Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

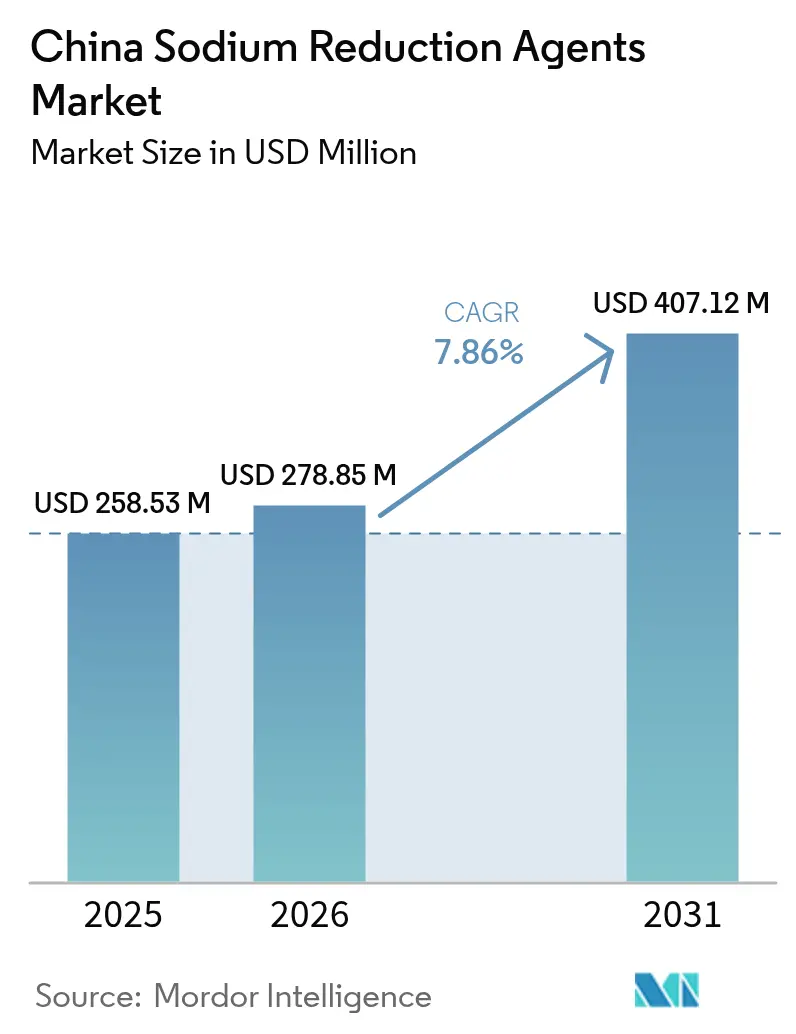

| Base Year Market Size (2025) | USD 258.53 Million |

| Market Size (2026) | USD 278.85 Million |

| Market Size (2031) | USD 407.12 Million |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

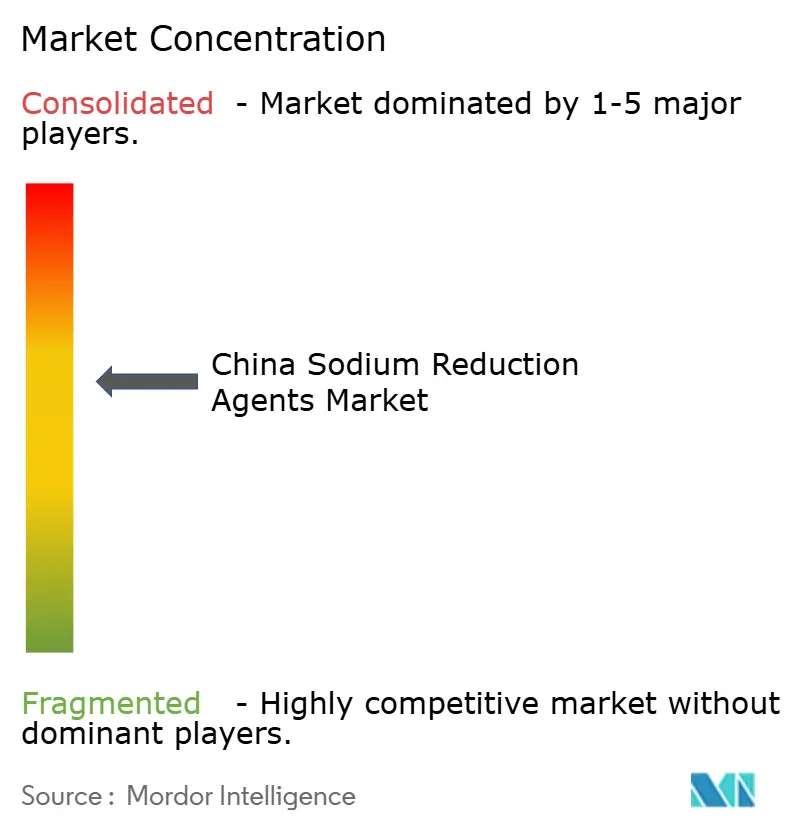

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Sodium Reduction Agents Market Analysis by Mordor Intelligence

China sodium reduction agents market size in 2026 is estimated at USD 278.85 million, growing from 2025 value of USD 258.53 million with 2031 projections showing USD 407.12 million, growing at 7.86% CAGR over 2026-2031. Beijing's "Healthy China 2030" initiative, which aims to reduce average salt consumption to 5 grams per day, is driving reformulation efforts in packaged foods. Urban consumers with higher health awareness are increasingly accepting sodium reductions of up to 35%, provided that the taste of the products remains intact. Technological advancements, such as yeast-extract umami enhancers and Artificial Intelligence (AI)-driven sensory modeling, have significantly shortened product development timelines from 24 months to nine months. Factors such as clear policy direction, the growing penetration of e-commerce for reformulated products into Tier-3 cities, and supply chain innovations that integrate taste masking with shelf-life improvements are collectively supporting the market's sustained growth. Competitive intensity remains moderate, with existing players scaling up domestic fermentation capacity to reduce China's 50% reliance on imported potash-based potassium chloride (KCl).

Key Report Takeaways

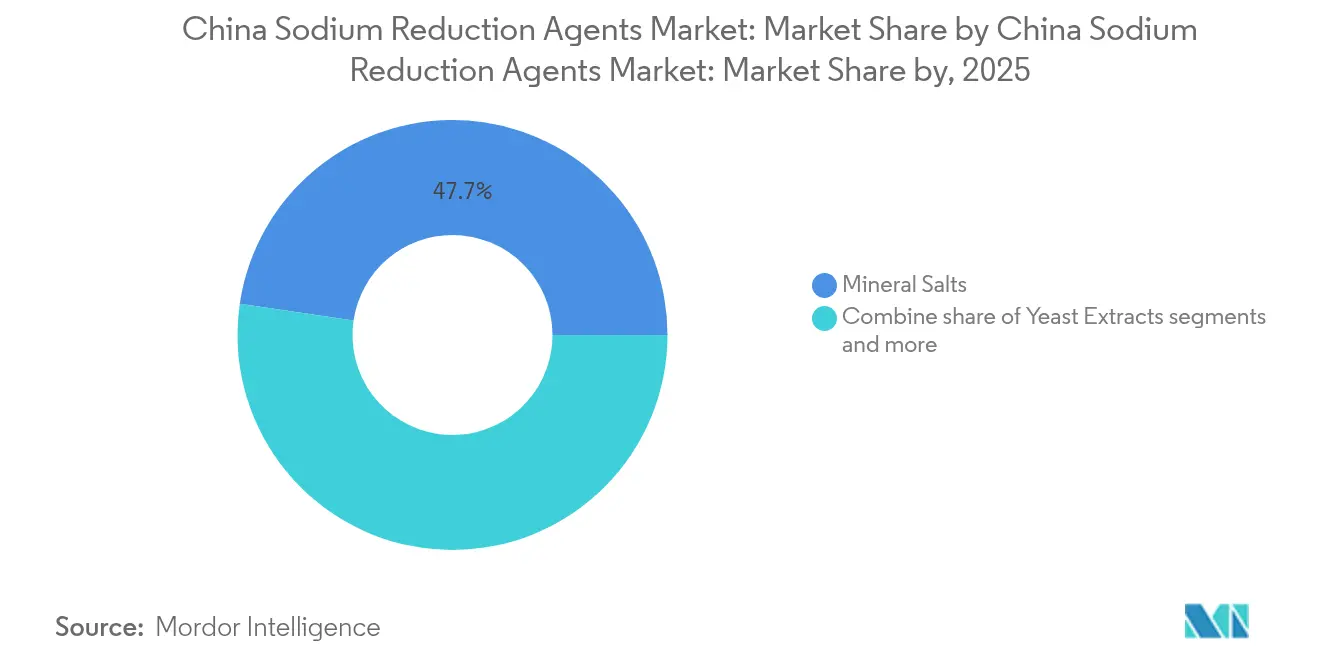

- By product type, mineral salts led with 47.68% of China sodium reduction agents market share in 2025, while yeast extracts are forecast to grow at a 8.74% CAGR to 2031.

- By form, powders and granules commanded 67.55% share of the China sodium reduction agents market size in 2025; liquids record the fastest 9.02% CAGR through 2031.

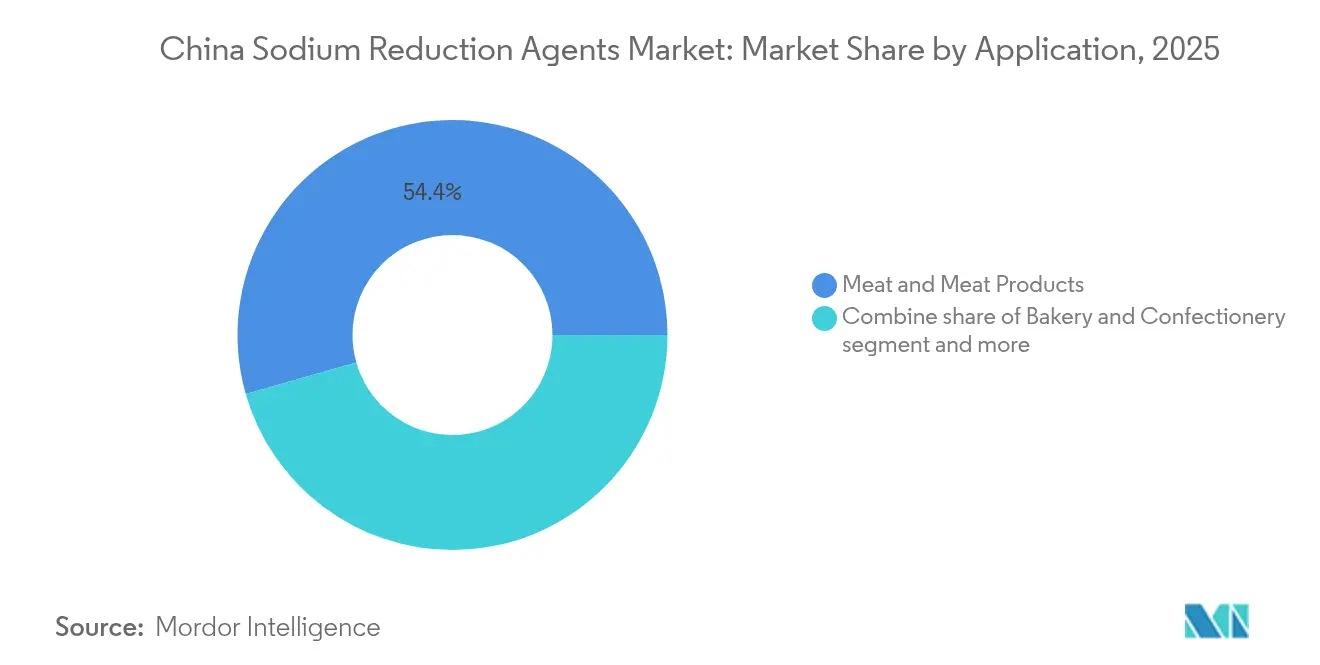

- By application, meat products captured 54.42% of the China sodium reduction agents market size in 2025 and are advancing at a 8.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Sodium Reduction Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased consumer awareness of sodium-related health risks driving demand for low-sodium food products | +2.1% | National, with stronger uptake in Tier-1 and Tier-2 cities (Beijing, Shanghai, Guangzhou, Shenzhen) | Medium term (2-4 years) |

| "Healthy China 2030" targets reducing salt intake, pressuring industries to reformulate products | +1.9% | National policy mandate; enforcement concentrated in packaged-food hubs (Shandong, Guangdong, Jiangsu) | Long term (≥ 4 years) |

| Government campaigns promoting reduced-sodium products through media, schools, and community initiatives | +1.3% | National, with pilot programs in urban centers and school feeding systems | Medium term (2-4 years) |

| Health-conscious urban consumers increasing demand for low-sodium packaged foods and beverages | +1.5% | Tier-1 and Tier-2 cities; spillover to Tier-3 cities via e-commerce channels | Short term (≤ 2 years) |

| Processed food category growth creating opportunities for sodium reduction reformulation | +1.2% | National, with highest growth in coastal manufacturing provinces (Guangdong, Zhejiang, Fujian) | Medium term (2-4 years) |

| Technological advancements improving salt replacers to better replicate traditional saltiness in foods | +0.8% | National, with R&D concentrated in Beijing, Shanghai, and Langfang innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased consumer awareness of sodium-related health risks driving demand for low-sodium food products

Urban Chinese consumers are increasingly altering their eating habits, as data indicates that a majority of adults consume sodium levels exceeding recommended limits. The 2024 Chinese Hypertension Guidelines emphasize the use of potassium-enriched salt substitutes as a clinical strategy to address this issue. This trend is particularly evident in Tier-1 cities, where higher disposable incomes and heightened health awareness enable consumers to choose premium-priced reformulated snacks, sauces, and ready meals labeled as "low-sodium" or "reduced-salt." A study of thousands of prepackaged foods in Zhejiang province revealed that a significant portion of these products were high in sodium, with an average sodium content exceeding 1,000 milligrams per 100 grams. In response, manufacturers in categories such as egg products, soy-based foods, and convenience meals are working to comply with the draft front-of-pack labeling guidelines released in August 2024. These guidelines propose a rating system ranging from A to D, along with warning labels specifically targeting children's food products. These regulatory measures align with the growing consumer willingness to pay a premium for healthier options, creating opportunities for ingredient suppliers to collaborate with brand owners through co-development partnerships. Further supporting this trend, the December 2024 Hunan cohort study demonstrated that salt substitutes containing 25 percent potassium chloride were more effective in reducing sodium intake compared to blends with 13 percent potassium chloride. This provides formulators with clinical evidence to justify the use of higher inclusion rates, even when sensory challenges may arise.

“Healthy China 2030” targets reducing salt intake, pressuring industries to reformulate products

Beijing's "Healthy China 2030" initiative aims to reduce the average salt consumption across the population to below 5 grams per day [1]Source: Ministry of Foreign Affairs of the People’s Republic of China, “China’s Progress Report,”fmprc.gov.cn. Achieving this target requires coordinated efforts from the food manufacturing, catering, and retail industries. The China Food and Nutrition Development Plan (2025-2030) supports this objective by establishing interim benchmarks for sodium content in processed foods. These benchmarks are enforced through GB 28050-2025 nutrition labeling standards, which mandate the declaration of sodium content and set thresholds for "low-sodium" and "sodium-free" claims. This regulatory framework compels manufacturers in key provinces such as Shandong, Guangdong, and Jiangsu, which together account for over 40 percent of China's packaged food production, to adopt sodium reduction strategies or risk reputational and regulatory consequences. In November 2024, the Chinese Center for Disease Control and Prevention released the China Food Industry Salt Reduction Guide (Second Edition). This guide outlines technical approaches for gradual sodium reduction, exploration of alternative flavors such as spicy, sour, and aromatic spices, and process innovations. It serves as a regulatory roadmap, reducing the risks associated with reformulation investments. The guide also emphasizes the use of front-of-pack nutrition labels and encourages public sharing of reformulation achievements. These measures are expected to accelerate competitive benchmarking and shorten the time-to-market for sodium-reduced stock-keeping units (SKUs), amplifying the long-term impact of sodium reduction efforts.

Government campaigns promoting reduced-sodium products through media, schools, and community initiatives

State-sponsored media campaigns and school-based nutrition education programs are influencing consumer perceptions of sodium-related health risks. Organizations such as the Chinese Nutrition Society and China Centers for Disease Control and Prevention (China CDC) are utilizing multi-channel messaging to highlight the connection between excessive salt intake and health issues like cardiovascular disease, stroke, and kidney dysfunction. The 2024 Chinese Hypertension Guidelines endorse the use of salt substitutes as part of clinical management, supporting potassium-enriched formulations and equipping healthcare professionals with evidence-based guidance for patient counseling[2]Source: National Library of Medicine,"Effect of sodium-reduced potassium-enriched salt substitutes on stomach cancer," pmc.ncbi.nlm.nih.gov. Urban school feeding programs are piloting reduced-sodium meal plans, fostering a generation of younger consumers accustomed to lower-salt flavor profiles. This demographic shift is expected to sustain demand for sodium reduction agents in the medium term. Community-level initiatives, such as cooking demonstrations and salt-spoon distribution campaigns, emphasize that discretionary salt, which accounts for approximately 70 percent of sodium intake in China, can be reduced without compromising taste. These efforts are gradually lowering the sensory threshold for manufacturers reformulating products, as consumers adapt to less-salty taste profiles. The combined impact of policy-driven measures and grassroots behavior change is accelerating the market's transition from niche health-food products to broader mainstream adoption.

Health-conscious urban consumers increasing demand for low-sodium packaged foods and beverages

Affluent consumers in Beijing, Shanghai, Guangzhou, and Shenzhen are driving a trend toward premiumization in packaged foods, with low-sodium claims emerging as a key differentiator across categories such as instant noodles and dairy beverages. E-commerce platforms are further supporting this trend by providing Tier-3 city consumers access to reformulated products that were previously limited to Tier-1 retail channels. This has effectively broadened the availability of health-focused SKUs and expanded the market for sodium reduction agents. A 2024 study on prepackaged foods in Zhejiang revealed that high-sodium products (average 1,018.6 mg Na per 100 g) dominate categories such as egg, soy, convenience, meat, and vegetable products. However, brand owners are now actively reformulating their offerings in preparation for the August 2024 draft front-of-pack labeling guidelines, which propose A-to-D rating systems and warning labels for children's foods. This regulatory development aligns with increasing disposable incomes and growing health awareness, fostering a consumer base willing to pay a 10 to 15 percent premium for low-sodium alternatives. Ingredient suppliers can leverage this opportunity by co-developing formulations that emphasize clean-label attributes—such as yeast extracts, fermented peptides, and botanical extracts—rather than relying solely on potassium chloride blends, which are often perceived negatively by health-conscious consumers due to their "chemical" association.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Difficulty maintaining taste and consumer acceptance in sodium-reduced traditional Chinese foods | -1.4% | National, with acute challenges in Sichuan, Hunan, and Guangdong cuisines reliant on fermented condiments | Short term (≤ 2 years) |

| Sensory issues with potassium chloride requiring advanced masking techniques for bitterness and metallic notes | -1.1% | National, affecting all product categories using mineral-salt replacers | Medium term (2-4 years) |

| Food safety concerns due to reduced preservative effects in low-sodium products like meats and sauces | -0.7% | National, with heightened scrutiny in meat processing hubs (Henan, Shandong, Sichuan) | Medium term (2-4 years) |

| Higher production costs and lower profit margins for reduced-sodium and blended salts | -0.6% | National, with cost pressures most acute for small and medium-sized enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Difficulty maintaining taste and consumer acceptance in sodium-reduced traditional Chinese foods

Traditional Chinese condiments, such as soy sauce, oyster sauce, fermented bean pastes, and pickled vegetables, derive their characteristic flavors from high sodium chloride concentrations, which also act as microbial inhibitors during fermentation and storage. Reformulating these products to comply with GB 28050-2025 thresholds poses a significant sensory challenge, particularly in Sichuan, Hunan, and Guangdong cuisines, where salty, umami, and fermented flavors are integral. A review published in 2024 in *Food Science & Human Wellness* highlighted that reduced-salt soy sauce formulations often experience diminished umami intensity and altered fermentation kinetics, necessitating extended aging or enzymatic interventions to restore flavor complexity. The China Food Industry Salt Reduction Guide (Second Edition) addresses this issue by recommending gradual sodium reduction protocols with small percentage decrements over multi-year cycles and exploring alternative flavoring options, such as spicy, sour, and aromatic spices, to offset sodium loss. However, even incremental changes risk consumer rejection in categories where brand loyalty is closely tied to taste consistency. This forces manufacturers to invest in consumer education and trial-size stock-keeping units (SKUs) to help consumers adapt to the new formulations. The short-term impact is particularly challenging for small and medium-sized enterprises, which often lack the research and development resources and sensory testing facilities needed to validate reformulations. This creates a competitive advantage for multinational ingredient suppliers, who can provide turnkey solutions supported by clinical taste panels.

Sensory issues with potassium chloride requiring advanced masking techniques for bitterness and metallic notes

Potassium chloride, the primary mineral-salt replacer in the market for 2024, introduces bitterness and metallic off-notes when inclusion rates exceed 25 percent. This limitation restricts the extent of sodium reduction achievable and necessitates the use of expensive masking strategies. A 2025 peer-reviewed study published in Frontiers in Nutrition revealed that wheat-based bakery products formulated with 3.6 grams of potassium chloride (KCl) per 1,000 grams of flour maintained acceptable saltiness without significant off-flavors. However, higher inclusion levels (5.4 grams per 1,000 grams of flour) negatively impacted flavor acceptability, introducing bitterness and metallic aftertastes. Calcium chloride (CaCl2), tested as an alternative, produced even stronger soapy and metallic notes, making it unsuitable for most applications unless advanced encapsulation or co-ingredient masking techniques are utilized. Kerry Group's Tastesense Salt addresses these sensory challenges by incorporating botanical extracts, peptides, and fermented flavor modulators to mask potassium chloride's off-notes. However, these solutions come with a 20 to 30 percent cost premium compared to standard potassium chloride blends. Over the medium term, this is expected to create a division within the market. Premium brands are likely to adopt multi-ingredient masking systems to achieve sodium reductions of 40 to 60 percent, while value brands will remain limited to reductions of 20 to 25 percent using unmasked potassium chloride. This difference may strengthen consumer perceptions that low-sodium products are of lower quality compared to their standard counterparts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Yeast Extracts Gain as Clean-Label Umami Demand Surges

In 2025, mineral salts accounted for 47.68% of the China sodium reduction agents market, primarily driven by potassium chloride (KCl) blends, which act as substitutes for sodium chloride in processed meats, condiments, and instant noodles. Yeast extracts are projected to grow at a compound annual growth rate (CAGR) of 8.74% through 2031, driven by formulators' preference for clean-label umami enhancers that avoid the bitterness and metallic aftertastes associated with high levels of potassium chloride. Angel Yeast, with a global yeast extract production capacity of 150,000 tonnes and 21 production lines across 10 cities in China, is well-positioned to capitalize on this trend. The company's AnPro® yeast protein and yeast extract-based solutions enable up to 35% salt reduction while preserving umami flavor and mouthfeel.

Amino acids and glutamates, the third segment, are used in meat products, where basic amino acids such as L-lysine and L-arginine enhance salty perception and mask undesirable flavors. However, regulatory scrutiny of monosodium glutamate (MSG) limits growth in this segment, despite Meihua Holdings expanding its MSG production capacity to 3.2037 million tonnes in 2024. This regulatory environment continues to influence the adoption of glutamates in the market.

By Form: Liquid Formats Accelerate in Sauces and Beverages

Powder/granule forms accounted for 67.55% of the market in 2025, primarily due to their compatibility with dry seasoning blends, instant noodle packets, and bakery mixes. These formats enable manufacturers to utilize existing blending infrastructure, which helps avoid the need for significant capital investment in liquid-dosing systems. This ease of integration has made powder and granule forms a preferred choice for many manufacturers.

On the other hand, liquid sodium reduction agents are expected to grow at a compound annual growth rate (CAGR) of 9.02% through 2031. This growth is driven by the increasing adoption of in-line dosing systems by beverage and sauce manufacturers. These systems provide precise sodium control and address the challenges of dust handling and dissolution associated with powder formats. A notable example is Kerry Group's Tastesense Salt, launched in April 2024. This liquid solution for snack seasonings includes botanical extracts, peptides, and fermented flavor modulators pre-dissolved in a carrier system. It allows snack manufacturers to spray-apply sodium reduction agents during the final seasoning step, achieving over 60% sodium reduction with minimal reformulation of base recipes.

By Application: Meat Products Dominate Yet Face Acute Reformulation Complexity

Meat and meat products accounted for 54.42% of sodium reduction agents in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 8.88% through 2031. This growth is driven by reformulation mandates targeting products such as sausages, ham, and cured meats, where sodium traditionally serves as both a flavor enhancer and a microbial inhibitor. The publication of GB 2760-2024 in August 2024 eliminated preservatives such as epsilon-polylysine, nisin, and sorbates from canned foods. This change has prompted meat processors to adopt alternative preservation methods, including natural antioxidants, fermentation-derived antimicrobials, and modified-atmosphere packaging. These methods increase the complexity and cost of sodium-reduction initiatives. A 2024 review in Food Science and Human Wellness highlighted that reduced-salt meat formulations often experience issues such as diminished water-holding capacity, altered texture, and accelerated lipid oxidation. To address these challenges, multi-ingredient solutions, including phosphates, hydrocolloids, and antioxidants, are required to restore functionality.

Condiments, seasonings, and sauces represent the second-largest application for sodium reduction agents and face similar challenges. Balancing sodium reduction with microbial stability and flavor intensity is particularly difficult in fermented products, such as soy sauce and bean paste. In these products, sodium chloride plays a critical role in modulating fermentation kinetics and preventing spoilage. These challenges necessitate innovative approaches to maintain product quality while meeting sodium reduction goals.

Geography Analysis

The sodium reduction agents market in China is geographically concentrated in coastal manufacturing provinces such as Guangdong, Zhejiang, Jiangsu, and Shandong. These provinces collectively account for over 50% of the country's packaged-food production and host facilities for both multinational and domestic brands. These facilities are subject to GB 28050-2025 labeling standards and the "Healthy China 2030" reformulation mandates . Guangdong, the largest food-processing hub, is home to condiment manufacturers such as soy sauce and oyster sauce producers, as well as meat processors. These companies are early adopters of yeast extracts and mineral-salt blends to meet sodium-reduction targets set by provincial health bureaus. In Zhejiang, the concentration of snack and bakery producers drives demand for powder and granule formats that integrate seamlessly into dry seasoning blends and instant noodle packets.

Shandong, a major meat-processing center, faces significant reformulation challenges. Processors must balance sodium reduction with food safety requirements in products such as sausages, ham, and cured meats. This has created demand for multifunctional ingredients like Corbion's Origin® and Verdad® solutions, which provide both antimicrobial control and sodium reduction. Meanwhile, Jiangsu's dairy and beverage manufacturers are adopting liquid sodium reduction agents that enable in-line dosing and precise sodium control. This trend has been amplified by DSM-Firmenich's 2024 acquisition of full ownership in ArtSci Biology Technologies Company Limited, enhancing local research and development capabilities for dairy, beverage, and baked-goods formulations. Inland provinces such as Henan, Sichuan, and Hunan are lagging in sodium reduction adoption due to the prevalence of small and medium-sized enterprises with limited research and development budgets and sensory labs. However, these regions are poised for growth as provincial health bureaus enforce GB 28050-2025 thresholds and consumers in Tier-3 cities gain access to reformulated products through e-commerce platforms. Sichuan and Hunan, known for their spicy and fermented cuisines, face unique reformulation challenges. Traditional condiments like fermented bean paste and pickled vegetables rely on high sodium chloride concentrations for their flavor identity. Gradual-reduction protocols and alternative flavor strategies, such as incorporating spicy, sour, and aromatic spices, are recommended in the November 2024 China Food Industry Salt Reduction Guide. Tier-1 cities, including Beijing, Shanghai, Guangzhou, and Shenzhen, are demand epicenters where affluent, health-conscious consumers drive premiumization in packaged foods. These consumers are willing to pay 10 to 15 percent premiums for low-sodium variants, creating demand for clean-label yeast extracts and fermented peptides over commodity potassium chloride blends. Tier-2 cities are experiencing rapid adoption as dual-income households and convenience-store proliferation expand access to reformulated stock-keeping units (SKUs). Meanwhile, Tier-3 cities remain price-sensitive but are gradually acclimating to lower-salt flavor profiles through government campaigns and school-based nutrition education. The geographic dispersion of reformulation activity, from coastal manufacturing hubs to inland processing centers and from Tier-1 urban consumers to Tier-3 price-sensitive shoppers, creates a heterogeneous market. Ingredient suppliers must tailor product portfolios, such as powder versus liquid formats and mineral salts versus yeast extracts, and adjust go-to-market strategies, such as direct sales versus distributor partnerships, to align with regional manufacturing capabilities, regulatory enforcement intensity, and consumer willingness to pay.

Competitive Landscape

The China sodium reduction agents market is moderately consolidated. Angel Yeast leads in clean-label umami enhancers, supported by its 150,000-tonne global yeast extract capacity, 21 production lines across 10 cities in China, and 38 years of fermentation expertise. Meanwhile, multinational ingredient companies, including DSM-Firmenich, Kerry Group, Cargill, and Corbion, are employing precision fermentation platforms, AI-driven sensory modeling, and strategic acquisitions to expedite reformulation processes and expand their presence in premium market segments.

DSM-Firmenich's acquisition of full ownership in ArtSci Biology Technologies Co., Ltd. in 2024 and its Global Strategic Cooperation Memorandum with Yili Group highlight its strategy of embedding local research and development capabilities and co-developing formulations with Tier-1 brand owners to mitigate adoption risks. Similarly, Kerry Group's launch of Tastesense Salt in April 2024, a liquid solution capable of achieving over 60% sodium reduction in snacks, demonstrates the competitive advantage of multi-modal flavor enhancement over single-ingredient solutions. Meihua Holdings' acquisition of Kyowa Hakko Bio's food-grade and pharmaceutical amino acid assets in November 2024 for approximately JPY 10.5 billion (USD 70 million) marks a strategic shift toward precision-fermented ingredients and overseas production. This move positions the company to compete in higher-margin segments beyond commodity monosodium glutamate (MSG).

Growth opportunities exist in fermented peptides, botanical extracts, and enzymatic flavor modulators, which can achieve sodium reductions of 50% to 60% without the sensory limitations often associated with high-inclusion potassium chloride formulations. However, these solutions face challenges, including limited production scalability and the need for sensory validation across various food applications. Technology plays a crucial role in maintaining competitiveness. Companies that can shorten reformulation timelines from 18–24 months to 6–9 months using AI-driven receptor modeling and high-throughput sensory screening are positioned to gain a significant market advantage. This urgency is fueled by the need to meet GB 28050-2025 thresholds and front-of-pack labeling requirements. Corbion's planned 2024 launch of AI-powered Listeria control models and its expansion of natural preservation portfolios, such as Origin and Verdad, highlight the potential of multi-functional ingredients. These ingredients, which provide both sodium reduction and shelf-life extension, are expected to command premium pricing and achieve faster market adoption.

China Sodium Reduction Agents Industry Leaders

-

Angel Yeast Co. Ltd.

-

Givaudan SA

-

Lesaffre

-

Innophos Holdings Inc.

-

ABF Ingredients

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Angel Yeast Co., Ltd. showcased its yeast extract-based salt reduction solutions and AnPro yeast protein at FIC2025 in Shanghai, demonstrating formulations that achieve up to 35 percent salt reduction while maintaining umami depth and mouthfeel. The company's 150,000-tonne global yeast extract capacity and 21 production lines across 10 Chinese cities position it to capture growing demand for clean-label sodium reduction agents

- January 2025: Cargill launched a comprehensive sodium reduction content series highlighting potassium chloride's dual benefit of reducing sodium while increasing potassium intake, which most Americans consume at only 50% of recommended levels.

- April 2024: Kerry Group PLC launched Tastesense Salt, a sodium-free solution for snacks that combines natural botanical extracts, peptides, and yeast/non-yeast ferments to achieve greater than 60 percent sodium reduction. The liquid format enables spray-application during final seasoning, allowing snack manufacturers to reformulate without overhauling base recipe

China Sodium Reduction Agents Market Report Scope

By product type, the Chinese sodium reduction ingredients market is segmented into amino acids and glutamates, mineral salts (potassium chloride, magnesium sulfate, potassium lactate, and calcium chloride), yeast extracts, and other types. Based on application, the market is segmented into bakery and confectionery, condiments, seasonings and sauces, dairy and frozen foods, meat and meat products, snacks, and other applications.

By Product Type

| Amino Acids and Glutamates |

| Mineral Salts |

| Yeast Extracts |

| Others |

By Form

| Powder/Granules |

| Liquid |

By Application

| Bakery and Confectionery |

| Condiments, Seasonings and Sauces |

| Dairy and Frozen Foods |

| Meat and Meat Products |

| Snacks |

| Others |

| By Product Type | Amino Acids and Glutamates |

| Mineral Salts | |

| Yeast Extracts | |

| Others | |

| By Form | Powder/Granules |

| Liquid | |

| By Application | Bakery and Confectionery |

| Condiments, Seasonings and Sauces | |

| Dairy and Frozen Foods | |

| Meat and Meat Products | |

| Snacks | |

| Others |

Key Questions Answered in the Report

How large is the China sodium reduction agents market in 2026?

The market is valued at USD 278.85 million in 2026.

What is the expected CAGR for sodium reduction agents in China?

Forecasts point to an 7.86% CAGR between 2026 and 2031.

Which product segment is growing fastest?

Yeast extracts are expanding at a 8.74% CAGR as clean-label demand rises.

Which application accounts for the largest share of demand?

Meat products capture 54.42% of use due to regulatory pressure and high baseline sodium levels.

Page last updated on: