Antifog Additives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

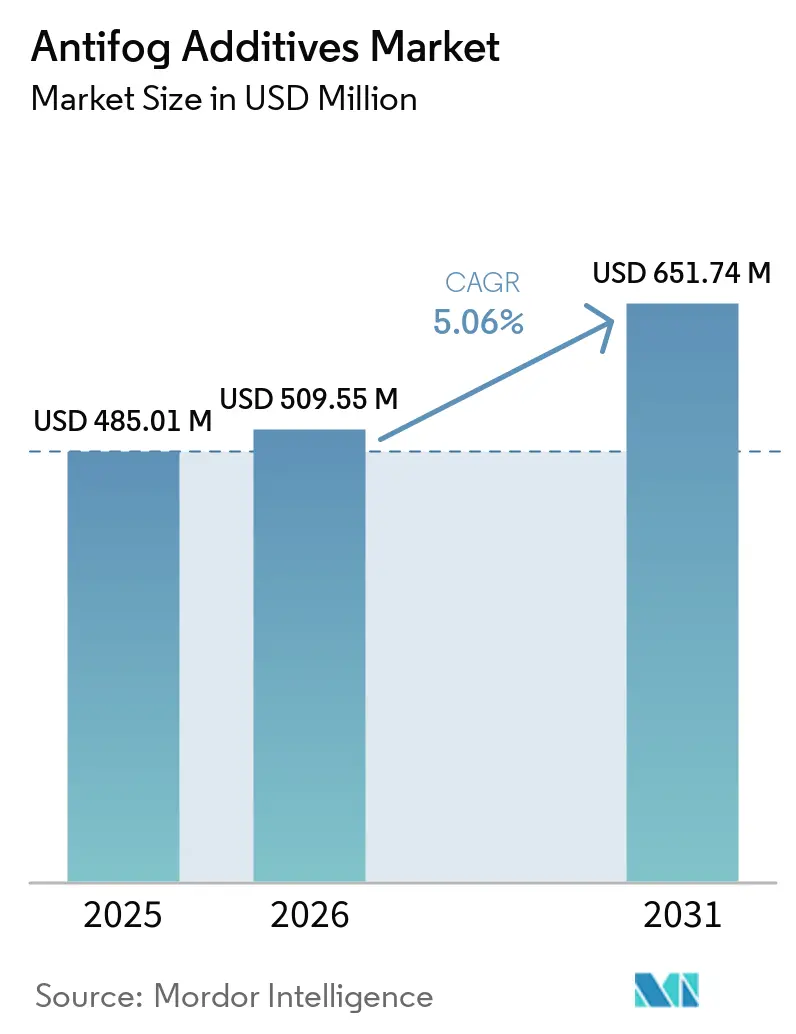

| Market Size (2026) | USD 509.55 Million |

| Market Size (2031) | USD 651.74 Million |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

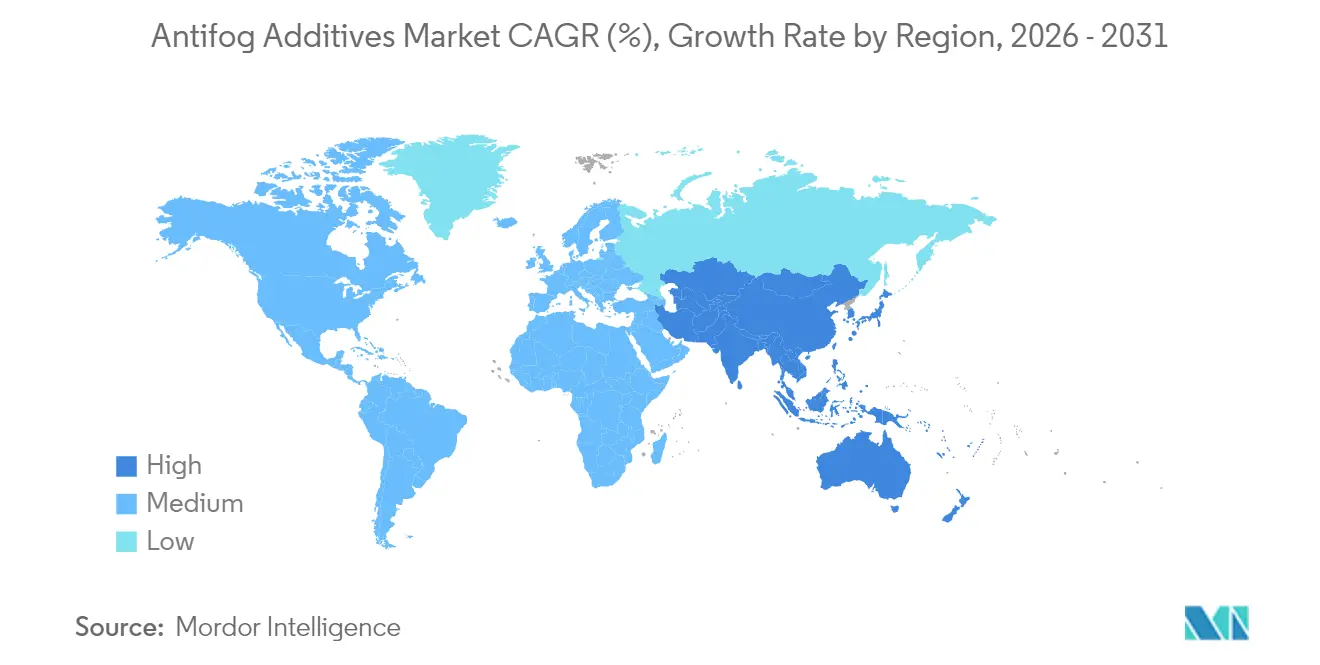

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antifog Additives Market Analysis by Mordor Intelligence

Antifog Additives Market size in 2026 is estimated at USD 509.55 million, growing from 2025 value of USD 485.01 million with 2031 projections showing USD 651.74 million, growing at 5.06% CAGR over 2026-2031. Regulatory convergence in food‐contact materials and agriculture is forcing suppliers to rethink formulations while maintaining performance. The European Union’s stricter migration limits and Japan’s new Positive List system accelerate reformulation work, yet they also create a premium for compliant, high-purity solutions. Simultaneously, controlled-environment agriculture and mono-material packaging trends ensure that high-clarity films remain a critical application arena. Competitive differentiation is migrating from scale toward technology, particularly around biobased feedstocks and controlled-migration delivery systems.

Key Report Takeaways

- By type, glycerol esters led with 37.58% of antifog additives market share in 2025; polyglycerol esters are projected to expand at a 5.65% CAGR to 2031.

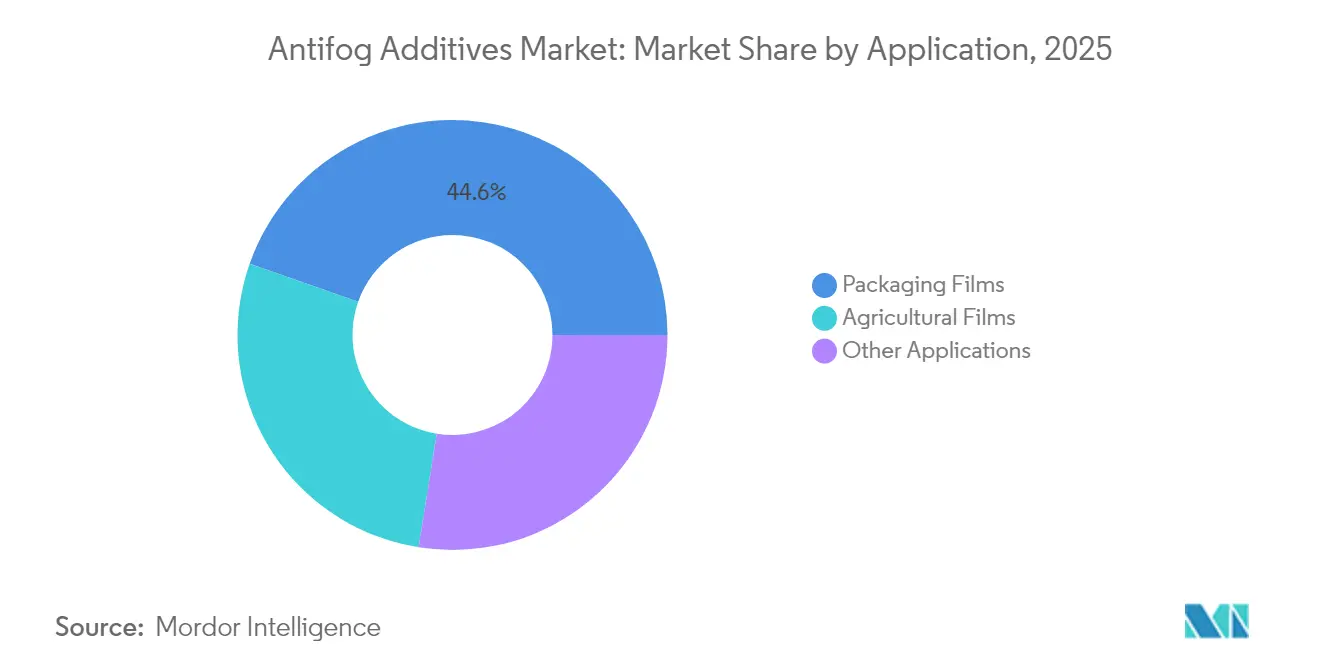

- By application, packaging films captured 44.62% of the antifog additives market size in 2025; agricultural films are advancing at a 5.88% CAGR through 2031.

- By geography, Asia-Pacific held 36.31% revenue share in 2025, and is forecast to grow at a 5.59% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antifog Additives Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to high-clarity greenhouse films in vertical farming | +1.2% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Surge in mono-material flexible food packaging demand | +0.9% | Europe and North America, expanding to APAC | Short term (≤ 2 years) |

| Mandatory cold-chain labeling regulations in North America | +0.6% | North America, with spillover to aligned markets | Short term (≤ 2 years) |

| Biobased ester innovation pipelines at key suppliers | +0.8% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Asia-Pacific agricultural subsidy programs for anti-fog films | +0.7% | APAC core, with technology transfer to emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to high-clarity greenhouse films in vertical farming

Vertical farming relies on optical precision, making condensation control a direct productivity lever. Chinese trials show that selecting advanced antifog films lifts solar radiation penetration by 5.33%, enhancing yields and farmer margins. Berry Global’s Tufflite Infrared film illustrates how anti-drip chemistry lengthens growing seasons and justifies premium pricing[1]. As luminescent quantum-dot films gain traction, any fog interference diminishes wavelength tuning, creating a self-reinforcing cycle of clarity requirements, higher prices, and performance‐driven demand in the antifog additives market for next-generation additives.

Surge in mono-material flexible food packaging demand

The EU Packaging & Packaging Waste Regulation propels a pivot toward recyclable mono-material structures, removing traditional barrier layers that previously contained additive migration. Huhtamaki guidance under the India Plastics Pact places mono-material solutions at 73% of national plastic use, widening the addressable base for compliant antifog solutions in the antifog additives market. DNP Group’s polyethylene-only pouches maintain oxygen and water-vapor resistance, yet require antifog chemistries that neither hinder sorting nor raise migration risk. Younger consumers’ scrutiny of environmental claims forces brands to pick suppliers with demonstrable sustainability credentials.

Mandatory cold-chain labeling regulations in North America

The FDA FSMA 204 Final Rule imposes enhanced traceability, demanding label legibility from loading dock to retail case. GS1-71 standard barcodes must remain scannable when surfaces condense, pushing converters to favour high-clarity, fast-acting antifog additive packages within the antifog additives market. The Global Cold Chain Alliance highlights visibility for quick temperature checks as a best practice. EPA 40 CFR 84.58 mandates durable labels on refrigerants, broadening the compliance footprint. Hence, antifog formulations transition from optional performance boosters to regulatory enablers.

Biobased ester innovation pipelines at key suppliers

Biodiesel expansion boosts glycerine supply, lowering feedstock costs for biobased antifog esters. The International Energy Agency anticipates 28% growth in biofuel demand through 2026, giving ester manufacturers a steady glycerine pool[2]. Solvay’s glycerine-based ECH process now covers 50% of China’s demand, demonstrating commercial scale. Dow-Evonik’s hydrogen-peroxide-to-propylene-glycol pilot showcases alternative green routes that may disrupt conventional glycerol ester chains. R&D intensity rises as firms strive for parity with petroleum-derived alternatives while staying cost competitive in the antifog additives market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening REACH limits on ester migration in food contact films | -1.1% | Europe, with regulatory harmonization effects globally | Short term (≤ 2 years) |

| Short service-life complaints in hot-humid equatorial zones | -0.8% | Southeast Asia, tropical regions, with performance implications | Medium term (2-4 years) |

| Volatile mono- and poly-glycerol feedstock pricing | -0.6% | Global, with particular impact on cost-sensitive applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening REACH limits on ester migration in food-contact films

Regulation (EU) 2025/351 introduces new purity standards and NIAS risk-assessment thresholds. Any migration above 0.00015 mg/kg food now demands extensive toxicological data, pushing up testing costs and elongating development timelines. EFSA modeling shows polyglycerol packages could migrate up to 50 mg/kg food under worst-case conditions, limiting design windows. Suppliers unwilling to fund reformulation face potential market exit by the September 2026 compliance deadline, reshaping competition in the antifog additives market.

Short service-life complaints in hot-humid equatorial zones

Elevated temperature and humidity accelerate additive migration, cutting film life in Southeast Asian greenhouses. Studies on polyolefin films indicate diffusion spikes once ambient temperatures surpass polymer glass-transition levels. Acidic-sauce permeation experiments confirm that higher heat loads hasten polymer degradation and compromise antifog layers. Customer trust erodes when greenhouse covers lose clarity mid-season, forcing premium additives or thicker films that raise costs in the antifog additives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dominance of Glycerol Esters and Growth of Polyglycerol Esters

Glycerol esters held 37.58% of antifog additives market share in 2025 owing to decades-long acceptance by regulators and processors. The FDA 21 CFR 172.854 and WHO ADI of 0-25 mg/kg body weight underpin confidence in food packaging use. However, polyglycerol esters are outpacing at 5.65% CAGR thanks to superior thermal stability and lower volatility, properties validated in lab extrusion studies.

Sorbitan esters service niche polymer systems where specific migration properties are needed. An emerging cluster of biobased specialty blends targets controlled-release delivery that sustains antifog performance under temperature swings. Avient’s Cesa platform integrates these chemistries, demonstrating how smart carrier matrices can extend film clarity in multi-cycle use.

By Application: Agriculture Applications Accelerate While Packaging Remains the Base

Packaging films occupied 44.62% of the antifog additives market size in 2025, reflecting universal demand for clear, condensation-free food wraps. Supply chain traceability and brand visibility mean that fog-free windows have turned from nice-to-have to required. Agricultural films, however, clock the highest 5.88% CAGR as urban food demand, climate volatility, and subsidy structures expand protected cultivation acreage. Each incremental square meter of greenhouse plastic requires reliable anti-drip performance over at least one planting cycle; poor clarity translates into lower yields, lost subsidies, and reputational risk for suppliers.

Other emerging uses include smart labels, industrial anti-mist coatings, and electronics packaging where optical sensor readouts need fog-free surfaces. Cargill’s Atmer catalog shows granular tailoring: Atmer 1440 NV optimizes water droplet spread in retail wraps, while Atmer 103 targets multi-season greenhouse applications.

Geography Analysis

Asia-Pacific leads the antifog additives market with 36.31% share in 2025, underpinned by state-driven agricultural modernization. Chinese subsidy programs increase cropland scale, encouraging investments in high-clarity greenhouse films that feature controlled antifog agents. India’s protected cultivation is jumping to 250 million tons output by 2025, sustaining long-term additive demand. Japan’s Positive List system, active since June 2025, requires local and imported films to pass stringent migration tests before market entry, thereby lifting technical barriers and unit pricing.

North America relies on cold-chain compliance to maintain food safety. FSMA 204 requires legible labeling during the entire distribution channel, making antifog visibility a compliance cost rather than an optional upgrade. The Global Cold Chain Alliance lists clear pack windows as a KPI for logistics quality audits.

Europe is in regulatory flux. REACH alignment under Regulation (EU) 2025/351 calls for extensive NIAS assessments and purity upgrades. While that creates near-term cost burdens, it also rewards early movers capable of documenting migration behavior at sub-ppm levels—often the global multinationals already invested in analytic capacity. South America and Middle East & Africa provide greenfield growth opportunities. Government greenhouse programs in Peru and Morocco pilot anti-drip films, but fragmented regulations and price sensitivity keep adoption gradual.

Competitive Landscape

The antifog additives market is moderately fragmented. Avient markets the Cesa Anti-Fog suite that bundles performance with sustainability narratives, targeting both food packaging and horticulture. Dow and Evonik jointly pilot hydrogen-peroxide-to-propylene-glycol technology to unlock renewable ester intermediates, signaling strategic integration between base chemicals and performance additives. Evonik’s AgraLine solutions highlight biobased chemistry aimed at greenhouse films, positioning the company against glycerol-dominant incumbents.

Other notable players include Clariant, Croda, A. Schulman, and Palsgaard, all investing in low-migration grades to meet EU and Japanese approvals. Start-ups focusing on nanostructured coatings offer disruptive visibility, yet regulatory hurdles and qualification cycles remain high. Overall, bargaining power is shifting to converters and brand owners who demand life-cycle data, putting pressure on suppliers to build analytical and regulatory consulting capabilities in-house.

Antifog Additives Industry Leaders

LyondellBasell Industries Holdings B.V.

Avient Corporation

Corbion

Croda International PLC

Palsgaard

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tosaf introduced its FogFree portfolio, providing integrated antifog masterbatch solutions specifically designed for challenging polymers. These antifog compounds modify surface tension and facilitate the formation of a uniform water layer, effectively preventing droplet formation.

- December 2023: Kraton Corporation launched Nexar Anti-Fog films. This solution addresses persistent fogging issues encountered by healthcare professionals using personal protective equipment (PPE), such as face shields and eye protection.

Global Antifog Additives Market Report Scope

The chemicals that prevent water condensation in small droplets on surfaces are known as antifog additives. The antifog additives market is segmented by type, application, and geography. By type, the market is segmented into glycerol esters, polyglycerol esters, sorbitan esters of fatty acids, and other types. By application, the market is segmented into agricultural films, packaging films, and other applications. The report also covers the market sizes and forecasts for the antifog additives market in 15 countries across major regions. The market sizing and forecasts have been done for each segment based on revenue (in USD million).

| Glycerol Esters |

| Polyglycerol Esters |

| Sorbitan Esters of Fatty Acids |

| Other Types |

| Agricultural Films |

| Packaging Films |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Glycerol Esters | |

| Polyglycerol Esters | ||

| Sorbitan Esters of Fatty Acids | ||

| Other Types | ||

| By Application | Agricultural Films | |

| Packaging Films | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Antifog Additives Market size?

The antifog additives market size stands at USD 509.55 million in 2026.

Which region leads demand for antifog additives?

Asia-Pacific holds 36.31% share due to rapid greenhouse expansion and supportive subsidies.

Why are polyglycerol esters gaining traction?

They offer superior thermal stability and lower volatility, driving a 5.65% CAGR through 2031.

How do new EU rules affect antifog additives suppliers?

Regulation (EU) 2025/351 imposes lower migration limits, pushing firms to reformulate high-purity, low-migration grades.

Page last updated on: