RFID In Pharmaceuticals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.81 Billion |

| Market Size (2031) | USD 6.96 Billion |

| Growth Rate (2026 - 2031) | 7.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

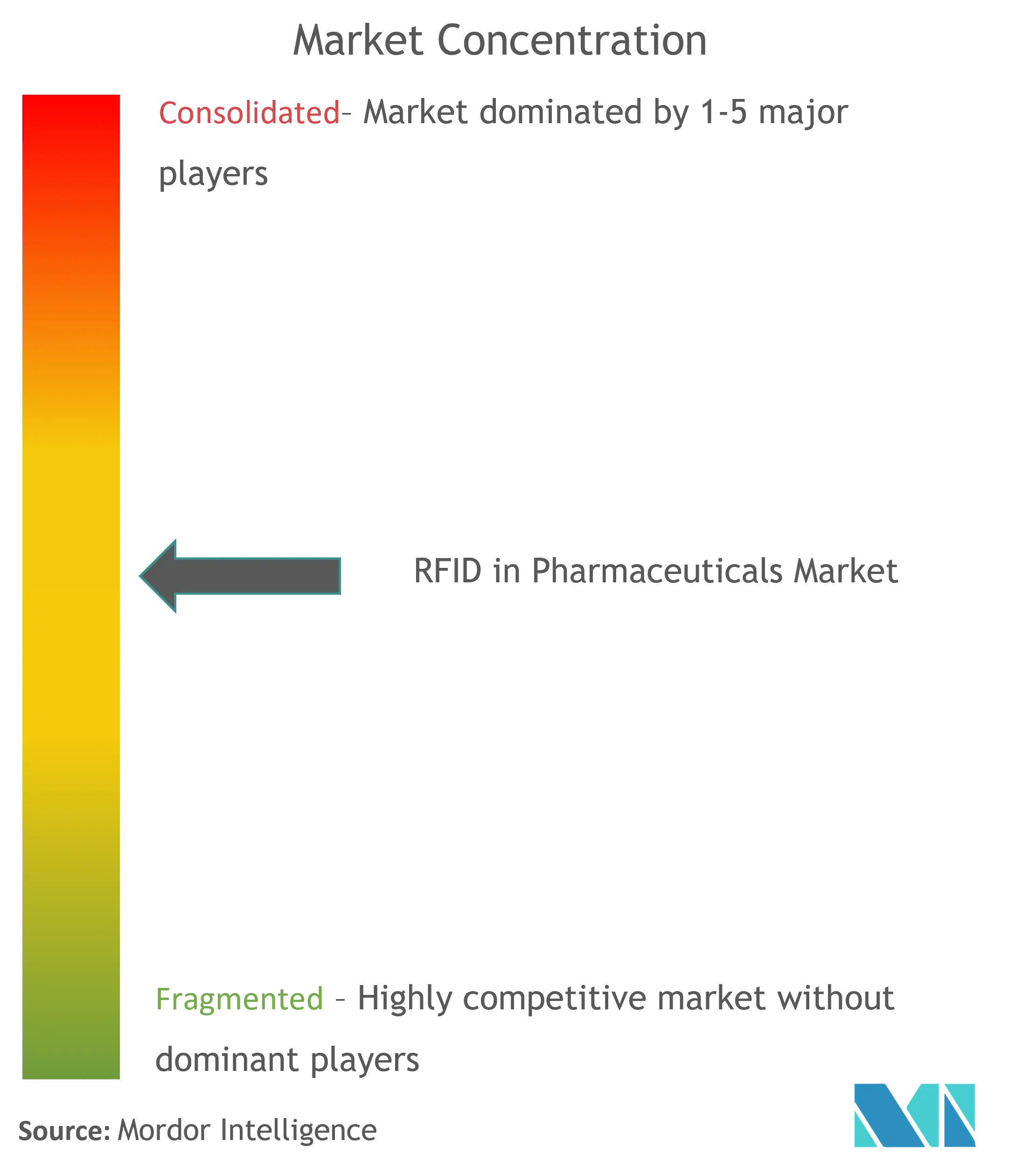

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RFID In Pharmaceuticals Market Analysis by Mordor Intelligence

RFID In Pharmaceuticals market size in 2026 is estimated at USD 4.81 billion, growing from 2025 value of USD 4.47 billion with 2031 projections showing USD 6.96 billion, growing at 7.66% CAGR over 2026-2031. Strong demand for end-to-end traceability, enforcement of the Drug Supply Chain Security Act (DSCSA) in the United States, and wider adoption of serialization in the European Union are pushing pharmaceutical companies to move beyond barcodes toward real-time item-level data capture. Capital spending has shifted toward integrated platforms that convert raw tag reads into predictive supply-chain intelligence, while falling tag costs reduce the payback period on new deployments. Temperature-controlled biologics, omnichannel retail pharmacies, and next-generation biologic therapies add further urgency for continuous environmental monitoring. Competitive rivalry remains moderate because legacy auto-ID vendors, enterprise software leaders, and specialist healthcare start-ups each own distinctive pieces of the value chain, creating room for niche innovators.

Key Report Takeaways

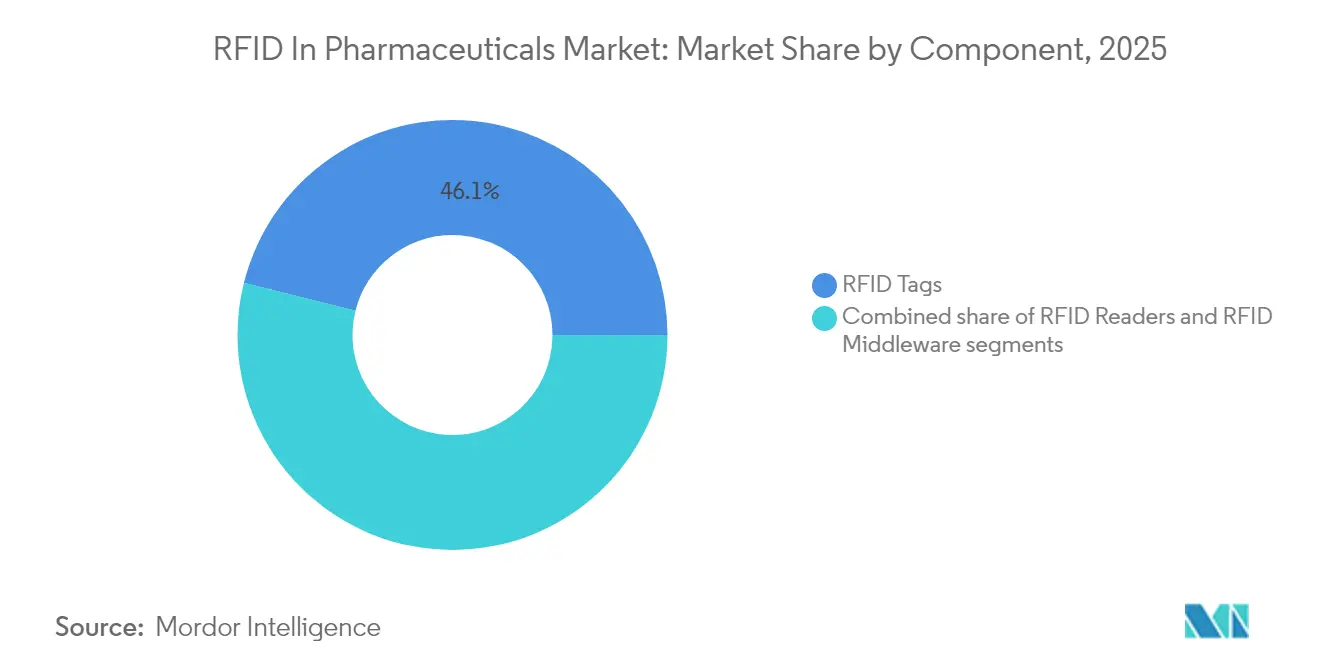

- By component, RFID Tags led with 46.10% revenue share in 2025, whereas RFID Middleware is projected to log the fastest 9.22% CAGR through 2031.

- By type, chipped RFID held 70.85% of the RFID In Pharmaceuticals market share in 2025; chipless RFID is forecast to grow at 9.31% CAGR to 2031.

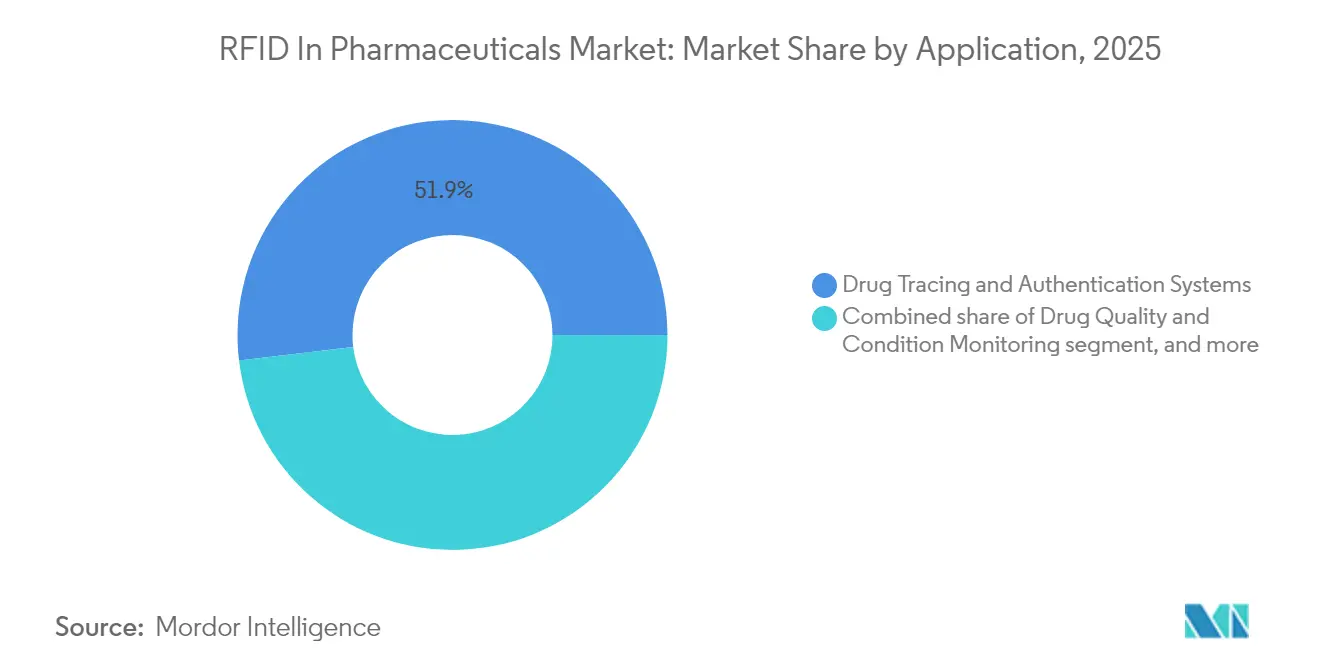

- By application, Drug Tracing & Authentication Systems accounted for 51.90% share of the RFID In Pharmaceuticals market size in 2025, while Temperature-Controlled Logistics is rising at 10.35% CAGR.

- By end user, Drug Manufacturers commanded 49.10% revenue share in 2025; Retail & e-Pharmacies are advancing at 9.88% CAGR through 2031.

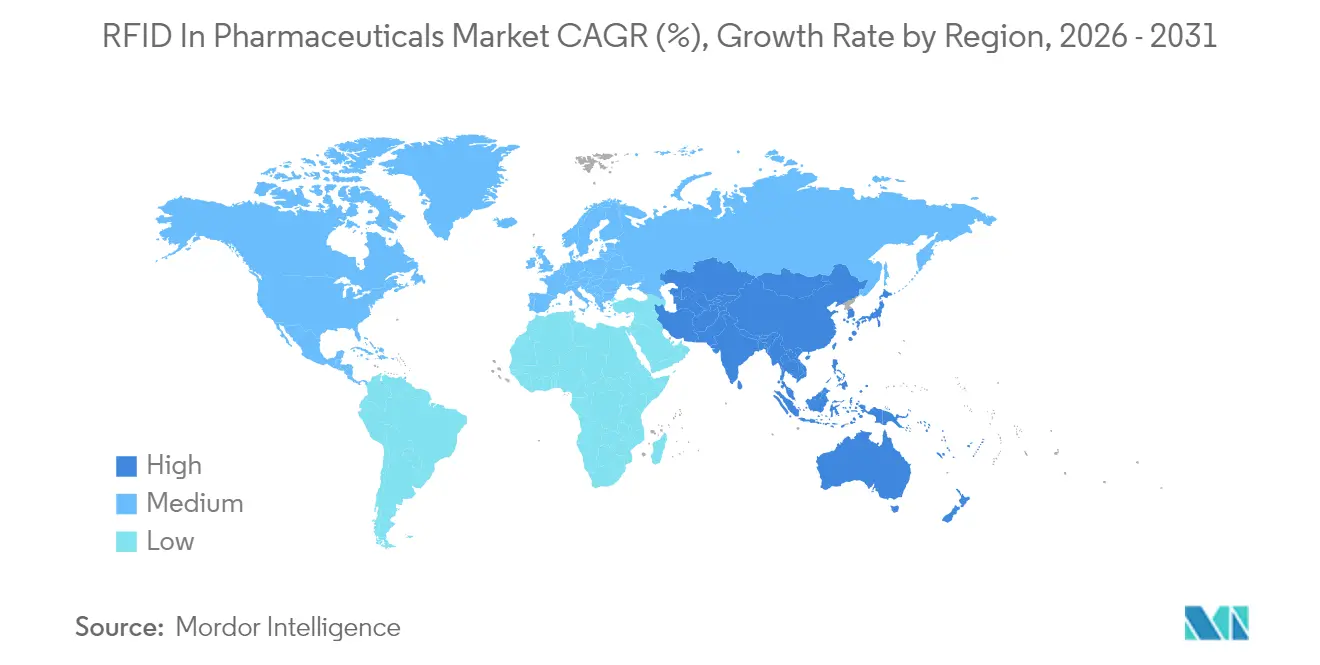

- Geographically, North America captured 43.10% revenue in 2025; Asia-Pacific is the fastest-expanding region at 8.31% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global RFID In Pharmaceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global pharmaceutical supply chain complexity | +1.8% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Stringent drug safety and anti-counterfeiting regulations | +2.1% | North America and EU primary, APAC emerging | Short term (≤ 2 years) |

| Expansion of cold-chain biologics and specialty therapies | +1.5% | Global, led by North America and EU | Long term (≥ 4 years) |

| Growing hospital automation and inventory visibility demands | +1.2% | North America and EU core, APAC accelerating | Medium term (2-4 years) |

| Falling RFID tag costs and improved read accuracy | +0.9% | Global | Short term (≤ 2 years) |

| Rise of omni-channel pharmacies and direct-to-patient delivery | +1.1% | North America and EU primary, urban APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Pharmaceutical Supply Chain Complexity

Modern drug supply chains span 15–20 hand-offs that include contract manufacturing and logistics partners. In 2024 these intermediaries represented 49.56% of end-user deployments, underscoring how visibility gaps expose companies to compliance and counterfeiting risks. RFID enables automatic capture at every node, avoiding human error that barcode workflows create in high-volume hubs. The FDA’s June 2024 guidance calls for interoperable systems able to exchange granular movement events, positioning RFID as the practical route to meet such data hand-shaking demands[1]U.S. Food & Drug Administration, “Interoperable Systems Guidance for Drug Distribution Security,” fda.gov. Early adopters benefit from fewer stock-outs and lower recall costs, prompting peers to accelerate programs. High-value specialty drugs heighten urgency because temperature excursions or delays can spoil an entire lot, turning real-time monitoring from a luxury into a necessity.

Stringent Drug Safety and Anti-Counterfeiting Regulations

Full DSCSA enforcement in November 2024 and earlier EU Falsified Medicines Directive mandates have converted serialization from best practice to legal requirement. Industry executives now target automated verification rather than manual line-side scanning, a preference that favors RFID’s near-zero read latency. Analyst commentary from TraceLink projects end-to-end digitalization to dominate 2025 budgets. The FDA’s September 2024 draft on innovative manufacturing highlights real-time data proofs as a route to quicker regulatory reviews. Authentication stakes are high because counterfeit drugs account for an estimated 10% of global supply. RFID tags that embed tamper indicators satisfy emerging compliance audits and lower investigation time when anomalies appear.

Expansion of Cold-Chain Biologics and Specialty Therapies

Biologics now exceed 40% of global pharmaceutical revenue. Spoilage costs touch USD 35 billion per year when shipments stray outside allowable temperatures. RFID tags with embedded sensors deliver continuous readings that barcodes cannot produce, providing immediate alerts across transit legs. Avery Dennison’s Saga Card, launched with Controlant, blends passive RFID, cellular connectivity, and cloud analytics to give an unbroken cold-chain record. Predictive models are beginning to use weather forecasts and route data to reroute shipments proactively. As cell- and gene-therapy volumes rise, item-level custody chains become critical, and RFID offers the only practical toolset for personalized payloads.

Growing Hospital Automation and Inventory Visibility Demands

Hospitals are automating pharmacy operations to curb labor shortages and expiry waste. Bluesight’s KitCheck platform documents 96% faster inventory counts and 91.6% fewer expired medications after RFID rollout. Oracle’s Fusion Cloud now embeds RFID signals in replenishment workflows, letting nurses consume drugs at point-of-care while the back-office triggers reorder lines automatically. Capital tied up in stock drops once real-time data exposes slow-moving items. Workflow gains depend on cross-department coordination; pilot programs that include nursing, pharmacy, and IT leaders achieve the quickest payback.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial system integration and validation expenses | -1.4% | Global, especially small and mid-size firms | Short term (≤ 2 years) |

| Limited radio-frequency performance in metal and liquid environments | -0.8% | Global, impacting manufacturing floors | Medium term (2-4 years) |

| Data security, privacy, and regulatory compliance concerns | -0.7% | Global, heightened in EU and North America | Short term (≤ 2 years) |

| Fragmented global standards and interoperability issues | -0.6% | Global, pronounced across emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial System Integration and Validation Expenses

Full-scale pharmaceutical RFID deployments range from USD 500,000 to USD 5 million when factoring enterprise resource planning links, 21 CFR Part 11 validation, and staff training. Annual support often equals 25–30% of capital outlay, a hurdle for mid-sized firms. Cloud-hosted SaaS pricing models are easing entry barriers by spreading costs over subscription periods, yet validation burdens remain because regulators scrutinize electronic records and audit trails with the same rigor as production equipment.

Limited Radio Frequency Performance in Metal and Liquid Environments

Read rates fall 40–60% in cleanrooms packed with stainless-steel vessels or liquid-filled vials. Specialized antenna geometries and pharmaceutical-grade tags mitigate but do not eliminate dead zones. Alternative frequencies and chipless materials improve reliability while raising unit costs 30–50% over standard retail tags. Hybrid solutions that overlay 2D codes with RFID chips are gaining attention because they work even when RF reflections degrade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Middleware Drives Integration Innovation

RFID Tags captured 46.10% revenue in 2025, confirming their indispensable role as the serialized identifier anchoring every data record within the RFID In Pharmaceuticals market. However, Middleware is accelerating at a 9.22% CAGR because decision-makers want dashboards and predictive analytics rather than raw tag reads. Oracle embedded RFID pipelines inside its Fusion Cloud Supply Chain suite in September 2024, illustrating how enterprise platforms position themselves as the compliance nerve center. Middleware converts tag pings into exception alerts, recall triggers, and automated Electronic Product Code Information Services (EPCIS) messages that regulators demand. Handheld and fixed Readers bridge physical capture with these analytic layers, ensuring closed-loop visibility from factory to bedside. Continuous investment spotlighting software underscores how the RFID In Pharmaceuticals market is shifting from discrete hardware projects to integrated digital ecosystems.

RFID In Pharmaceuticals market implementations increasingly pair low-cost passive tags with cloud analytics to keep lifetime ownership costs predictable. HF, UHF, and NFC variants dominate daily operations, while specialty biologic shipments justify battery-assisted tags able to stream temperature data every few minutes. Middleware’s rise signals a maturity phase where companies regard RFID data as a strategic asset feeding demand forecasts, quality dashboards, and automatic DSCSA compliance reports rather than a siloed inventory tool. This transition cements the RFID In Pharmaceuticals market’s role in broader pharmaceutical digitalization roadmaps.

By Type: Chipless Innovation Challenges Traditional Dominance

Chipped tags retained 70.85% share in 2025 because silicon-based UHF products enjoy global certification and reliable performance in regulated spaces. Yet Chipless RFID is expanding at 9.31% CAGR on the strength of lower material costs and resilience around metal surfaces. Pharmaceutical production suites filled with stainless equipment create radio reflections that impair conventional labels. Chipless substrates transmit unique electromagnetic signatures without integrated circuits, cutting per-tag costs up to 60%. Zebra Technologies’ M-Trust prototype with Merck KGaA merges traditional scanners with covert chipless pigments to prove authenticity in seconds. Such hybrid designs show how incumbents protect installed bases while easing customers toward next-generation labels.

Early chipless rollouts support items that are hard to tag, including foil blister packs and vial stoppers. Regulation still favors deterministic serial numbers, so pilots often append a human-readable code to satisfy inspectors. Nonetheless, as labs validate that spectral fingerprints cannot be counterfeited easily, chipless adoption will climb, especially in emerging markets where unit economics dominate vendor selection. The evolution reaffirms that the RFID In Pharmaceuticals market rewards solutions that tackle both cost and performance hurdles.

By Application: Temperature Monitoring Drives Specialized Growth

Drug Tracing & Authentication Systems owned 51.90% revenue in 2025 as serialization compliance pushed every manufacturer to embed unique identities on saleable units. Yet Temperature-Controlled Logistics is rising fastest at 10.35% CAGR, mirroring the boom in monoclonal antibodies and cell therapies that must remain within narrow temperature bands. Passive sensors attached to vials now store excursion data for auditors, while active trackers broadcast continuous feeds to cloud dashboards that logistics planners monitor in real time. The RFID In Pharmaceuticals market size for temperature-control sub-applications is projected to widen steadily as biologics expand their share of the global drug pipeline.

Cold-chain failures destroy product worth billions; therefore stakeholders now budget proactively for in-transit analytics. Avery Dennison and Controlant co-developed the Saga Card to overlay cellular telemetry on RFID check-points, adding redundancy that regulators appreciate. Drug Quality & Condition Monitoring tags that sense shock or humidity are also penetrating vaccine programs, providing a holistic view of product integrity. These niche innovations demonstrate that the RFID In Pharmaceuticals industry evolves in lock-step with therapeutic science.

By End User: Retail Transformation Accelerates Adoption

Drug Manufacturers accounted for 49.10% revenue in 2025 by embedding tags on packaging lines to satisfy DSCSA and EU FMD rules. Retail & e-Pharmacies, however, will post the quickest 9.88% CAGR through 2031 because last-mile delivery verification and home-based therapies necessitate item-level status confirmation. The RFID In Pharmaceuticals market size tied to retail channels is scaling as consumers demand assured authenticity for high-value prescriptions delivered directly to residences.

Hospitals & Clinics adopt RFID to automate crash-cart replenishment and reduce controlled-substance discrepancies, while Wholesale & Distribution Centres invest to secure their central role amid direct-to-patient shifts. Contract manufacturers and CROs view RFID as a differentiator when courting sponsors; verified custody data help win outsourcing bids. This end-user mosaic confirms that the RFID In Pharmaceuticals market grows whenever traceability moves downstream toward patients.

Geography Analysis

North America controlled 43.10% of 2025 revenue after DSCSA’s final compliance date forced complete serialization and event capture across supply chains. The RFID In Pharmaceuticals market gained critical mass as Pfizer, Johnson & Johnson, and Merck retrofitted production and distribution assets, catalyzing uptake across contract partners. Oracle, Zebra Technologies, and TraceLink capitalized by positioning cloud analytics as an out-of-the-box route to FDA audit readiness. Canada and Mexico ride the same regulatory wave by aligning exports with U.S. handling codes, making North American supply networks an interoperable RFID corridor.

Asia-Pacific is expanding at an 8.31% CAGR, the fastest regional pace in the RFID In Pharmaceuticals market. China and India, as leading generic suppliers, tag bulk product to assure western buyers of pedigree, while Japan and South Korea deploy RFID for biologic cold chains. Singapore’s biologics cluster and Australia’s domestic vaccine programs adopt item-level tracking to meet Good Distribution Practice audits. Regional regulators are coordinating under PIC/S GMP, creating a harmonized compliance baseline that encourages cross-border implementations.

Europe registers steady uptake because the EU Falsified Medicines Directive obliges pharmacy-level verification. Germany, Switzerland, and Ireland—home to many high-value manufacturing sites—leverage RFID to satisfy both FMD and forthcoming Digital Product Passport rules. Sustainability directives add another pull, as RFID-enabled reuse programs help reduce packaging waste. The consistent momentum affirms that every major geography now embeds RFID as a standard defensive line against counterfeit drugs.

Competitive Landscape

The industry shows moderate fragmentation. Hardware specialists such as Zebra Technologies and Impinj dominate reader platforms, but software and analytics are rapidly concentrating around players like Oracle and TraceLink that offer validated compliance workflows[3]Zebra Technologies, “Asset Intelligence & Tracking Q1 2025 Results,” zebra.com. Avery Dennison extends into cloud networks through its Controlant tie-up, signaling that former label suppliers now evolve into end-to-end visibility providers. Bluesight’s acquisition by Thoma Bravo highlights growing private-equity activity as investors seek scale advantages in hospital automation tools.

Strategic collaborations increasingly bundle authentication pigments, AI analytics, and connectivity in single offerings. Identiv-Novanta’s 2025 healthcare OEM pact exemplifies a push to shorten device makers’ design cycles by embedding complete RFID modules. Ambient IoT entrants such as Wiliot approach the sector with battery-free sensors, yet regulatory acceptance remains cautious. Overall, data analytics rather than tag manufacture is shaping durable advantages, pushing vendors to build pharmaceutical domain knowledge or partner with those who already have it.

RFID In Pharmaceuticals Industry Leaders

Avery Dennison Corporation

Zebra Technologies Corp.

Impinj Inc.

CCL Industries (Smartrac)

Fresenius Kabi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zebra Technologies and Merck KGaA unveiled the M-Trust platform to pair handheld scanners with security-pigment detection for on-the-spot product verification.

- February 2025: Identiv partnered with Novanta to pre-integrate RFID inlays and readers for healthcare device OEMs.

- January 2025: BD showcased the BD iDFill prefillable syringe ID system at Pharmapack 2025, embedding RFID inside glass barrels for automatic fill-and-finish traceability.

- January 2025: Zebra Technologies released an Android NFC smartphone featuring integrated RFID reading for mobile hospital workflows.

- October 2024: BD and ten23 health partnered on RFID-enabled prefillable syringes to streamline aseptic manufacturing.

Global RFID In Pharmaceuticals Market Report Scope

As per the scope of the report, RFID (radio-frequency identification) is a technology that uses electromagnetic fields to identify and track tags attached to objects automatically. The RFID in pharmaceuticals market is segmented by component, application, type, and geography. The component segment is further divided into RFID readers, RFID tags, and RFID middleware. The application segment is further bifurcated into chipped RFID and chipless RFID. The type segment is further segmented into drug tracing systems, drug quality management, and other types. The geography segment is further segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.

| RFID Readers | Handheld Readers |

| Fixed Readers | |

| RFID Tags | Passive (HF, UHF, NFC) |

| Active & BAP (Battery-Assisted Passive) | |

| RFID Middleware |

| Chipped RFID |

| Chipless RFID |

| Drug Tracing & Authentication Systems |

| Drug Quality & Condition Monitoring |

| Other Applications |

| Drug Manufacturers |

| Wholesale & Distribution Centres |

| Hospitals & Clinics |

| Retail & E-Pharmacies |

| Contract Research / Manufacturing Organisations (CROs/CMOs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | RFID Readers | Handheld Readers |

| Fixed Readers | ||

| RFID Tags | Passive (HF, UHF, NFC) | |

| Active & BAP (Battery-Assisted Passive) | ||

| RFID Middleware | ||

| By Type | Chipped RFID | |

| Chipless RFID | ||

| By Application | Drug Tracing & Authentication Systems | |

| Drug Quality & Condition Monitoring | ||

| Other Applications | ||

| By End User | Drug Manufacturers | |

| Wholesale & Distribution Centres | ||

| Hospitals & Clinics | ||

| Retail & E-Pharmacies | ||

| Contract Research / Manufacturing Organisations (CROs/CMOs) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the RFID In Pharmaceuticals market?

The RFID In Pharmaceuticals market stands at USD 4.81 billion in 2026.

How fast is the RFID In Pharmaceuticals market expected to grow?

The market is forecast to rise at a 7.66% CAGR, reaching USD 6.96 billion by 2031.

Which component segment is growing the quickest?

RFID Middleware is the fastest-advancing component, expanding at 9.22% CAGR as companies seek integrated analytics.

Why is Asia-Pacific the fastest-growing region?

Manufacturing expansion in China and India, coupled with regulatory harmonization across ASEAN, drives an 8.31% CAGR in Asia-Pacific.

What regulatory changes are driving adoption in North America?

Full enforcement of the DSCSA in November 2024 now requires end-to-end traceability, making RFID implementations effectively mandatory.

Which application area shows the highest growth?

Temperature-Controlled Logistics leads application growth at 10.35% CAGR due to the surge in biologics and other cold-chain therapies.

Page last updated on: