Personalized Medicine Bioinformatics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

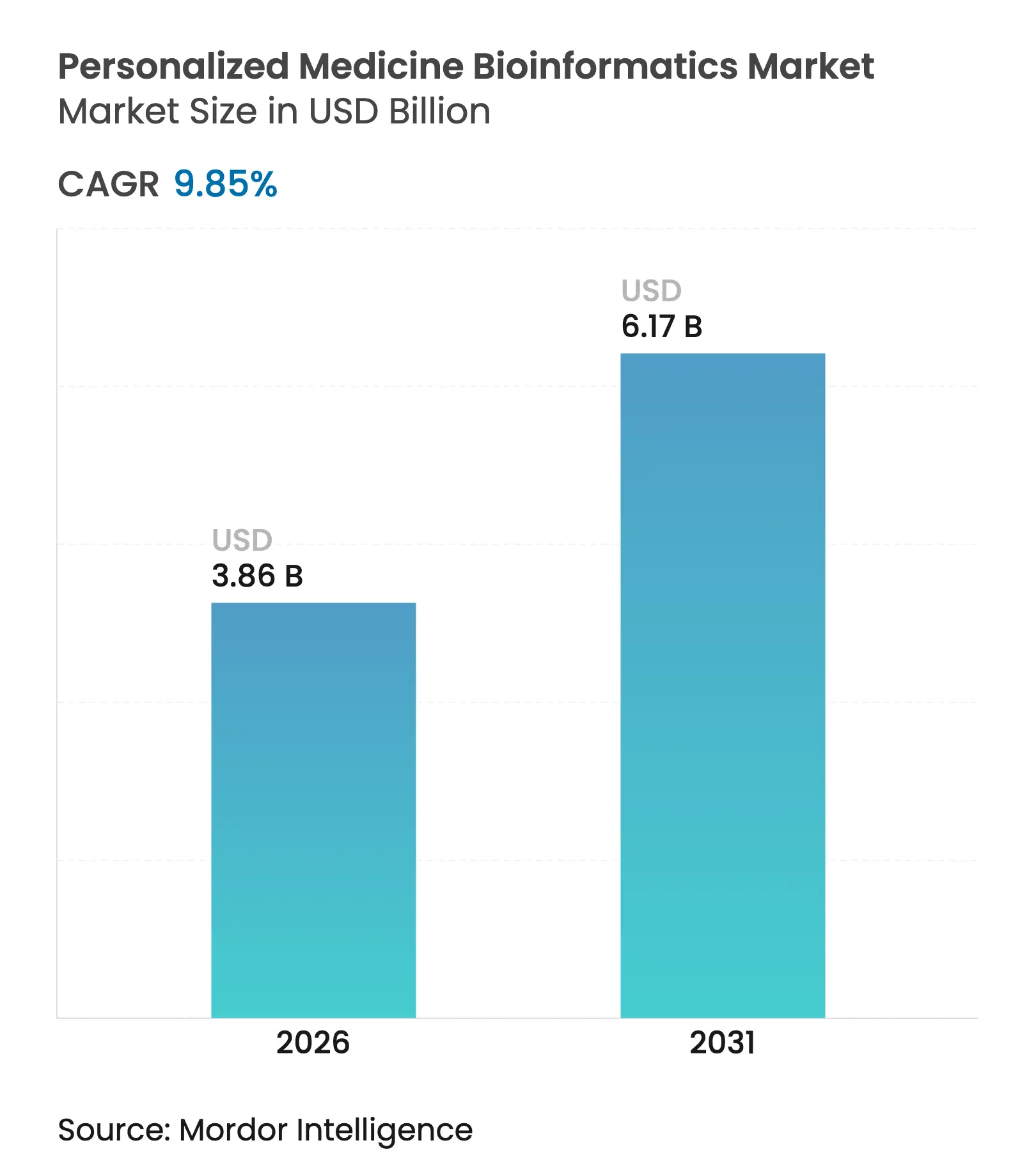

| Market Size (2026) | USD 3.86 Billion |

| Market Size (2031) | USD 6.17 Billion |

| Growth Rate (2026 - 2031) | 9.85 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Personalized Medicine Bioinformatics Market Analysis by Mordor Intelligence

The personalized medicine bioinformatics market size in 2026 is estimated at USD 3.86 billion, growing from 2025 value of USD 3.51 billion with 2031 projections showing USD 6.17 billion, growing at 9.85% CAGR over 2026-2031. This momentum is propelled by the steady fall in whole-genome sequencing costs, the maturation of cloud-native architectures, and rapid advances in AI-driven analytics models. North America leads current revenue owing to sustained grant funding, robust electronic health record (EHR) penetration, and early clinical adoption of genomic testing. Meanwhile, favorable reimbursement decisions, liquid-biopsy approvals, and large-scale multi-omics initiatives are broadening the technology’s clinical footprint. In parallel, Asia Pacific is accelerating as the region leverages universal healthcare systems, ambitious national precision-medicine programs, and a fast-growing pool of AI talent. Industry participants are strengthening platform propositions by adding spatial-omics workflows, federated-learning capabilities, and turnkey regulatory compliance modules to address rising data-sovereignty requirements. Heightened demand from life-science researchers, contract research organizations (CROs), and hospital laboratories underscores a global shift toward outsourced, pay-per-use bioinformatics services that can scale with data volumes.

Key Report Takeaways

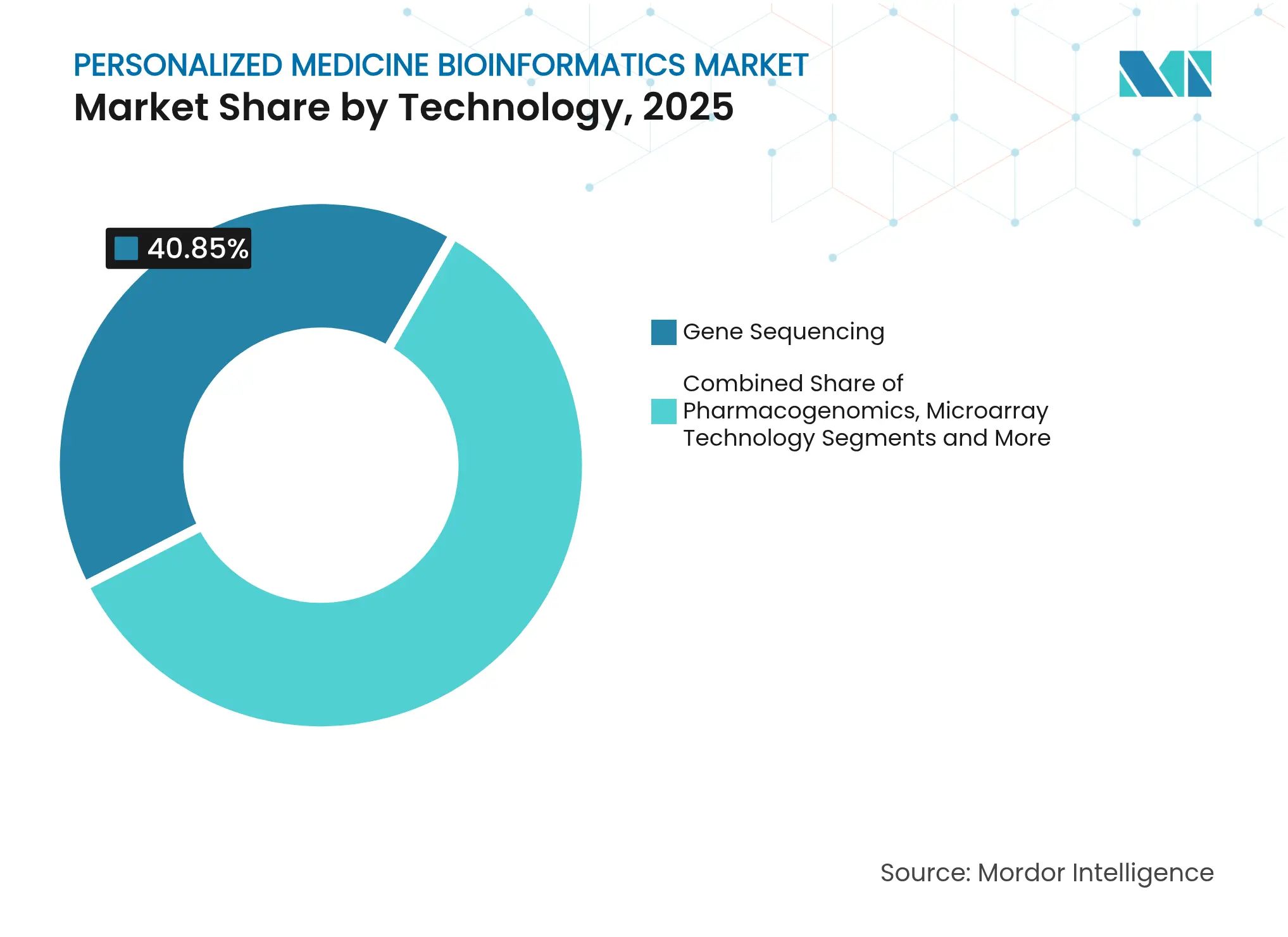

- By technology, Gene Sequencing held 40.85% of the personalized medicine bioinformatics market share in 2025; AI-driven Analytics Platforms are forecast to grow at 17.95% CAGR.

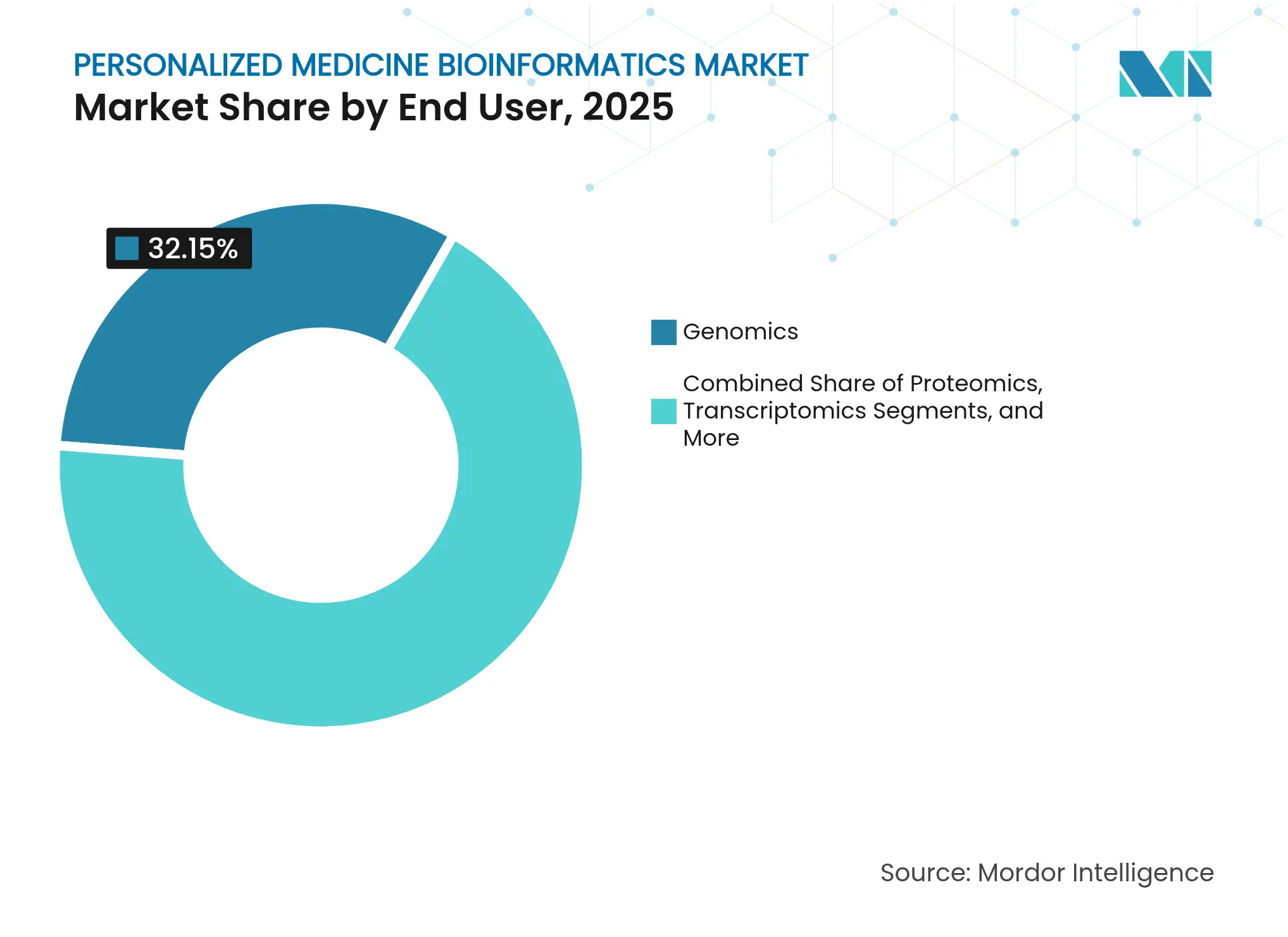

- By application, Genomics captured 32.15% of the personalized medicine bioinformatics market size in 2025, while Spatial-Omics is predicted to expand at a 19.05% CAGR to 2031.

- By end user, Biotechnology and pharmaceutical Companies represented 47.55% of revenue in 2025; CROs and biobanks are set to climb at a 15.35% CAGR over the forecast horizon.

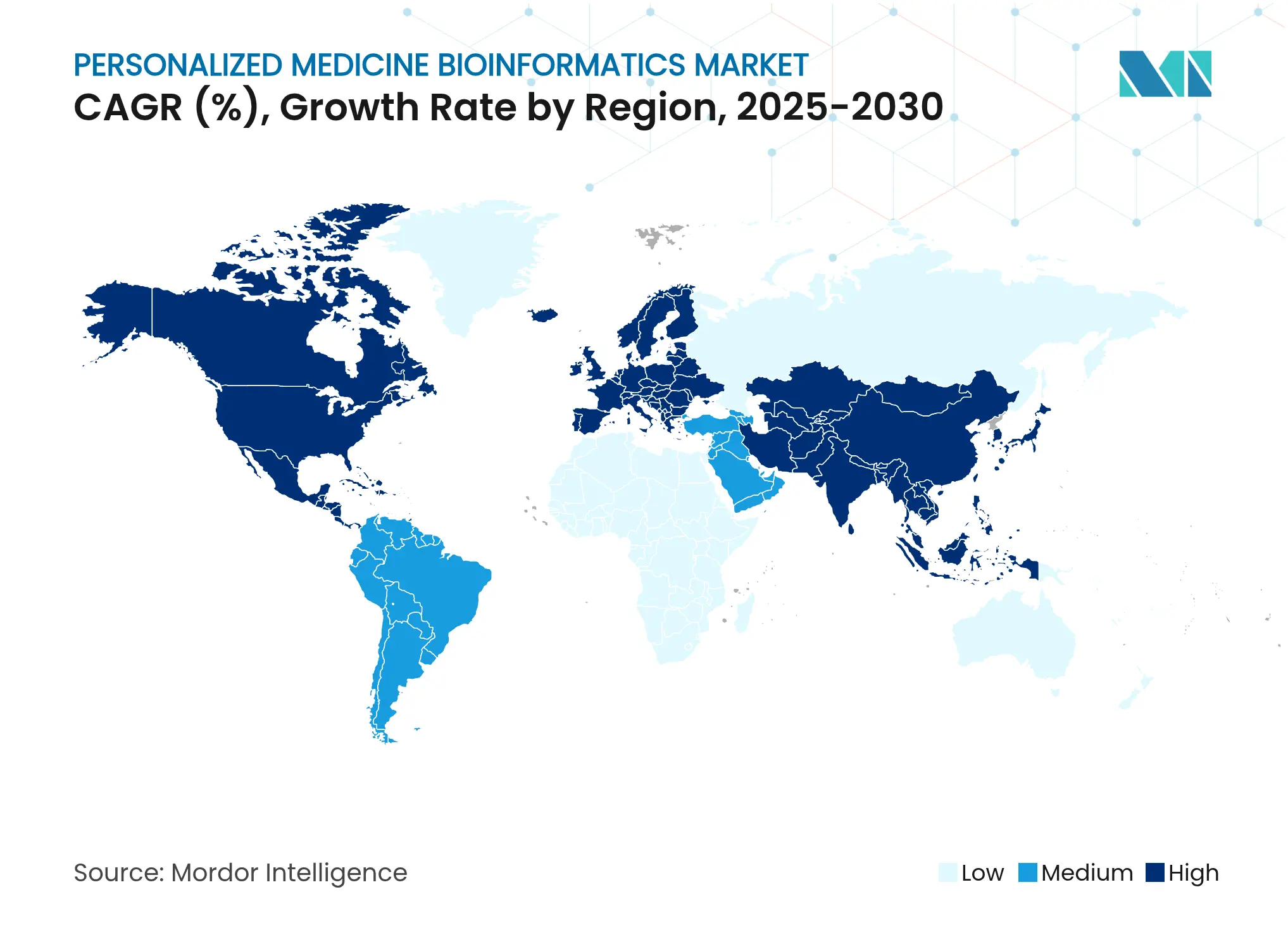

- By geography, North America accounted for 46.05% revenue in 2025, whereas Asia Pacific is projected to advance at a 14.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personalized Medicine Bioinformatics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerating Adoption Of Precision & Genomic-Guided Care Accelerating Adoption Of Precision & Genomic-Guided Care | +2.10% | Global, with North America & EU leading clinical implementation | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.10% | Geographic Relevance:Global, with North America & EU leading clinical implementation | Impact Timeline:Medium term (2-4 years) |

Rapid Fall In Sequencing Costs & Data Generation Economics Rapid Fall In Sequencing Costs & Data Generation Economics | +1.80% | Global, with strongest impact in emerging markets | Short term (≤ 2 years) | |||

Expansion Of Cloud-Native Bioinformatics Platforms Expansion Of Cloud-Native Bioinformatics Platforms | +1.50% | Global, with APAC showing highest adoption rates | Medium term (2-4 years) | |||

Government Mega-Projects Funding Multi-Omics Databases Government Mega-Projects Funding Multi-Omics Databases | +1.30% | North America, China, UK primarily | Long term (≥ 4 years) | |||

Spatial-Omics & Single-Cell Analytics Unlocking New Insights Spatial-Omics & Single-Cell Analytics Unlocking New Insights | +1.10% | Global, concentrated in research institutions | Medium term (2-4 years) | |||

Federated Learning Enabling Secure Distributed Model Training Federated Learning Enabling Secure Distributed Model Training | +0.90% | EU, North America due to data sovereignty requirements | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerating Adoption of Precision & Genomic-Guided Care

FDA approvals for next-generation companion diagnostics in oncology and rare diseases have pushed genomic testing beyond research facilities into routine clinical decision-making. Approvals for FoundationOne Liquid CDx, including indications for BRCA-positive metastatic prostate cancer and MET exon 14-skipping lung cancer, exemplify this trend. Liquid-biopsy workflows address tissue-availability constraints while supporting longitudinal monitoring. Concurrently, personalized RNA cancer vaccines combined with immune checkpoint inhibitors reduced melanoma recurrence by 44% in 2024 trials.[1]Natalie L. Vokes, “RNA Vaccine Therapy Reduces Melanoma Recurrence,” mdpi.com Providers now view genomic results as influencing nearly 70% of medical decisions, making tight EHR integration non-negotiable.

Rapid Fall in Sequencing Costs & Data-Generation Economics

The whole-genome price tag dropped from USD 100 million in 2001 to roughly USD 500–600 in 2024 and could plunge to USD 200 by 2030. Nature projects a future floor of USD 10 per genome, accelerating population-scale initiatives across the United Kingdom, Australia, and the United States.[2]N. Jumper, “Nucleotide Transformer Models Genomics Data,” nature.com Yet analytical costs now dominate spending: as data output soars, compute, storage, and compliance expenses risk outpacing sequencing savings, as per Genetic Engineering & Biotechnology. Firms such as 3billion already market USD 200 genome services to expand access in low-income regions.

Expansion of Cloud-Native Bioinformatics Platforms

Providers are shifting petabyte-scale workloads into elastic clouds that support containerized pipelines, serverless execution, and streamlined accreditation. DNAnexus now manages more than 80 PB of genomic data and recently embedded Intelliseq’s automated variant-interpretation engine within its Precision Health Data Cloud. Canadian researchers adopted the CanDIG federation to analyze sensitive datasets across provinces under national privacy rules. Hyperscale vendors Google Cloud and AWS supply dedicated genomics APIs, while Kubernetes-based workflow engines orchestrate parallel compute tasks for multi-omics studies.

Government Mega-Projects Funding Multi-Omics Databases

The NIH Multi-Omics for Health and Disease Consortium harmonizes genomic, transcriptomic, proteomic, and environmental data into unified resources. China’s 15-year precision-medicine plan commits USD 9.2 billion to sequencing 1 million genomes and curating longitudinal phenotypic records. The NIH AnVIL platform operationalizes FAIR data principles, hosting large shared cohorts and enabling cloud-native analysis without downloading files.[3]Eric Green, “AnVIL: Cloud-Native Genomic Data Sharing,” genome.gov

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High CAPEX & OPEX For Bioinformatics Infrastructure High CAPEX & OPEX For Bioinformatics Infrastructure | -1.40% | Global, with higher impact in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.40% | Geographic Relevance:Global, with higher impact in emerging markets | Impact Timeline:Short term (≤ 2 years) |

Shortage Of Skilled Bioinformaticians / Data Scientists Shortage Of Skilled Bioinformaticians / Data Scientists | -0.80% | Global, particularly acute in APAC and emerging markets | Medium term (2-4 years) | |||

EHR–Omics Interoperability Gaps Delaying Clinical Uptake EHR–Omics Interoperability Gaps Delaying Clinical Uptake | -0.60% | North America & EU primarily, due to complex healthcare systems | Medium term (2-4 years) | |||

Data-Sovereignty Laws Limiting Cross-Border Genomics Flows Data-Sovereignty Laws Limiting Cross-Border Genomics Flows | -0.40% | EU, China, with spillover effects globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High CAPEX & OPEX for Bioinformatics Infrastructure

Genomic-data volumes roughly double every 18 months, stressing compute budgets even as sequencing becomes cheaper. Healthcare leaders struggle to capture downstream clinical ROI when justifying large software and hardware outlays, an issue highlighted in the health-IT finance literature. FDA’s 2024 Laboratory-Developed Test rule adds an estimated USD 566 million to USD 3.56 billion industry-wide in compliance outlays, with smaller laboratories facing disproportionate burdens.

Shortage of Skilled Bioinformaticians / Data Scientists

Demand for multidisciplinary talent spanning statistics, computer science, and molecular biology continues to exceed supply. The NIH allocated USD 900,000 for computational genomics education to close diversity gaps in 2025 grants. Pan-African initiatives such as H3ABioNet have trained more than 4,500 professionals, yet large consortia still cite workforce shortfalls as a major execution risk. Academic reports emphasize the need for cross-disciplinary communication skills and project management abilities in big-data medicine.

Segment Analysis

By Technology: AI Platforms Drive Next-Generation Analytics

Gene Sequencing commanded 40.85% revenue in 2025, a position reinforced by continuing demand for flexible short-read and emerging long-read chemistries. However, AI-driven Analytics Platforms are forecast to post a 17.95% CAGR, reflecting surging interest in transformer-based language models trained on genomic tokens and cross-species alignments. QIAGEN’s PGXI knowledgebase automates pharmacogenomic annotations by merging FDA and CPIC references, underscoring the move toward end-to-end clinical interpretation workflows. Integrated stacks that merge variant calling, multi-omic harmonization, and explainable AI are redefining the personalized medicine bioinformatics market. Quantum-inspired optimization prototypes are also under evaluation for accelerating search space exploration in drug repurposing scenarios.

Full-service platforms increasingly couple data-management consoles with modular analytics engines. The personalized medicine bioinformatics market size for AI-enhanced analytics is projected to outpace legacy microarray solutions as institutions transition population-screening programs to sequencing-plus-AI workflows. Meanwhile, microarrays retain a foothold in lower-cost genotyping panels for epidemiological studies where sample throughput outweighs per-sample depth. Vendors differentiate through embedded algorithm libraries, low-code workflow designers, and compliance toolkits that shorten time-to-result for regulated assays.

Note: Segment shares of all individual segments available upon report purchase

By Application: Spatial-Omics Revolutionizes Tissue Analysis

Genomics retained 32.15% revenue in 2025 as oncology, rare-disease diagnostics, and pharmacogenomics remain foundational use cases. Spatial-Omics, however, is predicted to register a 19.05% CAGR by 2031, lifting its contribution to the personalized medicine bioinformatics market size as high-resolution tissue mapping reaches mainstream laboratories. Proteomics has accelerated following the confirmation of 93% of predicted human proteins, enabling richer biomarker discovery pipelines. Transcriptomics benefits from multi-modal protocols such as Spatial-Mux-seq that co-profile RNA, protein, and chromatin states within a single experiment.

Researchers now integrate metabolomics and epigenomics to pinpoint pathway-level perturbations that underlie disease phenotypes. Multi-omics assembly methods like MINDSETS yield 89.25% accuracy in distinguishing Alzheimer’s disease from vascular dementia, illustrating clinical utility. The personalized medicine bioinformatics market continues to reward vendors that harmonize data matrices across omic layers, automate phenotype linkage, and deliver interpretable outputs that clinicians can act on at the point of care. As workflows mature, spatial-omics is expected to permeate translational research centers first, then diffuse into clinical pathology labs pending regulatory guidance on data standards and quality metrics.

By End User: CROs Accelerate Outsourced Analytics

Biotechnology and pharmaceutical Companies contributed 47.55% of 2025 spending as drug discovery pipelines increasingly embed multi-omic biomarkers and adaptive trial designs. CROs and biobanks are forecast to rise at a 15.35% CAGR through 2031, illustrating a pivotal outsourcing shift in the personalized medicine bioinformatics market. Outsourced providers offer turn-key variant-calling, data curation, and federated-analysis services that help smaller biotech entrants avoid heavy capital outlays. Foundation Medicine’s collaborations with Syndax Pharmaceuticals and PMV Pharma for AML and p53-targeted companion diagnostics underline the strategic advantage of specialized service platforms.

Clinical Diagnostics Laboratories continues scaling NGS oncology panels, yet many rely on cloud partners for the heavy lifting of bioinformatics as data-center costs climb. Academic medical centers, meanwhile, form consortia with platform vendors for access to cutting-edge analytics and for beta-testing emerging pipelines, evidenced by QIAGEN’s three-year microbiome collaboration with McGill University. The personalized medicine bioinformatics market share held by CROs is likely to expand further as labor shortages and compliance complexities push hospitals toward managed bioinformatics subscriptions.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America contributed 46.05% revenue in 2025 due to sustained National Institutes of Health funding, clear reimbursement pathways, and widespread EHR penetration that simplifies integration with clinical workflows. The NIH Computational Genomics program alone consumed roughly 30% of the institute’s FY 2023 research budget, keeping domestic infrastructure at the forefront. Public–private partnerships between sequencing vendors and healthcare networks have extended testing capacity into community oncology and cardiology clinics, further anchoring demand in the region.

Europe follows with a sizeable share, supported by initiatives such as the EUCAN ELSI Collaboratory that tackles GDPR compliance in cross-border data sharing. National health-service funding in the United Kingdom and Nordic countries finances large-scale population sequencing, while federated-learning pilots in Germany and France highlight regulatory-aligned approaches to distributed analytics. The personalized medicine bioinformatics market benefits from the region’s emphasis on interoperability standards, fostering vendor competition around CE-IVD-ready pipelines.

Asia Pacific is projected to grow at a 14.55% CAGR through 2031, the fastest globally. China’s 15-year precision-medicine initiative earmarks USD 9.2 billion for genomics infrastructure and positions domestic firms such as BGI as sequencing powerhouses. Nationwide EHR networks in Japan, South Korea, and Australia expedite clinical data linkage, while Singapore’s federated sandbox programs test secure analytics on de-identified cohorts. The region’s universities graduate a growing cadre of AI specialists, enabling local customization of language models for population-specific polymorphisms.

The Middle East represents an emerging opportunity as governments diversify their economies around knowledge-based sectors. Saudi Arabia’s Vision 2030 invests heavily in biotechnology through entities such as the Hevolution Foundation, focusing on health-span research that relies on multi-omics datasets. Latin America and Africa maintain smaller footprints, but consortia such as H3ABioNet illustrate rising regional capacity for multi-site genomics projects. Multilateral funding and technology-transfer agreements are expected to build foundational infrastructure, unlocking latent demand over the next decade.

Competitive Landscape

Market Concentration

The personalized medicine bioinformatics market remains moderately fragmented. Incumbent sequencing giants Illumina, Thermo Fisher Scientific, and QIAGEN vie with AI-native players such as Tempus Labs and DNAnexus for platform dominance. Strategic partnerships outpace outright acquisitions as firms pursue complementary capabilities: Illumina and NVIDIA jointly optimize DRAGEN variant-calling pipelines on GPU clusters to hasten multi-omic data processing. Tempus inked a USD 200 million data-licensing pact with AstraZeneca to train multi-modal foundation models, demonstrating pharmaceutical appetite for curated, clinically annotated datasets.

Product differentiation centers on algorithmic performance, federated-analysis features, and compliance toolkits. QIAGEN’s AI-derived knowledge graph now spans over 640 million biomedical relationships, enhancing automated pathway interpretation in Ingenuity Pathway Analysis. Seqera’s acquisition of Tinybio aims to democratize AI-powered analytics for mid-tier laboratories by embedding natural-language queries into workflow orchestration tools. bioMérieux added Applied Maths to boost microbiology analytics, signaling interest from clinical-diagnostic incumbents in omics-driven decision support.

White-space opportunities remain in spatial-omics, single-cell analytics, and quantum-enhanced algorithms. Start-ups leverage transformer architectures and self-supervised learning on unlabeled genomic data to rapidly annotate variants of uncertain significance. Larger vendors focus on end-to-end suites that integrate cloud storage, secure compute, and real-time result visualization, simplifying adoption for hospitals with limited in-house expertise. Success increasingly requires demonstrable clinical ROI as hospital systems demand evidence of improved patient outcomes and operational efficiencies before committing to multi-year bioinformatics contracts.

Personalized Medicine Bioinformatics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Illumina unveiled a first-of-its-kind spatial transcriptomics technology enabling unbiased whole-transcriptome profiling with cellular resolution. The technology is slated for commercial launch in 2026 and includes a collaboration with the Broad Institute for large-scale spatial datasets.

- February 2025: Foundation Medicine introduced hereditary germline tests, FoundationOne Germline and FoundationOne Germline More, through a partnership with Fulgent Genetics. These tests cover 50 and 154 genes, respectively, for hereditary cancer risk assessment.

- January 2025: Illumina and NVIDIA formalized a collaboration to accelerate precision health by optimizing DRAGEN pipelines on NVIDIA GPUs and co-developing multi-omics analysis workflows.

- January 2025: DNAnexus partnered with Intelliseq to embed automated variant interpretation and clinical reporting in the Precision Health Data Cloud, enhancing somatic-cancer and hereditary-disease applications.

Table of Contents for Personalized Medicine Bioinformatics Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Accelerating Adoption Of Precision & Genomic-Guided Care

- 4.2.2Rapid Fall In Sequencing Costs & Data Generation Economics

- 4.2.3Expansion Of Cloud-Native Bioinformatics Platforms

- 4.2.4Government Mega-Projects Funding Multi-Omics Databases

- 4.2.5Spatial-Omics & Single-Cell Analytics Unlocking New Insights

- 4.2.6Federated Learning Enabling Secure Distributed Model Training

- 4.3Market Restraints

- 4.3.1High CAPEX & OPEX For Bioinformatics Infrastructure

- 4.3.2Shortage Of Skilled Bioinformaticians / Data Scientists

- 4.3.3EHR–Omics Interoperability Gaps Delaying Clinical Uptake

- 4.3.4Data-Sovereignty Laws Limiting Cross-Border Genomics Flows

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Technology

- 5.1.1Gene Sequencing

- 5.1.2Pharmacogenomics

- 5.1.3Microarray Technology

- 5.1.4AI-driven Analytics Platforms

- 5.1.5Other Technologies

- 5.2By Application

- 5.2.1Genomics

- 5.2.2Proteomics

- 5.2.3Transcriptomics

- 5.2.4Metabolomics

- 5.2.5Epigenomics

- 5.2.6Other Applications

- 5.3By End User

- 5.3.1Biotechnology & Pharmaceutical Companies

- 5.3.2Clinical Diagnostics Laboratories

- 5.3.3Hospitals & Academic Medical Centers

- 5.3.4CROs & Biobanks

- 5.3.5Other End Users

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Services, and Recent Developments)

- 6.3.1DNAnexus

- 6.3.2Illumina

- 6.3.3Thermo Fisher Scientific

- 6.3.4Flatiron Health

- 6.3.5Syapse

- 6.3.6Sophia Genetics

- 6.3.7Tempus Labs

- 6.3.8Foundation Medicine

- 6.3.9Qiagen

- 6.3.10IBM Watson Health

- 6.3.11Aster Insights

- 6.3.12Concert Genetics

- 6.3.13C4X Discovery

- 6.3.14Nucleai

- 6.3.15Protica Bio

- 6.3.16Verily Life Sciences

- 6.3.17Genomate Health

- 6.3.18Assurance Health Data

- 6.3.19Amazon Web Services (AWS) Genomics

- 6.3.20Google Cloud Life Sciences

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the personalized medicine bioinformatics market as revenue earned from software, analytic services, and cloud infrastructure that turn patient-level genomic, transcriptomic, proteomic, and allied data into usable insights for precision diagnosis, therapy choice, or companion-diagnostic development across care providers and biopharma firms.

Scope exclusion: Generic bioinformatics tools deployed only in agriculture, veterinary, or classroom settings fall outside this report.

Segmentation Overview

- By Technology

- Gene Sequencing

- Pharmacogenomics

- Microarray Technology

- AI-driven Analytics Platforms

- Other Technologies

- Gene Sequencing

- By Application

- Genomics

- Proteomics

- Transcriptomics

- Metabolomics

- Epigenomics

- Other Applications

- Genomics

- By End User

- Biotechnology & Pharmaceutical Companies

- Clinical Diagnostics Laboratories

- Hospitals & Academic Medical Centers

- CROs & Biobanks

- Other End Users

- Biotechnology & Pharmaceutical Companies

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with directors of high-throughput sequencing centers, hospital molecular-pathology chiefs, and product managers at bioinformatics platform vendors across North America, Europe, and Asia.

Their experience refined uptake rates, typical service bundles, and near-term investment signals that our desk work could not fully capture.

Desk Research

We began by mapping open datasets from the US National Institutes of Health, the European Bioinformatics Institute, and the China National Center for Bioinformation, after which we checked sequencer imports through Volza to trace installed bases country by country.

Annual reports, 10-Ks, and investor decks of sequencing platform vendors let us anchor average interpretation fees, while white papers from the Personalized Medicine Coalition and peer-reviewed work in journals such as Nature Biotechnology clarified clinical adoption curves.

A second sweep drew on paid feeds, D&B Hoovers for company splits, Dow Jones Factiva for deal flow, and Questel for patent velocity, so we could cross-verify pipeline counts and pricing ladders.

These examples are illustrative; many other open and subscription sources informed data collection, validation, and contextual checks.

Market-Sizing & Forecasting

We coupled a top-down and bottom-up blend.

A demand rebuild used cancer incidence, pharmacogenomic test penetration, installed next-generation sequencing capacity, and per-sample analysis fees; supplier roll-ups and sampled ASP × volume served as counter-checks.

Key drivers, cloud compute spend per tertiary center, fresh companion-diagnostic approvals, and active multi-omics projects, feed a multivariate regression that shapes the 2025-2030 outlook.

Divergences between approaches were blended using analyst-agreed weights.

Data Validation & Update Cycle

Outputs pass a two-step peer review, variance flags trigger source call-backs, and figures are reconciled with independent indicators before sign-off.

Reports refresh annually, and any material event prompts an interim update so clients always receive our latest view.

Why Mordor's Personalized Medicine Bioinformatics Baseline Earns Trust

Benchmark comparison

Published estimates diverge because firms adopt wider bioinformatics scopes, apply list versus realized prices, or update on different cadences. Our disciplined segmentation and yearly recalibration keep numbers rooted in patient-centric use cases.

Key gap drivers include whether indirect informatics tools are counted, how price indexing is handled, and the currency conversion method. Studies folding the full bioinformatics landscape naturally read higher, while service-only lenses undercount integrated platforms.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 3.51 B | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 3.87 B | Global Consultancy A | Omits cloud-platform license fees | ||

USD 31.74 B | Global Consultancy B | Counts full bioinformatics, not limited to personalized care | ||

USD 4.18 B | Trade Journal B | Focuses on outsourced services, excludes on-premise software |