Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.3 Billion |

| Market Size (2031) | USD 18.02 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

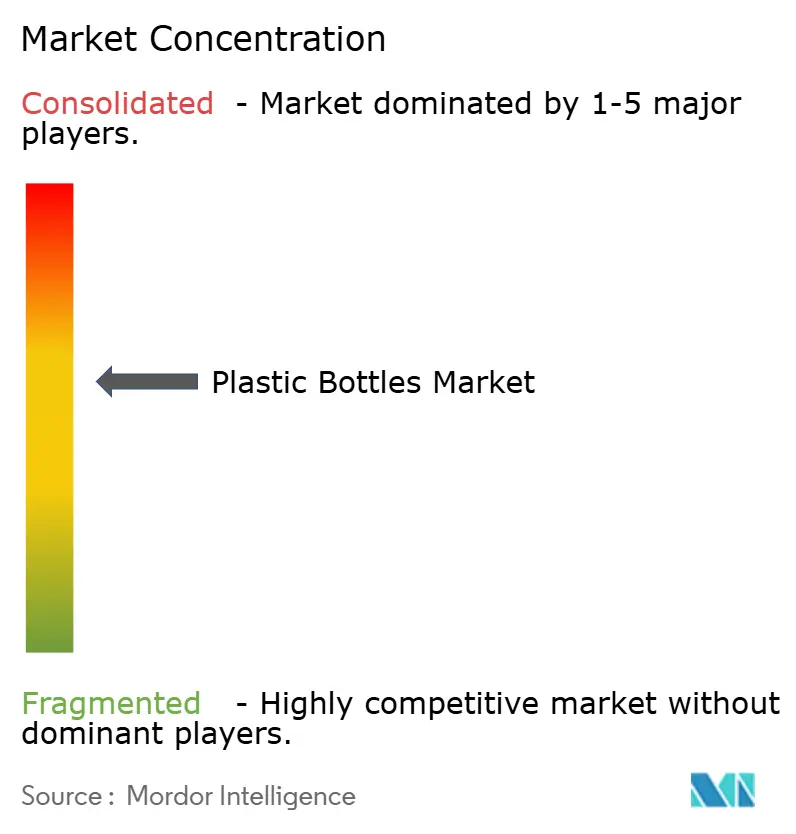

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Bottles Market Analysis by Mordor Intelligence

plastic bottles market size in 2026 is estimated at USD 15.3 billion, growing from 2025 value of USD 14.81 billion with 2031 projections showing USD 18.02 billion, growing at 3.32% CAGR over 2026-2031. Momentum persists because manufacturers continue to leverage lightweight designs, cost efficiency, and global supply chain scalability, even as regulatory and sustainability pressures mount. Demand escalates in beverage, pharmaceutical, and personal-care categories where shatter resistance, barrier performance, and portability remain core purchase drivers. A parallel wave of regulatory action, most notably single-use plastic taxes and tethered-cap mandates, accelerates investment in recycled PET (rPET) and advanced lightweighting technologies.[1]European Commission, “Single-Use Plastics Directive Implementation Report 2024,” ec.europa.eu Competitive intensity is shaped by brand commitments to circularity, surging e-commerce logistics needs, and steady capital inflows that fund capacity upgrades and acquisitions. Continuous process automation, real-time quality monitoring, and high-speed molding lines enable leading converters to protect their margins despite volatile resin prices and the rising costs of extended producer responsibility programs.

Key Report Takeaways

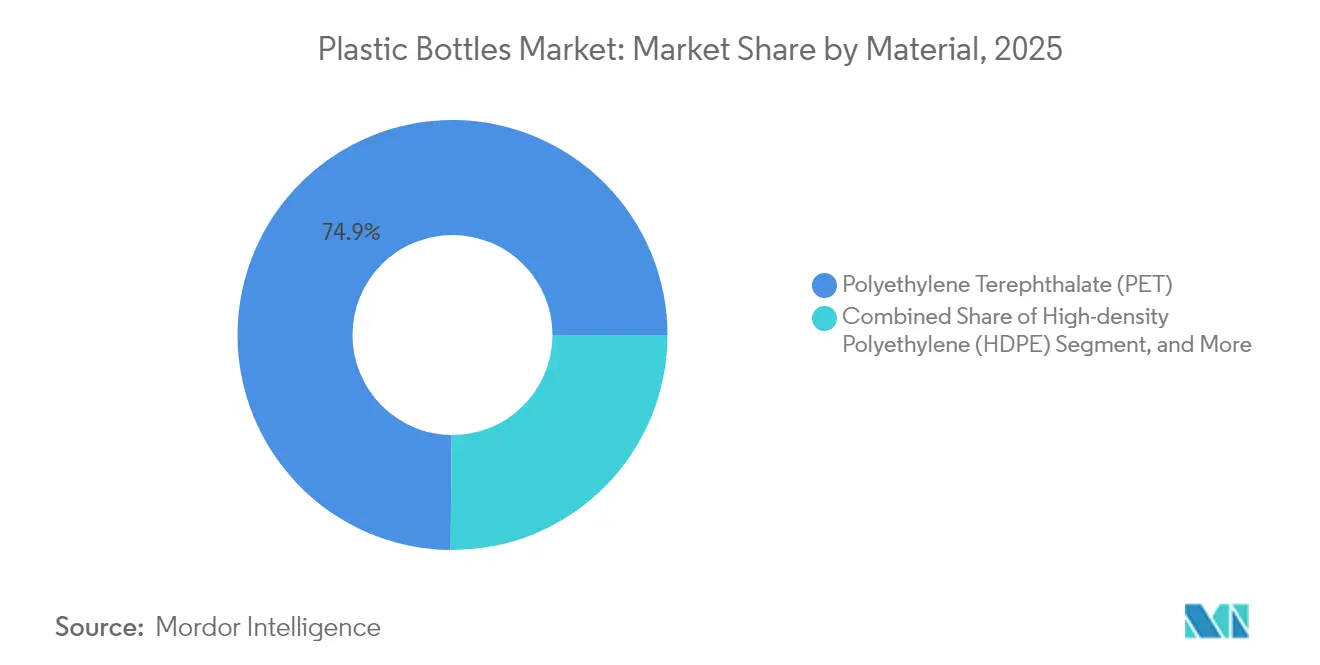

- By material, PET accounted for 74.86% of the plastic bottle market share in 2025, while bio-based PET posted the fastest expansion at a 4.03% CAGR through 2031.

- By manufacturing process, injection blow molding accounted for 47.55% of the plastic bottles market size in 2025, whereas extrusion blow molding recorded the highest growth at a 4.45% CAGR from 2025 to 2031.

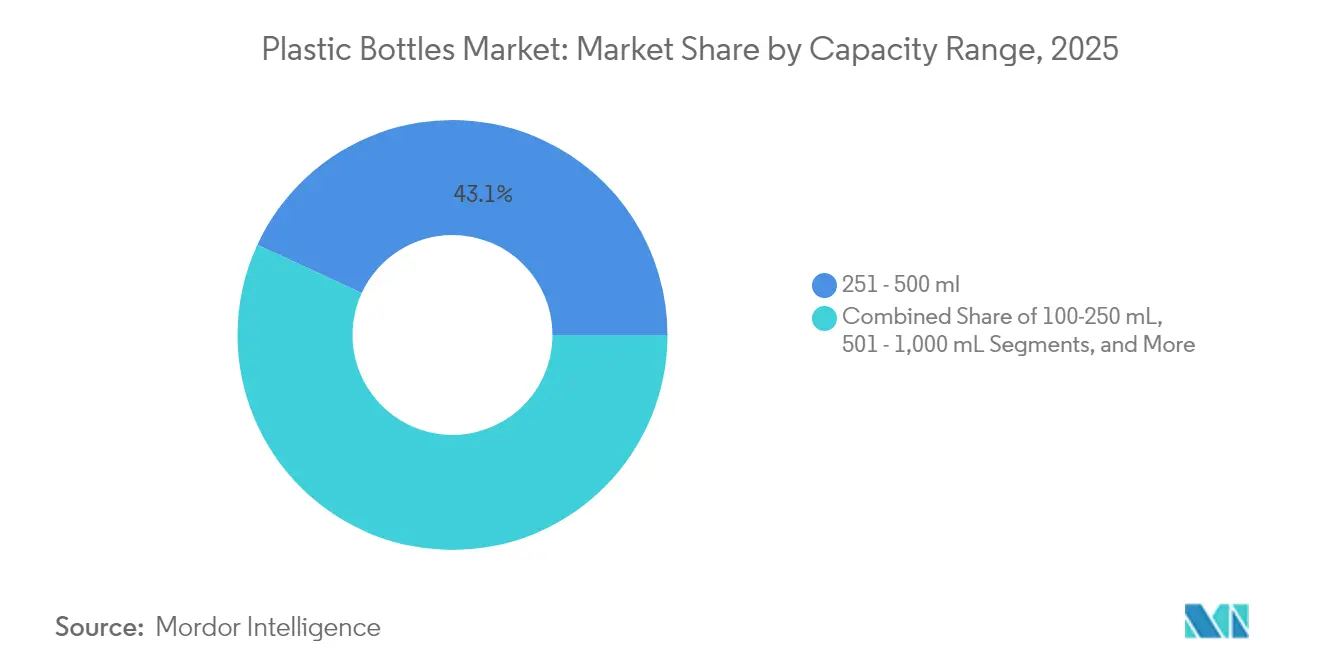

- By capacity, the 251-500 mL segment captured 43.10% share of the plastic bottles market size in 2025, and the 100-250 mL category is projected to advance at a 4.29% CAGR during the forecast period.

- By end-user, beverages led with 55.02% revenue share in 2025, while pharmaceuticals are forecast to expand at 4.11% CAGR through 2031.

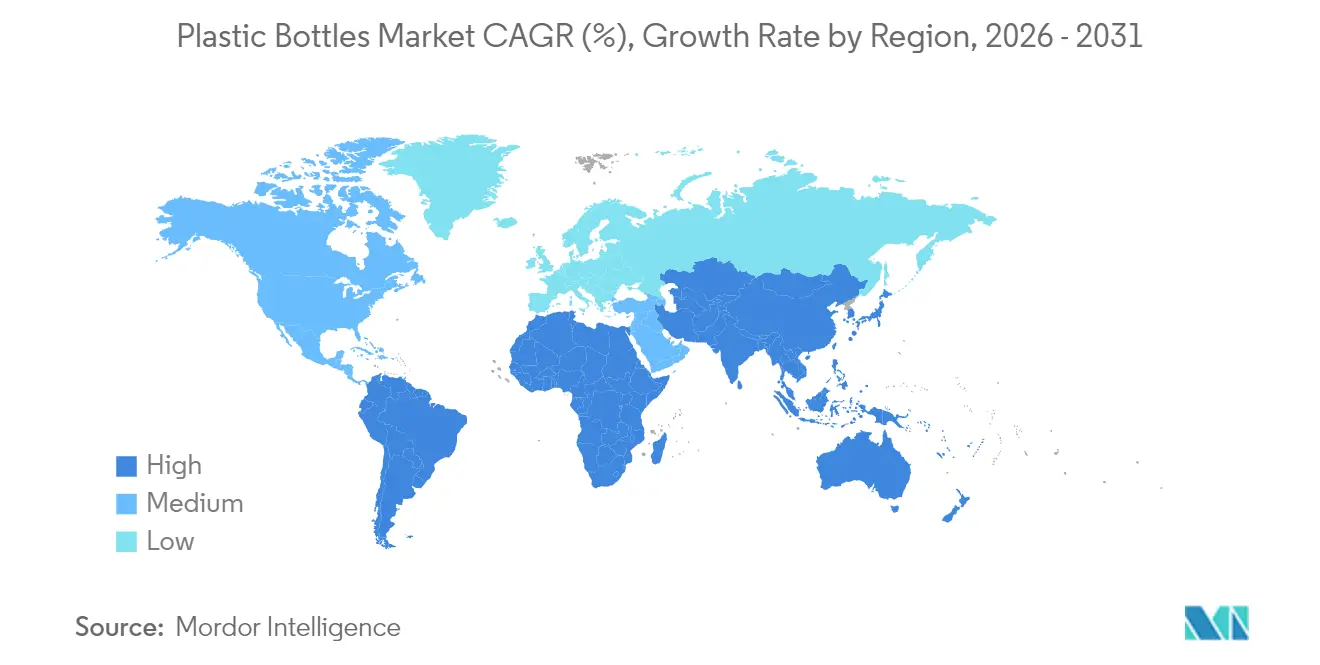

- By geography, the Asia Pacific accounted for 45.92% of the plastic bottles market share in 2025 and remains the fastest-growing region, with a 4.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plastic Bottles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for lightweight, shatter-resistant packaging | +0.8% | Global with stronger impact in Asia Pacific and North America | Medium term (2–4 years) |

| Cost advantage and scalability of PET/HDPE | +0.6% | Global, significant in price-sensitive markets | Long term (≥ 4 years) |

| Surge in e-commerce logistics | +0.5% | North America and Europe leading, Asia-Pacific catching up rapidly | Short term (≤ 2 years) |

| Brand circularity push for rPET | +0.4% | Europe and North America core, expanding to Asia Pacific | Medium term (2–4 years) |

| EU tethered-cap regulation-driven volumes | +0.3% | Europe primary, spillover globally | Short term (≤ 2 years) |

| Aseptic cold-fill for dairy alternatives | +0.2% | Global, early adoption in developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight, Shatter-Resistant Packaging

Weight-optimized PET bottles now come in 30% lighter than earlier versions yet maintain structural integrity, letting brand owners cut transport costs by as much as 15% per unit shipped. E-commerce amplifies the benefit because each gram saved lowers dimensional-weight charges and carbon footprints over long, parcel-based distribution routes. Continuous resin engineering enables thinner wall sections without compromising top-load strength, allowing for high-speed filling and reducing pallet weight in bulk channels. PlantBottle technology, which blends PET with 30% plant-derived content, illustrates how weight reduction and renewable feedstocks can coexist for mainstream beverage formats. Collectively, these advances keep the plastic bottles market competitive against glass and aluminum in logistics-intensive supply chains.

Cost Advantage and Scalability of PET/HDPE

Production economics remain compelling: PET and HDPE bottles cost 40-60% less per liter of capacity than aluminum and 70-80% less than glass. During the 2024 supply-chain disruptions, plastic converters restored normal output 3 times faster than glass producers, thanks to shorter furnace downtime and more flexible labor needs. New high-speed injection systems deliver 25% productivity gains and 15% lower kilowatt-hour consumption per bottle, easing operating-expense pressure even when crude-derived resin prices fluctuate. Scalable line changeovers allow contract packers to adjust quickly to SKU rotations tied to seasonal promotions, thereby reinforcing the dominance of the plastic bottles market across mass-volume consumer categories.

Surge in E-Commerce Logistics

Online retail triggers packaging redesign to survive multiple handoffs and automated fulfillment centers. Digital platforms report 40% lower breakage for plastic compared with glass containers over equivalent shipping distances. Consequently, brands reformulate packaging specifications to prioritize drop-test performance, side-wall crush resistance, and stack-height metrics over shelf-display aesthetics. The transition is especially intense in emerging economies where e-commerce infrastructure scales faster than brick-and-mortar retail. Amazon’s Frustration-Free Packaging certification incorporates performance criteria that favor PET and HDPE bottles, influencing upstream mold designs and resin choices among suppliers in the plastic bottle market.

Brand Circularity Push for rPET

Major beverage and personal-care companies have pledged to achieve 25-50% recycled content by 2030. Coca-Cola aims for 50% globally, and Danone has sold 100% rPET Evian bottles in several European countries.[2]Coca-Cola Company, “2024 Sustainability Report: Packaging Innovation and Circular Economy Progress,” thecoca-colacompany.com Recycled resin fetches a 10-15% premium over virgin feedstock; yet, brands absorb the surcharge for marketing benefits and regulatory compliance under extended producer responsibility rules. Stable demand signals unlock capital investment in advanced recycling, enabling the chemically depolymerization of PET for a near-virgin quality resin supply. Securing a rPET supply thus becomes a strategic imperative, driving joint ventures, long-term offtake contracts, and technology licensing in the plastic bottles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use-plastic bans and taxes | -0.7% | Europe leading, expanding globally | Short term (≤ 2 years) |

| Shift to aluminum and paper alternatives | -0.5% | North America and Europe primary | Medium term (2-4 years) |

| Volatile PCR resin supply | -0.3% | Global, acute in mandate regions | Short term (≤ 2 years) |

| Lightweight glass tech eroding weight edge | -0.2% | Premium segments in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Single-Use-Plastic Bans and Taxes

The European Union’s directive removed 2.3 billion bottles from circulation in 2024, while Germany’s 0.49 USD per kg plastic tax increased compliance costs and accelerated the adoption of recycled content. Canada and multiple U.S. states drafted comparable measures, complicating global SKU management and labeling requirements. Smaller converters feel disproportionate margin pressure because they lack the capital to retrofit lines or diversify into alternative substrates. Although phased timelines soften the short-term shock, the cumulative impact clips volume growth inside the plastic bottles market.

Shift to Aluminum and Paper Alternatives

Aluminum bottle volumes climbed 15% in 2024, piggybacking on premium energy-drink and water brands that target sustainability-minded consumers. Paper-bottle pilots from Paboco transitioned from the lab to a limited shelf rollout with Carlsberg and L’Oréal, demonstrating consumer acceptance in niche segments. A stark 2-3 times unit-cost gap versus plastic still constrains mass adoption; yet, lifestyle branding and deposit-return incentives keep migration options on the brand manager's agenda. The resulting substrate diversification siphons incremental demand away from the plastic bottles market in high-margin categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PET Dominance Drives Recycling Innovation

PET accounted for 74.86% of the plastic bottles market size in 2025, reflecting its performance balance of clarity, strength, and recyclability. HDPE is used for chemical-resistant household and pharma products, while LDPE serves squeezable formats and PP supports hot-fill needs. Bio-based resins such as PLA and PHA command premium pricing but gain traction under Europe’s renewable-content targets. Between 2026 and 2031, PET is projected to retain its leadership position, while bio-based blends are expected to log the highest CAGR, as brand owners pilot compostable solutions for niche use cases.

R&D collaborations proliferate: Danimer and PepsiCo advance PHA commercialization, and NatureWorks doubles PLA output to 150,000 tpa in its Thailand expansion. These moves expand material options, stimulate barrier-coating innovation, and reshape procurement strategies across the plastic bottles market.

By Manufacturing Process: Injection Molding Leads Despite Extrusion Growth

Injection blow molding captured 47.55 of % plastic bottles market share in 2025, owing to precision tolerance and surface-finish uniformity critical for pharma and cosmetics lines. Stretch-blow systems dominate the production of high-clarity beverage bottles, while extrusion blow molding, although only the second most popular by volume, is projected to grow at a 4.45% CAGR to 2031 due to its tooling flexibility and tolerance for recycled materials.

Industry 4.0 upgrades layer vision systems and predictive maintenance onto extrusion lines, minimizing downtime and scrap. Hybrid machines capable of both extrusion and injection operations facilitate shorter product-development cycles, supporting the agile SKU refreshes demanded by private-label retailers in the plastic bottles market.

By Capacity Range: Mid-Range Bottles Capture Consumer Preferences

The 251-500 mL bracket accounted for 43.10% of the plastic bottle market size in 2025, striking a balance between grab-and-go convenience and value. The 100-250 mL mini format exhibits a 4.29% CAGR, as on-the-go nutrition shakes and functional beverages continue to proliferate. Premium branding banks on smaller footprints to justify higher per-ounce pricing while reducing waste from unfinished servings.

Conversely, 501-1,000 mL SKUs support family consumption, and packs above 1 L remain crucial in institutional catering. Portfolio analytics are increasingly factoring in carbon impact per liquid ounce, prompting some brands to recalibrate their size mixes to optimize both consumer experience and sustainability KPIs within the plastic bottles market.

By End-User Vertical: Beverage Sector Leadership Amid Diversification

Beverages represented 55.02% of the plastic bottle market share in 2025, as carbonated soft drinks, bottled water, and RTD teas rely on PET for their shelf appeal and CO₂ retention. Pharmaceutical bottles, although smaller in volume, are expected to register a 4.11% CAGR due to the increasing demand for liquid-drug formulations, pediatric suspensions, and syrups that require barrier-enhanced PET.

Personal-care packaging features sophisticated shapes, tactile finishes, and post-consumer resin blends to reinforce brand storytelling centered on wellness. Meanwhile, food sauces and dressings are migrating to squeezable multilayer bottles that extend shelf life without the need for preservatives, thereby diversifying volume streams within the plastic bottles market.

Geography Analysis

The Asia Pacific held a 45.92% market share of the plastic bottles market in 2025 and is projected to grow at a 4.36% CAGR through 2031. China, accounting for more than half of the regional volume, leverages an integrated PET resin supply and cost-competitive labor to meet both domestic and export demand. India’s rapid adoption of e-commerce, combined with stricter food packaging laws, fuels double-digit unit growth, while Indonesia, Malaysia, and Thailand emerge as contract manufacturing nodes for multinational brand owners. Nations across the region are rolling out deposit-return schemes that stimulate post-consumer collection, yet they still lag behind European recovery rates.

North America displays maturity, but not as much innovation depth. The United States hosts advanced chemical recycling pilots and brand-led post-consumer resin offtake contracts that secure rPET feedstock. Canada’s federal single-use plastic ban accelerates substrate and design shifts, and Mexico leverages cost-advantaged conversion capacity that serves both domestic and export-oriented filling plants. Sustainability labeling and California’s 2024 minimum-recycled-content law compel supply-chain transparency and elevate recycled-resin pricing across the plastic bottles market.

Europe remains regulation-driven. Germany’s deposit system recovers more than 90% of PET, and tethered-cap rules drive mold and hardware upgrades. France intensifies PCR mandates, while Italy focuses on biodegradable products. The United Kingdom, post-Brexit, establishes parallel but divergent EPR fees that spur localized design tweaks. Central and Eastern Europe see capacity investment as converters chase lower utilities and labor expenses. Elsewhere, South America expands its penetration of packaged goods, while the Middle East and Africa markets anchor long-term prospects as urbanization and cold-chain infrastructure mature.

Regulatory Landscape

Regulation is tightening around recycled-content verification, labeling, and end-of-life responsibility for plastic packaging, with the European Union setting the main direction for global bottle specifications. Regulation (EU) 2025/40 (Packaging and Packaging Waste Regulation, PPWR) entered into force on 11 February 2025 and is due to apply generally from 12 August 2026, introducing compliance requirements that affect bottle design, labeling, and cross-border documentation.

For beverage bottles, the EU Single-Use Plastics Directive (EU) 2019/904 sets a minimum recycled content target of 25% by 2025 for PET beverage bottles, reinforcing demand for verified rPET and traceability systems. The European Commission adopted Commission Implementing Decision (EU) 2026/1425 on 30 June 2026, setting rules to calculate and verify recycled plastic content in single-use beverage bottles, including accounting approaches for chemical recycling outputs. In the United States, the EPA has elevated microplastics within federal water-policy activity, including adding microplastics as a priority contaminant group in the draft Sixth Contaminant Candidate List (CCL 6) under the Safe Drinking Water Act, which increases scrutiny on material choices and potential downstream impacts relevant to bottled beverage applications.

Competitive Landscape

The plastic bottles market is moderately fragmented, with the top five converters controlling about 45% of global volume. Amcor, ALPLA, and Graham Packaging combine worldwide footprints, proprietary lightweighting tech, and multi-year supply contracts with the largest FMCG firms. Amcor’s USD 8.43 billion acquisition of Berry Global’s rigid unit in October 2024 adds North American closures, boosting vertical integration and customer wallet share.

ALPLA’s USD 49 million Vietnam plant brings 1.2 billion bottles of annual capacity online, exemplifying the direction of capex toward Asia Pacific end-markets.[3]ALPLA Group, “Vietnam Manufacturing Facility Expansion Project,” alpla.com Graham Packaging’s pharma barrier PET breakthrough triples oxygen-shelf-life performance, safeguarding high-value liquid drugs and reinforcing premiumization. Private-equity ownership of medium-sized converters, such as Silgan’s acquisition of Weener Plastics for EUR 270 million (USD 293 million), underscores sustained deal appetite and the search for closures and dispensing.

Strategic themes center on weight reduction, scaling of recycled content, and digital traceability. Proprietary resin blends and design-for-recycling guidelines align with brand owner scorecards. Emerging disruptors invest in smart bottles that embed QR codes and NFC chips for authentication and refill programs. Combined, these vectors influence price realization, customer lock-in, and margin resilience across the plastic bottles market.

Plastic Bottles Industry Leaders

Gerresheimer AG

Amcor plc

ALPLA Werke Alwin Lehner GmbH & Co KG

Grief, Inc.

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven demand for verifiable recycled content creates opportunities in certified rPET supply, chain-of-custody systems, and packaging designs that can help reduce EPR fees while improving sortability. The European Commission Implementing Decision (EU) 2026/1425 (30 June 2026) formalizes how recycled plastic content is calculated and verified for single-use beverage bottles, pushing brand owners and converters toward auditable mass-balance and documentation processes. That emphasis also raises the bar for bottle supply where chemical recycling is part of the recycled-content strategy, benefiting material suppliers and bottle converters that can provide certified inputs, traceable documentation, and design-for-recycling compatibility aligned with EU packaging labeling and PPWR implementation timelines.

Capacity and technology investments across resin and packaging footprints support near-term opportunity in localized supply for beverage and pharma bottles, with a particular focus on Asia and adjacent manufacturing hubs. In April 2026, thyssenkrupp Uhde signed a contract with KOKSAN for a 324,000 tons/year low-emission polyester plant in Yumurtalik, Turkey, signaling continued investment in PET value chains that can support bottle-grade material availability. In July 2026, Amcor announced an expansion of a packaging facility in China, consistent with Asia Pacific's leading share of plastic bottle demand and the shift toward added capacity close to end markets. Meanwhile, rising recycled-content mandates in large markets, including India (Plastic Waste Management Rules requiring 30% recycled content for rigid packaging in 2025-2026), expand the addressable market for domestically compliant bottle designs, qualified recycled feedstock, and production lines that can run higher PCR blends while meeting performance needs in beverages and pharmaceuticals.

Recent Industry Developments

- July 2026: Amcor announced an expansion of a packaging facility in China. The company added regional manufacturing capability closer to Asia-Pacific demand centers, helping shorten lead times for brand owners managing fast SKU rotations and sustainability-driven material changes.

- June 2026: The European Commission adopted Implementing Decision (EU) 2026/1425 setting rules to calculate and verify recycled plastic content in single-use beverage bottles. Standardized verification and accounting increase the value of traceable rPET and documented recycled-content claims, shaping procurement and quality-control requirements for PET bottle supply.

- October 2024: Amcor announced the acquisition of Berry Global’s rigid packaging business for USD 8.43 billion. The transaction expanded its global rigid bottle and container capabilities and strengthened scale and portfolio breadth in bottles and closures, reinforcing its position with large FMCG customers seeking integrated packaging partners.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the plastic bottles market covers rigid plastic bottles used as primary packaging for consumer and industrial products, counted when they are produced and sold as bottles (empty or supplied with filled goods, depending on the data source boundary).

Scope exclusions: Excluded from this sizing are flexible pouches, paper or glass bottles, and caps, closures, labels, and secondary packaging like trays and cartons.

Segmentation Overview

- By Material

- Polyethylene Terephthalate (PET)

- High-density Polyethylene (HDPE)

- Low-density Polyethylene (LDPE)

- Polypropylene (PP)

- Bio-based and Compostable Plastics

- Other Materials

- By Manufacturing Process

- Extrusion Blow Molding

- Injection Blow Molding

- Stretch Blow Molding

- Other Manufacturing Processes

- By Capacity Range

- Less than 100 mL

- 100 - 250 mL

- 251 - 500 mL

- 501 - 1,000 mL

- More than 1,000 mL

- By End-user Vertical

- Beverages

- Food

- Cosmetics and Personal Care

- Pharmaceuticals

- Household Care

- Other End-user Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Malaysia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand context and the rules for what counts as a bottle in value terms. We reviewed public manufacturing and plastics indicators from sources such as the UN Comtrade database, national statistical agencies, and customs or tariff classification notes used for bottles and similar plastic articles.

To keep the model grounded, we also referenced material and packaging signals from sources such as the US EPA and Eurostat (for recycling and packaging waste policy indicators), plus trade associations and peer-reviewed packaging journals for lightweighting, rPET adoption, and bottle format shifts. Company annual reports, investor presentations, and earnings commentary were used to understand capacity additions, price pass-through language, and mix changes. Where needed, paid subscriptions for company financials and intelligence, patent databases, and an import/export shipment-level database were used to sanity check directionally. The sources listed here are illustrative, and many other public documents and datasets were also used for validation and clarification.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys across bottle manufacturers, resin and preform participants, converters, and downstream buyers in beverages, food, personal care, and pharmaceuticals. We used these discussions to stress test pricing logic tied to resin and utilization changes, substitution toward alternative packaging, and then to confirm regional differences in demand and the timing of regulatory implementation.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 20% | APAC: 49% |

| Mid tier: 44% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 22% | Managers: 50% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production, trade, and packaging consumption signals are used to reconstruct the bottle demand pool by region, and then translated into value using blended price bands. Once the totals are formed, they are corroborated with selective bottom-up approximations such as sampled supplier revenue cross-checks, a few channel checks on common bottle formats, and indicative ASP times volume math for high-use end markets.

Key inputs that move the model include resin price trends for PET, HDPE, and PP, rPET content targets that shift material mix and cost, beverage and packaged food output indicators, pharmaceutical and personal care volume signals, and manufacturing utilization direction (which impacts realized pricing). Forecasting uses scenario analysis, where the base case is shaped by expert views on regulation pace, recycled-content availability, and expected price pass-through, followed by adjustments for macro demand softening or rebound periods. When bottom-up visibility is weaker in smaller countries, gaps are handled through proxying with trade intensity, per-capita packaged beverage consumption, and local price levels, and then rechecked with regional interview feedback.

Data Validation & Update Cycle

Validation is done through repeated triangulation across independent signals, so one dataset does not drive the final number. We compare model outputs against trade flows, packaging waste and recycling indicators, and company level commentary, and then flag sharp variances for review before sign-off.

Outliers are investigated by checking currency timing, inflation effects on price, and sudden mix shifts across end uses and bottle sizes. When a material event happens, such as a major regulation change, resin supply shock, or capacity start-up, we re-contact selected respondents to confirm direction and magnitude. Reports are refreshed annually, and interim updates are made when market-moving events occur, with a final pre-delivery pass to make sure clients receive the latest updated view.

Mordor Intelligence's Plastic Bottles Market Sizing Compared With Other Published Estimates

Published market values for plastic bottles can look far apart, even when they are talking about the same packaging item, because each publisher draws the line around scope and pricing in their own way. Differences usually come from whether the study counts bottles only or bundles adjacent plastic packaging, and whether values reflect producer pricing, wholesale pricing, or downstream retail pricing.

The benchmark table shows a much smaller total than some broad packaging reads, and in Mordor Intelligence's model, the value is kept specific to plastic bottles by resin and end-use, rather than being expanded to include wider plastic containers or full packaging system costs, which can inflate the reported size. Another driver is timing and currency, since some sources apply nominal wholesale pricing and longer-horizon assumptions, while others keep nearer-term pricing logic tied to current resin trends and validated utilization changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.30 B (2026) | |

| Trade Data Publisher A | USD 134.90 B (2024) | Uses a broad trade category for bottles and similar plastic articles and reports value at nominal wholesale prices, which can include wider container groupings and price bases not aligned to bottle-only producer economics. |

| Global Consultancy B | USD 111.60 B (2025) | Often reflects a wider packaging scope with larger end-use coverage and longer forecast framing, and it can apply different ASP progression assumptions that do not separate bottle formats and resin mix changes in the same way. |

Taken together, the spread is mainly explained by what is counted as a bottle market and which price layer is used for valuation. Our approach stays traceable to clear levers like resin-linked pricing, end-use demand indicators, and regional trade and production signals, which makes the estimate easier to reproduce and update when conditions change.

Key Questions Answered in the Report

What is the current value of the plastic bottles market?

The plastic bottles market size reached USD 15.3 billion in 2026.

How fast is demand for rPET bottles growing?

Recycled-content bottles benefit from brand commitments that push rPET volumes at a 4.03% compound rate through 2031.

Which region leads the consumption of plastic bottles?

Asia Pacific holds 45.92% of global volume and remains the fastest expanding geography.

Which capacity range sells the most units?

Bottles between 251-500 mL account for 43.10% of global demand due to a preference for portion control.

How are regulations shaping material choices?

Single-use plastic taxes and tethered-cap mandates in Europe and North America accelerate the adoption of lightweight and recycled PET formats.

Who are the top companies?

Amcor, ALPLA, and Graham Packaging lead in scale, technology, and global customer relationships within the plastic bottles market.

Page last updated on: