Thermoplastic Polyurethane (TPU) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

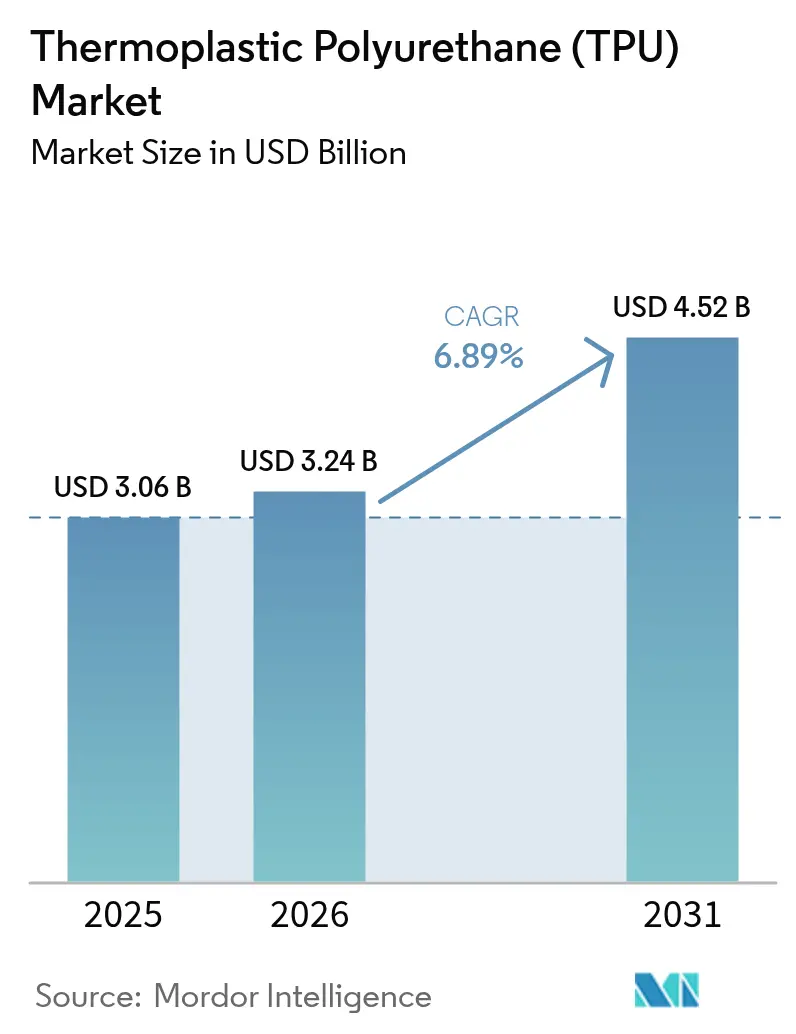

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 4.52 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoplastic Polyurethane (TPU) Market Analysis by Mordor Intelligence

The Thermoplastic Polyurethane Market size is expected to increase from USD 3.06 billion in 2025 to USD 3.24 billion in 2026 and reach USD 4.52 billion by 2031, growing at a CAGR of 6.89% over 2026-2031. Regulatory pressure on volatile-organic-compound emissions, a pivot toward bio-based feedstocks, and the rise of circular-design mandates all accelerate the shift from commodity polyester grades to specialty formulations. Medical-grade demand benefits from on-body wearables that require shore-A hardness below 70 and validated ISO 10993 biocompatibility. In electric vehicles, original equipment manufacturers specify solvent-free reactive grades for in-mold decoration that eliminate post-painting steps. Footwear brands pursue mono-material constructions that allow mechanical recycling, compelling converters to raise recycled-content thresholds above 30%. Feedstock integration and backward-linked 1,4-BDO capacity increasingly determine supplier margins.

Key Report Takeaways

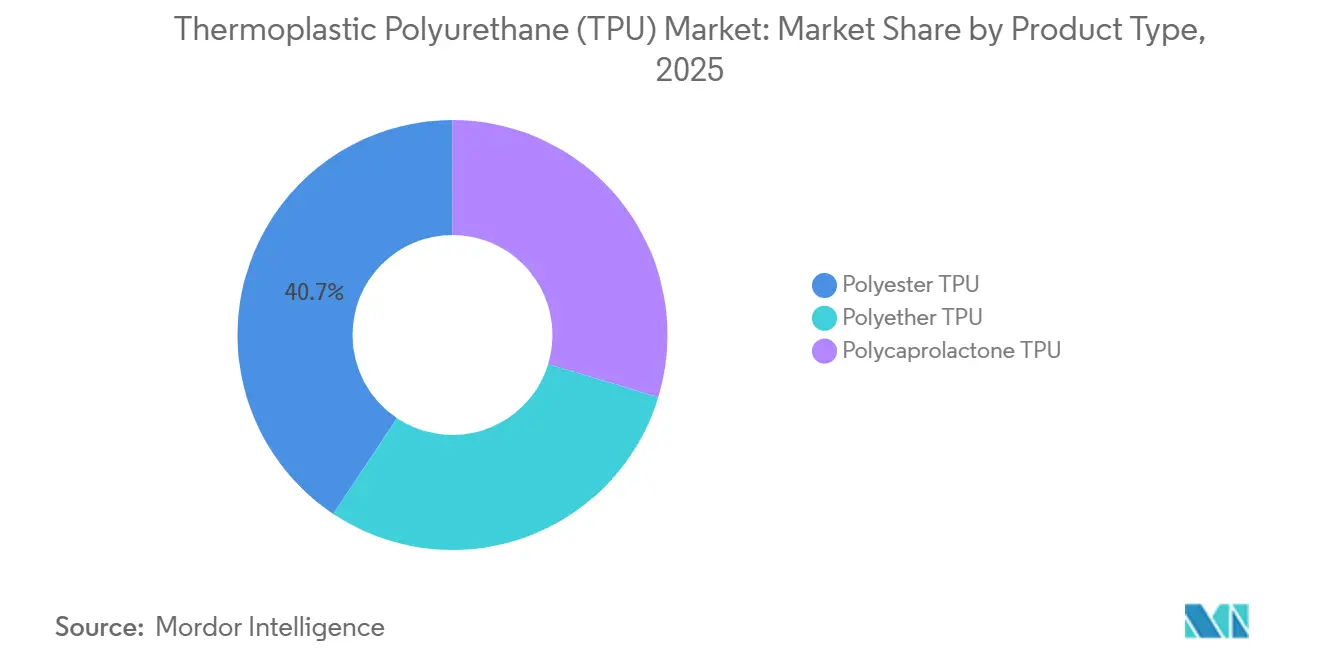

- By product type, polyester TPU led with 40.65% revenue share in 2025 and is projected to expand at a 7.92% CAGR through 2031.

- By application, extruded products held 44.19% of the thermoplastic polyurethane market share in 2025, while injection-molded products are expected to witness the highest projected CAGR at 7.99% through 2031.

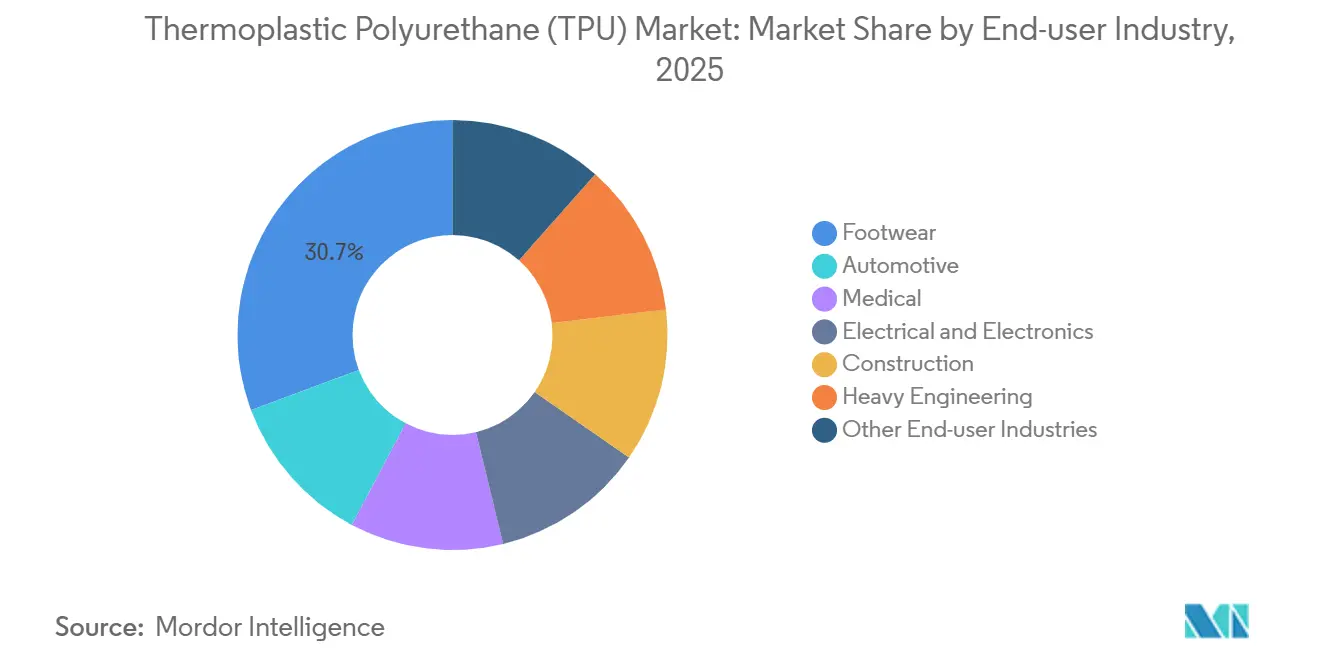

- By end-use industry, footwear commanded 30.68% of the thermoplastic polyurethane market size in 2025; automotive components are set to grow at 8.07% CAGR between 2026-2031.

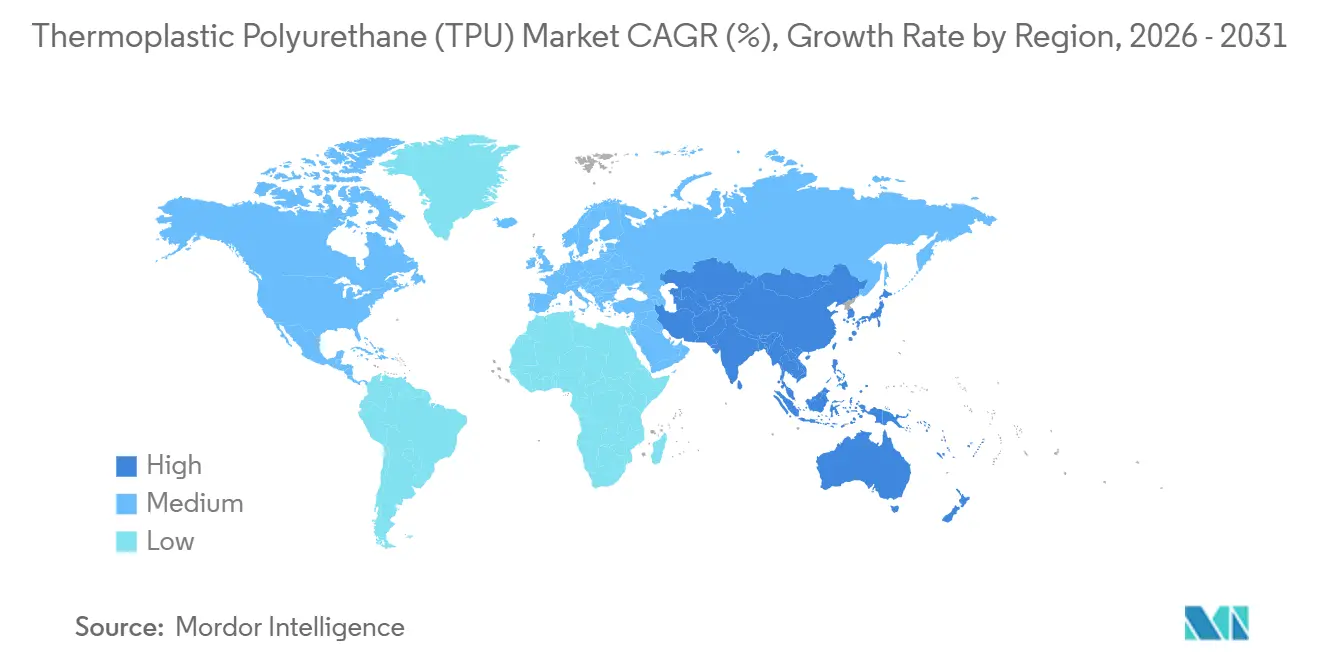

- By region, Asia Pacific captured 58.72% of global revenue in 2025 and is advancing at a 7.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermoplastic Polyurethane (TPU) Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wearable Medical Devices Driving Medical-Grade TPU Demand | +1.2% | Global, with North America and Europe leading regulatory approvals | Medium term (2-4 years) |

| 3D-Printing Filaments & Powders Accelerating Prototyping Adoption | +0.9% | North America, Europe, APAC manufacturing hubs | Short term (≤ 2 years) |

| Bio-Based Mono-Material Footwear Programs Boosting Consumption | +1.4% | Global, concentrated in Asia-Pacific production and Europe/North America brand adoption | Long term (≥ 4 years) |

| PVC-to-TPU Shift in Flexible Solar & Architectural Membranes | +0.8% | Europe, North America, Middle East infrastructure projects | Medium term (2-4 years) |

| Solvent-Free Reactive Extrusion Grades Enabling In-Mold EV Interior Decoration | +1.3% | APAC core (China, South Korea), spill-over to North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Wearable Medical Devices Driving Medical-Grade TPU Demand

Continuous glucose monitors and smart cardiac patches have reached an installed base worth USD 40 billion. They require tensile strength above 30 MPa and full ISO 10993 validation. Polyether TPU dominates due to superior hydrolysis resistance. Abbott’s FreeStyle Libre 3 adopted a custom polyether grade with elongation beyond 500% to withstand flex cycling[1]Medical Devices Section, “FreeStyle Libre 3 FDA Clearance,” Abbott, abbott.com. Device makers add antimicrobial masterbatches at 2–5%, raising resin cost by about 15% yet enabling premium pricing for Class II products. Smaller converters struggle to finance clean-room facilities, concentrating share with vertically integrated resin suppliers that provide toll compounding and regulatory dossiers.

3D-Printing Filaments and Powders Accelerating Prototyping Adoption

Additive manufacturing consumed 12,000 t of TPU in 2025, split between filament and powder. Automotive Tier-1s reduce prototype lead time from 12 weeks to 48 hours and apply lattice structures that tune crash energy absorption. BASF’s Ultrasint TPU 88A introduced a hydrophobic treatment that extends powder shelf life to 12 months, solving moisture-uptake failures[2]Additive Manufacturing Team, “Ultrasint TPU 88A Whitepaper,” BASF, basf.com. Footwear brands print midsoles with weight savings near 20% and rebound retention above 55%. Moisture sensitivity remains the primary technical hurdle; filament must be dried to below 0.02% moisture prior to printing, or steam voids appear.

Bio-Based Mono-Material Footwear Programs Boosting Consumption

Nike and Adidas target fully recyclable shoes by 2030. Desmopan 37385A reaches 69 % renewable carbon content and meets ASTM D6866 certification, letting brands allocate renewable claims in climate reporting. Lubrizol’s Estane ETE 75DT3 adds 45 % post-consumer content while keeping tensile strength over 35 MPa. Collection systems are the bottleneck; only 8 % of athletic shoes entered take-back programs in 2025. Forthcoming EU ecodesign rules from January 2027 will penalize footwear that cannot be mechanically recycled.

PVC-to-TPU Shift in Flexible Solar and Architectural Membranes

Phthalate bans under REACH Annex XVII push photovoltaic backsheets toward TPU, extending module life by a decade and lowering the levelized cost of energy by 4%. Covestro’s Platilon U 4201 AU passed IEC 61215 damp-heat testing at 3,000 h without delamination. The Middle East represents 22 % of global architectural-membrane demand with projects that face ambient temperatures above 50°C.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 1,4-BDO Feedstock Volatility Inflating Polyester/Ether TPU Prices | -1.1% | Global, acute in Asia-Pacific spot markets | Short term (≤ 2 years) |

| Tightening Isocyanate-Exposure Regulations | -0.7% | Europe (REACH), North America (OSHA), spillover to APAC | Medium term (2-4 years) |

| Displacement Risk from High-Heat TPEE & TPV in Automotive Applications | -0.5% | Global automotive supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

1,4-BDO Feedstock Volatility Inflating Polyester/Ether TPU Prices

Asian spot values fluctuated between USD 1,800 and USD 2,400 t in 2024-2025, taking 4-6 percentage points off gross margin for non-integrated producers. BASF and Wanhua benefit from backward-integrated BDO capacity that shields contracts from spot swings. Smaller players reformulate toward polycaprolactone TPU but accept lower tensile strength. Capacity is concentrated in China, which holds 68 % of the global BDO nameplate; power rationing can idle plants without notice.

Tightening Isocyanate-Exposure Regulations

The August 2023 REACH amendment obliges certified training for handlers of formulations above 0.1% free diisocyanate, raising compliance costs by EUR 800 per worker. OSHA proposed a 5 ppb ceiling for MDI in October 2024, spurring US producers to install closed systems. Covestro spent EUR 15 million in 2025 upgrading Dormagen to meet these levels. Polyester TPU is more exposed than polyether because of MDI reliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polyester Dominance Masks Polycaprolactone's Niche Surge

Polyester TPU delivered 40.65% of 2025 revenue and will maintain a healthy trajectory given balanced mechanical strength and cost edge. Polycaprolactone TPU, while small in volume, is expanding at a 7.92% rate as brands adopt compostable packaging. Medical-grade polyether TPU secures ISO 10993 approvals, insulating it from price pressure. Recycled-content polyester grades, including Desmopan 2590A with 25 % post-industrial regrind, meet voluntary sustainability targets without impacting hardness. Adipic-acid feedstock remains concentrated in China, creating supply-risk premiums that could erode the long-run cost advantage of commodity polyester.

Polycaprolactone TPU relies on a monomer base below 150 kt global capacity, constraining scale. Yet in applications such as temporary orthopedic implants, its biodegradability offsets performance gaps. Waterborne TPU dispersions that eliminate solvents are gaining traction in coatings. These dispersions contain less than 50 g/L VOC and comply with CARB 1168, positioning them for architectural coatings across North America.

By Application: Injection Molding Gains as Extrusion Faces Margin Pressure

Extruded products maintained 44.19% share of 2025 revenue. High-volume Asian converters run at elevated utilization, squeezing global net margins below 8%. Injection-molded articles are forecast to grow at 7.99%, driven by airbag covers, slim consumer-electronics housings, and ski-boot shells that require wall sections under 0.8 mm with premium surface finish. Adhesives, though smaller in turnover, benefit from moisture-curing reactive hot melts that bond polycarbonate to aluminum without primers, supporting lightweighting.

Advances in nucleating agents cut demolding time to 22 s for a 2 mm part, improving tooling return on investment. Conductive TPU with graphene loads achieves surface resistivity under 10⁶ Ω sq, enabling electrostatic-dissipative cases in semiconductor fabs. EU battery regulation dictating removable batteries by 2027 will increase TPU demand in peelable adhesives that soften at 80°C, facilitating repair and recycling.

By End-Use Industry: Automotive Electrification Outpaces Footwear's Volume Base

Footwear still delivers 30.68 % of turnover, but pair-wise material intensity falls as brands adopt foamed TPU and supercritical molding. Automotive applications advance at an 8.07% CAGR as electric-vehicle interiors need light, flame-retardant skins that meet UL 94 V-0 without halogens. Medical devices use biocompatible polyether grades to satisfy ISO 10993 and FDA 510(k) pathways, anchoring suppliers through long validation cycles.

Electronics leverages TPU in cable jacketing and smartphone frames due to dielectric strength above 20 kV/mm. Construction uses TPU membranes in bridge joints where freeze-thaw cycling is severe. Heavy engineering segments value abrasion loss under 100 mg per 1,000 cycles, accessible only with high molecular-weight polyester TPU. Automotive brand programs report 1.2 kg interior mass reduction per vehicle when replacing PVC skins with TPU, improving range in battery-electric models.

Geography Analysis

Asia-Pacific represented 58.72 % of 2025 revenue and is projected to post a 7.75% CAGR to 2031. China localizes medical-grade resin, with Wanhua, Shandong INOV, and Miracll operating integrated complexes near footwear and automotive clusters. India’s Production-Linked Incentive offers 15 % capital subsidy for footwear resin investments, yet local capacity remains thin, forcing imports that lift landed cost by 18 %. Japan and South Korea focus on low-VOC waterborne dispersions for premium interiors, while ASEAN countries supply labor-intensive footwear assembly but lack sizable compounding assets.

North America’s market share is buoyed by USMCA rules boosting Mexican Tier-1 automotive suppliers. FDA clearances for 14 TPU-based medical devices in 2025 sustain polyether uptake. Canadian low-slope roofing membranes use TPU for thermal cycling below -40°C. In Europe, compliance with REACH diisocyanate training consolidates volumes among BASF, Covestro, and Huntsman. Germany specifies bio-based TPU for EV interiors, while Nordic arenas adopt translucent TPU membranes for 50-meter column-free spans.

In South America, and Middle East & Africa, Brazil’s footwear exports grow, yet domestic resin output is inadequate, mandating Asian imports. Saudi Arabia’s USD 500 billion infrastructure pipeline pulls TPU membranes for stadium roofs where daytime highs top 50°C. BASF’s Abu Dhabi plant at 25 kt begins regional supply in 2024, serving Gulf Cooperation Council construction and automotive demand.

Competitive Landscape

The Thermoplastic Polyurethane (TPU) market is moderately concentrated. BASF and Covestro leverage captive 1,4-BDO, while Lubrizol and Huntsman specialize in medical and automotive grades with intensive regulatory support. Wanhua’s Yantai complex blends integrated MDI and BDO at a cash cost of near USD 2.80 kg. White-space opportunity lies in conductive grades for flexible electronics and in powder-bed fusion feedstocks. Several start-ups focus on enzymatic recycling, which may unlock closed-loop TPU within the decade.

Thermoplastic Polyurethane (TPU) Industry Leaders

The Lubrizol Corporation

Covestro AG

Huntsman International LLC

Wanhua Chemical Group Co. Ltd

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Covestro inaugurated a new thermoplastic polyurethane (TPU) production facility in Zhuhai, located in South China. Starting with an annual production capacity of 30,000 tons, the facility is projected to ramp up its output to 120,000 tons annually by the 2030s, positioning it as Covestro's largest TPU production site worldwide.

- February 2025: Lubrizol Corporation launched a new ESTANE TPU production line in Shanghai and released a white paper on growth in the Car Paint Protection Film (PPF) industry, reinforcing its commitment to innovation and meeting rising demand for high-quality PPF products.

Global Thermoplastic Polyurethane (TPU) Market Report Scope

Thermoplastic polyurethane (TPU) is a complete thermoplastic elastomer. As with other thermoplastic elastomers, TPU is elastic and can be melted. It can also be processed on extrusion, injection, blast, and compression molding machines. It can be vacuum-formed or solution-coated and is well-suited to various manufacturing methods.

The thermoplastic polyurethane (TPU) market is segmented by product type, application, end-use industry, and geography. By product type, the market is segmented into Polyester TPU, Polyether TPU, and Polycaprolactone TPU. By application, the market is segmented into extruded products, injection molded products, adhesives, and other applications. By end-use industry, the market is segmented into construction, automotive, footwear, medical, electrical and electronics, heavy engineering, and other industries. The report also covers the size and forecasts for the thermoplastic polyurethane market in 18 countries across major regions. Each segment's market sizing and forecasts are based on revenue (USD).

| Polyester TPU |

| Polyether TPU |

| Polycaprolactone TPU |

| Extruded Products |

| Injection Molded Products |

| Adhesives |

| Other Applications |

| Footwear |

| Automotive |

| Medical |

| Electrical & Electronics |

| Construction |

| Heavy Engineering |

| Other End-user Industries |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Polyester TPU | |

| Polyether TPU | ||

| Polycaprolactone TPU | ||

| By Application | Extruded Products | |

| Injection Molded Products | ||

| Adhesives | ||

| Other Applications | ||

| By End-Use Industry | Footwear | |

| Automotive | ||

| Medical | ||

| Electrical & Electronics | ||

| Construction | ||

| Heavy Engineering | ||

| Other End-user Industries | ||

| By Geography | Asia Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for Thermoplastic Polyurethane (TPU) through 2031?

A compound annual growth rate of 6.89% is forecast from 2026 to 2031, taking revenue to USD 4.52 billion.

Which region leads TPU demand today?

Asia-Pacific held 58.72 % of 2025 revenue and is growing the fastest due to China’s integrated supply chains and India’s footwear incentives.

Which end-use is expected to grow quicker than footwear?

Automotive interiors are forecast to expand at 8.07% CAGR, outpacing footwear as electric-vehicle makers shift to light, flame-retardant trims.

Why is 1,4-BDO volatility a key restraint?

BDO swings of USD 600 t squeeze non-integrated producers because it represents up to 30 % of polyester TPU raw-material cost.

How are regulations shaping TPU grades?

REACH diisocyanate limits and cabin VOC caps push suppliers toward solvent-free reactive and bio-based formulations that cut emissions and meet worker-safety rules.

Page last updated on: