Polymer Nanocomposite Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

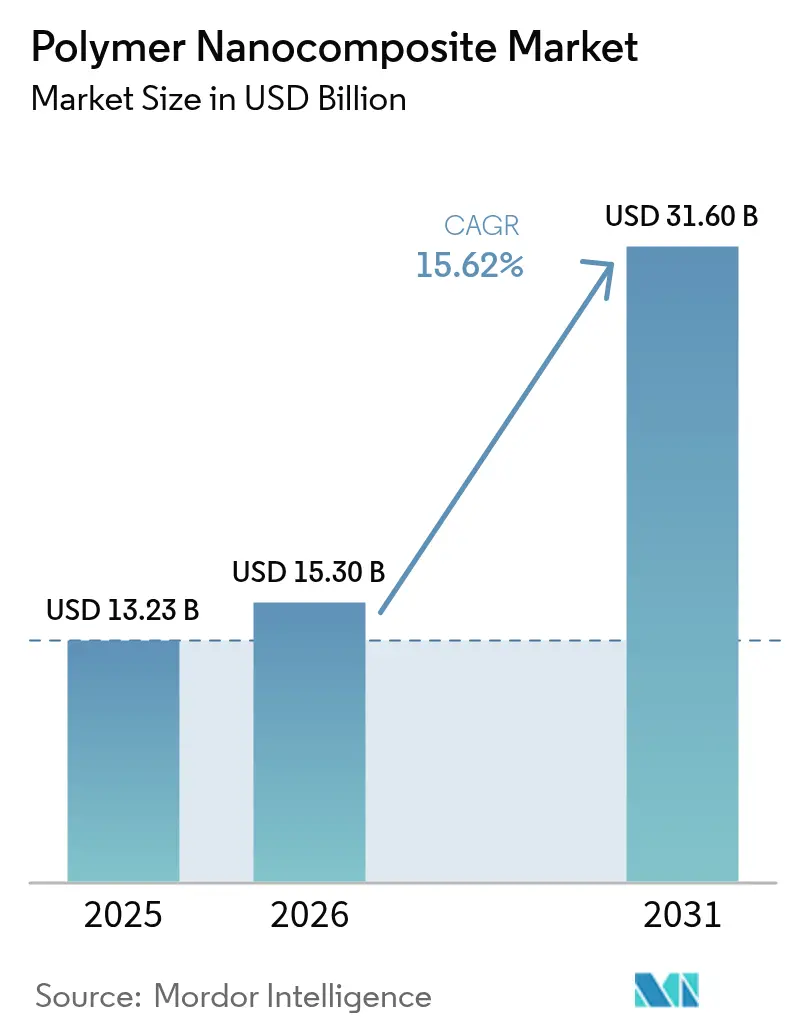

| Market Size (2026) | USD 15.3 Billion |

| Market Size (2031) | USD 31.6 Billion |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polymer Nanocomposite Market Analysis by Mordor Intelligence

The Polymer Nanocomposite Market size in 2026 is estimated at USD 15.3 billion, growing from 2025 value of USD 13.23 billion with 2031 projections showing USD 31.6 billion, growing at 15.62% CAGR over 2026-2031. Demand accelerates as nanoscale fillers unlock simultaneous gains in strength, thermal conductivity, and barrier performance, making the material central to lightweight electric-vehicle parts, high-density electronics, and next-generation packaging. Automotive programs anchor near-term volumes, while fast-moving 5G infrastructure and halogen-free flame-retardant regulations broaden the customer base. Cost-down progress in graphene and carbon-nanotube production improves economics, and regional supply chains in Asia-Pacific shorten lead times, sustaining momentum. Investments in recycling-friendly thermoplastic matrices further position the polymer nanocomposites market as a preferred solution for circular-economy goals.

Key Report Takeaways

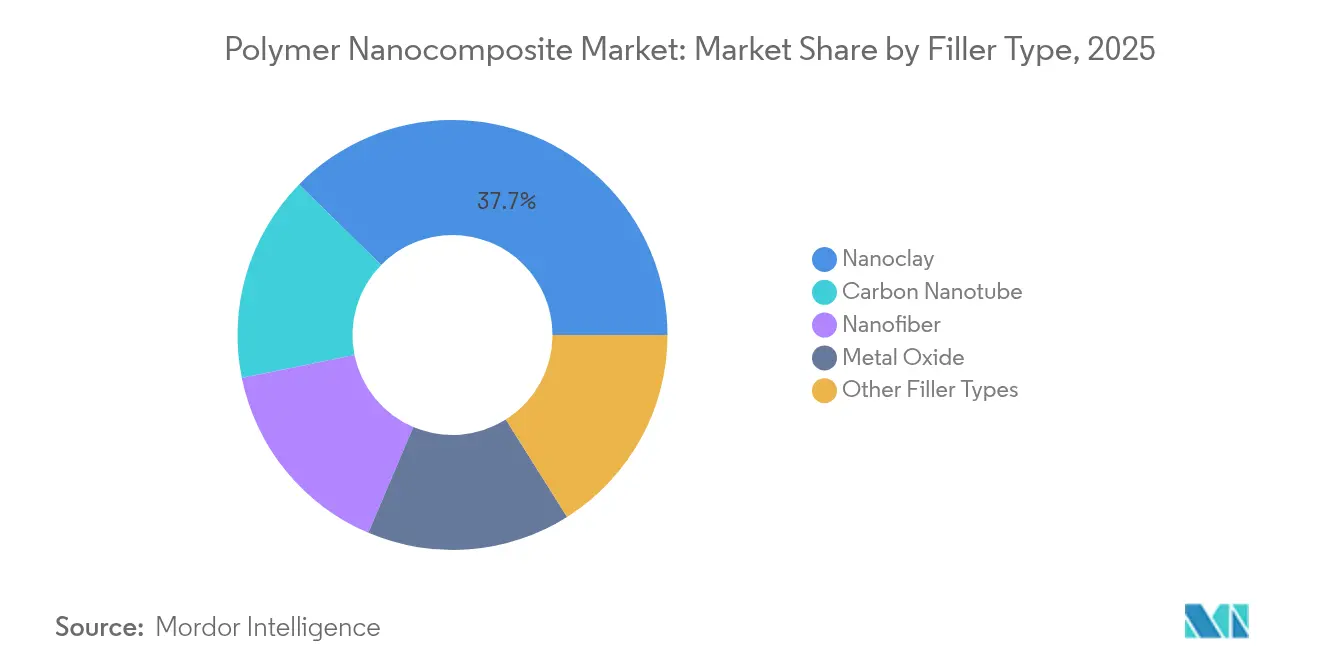

- By filler type, nanoclay led with 37.65% revenue share in 2025; the “other filler types” category, driven by graphene and nanodiamond, grows fastest at 18.72% CAGR to 2031.

- By polymer matrix, thermoplastics captured 53.74% share of the polymer nanocomposites market size in 2025, while thermosets posted the highest 17.63% CAGR to 2031.

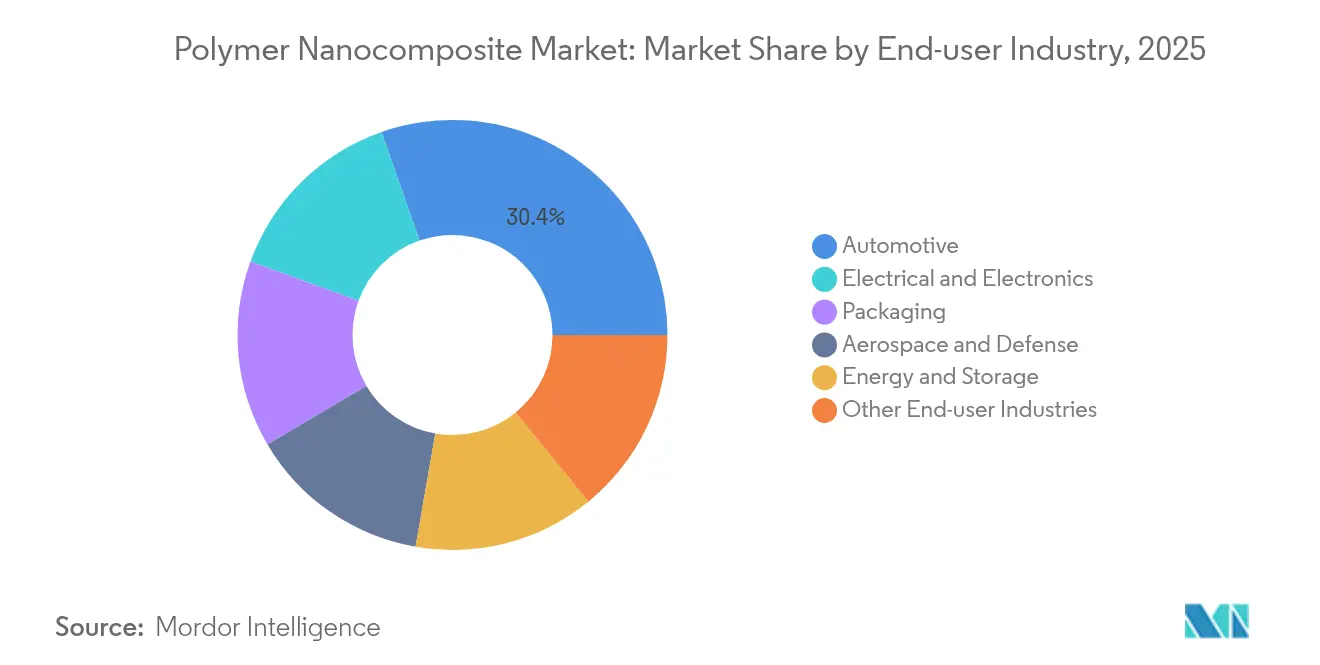

- By end-user industry, automotive commanded 30.35% of the polymer nanocomposites market share in 2025 and is expanding at a 17.21% CAGR through 2031.

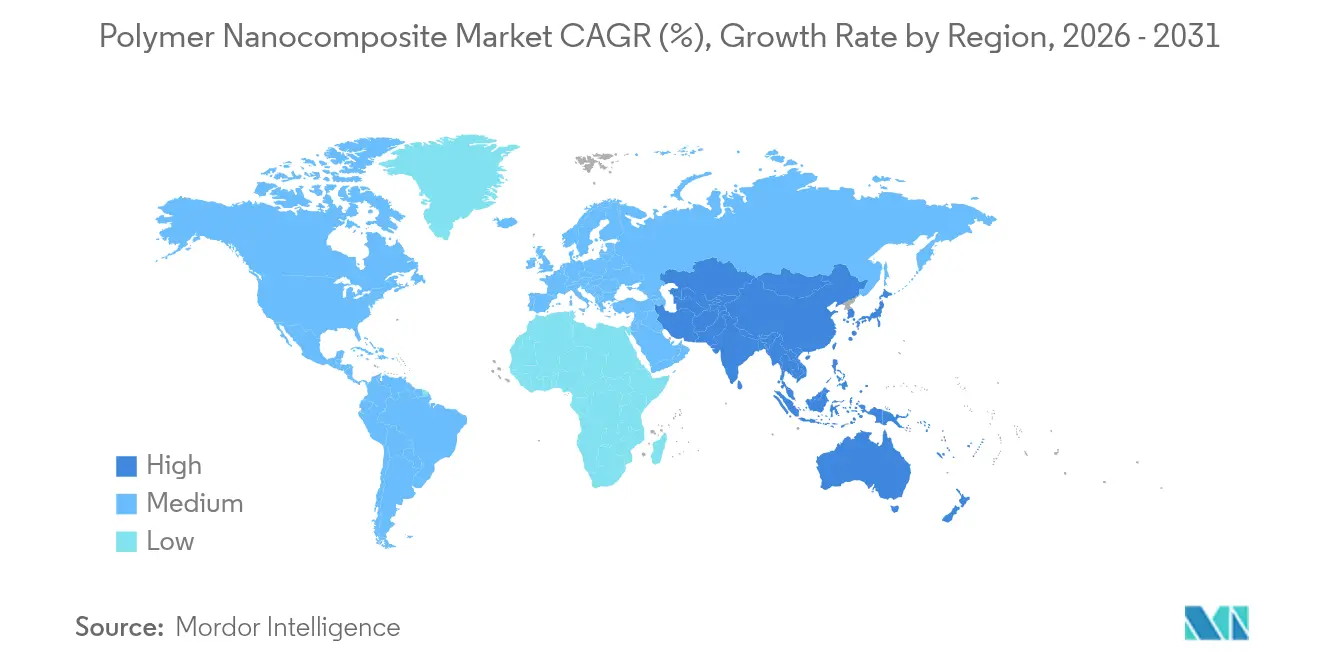

- By geography, Asia-Pacific accounted for 39.92% of the polymer nanocomposites market in 2025 and records an 18.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polymer Nanocomposite Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-barrier packaging in food and pharma | 3.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Lightweighting targets in automotive and mobility composites | 2.8% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) |

| Thermal management needs in 5G and power electronics | 1.9% | Global, early adoption in APAC and North America | Short term (≤ 2 years) |

| Regulatory push for flame-retardant, halogen-free materials | 1.6% | EU and North America, expanding to APAC | Medium term (2-4 years) |

| Battery-housing materials for electric vehicles | 1.2% | Global, with early gains in China, Germany, California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Barrier Packaging in Food and Pharma

Polymer nanocomposites lower oxygen transmission below 0.1 cc/m²/day, matching multilayer laminates while cutting film thickness by up to 40%. Antimicrobial metal-oxide nanoparticles extend shelf life, so food processors shift from chemical preservatives to active-packaging formats[1]Walaa M. Abd El-Gawad, “Utilization of Affordable Nanocomposites with Outstanding Antimicrobial Activity in Waterborne Coatings,” Sci Rep, doi.org. Moisture-sensitive pharmaceuticals also benefit, allowing single-layer blister designs that simplify recycling. FDA guidance on nanomaterial risk assessment shortens approval cycles, and line integration eliminates lamination steps, improving throughput and waste ratios.

Lightweighting Targets in Automotive and Mobility Composites

Carbon-fiber-reinforced thermoplastic nanocomposites yield 40% mass savings versus steel and support automated fiber-placement lines, aligning with high-volume e-mobility programs. Recyclability boosts total-life economics, meeting circular mandates. Beyond mass reduction, nanoscale fillers enhance crash energy absorption and damp NVH, enabling thin-wall designs. European OEMs plan 20–25% weight cuts by 2030, catalyzing resin and reinforcement investment.

Thermal Management Needs in 5G and Power Electronics

Graphene-loaded polymer nanocomposites surpass 10 W/mK thermal conductivity while remaining electrically insulating, replacing aluminum heat sinks in space-constrained base stations. Printable grades allow lattice geometries that direct heat away from chip hotspots. Telco densification and AI inference at the edge accelerate adoption, shifting thermal design from passive to integrated material solutions.

Regulatory Push for Flame-Retardant, Halogen-Free Materials

REACH restrictions on brominated compounds spur uptake of nanoscale phosphorus and metal-hydroxide systems that cut additive loading 40–60% yet meet UL-94 V-0. Layered-double-hydroxide dispersions form heat-shield barriers, preserving polymer toughness. Construction panels and rail interiors lead early demand, and suppliers leverage compliance credentials as tender prerequisites.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High compounding and dispersion costs | 2.1% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Nanotoxicity/EHS compliance uncertainty | 1.4% | EU and North America, expanding globally | Medium term (2-4 years) |

| Scale-up challenges for graphene and CNT supply | 1.8% | Global, with acute impact in APAC manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Compounding and Dispersion Costs

Uniform distribution of high-aspect-ratio fillers demands twin-screw extruders with intensified shear, adding 200–400% to processing cost versus standard polymers. Functionalization to curb nanotube agglomeration introduces extra steps and licensing fees[2]European Commission, “REACH Regulations for Nanomaterials and Microparticles,” ec.europa.eu . Dry-powder and masterbatch routes lower capex but widen supply-chain complexity. Cost pressure limits penetration into price-sensitive packaging and consumer goods until scale economies materialize.

Nanotoxicity/EHS Compliance Uncertainty

Divergent global test protocols leave producers navigating multiple dossiers for identical materials. EU REACH data packages for carbon nanotubes often exceed USD 1 million, stalling SME participation. Food-contact and medical-device segments delay launches pending harmonized guidance. Industry consortia now co-fund toxicology libraries, yet regulatory alignment remains years away, tempering near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filler Type: Nanoclay Stability, Graphene Upside

Nanoclay held 37.65% polymer nanocomposites market share in 2025 on the strength of low cost and established film-extrusion know-how. Barrier gains allow 5–7 µm downgauging in snack packaging without compromising shelf life. Carbon nanotubes occupy premium niches where 10^3 S/m conductivity offsets price, while metal-oxide fillers address UV, antimicrobial, and flame-retardant needs. The other-filler category captures 18.72% CAGR as scalable graphene and nanodiamond grades unlock EMI shielding and thermal paths. Combined, these trends suggest widening formulation diversity rather than one-filler dominanc.

By Polymer Matrix: Thermoplastics Dominate, Thermosets Accelerate

Thermoplastics commanded 53.74% of the polymer nanocomposites market in 2025, thanks to re-melt capability and alignment with injection-molding infrastructure. Polypropylene nanocomposites cut bumper beam mass by 18% while meeting pedestrian impact norms. In contrast, thermosets chart an 17.63% CAGR on aerospace, wind-blade, and high-temperature electronics demand. Epoxy systems infused with nano-silica extend glass-transition temperature above 200 °C, meeting aircraft secondary-structure specs. Bio-based matrices emerge as a niche, coupling cellulose nanofibers with PLA to address compostability mandates.

By End-user Industry: Automotive Leads Dual-Role Growth

Automotive accounted for 30.35% of the polymer nanocomposites market size in 2025 and retains the fastest 17.21% CAGR through 2031 as battery housings, under-body shields, and CFRT structures proliferate. Packaging retains volume stability, driven by oxygen-sensitive snacks and pharma blister films. Aerospace specifies nanocomposites for lightning-strike protection, while electronics accelerate uptake through 5G antenna modules requiring thermal and EMI performance in one part. Energy-storage applications expand with solid-state electrolytes and super-capacitor films.

Geography Analysis

Asia-Pacific’s 39.92% polymer nanocomposites market share in 2025 mirrors deep manufacturing ecosystems and proactive state programs. China’s scale in graphene nanotube production compresses cost curves, while India’s additive-manufacturing roadmap targets a 5% global stake, stimulating downstream demand. Japan funds cellulose nanofiber pilots that blend sustainability with high modulus, drawing appliance and auto tier-ones.

North America leverages automotive lightweighting legislation and aerospace certification pipelines. The USMCA trade framework eases cross-border supply of compounded pellets, aiding vehicle platforms assembled in Mexico yet sold in the United States. Europe couples stringent EHS rules with circular-economy targets, accelerating halogen-free nanocomposite adoption in building panels and rail interiors. The Middle East and Africa open pockets of demand through green-building codes and petrochemical diversification, while South America’s progress hinges on Brazilian packaging converters and nascent EV component lines. Collectively, regional differentiation ensures balanced expansion for the polymer nanocomposites market over the forecast horizon.

Regulatory Landscape

Polymer nanocomposites operate under chemical safety and product compliance regimes that increasingly treat nanoforms as distinct, data-intensive substances. In the European Union, REACH introduced explicit nanoform information requirements effective January 2020 (via nano-related REACH annex updates), and ECHA supports implementation through its Nanomaterials Expert Group, alongside CLP classification and labeling obligations for hazardous nano-enabled additives.

Recent policy upgrades also create additional compliance touchpoints for suppliers of nanofillers and nano-additives used in polymer matrices. Regulation (EU) 2025/2455, adopted in November 2025, established a common data platform on chemicals to improve data accessibility and monitoring. Commission Recommendation (EU) 2026/510 in March 2026 advances the Safe and Sustainable by Design (SSbD) assessment framework for chemicals and materials, increasing the emphasis on lifecycle documentation and safer-by-design formulation choices, including tighter evidence trails from nanomaterial producers through compounders to downstream OEMs.

Value Chain Analysis

The value chain begins with upstream producers of nano-scale fillers and additives, including nanoclays, metal oxides, carbon nanotubes, graphene, and other emerging fillers, alongside base polymer matrices such as thermoplastics, thermosets, and niche bio-based polymers. Formulation and dispersion are typically handled by specialty compounders and integrated chemical producers using high-shear mixing and twin-screw compounding, with masterbatch and pellet distribution to converters and OEM supply chains serving automotive, electronics, packaging, aerospace, and energy-storage applications.

Midstream processing is where most of the cost and performance constraints concentrate. Achieving uniform dispersion and repeatable properties with high-aspect-ratio fillers increases compounding complexity and can add 200-400% to processing cost versus standard polymers. EHS dossier work for some nanoforms can also exceed USD 1 million in the EU under REACH. These constraints raise the importance of application labs, digital process controls including inline monitoring, and co-development programs between material suppliers and tier-one OEMs to shorten qualification cycles and reduce scrap and variability during scale-up.

Competitive Landscape

The polymer nanocomposites market shows moderate fragmentation. BASF, Dow, and DuPont exploit integrated monomer-to-compound chains, offering application labs that shorten design cycles. Merger and acquisition activity intensifies as polymer majors buy nanomaterial startups to access patent estates and pilot lines; Birla Carbon’s purchase of Nanocyl illustrates this convergence trend. Partnerships between material suppliers and OEMs proliferate. For instance, Haydale pairs with printed-electronics researchers to formulate graphene-ink for low-loss 5G antennas, demonstrating co-development as a go-to-market route. Digital twins and inline Raman monitoring improve batch-to-batch consistency, a key hurdle when scaling nano-dispersions.

Polymer Nanocomposite Industry Leaders

Evonik Industries AG

Arkema

BASF

Dow

SABIC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One near-term white-space is high-barrier packaging that improves recyclability by reducing reliance on multilayer structures. Nanocomposite films already target oxygen transmission below 0.1 cc/m2/day while supporting material reduction, with up to 40% thinner films cited in the market context. Supplier activity continues to broaden converter-ready options, including in June 2026 when NanoXplore and Techmer PM launched GrapheneBlack xGnP masterbatch for high-performance plastic films, focused on thickness reduction and mechanical-strength gains to support downgauging without reverting to complex laminates.

Thermal and electrical performance needs in electrification and 5G electronics create a second pull-through path for polymer nanocomposites that combine lightweighting with thermal management and flame-retardant compliance. Activity is shifting beyond filler supply toward system solutions such as advanced binders, curing agents, and engineering polymers tuned for fast processing and reliability in demanding parts, which in turn increases demand for compounding know-how and qualification support across Asia-Pacific, North America, and Europe. Regulatory and customer scrutiny on nanoform data and safer material design, including REACH nanoform requirements and the EU SSbD framework work in 2026, supports opportunities for suppliers that can provide traceable datasets, validated dispersion routes, and circularity-compatible thermoplastic formulations.

Recent Industry Developments

- June 2026: BASF introduced Oppanol N PLUS, a polyisobutene-based high-performance binder engineered to improve stability and lifetime of electric-vehicle battery cathodes and anodes. The launch expands the addressable space for polymer-based functional materials in battery components, complementing nanocomposite adoption where binders, additives, and dispersion quality drive reliability.

- September 2025: Dow launched DOWSIL EG-4175 Silicone Gel for high-voltage power electronics used in electric vehicles and renewable energy systems. The product underscores increasing material demand around insulation, thermal management, and long-term protection in electrified platforms, aligning with broader polymer nanocomposite pull in power-dense electronic modules.

- November 2024: Evonik unveiled flame-retardant PA12 and carbon-black-embedded 3D-printable powders for additive manufacturing. This widens the route-to-market for nano-enabled and advanced compound systems by enabling complex geometries and functional parts, reinforcing convergence between polymer compounding and industrial 3D printing qualification workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue earned from polymer materials that have nanoscale fillers dispersed in them to improve performance, including sales across major end-use industries and regions, measured in value terms.

Scope exclusions: We exclude nano-enabled coatings that are not sold as polymer nanocomposite materials, along with R&D-only lab samples and internal transfer pricing that does not reflect external market sales.

Segmentation Overview

- By Filler Type

- Carbon Nanotube

- Metal Oxide

- Nanoclay

- Nanofiber

- Other Filler Types

- By Polymer Matrix

- Thermoplastics

- Thermosets

- Bio-based Polymers

- By End-user Industry

- Automotive

- Packaging

- Aerospace and Defense

- Electrical and Electronics

- Energy and Storage

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear fact base for where demand can come from and how it moves across regions over time. We lean on public sources such as the USGS and other geological or minerals statistics for key nano-filler raw materials, UN Comtrade and national customs portals for trade flows, and agencies such as the US EPA for relevant materials and chemical-use context.

To keep assumptions realistic, we also reviewed standards and technical publications from organizations such as ISO, along with peer-reviewed journals that track adoption patterns in packaging, automotive, electronics, and construction uses. Company annual reports, investor presentations, and reputable industry press were used to understand capacity announcements, pricing direction, and product positioning. For cross-checking corporate financial signals and patent activity, we also used paid subscriptions for company financials and patent databases where it helped clarify ownership and innovation intensity. These desk sources are not exhaustive, and we also checked additional public references to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what we saw in desk findings and to close gaps around pricing, adoption timing, and substitution behavior. Interviews covered material suppliers, compounders, converters, and downstream users, and we rechecked key assumptions across APAC, EMEA, and the Americas so regional differences in demand drivers were not averaged out.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 18% | APAC: 50% |

| Mid tier: 55% | Functional/Unit leaders: 30% | EMEA: 30% |

| Smaller Players: 18% | Managers: 52% | Americas: 20% |

Market-Sizing & Forecasting

Market sizing was built using a combined top-down and bottom-up approach. The top-down view was reconstructed from end-use demand pools where polymer nanocomposites are commonly specified, and then applied through penetration rates that were adjusted by region and application maturity.

On the model input side, we tracked variables such as lightweighting intensity in automotive components, packaged food and barrier packaging output, electronics and electrical component production trends, construction activity tied to performance polymers, and the availability and pricing direction of nano-fillers (such as nanoclays and carbon-based additives). Average selling price was handled as a controlled assumption, where we separated commodity-like compounding from higher-spec grades so the model did not overstate value when volumes rise.

Forecasts were run using scenario analysis, with base, conservative, and accelerated adoption paths anchored to what interviewees expect for qualification cycles and end-use approvals. Selective bottom-up approximations, such as sampled volume by application multiplied by typical price bands and cross-checked against supplier revenue disclosure patterns, were used to corroborate totals and refine any obvious gaps. Where direct volume visibility was limited, we used proxy indicators (trade, capacity signals, and adoption shares) and documented the gap-handling logic before finalizing totals.

Data Validation & Update Cycle

Outputs were validated through multiple checks so they stay consistent with real-world signals. We compared the final totals against independent indicators like polymer consumption trends in key end uses, regional manufacturing output, and the direction of raw material and additive pricing, and then unusual jumps were reviewed again at the assumption level.

Before sign-off, the model goes through a multi-step analyst review where calculations, unit consistency, and currency conversions are rechecked, followed by targeted re-contacts when a number falls outside expected ranges. Reports are refreshed annually, and interim updates are made when material events occur, such as capacity changes, policy shifts, or sharp feedstock movements. Right before delivery, we complete a final pass so clients receive the most current view available.

Mordor Intelligence's Polymer Nanocomposite Market Estimate Compared With Other Published Estimates

Published market sizes for polymer nanocomposites often do not line up because the underlying counting rules are different, even when the titles look similar. The biggest differences usually come from what is treated as a true polymer nanocomposite sale versus adjacent nano-enabled materials, and from how pricing and adoption timing are handled.

In this study, the key gap drivers were the scope cut between polymer nanocomposites and broader nanocomposites, the way end-use penetration is applied (qualification cycles in packaging and automotive can delay volume ramps), and how average selling prices are moved over time in each region. Some estimates also mix years, use different currency timing, or rely on aggressive adoption assumptions that were not rechecked with industry participants, which can inflate near-term values versus a demand-pool based build.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.3 B (2026) | |

| Industry Publisher A | USD 14.1 B (2024) | Uses an earlier base year and can compress near-term growth if adoption is not re-rated for recent qualification wins, and scope can differ on whether nano-enabled polymer additives sold into masterbatches are counted as finished nanocomposite value. |

| Industry Publisher B | USD 12.22 B (2024) | Often applies a broad type-based segmentation that can undercount higher-value grades when pricing bands are not separated by application, and it may assume faster volume scale-up without matching it to regional end-use production indicators. |

Overall, the spread is mainly explained by base-year selection, scope cuts around what is counted as a nanocomposite sale, and the discipline used in moving penetration and ASP by end use and region. In this approach, those inputs are handled explicitly in the market model and refreshed through interview-led checks, with the latest sizing anchored at 2026 by Mordor Intelligence.

Key Questions Answered in the Report

What are polymer nanocomposites?

Polymer nanocomposites are plastics reinforced with nanoscale fillers—such as nanoclay, graphene, or carbon nanotubes—that markedly enhance strength, thermal conductivity, and barrier performance compared with conventional polymers.

How large is the polymer nanocomposites market in 2026?

The market is valued at USD 15.3 billion in 2026 and is projected to reach USD 31.6 billion by 2031, reflecting a 15.62% CAGR over the forecast period.

Which end-user industry currently drives the most demand?

Automotive applications lead with 30.35% market share in 2025, and the sector is also the fastest-growing at a 17.21% CAGR through 2031.

Why are polymer nanocomposites important for electric vehicles?

They cut component weight by about 40% versus steel, improve battery-housing thermal management, and enable recyclable thermoplastic structures, all of which help extend driving range and meet sustainability goals.

Which geographic region is expanding the fastest?

Asia-Pacific holds 39.92% of global revenue and records the highest growth rate at an 18.05% CAGR, aided by integrated supply chains and government support for advanced materials.

Page last updated on: