Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

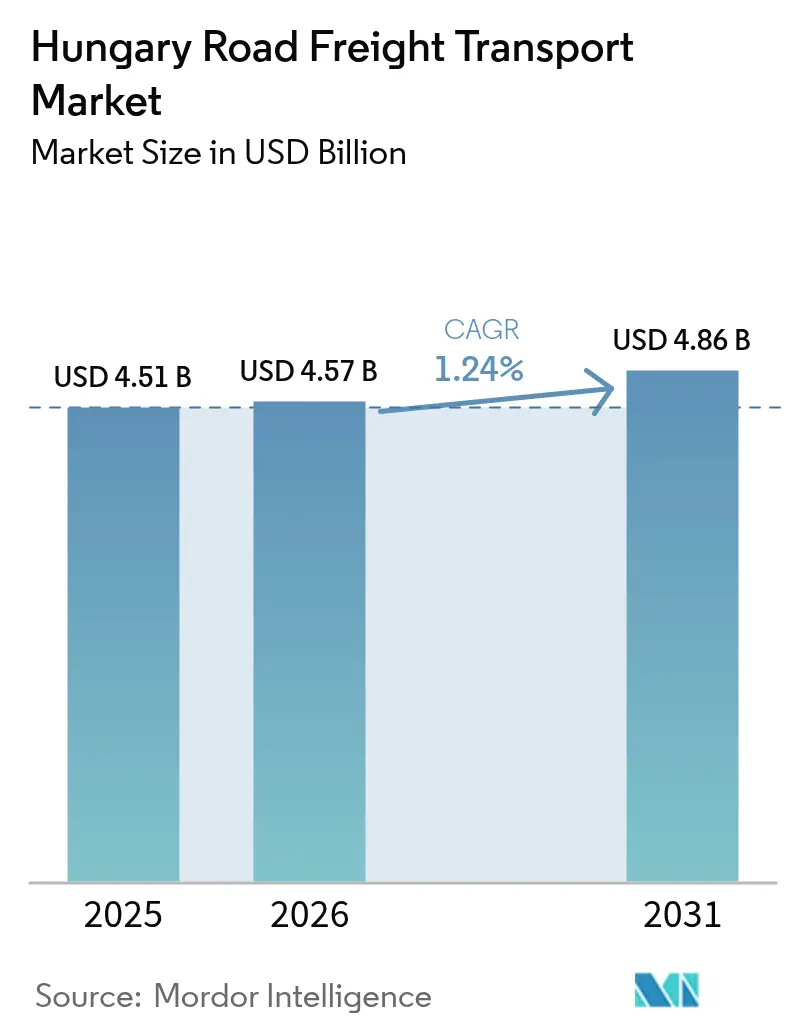

| Base Year Market Size (2025) | USD 4.51 Billion |

| Market Size (2026) | USD 4.57 Billion |

| Market Size (2031) | USD 4.86 Billion |

| Growth Rate (2026 - 2031) | 1.24% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Road Freight Transport Market Analysis by Mordor Intelligence

The Hungary road freight transport market size was valued at USD 4.51 billion in 2025 and estimated to grow from USD 4.57 billion in 2026 to reach USD 4.86 billion by 2031, at a CAGR of 1.24% during the forecast period (2026-2031). Near-shoring of European supply chains, sustained automotive and electronics exports, and EU-funded infrastructure upgrades provide a foundation for stable growth. At the same time, acute driver shortages, rising HU-GO distance-based tolls, and looming Euro-7 CAPEX outlays tighten margins. The market’s ability to deploy advanced fleet telematics, real-time documentation, and intermodal connectivity continues to offset operating-cost pressure. As a result, the Hungary road freight transport market increasingly supports high-value just-in-time flows for original-equipment manufacturers and surging e-commerce volumes concentrated in Budapest and Central Hungary.

Key Report Takeaways

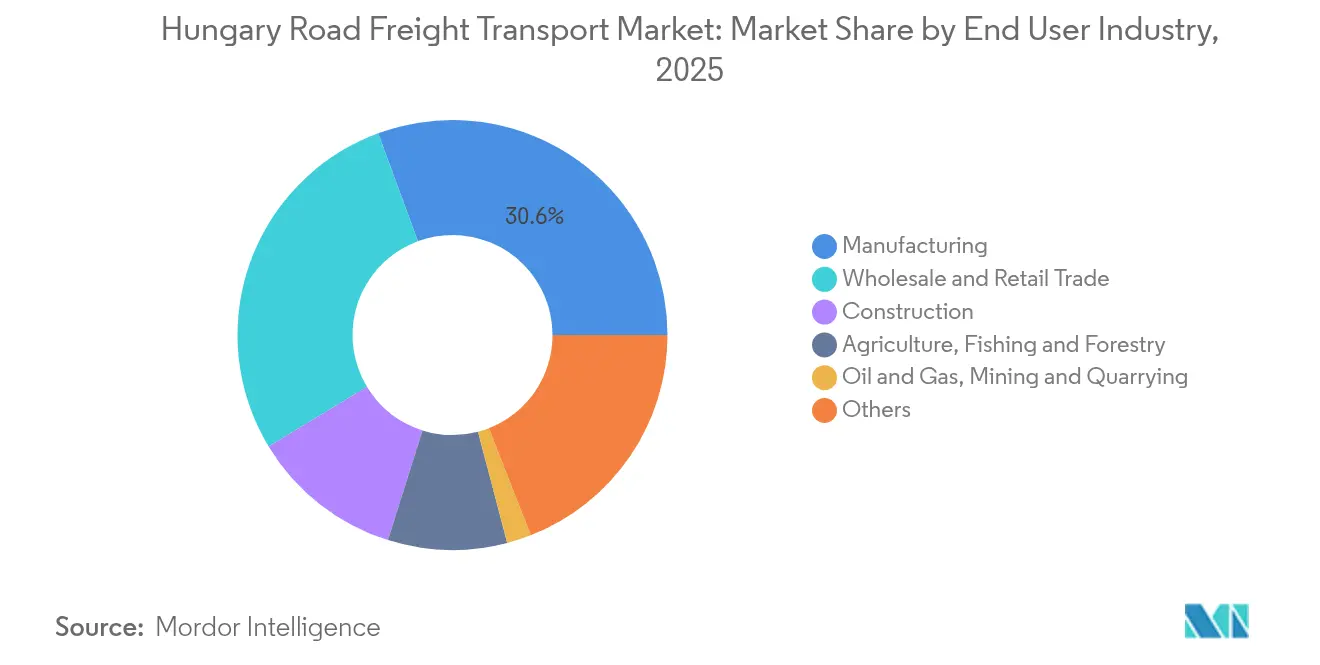

- By end user industry, manufacturing led with 30.62% of the Hungary road freight transport market share in 2025; wholesale and retail trade is forecast to expand at a 1.44% CAGR between 2026-2031.

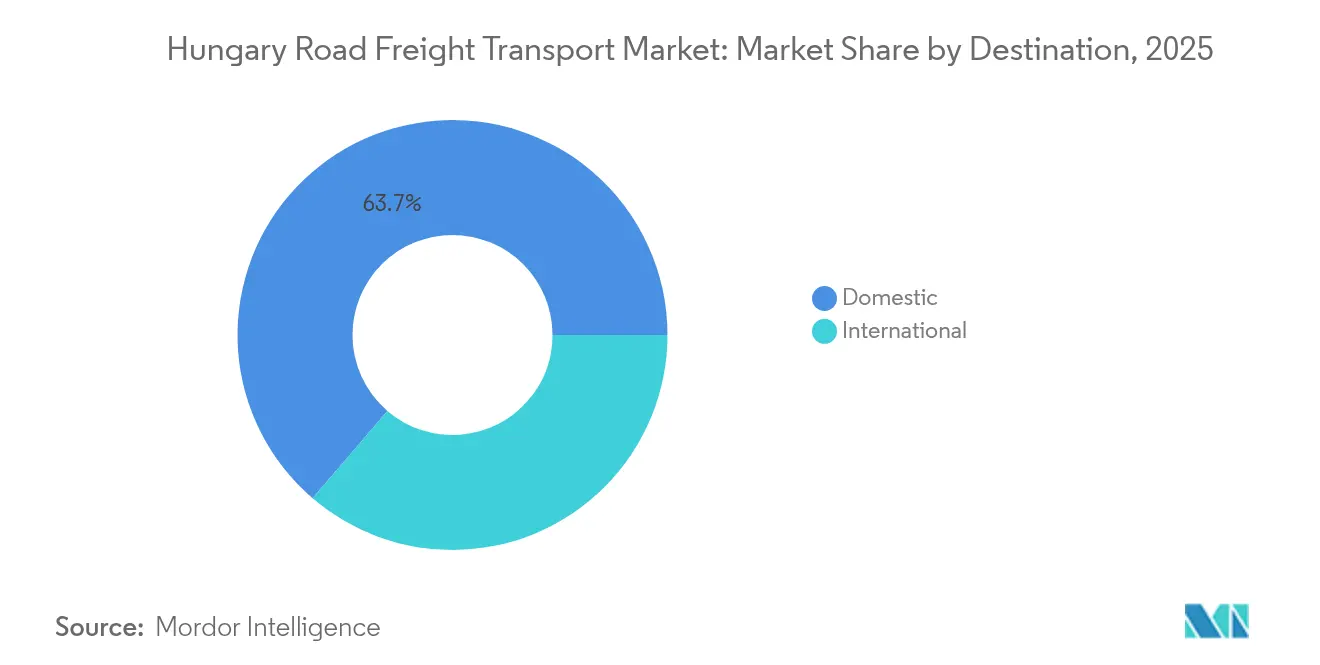

- By destination, the domestic sub-segment commanded 63.72% of the Hungary road freight transport market size in 2025, while the international sub-segment is projected to grow at a 1.61% CAGR between 2026-2031.

- By truckload specification, full-truck-load operations held 69.78% revenue share in 2025; less-than-truck-load is set to advance at a 1.41% CAGR between 2026-2031.

- By containerization, the non-containerized sub-segment represented 87.42% revenue share in 2025, whereas the containerized sub-segment is set to rise at a 1.29% CAGR between 2026-2031.

- By distance, long-haul services captured 73.05% revenue share in 2025, while short-haul movements recorded the fastest 1.43% CAGR between 2026-2031.

- By goods configuration, solid goods dominated with 74.44% market share in 2025; fluid goods are predicted to grow at a 1.37% CAGR between 2026-2031.

- By temperature control, the non-temperature controlled sub-segment accounted for 94.12% revenue share in 2025; the temperature controlled sub-segment is projected to increase at a 1.39% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hungary Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hungary’s expanding automotive and electronics export base is intensifying just-in-time road-haulage requirements | +0.3% | Budapest–Debrecen–Győr corridors | Medium term (2-4 years) |

| Surging e-commerce parcel activity in Budapest and Central Hungary is multiplying middle-mile and urban LTL movements | +0.2% | Budapest andCentral Hungary | Short term (≤ 2 years) |

| Accelerated near-shoring of OEM supply chains is boosting domestic component shuttle lanes | +0.2% | National clusters | Medium term (2-4 years) |

| CEF2 funded intermodal terminals are creating extra first/last-mile trucking demand | +0.1% | National corridors | Long term (≥ 4 years) |

| Post drought capacity constraints on rail and barge networks have shifted seasonal agri-bulk flows onto roads | +0.1% | Agricultural regions | Short term (≤ 2 years) |

| Nationwide ITS deployment and digital documentation are raising fleet utilization | +0.1% | Country-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hungary’s Expanding Automotive and Electronics Export Base Intensifying Just-in-Time Road-Haulage Requirements

Automotive accounts for over one-quarter of Hungary’s manufacturing output, reinforced by BYD’s European headquarters and BMW’s new plant beginning series production in the second half of 2025[1]U.S. Department of Commerce, “Country Commercial Guide Hungary,” trade.gov . These facilities rely on high-frequency shuttle lanes that prioritize road over rail for component flows needing sub-24-hour lead times. The USD 167.7 billion merchandise-export tally in 2024 underlines the scale of precision logistics needed to keep assembly lines supplied. Dedicated carriers gain volume from temperature-controlled and time-sensitive electronics, while less-than-truck-load (LTL) networks capture incremental traffic created by lean inventory strategies. Dense corridors around Budapest, Debrecen, and Gyor allow route optimization systems to lift asset-utilization levels and mitigate driver-shortage risk.

Surging E-Commerce Parcel Activity in Budapest and Central Hungary Multiplying Middle-Mile and Urban LTL Movements

E-commerce gross merchandise value reached USD 2.77 billion in 2025, sharply increasing parcel density in the capital region[2] International Transport Forum, “Smart Urban Logistics Projects,” itf-oecd.org. Online retailers now prioritize two-hour to next-day delivery windows, pushing carriers to adopt load-pooling algorithms for middle-mile transfer between fulfillment hubs and micro-depots. Budapest’s smart loading-area pilots and dynamic vehicle-routing tools developed under EU urban-logistics programs enhance curb-side productivity and limit congestion fees. LTL providers benefit from multi-stop optimization that amortizes tolls and driver time over larger delivery maps. The resulting uptick in Hungary road freight transport market demand for smaller vans and rigid trucks fuels incremental fleet orders despite higher unit CAPEX.

Accelerated Near-Shoring of OEM Supply Chains Boosting Domestic Component Shuttle Lanes

Heightened geopolitical risk accelerates supplier relocation from distant locations to the Visegrád group. Hungary earmarked EUR 15.4 billion (USD 16.99 billion) for a decade-long rail upgrade to reinforce national manufacturing ecosystems and trim cross-border complexity. As inputs travel shorter distances, daily component shuttles between tier-1 suppliers and assembly plants grow in frequency, underpinning full-truck-load (FTL) corridors and fostering stable, contract-backed lane density. Single-market customs clearance simplifies scheduling and enables backhaul pairing, reducing empty-run kilometers and cushioning Hungary road freight transport market operators against rising toll outlays.

CEF2-Funded Intermodal Terminals Creating Extra First/Last-Mile Trucking Demand

Four green-field terminals financed through the EU’s Connecting Europe Facility Phase 2 will add more than 1.5 million TEU of rail throughput by 2027, led by the fully operational Fényeslitke East-West Gate hub. Intermodal transfers rarely negate the need for trucks; instead, they spawn first- and last-mile drayage contracts that elevate demand for 40-ft skeletal trailers, lift-gate rigid trucks, and container-chassis fleets. Operators that integrate rail and road visibility platforms position themselves to win high-frequency shuttles linking inland depots with automotive or consumer-goods warehouses scattered across Central Hungary.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| A persistent shortage of qualified drivers is inflating labor costs and limiting capacity growth | -0.4% | Country-wide, acute in rural zones | Long term (≥ 4 years) |

| HU-GO toll increases are compressing operating margins on main corridors | -0.2% | Core motorway network | Short term (≤ 2 years) |

| Euro-7 emission standards impose high cap-ex burdens on SME fleets | -0.2% | National; larger drag on SME fleets | Medium term (2-4 years) |

| Congestion on the M3/M35 motorways is eroding on-time performance and raising penalties | -0.1% | Eastern Hungary | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Qualified Drivers Inflating Labor Costs and Limiting Capacity Growth

Europe may face a 745,000-driver gap by 2028; Hungary mirrors this trend, where 31.6% of drivers exceed 55 years of age and only 6.5% are younger than 25[3]International Road Transport Union, “Driver Shortage Report 2024,” iru.org . Wage escalation, bonus schemes, and retention programs add direct operating expense, while unseated assets erode utilization. SMEs lacking human-resource scale are most exposed, accelerating consolidation toward well-capitalized fleets able to fund training and automation initiatives, such as assisted-driving retrofits aimed at improving work conditions.

HU-GO Toll Increases Compressing Operating Margins on Main Corridors

A 3.4% tariff adjustment effective January 2025 lifted Hungary’s distance-based road-user charges across the M0, M1, and M3 axes, raising the cost per km for both domestic and cross-border hauls. Carriers with route-planning analytics mitigate exposure, yet profitability headroom shrinks, particularly for low-margin bulk segments. Anticipated CO₂-indexed toll differentiation from 2026 further incentivizes accelerated fleet renewal toward Euro-6d and alternative-fuel drivetrains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Manufacturing Underpins Automotive Supply Chain Precision

Manufacturing held 30.62% Hungary road freight transport market share in 2025, sustained by USD 167.7 billion worth of automotive and electronics exports. The segment generates high-frequency FTL shuttle flows of components, engines, and finished vehicles that demand GPS-tracked curtain-side trailers and selective temperature control for sensitive electronics. Upskilling toward electric-vehicle power-train production expands demand for lithium-battery transport in ADR-compliant equipment. In contrast, wholesale and retail trade, enabled by e-commerce, GMV of USD 2.77 billion, expands fastest at 1.44% CAGR between 2026-2031 as omnichannel retailers migrate to hub-and-spoke networks. These dynamics shift resource allocation toward LTL vans fitted with barcode-linked proof-of-delivery apps.

Across lower-volume verticals, construction sustains flat yet steady traffic aligned to the EUR 15.4 billion (USD 16.99 billion) rail-modernization rollout; agriculture taps spot capacity during harvest peaks; and oil and gas retains specialized tanker demand despite rerouted energy imports. Each niche forces carriers to diversify equipment: walking-floor trailers for grain, flatbeds for steel, and pressurized tanks for refined fuels. As a result, the Hungary road freight transport industry relies on multi-commodity fleet strategies to preserve margin.

By Truckload Specification: FTL Dominance Faces Technology-Driven LTL Upswing

Full-truck-load services commanded 69.78% Hungary road freight transport market share in 2025, reflecting repetitive plant-to-plant moves. Large shippers lock in contract capacity, shielding carriers from spot-rate swings. However, LTL advances at 1.41% CAGR between 2026-2031 as cloud-based consolidation platforms match partial loads into optimized multi-drop tours. Algorithms dynamically group consignments that share delivery slots, tightening empty-space ratios and improving driver work-life balance through predictable regional loops.

FTL providers counter by adopting drop-and-hook trailer pools and predictive-maintenance sensors to retain service reliability. Yet expanding e-commerce triggers a structural flow toward pallet-level distribution, enhancing the strategic relevance of LTL within the Hungary road freight transport market.

By Containerization: Bulk-Driven Non-Containerized Strength as TEU Share Inches Up

Non-containerized cargo represented 87.42% share of the Hungary road freight transport market size in 2025 given the prevalence of grain, construction materials, and oversized machinery. Tipper, walking-floor, and low-bed trailers remain essential, particularly when Danube navigation limits or rail congestion redirect bulk volumes onto roads.

Meanwhile, containerized traffic grows at a 1.29% CAGR between 2026-2031, propelled by Fényeslitke’s remote-operated cranes and inland depots extending 45G connection to shipping lines. Operators offering tri-modal visibility suites win tenders from freight forwarders seeking single-invoice drayage.

By Distance: Long-Haul Backbone Meets Urban-Centered Short-Haul Expansion

Long-haul corridors absorbed 73.05% market share in 2025, leveraging Hungary’s central location to connect Vienna, Bratislava, and the Port of Koper with Balkan and Black Sea endpoints. These routes suffer most from driver scarcity and time-window penalties.

Short-haul flows, projected at 1.43% CAGR between 2026-2031, are driven by Budapest’s urban-consolidation centers and daily component shuttles under 200 km radius. Autonomous yard tractors and electric light-commercial vehicles gradually penetrate the short-haul niche, supported by municipal zero-emission-zone incentives.

By Destination: Domestic Corridor Density Meets Rising Cross-Border Momentum

Domestic freight retained a 63.72% share of the Hungary road freight transport market size in 2025 on the back of clustered industrial geography and EU customs-free movement. Dense loops linking Budapest, Debrecen, and Győr enable 2-turn daily cycles that heighten tractor productivity. Nevertheless, the international segment’s 1.61% CAGR between 2026-2031 underscores Hungary’s pivot toward an East-West gateway for Asian cargo redirected through new Silk Road alignments. Fleet operators refreshing tractors with comfortable cabs and digital tachograph upgrades compete more effectively for long-haul stages to Germany, Italy, and Romania.

Seasonal volatility still favors domestic specialization, yet cross-border carriers that combine bonded-warehouse services and customs brokerage capture incremental throughput amid geopolitical rerouting. This evolution keeps the Hungary road freight transport market versatile across intra-EU and broader Eurasian corridors.

By Goods Configuration: Solid Cargo Core vs. Specialized Fluid Opportunities

Solid goods accounted for 74.44% of the Hungary road freight transport market share in 2025, comprising everything from auto parts and white goods to parcel traffic. Carriers invest in load-securing automation and video-telematics to protect high-value electronics.

Fluid goods, projected at 1.37% CAGR between 2026-2031, include fuels, lubricants, dairy, and edible oils. ADR compliance, stainless-steel tank cleaning, and temperature-control linings elevate entry barriers, allowing specialized operators to command premium rates yet face higher equipment renewal costs under Euro-7.

By Temperature Control: Broad Dry-Cargo Base With Focused Cold-Chain Growth

Non-temperature-controlled freight captured a 94.12% share in 2025, as most manufactured and bulk commodities travel dry. Temperature-controlled flows expand at 1.39% CAGR between 2026-2031, reflecting Hungary’s meat-processing exports and vaccine logistics aligned to EU pharmaceutical distribution hubs.

Reefer carriers deploy real-time temperature trackers and door-sensor telemetry to maintain GDP compliance, creating a differentiated service tier within the broader Hungary road freight transport market.

Geography Analysis

Hungary’s central location keeps 63.72% of freight movements domestic, yet its strategic corridors enable consistent cross-border growth. Budapest sits at the confluence of TEN-T Core Network corridors and records the nation’s highest logistics land values, driven by e-commerce GMV of USD 2.77 billion that sustains final-mile demand. The surrounding Central Transdanubia and Northern Great Plain regions accommodate automotive tier-1 suppliers, forming dense FTL lanes that underpin fleet investments.

Eastern gateways gain prominence as Fényeslitke’s intermodal hub scales, allowing Ukrainian agribulk and Chinese overland containers to penetrate EU markets with one stop. Northern cross-border links via Bratislava and Vienna remain high-frequency due to synchronized production schedules between Hungarian assembly plants and Austrian component makers. Southern routes into Serbia and Romania absorb rerouted cargo while EU accession negotiations continue, providing growth headroom once customs formalities decline.

Rural counties leverage EU Cohesion Funds to modernize feeder roads, enabling higher weight limits and thus improving backhaul opportunities for regional carriers. Nonetheless, the HU-GO E-toll’s 3.4% uplift hits longer domestic stretches hardest, pressuring rate recalculations that ripple across the Hungary road freight transport market.

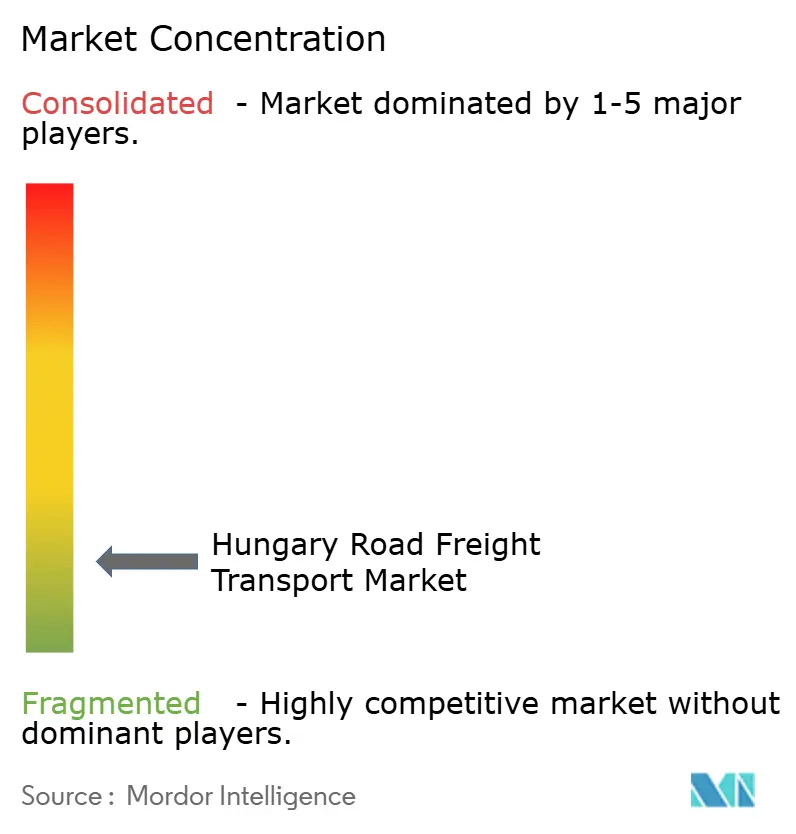

Competitive Landscape

The Hungary road freight transport market is highly fragmented. However, the top five to ten providers collectively hold a significant revenue share, leaving space for niche specialists. Waberer’s International operates nearly 3,000 tractors and 250,000 m² of warehousing, supported by proprietary AI-driven dispatch systems that lift the empty-km ratio below 10%[4]Waberer’s International, “Integrated Annual Report 2024,” waberers.co. Its 62.5% acquisition of GySEV Cargo in 2025 aims to fuse rail-road services and hedge against fuel-price volatility.

Multinationals such as DHL Freight and DSV capitalize on pan-European network density to offer guaranteed cross-border capacity and integrated customs brokerage. Domestic mid-caps target temperature-controlled and dangerous-goods haulage where skill scarcity discourages entry. Start-ups backed by venture capital deploy freight-matching platforms that aggregate SME carrier capacity, offering dynamic pricing to e-commerce shippers.

Regulatory costs and driver attrition hasten consolidation. Carriers able to finance Euro-7 tractor replacements and implement CO₂ telematics reporting are positioned to win tenders from automotive OEMs seeking Scope 3 emissions visibility. Technology adoption—digital proof-of-delivery, real-time truck-parking apps, and predictive maintenance—has become a primary competitive lever across the Hungary road freight transport market.

Hungary Road Freight Transport Industry Leaders

Waberer’s International Nyrt.

Trans-Sped Kft.

Revesz Group

DHL Group

Raben Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Waberer’s International acquired a 62.5% stake in GySEV Cargo to expand intermodal capabilities and integrate rail + road services.

- November 2024: Waberer’s International broke ground on a EUR 9 billion (USD 9.93 billion) logistics hub spanning 22,000 m² in Debrecen as the flagship site in a EUR 400 million (USD 441.45 million) national expansion that will add almost 100,000 m² of capacity by 2032.

- November 2024: Kuehne + Nagel enhanced its Hungary-wide LTL network for healthcare cargo by upgrading temperature-controlled facilities, introducing specialized handling protocols, and deploying advanced tracking to meet rigorous cold-chain regulations.

- July 2024: DHL Group reaffirms Hungary growth focus in its investor update, citing e-commerce parcel momentum.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Hungary's road freight transport market as all revenue earned inside the country from moving commercial cargo by motor vehicles, rigid trucks or tractor-trailers, whether full-truck-load or less-than-truck-load, containerized or bulk, temperature-controlled or ambient, across domestic and cross-border routes.

Scope Exclusion: Shipments executed by courier and parcel networks or foreign-registered hauliers are not counted.

Segmentation Overview

- End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- Destination

- Domestic

- International

- Truckload Specification

- Full-Truck-Load (FTL)

- Less than-Truck-Load (LTL)

- Containerization

- Containerized

- Non-Containerized

- Distance

- Long Haul

- Short Haul

- Goods Configuration

- Fluid Goods

- Solid Goods

- Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed fleet operators, shipper logistics heads, driver unions, and equipment dealers across Budapest, Győr, and Szeged, testing desk assumptions around load factors, average haul length, and contract rate inflation, and refining outlook ranges until responses converged.

Desk Research

We first built a fact base from open sources such as the Hungarian Central Statistical Office, Eurostat transport tables, UN Comtrade lane data, and logistics association white papers. We then added corporate filings and investor decks from leading carriers. Road-specific operating-cost trackers, HU-GO toll bulletins, and EU Mobility Package documents supplied price and regulatory markers that shape capacity and tariff moves. Paid libraries including D&B Hoovers for company revenues and Dow Jones Factiva for deal flow let us spot outliers and cross-check growth claims. This list is illustrative; many other public and subscription datasets fed the desk study.

Market-Sizing & Forecasting

A top-down demand pool was reconstructed from ton-kilometer output and average freight rates, which are then validated against a sampled bottom-up roll up of leading hauliers' revenues and truck counts. Key variables inside the model include the industrial production index, e-commerce parcel volume, diesel price trend, driver wage inflation, toll escalators, and fleet renewal rates. According to Mordor Intelligence, the current-year value forms the anchor point of the model. Long-run forecasts apply multivariate regression with scenario overlays to capture shifts in export demand and sustainability policies, while gaps in firm-level data are bridged with calibrated load-factor proxies.

Data Validation & Update Cycle

We run variance checks versus historical series, peer ratios, and fresh interview snippets before a senior analyst signs off. The file refreshes annually, with interim updates triggered by material events such as major toll hikes or emission mandates, ensuring clients receive the latest view.

Why Our Hungary Road Freight Transport Baseline Commands Reliability

Published estimates often diverge because firms slice the market differently and refresh models at unequal speeds.

Key gap drivers include whether courier volumes are folded in, how foreign-carrier revenues are treated, the aggressiveness of export-rebound assumptions, and currency conversion choices. Mordor fixes scope tightly on domestic hauliers and refreshes inputs each quarter, limiting drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.51 B | Mordor Intelligence | |

| USD 7.45 B | Global Consultancy A | Includes courier and parcel turnover, uses 2022 average euro rate |

| USD 13.80 B (2024) | Industry Journal B | Applies regional inflation uplift, does not isolate domestic haulier share |

These comparisons show that Mordor's disciplined scope selection and balanced model give decision makers a dependable, transparent baseline traceable to observable traffic, price, and capacity signals.

Key Questions Answered in the Report

What is the current size of the Hungary road freight transport market?

The market is valued at USD 4.57 billion in 2026 and is forecast to reach USD 4.86 billion by 2031 at a 1.24% CAGR.

Which end-user industry contributes most to Hungarian road freight demand?

Manufacturing, driven by automotive and electronics exports, accounts for 30.62% of national freight revenues.

How are driver shortages affecting carriers’ profitability?

With 31.6% of drivers older than 55 and a widening talent gap, carriers raise wages and invest in retention, squeezing profit margins and accelerating fleet consolidation.

What role do intermodal terminals play in future growth?

EU-funded terminals such as Fényeslitke generate first- and last-mile trucking contracts, supporting containerized-traffic CAGR of 1.29% through 2031.

Why is less-than-truck-load (LTL) service gaining traction?

E-commerce GMV of USD 2.77 billion fuels frequent, small-lot deliveries that suit LTL networks supported by route-optimization technology, yielding a 1.41% segment CAGR.

How will Euro-7 standards influence fleet investment?

Stricter emission limits from 2027 compel carriers to renew tractors or adopt LNG/EV alternatives, increasing CAPEX but unlocking lower CO₂-indexed toll rates.

Page last updated on: