510(k) clearance for fetal monitors stretched to 12 months in 2024, and AI-rich devices required up to 18 months as the FDA sought additional validation data. Europe’s Medical Device Regulation adds six-to-nine-month delays amid notified-body bottlenecks. Start-ups bear the brunt, often needing multi-site trials that cost USD 5+ million. Resultant capital drag slows innovation diffusion, trimming 0.5 percentage points from fetal and neonatal monitoring market growth over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Neonatal Devices Narrow the Gap

Neonatal monitors are closing on fetal systems, expanding 7.43% annually against the broader fetal and neonatal monitoring market CAGR of 6.74%. Fetal CTG and external Doppler devices still anchor 61.45% of revenue, but AI-enabled software subscriptions, such as PeriGen Cerebro, blur hardware boundaries. Multiparameter neonatal platforms, exemplified by Mindray BeneVision and Dräger Infinity Delta, now bundle capnography, pulse oximetry, and invasive blood pressure in one chassis, driving upgrade cycles. Masimo’s 2024 acquisition of Stork extends neonatal surveillance beyond discharge, hinting at post-acute use cases that add fresh volume to the fetal and neonatal monitoring market size.

Demand migrates toward integrated modules because single-function monitors crowd limited NICU head-wall slots. Capnograph volumes rose notably in 2024 as lung-protective strategies targeted extremely low-birth-weight infants. AI layers that predict sepsis risk are next, with patent filings for machine-learning signal processing now 38% of total fetal-monitoring patent applications. Collectively, these shifts set a taller performance bar, tightening competition among incumbents while leaving niche space for cloud-native entrants.

By Method: Non-Invasive Dominance with Niche Invasive Applications

Non-invasive techniques command 69.98% of 2025 revenue and are also expected to register the fastest growth in the forecast period, with a CAGR of 7.65%. Transcutaneous CO₂ monitors slash neonatal heel sticks by 30%, improving nursing efficiency. Meanwhile, the ICE 80601 standard aligns alarm protocols across devices, streamlining clinician workflows. Conversely, invasive tools—fetal scalp electrodes, intrauterine pressure catheters—retain use in obese patients or when signal quality degrades. Goldtrace’s 2025 wireless scalp electrode mitigates cable clutter, but adoption remains selective, anchoring a low-volume, high-margin niche.

Training requirements are higher for invasive placements, and malpractice insurers in the United States often mandate credentialing, dampening uptake. Still, the devices’ diagnostic precision in complex labor ensures continued procurement, safeguarding a small but critical adjacency inside the larger fetal and neonatal monitoring market.

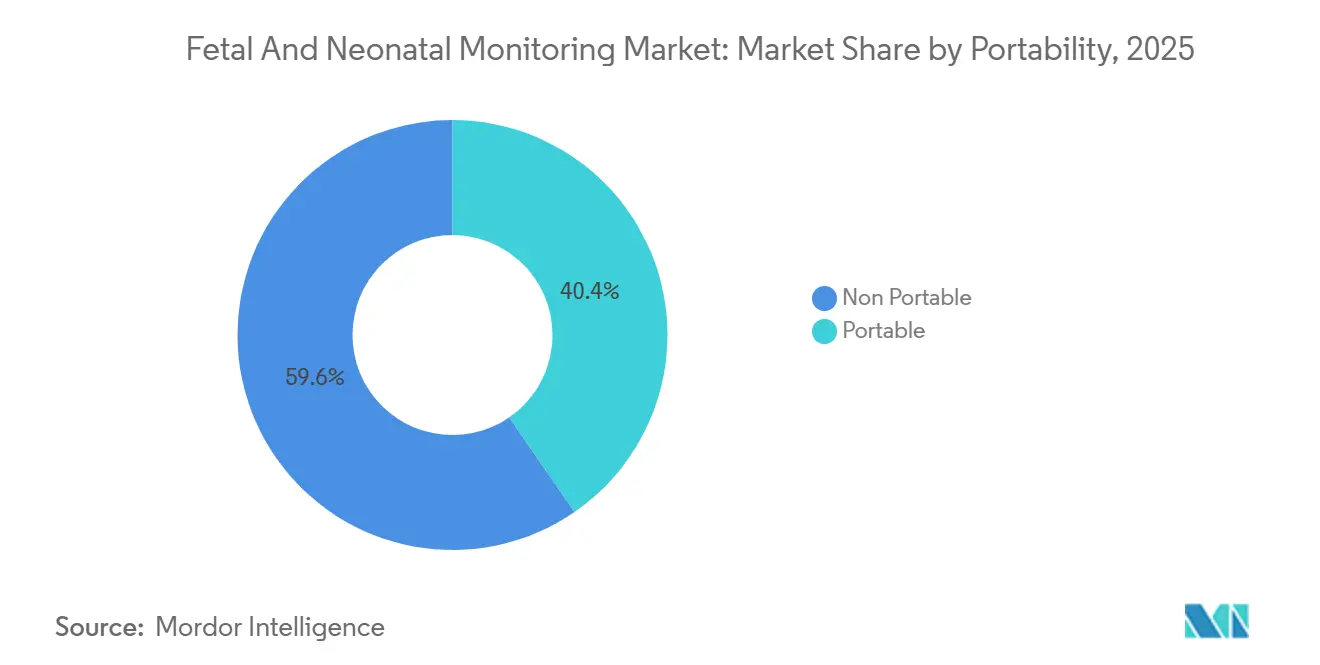

By Portability: Portable Monitors Capture Home and Ambulatory Niches

Portable monitors, weighing under 2 kg and offering eight-to-twelve-hour battery life, are on pace for an 8.23% CAGR. The CMS decision that codified remote-patient-monitoring codes 99453, 99457, and 99458 fuels U.S. demand for devices such as GE Novii+ and Nuvo INVU. In sub-Saharan Africa, handheld Dopplers dominate antenatal check-ups, sustaining baseline volume. Conversely, non-portable systems still hold 59.65% of revenue in 2025 because fixed CTG consoles and bedside NICU monitors integrate with enterprise electronic health records, a feature valued in high-acuity settings.

Vendor economics diverge: portable hardware sells for USD 200-800 but depends on consumable streams and subscription analytics; fixed units cost USD 15,000-40,000 and lock in multiyear service revenue equal to 20-25% of hardware value. Both models coexist, expanding the fetal and neonatal monitoring market size across care settings.

By End User: Neonatal Care Centers Emerge as Growth Locus

Hospitals remain the core buyer, yet stand-alone neonatal centers grow fastest at 7.23% because insurers pursue bundled payments and lower per-diem charges. Rainbow Children’s opened six such centers in 2024, each specifying Mindray BeneVision monitors and Dräger Babylog ventilators. These facilities target a 25% unit-cost edge versus tertiary hospitals, validating specialized, high-volume models of care that elongate the demand curve for the fetal and neonatal monitoring market.

Home-care settings, which accounted for a notable share of 2025 spending, receive oxygen thanks to permanent U.S. and selective European reimbursement. Yet, only 5% of the 2.2 million women living in maternity-care deserts adopted home fetal monitors in 2024 because of connectivity gaps and privacy worries. Over time, satellite connectivity and cheaper SIMs should lift penetration, adding another growth lever.

Geography Analysis

North America contributed 45.3% of global revenue in 2025, led by 3,000 U.S. hospitals with networked CTG and 800 Level III/IV NICUs. Permanent remote-monitoring codes amplify sales of wearable fetal patches, while the FDA’s cybersecurity mandate, activated in 2024, raises entry barriers for low-cost importers. Canada’s provincial health services replace decade-old consoles on standard five-year cycles, whereas Mexico lags because public budgets favor basic obstetric kits over digital networks.

Asia-Pacific is the fastest-growing theatre at 8.11% per year. China cut maternal mortality to 15.1 per 100,000 births in 2023 after pouring CNY 2+ billion into county-level maternal-child hospitals. Mindray shipped 18,000 neonatal monitors in 2024, up 22% year-on-year. India’s LaQshya program funnels INR 3,200 crore (USD 385 million) into labor-room upgrades across 5,000 facilities, supporting broad diffusion of portable Dopplers. Japan bucks the low-birth trend by spending heavily on AI-enabled monitors to offset staffing gaps, while Australia and South Korea grow at mid-single-digit levels tied to routine replacement.

Europe contributed significant share of 2025 revenue, but MDR-related CE delays and GDPR encryption rules dampen cloud-based deployments. Germany, France and the U.K. still account for majority of regional sales thanks to dense hospital networks. The Middle East and Africa combine for notable share; Gulf states invest in maternal-child megahospitals, but sub-Saharan Africa struggles with power outages that curtail digital uptake. South America faces currency swings that cap capital-equipment budgets.

Competitive Landscape

The fetal and neonatal monitoring market is moderately concentrated: the top five suppliers, GE Healthcare, Koninklijke Philips, Siemens Healthineers, Medtronic, and Becton, Dickinson and Company, collectively held the majority of revenue share in 2025. They defend turf through installed-base service contracts, interoperability modules, and vendor-financing programs that stretch hardware refresh cycles to seven-plus years. Region-specific challengers such as Mindray and Phoenix Medical capture notable share at home by pairing lower prices with local support.

Product differentiation tilts toward software. PeriGen Cerebro, installed in more than 500 U.S. hospitals, analyzes two million labor records to predict cesarean and hemorrhage risk. Masimo’s acquisition of Stork injects rainbow-sensor technology into home neonatal monitoring. Cybersecurity costs concentrate power; smaller Asian vendors lacking ISO 27001 credentials absorb margin hits of 3-5 percentage points, prompting mergers or exits.

White-space opportunities include portable multiparameter monitors for birthing centers and AI-driven analytics that flag fetal distress 20-30 minutes earlier than Doppler alone. Post-discharge neonatal monitoring could be worth USD 300 million by 2030, a niche Masimo now targets. Collectively, these niches add upside to the long-run trajectory of the fetal and neonatal monitoring market.

Fetal And Neonatal Monitoring Industry Leaders

-

GE Healthcare

-

Medtronic Plc

-

Becton, Dickinson and Company

-

Siemens Healthineers

-

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Philips deployed Avalon CL cableless monitors and IntelliSpace Perinatal at Qatar’s The View Hospital, enhancing continuous monitoring with greater maternal mobility

- May 2025: GE HealthCare and Raydiant Oximetry began joint R&D on fetal oxygen-saturation monitoring, aiming to improve distress detection.

Global Fetal And Neonatal Monitoring Market Report Scope

As per the scope of the report, fetal and neonatal monitoring devices are machines used for monitoring and designed to take care of the unique needs of unborn fetal and newborn babies.

The fetal and neonatal monitoring market is segmented by product, method, portability, end-user, and geography. By product, it is segmented into fetal monitoring devices (external doppler HR monitors, cardiotocography (CTG) systems, uterine contraction monitors, fetal pulse oximeters, wireless/wearable fetal patches, ai-enabled predictive platforms, and other fetal monitoring devices) and neonatal monitoring devices (cardiac monitors, capnographs, blood-pressure monitors, pulse oximeters, integrated multiparameter monitors, respiratory monitors, and other neonatal monitoring devices). By method, the market is segmented into invasive and non-invasive. By portability, the market is divided into portable and non-portable. By end users, the market is segmented into hospitals, neonatal care centers, home-care settings, and other end users.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

By Product

| Fetal Monitoring Devices | External Doppler HR Monitors |

| Cardiotocography (CTG) Systems | |

| Uterine Contraction Monitors | |

| Fetal Pulse Oximeters | |

| Wireless/Wearable Fetal Patches | |

| AI-Enabled Predictive Platforms | |

| Other Fetal Monitoring Devices | |

| Neonatal Monitoring Devices | Cardiac Monitors |

| Capnographs | |

| Blood-Pressure Monitors | |

| Pulse Oximeters | |

| Integrated Multiparameter Monitors | |

| Respiratory Monitors | |

| Other Neonatal Monitoring Devices |

By Method

| Invasive |

| Non-Invasive |

By Poribility

| Portable |

| Non Portable |

By End User

| Hospitals |

| Neonatal Care Centres |

| Home-Care Settings |

| Other End Users |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Fetal Monitoring Devices | External Doppler HR Monitors |

| Cardiotocography (CTG) Systems | ||

| Uterine Contraction Monitors | ||

| Fetal Pulse Oximeters | ||

| Wireless/Wearable Fetal Patches | ||

| AI-Enabled Predictive Platforms | ||

| Other Fetal Monitoring Devices | ||

| Neonatal Monitoring Devices | Cardiac Monitors | |

| Capnographs | ||

| Blood-Pressure Monitors | ||

| Pulse Oximeters | ||

| Integrated Multiparameter Monitors | ||

| Respiratory Monitors | ||

| Other Neonatal Monitoring Devices | ||

| By Method | Invasive | |

| Non-Invasive | ||

| By Poribility | Portable | |

| Non Portable | ||

| By End User | Hospitals | |

| Neonatal Care Centres | ||

| Home-Care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will the fetal and neonatal monitoring market grow through 2031?

Revenue is projected to rise from USD 10.47 billion in 2026 to USD 14.50 billion by 2031, reflecting a 6.74% CAGR

Which product segment is expanding quickest?

Neonatal monitoring devices are forecast to grow 7.43% annually, narrowing the gap with fetal devices.

Why is Asia-Pacific the fastest-growing region?

China’s three-child policy, India’s LaQshya program and private NICU investments give Asia-Pacific an expected 8.11% CAGR.

What role does AI play in new monitors?

Algorithms such as Dawes-Redman and PeriGen Cerebro automate CTG interpretation and predict complications, lowering clinician workload and intervention time.

What are key barriers to rural deployment?

Power outages, consumable logistics and limited staff training slow adoption in low-income countries despite low-cost handheld Dopplers.

Page last updated on: