Industrial Absorbent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

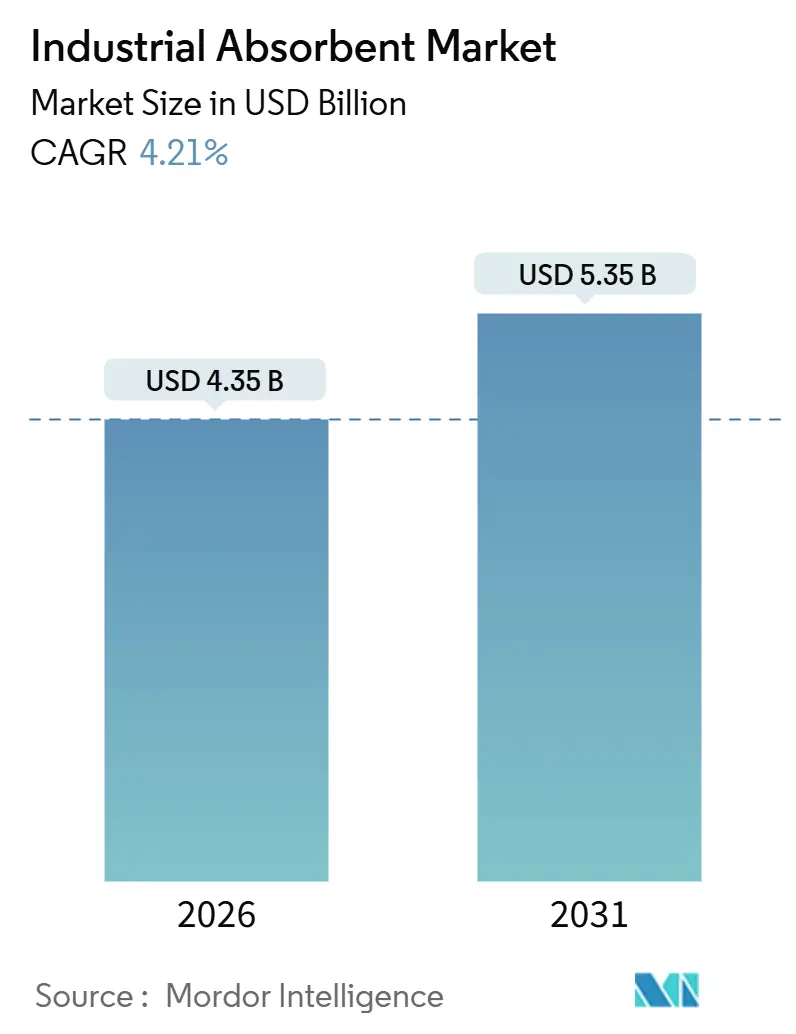

| Market Size (2026) | USD 4.35 Billion |

| Market Size (2031) | USD 5.35 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Absorbent Market Analysis by Mordor Intelligence

The Industrial Absorbent Market size is estimated at USD 4.35 billion in 2026, and is expected to reach USD 5.35 billion by 2031, at a CAGR of 4.21% during the forecast period (2026-2031). The outlook reflects a decisive migration from ad-hoc spill response to integrated safety ecosystems that couple absorbents with leak-detection sensors and predictive-maintenance software. Buyers in petrochemicals and heavy manufacturing are embedding these consumables into capital-project budgets, a change that smooths demand even when production cycles fluctuate. Asia-Pacific remains the volume anchor, yet its growth narrative is increasingly propelled by regulatory ratchets in China and India that mandate certified absorbent materials with documented end-of-life traceability. Competitive intensity remains elevated because the five largest suppliers control less than 40% of revenue, leaving room for regional specialists to undercut on price or out-innovate on sustainability.

Key Report Takeaways

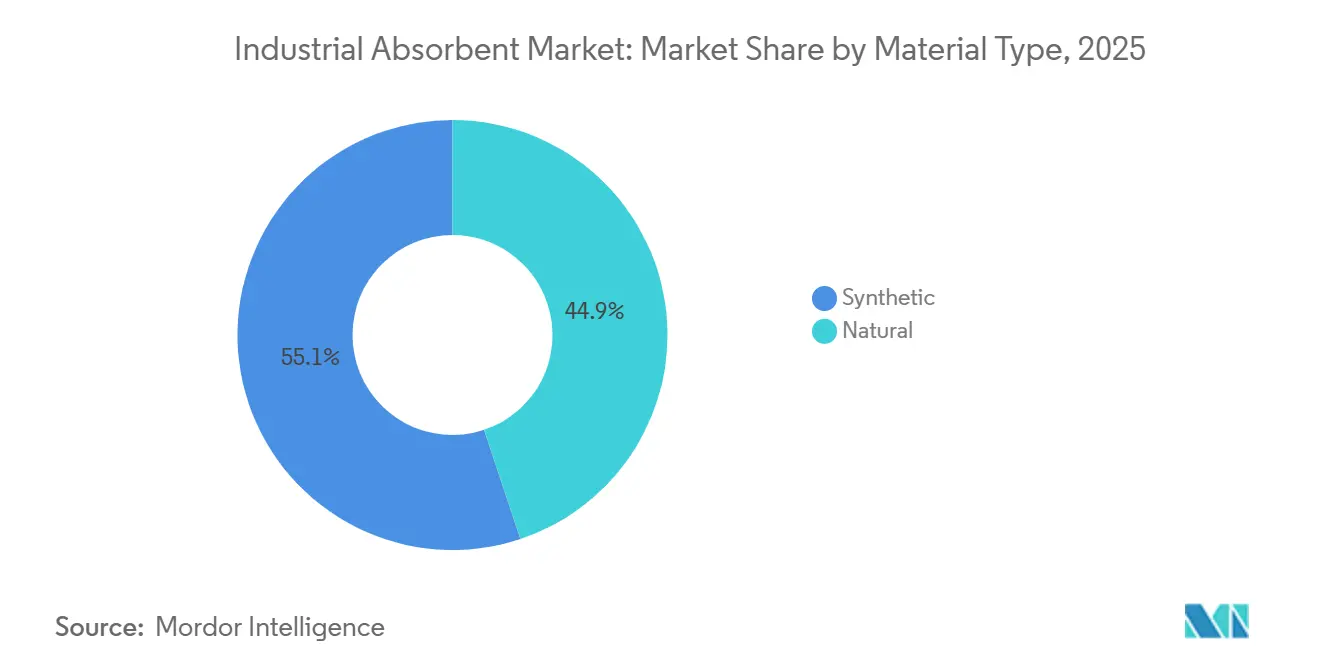

- By material type, synthetic absorbents led with 55.12% of the industrial absorbent market share in 2025, whereas natural materials are projected to post the fastest 5.13% CAGR through 2031.

- By type, oil-only absorbents captured 35.67% revenue share of the industrial absorbent market size in 2025 and are expected to advance at a 4.89% CAGR to 2031.

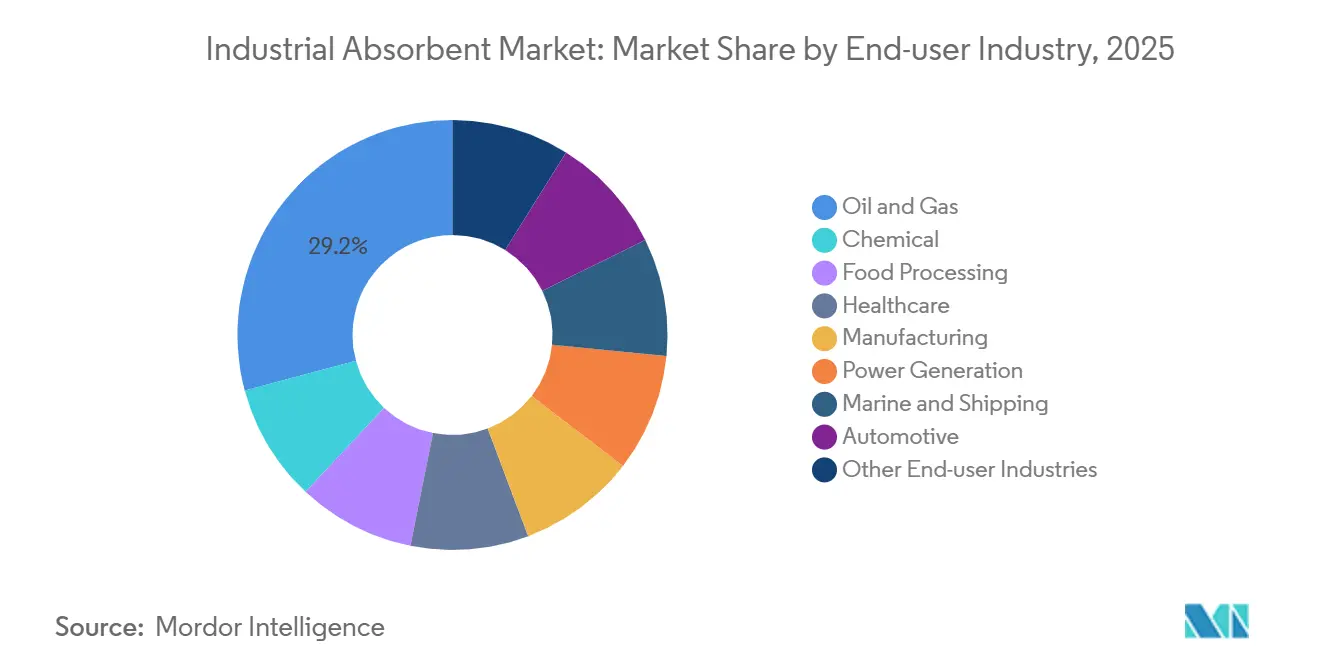

- By end-user industry, oil and gas accounted for a 29.16% share of the industrial absorbent market size in 2025, while healthcare is on track for a 5.67% CAGR through 2031.

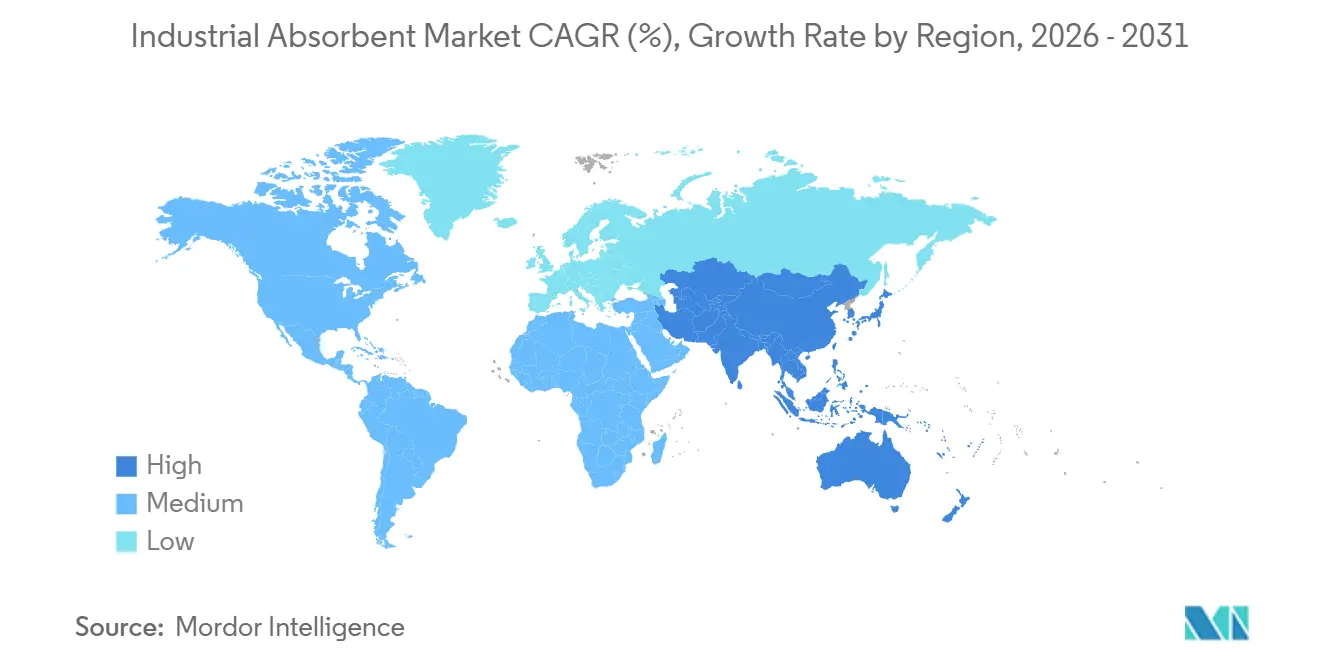

- By geography, Asia Pacific dominated with 38.32% industrial absorbent market share in 2025; the region is set to grow at a 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Absorbent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for spill-control in oil and gas expansion | +1.2% | Middle East, North America, Asia-Pacific | Medium term (2-4 years) |

| Stricter multi-regional environmental enforcement | +1.0% | Global, with EU and China leading | Long term (≥4 years) |

| Increasing cost and frequency of industrial spills | +0.8% | Global | Short term (≤2 years) |

| Rapid growth of Asia-Pacific petrochemical output | +0.9% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| Commercialization of bio-based sorbents from agro-waste | +0.5% | North America, Europe, India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Spill-Control in Oil and Gas Expansion

Global upstream capital expenditure reached USD 525 billion in 2025, a 12% jump over 2024, with the Middle East supplying 38% of the incremental outlay[1]International Energy Agency, “World Energy Investment 2026,” iea.org. Each new rig, pipeline, or processing skid requires oil-only booms and pads to comply with spill-prevention standards under the US Clean Water Act and similar regulations in the Gulf Cooperation Council. North American shale operators drilled 1,200 additional horizontal wells in 2025, and each completion generated spill-control demand for hydrophobic mats that contain 18 barrels of flow-back fluid during tank transfers. Longer-lateral wells, some exceeding 3 km, raise the number of surface connections and elevate micro-leak risks, which sustains absorbent pull-through even as rig counts plateau. Insurance carriers now request documented absorbent inventories before underwriting general liability policies, pushing facilities to hold safety-stock levels that further buoy the industrial absorbents market.

Stricter Multi-Regional Environmental Enforcement

The European Union’s Industrial Emissions Directive, revised in 2024, obliges sites handling more than 10 t of hazardous liquids annually to demonstrate “best available techniques” for spill containment, effectively codifying certified absorbent usage and disposal trails. China’s Ministry of Ecology and Environment instituted a parallel framework in 2025 for petrochemical clusters along the Yangtze River Economic Belt, requiring absorbent liners that meet GB 18597 leachate-prevention standards. Enforcement intensity is tangible: EU states issued 1,840 spill-control citations in 2025 and lifted average fines to EUR 47,000 per incident[2]European Environment Agency, “Industrial Emissions Compliance 2025,” eea.europa.eu. ISO 14001 audits now include absorbent stock verification, turning previously discretionary spending into a non-negotiable compliance line item. This regulatory ratchet is translating into a full percentage point of additional long-term CAGR for the industrial absorbents market.

Increasing Cost and Frequency of Industrial Spills

The US National Response Center recorded 11,200 hazardous-material incidents in 2025, a 9% uptick from 2024, with chemical manufacturing and transport responsible for 42% of cases. Average cleanup expense for a 50-gallon industrial spill climbed to USD 8,500 in 2025 after disposal fees and contractor rates rose 15%. Facilities are therefore pre-positioning absorbent kits at high-risk transfer points to contain leaks within the first 10 minutes, a practice that can trim cleanup costs by 60% according to OSHA incident data. Insurers have tightened policy language to require on-site absorbent inventories, effectively hard-coding baseline demand into risk-management programs. This behavior change adds 0.8 percentage points to the near-term growth trajectory of the industrial absorbents market.

Rapid Growth of Asia-Pacific Petrochemical Output

China brought 4.2 million t per year of new ethylene capacity online in 2025, each cracker demanding 120–180 t of absorbents annually for maintenance and emergency response. India’s petrochemical output grew 11% as Reliance Industries and Indian Oil ramped up cracker utilization. Southeast Asian nations such as Vietnam and Indonesia are also adding downstream polymer assets under stricter environmental-impact assessments that mandate certified absorbents. The spill-over effect reaches the Middle East, where Saudi Arabia’s USD 20 billion Amiral complex sources absorbents from Asian vendors, tightening regional supply. Collectively, these expansions inject 0.9 percentage points into medium-term CAGR for the industrial absorbents market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Worker-exposure hazards in manufacturing and disposal | -0.4% | Global, with stricter enforcement in North America and EU | Medium term (2-4 years) |

| Volatile polypropylene and mineral feedstock prices | -0.6% | Global | Short term (≤2 years) |

| Shift toward reusable spill-containment booms and pads | -0.3% | Marine and offshore sectors, North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Worker-Exposure Hazards in Manufacturing and Disposal

OSHA’s 2025 crystalline-silica rule lowered permissible exposure to 50 µg/m³, forcing clay-absorbent plants to install high-capacity ventilation or switch to amorphous silica at 30–40% higher material cost. Three US manufacturers accrued USD 1.2 million in fines during the first compliance year. On the disposal side, spent absorbents contaminated with hazardous chemicals are now F-listed waste under the Resource Conservation and Recovery Act, and incineration fees rose 18% in 2025 amid landfill-capacity tightness. EU “duty of care” clauses extend liability down the waste stream, discouraging smaller firms without dedicated compliance staff from adopting single-use absorbents. These factors remove 0.4 percentage points from medium-term CAGR.

Volatile Polypropylene and Mineral Feedstock Prices

Polypropylene resin traded between USD 1,200 and USD 1,650 /t in 2025 as naphtha prices swung with crude volatility and hurricane-related cracker outages on the US Gulf Coast. Spot spikes above USD 1,600 /t pushed several mid-tier converters into negative gross margins. Mineral absorbents faced comparable headwinds as Chinese attapulgite exports tightened and US mining energy costs climbed; attapulgite prices rose 22% while diatomaceous earth gained 14%. Buyers negotiated quarterly price-adjustment clauses, yet smaller distributors cut inventories, slowing market velocity. The result is a 0.6 percentage-point drag on near-term growth for the industrial absorbents market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Natural Fibers Gain Ground on Cost and Compliance

Synthetic formats still held 55.12% revenue in 2025, a lead underpinned by the five-year shelf life of sealed melt-blown webs compared with 18–24 months for untreated natural fibers, yet bio-based suppliers are closing the gap with barrier-coated foil packaging. Universal absorbents that sandwich polypropylene layers around a cellulose core are gaining favor in automotive plants where spills may involve both water and oil, thereby simplifying inventory management. Hazmat absorbents, tailored for acids and aggressive chemicals, enjoy niche demand in battery manufacturing, where electrolyte leaks require polypropylene fabrics resistant to hydrofluoric acid. Natural fibers are projected to grow at a 5.13% CAGR through 2031, outpacing synthetics despite their smaller base. In 2025, rice-husk absorbents processed via carbonization and hydrophobization delivered 8–12× oil retention at 20–30% lower landed cost than polypropylene pads. India’s Council of Scientific and Industrial Research validated coconut-coir mats treated with silane coupling agents, unlocking export potential to Europe and North America.

In disposal economics, lighter-weight natural mats reduce landfill tonnage and transportation costs, advantages amplified by rising waste-management fees in the EU and Japan. Carbon accounting adds a further tailwind: a bio-based mat carries about one-third the cradle-to-gate emissions of a polymer equivalent, a metric now scrutinized under the EU Corporate Sustainability Reporting Directive. As natural suppliers integrate upstream into feedstock aggregation and downstream into finished pad production, their delivered-cost advantage could widen. Nonetheless, scale constraints persist; agro-waste availability is seasonal, and pre-treatment plants often operate below optimal utilization, limiting price competitiveness during peak polymer oversupply.

By Type: Oil-Only Absorbents Lead on Offshore and Petrochemical Demand

Oil-only absorbents commanded 35.67% of 2025 revenue and are advancing at a 4.89% CAGR, driven by offshore wind construction and petrochemical expansions that require hydrophobic materials impervious to seawater. Each new offshore turbine nacelle consumes about 12 kg of pads during annual maintenance. Engineered oleophilic coatings on these pads deliver oil-to-water selectivity exceeding 20:1, a threshold that universal variants cannot match. Middle Eastern complexes such as the Amiral project installed 4,200 m of boom for secondary containment around storage tanks.

Universal absorbents, the workhorse for mixed-fluid environments, benefit from simplified inventory rules in food and beverage plants where spills may involve water, cleaning solutions, or cooking oils. Hazmat formats, though volumetrically smaller, are experiencing steady uptake in battery gigafactories, where electrolyte spills require fabrics resistant to corrosive lithium salts. Specialty types designed for mercury or radioactive liquids serve episodic niches in healthcare and nuclear decommissioning. Competition among types is, therefore, more a matter of application specificity than price. As offshore wind and petrochemical investments surge, oil-only formats will likely extend their lead, though universal products will continue to dominate in multi-fluid manufacturing settings, sustaining diverse demand across the industrial absorbents market.

By End-User Industry: Healthcare Surges on Infection-Control Protocols

Oil and gas retained the revenue crown with 29.16% in 2025, underpinned by continuous drip-pan and valve-leak applications at well sites and midstream terminals. Healthcare is set to post the fastest 5.67% CAGR to 2031 as hospitals adopt single-use mats impregnated with silver ions to contain blood-borne pathogens during surgery. The US CDC revised its spill-control guidelines in March 2025, recommending absorbent barriers for all Category A infectious substances. European hospitals followed suit after ECDC data showed 3.2 million patients affected by healthcare-associated infections in 2025.

Chemical manufacturing remains a core consumer, especially in batch reactors that produce frequent microspills of corrosive or flammable liquids. Food-processing demand is accelerating as US FDA sanitation audits now survey absorbent protocols, and production holds linked to non-compliance can cost USD 15,000–30,000 per day. Marine and shipping segments see periodic spikes tied to International Maritime Organization regulations requiring vessels over 400 GT to carry oil-only booms and pads. Manufacturing, power generation, and automotive each maintain mid-single-digit shares, their trajectories tethered to capacity additions and regulatory vigilance. The industrial absorbents market therefore exhibits a broad end-user portfolio, with healthcare emerging as the fastest growth vector while energy and chemicals anchor volume.

Geography Analysis

Asia-Pacific contributed 38.32% of 2025 revenue and is projected to expand at a 5.78% CAGR to 2031, underscoring its dual drivers of petrochemical capacity growth and increasingly stringent environmental mandates. China’s 4.2 million t ethylene additions in 2025 created recurring demand of roughly 120–180 t of absorbents per cracker for maintenance and emergency readiness. India’s Central Pollution Control Board broadened mandatory spill-response plans to facilities handling more than 5 t of hazardous liquids, capturing 1,200 additional sites in 2025. Japan’s April 2025 revision of the Industrial Safety and Health Act requires documented absorbent stockpiles, adding 800 t of annual demand. ASEAN petrochemical entrants face export-oriented customers that demand ASTM-compliant spill kits, lifting import volumes into Vietnam and Indonesia.

North America remains the second-largest region, buoyed by shale expansion and Gulf Coast chemical builds. The Permian Basin added 1,200 horizontals in 2025, each requiring hydrophobic mats for flow-back containment. The US SPCC rule applies to 638,000 facilities with above-ground oil storage exceeding 1,320 gal and underpins baseline demand for oil-only absorbents. Canada’s oil-sands production rebounded to 3.1 mb/d, triggering restock cycles for clay granules and polypropylene pads. Mexico’s Pemex began upgrading spill-response kits after environmental fines in 2024, creating fresh orders for universal and hazmat variants.

Europe is oriented toward sustainability-driven procurement. The Corporate Sustainability Reporting Directive forces large enterprises to disclose carbon footprints of consumables, accelerating adoption of bio-based mats and reusable systems. Germany, the UK, and France collectively account for more than half of regional demand, with volumes anchored in chemicals, automotive, and food. Price sensitivity has moderated as corporations assign internal carbon prices that favor low-emission alternatives.

South America’s growth pivots on energy and mining. Brazil’s pre-salt output rose by 240,000 b/d in 2025, and Ibama licenses require oil-only booms on each offshore platform. Argentina’s Vaca Muerta ramped 180 new wells in 2025, sourcing absorbent supplies both locally and from the US. The Middle East and Africa rely on hydrocarbon investments; Saudi Arabia’s Amiral complex, operational since late 2024, imports pads and socks from Asian fabricators. UAE and Qatar LNG projects mirror those specifications, while South Africa and Nigeria see intermittent demand spikes tied to power-plant overhauls and port expansions. Collectively, the geographic mosaic confirms that the industrial absorbents market maintains diversified regional anchors, with Asia-Pacific setting the pace.

Competitive Landscape

The Industrial Absorbent market is moderately consolidated. Consolidation pressure is rising, however, as large buyers demand integrated solutions that bundle materials with sensor-enabled cabinets and inventory-tracking software. In 2025, Brady rolled out connected spill-response stations that trigger automatic reorders when stock falls below thresholds, an innovation already piloted in 18 chemical plants. Vertically integrated players that control polymer extrusion, nonwoven production, and spill-service contracts are best positioned to weather raw-material volatility and capture premium margins.

Industrial Absorbent Industry Leaders

3M

Brady Worldwide, Inc.

Kimberly-Clark Worldwide, Inc.

Oil-Dri Corporation of America

New Pig Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sumitomo Seika Chemicals Co. completed a dedicated pilot plant for super or industrial absorbent polymers at its Himeji Works in Japan. This plant is designed as a scaled-down model of its actual manufacturing plant, enabling medium-scale experiments under conditions similar to actual manufacturing environments.

- April 2025: FyterTech Nonwovens upgraded its Sustayn product line. The enhanced Sustayn line boasts a biodegradation acceleration technology, enabling it to biodegrade three times faster than conventional meltblown absorbent pads within the same timeframe.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the industrial absorbent market as all loose, sheet, pad, mat, boom, sock, pillow, and granular media, whether natural fiber, mineral, or synthetic polymer, that are purpose-built to contain or recover oils, chemicals, or other industrial liquids during routine operations, maintenance, and spill response. We size only new, first-use absorbent products and track revenues at manufacturer selling price.

Scope exclusion: consumer hygiene items, personal wipes, and bulk super-absorbent polymer feedstocks are left outside this assessment.

Segmentation Overview

- By Material Type

- Natural

- Synthetic

- By Type

- Universal

- Oil-only

- Hazmat

- Other Types

- By End-user Industry

- Oil and Gas

- Chemical

- Food Processing

- Healthcare

- Manufacturing

- Power Generation

- Marine and Shipping

- Automotive

- Other Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Structured discussions with EHS managers at refineries, distributors across Southeast Asia, and product engineers at absorbent converters helped us verify consumption rates, seasonality shifts, and prevailing average selling prices. Follow-up surveys with facility maintenance buyers in North America and Europe further calibrated adoption trends for bio-based alternatives.

Desk Research

We gathered baseline demand cues from freely available tier-one sources such as the US Environmental Protection Agency spill incident database, Eurostat hazardous-waste generation files, the International Tanker Owners Pollution Federation spill statistics, and UN Comtrade export codes for polypropylene sorbents. Company 10-Ks, refinery maintenance filings, and reputable trade journals filled product mix and price gaps.

To test financial reasonableness, Mordor analysts referenced snapshots from D&B Hoovers for supplier revenue splits, tapped Dow Jones Factiva for tender awards, and skimmed Asia Metal customs tracks for mineral absorbent trade flows. The sources listed here are illustrative; many other public and subscription assets informed data validation and clarification activities.

Market-Sizing & Forecasting

A top-down and bottom-up blend underpins the model. We first reconstructed the global demand pool by mapping refinery throughput, well-drilling meterage, chemical plant capacity additions, and global industrial PPE spending against historical spill probabilities. We then converted liquid volumes to absorbent weight equivalents using standard uptake ratios. Select bottom-up checks, manufacturer shipment audits, and sampled polypropylene fiber ASP × volume tempered the totals.

Forecasts draw on a multivariate regression where the leading indicators above, plus regulatory penalty intensity and oil price outlook, explain 92% of past variance. ARIMA overlays capture short-cycle shocks before results are aligned to expert consensus gathered through primary research.

Data Validation & Update Cycle

Outputs pass variance scans versus independent trade, price, and incident data, after which a senior reviewer clears anomalies. Reports refresh each year; material events such as a major spill or regulatory change trigger interim revisions. A final analyst pass occurs just before client delivery to ensure the freshest snapshot.

Why Mordor's Industrial Absorbent Baseline Commands Reliability

Published values often diverge because each firm picks different product mixes, geographic splits, and refresh rhythms. Our disciplined scoping and annual recalibration keep the playing field level and transparent for decision-makers.

Key gap drivers stem from three areas: some publishers omit mineral sorbents, others stop at historical spill volumes without price normalization, while a few fold in consumer pad revenues that inflate the base. Mordor's clear boundary setting, variable selection, and yearly update cycle minimize such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.31 billion (2025) | Mordor Intelligence | |

| USD 4.43 billion (2024) | Global Consultancy A | Excludes clay-based absorbents and Asia's smaller producers |

| USD 4.30 billion (2023) | Industry Association B | Relies on spill-volume weighting without forward price adjustment |

| USD 4.63 billion (2024) | Regional Consultancy C | Includes consumer absorbent pads within revenue pool |

In short, Mordor's stepwise modeling, balanced variable mix, and tight scope give end users a dependable, reproducible baseline that aligns closely with real industrial demand yet avoids hidden over- or under-counts.

Key Questions Answered in the Report

What is the current size of the industrial absorbents market?

What is the current size of the industrial absorbents market?

Which segment leads by material type?

Which segment leads by material type?

Why are oil-only absorbents gaining traction?

Why are oil-only absorbents gaining traction?

Which region will grow the fastest?

Which region will grow the fastest?

How fragmented is supplier competition?

How fragmented is supplier competition?

Page last updated on: