Intrapartum Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

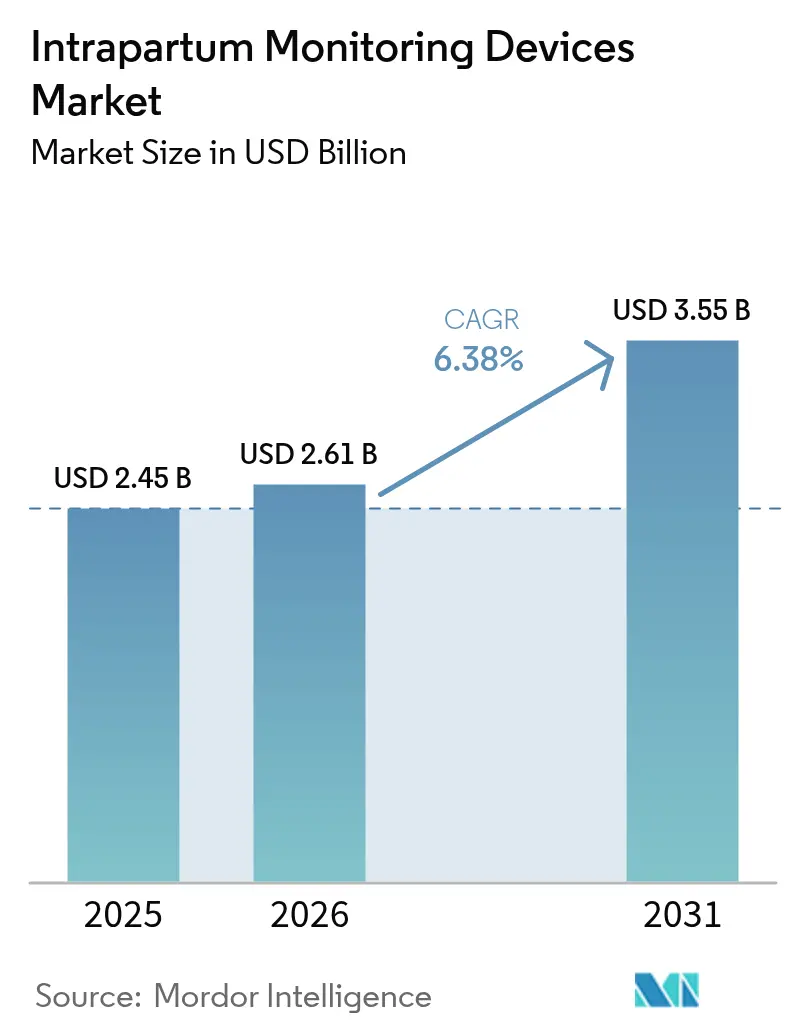

| Market Size (2026) | USD 2.61 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

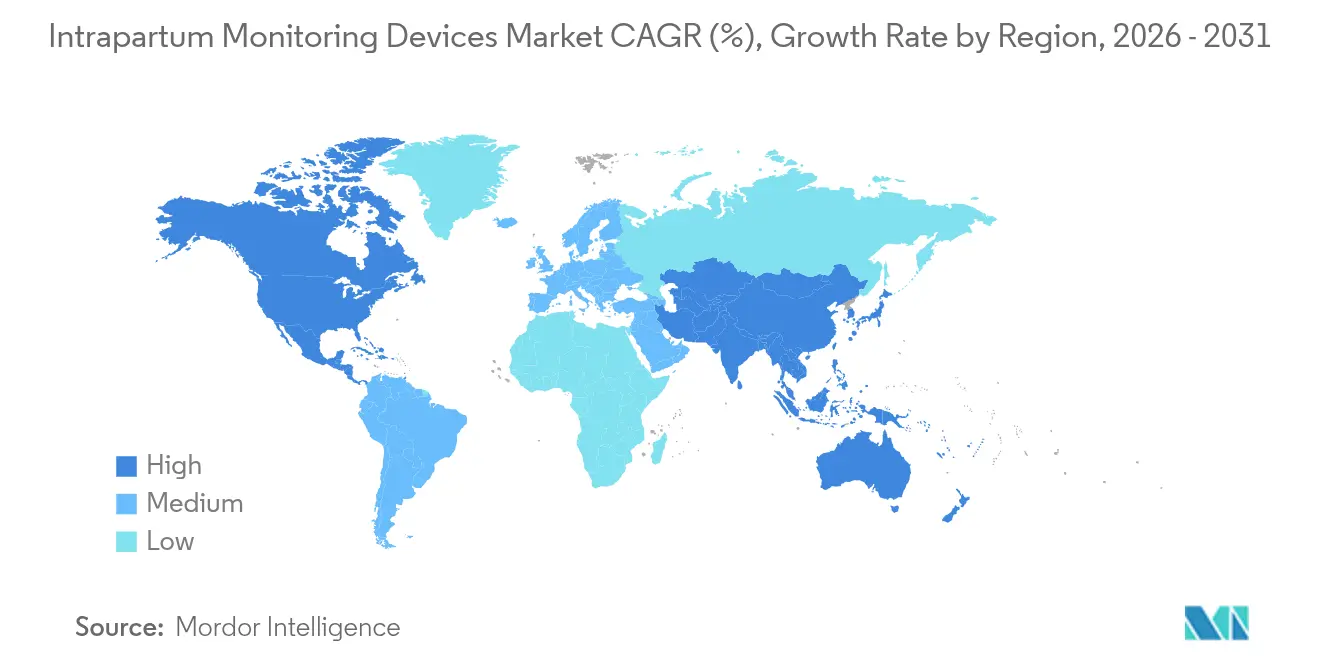

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

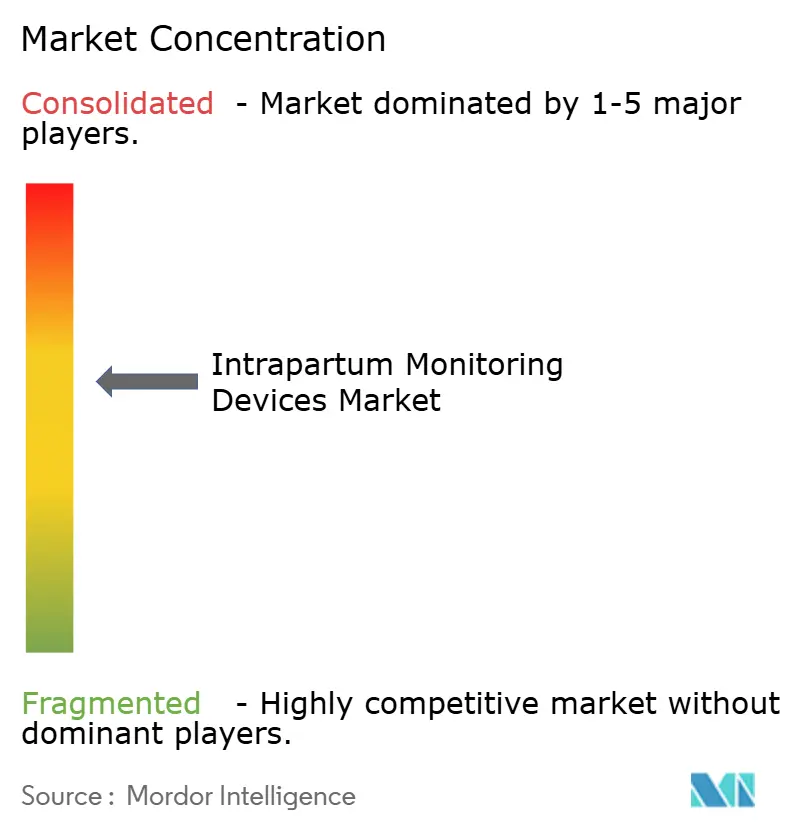

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Intrapartum Monitoring Devices Market Analysis by Mordor Intelligence

The Intrapartum Monitoring Devices Market size was valued at USD 2.45 billion in 2025 and estimated to grow from USD 2.61 billion in 2026 to reach USD 3.55 billion by 2031, at a CAGR of 6.38% during the forecast period (2026-2031). Growth momentum reflects the rapid pairing of artificial intelligence with traditional cardiotocography, where deep-learning models have achieved 97.9% accuracy in separating fetal and maternal heart signals. Rising pre-term birth prevalence—up 12% in the United States between 2014 and 2022—and the parallel increase in NICU admissions fuel demand for smarter surveillance during labor. Healthcare providers also favor non-invasive technologies that improve maternal mobility; these external systems captured almost 70% of 2024 revenues and continue to expand as reimbursement frameworks reward patient-comfort metrics. Meanwhile, manufacturers differentiate through portable, AI-ready devices that serve rural facilities and emergency teams, a positioning reinforced by policy mandates requiring fetal monitoring hardware in all labor rooms from January 2026.

Key Report Takeaways

- By product type, electrodes held 64.88% of the intrapartum monitoring devices market share in 2025, while monitors are projected to advance at a 6.89% CAGR through 2031.

- By monitoring method, non-invasive systems accounted for 69.22% of the intrapartum monitoring devices market size in 2025 and are growing at 6.96% CAGR to 2031.

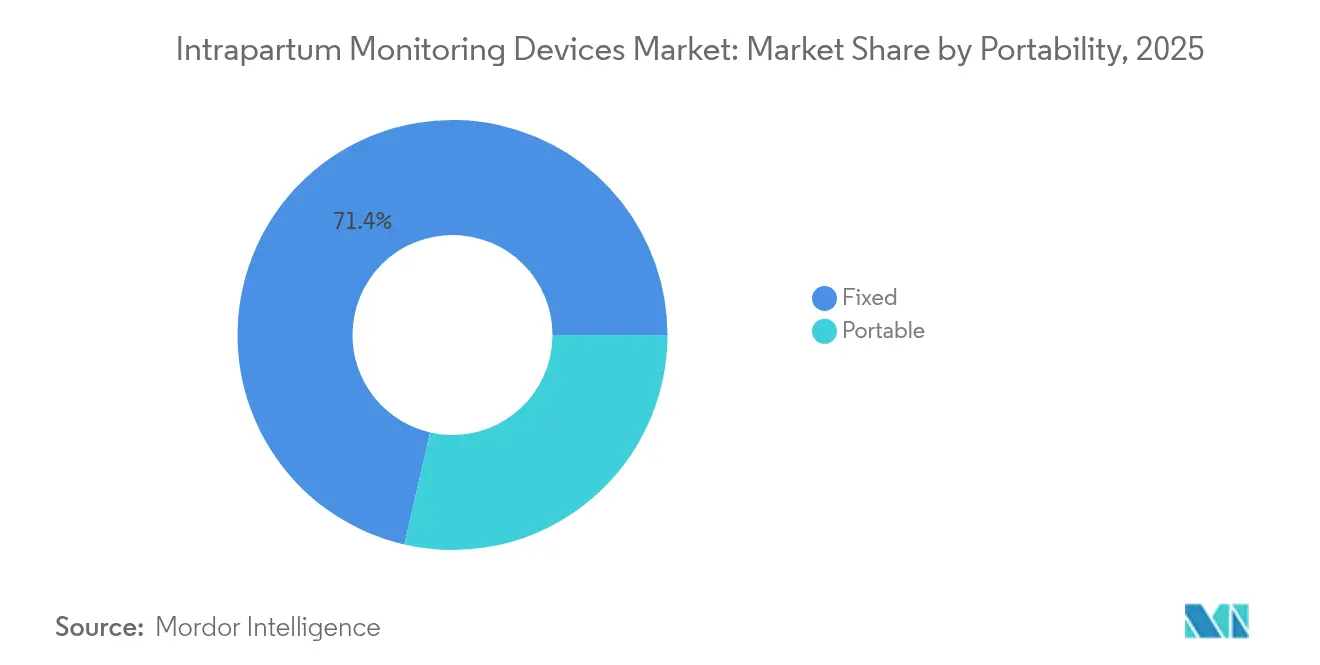

- By portability, fixed units controlled 71.40% revenue in 2025; portable solutions are slated for the quickest expansion at 7.05% CAGR.

- By end-user, hospitals commanded 64.95% share in 2025, while specialty clinics exhibit the strongest CAGR of 6.74% toward 2031.

- By geography, North America led with 41.85% 2025 share, whereas Asia-Pacific is poised for the steepest 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intrapartum Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of non-invasive fetal ECG technology | +1.2% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Rising pre-term births & NICU admissions | +1.8% | Global, particularly acute in North America & Asia-Pacific | Short term (≤ 2 years) |

| Government mandates on intrapartum monitoring standards | +0.9% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth of high-risk pregnancies in women more than 35 yrs | +1.1% | Global, concentrated in developed economies | Medium term (2-4 years) |

| AI-powered real-time labour analytics embedded in CTG systems | +1.3% | North America & Europe, with rapid Asia-Pacific adoption | Short term (≤ 2 years) |

| Reimbursement uplifts for remote labour wards in Sub-Saharan Africa | +0.4% | Sub-Saharan Africa, with spillover to other LMICs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Non-Invasive Fetal ECG Technology

Non-invasive fetal electrocardiography offers beat-to-beat heart-rate analysis without belts or scalp electrodes, matching or surpassing Doppler accuracy, particularly in high-BMI patients. Its freedom of movement boosts maternal satisfaction scores, a metric now tied to hospital reimbursement. Pandemic-era remote-monitoring pilots validated home-based ECG patches that transmit continuous data to clinicians, lowering exposure risk while sustaining oversight. Health-system purchasing committees thus rank mobility, comfort, and signal robustness as core criteria, pushing suppliers to embed ECG channels into wireless patch platforms. Start-ups focused on AI interpretation layer additional value by converting continuous waveforms into actionable alerts within seconds.

Rising Pre-Term Births & NICU Admissions

Worldwide, 13.4 million babies were born preterm in 2020, equivalent to 9.9% of live births [1]Ellen Bradley, "Born too soon: global epidemiology of preterm birth and drivers for change," Reproductive Health," reproductive-health-journal.biomedcentral.com. In the United States, NICU admissions rose from 8.7% in 2016 to 9.8% in 2023. Each NICU day costs USD 3,000–5,000, making early intrapartum detection financially attractive to payers [2]CDC, “National Center for Health Statistics Natality Files,” cdc.gov. Advanced monitoring that flags decelerations or uterine tachysystole minutes earlier can reduce emergency cesareans and neurodevelopmental morbidity. The trend is amplified by women delaying childbirth; pregnancies in mothers > 35 years carry higher risks and more often trigger continuous electronic surveillance rather than intermittent auscultation.

Government Mandates on Intrapartum Monitoring Standards

CMS Conditions of Participation will obligate U.S. hospitals to keep fetal dopplers and cardiac monitors within immediate reach of every labor room by January 2026 [3]United States Code of Federal Regulations, “Medicare/Medicaid Conditions of Participation for Hospitals,” cfr.gov. Similar requirements surface across Europe as EU-MDR codifies safety and performance benchmarks. Compliance extends beyond hardware to training and traceability, lifting demand for software updates that log staff proficiency and generate audit artifacts. The FDA’s forthcoming Quality System Regulation alignment with ISO 13485, effective February 2026, elevates documentation depth and lifecycle vigilance. These moves collectively standardize baseline technology adoption and incentivize premium analytics that document preventative interventions.

Growth of High-Risk Pregnancies in Women More Than 35 Years

Machine-learning classifiers using maternal age, BMI, and obstetric history now reach 91% accuracy in predicting high-risk pregnancies. As delayed childbearing expands in OECD economies, first-time mothers over 35 represent the fastest-growing cohort. Clinical guidelines prescribe continuous CTG for this demographic, multiplying monitor utilization hours per labor case. Staffing norms require 1:1 nurse-to-patient ratios in high-risk rooms, prompting health systems to lean on smart central stations that aggregate multibed data and surface deterioration early. Color Doppler ultrasound studies confirm abnormal flow indices in such pregnancies correlate with fetal distress, reinforcing continuous monitoring adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital outlay for advanced central surveillance stations | -0.8% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Stringent FDA & EU-MDR clinical evidence demands | -0.6% | North America & Europe, with global spillover effects | Long term (≥ 4 years) |

| Cyber-security liabilities of Wi-Fi enabled CTG monitors | -0.4% | Global, with heightened concern in developed markets | Short term (≤ 2 years) |

| Shortage of trained obstetric nurses | -0.7% | Global, most severe in rural and underserved areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Outlay for Advanced Central Surveillance Stations

Hospitals investing in multi-bed fetal telemetry platforms often face seven-figure budgets when integration with EHR, cybersecurity hardening, and staff re-training are included. Prisma Health’s USD 41 million smart-bed deployment across 1,500 units illustrates the scale of capital commitments. Procurement tenders such as BARTS Health NHS Trust’s site-wide vital-signs monitoring call for open APIs and ISO 27001 compliance, adding IT overhead. Under-funded community hospitals postpone upgrades, creating a tiered technology landscape where rural mothers receive palpation or intermittent doppler checks instead of continuous CTG.

Stringent FDA & EU-MDR Clinical Evidence Demands

LucidAI’s fetal monitoring application underwent validation on 65,324 ultrasound images from 2,985 fetuses before clearance, reflecting the evidence bar for algorithmic devices. Post-market surveillance now demands real-world performance logging, and annual software updates trigger new regulatory filings. Small manufacturers bear higher per-unit costs, nudging them toward OEM licensing or partnership exits. Simultaneously, the FDA’s cybersecurity guidance obliges patch cycles and vulnerability disclosures, widening the resource gap between incumbents and entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Integrated Monitors Outpace Electrode Mainstays

Electrodes retained 64.88% revenue in 2025, underscoring their indispensable role in signal capture across all modalities. Yet monitors post a faster 6.89% CAGR, reflecting demand for multi-parameter, AI-ready platforms that house fetal, maternal, and uterine channels in one chassis. GE’s Novii wireless patch incorporates ECG and EMG within a belt-free shell that elevates patient comfort while satisfying documentation mandates. Samsung’s USD 92.4 million Sonio purchase highlights the premium on ultrasound-linked analytics that augment CTG workflows. Such integrations deliver holistic intrapartum monitoring devices market value propositions that transcend hardware replacement cycles. Electrode unit sales nonetheless rise steadily because each monitor still needs disposable or reusable transducers, preserving a large consumables revenue stream.

Second-generation monitors bundle cloud connectivity and decision support, shifting purchasing criteria from hardware specifications toward software roadmaps. EDAN’s F3 fetal monitor offers on-board CTG analytics, easing interpretation load for junior staff. Vendors exploring subscription-based algorithm updates can smooth revenue while hospitals gain access to continuously improving classifications without capital refresh. The resulting convergence repositions monitors as software platforms backed by consumable electrodes, ensuring lasting traction within the intrapartum monitoring devices market.

By Monitoring Method: External Platforms Sustain Dual Leadership

Non-invasive systems captured 69.22% of 2025 revenue and are forecast for a 6.96% CAGR, maintaining dual leadership in size and growth. External Doppler ultrasound and tocodynamometers dominate routine obstetric care because they avoid cervical dilation and infection risk. Intrapartum monitoring devices market size gains further as new patches relay signals via Bluetooth, freeing mothers to ambulate or use birthing balls without strap readjustments. Internal scalp electrodes and intrauterine pressure catheters remain the precision gold standard when obesity, malpresentation, or signal noise impede external readings. Recent trials show internal CTG neither raises cesarean incidence nor worsens neonatal outcomes versus external monitoring, potentially broadening clinical indications. However, the need for ruptured membranes limits usage.

Hybrid telemetry arranges dual benefits: high-fidelity signals plus mobility. University of Helsinki findings on simultaneous maternal pulse recording confirm that artifact filtering prevents neonatal encephalopathy, accelerating adoption of multiparameter solutions. External platforms therefore evolve to include maternal ECG channels that auto-subtract cross-talk, reinforcing non-invasive dominance inside the intrapartum monitoring devices market.

By Portability: Wireless Units Reshape Deployment Economics

Fixed consoles supplied 71.40% of 2025 revenues but face decelerating share as portable devices grow 7.05% CAGR. Hospital command centers favor fixed racks feeding central viewers and EHR links. Yet rural outreach, ambulance transfers, and surge capacity after unit closures drive mobile purchasing. Melody International’s iCTG, operable on internal battery and mobile networks, shows how portability serves facilities lacking stable power.

Pandemic protocols that separated infected and non-infected cohorts underscored the benefit of moving monitors rather than patients. Wireless patches like Novii blur category lines, delivering fixed-grade readings while untethering women from the bedside. Procurement teams now weigh network reliability, battery endurance, and cybersecurity when evaluating portable proposals—and their decisions set a new competitive cadence in the intrapartum monitoring devices market.

By End-User: Focused Clinics Capture Agility Dividend

Hospitals still account for 64.95% 2025 spend because they manage high-risk deliveries and hold anesthesia and surgical back-up. Yet specialty clinics register a 6.74% CAGR through 2031 as decentralization and value-based reimbursement reward boutique birthing experiences. Clinics differentiate via lower nurse-to-patient ratios, hydrotherapy amenities, and wireless CTG that allows waterbirth compatibility. Australian satisfaction studies place wireless monitoring at the top of patient preference lists, noting perceived empowerment and lower anxiety.

Home-birth segments and tele-consult platforms broaden the “others” bucket, leveraging FDA-cleared consumer devices such as Masimo Stork for post-discharge surveillance. As these channels mature, they collectively chip away at hospital primacy and diversify procurement patterns within the intrapartum monitoring devices market.

Geography Analysis

North America’s 41.85% stake stems from stringent standards and high per-capita healthcare spending. Forthcoming CMS rules compel universal fetal-monitor access, and NICU admissions edging toward 10% of births intensify monitoring sophistication. Yet 2024 saw multiple rural obstetric unit shutdowns and rising malpractice premiums, pushing health systems to pilot tele-CTG hubs that extend oversight without on-site specialists. Vendor partnerships, such as Philips’ collaboration with Georgia health plans for remote maternal programs, illustrate how the intrapartum monitoring devices market adapts to workforce deficits.

Asia-Pacific claims the speed crown at 7.18% CAGR, lifted by maternal mortality reduction drives and urban hospital construction booms. Governments subsidize digital health pilots that outfit district maternity wards with Bluetooth CTG linked to cloud dashboards in tertiary centers. In Japan and South Korea, AI-interpretation pilots expedite decision making, while emerging economies prioritize basic device deployment alongside midwife training. The Asian Development Bank’s integrated-care grants finance hybrid maternal–NCD telemetry networks, further scaling demand.

Europe sits in a regulatory sweet spot: EU-MDR harmonization simplifies cross-border certifications, and established reimbursement structures cover advanced CTG usage. French hospitals using Masimo SafetyNet for premature newborn early discharge evidence willingness to invest in telemonitoring when cost-benefit aligns. Middle East, Africa, and South America remain nascent but promising. Sub-Saharan Africa’s digital-health lens positions mobile CTG as a leapfrog technology in regions lacking fixed infrastructure.

Regulatory Landscape

Intrapartum monitoring devices are regulated as Class II systems in major markets, with U.S. products commonly cleared through the FDA 510(k) pathway under 21 CFR 884.2740 (product code HGM). Recent clearances reinforce the momentum of software-enabled and wireless platforms being incorporated into standard obstetric workflows, including Sibel Healths FDA 510(k) clearance for the ANNE Maternal monitor (February 2026), Edans 510(k) clearance for its fetal and maternal monitor models (August 2025), and Philips 510(k) clearance for the Avalon CL fetal and maternal pod and patch (July 2024).

In Europe, EU MDR requirements continue to shape technical documentation, labeling, and post-market obligations, and 2026 actions add more operational specificity. The EU adopted Implementing Regulation (EU) 2026/977 (May 2026) covering elements of the notified body conformity assessment process, and the European Commission MDCG issued an updated EMDN nomenclature and borderline guidance (Version 5, April 2026). EU MDR infrastructure also tightened as EUDAMED modules became mandatory for actors and device/UDI registration and market surveillance (May 2026). Harmonised standards updates published in the Official Journal in June 2026, including EN ISO 15223-1:2021/A1:2025 for symbols and labeling, further increase the focus on compliant packaging and traceability for both monitors and accessories.

Competitive Landscape

The intrapartum monitoring devices market exhibits moderate fragmentation. GE Healthcare, Philips, and Medtronic anchor the field with diversified portfolios and sizable installed bases. Their strategy pivots on embedding AI modules that convert continuous traces into risk categories, a move exemplified by GE’s AI Innovation Lab that automatically flags decelerations. Samsung’s USD 92.4 million Sonio purchase exemplifies vertical expansion into software that enriches hardware ecosystems. Mid-tier firms such as Edan leverage cost-competitive monitors bundled with analytical firmware for value-driven buyers.

White-space competitors chase cyber-secure architectures. Several FDA safety communications on patient-monitor vulnerabilities spurred demand for devices with secure-boot, encrypted firmware, and authenticated Wi-Fi stacks. Vendors boasting IEC 81001-5-1-certified software differentiate on trust. Portable specialists, including Melody International, target NGOs and rural health ministries with battery-powered kits priced well below central stations. Meanwhile, AI-only start-ups license classification engines that retrofit legacy CTG files, creating recurring revenue patterns.

Partnerships define 2025 activity: Medtronic allied with Philips to fuse Nellcor pulse oximetry into Philips monitors, expediting integrated fetal–maternal dashboards. GE tied up with Raydiant Oximetry for optical fetal oxygenation sensors, anticipating regulatory acceptance of multi-parametric intrapartum indices. These collaborations illustrate convergence, where data-rich multimodal devices anchor long-term platform control over the intrapartum monitoring devices market.

Intrapartum Monitoring Devices Industry Leaders

-

Cardinal Health

-

GE Healthcare

-

Koninklijke Philips N.V.

-

MindChild Medical

-

The Cooper Companies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Wireless, wearable intrapartum monitoring is shifting from product differentiation to a clearer commercialization pathway, creating whitespace in beltless monitoring, remote oversight, and software-defined upgrades. FDA 510(k) clearance for Sibel Healths fully wireless ANNE Maternal platform (2026) provides a fresh predicate and procurement signal for cable-free maternal-fetal monitoring designs that support mobility and reduce setup burden in high-turnover labor wards. This direction aligns with the market's structural tilt toward non-invasive monitoring, which already accounts for most revenues, as well as hospital demand for AI-ready platforms that can standardize interpretation and documentation.

Vendors can also use this momentum to expand beyond fetal heart rate and uterine activity into additional physiologic sensing to improve decision confidence without adding invasive steps. In 2026, published intrapartum feasibility work on fetal pulse oximetry (OxiReed/First Touch) and reliability testing of flexible fetal-maternal wearable monitors, alongside Stanfor d Medicines 2026 announcement of an early validated wearable ultrasound patch for continuous fetal blood flow monitoring, point to clinical development toward richer, continuous intrapartum data streams. Platforms that pair these signals with cloud-based dashboards and cybersecurity-hardened connectivity address two purchase constraints at once, clinician workload and device-network risk, while supporting hub-and-spoke labor monitoring models in health systems constrained by obstetric staffing.

Recent Industry Developments

- June 2026: GE HealthCare introduced CareIntellect for Perinatal, a cloud-based SaaS application that unifies maternal and fetal data streams such as fetal heart rate, uterine activity, and maternal SpO2 into a single interface. The launch reinforces a shift from standalone CTG devices toward connected software layers that standardize review and escalation across labor units and multi-site health systems.

- July 2025: Medtronic and Philips agreed to integrate Nellcor pulse oximetry and Microstream capnography into Philips bedside monitors, expanding the combined maternal parameter set available alongside obstetric monitoring workflows. The integration supports consolidated dashboards and can reduce the need for separate monitoring hardware in high-acuity labor and delivery rooms.

- July 2024: Philips received FDA 510(k) clearance for the Avalon CL Fetal and Maternal Pod and Patch, adding a regulatory anchor for cableless, patch-based monitoring configurations. Clearance supports broader hospital adoption of beltless monitoring approaches that improve maternal mobility while maintaining continuous surveillance and documentation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the intrapartum monitoring devices market covers the devices and accessories used during labor to track fetal heart rate and key maternal and fetal signals, including monitors and intrapartum electrodes used in clinical settings.

Scope exclusions: This sizing excludes antepartum-only monitoring, neonatal monitoring after birth, and broader obstetric consumables that are not used for intrapartum monitoring.

Segmentation Overview

-

By Product Type

-

Electrodes

- Intra-uterine Pressure Catheters (IUPC)

- Fetal Scalp Electrodes

- Uterine Contraction Transducers

- Fetal Heart-Rate Transducers

- Monitors

-

Electrodes

-

By Monitoring Method

- Invasive

- Non-Invasive

-

By Portability

- Fixed

- Portable

-

By End-User

- Hospitals

- Specilaty Clinics

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base around births, labor monitoring protocols, and the installed workflow in hospitals, then to sanity check regional shares. We referenced public sources such as World Health Organization maternal health publications, World Bank health indicators, UN population and birth statistics, and national public health agencies that publish natality and maternal outcomes data.

To translate clinical activity into a market model, we also reviewed regulatory and product information from agencies such as the US FDA device databases and the European Commission device framework updates, along with peer reviewed clinical literature on cardiotocography use and invasive versus non-invasive monitoring practices. Company annual reports, investor materials, and reputable press helped validate product mix changes like portable monitoring uptake, while selective paid subscriptions for company financials and patent databases were used to cross-check innovation intensity and business footprints. This desk source list is illustrative, and additional references were used to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary work was used to validate which monitoring approaches are actually used during labor by setting, and how purchasing happens for monitors and electrodes across mature and developing healthcare systems. We spoke with a mix of clinical stakeholders and commercial roles across hospitals, specialty clinics, and distribution channels, with coverage balanced across major regions so differences in labor-room protocols and reimbursement could be reflected in assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | APAC: 49% |

| Mid tier: 53% | Functional/Unit leaders: 30% | EMEA: 33% |

| Smaller Players: 16% | Managers: 54% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where live births and facility delivery rates are converted into an addressable labor pool. That pool is then adjusted for the share of deliveries that use continuous electronic monitoring versus intermittent checks. Once the demand pool is set, we apply adoption by monitoring method (invasive versus non-invasive) and map it to device categories used in labor rooms, followed by typical replacement cycles and average selling price ranges by region.

To keep the totals realistic, we cross-check the outputs using selective bottom-up approximations, including sampled hospital procurement patterns, distributor channel checks, and volume based on typical monitor placements per labor and delivery unit, multiplied by feasible price bands. Inputs that mattered in this market include annual births, C-section and high-risk pregnancy incidence as a proxy for higher monitoring intensity, penetration of portable systems versus fixed units, electrode utilization per monitored delivery, and pricing drift linked to feature upgrades and service bundles.

For forecasting, we run scenario analysis around a central case, because adoption and pricing can move differently by region when guidelines, staffing levels, and purchasing cycles change. Assumptions are finalized after reconciling expert views on adoption speed for portable and AI-assisted interpretation features, and gaps in bottom-up checks are handled by using conservative placement rates and wider ASP ranges until they are validated through follow-up conversations.

Data Validation & Update Cycle

Results are validated through multiple checks so the final series aligns with real-world healthcare activity. We compare model outputs against independent signals such as regional birth trends, hospital infrastructure additions, and shifts in monitoring method mix, then review outliers to confirm whether they reflect a true demand change or a modeling input that needs correction.

Before sign-off, assumptions and calculations are reviewed in steps by analysts. If there is a large variance versus prior-year patterns, we re-check the driver tree and, when needed, re-contact interviewees. Reports are refreshed annually, and interim updates are made when material events occur, such as regulatory changes, major product launches, or sharp currency movements. Right before delivery, a final pass is completed so clients receive the most current view supported by the latest available public data and field feedback.

Mordor Intelligence's Intrapartum Monitoring Devices Market Size Versus Other Published Estimates

Published numbers for intrapartum monitoring devices often do not line up because included device scope and the anchor year can change from one publisher to another. Differences also come from how the labor monitoring demand pool is constructed, and whether price and replacement assumptions are updated using recent field feedback.

The benchmark table shows a spread that is mainly explained by year alignment and category boundaries. Under Mordor Intelligence's scope, the value is anchored to a 2026 estimate and focuses on intrapartum monitors and electrodes, rather than folding in adjacent maternal or neonatal monitoring categories that can inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.61 B (2026) | |

| Global Research House A | USD 2.45 B (2025) | Uses a different anchor year and blends intrapartum monitoring with a broader fetal monitoring view in some sections, which can shift both the base value and implied growth pattern. |

| Industry Publisher B | USD 2.13 B (2024) | Earlier base year and a narrower counted demand pool tied to reported purchasing settings, which can reduce the starting value when coverage of specialty clinics and replacement cycles is treated conservatively. |

Taken together, the comparison suggests the largest differences are created by what is counted as intrapartum-only equipment and how the base year is chosen before forecasting is applied. By keeping the driver tree tied to births, monitoring intensity, method mix, and practical pricing ranges, the final estimate stays transparent and can be repeated with the same set of observable inputs.

Key Questions Answered in the Report

How large is the intrapartum monitoring devices market in 2026?

The intrapartum monitoring devices market size stands at USD 2.61 billion in 2026.

What CAGR is forecast for intrapartum monitoring devices to 2031?

Revenue is expected to rise at a 6.38% CAGR through 2031.

Which product category is expanding fastest?

Monitors lead growth with a 6.89% CAGR thanks to integrated AI analytics.

Why are non-invasive monitoring methods preferred?

They capture 69.22% of 2025 revenue because they maximize maternal mobility and comfort while meeting clinical accuracy standards.

Which region will post the highest growth rate?

Asia-Pacific is projected for a 7.18% CAGR as governments scale digital maternal-health infrastructure.

How are AI tools changing fetal monitoring?

Deep-learning engines now auto-interpret CTG traces with up to 97.9% accuracy, reducing clinician workload and enhancing early-warning capabilities.

Page last updated on: