Poland ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 31.59 Billion |

| Market Size (2026) | USD 34.75 Billion |

| Market Size (2031) | USD 56.01 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Poland ICT Market Analysis by Mordor Intelligence

The Poland ICT market size was valued at USD 31.59 billion in 2025 and estimated to grow from USD 34.75 billion in 2026 to reach USD 56.01 billion by 2031, at a CAGR of 10.02% during the forecast period (2026-2031).

Robust EU funding, widespread 5G rollout, and an enterprise-wide shift to cloud platforms keep digitalization momentum high, while a heightened cyber-threat environment pushes security spending to the top of corporate agendas. Large technology investments by multinational vendors and a resilient startup scene provide fresh competition, yet local champions retain strong public-sector relationships. The Poland ICT market benefits from Warsaw’s and Kraków’s deep developer pools, as near-shoring demand from Western Europe drives service-export revenues. Ongoing rural fiber builds and spectrum auctions ensure nationwide connectivity improvements that unlock new addressable demand in previously underserved areas

Key Report Takeaways

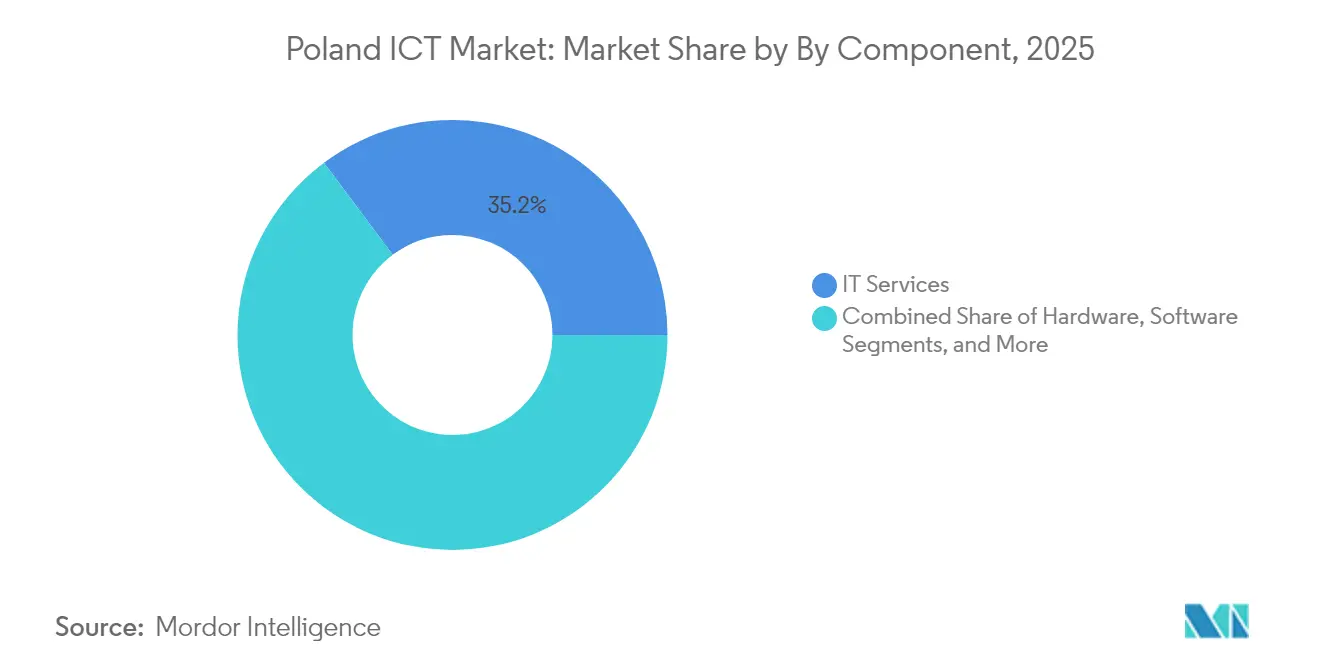

- By component, IT services led with 35.20% revenue share of the Poland ICT market in 2025; public cloud services are forecast to expand at an 17.78% CAGR to 2031.

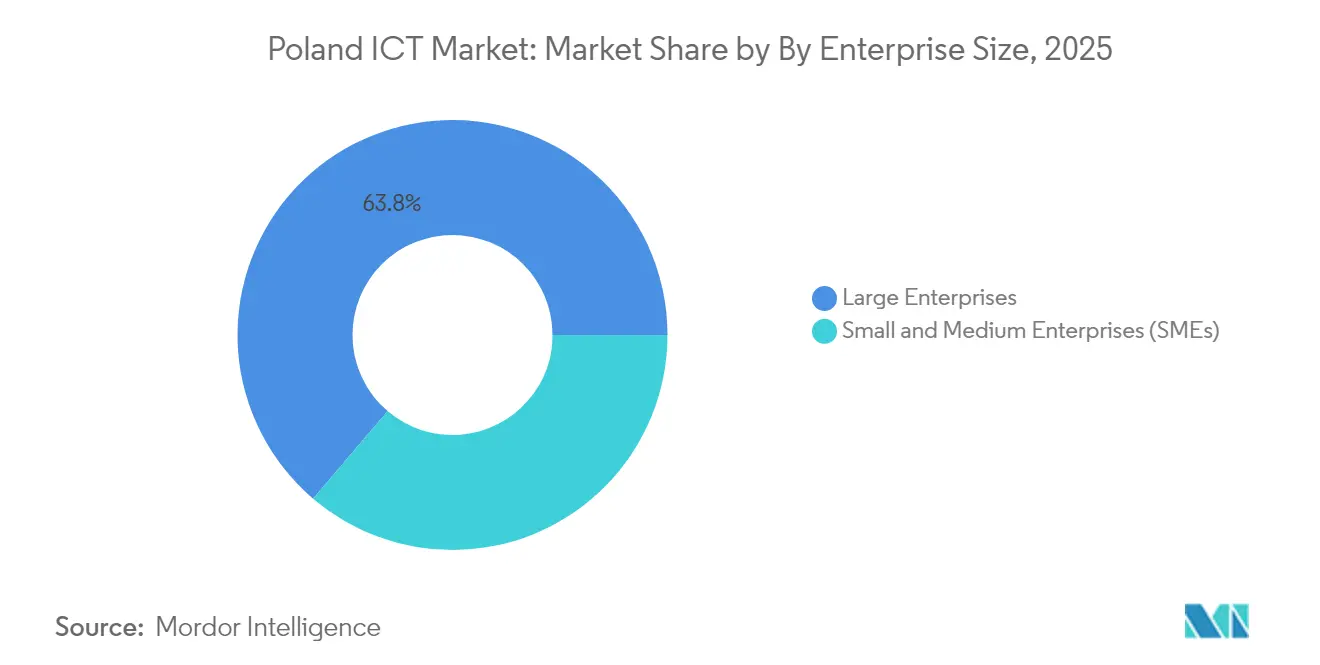

- By enterprise size, the large-enterprise segment held 63.77% of the Poland ICT market size in 2025, while SMEs record the highest projected CAGR at 13.74% through 2031.

- By industry vertical, BFSI accounted for 22.05% share of the Poland ICT market size in 2025 and healthcare is advancing at a 14.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland ICT Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EU-funded digital transformation programs | +2.1% | National, with concentration in major metropolitan areas | Medium term (2-4 years) |

| Surging internet and 5G penetration | +1.8% | National, with rural areas showing accelerated adoption | Short term (≤ 2 years) |

| Enterprise cloud-first adoption | +2.3% | National, with SME segment leading growth | Medium term (2-4 years) |

| Heightened cyber-threat environment | +1.9% | National, with critical infrastructure focus | Short term (≤ 2 years) |

| Semiconductor FDI inflows (Intel facility) | +0.7% | Regional, concentrated in Lower Silesia | Long term (≥ 4 years) |

| ICT service-export near-shoring boom | +1.7% | National, with Warsaw and Krakow hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising EU-funded Digital Transformation Programs

Poland's access to EUR 7.59 billion through the Digital Europe Programme creates a multiplier effect that extends beyond direct government spending into private sector investment acceleration. The CyberPoland 2025 initiative allocates PLN 700 billion for economic transformation, representing the largest investment commitment in Polish history[1]Government of Poland. "CyberPoland 2025." Accessed August 8, 2025. https://www.gov.pl/web/cyfryzacja/cyberpoland-2025. This funding structure incentivizes enterprises to advance digital transformation timelines, as co-financing requirements drive complementary private investments. The e-Doręczenia electronic delivery system implementation demonstrates how regulatory mandates create immediate demand for integration services, while the KSeF e-invoicing system rollout generates sustained revenue streams for software providers and system integrators. The mObywatel app enhancement with AI virtual assistant capabilities signals government commitment to advanced technology adoption, creating demonstration effects that influence enterprise procurement decisions across multiple sectors.

Enterprise Cloud-First Adoption

Cloud adoption among Polish enterprises reached 64% in 2024, yet the underlying dynamics reveal strategic gaps that create premium service opportunities. McKinsey analysis indicates cloud implementation could generate EUR 27 billion in economic value by 2030, equivalent to 4% of GDP, suggesting current adoption rates significantly underestimate market potential. 40% of companies that resist cloud migration cite cost concerns, creating opportunities for hybrid deployment models and managed service providers that can demonstrate ROI through operational efficiency gains. Public cloud services growth at 18.23% CAGR reflects enterprise preference for consumption-based models over capital expenditure commitments. The healthcare sector's 68% physician optimism regarding AI integration indicates cloud infrastructure demand will accelerate as regulatory frameworks for medical AI applications mature[2]Polish Ministry of Health. "AI Healthcare Strategy 2025." Accessed August 8, 2025. https://www.gov.pl/web/zdrowie/ai-healthcare-strategy-2025.

Heightened Cyber-Threat Environment

Poland's designation as the most cyber-attacked country globally, with over 1000 weekly incidents, transforms cybersecurity from a cost center to a revenue driver for ICT service providers. The NIS2 directive implementation creates mandatory spending requirements across 18 regulated sectors, with essential entities facing fines up to EUR 10 million for non-compliance. This regulatory framework generates predictable revenue streams for cybersecurity consultants and managed security service providers. The geopolitical context, particularly threats from Russian state actors, elevates cybersecurity to a national security priority, ensuring sustained government funding and enterprise investment. Supply chain attack sophistication requires advanced threat detection capabilities, creating demand for AI-powered security platforms and real-time monitoring services that command premium pricing.

Surging Internet and 5G Penetration

Household 5G coverage climbed past 71.9% in 2024 and fiber passed over 86.9% of urban premises, giving enterprises reliable bandwidth for latency-sensitive workloads[3]Polish Ministry of Digital Affairs, “5G Network Coverage Poland 2024,” gov.pl Source: European Commission, “Digital Economy and Society Index – Poland,” digital-strategy.ec.europa.eu . Rural broadband projects financed by the PLN 450 million Digital Poland program close connectivity gaps and unlock fresh SME demand. The Poland ICT market quickly commercializes edge-compute, IoT, and video-analytics services once high-speed access becomes ubiquitous.

Restraint Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiber and rural infrastructure gaps | –1.4% | Rural counties | Medium term (2-4 years) |

| ICT talent shortages and brain drain | –1.8% | Nationwide | Long term (≥ 4 years) |

| SME digital-skills deficit | –1.2% | Traditional industry belts | Medium term (2-4 years) |

| DSA-related compliance cost burden | –0.9% | Platform providers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fiber and Rural Infrastructure Gaps

While urban fiber is near-saturation, only 74% of rural premises enjoy high-speed links, delaying uptake of data-intensive SaaS tools outside cities. Smaller municipalities, therefore, postpone advanced ICT projects, flattening demand curves for integrators that rely on nationwide rollouts. Accelerated public-private investment aims to add 1.7 million new fiber connections by 2027, but near-term revenue leakage persists.

ICT Talent Shortages and Brain Drain

Poland posts 275% more tech vacancies per employed specialist than the OECD average, with 59% of firms citing hiring difficulties. Remote-work options in higher-pay EU markets intensify brain drain, pushing wage costs upward and compressing service-provider margins. Upskilling programs in STEM fields and new visa routes promise long-term relief, yet immediate capacity constraints limit how fast the Poland ICT market can scale complex transformation projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Digital Transformation

IT services held a 35.20% Poland ICT market share in 2025, underlining enterprises’ tilt toward outsourcing complex workloads. Public cloud’s 17.78% CAGR through 2031 means the services layer grows even faster than the underlying infrastructure, as firms seek migration, DevOps, and managed-security expertise. Hardware spending continues but centers on edge devices and private 5 G kits that pair tightly with software orchestration layers. Telecom services profit from data-traffic surges tied to IoT and video collaboration, while software platforms enjoy predictable subscription cash flows.

Rising adoption of AI-enabled ERP, cyber-defense suites, and verticalized health-IT systems keeps software demand resilient. Meanwhile, hyperscalers choose Warsaw for regional availability zones, encouraging SaaS vendors to colocate. Together, these trends sustain a virtuous circle of infrastructure build-outs and high-margin service engagements across the Polish ICT market.

By Enterprise Size: SME Growth Outpaces Large-Enterprise Adoption

Large organizations owned 63.77% of the Poland ICT market size in 2025, yet SMEs will compound at 13.74% annually, boosted by EU vouchers and simplified SaaS onboarding. Low upfront capital and pay-per-user billing help smaller firms overcome budget hurdles, while industry associations deliver free cyber-hygiene courses to speed adoption. Vendors with “one-click” marketplaces and local-language support capture wallet share early, locking in renewal revenue.

Large enterprises remain critical for big-ticket projects such as multi-cloud orchestration, zero-trust security, and predictive-maintenance analytics. Their long procurement cycles favor incumbents, but innovation labs increasingly pilot cutting-edge solutions from Polish startups. This dual-track demand profile ensures both scale and agility exist side by side within the Poland ICT market.

By Industry Vertical: Healthcare Leads Growth Trajectory

BFSI contributed 22.05% of 2025 revenue, propelled by open-banking APIs, biometric authentication, and real-time payment rails. Telemedicine expansion and AI-assisted diagnostics lift healthcare to the fastest 14.91% CAGR, with hospitals migrating imaging archives to secure clouds and investing in e-prescription systems. Government and public services modernize citizen portals and tax platforms, while manufacturing accelerates Industry 4.0 rollouts that blend IoT sensors with data lakes.

Retail focuses on omnichannel payment integration and last-mile logistics optimization, whereas energy utilities deploy smart-meter networks. Each segment’s distinct requirements create room for niche specialists and multi-domain integrators who can translate regulatory constraints into technical blueprints-a dynamic that expands addressable value pools across the Poland ICT market.

Geography Analysis

The Poland ICT market clusters around Warsaw, Kraków, Tricity, and Wrocław, where dense talent pools and VC capital converge. These metros host 25% of Central and Eastern Europe’s developer workforce, providing scale advantages for both startups and multinationals. Microsoft’s USD 700 million hyperscale region in Warsaw cements the capital as a cloud gateway for the entire CEE bloc.

Second-tier cities such as Łódź, Poznań, and Katowice gain traction through lower real-estate costs and targeted university-industry collaborations. Rural districts lag on fiber but benefit from government subsidy schemes that aim to deliver gigabit-class links to 1.7 million extra households. These programs expand total addressable demand for the Poland ICT market by bringing SMEs in agribusiness and tourism online.

Cross-border corridors linking Poland to Germany, Czechia, and Slovakia enable shared R&D on quantum computing and high-performance cloud workloads. Participation in the European High-Performance Computing Joint Undertaking offers access to exascale resources, letting local firms test AI models without exporting data. This integration reinforces Poland’s position as a digital bridge between Western Europe and emerging Eastern markets.

Competitive Landscape

Domestic leaders such as Asseco Poland and Comarch leverage long-standing public-sector ties and deep localization expertise. Asseco’s PLN 349.55 million ZUS contract exemplifies its hold on government workloads, while Comarch’s ERP suite dominates SME back-office digitalization. International hyperscalers aggressively expand: Microsoft’s USD 700 million spend secures cloud primacy, and Google’s AI partnership channels research grants to local universities, broadening ecosystem gravity.

Telecom operators Orange, T-Mobile, Play, and Plus accelerate 5G rollouts and fiber builds, bundling edge-compute and security add-ons for enterprise accounts. These carriers co-invest in neutral-host towers to trim capex and shorten rural coverage timelines. Startups concentrate on fintech, health-tech, and cybersecurity niches, often graduating from Polish accelerators into EU-wide scale-ups, which enriches the Poland ICT market with innovative IP.

Talent scarcity shapes competitive tactics: firms offer remote-first contracts, equity incentives, and funded training to secure specialists. Vendors that embed Polish-language LLMs inside support bots or code-assistant tools differentiate against global rivals. The cancelled Intel wafer-fab redirects FDI toward software and AI, elevating competition in high-value professional services rather than capital-intensive manufacturing.

Poland ICT Industry Leaders

-

Microsoft Polska Sp. z o.o.

-

Google Polska Sp. z o.o.

-

Oracle Polska Sp. z o.o.

-

Cognizant Technology Solutions Poland Sp. z o.o.

-

Adobe Systems Polska Sp. z o.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Intel cancelled its USD 4.6 billion semiconductor facility near Wrocław, redirecting public incentives toward AI and software ventures.

- April 2025: IQM deployed Poland’s first superconducting quantum computer, enabling academic and commercial quantum-algorithm testing.

- February 2025: Microsoft committed PLN 2.8 billion (USD 700 million) to build a Warsaw hyperscale region and co-develop defense-grade cybersecurity solutions with the Ministry of National Defence.

- February 2025: Google launched an AI research partnership with Polish universities to advance multilingual LLMs for Central European languages.

- November 2024: Cyfrowy Polsat posted PLN 609.6 million profit for 9M 2024 as green-energy diversification lifted margins.

Poland ICT Market Report Scope

Information and communication technologies, or ICT, is a broader term for information technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services, that enable users to store, access, transmit, retrieve, and manipulate information in digital form.

Poland's ICT market is segmented by type (hardware, software, IT services, and telecommunication services), the size of the enterprise (small and medium enterprise and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, and energy and utilities). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | Computer Hardwar |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Government and Public Administration |

| Retail, E-commerce and Logisitcs |

| Manufacturing and Industry 4.0 |

| Halthcare and Life Sciences |

| Gaming and Esports |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Energy and Utilities |

| Other Verticals |

| By Type | Hardware | Computer Hardwar |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Size of Enterprise | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | BFSI | |

| Government and Public Administration | ||

| Retail, E-commerce and Logisitcs | ||

| Manufacturing and Industry 4.0 | ||

| Halthcare and Life Sciences | ||

| Gaming and Esports | ||

| Oil and Gas (Up-, Mid-, Down-stream) | ||

| Energy and Utilities | ||

| Other Verticals | ||

Key Questions Answered in the Report

How big will spending on cloud services in Poland reach by 2031?

Public cloud revenue is on track to grow at an 17.78% CAGR, making it the fastest-expanding line within the Poland ICT market through 2031.

Which customer segment offers the highest growth potential?

SMEs are projected to grow at 13.74% annually, outpacing large enterprises as subsidies and SaaS pricing lower adoption barriers.

What keeps cybersecurity demand elevated?

Poland records more than 1,000 weekly cyber incidents and faces NIS2 fines up to EUR 10 million, prompting companies to boost security budgets.

Why is healthcare accelerating technology purchases?

Telemedicine, AI-assisted diagnostics, and electronic health-record mandates push healthcare spending to a 14.91% CAGR through 2031.

How will 5G influence digital services revenue?

Nationwide 5G coverage enables IoT, edge analytics, and high-bandwidth applications, raising data-traffic-driven service revenues across carriers.

Page last updated on: