Portugal Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

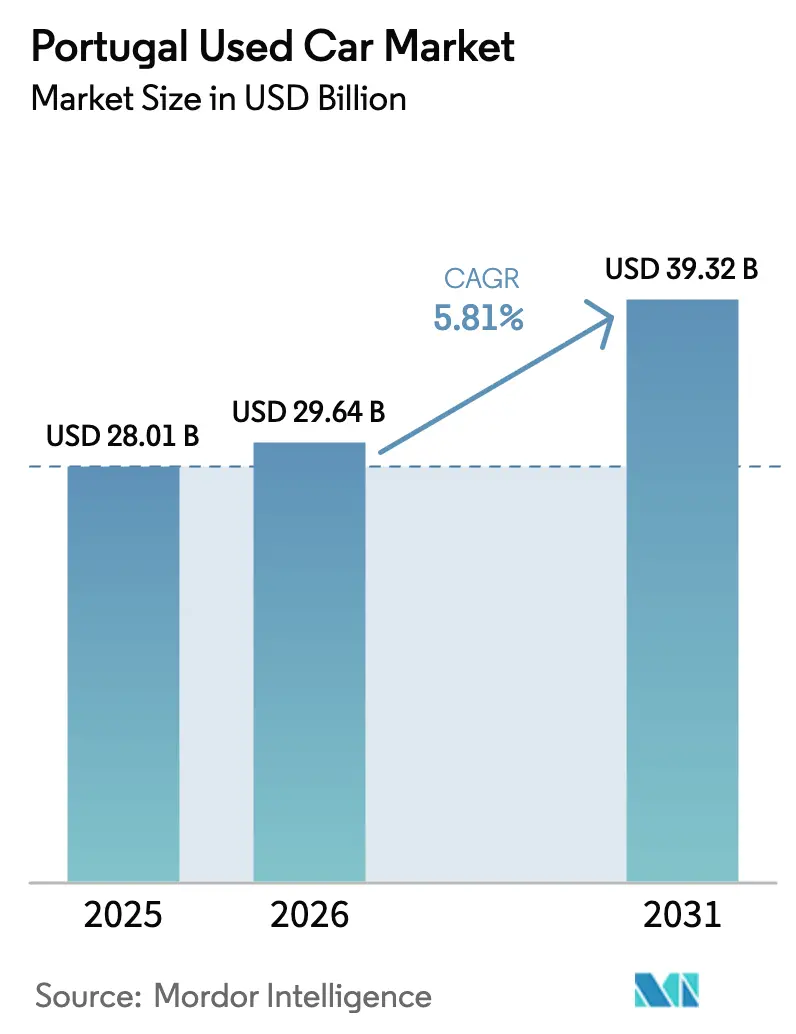

| Base Year Market Size (2025) | USD 28.01 Billion |

| Market Size (2026) | USD 29.64 Billion |

| Market Size (2031) | USD 39.32 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

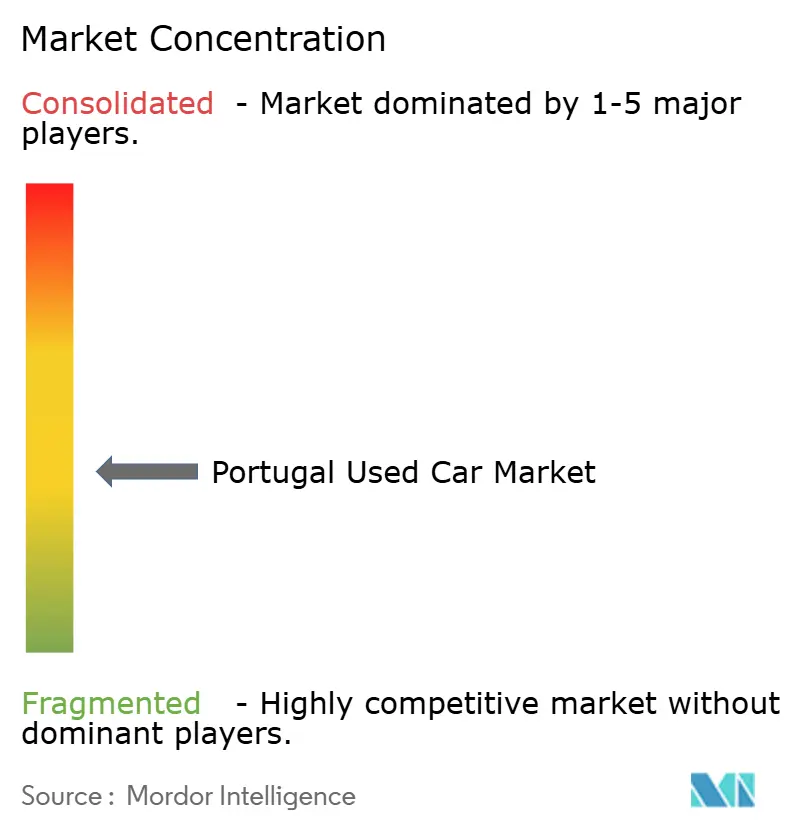

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Used Car Market Analysis by Mordor Intelligence

The Portugal used car market size in 2026 is estimated at USD 29.64 billion, growing from 2025 value of USD 28.01 billion with 2031 projections showing USD 39.32 billion, growing at 5.81% CAGR over 2026-2031. Strong demand stems from widening price gaps between new and used vehicles, a steady inflow of low-mileage Nordic electric cars, and a surge of quality ex-lease stock returning after pandemic deferrals. Government incentives encourage battery-electric adoption, while digital classifieds accelerate inventory discovery and price transparency. Lisboa leads national sales, yet online sales channels are reshaping dealer economics by growing nearly twice as fast as physical outlets. Fragmentation persists because unorganized vendors dominate, but organized players leverage scale, omnichannel models, and financing partnerships to win a share in the Portuguese used car market[1] “Passenger Car Registrations January 2025,” European Commission, ec.europa.eu.

Key Report Takeaways

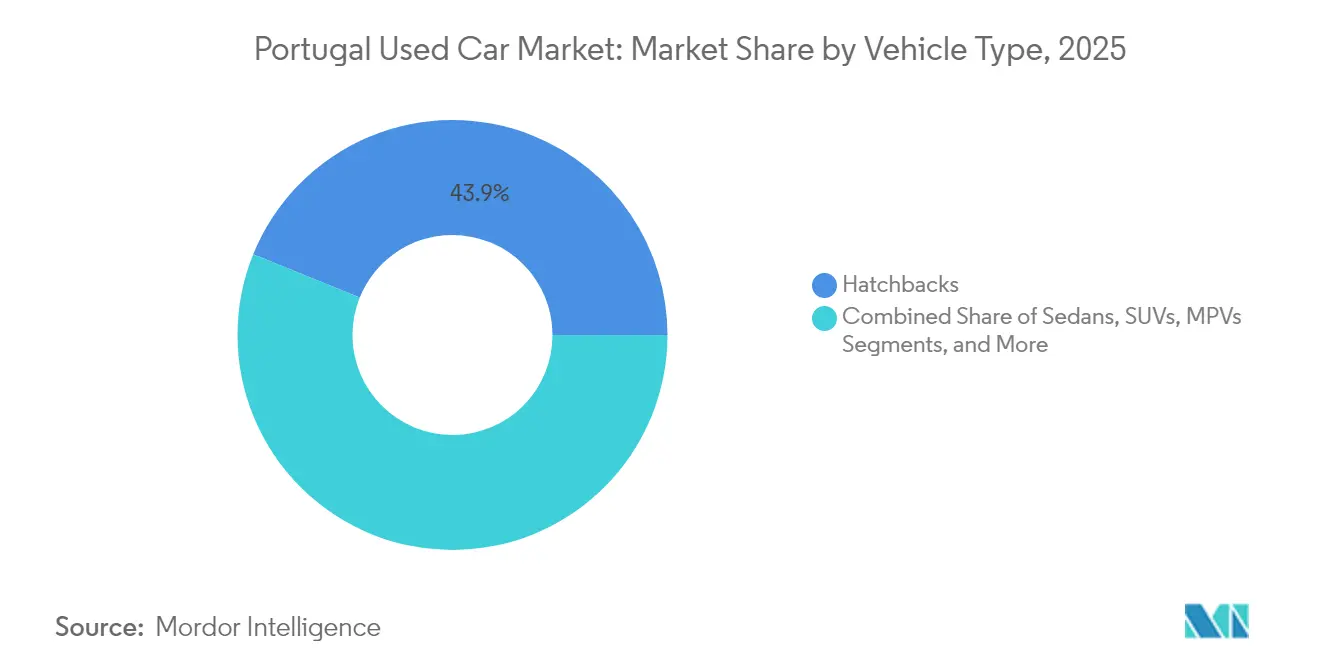

- By vehicle type, hatchbacks led Portugal's used car market revenue share with 43.88% in 2025; SUVs are projected to advance at an 8.02% CAGR by 2031.

- By sales channel, offline OEM-franchised dealers held 58.85% of Portugal's used car market size in 2025, whereas the Online sales channel records the highest projected CAGR at 9.42% through 2031.

- By vendor type, unorganized vendors controlled 56.53% of Portugal's used car market share in 2025; organized vendors are expanding at a 6.93% CAGR.

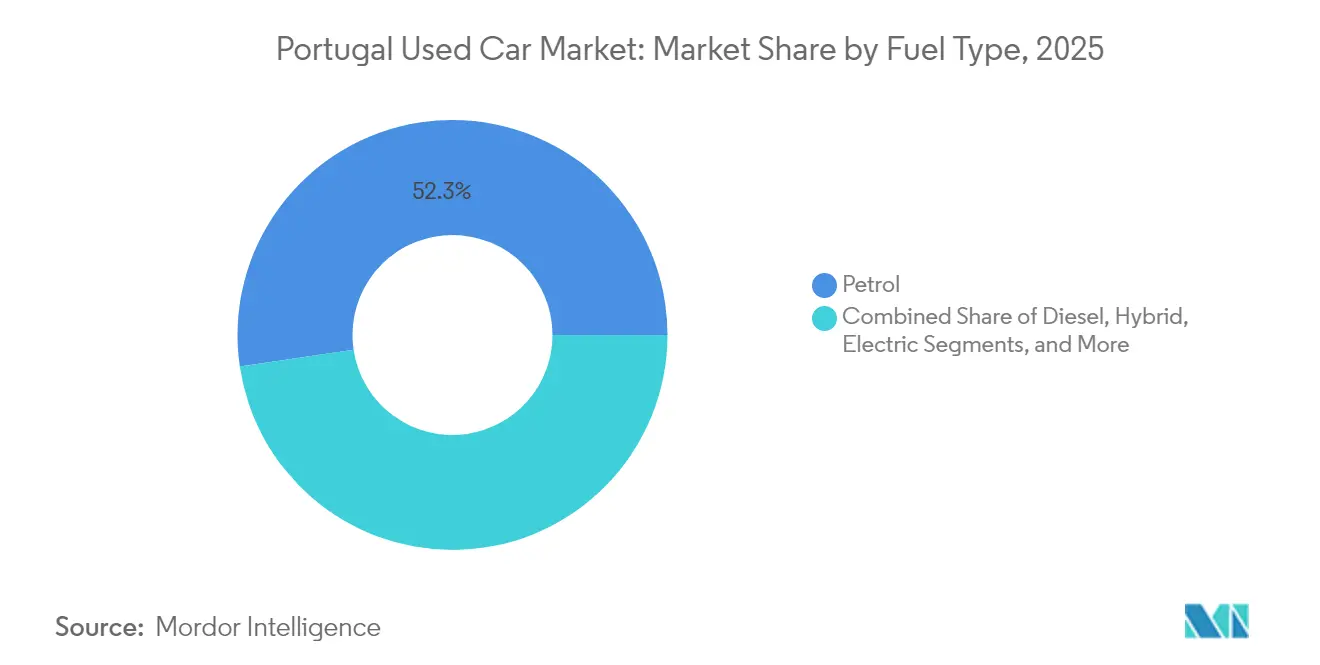

- By fuel type, Petrol accounted for 52.34% share of Portugal's used car market size in 2025, while battery electric vehicles are rising at a 10.21% CAGR.

- By vehicle age, the 3-5 year segment held a 39.87% share of the Portugal used car market in 2025; the 0-2 year bracket shows the fastest 8.63% CAGR amid lease returns.

- By price segment, the USD 5,000-9,999 bracket secured 33.12% of transactions in 2025; the USD 20,000-29,999 tier expands most rapidly at an 8.11% CAGR.

- By transaction type, full-payment deals dominated with 55.27% in the Portugal used car market share in 2025, whereas finance-based deals grow at 8.79% CAGR.

- By region, Lisboa and Vale do Tejo captured 37.88% of Portugal's used car market share in 2025, and the same region is forecast to post a 7.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market participation spans countries and regions, making Portugal competition one layer within a larger international field. In its global used car industry statistics, Mordor Intelligence maps that multi-region structure.

Portugal Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-Driven Widening Price Gap (New Vs Used) | +1.2% | National, with acute impact in Lisboa & Vale do Tejo, Norte | Short term (≤ 2 years) |

| Post-COVID Lease-Fleet Renewals Releasing Quality Stock | +1.1% | National, concentrated in Lisboa & Vale do Tejo, Norte | Short term (≤ 2 years) |

| Nationwide Uptake of Digital Classifieds and E-Commerce | +0.8% | National, with early gains in Lisboa, Porto, Braga | Medium term (2-4 years) |

| Influx Of Low-Mileage Nordic BEV Imports | +0.7% | National, with processing hubs in Lisboa, Porto | Medium term (2-4 years) |

| Purchase-Tax Rebate for Below 8-Year-Old BEVs | +0.5% | National, with higher uptake in urban Lisboa, Porto | Medium term (2-4 years) |

| Growth Of Mobile Pre-Buy Inspection Services | +0.4% | National, with early adoption in metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Widening Price Gap (New Vs Used)

Escalating factory costs and stricter EU regulations lifted average new-car prices, while used-car price growth lagged. In 2025, an average Portuguese worker needs 22.4 months of wages to purchase a typical second-hand car compared with 15.4 months in Romania. The unequal rise reinforces the Portugal used car market as a value proposition, given that 74% of buyers rank price as the deciding factor[2]“2025 ISV Tax Reform Explained,” eCarsTrade, ecarstrade.com. Dealers capitalize on larger sourcing pools to widen gross margins and bridge inventory shortages caused by long domestic ownership cycles.

Nationwide Uptake of Digital Classifieds and E-Commerce

Online channel growth is 9.84% as consumers migrate online for transparent pricing, 360° imagery, and doorstep test drives. Cox Automotive introduced Kelley Blue Book auction-value dashboards in 2024, accelerating professional pricing discipline across the Portuguese used car industry. Government portals now offer downloadable inspection histories for EUR 27, down from EUR 30 on-site, removing paperwork friction. Mobile pre-buy inspection startups partner with ACP/DEKRA to certify vehicles in sellers’ driveways, boosting buyer confidence and fostering liquidity beyond major metro catchment areas.

Post-COVID Lease-Fleet Renewals Releasing Quality Stock

Leasing outstandings surpassed EUR 3 billion in 2024, and deferred replacement cycles are unwinding in 2025[3]“Portuguese Leasing and Factoring 2024,” Associação Portuguesa de Leasing, alf.pt. Ex-lease cars arrive with full maintenance logs, telematics histories, and relatively low mileage, making them premium inventory in the Portugual used car market. Organized vendors exploit priority relationships with leasing firms, acquiring vehicles before auctions and bundling extended warranties. The steady cadence of returns supports predictable advertising spend and smoother inventory turns for professional dealers.

Influx of Low-Mileage Nordic BEV Imports

Used BEV imports jumped 80.1% year-over-year to 1,666 units in January 2025, propelled by Scandinavian lease maturities. Portugal’s full ISV and IUC exemptions for EVs below EUR 62,500 make these imports cost-advantaged, especially after the 2025 rules ended ISV penalties for second-hand imports ecarstrade.com. The flow broadens EV selection, with Tesla, BMW, and BYD topping registrations, pushing BEV new-car share to 22.5% and seeding future used-EV supply.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Ownership Cycles Limiting Domestic Supply | -0.9% | National, with acute impact in rural Alentejo, Algarve | Long term (≥ 4 years) |

| Elevated Financing Costs | -0.6% | National, with disproportionate impact on lower-income regions | Medium term (2-4 years) |

| 23% VAT on Dealer Margin | -0.4% | National, affecting all organized dealers | Long term (≥ 4 years) |

| Odometer Fraud Concerns | -0.3% | National, with higher impact on unorganized segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long Ownership Cycles Limiting Domestic Supply

The average Portuguese household has owned cars for over 12 years, curbing the turnover of desirable 3-5 year-old vehicles. Dealers respond by intensifying import activity, but logistics and homologation paperwork erode margins and lengthen stock days. Prolonged cycles sustain residual values yet reduce on-lot choice, undermining cross-sell potential for warranties and accessories in the Portuguese used car market.

Elevated Financing Costs

Used-car loan APRs climbed to 14.2% in Q3 2025, depressing affordability and reinforcing a cultural bias toward cash purchases. Full-payment deals hold 55.87% share, restricting volume growth in the bigger-ticket SUV and EV segments. Nonetheless, finance transactions grow 9.25% annually as lenders pilot risk-based pricing and fintechs streamline approvals in minutes. Should ECB policy rates ease, latent demand could unlock, particularly for premium EV imports that already enjoy tax relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Drive Premium Shift

Hatchbacks commanded 43.88% of transactions in 2025, anchoring the Portugal used car market with compact, maneuverable options suited to city centers. Yet SUVs are on an 8.02% CAGR trajectory as consumers favor elevated seating, family utility, and the prestige of premium trims. This surge aligns with broader continental moves toward advanced driver-assist packages and plug-in variants now filtering into secondary channels. Dealers note that SUVs average 12% higher gross margins than hatchbacks, offsetting slower turnover. Electric SUVs such as the Tesla Model Y feed the higher-value USD 20,000-29,999 bracket, amplifying organized players’ share gains.

The influx of corporate SUVs from lease contracts bridges inventory bottlenecks while widening model diversity. Buyers previously loyal to sedans step up to used crossovers, driving substitution rather than incremental demand. Petrol-powered SUVs mitigate diesel dependency, and growing BEV choices satisfy green incentives. Dealers leverage predictive analytics to stock popular colors and trims to shorten sales cycles in the dynamic Portuguese used car market.

By Sales Channel: Digital Disruption Accelerates

Offline OEM-franchised dealers retained 58.85% of Portugal's used car market size in 2025 due to trusted service bays and bundled warranties. However, the Online sales channel, logging 9.42% CAGR, transformed journey stages from discovery to finance approval. Smartphones permit 24-hour listings, where VR interior tours and instant valuations shrink time-to-purchase. Web-based escrow diminishes fraud risk, channeling cross-district buyers toward niche stock in regional lots.

Franchised groups counter with omnichannel portals that let buyers check stock online and finish paperwork in-store. Classified aggregators monetize premium placements and data analytics, selling leads to independent dealers without ad tech budgets. Ultimately, convergence rather than displacement defines the Portugal used car market, as hybrids of bricks and clicks optimize convenience, trust, and after-sales touchpoints.

By Vendor Type: Professionalization Gains Momentum

Unorganized vendors controlled 56.53% of the Portugal used car market share in 2025, reflecting legacy corner-lot dealers and driveway resellers. Yet organized networks grow 6.93% annually, buoyed by bank partnerships, certified inspection programs, and scalable procurement from fleet auctions. Consolidators like Santogal acquire brand-aligned retail subsidiaries, securing OEM finance and parts contracts that lift after-sales revenue.

Digitalization raises compliance thresholds in advertising accuracy, GDPR, and tax reporting, squeezing small operators who lack back-office systems. Premium-focused organized dealers tout multipoint checks, free maintenance, and flexible return windows, shifting consumer perceptions of used-car reliability. As battery-electric penetration widens, organized players’ ability to invest in charging and high-voltage technician training cements their edge in the Portugal used car market.

By Transaction Type: Financing Gains Despite Rate Headwinds

Although full-payment deals still dominate at 55.27%, in the Portugal used car market, finance penetration’s 8.79% CAGR reveals demand elasticity once friction eases. Captive lenders roll out balloon structures that mimic operating leases, lowering monthly outlay even with APRs above 14%. Fintech aggregators embed credit checks into dealer websites, cutting approval times from days to minutes. Given household liquidity limits, SUVs and BEVs above USD 20,000 skew heavily toward financing.

APR relief would unlock further upside; until then, dealers refine sales scripts to demonstrate total cost-of-ownership savings from fuel-efficient powertrains. Bundled service contracts mitigate residual value risk, nudging shoppers toward higher trims. The financing trajectory underscores how liquidity innovations complement stock inflows to expand addressable volume in the Portuguese used car market.

By Fuel Type: Electric Transition Accelerates

In the Portugal used car market, Petrol’s 52.34% share in 2025 reflects historical dominance, yet battery electric vehicles are sprinting at 10.21% CAGR. ISV and IUC exemptions on sub-EUR 62,500 BEVs shrink upfront gaps while charging infrastructure doubled public points between 2023-2025. Every imported Nordic BEV widens consumer choice and normalizes range expectations. Petrol and LPG/CNG segments tread water, servicing budget buyers and rural users lacking chargers.

Organized dealers invest in diagnostic tools for electric powertrains, differentiating themselves via battery health certificates that reassure secondary buyers. Over time, policy-driven diesel disincentives could redirect residual value curves, accelerating turnover into cleaner stock. For now, cross-fuel flexibility cushions dealers’ gross profits through diversified inventory in the Portugal used car market.

By Vehicle Age: Near-New Segment Expands

In the Portugal used car market, the 3-5 year cohort retained a 39.87% share in 2025, prized for updated infotainment and remaining manufacturer warranty. Near-new 0-2 year cars, however, expand 8.63% per year due to lease return bulges and corporate fleet upgrades. These cars arrive with predictable condition profiles and fetch higher prices, pushing the Portugal used car market size upwards via mix improvement.

Older brackets face headwinds from rising maintenance costs and urban low-emission zones disfavoring high-NOx diesels. Dealers deploy dynamic pricing to clear aging stock, while fintech-driven microloans help lower-income buyers bridge affordability gaps. The shifting age pyramid reinforces the importance of diversified sourcing, including overseas auctions and rental fleet disposals.

By Price Segment: Premium Categories Gain Share

Transactions between USD 5,000-9,999 still dominate at 33.12%, yet the USD 20,000-29,999 tier races ahead at 8.11% CAGR as affluent urbanites pivot to late-model SUVs and BEVs. Tax incentives compress operating costs, mitigating sticker shock and stimulating upgrades. Luxury brackets above USD 30,000 inch upward, buoyed by tourism-related demand in Algarve and expatriate inflows into Lisbon’s tech hubs.

Dealers exploit higher gross profit per unit while managing credit risk through insured finance packages. Used-EV battery warranties reassure buyers that premium outlays carry predictable lifetime costs. The stratification illustrates how rising incomes and sustainability narratives intertwine to reshape wallet allocation in the Portugal used car market.

Geography Analysis

Lisboa retained 37.88% of the Portuguese used car market share in 2025 sales and will outpace the national average at 7.51% CAGR as startups, multinationals, and government agencies cluster around the capital. High digital literacy and dense charging networks support BEV penetration, while the Port of Lisbon facilitates Nordic import flows that diversify inventory. Shoppers gravitate toward premium SUVs and crossovers, lifting average ticket sizes.

Norte follows, anchored by Porto’s manufacturing heritage and cross-border trade links with Spain. Export-oriented suppliers generate fleet car turnover, feeding organized dealers with steady stock. Centro’s balanced mix of university hubs and agricultural zones sustains predictable demand for fuel-efficient hatchbacks.

Algarve contends with aging demographics and seasonal tourism, respectively. Alentejo’s sparse population and long ownership cycles limit volume yet create scarcity premiums that support dealer margins. Algarve’s rental fleet disposals inject convertibles and MPVs each spring, attracting local buyers seeking discounted ex-hire units. The island regions—Azores and Madeira—face freight costs but enjoy limited competition, allowing island operators to command higher prices within the Portugal used car market.

Coverage of the used car market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Africa, alongside detailed country-level intelligence for Norway, Switzerland, South Africa, New Zealand, Myanmar, Sri Lanka, Belgium, and Nigeria, each shaped by local operating conditions.

Competitive Landscape

The Portugal used car market remains fragmented; Due to the fragmentation, Santogal’s clearance to absorb Mercedes-Benz Retail underlines the regulator's comfort. Organized players couple brand-aligned showrooms with multi-make lots to capture trade-ins, while unorganized dealers rely on local reputation and word-of-mouth.

Digital-first entrants differentiate on convenience—door-to-door delivery, seven-day return policies, and AI-driven price suggestions. Traditional dealers respond via omnichannel investments and service contracts. Nordic BEV import specialists carve a niche by managing homologation and battery diagnostics, areas where small vendors struggle. Finally, fintech partnerships allow captive lenders to pre-approve customers online, capturing finance margins previously lost to banks.

Second-tier disruptors focus on blockchain title validation and predictive maintenance apps to streamline after-sales engagement. As the used-EV park grows, battery health analytics become a new battleground for competitive differentiation. The Portugal used car market illustrates an ecosystem in rapid professionalization yet still open to agile newcomers.

Portugal Used Car Industry Leaders

OOYYO Corp

ALD Automotive

Auto SAPO

BCA.

Guia do Automóvel.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Environmental Fund launched EUR 13 million zero-emission mobility incentives, offering up to EUR 4,000 for private and EUR 6,000 for corporate EV buyers.

- September 2024: The Automóvel Club de Portugal (ACP) urged the Government to adopt three urgent measures in the 2025 State Budget. One key proposal is a direct support of up to 6,000 euros for scrapping end-of-life vehicles. ACP advocates that the reinstated scrapping incentive should encompass all light vehicles aged over 15 years, with heightened benefits for purchasers of new or pre-owned combustion, hybrid, or electric vehicles.

- June 2024: Stellantis announced the opening of a business-to-business marketplace, Spoticar Trade, for pre-owned car sales in European countries like Portugal, Italy, Germany, Spain, France, the Netherlands, Belgium, and Austria.

Portugal Used Car Market Report Scope

The Portugal Used Car Market is Segmented by Vehicle Type (Hatchbacks, Sedans, and Sports Utility Vehicles/Multi-Purpose Vehicles), Vendor Type (Organized and Unorganized), Fuel Type (Petrol, Diesel, Electric, and Other Fuel Types (LPG, CNG, Etc. ), and Sales Channel (Online and Offline).

The Report Offers the Market Size and Forecast in Value (USD) for all the Above Segments.

| Hatchbacks |

| Sedans |

| Sport Utility Vehicle |

| Multi-Purpose Vehicle |

| Online |

| Offline OEM-Franchised Dealers |

| Multi-brand Independent Dealers |

| Physical Auction Houses |

| Organized |

| Unorganized |

| Full Payment |

| Finance |

| Petrol |

| Diesel |

| Hybrid |

| Electric |

| Others |

| 0 - 2 Years |

| 3 - 5 Years |

| 6 - 8 Years |

| 9 - 12 Years |

| Above 12 Years |

| Below USD 5,000 |

| USD 5,000 - 9,999 |

| USD 10,000 - 14,999 |

| USD 15,000 - 19,999 |

| USD 20,000 - 29,999 |

| Above USD 30,000 |

| Lisboa |

| Centro |

| Algarve |

| Rest of Portugal |

| Vehicle Type | Hatchbacks |

| Sedans | |

| Sport Utility Vehicle | |

| Multi-Purpose Vehicle | |

| Sales Channel | Online |

| Offline OEM-Franchised Dealers | |

| Multi-brand Independent Dealers | |

| Physical Auction Houses | |

| Vendor Type | Organized |

| Unorganized | |

| Transaction Type | Full Payment |

| Finance | |

| Fuel Type | Petrol |

| Diesel | |

| Hybrid | |

| Electric | |

| Others | |

| Vehicle Age | 0 - 2 Years |

| 3 - 5 Years | |

| 6 - 8 Years | |

| 9 - 12 Years | |

| Above 12 Years | |

| Price Segment | Below USD 5,000 |

| USD 5,000 - 9,999 | |

| USD 10,000 - 14,999 | |

| USD 15,000 - 19,999 | |

| USD 20,000 - 29,999 | |

| Above USD 30,000 | |

| Region | Lisboa |

| Centro | |

| Algarve | |

| Rest of Portugal |

Key Questions Answered in the Report

What is the current value of the Portugal used car market?

The Portugal used car market size stands at USD 29.64 billion in 2026 and is projected to reach USD 39.32 billion by 2031.

How fast are battery electric vehicles growing in the Portuguese used-car space?

Used BEVs are expanding at a 10.21% CAGR, supported by tax exemptions.

Why are financing rates considered a restraint?

Used-car loan APRs hit 14.2% in Q3 2025, raising monthly payments and limiting leveraged purchases, especially for mid-income buyers.

Which sales channel is growing the quickest?

Online Sales Channel is expected to a 9.42% CAGR, outpacing traditional dealer growth as online shopping gains trust and convenience features.

How long do Portuguese owners keep their vehicles?

Ownership cycles exceed 12 years on average, constricting domestic supply of desirable 3-5 year-old cars and prompting higher import volumes.

Page last updated on: