Plasma Etching Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.34 Billion |

| Market Size (2031) | USD 20.42 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

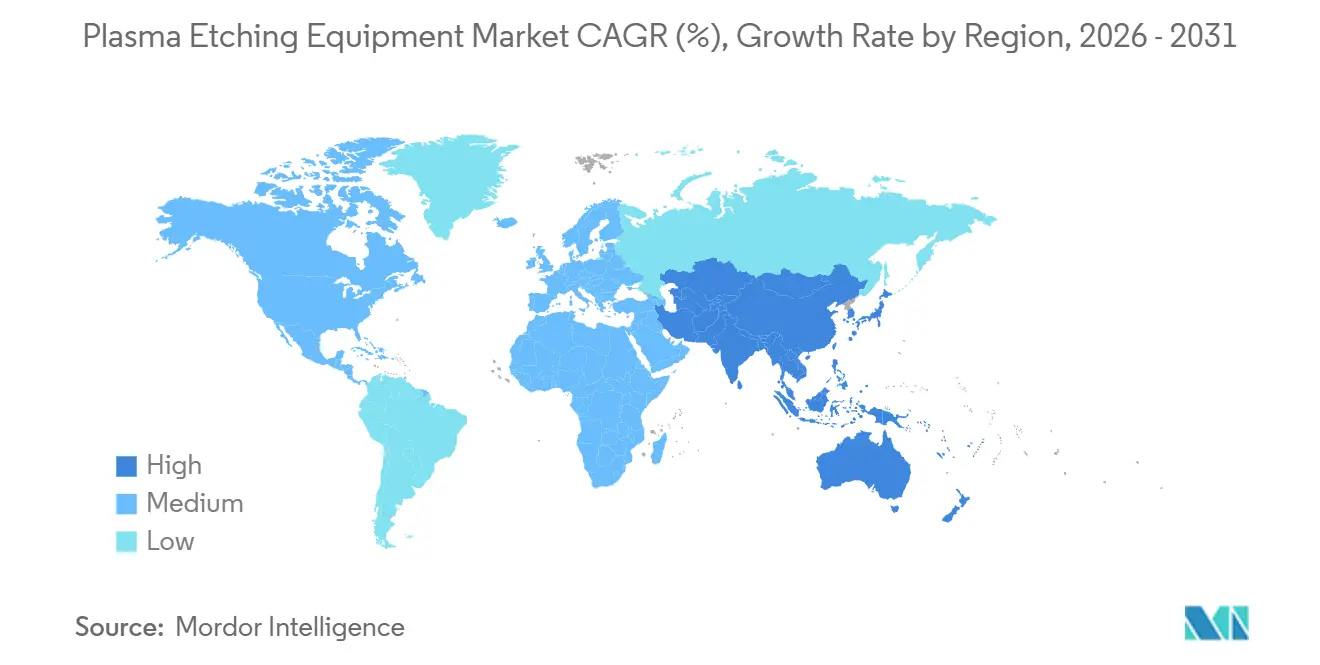

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

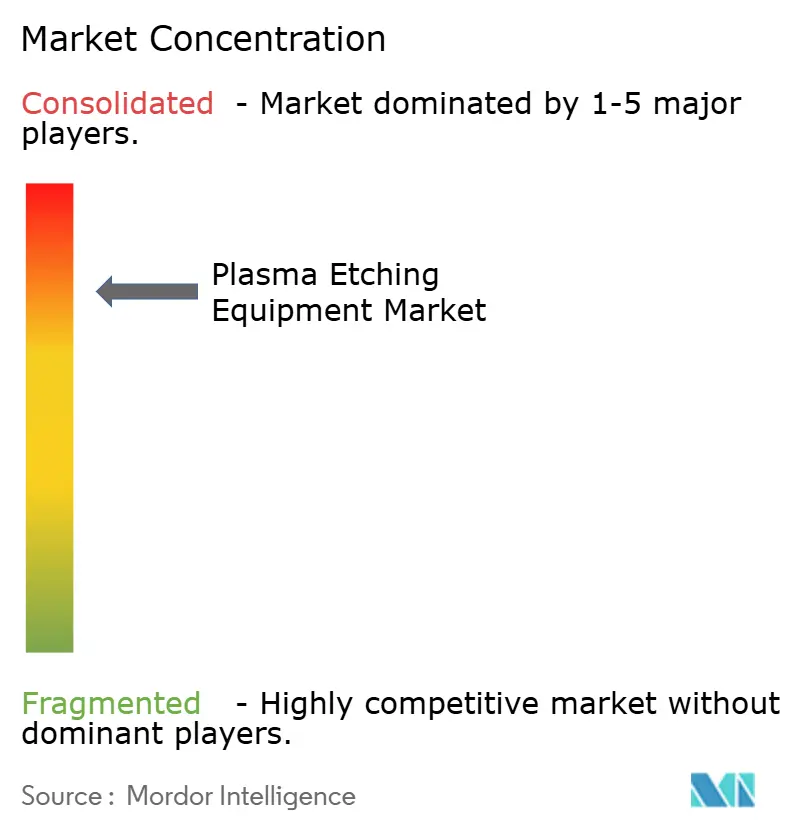

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plasma Etching Equipment Market Analysis by Mordor Intelligence

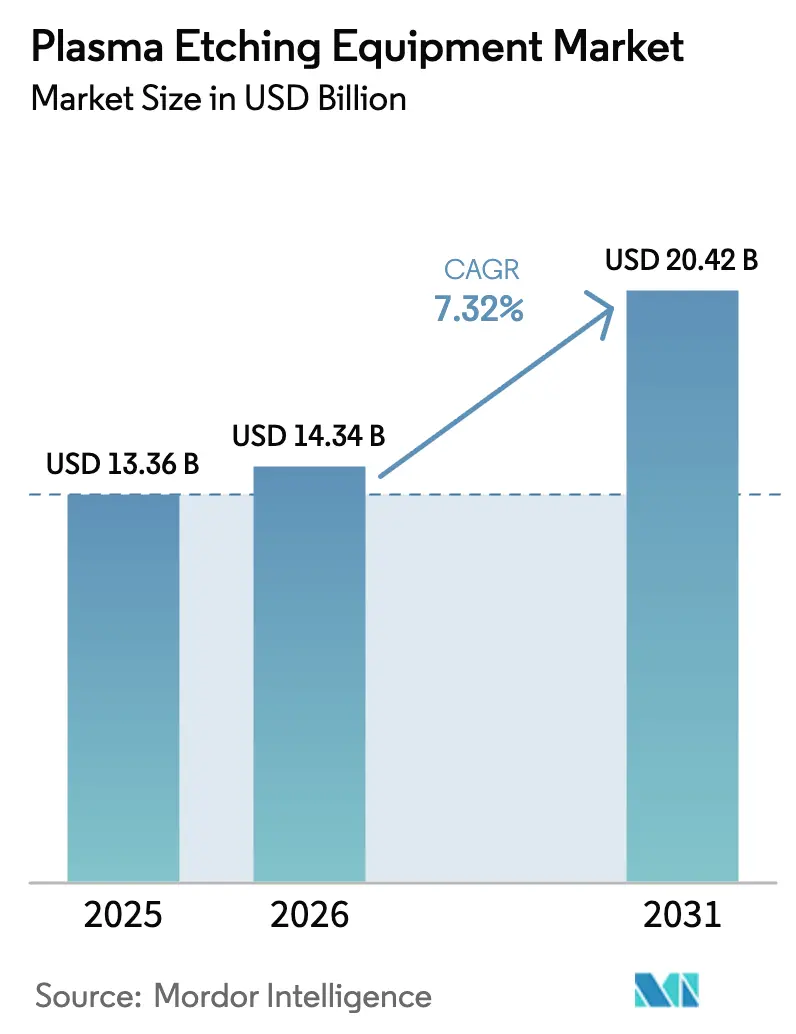

The Plasma Etching Equipment Market size is projected to be USD 13.36 billion in 2025, USD 14.34 billion in 2026, and reach USD 20.42 billion by 2031, growing at a CAGR of 7.32% from 2026 to 2031.

Demand is scaling as extreme ultraviolet lithography migrates into 3 nm production and 3-dimensional memory architectures surpass 200 vertical layers, both of which require aspect-ratio control beyond 100:1. Inductively coupled plasma tools dominate because their low-pressure, high-density plasmas protect fragile gate dielectrics while sustaining vertical sidewalls. Deep reactive ion platforms are gaining momentum, particularly through-silicon via formation for advanced packaging, and atomic layer approaches are transitioning from pilot lines to volume production. Government incentives in the United States, European Union, Japan, and South Korea are accelerating tool orders, while silicon carbide and gallium nitride adoption in electric vehicles and 5G infrastructure is diversifying material needs.

Key Report Takeaways

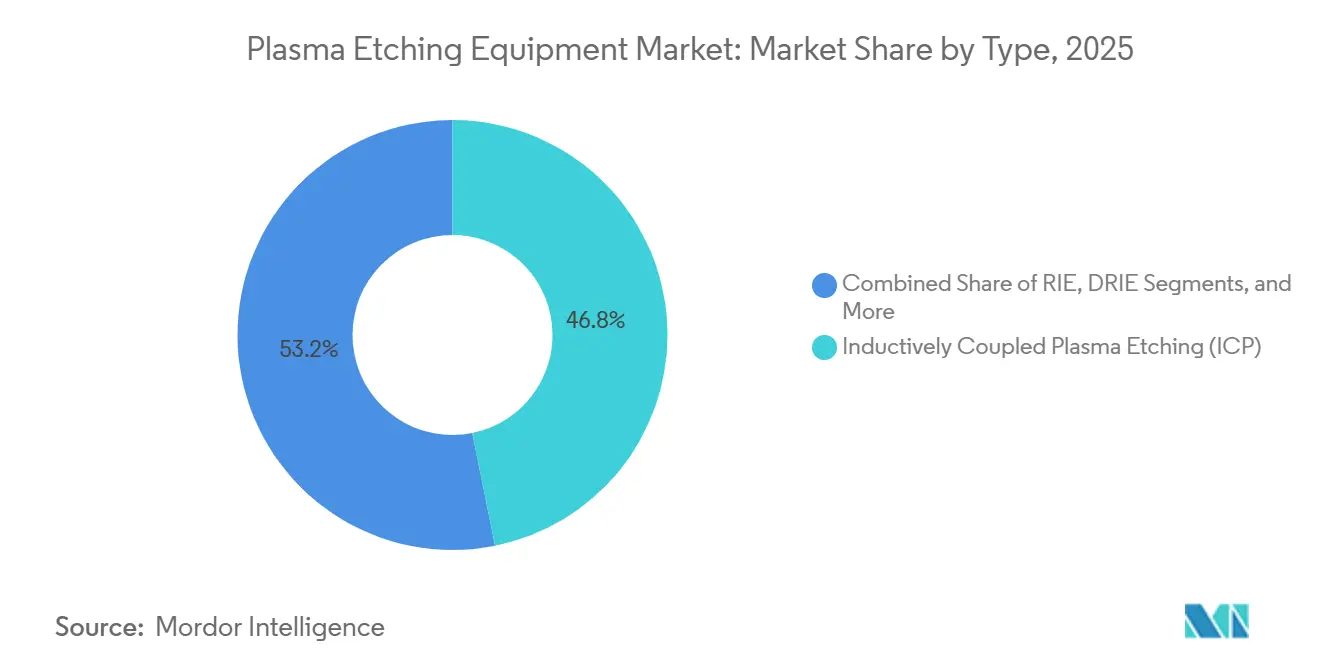

- By type, inductively coupled plasma systems commanded 46.83% of 2025 revenue, while deep reactive ion technology is on track to post a 7.99% CAGR through 2031.

- By wafer size, the 300 mm format secured 51.73% revenue share in 2025 and above-450 mm is projected to expand at 8.33% as cost-per-die considerations intensify.

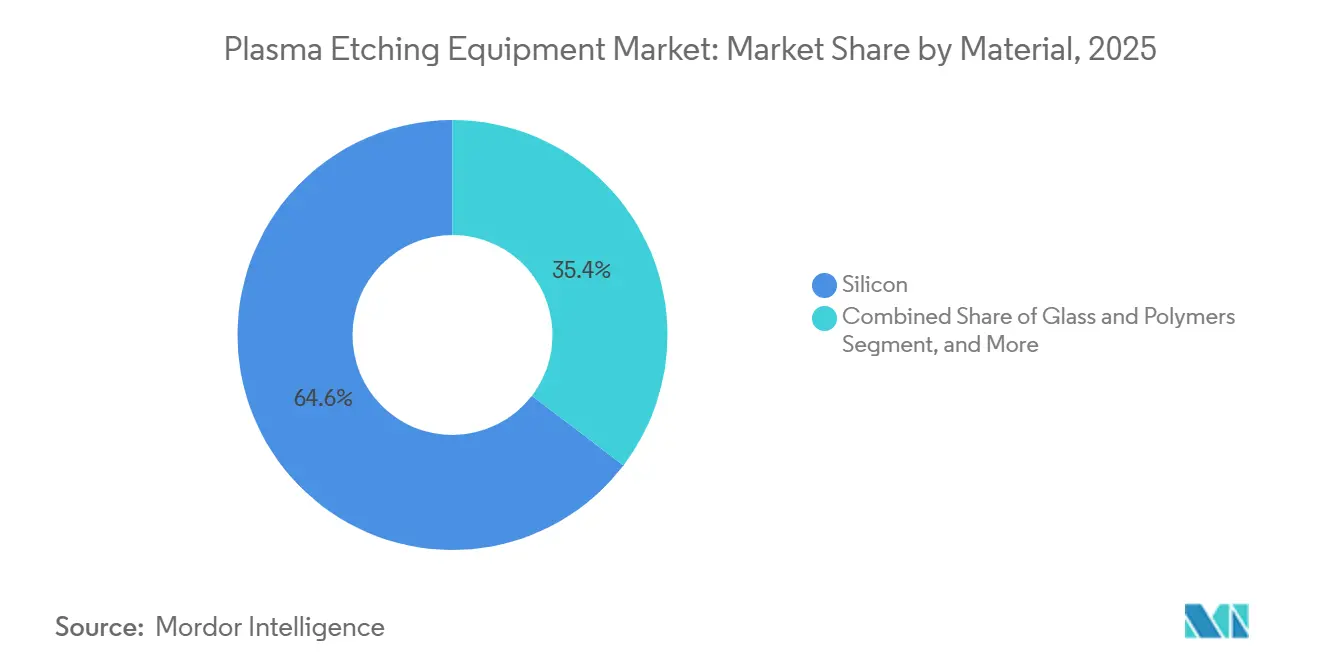

- By material, silicon captured 64.63% demand in 2025 whereas compound substrates are forecast to grow 8.56% annually on rising silicon carbide and gallium nitride use.

- By application, consumer electronics led with 38.61% revenue share in 2025; automotive electronics is expected to log a 7.88% CAGR to 2031 on electrification tailwinds.

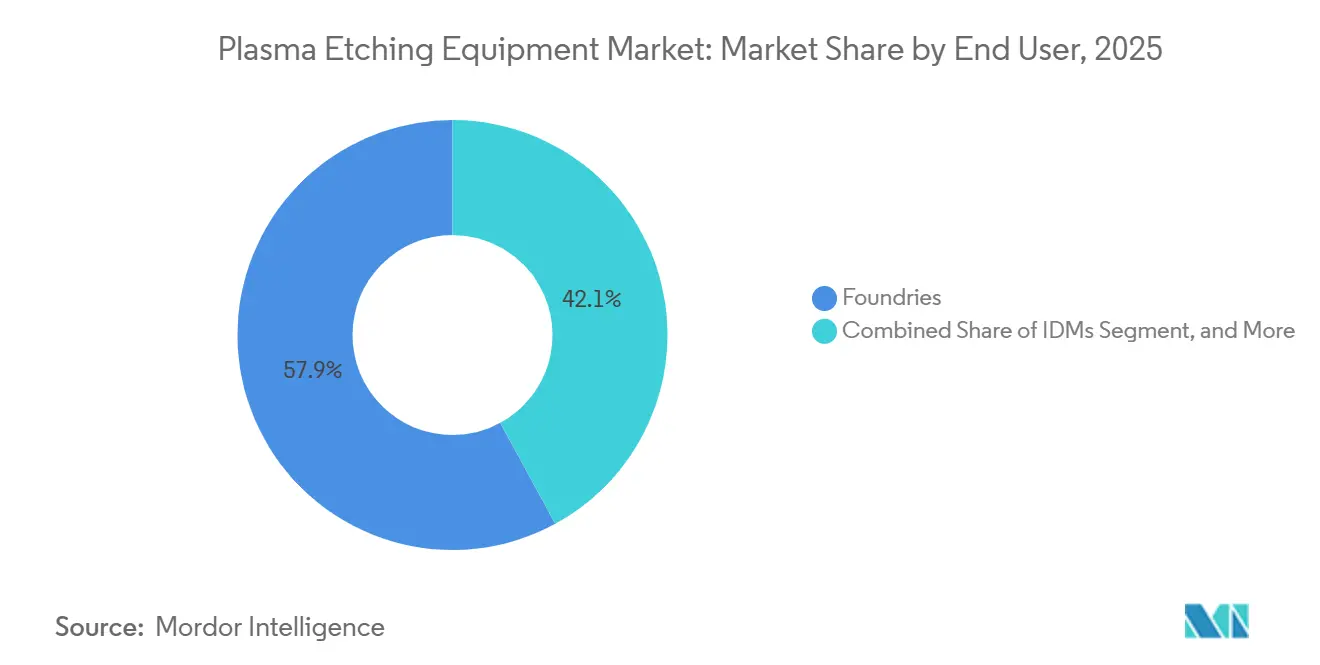

- By end user, foundries held 57.94% of 2025 spending and are set to deliver an 8.51% CAGR through 2031 as fabless design houses increase outsourcing.

- By geography, Asia-Pacific generated 55.72% of 2025 revenue and is on course for an 8.66% CAGR through 2031 owing to capacity additions in Taiwan, South Korea, Japan, and China.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plasma Etching Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of EUV Lithography Driving High Aspect-Ratio Etch Requirements | +1.8% | Asia-Pacific core, North America and Europe leading-edge fabs | Medium term (2-4 years) |

| Proliferation of 3D NAND and DRAM Node Shrinks | +1.6% | Asia-Pacific (South Korea, Japan, China), selective North America | Medium term (2-4 years) |

| Growing Demand for Compound-Semiconductor Power Devices | +1.4% | Global, with concentration in Europe and Asia-Pacific automotive hubs | Long term (≥ 4 years) |

| Government-Backed Chip Sovereignty Programs (US CHIPS Act, EU Chips Act) | +1.3% | North America and Europe, spillover to allied nations | Short term (≤ 2 years) |

| Shift Toward Heterogeneous Integration and Advanced Packaging | +1.0% | Global, led by Asia-Pacific foundries and North America design houses | Medium term (2-4 years) |

| Emerging Use in Quantum Computing Device Fabrication | +0.3% | North America and Europe research clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of EUV Lithography Driving High Aspect-Ratio Etch Requirements

Extreme ultraviolet lithography transitioned from pilot lines to high-volume manufacturing at the 3 nm node in 2025 and is slated for adoption at the 2 nm node by 2027. Each EUV step increases etch intensity because contact holes, vias, and gate spacers now require aspect ratios exceeding 120:1, with critical dimensions below 10 nm.[1]ASML, “Q1 2025 Results,” asml.com ASML shipped 20 EUV scanners in Q1 2025, a 33% year-over-year increase, and every scanner is paired with multiple inductively coupled plasma chambers. IBM validated nanosheet transistors that require 14 separate etch steps per gate stack, doubling complexity over finFET nodes.[2]IBM Research, “2 nm Chip Technology,” ibm.com Capital outlays for etch tools consequently rose to 18-22% of total fab spending in 2025. Tool makers are embedding real-time endpoint spectroscopy to suppress micro-trenching, and fabs are revising recipe libraries to execute ultra-low bias processes that cut sidewall bowing to within 1 degree.

Proliferation of 3D NAND and DRAM Node Shrinks

Samsung disclosed a 286-layer vertical NAND product in 2024 that necessitates etch depths exceeding 15 µm with sub-2-degree taper, magnifying demand for deep reactive ion equipment calibrated to mitigate aspect-ratio-dependent lag.[3]Samsung Electronics, “286-Layer V-NAND Announcement,” samsung.com SK Hynix adopted atomic layer etching to protect high-k dielectrics in its 1-alpha-nm DRAM, launched in 2025. Meanwhile, cryogenic processes cooled below 0 °C are being qualified to improve selectivity between silicon oxide and nitride. SEMI estimated memory companies spent USD 45 billion on capital equipment in 2025, 20% of which was devoted to etch platforms.[4]SEMI, “World Fab Forecast 2025,” semi.org High layer counts in 3D NAND and shrinking capacitor pitches in DRAM will keep etch process steps rising each year through 2031.

Growing Demand for Compound-Semiconductor Power Devices

Silicon carbide and gallium nitride power devices migrated to 200 mm and 300 mm wafers in 2025, driving a new wave of equipment capable of handling chemically inert substrates at temperatures exceeding 400 °C. Infineon ramped a 300 mm silicon carbide line in Malaysia with goals to halve cost per ampere by 2027. Onsemi announced a 300 mm silicon carbide fab in the Czech Republic to enter volume production in late 2026, further broadening the customer base for high-temperature plasma chambers. Electric vehicles are forecast to incorporate USD 1,200 of semiconductor content per unit by 2030, with power devices accounting for approximately 30% of that value, thereby elevating compound substrates as a growth engine.

Government-Backed Chip Sovereignty Programs

The United States CHIPS and Science Act, the EU Chips Act, and analogous incentives in Japan and South Korea collectively exceed USD 100 billion and are compressing fab construction timelines. Intel’s Ohio site broke ground in September 2024 following USD 8.5 billion in U.S. grants, and etch tool move-in is scheduled for the second half of 2026. Taiwan Semiconductor Manufacturing Company’s Arizona project secured USD 6.6 billion in direct funding and advanced its second fab start date to 2027. The European Union allocated EUR 43 billion (USD 46.7 billion) with the aim of doubling regional chip output by 2030. These incentives guarantee near-term tool orders and require domestic service hubs, prompting Applied Materials and Lam Research to expand spare-parts depots in Arizona and Saxony.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plasma-Induced Damage in Sub-5 nm Structures | -1.2% | Global, concentrated in leading-edge fabs (Asia-Pacific, North America) | Short term (≤ 2 years) |

| Rising Clean-Room Construction and Utility Costs | -0.9% | North America and Europe, moderate impact in Asia-Pacific | Medium term (2-4 years) |

| Supply Chain Volatility for High-Purity Specialty Gases | -0.7% | Global, acute in regions with limited domestic gas production | Short term (≤ 2 years) |

| IP Restrictions Limiting Equipment Exports to China | -0.6% | China primary impact, secondary effects on global equipment utilization | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plasma-Induced Damage in Sub-5 nm Structures

Lattice defects, charge accumulation, and interface roughness caused by ion bombardment during etch steps cut drive current and shift threshold voltage when the gate oxide thickness approaches 1 nm. Atomic layer etching reduces damage but triples the cycle time, thereby increasing the cost per wafer. Tokyo Electron’s latest atomic layer platform removes 0.5 nm per cycle but requires approximately 200 cycles to clear a 10 nm trench, compared to 30 seconds for a continuous plasma etch. Fabs are therefore limiting atomic layer methods to the most sensitive layers while accepting controlled damage in less critical regions.

Rising Clean-Room Construction and Utility Costs

Leading-edge fabs in the United States and Europe cost USD 20 billion or more, roughly double Asia-Pacific equivalents, driven by labor scarcity, environmental permitting, and higher energy tariffs. Intel’s Ohio investment estimate rose from USD 20 billion to USD 28 billion by mid-2025 as steel and specialized clean-room material prices climbed. Utility costs, especially electricity, remain 40-60% higher than in Taiwan or South Korea, extending payback periods from five to seven years and pushing some integrated device manufacturers to slow expansion schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Inductively Coupled Plasma Leads While Deep Reactive Ion Accelerates

Inductively coupled plasma platforms generated the largest plasma etching equipment market size contribution at 46.83% in 2025. Their capacity to decouple ion energy from plasma density lets fabs fine-tune anisotropy and protect fragile fins and nanosheets. Deep reactive ion equipment, projected to grow at a 7.99% CAGR through 2031, is key for through-silicon vias and wafer-level packaging that require depths of 50-100 µm at aspect ratios of greater than 20:1, thereby expanding the plasma etching equipment market share held by this segment. Conventional reactive ion tools remain in demand at mature nodes but are gradually migrating toward trailing-edge foundry lines.

Lam Research’s Sense.i platform employs machine learning for real-time bias adjustments that have raised yield by roughly 3 percentage points in contact-hole etch since 2025. Applied Materials added in-situ metrology to its Centris Sym3 to cut chamber-to-chamber variation below 0.3 nm, a necessity for 2 nm gate-all-around transistors. This convergence of plasma and data science is blurring legacy boundaries between tool categories and intensifying supplier competition.

By Wafer Size: 300 mm Stays Core, Above-450 mm Gains Momentum

The 300 mm format accounted for 51.73% of 2025 demand, anchoring the plasma etching equipment market size because Taiwan Semiconductor Manufacturing Company, Samsung, and Intel collectively ran more than 50 fabs on this diameter. Above-450 mm pilot work is picking up, and the segment is predicted to grow at 8.33% through 2031 as industry consortia revisit economies of scale. Intel restarted limited 450 mm pathfinding in 2024, seeking a 40% die-count boost per wafer to justify a projected USD 15 billion retrofit.

Compound-semiconductor makers are shifting from 150 mm and 200 mm to 300 mm lines to cut cost per die in silicon carbide and gallium nitride devices, further enlarging 300 mm tool requirements. SEMI released updated standards in June 2025 to certify etch uniformity and defect specifications for compound wafers, guiding suppliers in redesigning chamber materials for corrosive chemistries.

By Material: Silicon Dominates While Compound Substrates Surge

Silicon substrates captured 64.63% revenue in 2025, reflecting their decades-long role as the workhorse of logic and memory. Compound materials are forecast to expand 8.56% annually, widening the plasma etching equipment market share attributed to silicon carbide power devices and gallium nitride radio-frequency amplifiers. Silicon carbide’s thermal conductivity triples that of silicon, enabling junction temperatures over 200 °C in traction inverters, while gallium nitride’s electron mobility multiplies by ten, supporting amplifier power densities above 10 W per mm at millimeter-wave frequencies.

Wolfspeed demonstrated within-wafer etch variation below 3% across 200 mm silicon carbide substrates at its North Carolina fab, a threshold required for automotive qualification. Selective chemistries employing chlorine-based gases and pulsed bias waveforms now deliver 50:1 selectivity between gallium nitride and underlying silicon, illustrating tool makers’ progress in extending inductively coupled plasma platforms to tough materials.

By Application: Consumer Electronics Leads, Automotive Accelerates

Consumer electronics accounted for 38.61% of 2025 demand, maintaining their top spot in the plasma etching equipment market despite smartphone saturation. Automotive electronics, projected to advance at a 7.88% CAGR, is boosting the plasma etching equipment market size due to the increasing penetration of electric vehicles and the adoption of advanced driver assistance systems. Each battery electric vehicle contains two to three times more semiconductors than an internal-combustion model, with power devices and image sensors driving incremental content.

Tesla cut inverter cost 20% by vertically integrating silicon carbide devices across its vehicle lineup, prompting General Motors and others to lock in long-term deals with compound wafer suppliers. Industrial automation, medical devices, and aerospace form diverse tail segments, each valuing plasma etch precision but contributing lower aggregate volumes.

By End User: Foundries Continue to Expand, Integrated Device Manufacturers Stabilize

Foundries accounted for 57.94% of 2025 spending and are poised for an 8.51% CAGR to 2031 as fabless design houses such as NVIDIA, AMD, and Qualcomm amplify outsourcing. Taiwan Semiconductor Manufacturing Company allocated roughly USD 5.8 billion to etch tools in its USD 32 billion 2025 capex plan. Samsung installed nearly 120 new chambers in Hwaseong to enable gate-all-around production. Integrated device manufacturers, such as Intel, Micron, and SK Hynix, balance internal and external capacity, while university cleanrooms drive atomic layer etch research into emerging materials.

The outsourcing trend reflects rising fab construction costs that now exceed USD 20 billion per site, allowing only a handful of corporations to finance leading-edge capacity. Foundry share therefore remains on a steady upward trend, reinforcing the central role of their equipment roadmaps in shaping supplier revenue.

Geography Analysis

The Asia-Pacific region generated 55.72% of the revenue in 2025 and is projected to achieve an 8.66% CAGR, ensuring it continues to dominate the plasma etching equipment market. Taiwan’s cluster yielded USD 160 billion output in 2025, 65% of global foundry revenue. South Korea produced 70% of DRAM and 45% of NAND that year, cementing its position as the memory hub. China, constrained by export controls, accelerated the uptake of domestic tools, with Semiconductor Manufacturing International Corporation and Hua Hong Semiconductor qualifying NAURA and Advanced Micro-Fabrication Equipment systems for 14 nm and 28 nm flows. Japan reignited investment by allocating JPY 2 trillion (USD 13.5 billion) for local capacity, attracting Taiwan Semiconductor Manufacturing Company, Micron, and Western Digital.

North America represented roughly 25% of 2025 demand and is projected to grow 7.8% as CHIPS Act funds underwrite fabs in Arizona, Ohio, New York, and Texas. Intel’s two-fab Ohio campus alone is expected to need more than 200 etch chambers by 2028. Taiwan Semiconductor Manufacturing Company’s Arizona complex will host three fabs with combined capacity of 600,000 wafer starts per year by 2030, all equipped with leading-edge plasma tools.

Europe held about 10% share in 2025 but is aiming to capture 20% of global chip output by 2030 under the EUR 43 billion EU Chips Act allocation. Intel’s Magdeburg project, STMicroelectronics-GlobalFoundries’ French joint facility, and Infineon’s Dresden expansion represent more than EUR 80 billion (USD 87 billion) in announced investments. Middle East and Africa remain in the exploratory phase, with Abu Dhabi and Riyadh pursuing design and packaging hubs. South America’s activity is limited to assembly initiatives in Brazil and Argentina, while Australia and New Zealand contribute research but not large-scale fabrication.

Regulatory Landscape

Plasma etching equipment suppliers operate under a tightening mix of trade measures and dual-use export controls that affects tool shipments, spares, and field support. In January 2026, the United States issued a Section 232 Presidential Proclamation covering semiconductors and semiconductor manufacturing equipment, along with implementation messaging from U.S. Customs and Border Protection, raising compliance requirements around tariff classification and import documentation for equipment flows into the United States.

On the export side, U.S. Department of Commerce Bureau of Industry and Security (BIS) guidance released in May 2026 reiterated license requirements for advanced computing and semiconductor manufacturing items when dealing with entities headquartered in Country Group D:5 or Macau, even when those entities operate outside those destinations, increasing end-user diligence for global tool vendors. In Europe, the EU Chips Act framework incorporates supply-chain mapping and crisis-response mechanisms, including intervention tools that can influence priority allocation and coordinated controls during disruptions, which adds another layer of operational planning for equipment makers serving EU fabs.

Value Chain Analysis

The plasma etching equipment value chain starts with specialized upstream inputs such as RF power delivery systems, electrostatic chucks, vacuum pumps, and corrosion-resistant ceramics and coatings used in chamber hardware. OEMs integrate these into etch platforms (ICP, DRIE, HDP, and atomic layer etch variants) and qualify them through long customer acceptance cycles, commonly spanning 12 to 18 months for new platforms and process modules. This timing can concentrate demand into a small set of pre-qualified sub-suppliers during major node transitions.

Downstream, revenue concentrates in leading-edge logic and memory fabs and increasingly in advanced packaging lines that require high aspect-ratio profile control and low-damage processes, supported by a service and spares ecosystem tied to installed bases. Major OEMs such as Lam Research and Applied Materials anchor this chain with platform roadmaps aimed at atomic-scale process control (for example, Lam Researchs Akara conductor etch platform introduced in February 2025), while smaller and regional suppliers such as Samco Inc. (Kyoto) and SCI Automation Pte Ltd (Singapore, with manufacturing in Chennai, India) provide R&D, compound-semiconductor, and packaging-focused systems that broaden adoption beyond the largest foundries.

Competitive Landscape

Applied Materials, Lam Research, and Tokyo Electron collectively hold most of the leading-edge plasma etching equipment market share, reflecting high concentration. Applied Materials leverages a Centura installed base exceeding 10,000 chambers, allowing customers to port recipes with minimal re-qualification. Lam Research focuses on etch and deposition integration, supplying bundled process flows that simplify the ramp-up of advanced packaging. Tokyo Electron offers coater-developer and etch clusters in a single suite, streamlining procurement for lithography-adjacent steps.

Chinese suppliers Advanced Micro-Fabrication Equipment and NAURA Technology Group reached 15% domestic share in 2025 but lack the plasma uniformity, endpoint detection, and automation depth required for sub-7 nm nodes. Oxford Instruments, Plasma-Therm, and SPTS target niche opportunities such as atomic layer and cryogenic etching. Patent filings in cryogenic processes rose 40% year over year in 2024, and SEMI’s F47 automation standards update in April 2025 enables cloud-based predictive maintenance, lowering barriers for smaller entrants.

Selectivity in gate-all-around transistor flows is an emerging battleground. Oxford Instruments achieved 150:1 silicon-germanium to silicon selectivity with cyclic hydrogen-fluoride exposure, while Tokyo Electron is piloting pulsed plasma chemistries to surpass 100:1. These breakthroughs could erode incumbent dominance if commercialized at scale by 2027.

Plasma Etching Equipment Industry Leaders

Lam Research Corporation

Applied Materials Inc.

Tokyo Electron Ltd

SPTS Technologies (KLA company)

Oxford Instruments PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Process complexity at the leading edge is widening the addressable need for selective, low-damage, and materials-specific etch capabilities across logic, memory, and advanced packaging. Applied Materials June 2026 introductions of the Producer Selectra Mo Etch and Centris Spectral SiN ALD systems point to ongoing commercial development for high-aspect-ratio 3D structures and hard-to-pattern materials stacks, reinforcing demand for etch tools that combine in-situ monitoring with tighter profile and selectivity control.

Equipment demand is also being shaped by sustained 300 mm investment cycles and memory upgrades tied to AI infrastructure. SEMI pointed to global 300 mm fab equipment spending of USD 133 billion in 2026, and Tokyo Electron reported a sizable FY26 capex increase to support DRAM etch tool demand linked to HBM production. Beyond mainstream HVM, specialized adoption pockets in compound semiconductors and emerging devices continue to open incremental tool lanes, including Samco system selections in 2026 for GaN power device R&D in Poland and quantum photonics work at the Technical University of Denmark, which supports a broader mix of ICP-RIE and niche etch configurations outside the largest logic fabs.

Recent Industry Developments

- June 2026: Applied Materials introduced the Producer Selectra Mo Etch system and the Centris Spectral SiN ALD system to support 3D chip scaling in logic and memory. The additions target higher aspect-ratio structures and more selective material removal, expanding the process window for advanced nodes and 3D architectures and reinforcing Applied Materials position in etch-adjacent patterning steps.

- February 2025: Lam Research launched the Akara conductor etch platform using its DirectDrive solid-state technology for atomic-scale feature creation in 3D device manufacturing. The platform focuses on precision and repeatability needed for gate-all-around transistors and advanced memory scaling, strengthening Lam Researchs differentiation as etch steps multiply per wafer.

- November 2024: Hitachi High-Tech launched the DCR Etch System 9060 Series for isotropic etching of advanced 3D semiconductor devices, integrating wafer cooling and an infrared lamp in a single vacuum reactor. The release broadens options for profile shaping steps that complement anisotropic plasma etch, especially as 3D structures increase the need for controlled isotropic processes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the plasma etching equipment market covers revenue earned from tools used to etch patterns on wafers and related substrates during semiconductor and microfabrication processes, using both global manufacturing demand and R&D programs.

Scope exclusions: We exclude etching gases and chemicals, spare parts sold as standalone items, and downstream contract etching services when they are not bundled with equipment revenue.

Segmentation Overview

- By Type

- Reactive Ion Etching (RIE)

- Inductively Coupled Plasma Etching (ICP)

- Deep Reactive Ion Etching (DRIE)

- High Density Plasma Etching (HDPE)

- Other Types

- By Wafer Size

- Below 150 mm

- 200 mm

- 300 mm

- Above 450 mm

- By Material

- Silicon

- Compound Semiconductors

- Glass and Polymers

- Other Materials

- By Application

- Consumer Electronics

- Industrial

- Medical Devices

- Automotive Electronics

- Aerospace and Defense

- Other Applications

- By End User

- Foundries

- Integrated Device Manufacturers (IDMs)

- Research and Academic Institutions

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting fact base from semiconductor manufacturing activity and equipment investment cycles, and to track how etch intensity changes with technology nodes. We referenced public sources such as SEMI publications, World Semiconductor Trade Statistics releases, U.S. International Trade Commission trade statistics, World Bank macro indicators, and patent databases to sense technology direction and timing.

To make the numbers usable in a model, we also reviewed company filings and earnings call decks, fab expansion announcements, and credible industry news that tracks capital spending and capacity additions. A paid subscription for company financials and news intelligence was used selectively to align revenue timelines, standardize currency conversions, and account for corporate structure changes that can distort year-over-year comparisons. These sources are illustrative, and many other public documents were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating demand signals and pricing behavior for plasma etch tools across major fab regions, and then pressure-testing assumptions that were weak in public data. We spoke with equipment makers, component suppliers, and fab-side process and procurement professionals, which helped us confirm shipment timing, typical tool configurations, and how purchase decisions shift between memory, foundry, and logic cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 41% |

| Mid tier: 58% | Functional/Unit leaders: 31% | EMEA: 34% |

| Smaller Players: 17% | Managers: 56% | Americas: 25% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build that reconstructs the equipment revenue pool from semiconductor capex direction, fab capacity additions, and etch step intensity by node, then allocates into plasma etching equipment based on process share. After that, we corroborate with selective bottom-up approximations, including sampled shipment proxies, typical system pricing bands, and channel checks, before adjusting totals for obvious gaps.

Inputs used in the model include wafer starts and utilization trends, announced fab capacity ramps, etch tool mix shifts between logic, foundry, and memory, average selling price progression for advanced tools, and regional capex concentration (with APAC weight being an important check). When primary inputs were missing for smaller regions or niche applications, we applied conservative adoption ratios anchored to observed capex and import patterns, and then reviewed them again with interview feedback.

For forecasting, scenario analysis was used around capex cycles and node transitions. We translated scenarios into a single base case using expert consensus from interviews, then sanity-checked the forecast path against macro indicators and the expected timing of capacity coming online, so the curve stays realistic even when year-to-year ordering is lumpy.

Data Validation & Update Cycle

Multiple checks were used so the final numbers do not rely on a single assumption. Model outputs were compared with independent signals such as semiconductor capex direction, trade flows for relevant equipment categories, and publicly discussed tool demand by region, then large variances were investigated before sign-off.

Review steps included internal analyst cross-checks on calculations, consistency tests across years, and re-checking any outlier growth rates that did not match known cycle timing. Reports are refreshed annually, and if a material event occurs, such as a sharp capex revision or a major capacity delay, we trigger an interim update and re-contact relevant experts. Before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Plasma Etching Equipment Market Estimate Compared With Other Published Estimates

Published market numbers for plasma etching equipment often do not match because each publisher draws the line differently on what counts as equipment revenue, and because base years and currency timings vary. Differences can also come from how cyclical semiconductor capex is treated, since a single large fab ramp can shift the apparent growth curve.

Key gap drivers are usually scope boundaries and how tool pricing is handled across generations, particularly when advanced nodes raise tool complexity and service attach rates. Some estimates lean more on long-range trend growth without fully reflecting near-term order lumpiness, while others may blend adjacent etch categories or related process tools into one total, which pushes the value up even if the underlying demand pool is similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.34 B (2026) | |

| Industry Publisher A | USD 8.70 B (2025) | Uses an earlier base year and a broader label of plasma etch equipment, and the public summary does not clarify whether installed-base services and software are included, which can shift the total in either direction depending on treatment. |

| Industry Publisher B | USD 5.64 B (2025) | Appears to apply a longer-horizon demand curve and a narrower revenue capture approach, and the method notes are light on how pricing bands and cycle timing are translated into annual equipment revenue. |

The table shows a wide spread, and in the Mordor Intelligence model the total is tied to equipment product revenue with regional capex and wafer-fab expansion signals used as the main demand anchors rather than a simple long-run growth curve. When the scope, base year, and pricing logic are made explicit, the final number becomes easier to reconcile and repeat, even if different publishers still choose different reporting years.

Key Questions Answered in the Report

What is the current size of the plasma etching equipment market?

The market reached USD 14.34 billion in 2026 and is on track for USD 20.42 billion by 2031, reflecting a 7.33% CAGR.

Which segment accounts for the largest plasma etching equipment market share?

Inductively coupled plasma platforms led with 46.83% revenue in 2025, thanks to versatility across logic, memory, and advanced packaging.

What is driving future demand for plasma etching tools?

EUV lithography at 3 nm and 2 nm nodes, 3D NAND exceeding 200 layers, and silicon carbide adoption in electric vehicles are expanding etch intensity per wafer.

Which region will grow fastest through 2031?

Asia-Pacific is forecast for an 8.66% CAGR as Taiwan, South Korea, Japan, and China invest heavily in new capacity.

Who are the key suppliers of leading-edge etch equipment?

Applied Materials, Lam Research, and Tokyo Electron collectively deliver more than 80% of tools used at sub-7 nm nodes, while NAURA and Advanced Micro-Fabrication Equipment focus on mature-node demand in China.

Page last updated on: