Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

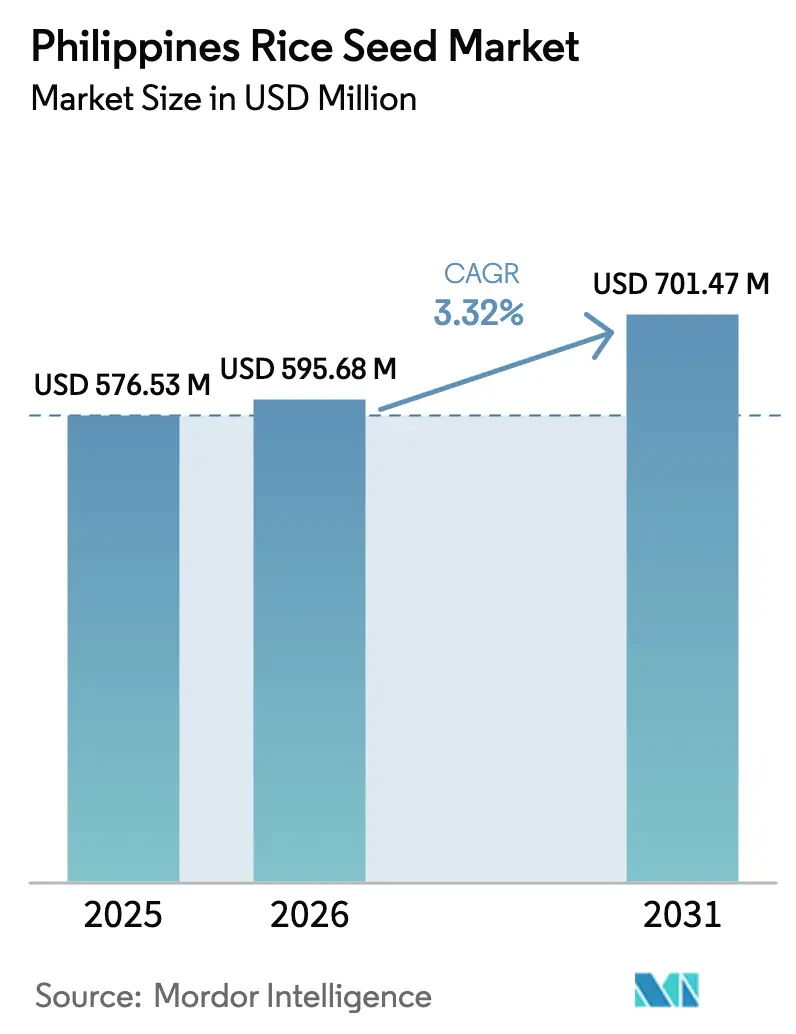

| Base Year Market Size (2025) | USD 576.53 Million |

| Market Size (2026) | USD 595.68 Million |

| Market Size (2031) | USD 701.47 Million |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Rice Seed Market Analysis by Mordor Intelligence

The Philippines rice seed market size in 2026 is estimated at USD 595.68 million, growing from 2025 value of USD 576.53 million with 2031 projections showing USD 701.47 million, growing at 3.32% CAGR over 2026-2031. Demand rises as smallholders transition toward commercial-scale production, buoyed by the government’s decision to triple the Rice Competitiveness Enhancement Fund (RCEF) to PHP 30 billion (USD 518 million) through 2031. Climatic shocks such as the 2024 El Niño event have accelerated adoption of climate-smart varieties, while mechanization incentives spur certified-seed uptake among mid-size farms. At the same time, revised biosafety rules enacted in 2024 cleared a path for private transgenic events, widening the technological choices available to estate growers and large cooperatives. These trends support a steady but measured growth trajectory for the Philippines rice seed market as farmers balance cost, risk, and yield in an increasingly volatile production environment.

Key Report Takeaways

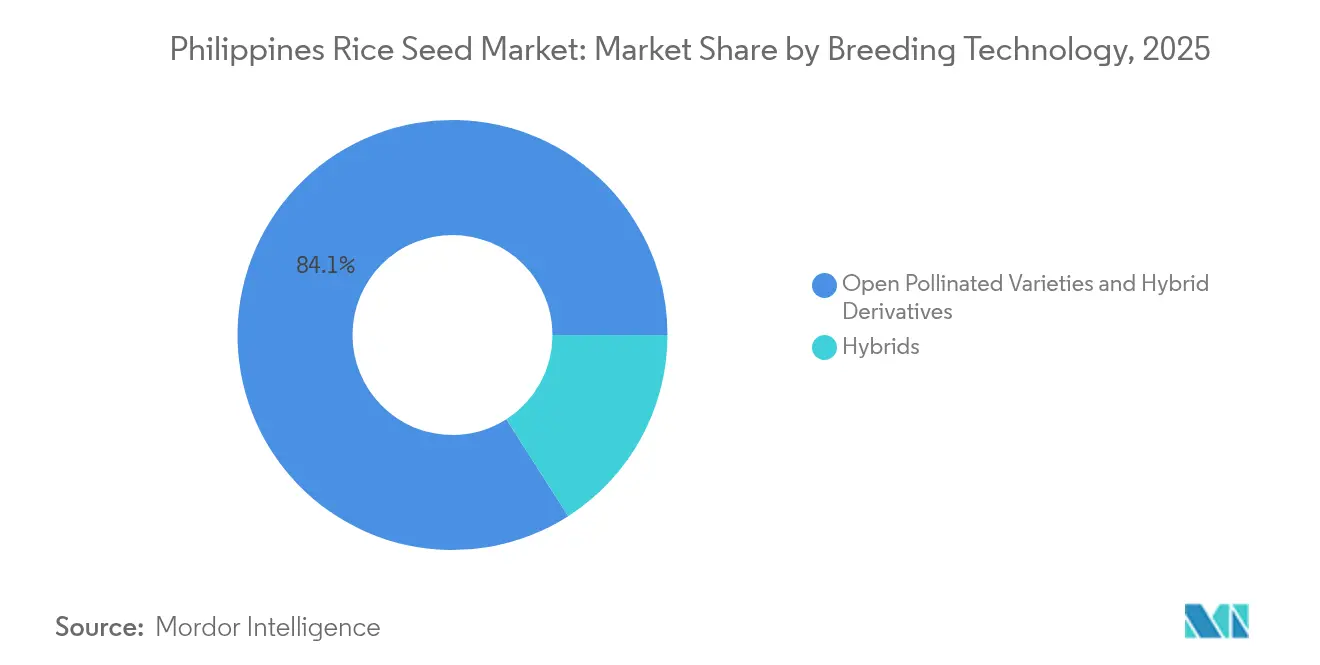

- By breeding technology, Open Pollinated Varieties and Hybrid Derivatives led with 84.05% of the Philippines rice seed market share in 2025; hybrids are projected to expand at a 4.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Rice Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government hybrid-seed subsidy expansion | +1.2% | National, concentrated in Central Luzon and Mindanao | Medium term (2-4 years) |

| Re-entry of private transgenic events post-biosafety rules revision | +0.8% | National, early adoption in Luzon commercial farms | Long term (≥ 4 years) |

| Climate-smart seed demand after 2024 El Niño losses | +0.6% | Western Visayas, Central Luzon, and Cagayan Valley | Short term (≤ 2 years) |

| Rapid mechanization of mid-size farms raising certified-seed adoption | +0.5% | Central Luzon and Mindanao estate farms | Medium term (2-4 years) |

| Growing rice-export ambitions of Mindanao estate growers | +0.3% | Mindanao, spillover to Visayas | Long term (≥ 4 years) |

| Digital agro-dealer networks are shortening replacement cycles | +0.2% | Urban-adjacent farming areas, and Central Luzon | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Hybrid-Seed Subsidy Expansion

The government extended the RCEF through 2031 and tripled annual funding to PHP 30 billion (USD 518 million), channeling resources into hybrid-seed distribution, mechanization support, and extension services[1]Source: Philippine Agency, “Rice Competitiveness Enhancement Fund Extension,” pna.gov.ph. The Binhi e-Padala voucher platform issues claim codes via text, cutting bottlenecks and letting farmers choose seed brands that suit local conditions. Coupled with the Development Bank of the Philippines credit windows, the subsidy lowers upfront seed costs for price-sensitive smallholders and accelerates certified-seed penetration in the Philippines rice seed market. Industry participants report that voucher-redeeming farmers increased their seed replacement frequency from every two cycles to every single cycle, boosting demand predictability for suppliers. Because the subsidy is embedded in a long-term budget, seed firms can plan multiyear production contracts with outgrowers, stabilizing supply. This predictable cash flow also underpins private investment in domestic seed processing and cold-storage capacity, a critical enabler for hybrid viability across island provinces.

Re-entry of Private Transgenic Events Post-Biosafety Rules Revision

Republic Act 12078, enacted in 2024, streamlined biosafety protocols and revived private-sector interest in gene-edited rice, positioning the Philippines rice seed market as a regional innovation hub[2]Source: USDA Foreign Agricultural Service, “Philippines Grain and Feed Annual,” fas.usda.gov. Collaboration between the International Rice Research Institute and BASF on CRISPR-enabled varieties underscores the convergence of global technology and local germplasm resources. Early commercial focus targets herbicide tolerance and virus resistance, traits that estate growers view as cost-saving substitutes for chemical control. Adoption hinges on farmer perception, segregation mechanisms, and intellectual-property compliance, dimensions that may delay widespread diffusion. Companies with in-house stewardship teams are building field-based compliance protocols that bundle seed, training, and audit services, thereby easing regulatory burdens for cooperatives. Over the forecast period, these integrated offerings are expected to anchor a premium niche within the Philippines rice seed market for tech-intensive growers.

Climate-Smart Seed Demand After 2024 El Niño Losses

The 2024 El Niño episode cut main-season yields by 3% below the five-year average in Western Visayas, Central Luzon, and Cagayan Valley[3]Source: DOST-PCAARRD, “Project SARAi CL-SEAMS and SPidTech,” dost-pcaarrd.dost.gov.ph. Farmers responded by shifting toward early-maturing, drought-tolerant cultivars with 90–110-day cycles instead of the customary 120 days. PhilRice’s climate-smart mapping tool and Project SARAi’s satellite-driven advisories guide cultivar selection, aligning seed choice with localized rainfall forecasts. Weather-indexed insurance bundled with seed purchases further cushions risk, encouraging adoption of higher-value varieties despite their price premium. The interplay of risk finance, precision advisories, and resilient genetics adds a new dimension to the Philippines rice seed market, intensifying competition among seed providers to demonstrate variety performance under stress. As climate volatility persists, the demand curve is likely to tilt in favor of hybrids that combine drought tolerance with high harvest index, sustaining long-run market expansion.

Rapid Mechanization of Mid-Size Farms Raising Certified-Seed Adoption

Precision planters and direct seeding machines now pervade farms of 2–5 hectares, a group that planted barely of certified seed in 2024 according to field surveys. These machines require uniform seed size and germination, attributes seldom achieved with farmer-saved seed. Under RCEF’s mechanization wing, subsidies on high-speed transplanters slash capital costs, tipping the economics in favor of certified-seed packages. The mechanization–seed quality nexus deepens supplier engagement, as firms bundle agronomic advice, machinery calibration, and seed. These value-adding services represent a strategic wedge for differentiation in the Philippines rice seed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent brown-planthopper outbreaks cutting hybrid ROI | -0.9% | Western Visayas, Central Luzon, and Mindanao | Short term (≤ 2 years) |

| High royalty costs on patented CMS lines | -0.6% | National, affecting hybrid seed pricing | Medium term (2-4 years) |

| Informal seed reuse by smallholders | -0.4% | Rural areas, particularly the Visayas | Long term (≥ 4 years) |

| Fragmented last-mile cold storage infrastructure | -0.3% | Remote farming areas, island provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Brown-Planthopper Outbreaks Cutting Hybrid ROI

Brown planthopper infestation resurfaced across 18 provinces, causing USD 308,000 in crop losses and eroding hybrid profit margins. Excessive insecticide use destroyed natural predators, reinforcing pest resurgence and spreading ragged stunt and grassy stunt viruses. Surveillance under PhilRice’s Prime Project flagged incidence rates in Antique, Aklan, Capiz, Iloilo, and Negros Occidental. The absence of curative treatments obliges pre-emptive varietal resistance, driving up R&D outlays for seed companies. Hybrids without built-in resistance lose economic appeal, prompting some farmers to revert to inbred lines, thereby capping potential gains in the Philippines rice seed market.

High Royalty Costs on Patented CMS Lines

Cytoplasmic Male Sterility (CMS) technology remains concentrated among a handful of multinationals, and license fees can be tacked to hybrid production costs. Layered patents covering restorer lines and marker-assisted heterosis compound this burden, pushing cumulative royalty shares above 30% of gross seed revenue in extreme cases. Domestic breeders with limited cash flow struggle to carry these costs and often exit the hybrid segment, shrinking the competitive field. As a result, price-sensitive smallholders hesitate to swap farmer-saved seed for hybrids, muting volume growth in the Philippines rice seed market until royalty structures ease or local CMS alternatives mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrid Growth Outpaces Traditional Lines

Open Pollinated Varieties and Hybrid Derivatives commanded 84.05% of the Philippines rice seed market share in 2025, mirroring smallholders’ preference for recyclable seed that fits tight cash cycles. Producers operating on less than 2 hectares value genetic familiarity and the freedom to save seed across seasons, thereby limiting annual cash outflow and preserving locally adapted landraces. Certified inbred lines distributed under government subsidy programs further entrench this segment, as many farmers stick with varieties received through public channels.

Hybrids are registering the fastest advance, posting a 4.18% CAGR to 2031 and gradually chipping away at inbred dominance. Commercial farms in Mindanao and precision-mechanized holdings in Central Luzon prize hybrids for their yield advantage and uniform grain quality that meets export grades. Pilot studies under Digital Clustered Rice Farming highlight net-income gains when hybrids replace farmer-saved seed, bolstering the economic case for the switch. As mechanization spreads and subsidy vouchers lower acquisition costs, the Philippines rice seed market size attributed to hybrids is set to expand, even though absolute dominance by open-pollinated lines will persist in the short run.

Geography Analysis

Central Luzon generates a good share of national paddy output and exhibits the country’s highest certified-seed penetration rates. Well-developed irrigation, contiguous landholdings, and proximity to Manila’s input markets underpin early adoption of hybrids and precision farming technologies, making the region the cornerstone of volume growth in the Philippines rice seed market. Government pilot hubs for mechanization and biosafety-approved trials also cluster here, giving seed companies a concentrated test bed for technology rollouts.

Mindanao follows as the fastest-growing geography, propelled by estate operations targeting premium export channels. All-year rainfall and multiple-cropping schedules amplify seed turnover, so estates adopt hybrids to secure consistently high milling recovery and tensile strength. Improved port infrastructure in Davao del Sur reduces freight bottlenecks, allowing seed plants in Bukidnon to deliver fresh lots within 48 hours, safeguarding viability. As export premium contracts multiply, Mindanao’s contribution to the Philippines rice seed market size is forecast to widen at a brisk clip, outpacing national averages.

Western Visayas, despite strong production potential, wrestles with recurrent brown-planthopper outbreaks and fragmented farm structures that curb mechanization. Limited cold-chain capacity and inter-island freight gaps further restrict certified-seed availability. Government voucher schemes and Project SARAi advisories are gradually improving access, yet farmer reliance on saved seed remains high. The region illustrates the structural ceiling confronting the Philippines rice seed market until integrated pest management, logistics investments, and behavior change converge to unlock suppressed demand.

Competitive Landscape

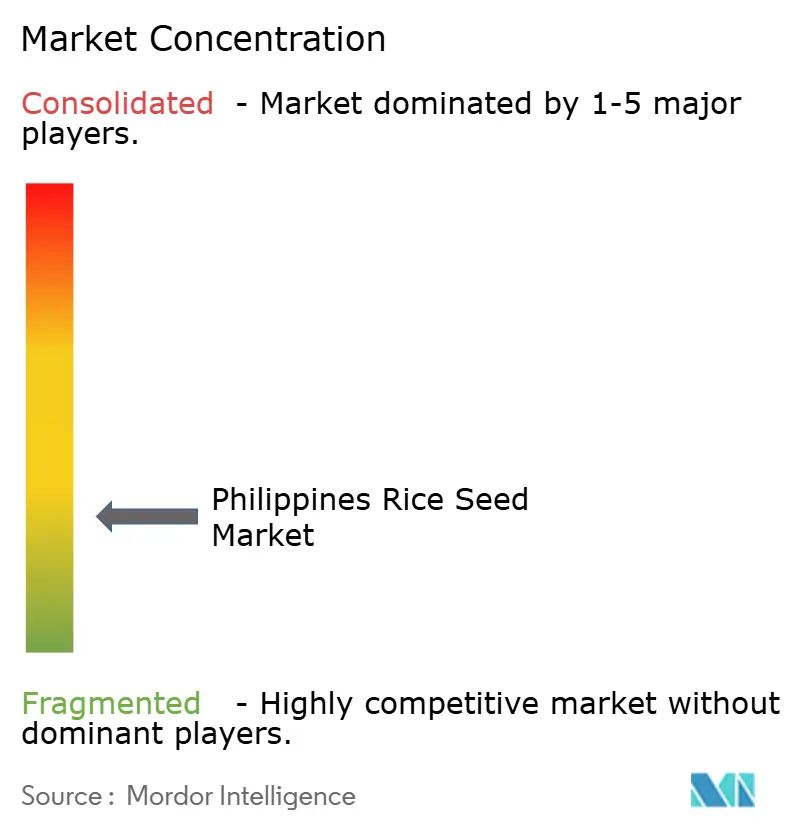

Market structure is fragmented, with multinationals such as Bayer AG, Syngenta Group, Yuan Longping High-Tech Agriculture Co. Ltd, and Advanta Seeds - UPL vying alongside homegrown leaders like SL Agritech Corporation (SLAC). Multinationals leverage proprietary CMS platforms and global R&D networks to push trait-stacked hybrids, while SL Agritech capitalizes on local network depth and price agility. Regulatory liberalization in 2024 injected new life into transgenic pipelines, allowing firms with biotech assets to differentiate through virus-resistant or herbicide-tolerant offerings. Intellectual property around CMS and CRISPR creates high entry barriers, funneling hybrid activity toward companies with robust patent portfolios.

Digital transformation is re-shaping competition. Seed firms now bundle satellite-based crop diagnostics, mobile credit scoring, and input e-commerce with seed sales to lock in farmer loyalty. For instance, Corteva’s pilot with an IoT farm-monitoring partner in Nueva Ecija records real-time canopy temperature and issues irrigation alerts, anchoring hybrid performance. Smaller distributors that lack digital reach risk marginalization, accelerating concentration within the Philippines rice seed market.

Pest resurgence and climate stress have nudged firms into collaborative R&D. Bayer and PhilRice co-invest in brown-planthopper-resistant lines using introgressed wild-rice genes, sharing field data to shorten breeding cycles. SL Agritech signed a memorandum with a regional cold-storage provider to secure year-round warehousing, aiming to cut germination loss. Such alliances suggest a competitive race not solely on genetics but on end-to-end service and logistics, sharpening differentiation in the years ahead.

Philippines Rice Seed Industry Leaders

Advanta Seeds - UPL

Bayer AG

SL Agritech Corporation (SLAC)

Syngenta Group

Yuan Longping High-Tech Agriculture Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The International Rice Research Institute partnered with BASF to accelerate CRISPR-derived disease-resistant rice, with field trials slated for 2025.

- December 2024: The Philippine government extended RCEF through 2031 and tripled its annual allocation to PHP 30 billion (USD 518 million), broadening seed, mechanization, and extension support.

- December 2024: Republic Act (RA) 12078, signed in the Philippines in December, maintains existing biosafety regulations for transgenic rice. The law amends the Rice Tariffication Law (RA 11203) by extending the Rice Competitiveness Enhancement Fund.

Philippines Rice Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology.Breeding Technology

| Hybrids | Non-Transgenic Hybrids |

| Transgenic Hybrids | |

| Other Traits | |

| Open Pollinated Varieties and Hybrid Derivatives |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids |

| Transgenic Hybrids | ||

| Other Traits | ||

| Open Pollinated Varieties and Hybrid Derivatives |

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms