Chemicals & Materials

2nd JuneUnlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

The Micro Perforated Films Market Report is Segmented by Material Type (Polypropylene, Polyethylene Terephthalate, and More), Perforation Method (Mechanical Needle Perforation, Laser Micro-Perforation, and More), Application (Fruits and Vegetables, Bakery and Confectionery, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

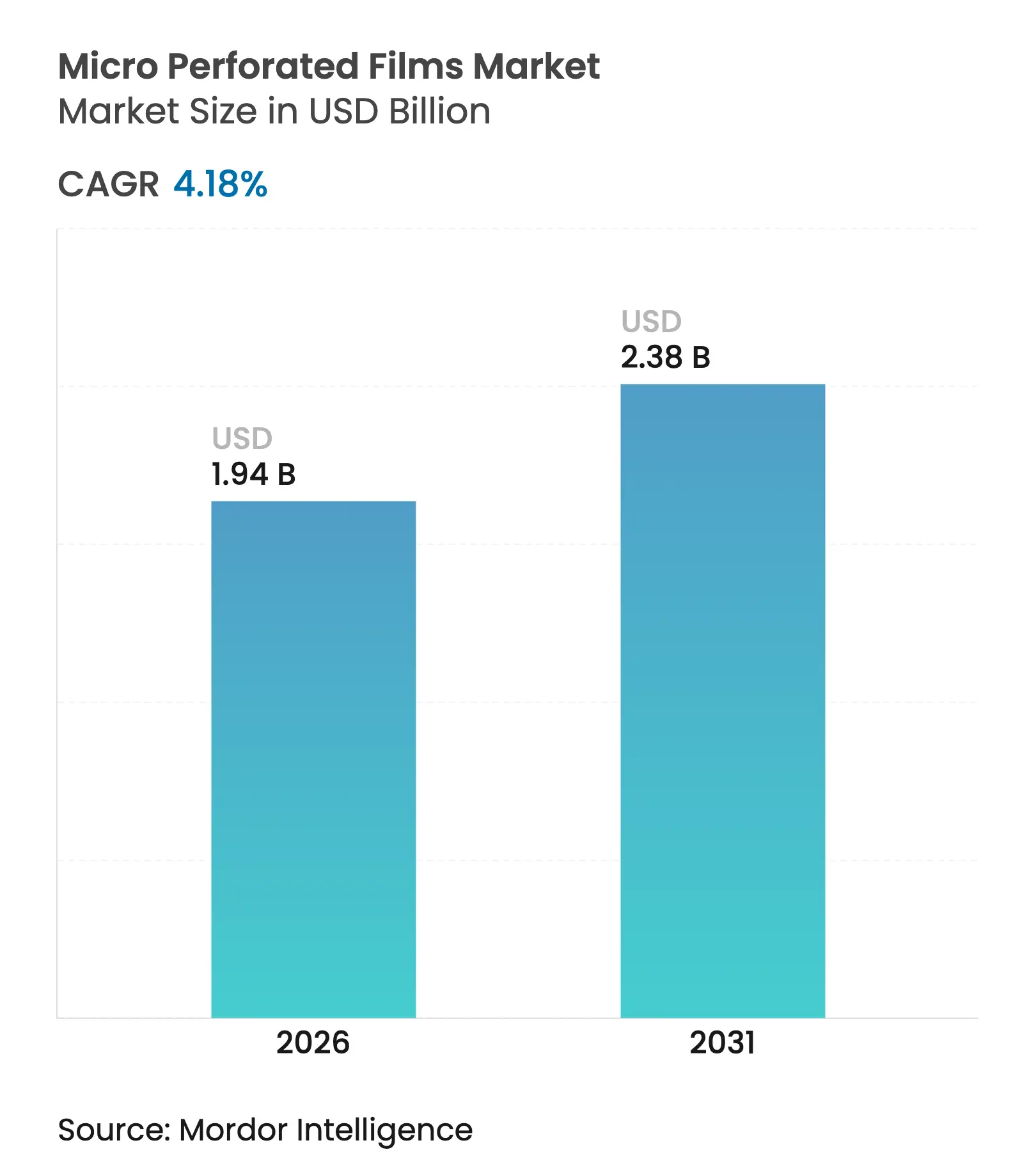

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.38 Billion |

| Growth Rate (2026 - 2031) | 4.18 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Micro Perforated Films market size in 2026 is estimated at USD 1.94 billion, growing from 2025 value of USD 1.86 billion with 2031 projections showing USD 2.38 billion, growing at 4.18% CAGR over 2026-2031. Rising demand for precision-engineered films that balance gas exchange with moisture retention keeps growth steady even as overall volume expansion moderates. Retail consolidation, e-commerce grocery adoption, and stringent shelf-life requirements intensify interest in laser micro-perforated solutions that extend freshness by 2-4 days for highly perishable items. Polypropylene (PP) retains leadership because it combines clarity, strength, and cost-effectiveness, yet polyethylene terephthalate (PET) gains traction on recyclability and higher barrier strength. Asia-Pacific remains the pivotal production and consumption center, bolstered by cold-chain investment and middle-class demand. Meanwhile, regulatory moves to curb PFAS in food contact materials and episodic shortages of specialty perforation needles nudge converters toward contamination-free laser technology.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Longer shelf-life fresh produce packaging

Longer shelf-life fresh produce packaging

| +1.2% | Global, APAC & North America | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, APAC & North America

|

Impact Timeline

:

Medium term (2-4 years)

|

Organised retail and e-commerce cold chains

Organised retail and e-commerce cold chains

| +0.8% | APAC core; spill-over Europe & North America | Long term (≥ 4 years) | |||

Shift to laser perforation

Shift to laser perforation

| +0.7% | Europe & North America first; APAC catching up | Short term (≤ 2 years) | |||

PP adoption in flexible packaging

PP adoption in flexible packaging

| +0.6% | Global, strongest in APAC | Medium term (2-4 years) | |||

Salad meal-kit uptake

Salad meal-kit uptake

| +0.5% | North America & Europe, rising in urban APAC | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Longer-Shelf-Life Fresh Produce Packaging

Retailers require packaging that keeps leafy greens, berries, and high-respiration produce marketable for multiple extra days. Micro perforated films maintain carbon dioxide at 3-5% and oxygen at 16-18% inside packs, lowering respiration and moisture loss. Shelf life gains of 4-8 days have cut waste costs by up to 25% for leading grocers. Precision perforation therefore translates into reduced shrinkage and broader delivery zones for produce suppliers. Brands see marketing advantages in fresher visual appearance, and converters able to customize hole density by crop type secure repeat contracts.

Expansion of Organised Retail and E-Commerce Cold Chains

Emerging markets build chilled warehouses and automated sortation hubs that expose produce to varied temperatures during transfers. Micro perforated films tailored for 0 °C to 10 °C prevent excess condensation and retain firmness across 24- to 48-hour shipment cycles. Meal-kit operators now specify films with integrated temperature dots and QR-based condition tracking. Consequently, cold-chain growth lifts film demand not only by volume but also by technical complexity, supporting premium pricing.

Shift from Needle to Laser Micro-Perforation for Uniform Gas Transmission

Laser systems generate holes with ±5 µm tolerance and avoid physical contact, eliminating metal shavings and microbial transfer risks. Changeovers occur via software settings rather than needle swaps, lifting uptime. Acoustic sensors embedded in the laser head verify penetration depth, a safeguard that has become critical for customers audited under Hazard Analysis and Critical Control Points (HACCP) regimes. Capital outlays prove defensible because labor and consumable savings plus quality gains recoup investments within two years for high-volume plants.

Growing Adoption of Polypropylene Films in Flexible Packaging

PP’s mechanical strength, clarity, and cost advantage cement its role, but sustainability expectations push development of bio-circular PP derived from used cooking oil that matches conventional grade performance. BOPP variants incorporating 30% post-consumer recycled resin still meet optical and barrier targets, helping brand owners hit recycled-content pledges[1]“Recycled Content BOPP Film Grades,” EUROPLAS.COM . PP’s easy machinability on both needle and laser lines gives converters operational flexibility when supply or regulations shift.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Contamination risk in conventional lines

Contamination risk in conventional lines

| -0.4% | Global, food-grade focus | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.4%

|

Geographic Relevance

:

Global, food-grade focus

|

Impact Timeline

:

Short term (≤ 2 years)

|

PFAS regulation limiting fluoropolymer laser masks

PFAS regulation limiting fluoropolymer laser masks

| -0.3% | Europe & North America, globalizing | Medium term (2-4 years) | |||

Tight supply of specialty stainless micro-punch needles

Tight supply of specialty stainless micro-punch needles

| -0.2% | Global, acute in APAC | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Contamination Risk in Conventional Lines

Needle tips contact film at speeds topping 300 strokes per minute, creating burrs and metal dust that threaten food safety. Plants must halt production for sanitizing breaks, pushing up downtime and cleaning chemical costs. Regulatory audits highlight perforation as a critical control point, leading some converters to cap run speeds, which limits capacity during seasonal demand spikes.

Emerging PFAS Regulation Limiting Fluoropolymer Laser Masks

The European Union’s 2026 deadline caps total PFAS at 25 ppb, disqualifying popular fluoropolymer masks that resist laser heat yet may leach trace compounds[2]“PFAS Regulatory Limits in Food Packaging,” TENTAMUS.COM . Substitutes such as ceramic composites deliver lower life cycles and reduced hole uniformity, meaning early adopters face recalibrations. Equipment original-equipment-manufacturers accelerate R&D yet still face bridge periods where clients must validate new mask materials under strict migration tests.

By Material Type: Polypropylene Leadership Meets Polyethylene Terephthalate Momentum

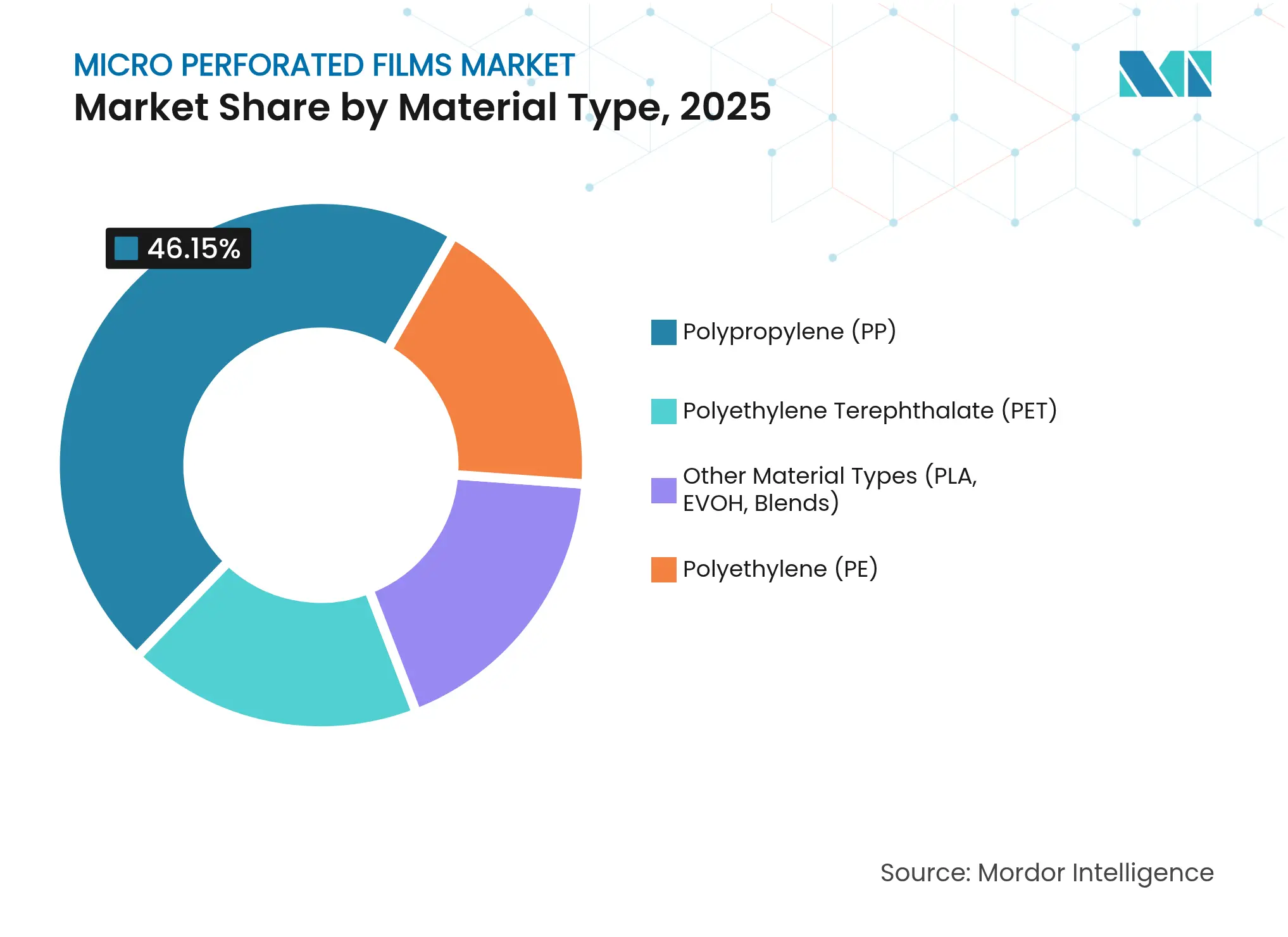

Polypropylene possessed the largest stake at 46.15% of the micro perforated films market in 2025 thanks to its balanced cost, strength, and water-vapor barrier. BOPP grades allow converters to hit tight hole sizes without film tearing. Bio-circular PP derived from used cooking oil now offers identical machinability while trimming carbon footprints.

PET ranks as the fastest riser at a 5.43% CAGR. Its higher oxygen barrier and clarity suit premium salad, berry, and medical packs that require visual checks. Recyclability in established PET bottle streams strengthens positioning in regions with extended producer responsibility rules. The micro perforated films market size for PET therefore expands faster than overall demand, especially in Europe where retailers prefer mono-polymer recyclability schemes. HDPE and LDPE stay relevant in colder-chain bakery wraps due to flexibility under sub-zero temperatures, though growth stabilizes. Emerging PLA and EVOH co-extrusions meet niche calls for biodegradability or extreme aroma protection but still represent single-digit shares.

Note: Segment shares of all individual segments available upon report purchase

By Perforation Method: Laser Gains on Mechanical Dominion

Needle perforation still commands 64.50% of 2025 revenue because legacy lines remain fully depreciated and can hit high web speeds. Yet downtime for needle swaps and cleaning continues to weigh on throughput. The micro perforated films market size attributed to laser solutions grows quickly as brands tighten tolerance standards.

Laser’s 5.52% CAGR rests on contactless processing, immediate hole pattern changes, and elimination of consumables. Nd:YAG and CO₂ heads process PP, PET, and recyclable PE alike, offering multi-material flexibility. Acoustic feedback loops detect incomplete penetration, preventing pinholes that could accelerate spoilage. Hot-pin and electrostatic techniques serve small niches where irregular hole geometry is demanded, but neither technology shows breakout potential.

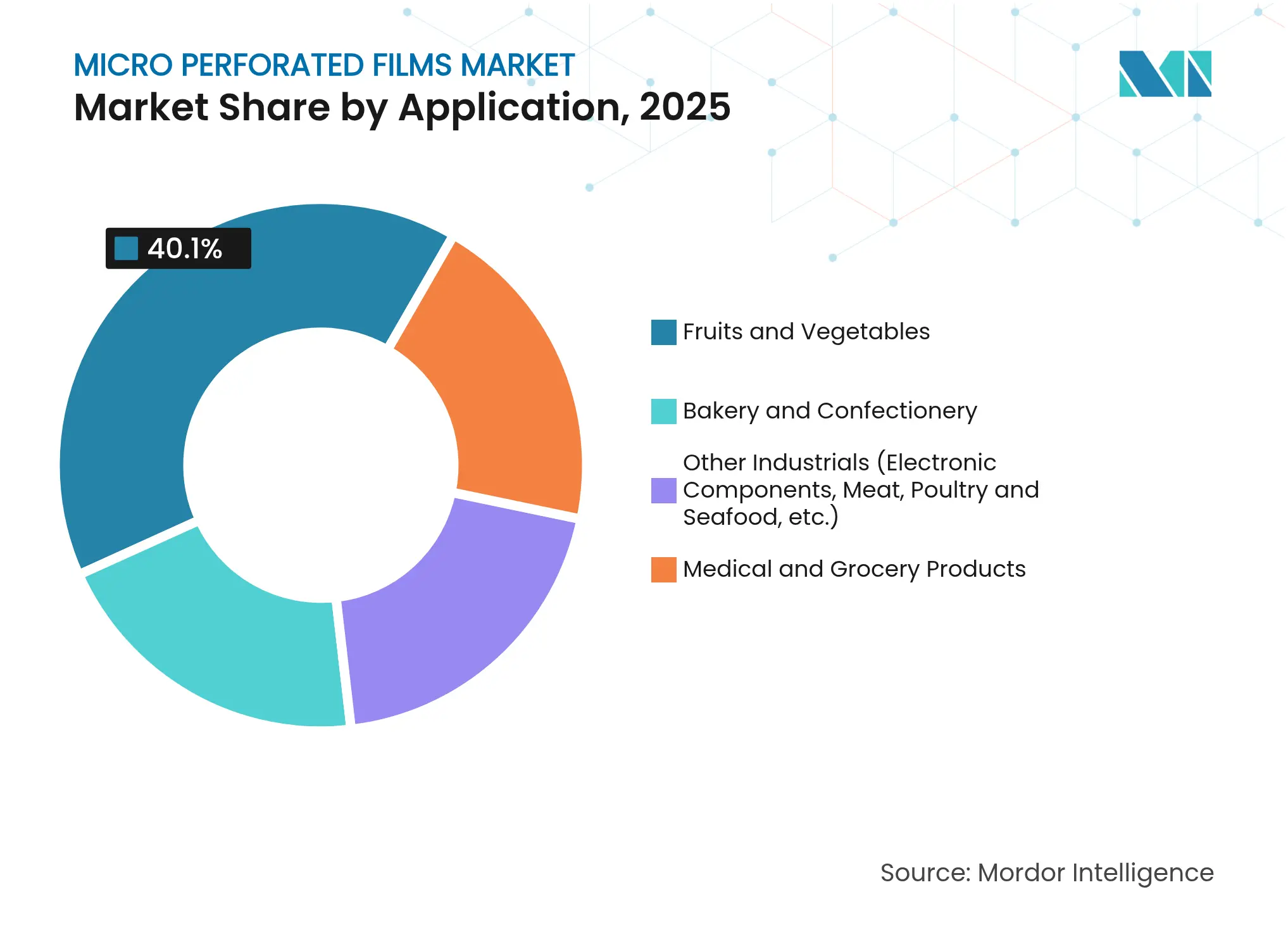

By Application: Produce Packaging Dominates, Diversification Emerges

Fresh fruits and vegetables accounted for 40.10% of 2025 value because respiration-sensitive crops like berries, grapes, and leafy greens cannot tolerate generic films. Converters supply crop-specific patterns that balance CO₂ buildup with dehydration control, winning multi-year supply contracts with retailers. Bakery snacks leverage smaller hole arrays that vent moisture without drying contents, retaining softness past shelf-date targets.

Medical packaging sees rising interest as sterilizable PET films with micro vents allow ethylene-oxide outgassing while blocking particulate ingress. Electronics pouches now specify micro perforated films to manage humidity and static charge simultaneously. The micro perforated films market share associated with these industrial uses remains modest yet posts a 5.74% CAGR as suppliers demonstrate case studies.

Note: Segment shares of all individual segments available upon report purchase

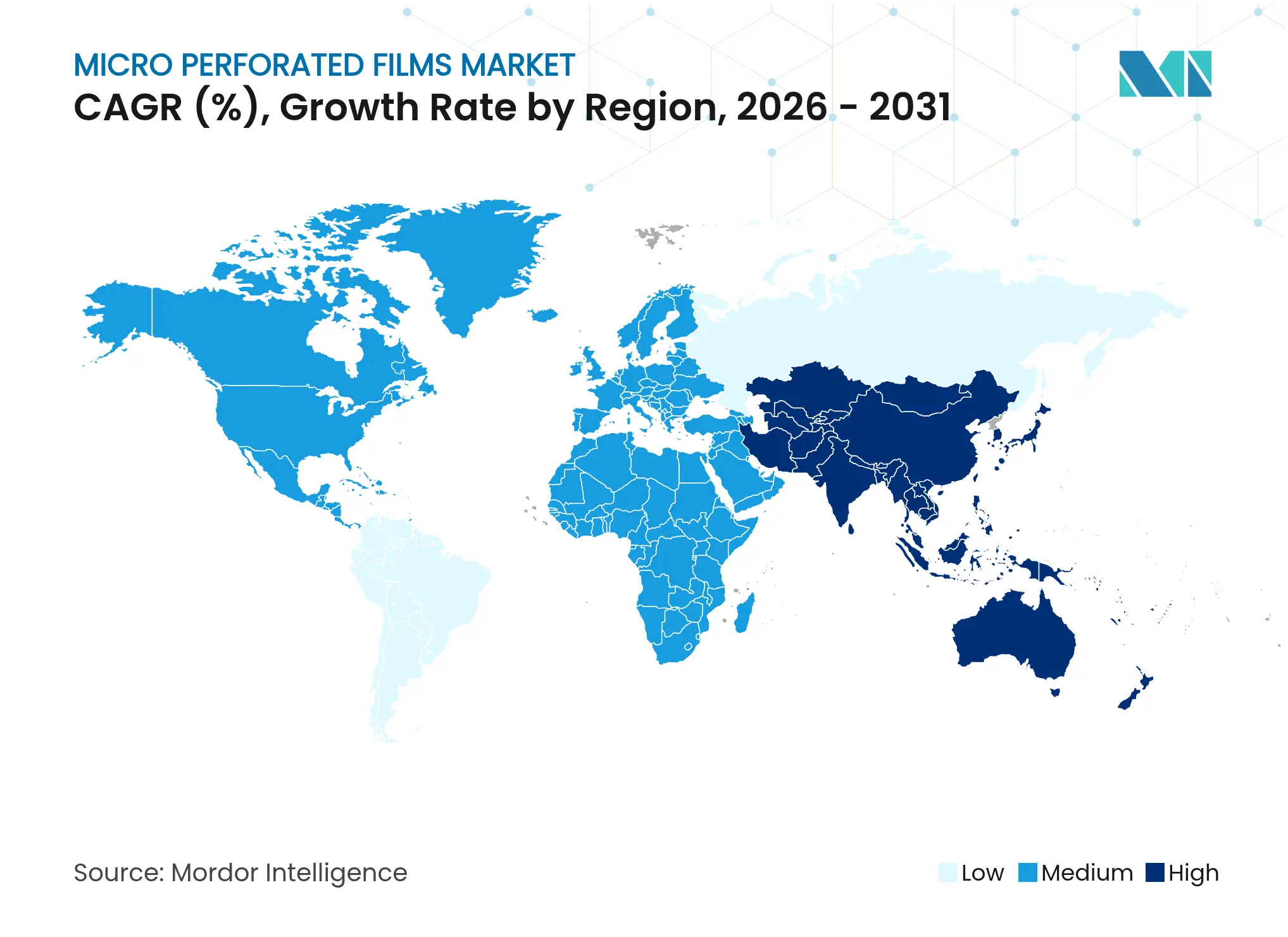

Asia-Pacific captured 44.30% of global 2025 revenue, reflecting both manufacturing cost advantage and swelling consumption of chilled fresh foods. China spent more than USD 20 billion on cold-chain nodes since 2024, broadening the addressable base for advanced produce packaging. Regional converters integrate high-speed laser arrays to serve domestic grocers and cross-border fruit exporters. India’s double-digit e-commerce grocery growth forces suppliers to meet 24-hour delivery windows despite tropical heat, spurring adoption of breathable film formats.

North America holds a solid second position. The United States leads technology uptake, with major salad processors retrofitting plants for laser micro-perforation to comply with Food Safety Modernization Act verification audits. Canadian berry exporters adopt PP-PET laminate structures in response to longer rail corridors that demand eight-day firmness retention. Latin produce sourced from Mexico now arrives fresher in northern retail thanks to optimized micro-vent packs. Europe emphasizes regulatory compliance and circularity. Retail chains require mono-material solutions compatible with deposit-return lines, favoring PET and PP films with 30% recycled content. Early enforcement of PFAS bans triggers faster pivot to ceramic laser masks, prompting European packers to partner closely with equipment suppliers on validation protocols. South America, the Middle East, and Africa collectively contribute smaller shares but exhibit catch-up potential. Brazil’s mango and grape exporters test micro perforated packs that minimize condensation during trans-Atlantic voyages. Gulf States supermarkets pilot salad bowls sealed with laser-vented lids to handle 35 °C logistics. African citrus exporters begin to trial breathable liners for sea shipments, aiming to slash waste rates that previously exceeded 15%.

Market Concentration

The Micro Perforated Films Market exhibits moderate fragmentation. Amcor’s 2025 introduction of AI-guided perforation monitors cut defect rates for citrus liners presented at IPPE. Sealed Air rolls out predictive maintenance software that alerts operators when laser optics drift out of calibration, trimming unscheduled downtime.

Mid-tier challengers specialize in laser retrofits, offering speed-boost modules that bolt on to older mechanical lines and lift output by 15%. These niche vendors win business where converters hesitate to scrap depreciated assets yet still need tighter tolerances. Asian converters leverage regional raw-material cost positions to bid aggressively on supermarket contracts, though lack of in-house R&D limits differentiation.

Regulatory trends create windows for disruptors. Firms that commercialize PFAS-free laser masks ahead of the 2026 European deadline could secure technology licensing royalties. Suppliers of bio-circular PP pellets forge alliance models with converters eager to advertise low-carbon footprints on produce labels. Meanwhile, ongoing tightness in needle steel triggers collaborative purchasing clubs among smaller converters aiming to secure allocation.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The Micro Perforated Films market report includes:

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.