Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

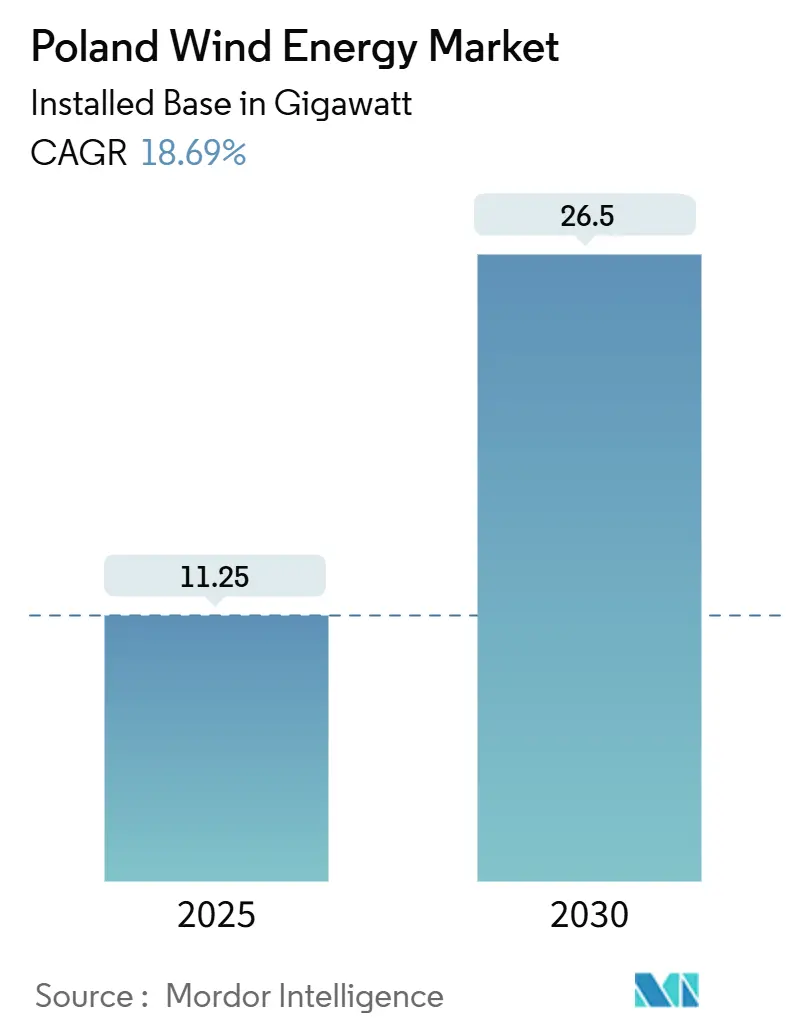

| Market Volume (2025) | 11.25 gigawatt |

| Market Volume (2030) | 26.5 gigawatt |

| Growth Rate (2025 - 2030) | 18.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Wind Energy Market Analysis by Mordor Intelligence

The Poland Wind Energy Market size in terms of installed base is expected to grow from 11.25 gigawatt in 2025 to 26.5 gigawatt by 2030, at a CAGR of 18.69% during the forecast period (2025-2030).

The expansion reflects the country’s pivot away from coal, the maturation of Baltic Sea offshore resources, and a steady pipeline of contracts for difference that guarantee 25-year inflation-indexed revenues for new capacity. Developers are pressing forward despite 400 kV transmission bottlenecks in northern voivodeships and a legacy 10H distance rule that has frozen most onshore permitting. Strategic decisions such as Vestas’ nacelle and blade factories in Szczecin and expanding electrolyzer pilots at offshore sites signal rising confidence in long-term policy stability. Overall, the Poland wind energy market is set to become the Baltic region’s fastest-growing renewable segment as grid upgrades, larger turbines, and local-content incentives combine to lift profitability.

Key Report Takeaways

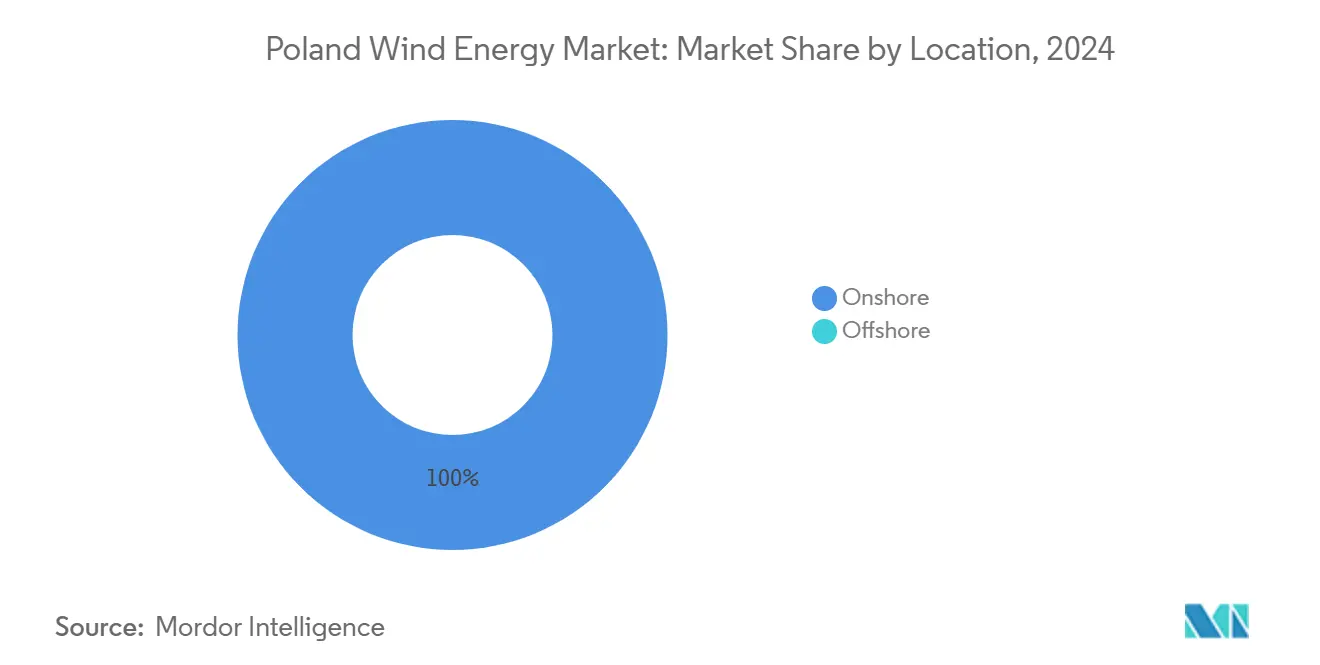

- By location, onshore wind accounted for 100% capacity in 2024, and 6 GW of offshore installations are expected to come online by 2030.

- By turbine class, 3-6 MW units held a 59.5% Poland wind energy market share in 2024, while turbines above 6 MW are projected to grow at 23.1% CAGR to 2030.

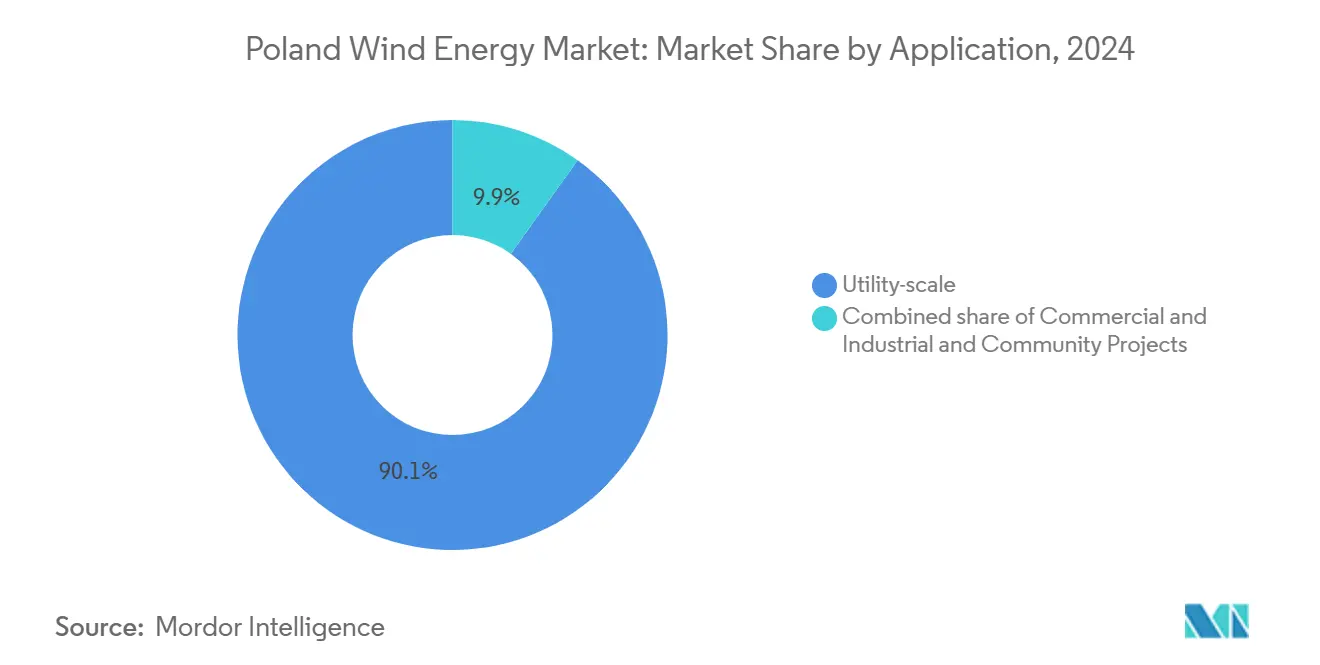

- By application, utility-scale projects commanded 90.1% of the 2024 project pipeline; community wind leads growth with a 25.7% CAGR to 2030.

Poland Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 2025–2027 CfD auctions pipeline | +4.2% | Coastal voivodeships | Medium term (2–4 years) |

| EU Fit-for-55 and REPowerEU compliance | +3.8% | National | Long term (≥4 years) |

| Declining LCOE of ≥5 MW onshore turbines | +2.1% | Central and western regions | Short term (≤2 years) |

| Grid-balancing revenues from offshore-to-hydrogen pilots | +1.9% | Pomorskie, Zachodniopomorskie | Medium term (2–4 years) |

| Local-content tax incentives for nacelle assembly | +1.5% | Szczecin and Gdańsk | Medium term (2–4 years) |

| Faster permitting under 10H-rule amendment | +2.7% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerated 2025–2027 CfD Auctions Pipeline

The December 2025 auction will award 4 GW of offshore contracts, each guaranteeing 25-year inflation-protected tariffs that derisk financing and stimulate early turbine orders.[1]Ørsted A/S, “Baltica Offshore Wind Farm Factsheet,” orsted.com A staggered schedule through 2027 sustains visibility for OEM investments such as Vestas’ Szczecin plants. Auction rules demand pre-arranged grid-connection agreements, effectively filtering out speculative bids. Onshore baskets remain smaller because the 10H rule caps available land, yet reform discussions signal potential upside. The predictable auction cadence underpins the Poland wind energy market by smoothing revenue expectations and lowering the cost of capital.

EU Fit-for-55 and REPowerEU Compliance Pressure

Poland’s National Recovery and Resilience Plan pledges 5.9 GW offshore by 2030 and 11 GW by 2040, forcing state utilities to prioritize wind development over coal refurbishments.[2]Polskie Sieci Elektroenergetyczne, “Development Plan 2023–2032,” pge.pl The European Commission links access to EU grants with renewable deployment milestones, ensuring that price caps in future auctions mirror true levelized costs. PSE’s USD 17 billion grid program, half funded by the Connecting Europe Facility, will add 4,850 km of 400 kV lines and a north–south HVDC link by 2030. New cross-border interconnectors with Germany and Lithuania widen arbitrage options for surplus wind. Regulatory pressure, therefore, accelerates manufacturing decisions, fosters technology transfer, and deepens market liquidity.

Declining LCOE of ≥5 MW Onshore Turbines

European onshore LCOE fell to USD 33–55/MWh in 2024 as developers adopted 5–6 MW platforms such as the Nordex N175/6.X with hybrid towers that cut civil costs 15–20%. Poland’s auction cap of PLN 319.04/MWh offers a comfortable margin for these machines once permitting barriers ease. Vestas’ 2025 acquisition of the Goleniów blade plant allows local manufacture of V172-7.2 MW blades, trimming logistics lead times and import fees. Turbine upsizing reduces foundation count per project, compressing construction schedules. Gains are contingent on modifying the 10H rule because larger rotors need wider setbacks, yet draft reforms promise designated acceleration zones with 12-month permit windows.

Grid-Balancing Revenues from Offshore-to-Hydrogen Pilots

PGE and Ørsted plan to pair 1 GW of electrolysis with Baltica 2 and 3, channeling curtailed power into hydrogen for Orlen’s Gdańsk refinery and improving project IRR by 1–2 percentage points. Direct coupling sidesteps coastal grid congestion and captures full price spreads between peak and off-peak hours. Equinor’s Bałtyk 1 is studying a similar configuration at Gdynia port. Early success could unlock a secondary revenue stream that stabilizes the Poland wind energy market during periods of negative pricing.

Restraints Impact Analysis*

| Restrain | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic 400 kV grid bottlenecks | −2.8% | Northern voivodeships | Medium term (2–4 years) |

| Zloty-denominated financing volatility | −1.4% | National | Short term (≤2 years) |

| Public opposition near Natura 2000 sites | −1.2% | Coastal and inland corridors | Long term (≥4 years) |

| OEM blade-recycling liabilities | −0.9% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Chronic 400 kV Grid Bottlenecks

PSE rejected 83.6 GW of connection requests in 2023 because northern substations lack export capacity to demand centers in Warsaw and Silesia.[3]PGE Baltica, “Grid Connection Agreements for Offshore Projects,” pgebaltica.pl Relief will arrive only after the HVDC backbone and 4,850 km of new 400 kV lines enter service between 2028 and 2030. Early offshore projects such as Baltica 2 secured slots before saturation, giving them superior economics. Later projects must co-locate storage or hydrogen to dodge curtailment, which inflates capital needs and slows build-out in the Polish wind energy market.

Zloty-Denominated Financing Volatility

Most local lenders price debt in Polish zloty, exposing projects without euro-pegged CfDs to currency swings that can widen interest spreads by 150–200 basis points. Developers hedge through cross-currency swaps that add 2–3 USD/MWh to levelized costs. The zloty has traded in a 12% band against the euro since 2023, and policy tightening cycles amplify volatility. Stable euro-denominated tariffs in forthcoming auctions could ease this funding headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Momentum Versus Onshore Constraints

Offshore capacity will jump from zero to 6 GW by 2030, driven by flagship projects such as Baltica 2 at 1.5 GW and Baltic Power at 1.2 GW. The Poland wind energy market will therefore depend increasingly on seabed leases where central permitting bypasses municipal vetoes. Early offshore projects enjoy grid slots yet still plan 1 GW of electrolyzers to handle curtailment.

Onshore installations remain limited to the repowering of pre-2016 farms because the 10H rule excludes 99% of land. Draft reforms promise 12-month permits in acceleration zones, but final approval rests with local councils. Consequently, developers with strong municipal ties can unlock pockets of capacity, while others pivot offshore. The result is a bifurcated Poland wind energy market in which near-term growth concentrates at sea and onshore advances in step with regulatory clarity.

By Turbine Capacity: Rise of ≥6 MW Platforms

Turbines above 6 MW will command future orders as offshore developers install Siemens Gamesa 14 MW and Vestas V236-15 MW units that deliver capacity factors above 50% in Baltic conditions. The Poland wind energy market size for this segment is forecast to rise sharply once Baltica 2 deploys 107 machines by 2027.

Legacy 3-6 MW turbines still dominate the operating fleet with a 59.5% share in 2024, but will lose ground as repowering and offshore phases advance. Nordex’s 148 MW onshore contract in 2024 shows continuing demand for mid-range capacity where setback rules restrict tower heights. Local blade production in Szczecin strengthens the supply chain for larger units, shortening lead times and reducing transport costs.

By Application: Utility Scale Dominance and Community Upside

Utility-scale assets held 90.1% of 2024 applications, reflecting the capital strength of PGE, Orlen, and foreign partners such as Ørsted. Their projects align with national targets and secure CfDs that underpin bankability.

Community wind, while small, is the fastest-growing niche at 25.7% CAGR to 2030. Prosumer law reforms now let municipalities buy equity stakes and share revenues, boosting local acceptance. However, higher upfront costs and grid-access complexity slow uptake compared with rooftop solar. The Poland wind energy industry may see accelerated community participation once standard templates for co-investment and long-term offtake mature.

Geography Analysis

Northern voivodeships anchor growth thanks to Baltic Sea resources that yield offshore capacity factors above 50%. Szczecin and Gdańsk shipyards host new nacelle, blade, and substation factories that add 2,500 jobs by 2026. Grid congestion remains acute because 400 kV corridors were built for coal in the south, prompting hydrogen and battery pilots as interim relief.

Central regions such as Wielkopolskie and Łódzkie possess moderate wind speeds but face 10H setbacks. The February 2025 draft acceleration law seeks to pre-zone land where councils approve projects within one year, potentially unlocking 2–3 GW by 2030.[4]Dentons, “Poland’s Renewable Acceleration Areas Draft Act,” dentons.com

Southern voivodeships lack wind resource yet will import offshore power via a north–south HVDC link by 2030. This infrastructure balances geographic disparities, enabling surplus Baltic output to feed industrial clusters in Katowice and Kraków. Cross-border lines with Germany and Lithuania further diversify offtake routes, improving price spreads for operators in the Polish wind energy market.

Competitive Landscape

Three joint ventures, PGE–Ørsted, Orlen–Northland-CIP, and Equinor–Polenergia, control 6 GW of Poland’s 7.5 GW offshore pipeline, giving the segment moderate concentration. Their structures pair local utilities with foreign expertise, sharing capital risk while retaining domestic value. Hybrid projects that co-locate wind with 1 GW of electrolysis at Baltica 2 and 3 illustrate innovation that boosts IRR by 1–2 percentage points.

Onshore competition is fragmented among more than 15 developers repowering legacy sites or pursuing small community projects. Nordex gained ground in 2024 with 148 MW of orders as Siemens Gamesa faced reliability setbacks.[5]Nordex SE, “Press Release on 148 MW Order in Poland,” nordex-online.com

OEM strategies hinge on local content. Vestas will assemble V236-15 MW nacelles and blades in Szczecin, securing preferential auction scores and lowering logistics expenses. Suppliers that can meet recycling mandates and deliver larger turbines on time are positioned to capture share as the Poland wind energy market expands.

Poland Wind Energy Industry Leaders

Siemens Gamesa Renewable Energy

Vestas Wind Systems A/S

GE Renewable Energy

Nordex SE

Enercon GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vestas has acquired LM Wind Power's blade factory in Goleniów, near Szczecin, Poland, integrating it into Vestas' expanding European manufacturing network. The financial details of the transaction remain undisclosed.

- May 2025: Equinor and Polenergia have successfully secured over EUR 6 billion in financing for their Bałtyk 2 and Bałtyk 3 offshore wind projects, marking a significant milestone for the 1.44 GW capacity initiatives set to rise in the Polish Baltic Sea.

- January 2025: Ørsted and PGE have jointly decided to invest in the 1.5 GW Baltica 2 Offshore Wind Farm. This wind farm, named Baltica 2, will be situated about 40 km off the Polish coast, close to Ustka, and is slated for full commissioning in 2027.

- September 2024: Polish utility Tauron Polska Energia SA's green unit has secured a 190.8-MW wind farm project in Poland from the German renewables developer VSB Group, as per the contract unveiled by both companies. Located in the Greater Poland Voivodeship, the Miejska Gorka wind project will feature up to 53 wind turbines, with a significant 148-MW order already placed by Nordex.

Poland Wind Energy Market Report Scope

Wind energy is a renewable energy source that harnesses the energy of wind to generate electricity, which is usually generated using a wind turbine. Wind turbines are mechanical systems that convert kinetic energy into electrical energy. Wind power is sustainable and has a much smaller environmental impact compared to fossil fuels.

The Poland wind energy market is segmented by location, turbine capacity, and application. By location, the market is segmented into onshore and offshore. By turbine capacity, the market is segmented into up to 3 MW, 3 to 6 MW, and above 6 MW. By application, the market is segmented into utility-scale, commercial and industrial, and community projects. The report offers market sizes and forecasts in terms of installed capacity (GW) for all the above segments.

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How big is Poland's installed wind capacity in 2025 and how fast will it grow?

Poland hosts 11.25 GW of installed wind capacity in 2025 and is forecast to reach 26.50 GW by 2030, equal to an 18.69% CAGR.

When will the first large Polish offshore wind farms start generating electricity?

Baltic Power at 1.2 GW is scheduled to come online in 2026, and the 1.5 GW Baltica 2 project is due to follow in 2027.

Which regions of Poland are attracting new wind component factories?

Szczecin and Gda?sk shipyard zones will house Vestas nacelle and blade plants that together create about 1,700 direct jobs by 2026.

What is the main barrier to new onshore wind projects in Poland?

The 10H distance rule requires turbines to sit ten times their height from buildings, leaving only 1% of land open to development and freezing most new onshore permits.

How are developers tackling grid congestion along the Baltic coast?

Offshore projects are pairing up to 1 GW of electrolyzers with wind farms to convert curtailed power to hydrogen while PSE upgrades 400 kV lines and an HVDC link slated for completion in 20292030.

What financing support mechanisms are available for Polish wind projects?

Competitive auctions award 25-year inflation-linked contracts for difference that lock in revenues and enable non-recourse bank financing.

Page last updated on: