Posture Corrector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

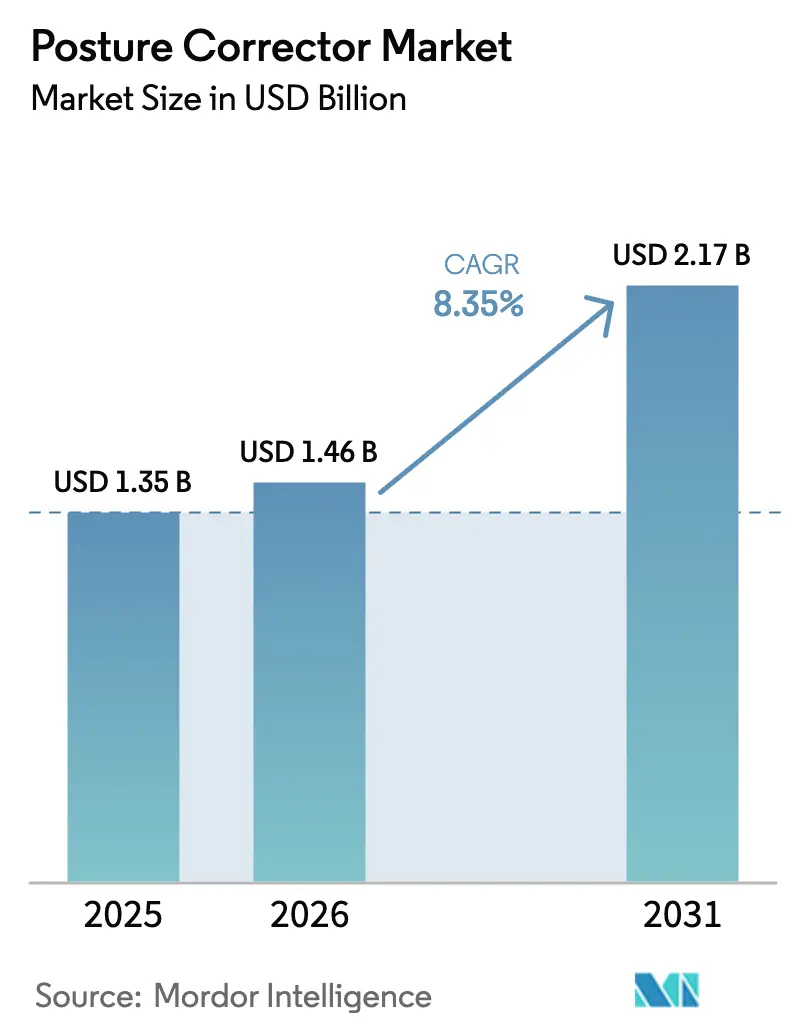

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 2.17 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Posture Corrector Market Analysis by Mordor Intelligence

The posture corrector market size is expected to increase from USD 1.35 billion in 2025 to USD 1.46 billion in 2026 and reach USD 2.17 billion by 2031, growing at a CAGR of 8.35% over 2026-2031. This expansion mirrors a structural shift in how employers and healthcare systems address musculoskeletal disorders as remote and hybrid work models intensify the need for accessible ergonomic solutions. Telehealth providers now pair virtual posture assessments with device prescriptions, converting what was once an impulse retail purchase into a clinically guided intervention. Conventional non-electronic products remain volume leaders, while smart wearable trainers are gaining ground as employers seek data-driven wellness programs. Meanwhile, kinesiology tape is outperforming other categories due to the crossover demand from the sports medicine sector. Regional growth differentials highlight the impact of regulatory clarity, digital health infrastructure, and e-commerce maturity on adoption rates across major markets.

Key Report Takeaways

- By product type, sitting support devices accounted for a 53.23% share of the posture corrector market in 2025, while kinesiology tape is projected to expand at a 10.54% CAGR through 2031.

- By 2025, conventional non-electronic devices held 64.67% of the posture corrector market size, whereas smart electronic trainers are projected to advance at a 10.65% CAGR through 2031.

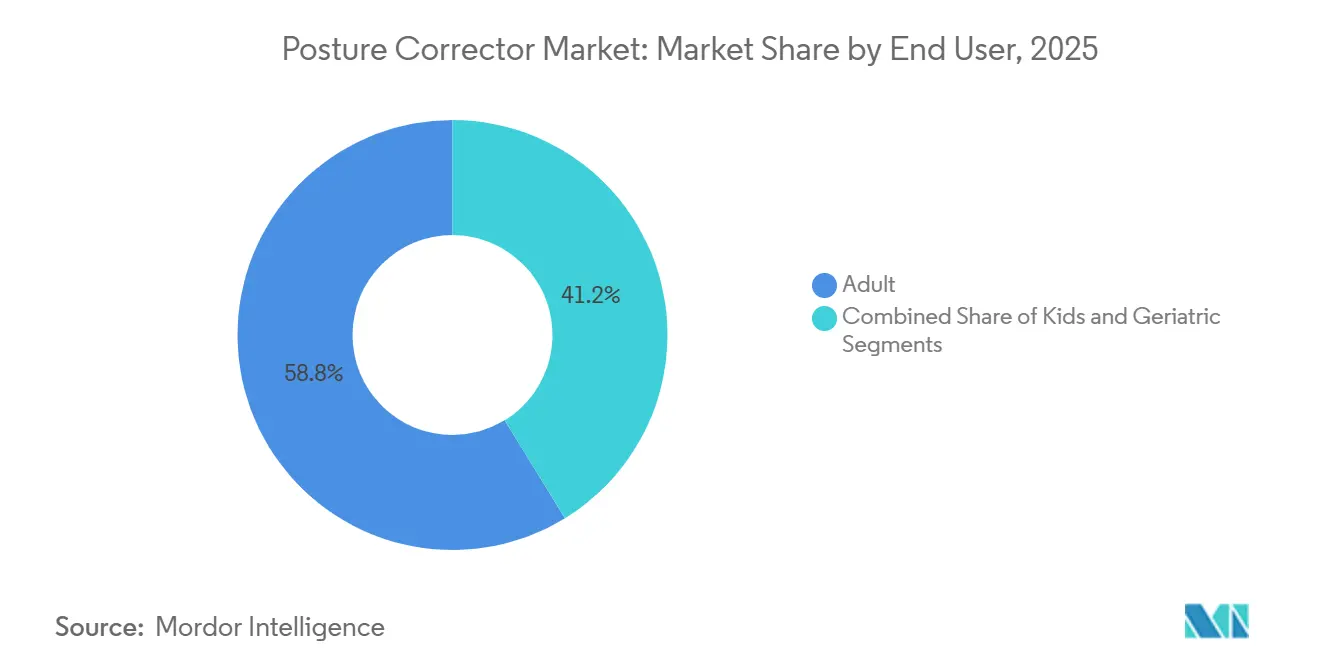

- By end user, adults represented 58.76% of the 2025 revenue, yet the geriatric segment is the fastest-growing at an 11.43% CAGR through 2031.

- By distribution channel, offline outlets maintained 69.54% share in 2025, but online platforms are set to increase at an 11.56% CAGR over the same period.

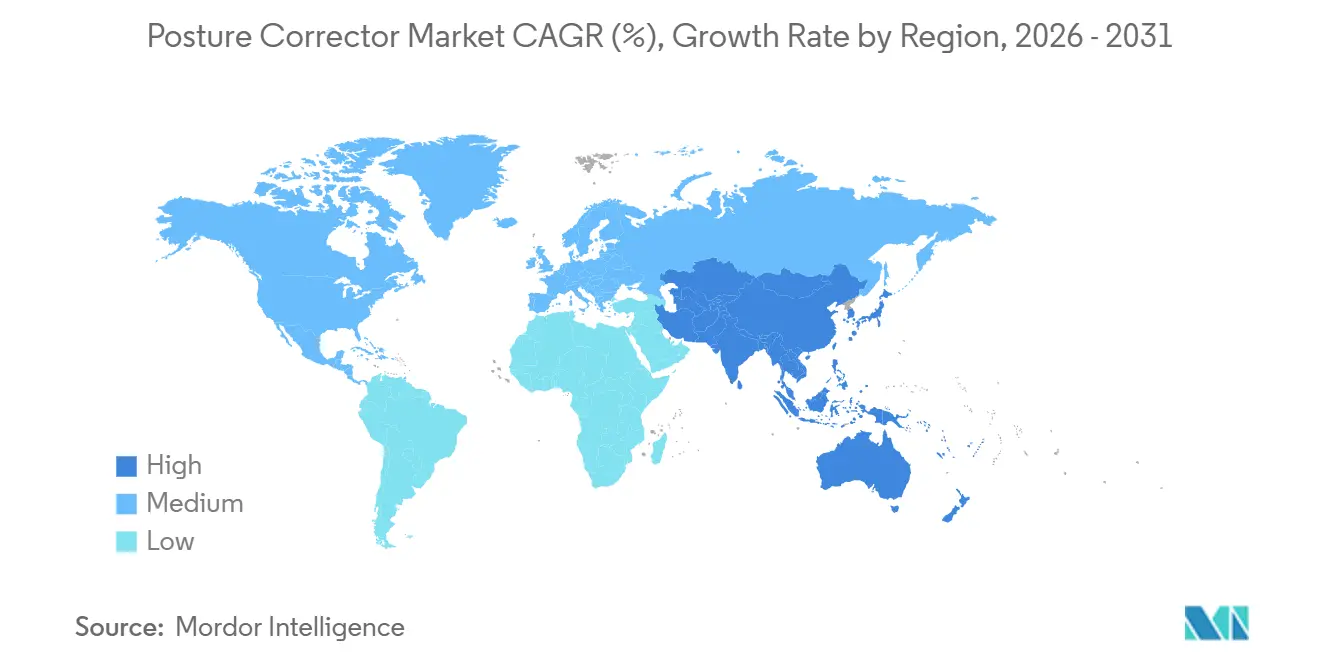

- By geography, North America led with 43.56% revenue share in 2025, while Asia–Pacific is forecast to record the highest regional CAGR at 9.32% up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Posture Corrector Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Telehealth Ergonomic Assessments | 1.8% | North America & EU, expanding to APAC urban centers | Medium term (2-4 years) |

| Surge In Work-From-Home Ergonomic Spending | 2.1% | Global, with concentration in North America, Western Europe | Short term (≤ 2 years) |

| Integration Of Smart Wearable Sensors | 1.5% | North America, EU, APAC tech hubs (South Korea, Japan, Singapore) | Long term (≥ 4 years) |

| Social Media Influencer Marketing Boosting Posture Awareness | 0.9% | Global, particularly North America, EU, urban APAC | Short term (≤ 2 years) |

| Growing Adoption In Preventive Corporate Wellness Programs | 1.4% | North America, EU, APAC multinational employers | Medium term (2-4 years) |

| Expanding E-Commerce Distribution Channels In Emerging Economies | 1.2% | APAC core (India, Southeast Asia), MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Telehealth Ergonomic Assessments

Telehealth platforms integrate remote posture analysis into musculoskeletal consultations, shifting corrective devices from over-the-counter items to prescribed tools endorsed by clinicians. A June 2024 review by the Physical Health Technologies Institute, which covered 12 virtual programs, showed that clinician-guided interventions increased device adherence by 34% compared to self-purchases[1]Physical Health Technologies Institute, “Virtual MSK Solutions Assessment,” phti.org. Enhanced follow-up mitigates the common abandonment of rigid braces and aligns usage with measurable postural improvement goals. Insurance coverage remains limited because many payers label correctors as durable medical equipment only for diagnosed impairment, yet partnerships with telehealth firms open higher-margin, lower-return-rate channels for brands.

Surge in Work-From-Home Ergonomic Spending

Frontiers in Public Health reported a 41% increase in neck pain and a 38% rise in lower-back pain among teleworkers compared to pre-pandemic baselines[2]Frontiers in Public Health Editorial Board, “Musculoskeletal Pain in Teleworkers,” frontiersin.org. Employers facing retention challenges often regard low-cost ergonomic interventions as a straightforward way to reduce absenteeism. BackJoy positioned its USD 39.95 sitting support device to pharmacy chains at NACDS Marketplace, citing more than 500,000 users. Vendors that align pricing with bulk procurement and supply analytics dashboards tap a corporate wellness budget that now rivals direct-to-consumer revenue for mid-tier players.

Integration of Smart Wearable Sensors

Smart posture correctors are evolving into biofeedback systems that prompt self-correction through the use of accelerometers, gyroscopes, and gentle vibration alerts. The American College of Sports Medicine ranked wearable technology as the top global fitness trend for 2025, validating mainstream interest in posture-tracking features. Clearer U.S. FDA Class II pathways for electronic trainers provide a predictable approval route, enabling scale without the cost of full premarket approval. Employers view data-rich devices as preventive wellness assets, spurring demand that is gradually overcoming higher price points and setup complexity.

Social Media Influencer Marketing Boosting Posture Awareness

Influencer-led campaigns demonstrate corrector use in real-time, translating posture education into immediate online sales conversions. Short-form videos showing before-and-after alignment drive peer-to-peer validation and reinforce product legitimacy. Brands partner with certified fitness coaches to sidestep misinformation concerns and spotlight evidence-based tutorials, a tactic that raises average order values when combined with e-commerce discount codes. Urban consumers in North America, Europe, and Asia tend to gravitate toward devices endorsed by recognizable health professionals, thereby amplifying word-of-mouth virality at lower acquisition costs than those of paid advertising alone.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Clinical Evidence For Long-Term Efficacy | -1.3% | Global, particularly North America & EU where evidence-based medicine dominates | Long term (≥ 4 years) |

| User Compliance Challenges Due To Discomfort | -1.1% | Global, with higher impact in APAC where product awareness is lower | Short term (≤ 2 years) |

| Proliferation Of Cheap Counterfeit Products Online | -0.8% | Global, concentrated in APAC and MEA e-commerce platforms | Medium term (2-4 years) |

| Regulatory Uncertainty Over Medical Device Classification | -0.6% | North America, EU, emerging in APAC as regulations tighten | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Clinical Evidence for Long-Term Efficacy

A 2024 meta-analysis in the Journal of Clinical Medicine found that kinesiology tape produced small, short-term pain reductions that dissipated beyond 12 weeks. Similar variability exists for rigid braces, with some trials showing a benefit and others achieving outcomes equivalent to those of posture education alone. The absence of data from ≥1-year follow-ups limits payer reimbursement and restricts integration into clinical guidelines. Consequently, brands compete primarily on price rather than differentiated evidence, squeezing margins and dampening R&D investment in advanced sensor technologies.

User Compliance Challenges Due to Discomfort

Rigid braces often cause shoulder or underarm irritation after extended wear, leading many users to abandon the devices sooner than the manufacturer's guidance suggests. Non-adherence erodes perceived efficacy, depresses repurchase rates, and inflates return volumes for e-commerce sellers. Education and telehealth follow-ups mitigate these issues, but they also raise acquisition costs. Soft tissue tapes and sensor-based wearables address comfort pain points but introduce fiscal trade-offs - tape requires recurring purchases, and smart devices demand higher entry prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sitting Devices Retain Lead while Tape Accelerates

Sitting support devices accounted for 53.23% of 2025 revenue, underscoring their procurement fit for hybrid work budgets and immediate relief benefits. This share anchors overall posture corrector market stability, even as kinesiology tape advances at a 10.54% CAGR, the fastest among all product types. Sitting cushions and lumbar rolls integrate seamlessly into corporate wellness kits, require minimal instruction, and present low return rates due to universal sizing. Braces remain popular for rehabilitation but suffer from discomfort-driven abandonment, which lowers their lifetime value despite initial sales.

Tape’s expansion mirrors consumer demand for low-profile solutions compatible with sports and daily movement. Trials highlight improvements in scapular positioning without restricting range, dovetailing with telehealth protocols that target specific body zones rather than a one-size-fits-all brace. Braces will retain relevance in clinical recovery pathways; however, tape’s versatility across the neck, thoracic, and lumbar regions positions it as the growth nucleus in the posture corrector market. Niche products such as posture pumps and neck stretchers remain confined to specialty channels pending more substantial evidence.

By Technology: Smart Trainers Narrow Gap with Conventional Devices

Conventional devices accounted for 64.67% of 2025 revenue, reflecting their affordability, battery-free convenience, and compatibility with one-time corporate purchases. However, smart electronic trainers are tracking a 10.65% CAGR as employers favor data visibility over static support. Conventional cushions and tape sell for USD 10-40, fit neatly into retail pharmacy assortments, and require no digital onboarding. Their simplicity helps keep return rates down, particularly when in-store pharmacists assist with sizing.

Smart trainers priced between USD 80-150 appeal to early adopters seeking real-time feedback on slouch events. The #1 fitness trend recognition from ACSM elevates consumer curiosity, while predictable FDA Class II pathways de-risk regulatory hurdles[3]American College of Sports Medicine, “Worldwide Survey of Fitness Trends 2025,” acsm.org. Conventional devices will remain volume champions through 2031; however, innovative products will capture disproportionate revenue in high-value B2B wellness contracts and data-centric consumer segments, steadily narrowing the market share gap.

By End User: Adults Dominate, but Geriatrics Scale Fastest

Adults generated 58.76% of 2025 revenue, buoyed by hybrid work ergonomics and employer subsidies. Nonetheless, the geriatric cohort is progressing at an 11.43% CAGR, the highest among all end-user groups. Aging populations face a rising musculoskeletal risk; posture interventions now feature in fall-prevention guidelines, catalyzing uptake through home health channels. Lightweight braces with easy closures and gentle anatomical contours resonate with older adults who may struggle with rigid designs.

Pediatric adoption remains a small but growing trend, especially in South Korea and Japan, where schools are spotlighting “tech neck” prevention. Adult dominance will persist, yet brands that tailor products for geriatric dexterity constraints and fragile skin will secure early leadership in a segment set for outsized expansion as global median age rises. Telehealth applications that facilitate remote posture monitoring for seniors add another lever to extend device adherence without clinic visits.

By Distribution Channel: Offline Stores Hold Majority While Online Surges

Offline venues accounted for 69.54% of 2025 revenue, reflecting consumers’ preference for in-store fitting and immediate product trials that reduce sizing-related returns. Pharmacy staff demonstrating brace application helps convert undecided shoppers and lowers dissatisfaction risks. Corporate wellness programs also rely on bulk offline deliveries tied to on-site ergonomic workshops, reinforcing the dominance of brick-and-mortar stores in the posture corrector market.

Online channels are growing at an 11.56% CAGR, thanks to telehealth-coupled sales flows, influencer-driven demand spikes, and logistics upgrades across emerging Asia–Pacific and Latin American cities. Marketplaces now badge HSA/FSA-eligible devices, easing purchase decisions for tax-advantaged spenders. Same-day delivery erodes historic fulfillment pain points for bulky supports, and detailed sizing videos reduce uncertainty. Offline outlets will still hold the majority share through 2031, but direct-to-consumer e-commerce offers brands unparalleled control over pricing, customer data, and post-purchase engagement, setting the stage for a gradual shift in power.

Geography Analysis

North America contributed 43.56% of global revenue in 2025, anchored by robust corporate wellness mandates, well-defined FDA pathways, and higher per-capita healthcare spending. Precise Class I registration for passive truncal orthoses streamlines launch timelines, while Class II routes for smart trainers reduce ambiguity, bolstering investor confidence. Nonetheless, insurers generally withhold reimbursement absent documented impairment, creating price sensitivity that slightly tempers the adoption of premium devices. Telehealth penetration offsets this constraint by bundling posture evaluations with prescribed correctors, introducing clinical oversight into purchasing decisions.

The Asia–Pacific region is forecast to lead growth at a 9.32% CAGR through 2031, driven by a surge in desk-centric employment, the expansion of digital health initiatives, and the widespread adoption of e-commerce, which is bypassing underdeveloped specialty retail. Government school programs in South Korea and Japan address adolescent spinal health, embedding early-life posture awareness that propels future device demand. China’s logistics networks enable same-day delivery of sitting devices in tier-1 cities, supporting volume strategies. Yet rampant counterfeit proliferation challenges brand equity, emphasizing the need for certification markings and platform partnerships to signal authenticity.

Europe and South America are poised for mid-single-digit CAGRs. Harmonized ISO 13485 standards lower compliance friction, benefitting cross-border suppliers serving multiple EU markets. Economic headwinds and tighter regulatory scrutiny moderate short-term uptake, but employer wellness adoption and aging demographics underpin steady demand. South American growth lags but remains strategic for companies seeking first-mover advantages before regulatory regimes tighten in alignment with U.S. and EU models.

Regulatory Landscape

Posture correctors sit between consumer wellness products and regulated medical devices, and classification generally tracks intended use and the claims made for the device. In the United States, truncal orthoses are covered under FDA regulation 21 CFR 890.3490 and are classified as Class I, with many configurations 510(k) exempt, while electronic posture trainers can face additional controls depending on claims and functionality.

In Europe, the EU Medical Device Regulation (MDR) 2017/745 applies when products are positioned for therapeutic or medical purposes, shaping technical documentation, clinical evaluation, and post-market surveillance expectations. Wellness positioning can avoid medical-device designation. The FDA Quality Management System Regulation (QMSR) (21 CFR 820), which takes effect on February 2, 2026, tightens quality-system requirements in the United States, incorporates ISO 13485:2016 alignment, and raises compliance expectations for manufacturers supplying posture-correction devices and adjacent wearable trainer products.

Competitive Landscape

The posture corrector market exhibits moderate fragmentation, with the ten largest suppliers controlling roughly 60–70% of global revenue, while smaller regional specialists and direct-to-consumer entrants divide the remainder. Established brands leverage clinical validation and long-standing pharmacy relationships to secure shelf presence. Start-ups differentiate themselves via smart sensor integration, AI-driven coaching, and subscription apps, although rising social-media advertising costs test the direct-to-consumer economics.

Competition is shifting toward ecosystem integration. Vendors pairing correctors with telehealth assessments, corporate analytics dashboards, and HSA/FSA compliance build defensible moats that transcend product commoditization. White space exists in geriatric-friendly designs that emphasize ease of use, next-generation kinesiology tape incorporating auxetic patterns and embedded sensors, and regulatory arbitrage in emerging markets where classifications remain fluid. Compliance with ISO 13485 and FDA registration is emerging as a trust badge on global e-commerce platforms, with Amazon strengthening gatekeeping protocols to weed out counterfeit goods.

Patent filings indicate a heightened focus on R&D for haptic feedback, automatic tension adjustment, and machine-learning algorithms that tailor corrective cues to individual biomechanics. Commercialization hinges on closing evidence gaps and navigating multi-jurisdictional approvals, tasks best tackled by companies with multidisciplinary teams that blend biomedical engineering, regulatory affairs, and digital service expertise.

Posture Corrector Industry Leaders

BackJoy

Swedish Posture

Ottobock

Acorn International

BodyRite

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key gap remains in clinically guided distribution models that move posture correctors from discretionary purchases into structured interventions, especially in channels where telehealth ergonomic assessments are already part of musculoskeletal consultations. The market context supports this, since clinician-guided virtual programs have shown improved adherence compared with self-purchase behavior, creating room for brands to package device selection, onboarding, and follow-up coaching for employers and telehealth partners, rather than competing only on unit price in retail and marketplaces.

Opportunities also follow from higher quality and compliance expectations and from employer demand for measurable wellness outcomes. The FDA QMSR effective February 2, 2026 (aligning 21 CFR 820 with ISO 13485:2016 concepts) increases the value of documented quality management and traceability for manufacturers serving regulated and institutional channels. In parallel, smart wearable trainers fit corporate wellness programs that look for usage data and engagement. On the conventional side, kinesiology tape growth and crossover use in sports and daily activity support recurring-consumption models and adjacent accessory lines, including brand extensions such as KT Tape launching CGM and insulin pump patches in May 2024, which broaden taped-adhesion knowledge into higher-wear use cases.

Recent Industry Developments

- May 2026: BackJoy expanded its retail distribution of its StandRight Zen footwear collection, leveraging Active Stabilization technology. The expansion broadens daily postural protection beyond devices and reinforces BackJoy as an end-to-end posture solution provider.

- October 2025: PostureUp launched its AI-powered Ergo-Audit posture assessment tool. The tool integrates digital posture assessment with devices, extending a telehealth-enabled posture correction workflow and improving clinical validation and uptake.

- May 2024: KT Tape launched CGM and insulin pump patches for diabetes management. The additions widen its kinesiology tape portfolio into chronic condition management and broaden active lifestyle and sports medicine solutions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers posture corrector products sold for everyday posture support and alignment, including wearable braces and trainers, sitting support solutions, and related taping products, measured in revenue terms across major regions.

Scope exclusions: Services, clinical procedures, and general furniture purchases that are not marketed or sold as posture correction products are excluded.

Segmentation Overview

- By Product Type

- Sitting Support Device

- Kinesiology Tape

- Posture Braces

- Other Product Types

- By Technology

- Smart Electronic Posture Trainers

- Conventional Non-Electronic Devices

- By End User

- Adult

- Kids

- Geriatric

- By Distribution Channel

- Online

- Offline

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the product boundary and demand triggers using public health and ergonomics references, and then tying that view to observable trade and retail signals. We leaned on open sources such as the US FDA device classification and safety notices, the US International Trade Commission trade statistics, UN Comtrade, and health surveillance publications from bodies such as the WHO and CDC to understand usage drivers tied to musculoskeletal discomfort and sedentary work.

To translate that context into a sizing model, company filings, investor presentations, product catalogs, and reputable press coverage were reviewed to track pricing bands, channel mix, and product refresh cycles. Where available, we also used paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment level import-export data to fill gaps on smaller private brands and cross-border supply flows. The desk sources listed above are illustrative, and many other public documents and datasets were used to collect, cross-check, and clarify inputs.

Primary Interviews and Surveys

Primary work was used to confirm what gets counted as a posture corrector in real buying situations and how demand differs between braces, trainers, and sitting supports. We spoke with a mix of manufacturers, distributors, retailers, and clinicians or ergonomics practitioners across key regions, and responses were used to validate price points, channel splits, and adoption assumptions where desk sources were thin.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 47% |

| Mid tier: 47% | Functional/Unit leaders: 40% | EMEA: 33% |

| Smaller Players: 17% | Managers: 45% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where broad demand pools and channel activity were first reconstructed and then checked with selective supplier and retailer reality tests. On the top-down side, we used a penetration rate based demand pool assessment anchored on adult population, prevalence of back and neck discomfort signals, work from home and desk job intensity, and the share of consumers choosing non-prescription support products.

Those demand pools were converted into value using typical units per buyer and average selling prices by product category, which were then adjusted for channel mix (online versus offline), discounting patterns, and replacement cycles. To corroborate totals, bottom-up approximations were applied where data was accessible, such as sampled brand revenues in braces and trainers, distributor feedback on sell-through by region, and import patterns that indicate category momentum.

Forecasts were produced using scenario analysis so that near-term volatility in consumer spending and promotional intensity can be reflected without overfitting the model. Inputs that mattered most for the outlook included e-commerce share gains, pricing pressure from private labels, adoption of smart wearable trainers, return rates in online channels, and region-level awareness of ergonomics. When country or channel data was missing, gaps were handled through peer-market proxies and then re-tested with interview feedback until assumptions sat within realistic ranges.

Data Validation & Update Cycle

Validation was done through multiple checks so that one data series does not dominate the outcome. We compared model outputs with independent signals such as trade flows, observable pricing, and channel growth indicators, and then investigated large variances before finalizing totals.

A second analyst review was used to re-check formulas, currency conversions, and year alignment, followed by targeted re-contact with interviewees if a key assumption shifted the totals materially. Reports are refreshed annually, and interim updates are made when major events occur (for example, a material regulatory change, a demand shock, or a noticeable price reset). Before delivery, the latest public updates are reviewed again so clients receive the most current view possible.

Mordor Intelligence's Posture Corrector Market Estimate Compared With Other Published Estimates

Published market sizes for posture correctors can look different because the scope and the counting logic are not always aligned, even when the product names sound similar. Differences usually come from what product types are included, what year is treated as the current estimate, and how online discounting and currency timing are handled.

The biggest gaps tend to show up when some estimates fold adjacent categories into one number, or when pricing is assumed to rise faster than what channel checks support. The table also reflects timing differences, where a 2024 based estimate and a 2026 based estimate can diverge simply because adoption and online penetration are moving quickly in this category.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.46 B (2026) | |

| Trade Journal A | USD 1.24 B (2024) | Uses an earlier base year and a broader product basket that can blend posture braces with neighboring back support items, which shifts the revenue pool and the starting price level. |

| Industry Data Publisher B | USD 1.45 B (2024) | Models the category as posture corrector devices with a type mix that can over-weight wearables and may not fully normalize channel discounting, creating a different ASP and growth path. |

The table shows a spread that is mostly explained by base year choice and what gets counted as a posture corrector versus a wider back support purchase. In Mordor Intelligence's model, only products sold and positioned for posture correction are included, and value is built from adoption and pricing that are rechecked through channel feedback, which keeps the number traceable to clear, repeatable inputs.

Key Questions Answered in the Report

How large is the posture corrector market in 2026?

The posture corrector market size is USD 1.46 billion in 2026, setting the stage for steady expansion to 2031.

What is the expected growth rate for posture correctors through 2031?

Market demand is forecast to rise at an 8.35% CAGR, driven by remote-work ergonomics, telehealth adoption, and corporate wellness programs.

Which product type is growing fastest?

Kinesiology tape leads growth with a projected 10.54% CAGR as sports-medicine applications broaden and telehealth prescriptions climb.

Which region will see the strongest market gains?

Asia-Pacific is on track for the highest regional CAGR at 9.32% thanks to widening desk-job prevalence and expanded e-commerce reach.

How are smart posture trainers positioned against conventional devices?

Smart electronic trainers offer real-time biofeedback and data analytics, growing at a 10.65% CAGR even though conventional supports remain the volume leader.

What restrains long-term adoption of posture correctors?

Limited multi-year clinical evidence, discomfort-driven non-adherence, and a surge in counterfeit products present meaningful headwinds to sustained uptake.

Page last updated on: