Pet Furniture Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.27 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

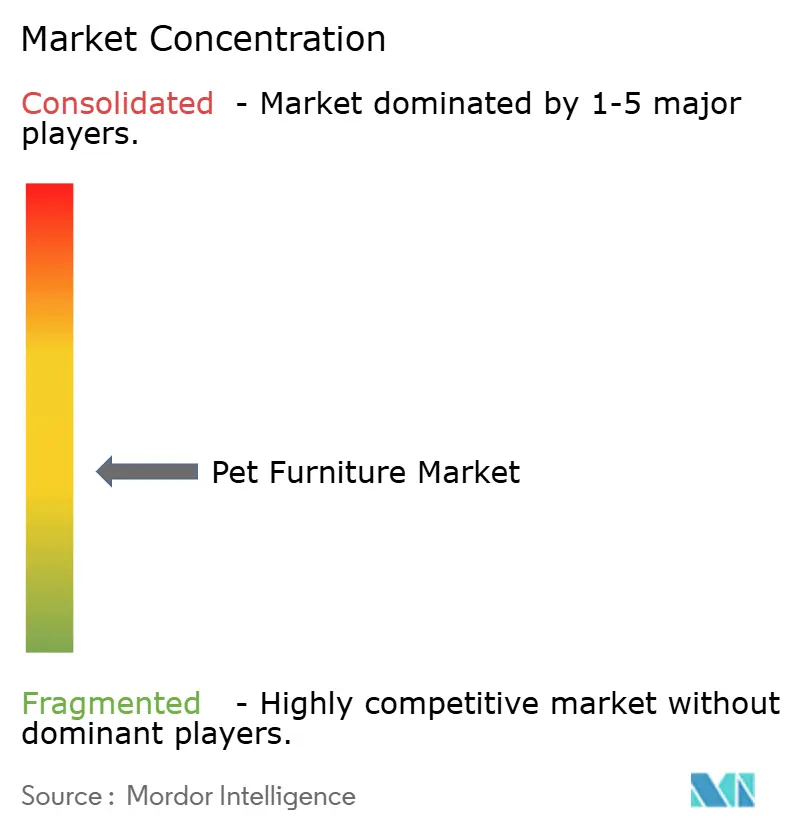

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Furniture Market Analysis by Mordor Intelligence

The pet furniture market size is projected to expand from USD 4.03 billion in 2025 and USD 4.27 billion in 2026 to USD 5.71 billion by 2031, registering a CAGR of 5.98% between 2026 to 2031. Growth is rooted in higher pet ownership, rising discretionary spending, and the repositioning of furniture from basic utility to an extension of home décor. Beds and sofas remain core purchases, yet multifunctional designs that conceal litter boxes or double as side tables are gaining traction as apartments shrink in major cities. E-commerce captures the largest channel share as direct-to-consumer models bypass specialty retail markups, while subscription programs increase customer lifetime value. Sustainability, wellness features, and AI-enabled customization are emerging as must-have attributes rather than optional add-ons, forcing incumbents to upgrade materials, integrate sensors, and shorten lead times.

Key Report Takeaways

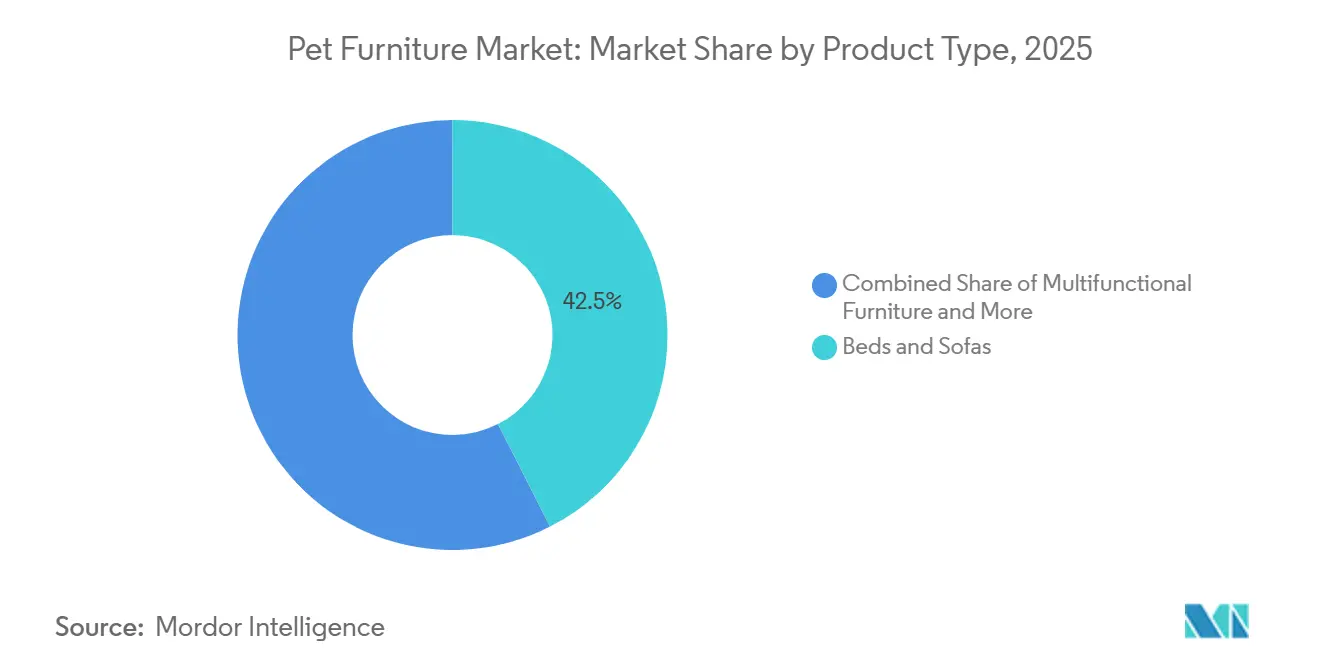

- By product type, beds and sofas accounted for 42.5% of the pet furniture market size in 2025, while multifunctional furniture is projected to expand at an 8.9% CAGR through 2031.

- By pet type, dogs represented 43.0% of the pet furniture market size in 2025, and cats are growing at an 8.2% CAGR through 2031.

- By material, wood commanded 29.0% of the pet furniture market size in 2025, and sustainable substrates are rising at a 9.8% CAGR through 2031.

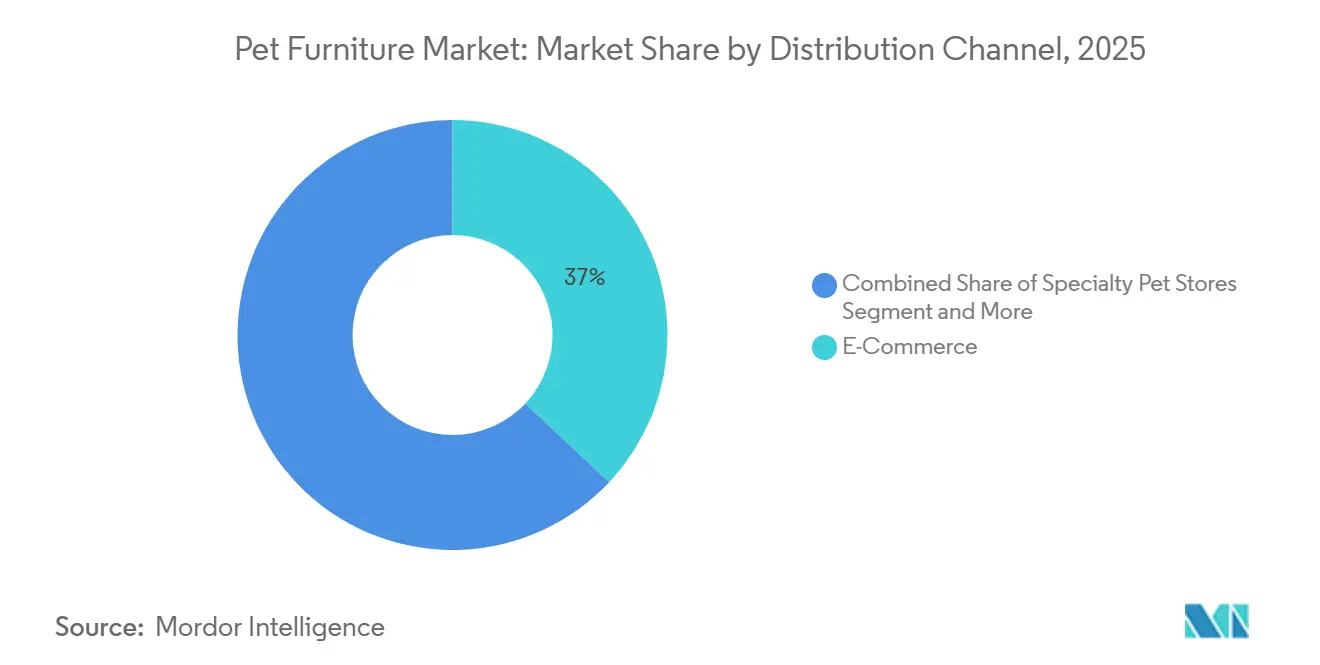

- By distribution channel, e-commerce accounted for 37.0% of the pet furniture market share in 2025 and is projected to advance at an 11.5% CAGR through 2031.

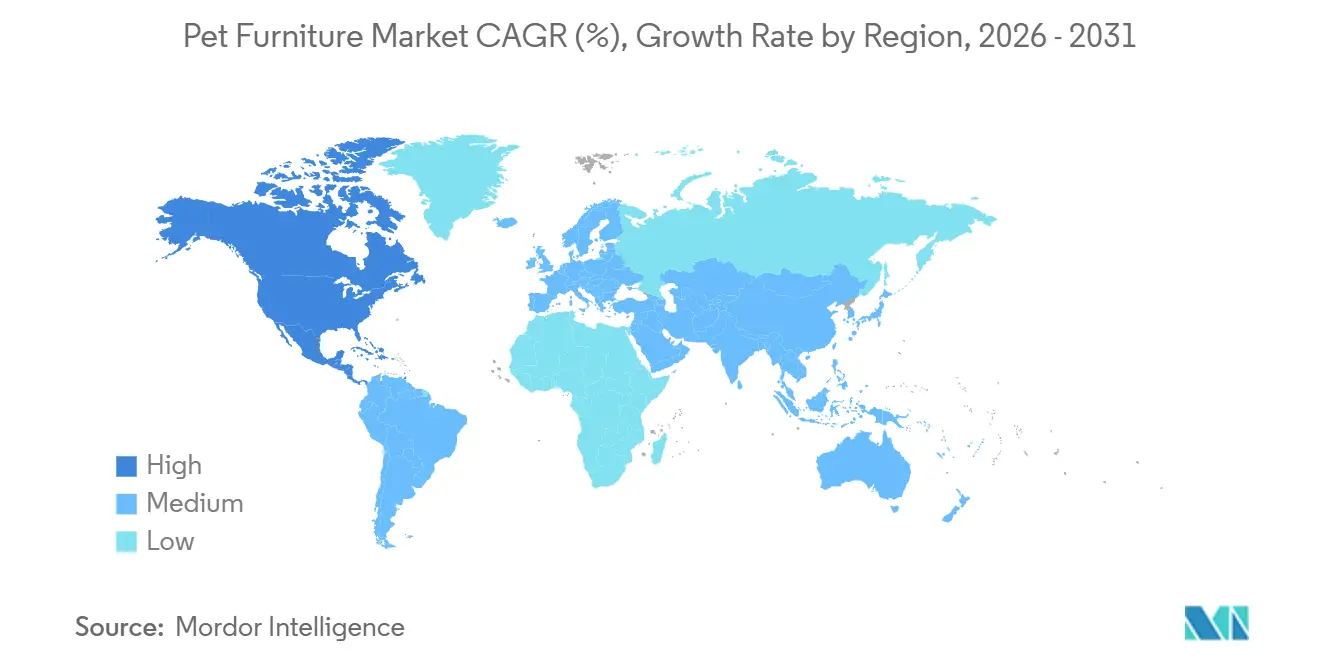

- By geography, North America holds a major share, accounting for 40% of the revenue in 2025, whereas the Asia-Pacific region is the fastest-growing geography, rising at an 8% CAGR through 2031.

- IKEA (Inter IKEA Group), Chewy, Inc., Petmate (Doskocil Manufacturing Company, Inc.), Midwest Metal Products Company, Inc., and Trixie Heimtierbedarf held a significant revenue share in 2025, reflecting the influence of high-volume retailers on product design and pricing.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Pet Furniture Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Impact of pet humanization on premium furniture trends | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Expansion of omnichannel and direct-to-consumer logistics | +1.5% | Global, led by North America and the Asia-Pacific | Short term (≤ 2 years) |

| Rising global pet adoption rates | +1.2% | Global, accelerating in Asia-Pacific, the Middle East, and South America | Long term (≥ 4 years) |

| Integration of biophilic and wellness-oriented designs | +0.7% | North America and Europe, emerging in the Asia-Pacific urban centers | Medium term (2-4 years) |

| Growth of pet-friendly co-living and co-working real-estate models | +0.5% | North America and Europe, early adoption in Asia-Pacific tier-1 cities | Long term (≥ 4 years) |

| Rapid scale-up of AI-guided mass-customization platforms | +0.6% | Global, fastest uptake in North America and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Impact of Pet Humanization on Premium Furniture Trends

Pet owners are increasingly dedicating discretionary income to furniture that aligns with human interior design standards, merging pet accessories with home decor. A 2025 Harris Poll revealed that 67% of United States pet owners created dedicated spaces in their homes for their pets. Additionally, Generation Z pet owners spent an average of USD 6,103 annually per pet, with 24% incurring pet-related debt [1]Source: Bank of America, “Consumer Spending Trends in Pet Care,” bankofamerica.com. This trend extends beyond consumables to durable goods, as consumers prefer items such as pet beds upholstered in performance fabrics that match their own sofas or cat trees finished in walnut veneer, rather than carpeted particle board. IKEA's May 2025 launch of the UTSADD pet furniture collection, developed in collaboration with veterinarians and tested with shelter animals, highlights recognition of pet furniture as a permanent category by mass-market retailers rather than a niche offering. Brands that do not incorporate therapeutic features risk losing market share to veterinary-endorsed lines, as pet owners increasingly seek veterinary advice before purchasing furniture for aging pets.

Expansion of Omnichannel and Direct-to-Consumer Logistics

Direct-to-consumer channels allow furniture brands to capture retail margins and implement subscription models that generate recurring revenue, significantly reshaping the competitive landscape. Chewy's Q2 FY2025 results reported net sales per active customer reaching a record USD 565, with 83% of sales driven by Autoship subscriptions. These subscriptions bundle furniture with consumables such as litter and treats, reducing customer acquisition costs and increasing customer lifetime value. This approach enables Chewy to subsidize furniture pricing and expand its market share in related categories. In the United Kingdom, 2024 Pet Care e-commerce data showed a 2.62% conversion rate and an average order value of USD 124. This data highlights that online furniture purchases are often part of basket-building behavior, where consumers add items like beds or scratchers to food orders to meet free shipping thresholds. Innovations in last-mile delivery, such as same-day fulfillment and buy-online-pick-up-in-store options, have reduced the time advantage previously held by specialty pet stores. These advancements enable online-only brands to compete on convenience while maintaining higher gross margins by avoiding the costs associated with physical retail locations.

Growth of Pet-Friendly Co-Living and Co-Working Real-Estate Models

Commercial real estate developers are incorporating pet amenities into co-living and co-working spaces to attract millennial and Generation Z tenants, creating institutional demand for durable, high-traffic furniture. Co-living operators such as Common and WeLive include pet-friendly units with built-in feeding stations, washable flooring, and communal pet lounges furnished with commercial-grade scratchers and beds designed to withstand daily use by multiple animals. The regulatory baseline expands the addressable market into affordable housing segments, where compact, washable, and fire-resistant furniture aligns with unit-size limits and sanitary standards. Institutional procurement cycles are longer and price-sensitive, favoring suppliers with volume manufacturing capacity and established distribution relationships over boutique brands, which may struggle to meet minimum order quantities or provide multi-year warranties required by property managers.

Rapid Scale-Up of AI-Guided Mass-Customization Platforms

Artificial intelligence is enabling furniture brands to offer bespoke dimensions, fabrics, and finishes at near mass production costs, thereby compressing lead times and reducing inventory risk. Chinese brand Pidan operates a configurator platform where consumers specify the cat tree height, scratching post diameter, and fabric color, then receive a custom-built unit within 14 days, leveraging flexible manufacturing cells that retool between orders. The system organizes stool and clump images into categorized clips, enabling veterinarians to review historical data during consultations, and pairs with occult blood test litter to form a closed-loop health-monitoring ecosystem. This data aggregation creates network effects, as PETKIT's AI learns from millions of litter-box usage experiences globally, improving diagnostic precision and creating a moat that competitors without similar data cannot replicate. Brands that fail to address these concerns may face consumer backlash or regulatory penalties, thereby undermining the competitive advantage that AI-enabled customization would otherwise provide.

Restraints Impact Analysis of Pet Furniture Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High average selling prices versus conventional furniture | -0.9% | Global, most acute in South America, Africa, and price-sensitive segments of the Asia-Pacific | Short term (≤ 2 years) |

| Limited product durability for highly active pets | -0.6% | Global, particularly in North America and Europe, where warranties are high | Medium term (2-4 years) |

| Compliance costs with evolving fire-safety and chemical standards | -0.4% | North America and Europe, emerging in the Asia-Pacific as regulations harmonize | Medium term (2-4 years) |

| Crowding from convertible human furniture substitutes | -0.3% | North America and Europe; limited impact in Asia-Pacific, where pet-specific designs dominate | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Product Durability for Highly Active Pets

Furniture designed for aesthetic appeal often lacks the structural integrity to withstand scratching, chewing, and repetitive use by energetic or large-breed pets, leading to warranty claims and negative reviews. An academic study published in 2024 found that 98% of cats use scratching posts, yet 41.67% still scratch household furniture, indicating that existing designs fail to fully satisfy feline scratching instincts and may require more durable substrates or alternative textures. Similarly, large-breed dogs weighing over 90 pounds can collapse beds constructed with lightweight frames and low-density foam, necessitating reinforced bases and memory foam cores that add cost and weight. K9 Carts, a manufacturer of orthopedic dog furniture, emphasizes custom-built wheelchairs and beds with measured fit to prevent pressure sores and accommodate changing mobility needs, highlighting the importance of durability and adjustability for senior or disabled pets.

Crowding from Convertible Human Furniture Substitutes

Mainstream furniture retailers are introducing pet-friendly designs that serve dual purposes, eroding demand for standalone pet furniture and intensifying price competition. IKEA's UTSADD collection includes beds and scratchers priced from USD 9.99, leveraging the company's global supply chain and flat-pack logistics to undercut specialty pet brands by 30% to 50% [2]Source: IKEA, “Launches First Pet Range,” insightdiy.co.uk. Similarly, Sauder Woodworking and other ready-to-assemble furniture manufacturers are adding pet-crate end tables and litter-box cabinets to their catalogs, targeting consumers who prefer furniture that blends into home decor rather than announcing pet ownership. This convergence blurs category boundaries and shifts purchasing decisions from pet specialty stores to home-furnishing retailers, where pet furniture competes on both price and aesthetics, rather than solely on pet-specific functionality. Convertible designs often sacrifice pet-specific features, such as orthopedic support, odor control, or washable covers, creating an opportunity for specialty brands to differentiate themselves on therapeutic attributes and durability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Pet Furniture Market Segment Analysis

By Product Type:

Multifunctional Designs Capture Urban DemandBeds and sofas accounted for 42.5% of the pet furniture market size in 2025, reflecting their status as foundational purchases for new pet owners. Petco's December 2025 product introduction included 800-plus new SKUs, featuring exclusive cat beds starting at USD 9.99 in fuzzy, plush pod, and shark-hooded styles, alongside music-themed scratchers shaped like guitars, records, and pianos that debuted in January 2026 as a multi-unit cat band, signaling retailers' recognition that furniture must double as conversation pieces to justify premium pricing. Suppliers that bundle complementary products, such as pairing orthopedic beds with raised feeders or scratchers with catnip toys, can increase average order values and reduce customer acquisition costs by encouraging multi-item purchases.

Multifunctional furniture is projected to expand at an 8.9% CAGR through 2031, as urban consumers seek space-saving designs that integrate pet amenities into human living areas. The shift toward multifunctional furniture is particularly pronounced in China, where 90% of pet owners reside in urban apartments, and 70% of purchases occur online, favoring compact designs that ship flat and assemble without tools. Brands that fail to offer modular, convertible, or dual-purpose furniture risk losing share to IKEA and other mass-market retailers entering the category with price-competitive alternatives.

By Pet Type:

Feline Furniture Outpaces Canine GrowthDogs represented 43.0% of the pet furniture market size in 2025, driven by their prevalence in suburban and rural households where outdoor access and larger living spaces accommodate bulkier furniture. Suppliers targeting both pet types must maintain separate design and manufacturing workflows, as materials, weight capacities, and aesthetic preferences diverge, which complicates inventory management and increases the proliferation of SKUs. Brands that specialize in a single pet type can achieve deeper category expertise and stronger brand associations; they often forgo cross-selling opportunities and remain vulnerable to shifts in pet ownership trends, such as the ongoing migration from dogs to cats in urban markets.

Cats are growing at an 8.2% CAGR through 2031 as urbanization and apartment living favor smaller, lower-maintenance pets. Japan's demographic inversion, where cats outnumber dogs, reflects space constraints in metropolitan areas where landlords prohibit dogs or charge higher deposits, making cats the default choice for renters. In 2023, this shift is mirrored in China, where 51% of the 68.62 million pet population are cats, concentrated in tier-1 cities such as Beijing, Shanghai, and Shenzhen, where high-rise apartments lack balconies or yards [3]Source: China Pet Industry Association, “China Pet Industry White Paper,” cpias.org.cn.

By Material:

Sustainable Substrates Gain Share Amid Certification PressureWood commanded 29.0% of the pet furniture market size in 2025, prized for its aesthetic appeal and structural integrity. Avocado Green Mattress has extended its Forest Stewardship Council (FSC)-certified wood and Global Organic Textile Standard (GOTS) cotton into pet beds, leveraging existing supply chains to enter the category with minimal incremental investment while commanding premium pricing. Engineered wood and plastic-and-polymer segments offer cost advantages and design flexibility, with injection-molded components enabling complex geometries and vibrant colors that appeal to younger consumers, yet these materials face scrutiny over microplastic shedding and end-of-life disposal.

Sustainable substrates are projected to rise at a 9.8% CAGR through 2031, as retailers mandate Forest Stewardship Council certification and consumers prioritize eco-labeled products. K9 Ballistics utilizes recycled polyethylene terephthalate bottles in its chew-resistant beds, while Approved by Fritz sources Global Recycle Standard-certified fabrics, indicating that recycled content is transitioning from a niche differentiator to a baseline. The European Union's Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) regulation restricts the use of flame retardants and volatile organic compounds in textiles and foams, requiring suppliers to source compliant materials and maintain traceability documentation.

By Distribution Channel:

E-Commerce Dominates as D2C Models Reshape MarginsE-commerce accounted for 37.0% of the pet furniture market share in 2025 and is projected to advance at an 11.5% CAGR through 2031, driven by direct-to-consumer logistics that bypass specialty retail markups and enable subscription models that lock in recurring revenue. China's e-commerce dominance is even more pronounced, with most pet products sold via Tmall, JD.com, and Douyin, creating a distribution scale that favors brands with digital-first go-to-market strategies and live-streaming capabilities.

Last-mile delivery innovations, including same-day fulfillment and buy-online-pick-up-in-store options, compress the time advantage that specialty pet stores once held, making it feasible for online-only brands to compete on convenience while maintaining higher gross margins by avoiding physical retail overhead. E-commerce channels also intensify price competition, as consumers can compare SKUs across dozens of retailers in seconds, and negative reviews on platforms such as Amazon can suppress conversion rates and organic search rankings.

Geography Analysis

North America Pet Furniture Market

North America holds a major share, accounting for 40% of the revenue in 2025, driven by high disposable incomes, widespread adoption of e-commerce, and pet-friendly workplace policies. Suburban migration among millennials is increasing demand for larger doghouses and sectional sofas, whereas urban areas tend to favor compact, modular furniture in the United States. Corporate campuses, such as Mars Petcare’s headquarters in Tennessee, now feature integrated dog parks and built-in furnishings, creating B2B sales opportunities for contract-grade items. In Canada, premium pet spending is rising alongside robust e-commerce logistics.

APAC Pet Furniture Market

The Asia-Pacific region is the fastest-growing geography, with an 8% CAGR projected through 2031. Growth is driven by urbanization, rising disposable incomes, and cultural shifts toward pet ownership in countries such as China, Japan, and India. According to the United States Department of Agriculture, in 2024, the total pet population in China was 124.1 million with 52.6 million dogs and 71.5 million cats. Approximately 90% of pet owners reside in urban areas, where apartment living drives demand for compact, odor-controlling furniture. India represents an emerging opportunity, with rising middle-class incomes and urbanization fueling pet adoption. However, limited local manufacturing capacity and import duties constrain supply, creating opportunities for regional players to establish production facilities. Australia and New Zealand contribute incremental growth, with high pet ownership rates and a cultural preference for outdoor activities driving demand for durable, weather-resistant furniture.

Europe Pet Furniture Market

Europe offers a significant opportunity, characterized by a focus on design and sustainability. Stringent sustainability standards and minimalist aesthetics drive growth. According to The People's Dispensary for Sick Animals, a 60% household pet ownership rate in 2024 helps sustain demand in the United Kingdom. Brexit-related supply chain disruptions and currency volatility have increased import costs, favoring domestic manufacturers and suppliers based in Europe. In France, growth in pet-friendly housing regulations in major cities is reducing barriers to pet ownership in rental units, thereby expanding the addressable market.

Regulatory Landscape

Pet furniture generally falls under broader consumer product and safety rules rather than category-specific pet regulations. As a result, compliance is shaped by chemical, materials, and human-injury safety requirements across major markets.

In the European Union, REACH affects allowable substances in textiles, foams, coatings, and adhesives used in pet beds, sofas, and scratchers, which raises documentation and traceability expectations for suppliers selling through mass retailers with ESG and safety audits. In the United States, oversight typically comes through broad product-safety expectations, with the US Consumer Product Safety Commission (CPSC) focused on products that can directly injure people and with no single federal, pet-furniture-specific standard providing uniformity across all states. Adjacent pet categories are also updating compliance playbooks through AAFCO model regulation updates (including the Pet Food Label Modernization project) and federal legislative activity such as the PURR Act of 2025 (H.R.597), which targets national uniformity in pet food regulation and can affect how retailers apply packaging, claims, and documentation practices across pet departments.

Competitive Landscape

The pet furniture market is moderately fragmented, with the five largest suppliers accounting for a significant share of global revenue. This leaves opportunities for specialist brands to expand their market presence. Inter IKEA Systems leads the market, driven by its LURVIG product line and extensive global store network. Chewy holds a notable share, supported by its Frisco private-label offerings and subscription-based customer retention model. Petmate (Doskocil Manufacturing Company, Inc.) captures significant market share due to its vertically integrated manufacturing capabilities. MidWest Metal Products specializes in pet housing, while Trixie Heimtierbedarf focuses on the premium segment in Europe.

Digital capabilities have become a critical competitive factor in the market. Mars Petcare is investing USD 1 billion over three years (starting in late 2024) to enhance its digital presence, including e-commerce and AI. Sustainability is also emerging as a key differentiator. IKEA's circular design program recycles over 80% of its furniture inputs, showcasing the alignment of scale with eco-efficiency. Additionally, digitally native brands are outpacing traditional retailers by leveraging direct-to-consumer models and social media engagement, a strategy that appeals strongly to Gen Z consumers who prioritize online discovery.

The integration of sustainability and technology is reshaping competitive differentiation in the pet furniture market. Start-ups like Tuft + Paw utilize augmented-reality applications to help customers visualize products, such as cat trees, in their homes, reducing return rates and minimizing landfill waste. Established brands are collaborating with material-science companies to incorporate ocean-bound plastics into product designs, addressing retailer ESG requirements. Competitive advantages are increasingly dependent on transparent sourcing, user-focused design, and data-driven after-sales services. While large incumbents can scale these innovations, agile start-ups are able to commercialize them more rapidly.

Pet Furniture Industry Leaders

IKEA (Inter IKEA Group)

Trixie Heimtierbedarf

Petmate (Doskocil Manufacturing Company, Inc.)

Chewy, Inc.

Midwest Metal Products Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Pet Furniture Market Companies Covered in this Report

- Go Pet Club Inc.

- Midwest Metal Products Company Inc.

- Chewy, Inc.

- Ware Manufacturing Inc.

- PetPals Group, Inc.

- Rolf C. Hagen Inc.

- AeroMark International Inc.

- Petmate (Doskocil Manufacturing Company, Inc.)

- Made4Pets SRL

- North American Pet Products (NAPP)

- Critter Couch Company

- Ultra Modern Pet

- Trixie Heimtierbedarf

- Sauder Woodworking Co.

- IKEA (Inter IKEA Group)

Market Opportunities and Future Outlook

E-commerce scale and subscription-led basket building create room for pet furniture assortments designed for ship-ability, including flat-pack, tool-less assembly, and compact packaging, as well as for replenishment attachment such as washable covers, replaceable scratch pads, and modular add-ons. The online channel already holds 37.0% share in 2025, and recurring programs can support higher-frequency order structures that bring pet furniture into broader carts. This is consistent with Chewy reporting 83% of sales driven by Autoship subscriptions and record net sales per active customer of USD 565 in Q2 FY2025, supporting product roadmaps centered on repeatable components, faster SKU refresh, and reduced return rates through digital visualization and configuration tools.

Sustainability and materials compliance also represent a practical opportunity, tied to retailer expectations for certified inputs and low-chemical designs, and consistent with the report context where wood held 29.0% share in 2025 and sustainable and recycled materials were the fastest-rising segment. Brands that can supply audited chains of custody, such as FSC-aligned wood sourcing, and compliant formulations for textiles and foams aligned with the EU REACH restrictions referenced in the report context may secure premium placements with mass retailers and home-furnishing channels. Multifunctional furniture growth in urban apartments further supports small-space and institutional use cases, including pet-friendly co-living and co-working procurement that prioritizes washable, fire-resistant, and higher-durability products over purely decorative designs.

Recent Industry Developments in Pet Furniture Market

- June 2026: IKEA Germany allowed dogs into all IKEA furniture stores and planning studios from June 15, 2026. The policy supports in-store trial and discovery for pet-adjacent home furnishings, reinforcing cross-selling for ranges such as UTSADD while normalizing pet-inclusive retail environments.

- December 2025: Petco introduced the launch of 800-plus new pet products for early 2026, including exclusive cat beds starting at USD 9.99 and themed scratchers. The expanded assortment points to faster SKU cycling and increased emphasis on design-led, value-priced pet furniture that can scale through big-box retail distribution.

- May 2024: IKEA introduced the UTSADD pet furniture collection in the United Kingdom as a 29-piece range developed with veterinarians and tested with shelter animals. Positioning pet furniture as a permanent, behavior-informed category within home furnishings increased competitive pressure on specialty brands to match mass-retail pricing and design integration.

Pet Furniture Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the pet furniture market covers purpose-built, factory-produced furniture made for companion animals, which is sold through offline retail and online channels. The sizing is captured in value terms at the manufacturer level (ex-factory), so it reflects product revenue before retail and distributor markups.

Scope exclusions: We exclude disposable pet accessories, pet apparel, and veterinary cages that are used only for clinical settings.

Segments Covered in This Report

- Product Type

- Beds and Sofas

- Houses

- Trees and Condos

- Scratchers and Climbers

- Multifunctional Furniture

- Other Products

- Pet Type

- Cats

- Dogs

- Others

- Material

- Wood

- Engineered Wood

- Metal

- Plastic and Polymer

- Sustainable / Recycled Materials

- Distribution Channel

- Specialty Pet Stores

- E-commerce

- Supermarkets and Hypermarkets

- Furniture Boutiques

- Veterinary Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build a practical fact base for demand signals, category boundaries, and trade movement of pet-related goods. Public sources such as US Census Bureau retail trade releases, US Bureau of Labor Statistics CPI series for household goods, UN Comtrade import and export statistics, and customs and tariff schedules from official portals help us anchor the direction of volumes and pricing.

We also reference sources such as government consumer expenditure surveys, trade association updates on pet ownership and spending, peer-reviewed articles on pet humanization, and company filings and investor decks for revenue mix hints and channel commentary. When needed, paid subscriptions are used only for company financials and intelligence, broader news and financials, patent databases, and shipment-level import and export records to support cross-checks. These examples are not exhaustive, and many other public and reference sources were also used to collect data, validate it, and clarify open questions.

Primary Interviews and Surveys

Primary work focuses on checking what is really being counted as pet furniture, and how pricing moves across materials and channels. We speak with manufacturers, distributors, retailers, and category specialists across APAC, EMEA, and the Americas to confirm adoption drivers, typical price bands, and what share is sold online versus in stores, and then those inputs are used to adjust assumptions that desk sources cannot fully explain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 46% |

| Mid tier: 55% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 16% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where pet ownership and household counts are translated into a furniture demand pool through spending and replacement behavior, which is then shaped by channel mix and typical price levels. To keep the totals realistic, the outputs are corroborated with selective bottom-up approximations such as supplier revenue roll-ups for sampled players, channel checks on unit movement, and price band mapping (ASP times estimated units) in major regions.

Key inputs include pet population and ownership growth, share of multi-pet households, online penetration for pet supplies, replacement and upgrade cycles for beds and cat trees, and material-driven price spreads (wood, engineered board, metal, and textile-heavy products). We also track seasonal purchase peaks tied to promotions and gifting, and how freight and raw material trends can shift ex-factory pricing. Forecasts are produced using scenario analysis with a base case that is stress-tested against expert views on discretionary spending and e-commerce growth, and gaps in regional data are handled by using proxy indicators such as retail category growth and import direction before being rechecked in follow-up calls.

Data Validation & Update Cycle

Validation is done by triangulating the modeled value against independent signals such as regional pet spending trends, online sales growth patterns, and trade movement for relevant product categories, and then checking that implied pricing stays within realistic ranges. When a region or channel shows a sharp jump, it is reviewed again, assumptions are revisited, and respondents are re-contacted if the variance cannot be explained by a known event.

Before sign-off, the model and narrative go through multi-step analyst reviews so calculation logic and scope rules are applied consistently across regions. Reports are refreshed annually, and interim updates are made when material events occur, such as major pricing shifts, regulation changes, or unusual demand spikes. Right before delivery, an analyst performs a fresh pass on the key inputs so clients receive the most current view available.

Mordor Intelligence's Pet Furniture Market Size Compared With Other Published Estimates

Published market sizes for pet furniture can differ even when the topic sounds similar, because the counted product set and the pricing point in the chain are not always the same. Differences also show up when one estimate leans on longer-range forecasts, or when currency timing and inflation treatment are not aligned.

The table shows a spread around the 2026 value, and in Mordor Intelligence's model the market is measured at ex-factory prices and excludes adjacent spend like disposable accessories and pet apparel, which can raise or lower totals depending on how other sources bundle categories and apply markups.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.27 B (2026) | |

| Global Consultancy A | USD 4.74 B (2026) | Uses a different pricing basis that can be closer to retail value and may capture a wider set of pet furniture-like items, which increases the total versus an ex-factory view. |

| Industry Publisher B | USD 4.69 B (2025) | Uses a different base year and a longer forecast window, and the definition is less explicit on whether markups and adjacent accessories are included, which can shift the reported market value. |

What this comparison mainly tells us is that the biggest gaps come from where value is measured in the chain, and what gets counted as furniture versus nearby accessories. By keeping the scope tied to manufacturer pricing and clear exclusions, the estimate stays traceable to practical demand and price inputs that can be repeated and checked.

Key Questions Answered in the Report

What is the projected value and growth rate of the pet furniture market?

The market is worth USD 4.27 billion in 2026 and is forecast to reach USD 5.71 billion by 2031, growing at a 5.98% CAGR.

Which product type is growing the fastest?

Multifunctional furniture that hides litter boxes or doubles as human side tables is projected to expand at an 8.9% CAGR through 2031.

Why is e-commerce so dominant in pet furniture purchases?

Online channels skip specialty-store markups, bundle furniture with consumables through subscriptions, and offer same-day delivery in major cities.

Which region shows the highest growth potential?

Asia-Pacific leads with a projected 8% CAGR through 2031, fueled by urbanization, rising incomes, and digital-first retail ecosystems.

Page last updated on: