Personal Cooling Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

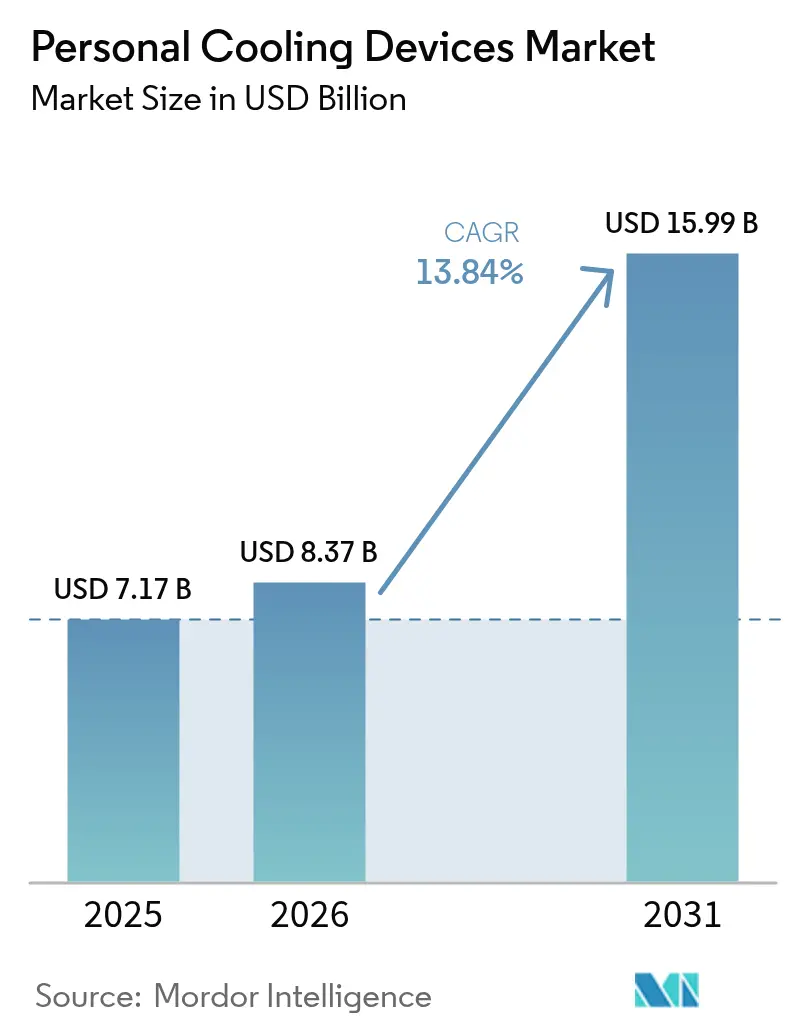

| Market Size (2026) | USD 8.37 Billion |

| Market Size (2031) | USD 15.99 Billion |

| Growth Rate (2026 - 2031) | 13.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Cooling Devices Market Analysis by Mordor Intelligence

The Personal Cooling Devices Market size was valued at USD 7.17 billion in 2025 and is estimated to grow from USD 8.37 billion in 2026 to reach USD 15.99 billion by 2031, at a CAGR of 13.84% during the forecast period (2026-2031).

Heightened climate volatility, tighter workplace‐safety codes, and the appeal of spot cooling over whole-room air conditioning are accelerating adoption across factories, homes, and medical facilities. Rapid cost declines in micro-Peltier modules, widespread USB-C charging infrastructure, and direct-to-consumer storefronts are shrinking payback periods, while recurring heat emergencies have moved personal cooling from a discretionary to a risk-mitigation purchase. At the same time, lithium-ion battery safety recalls and rising import tariffs are erecting new compliance and cost hurdles, nudging premium brands toward over-engineered thermal controls and localized manufacturing. Competition now spans consumer-electronics majors, industrial-safety specialists, and venture-backed healthcare start-ups, each leveraging unique channel advantages to capture the personal cooling devices market.

Key Report Takeaways

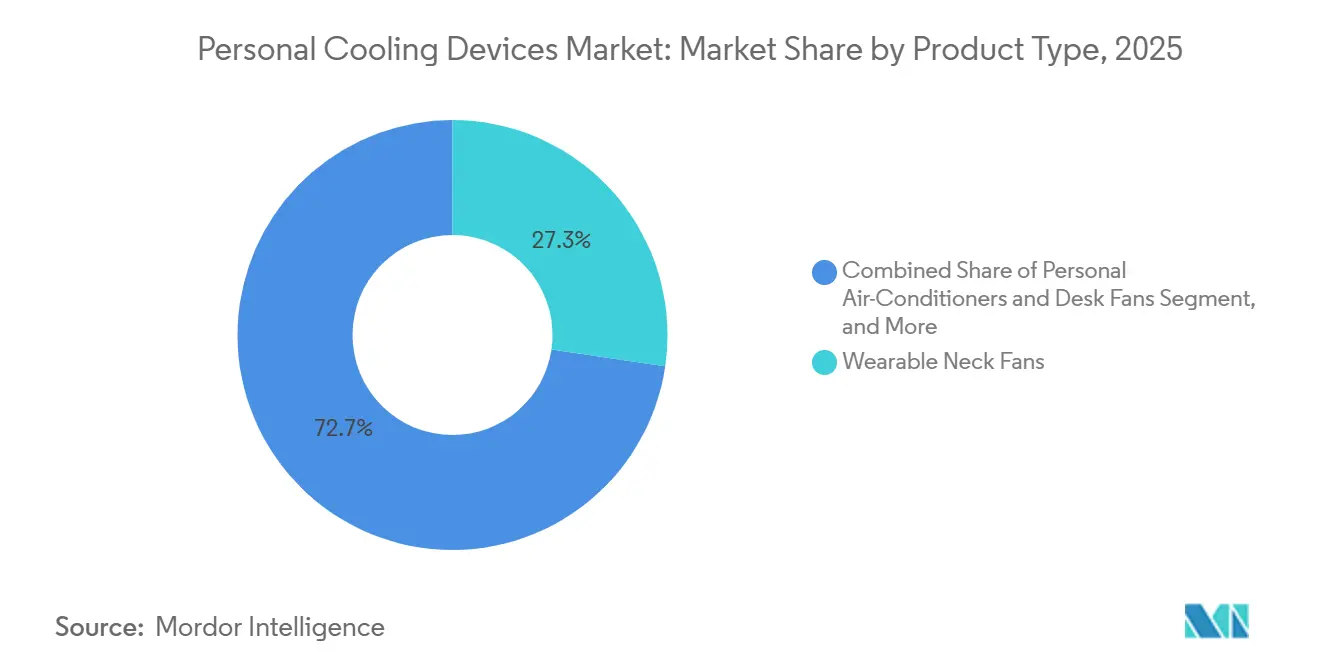

- By product type, wearable neck fans held 27.32% of the personal cooling devices market share in 2025 and are forecast to grow at a 14.82% CAGR through 2031.

- By cooling technology, evaporative formats commanded 36.54% of the personal cooling devices market in 2025, while hybrid solid-state systems are projected to post the fastest CAGR of 14.79% through 2031.

- By end user, the residential segment led with 29.62% revenue share in 2025; healthcare and elderly care applications are expected to advance at a 15.03% CAGR through 2031.

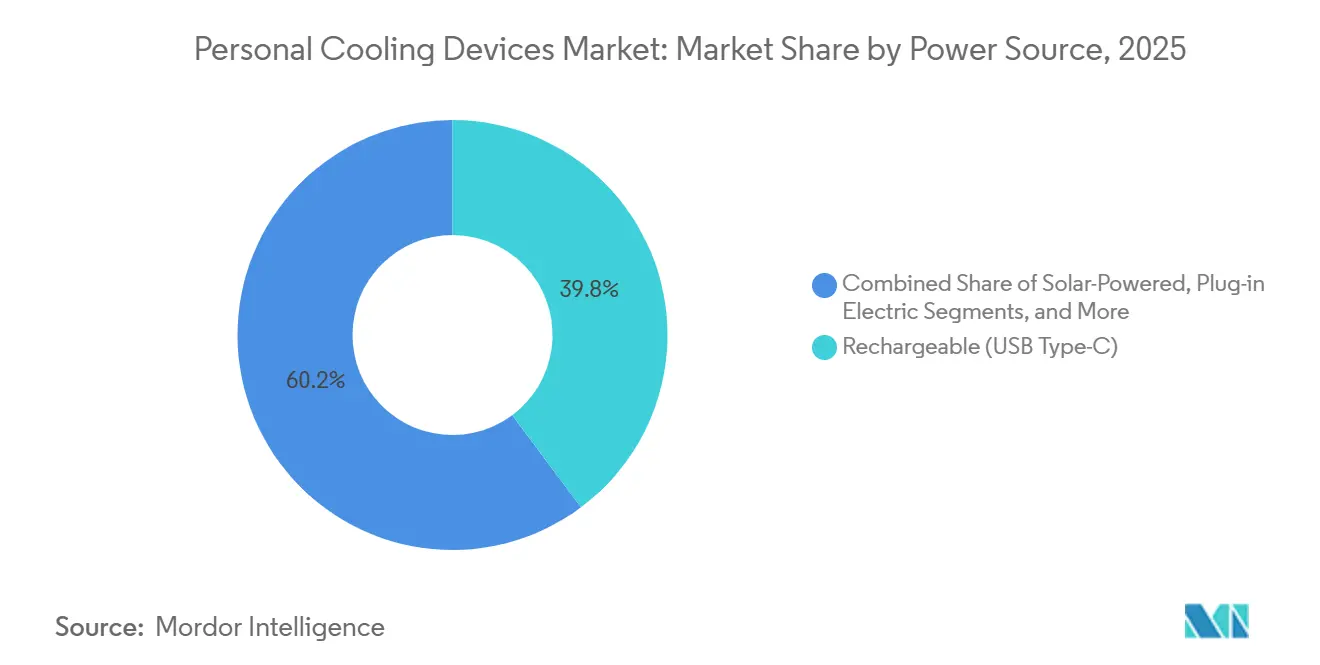

- By power source, USB Type-C rechargeable devices captured 39.80% share of the personal cooling devices market size in 2025, while solar-powered units are projected to expand at a 14.88% CAGR through 2031.

- By distribution channel, the online e-commerce and direct-to-consumer segment secured 65.33% of the personal cooling devices market share in 2025 and is projected to expand at a 14.27% CAGR through 2031.

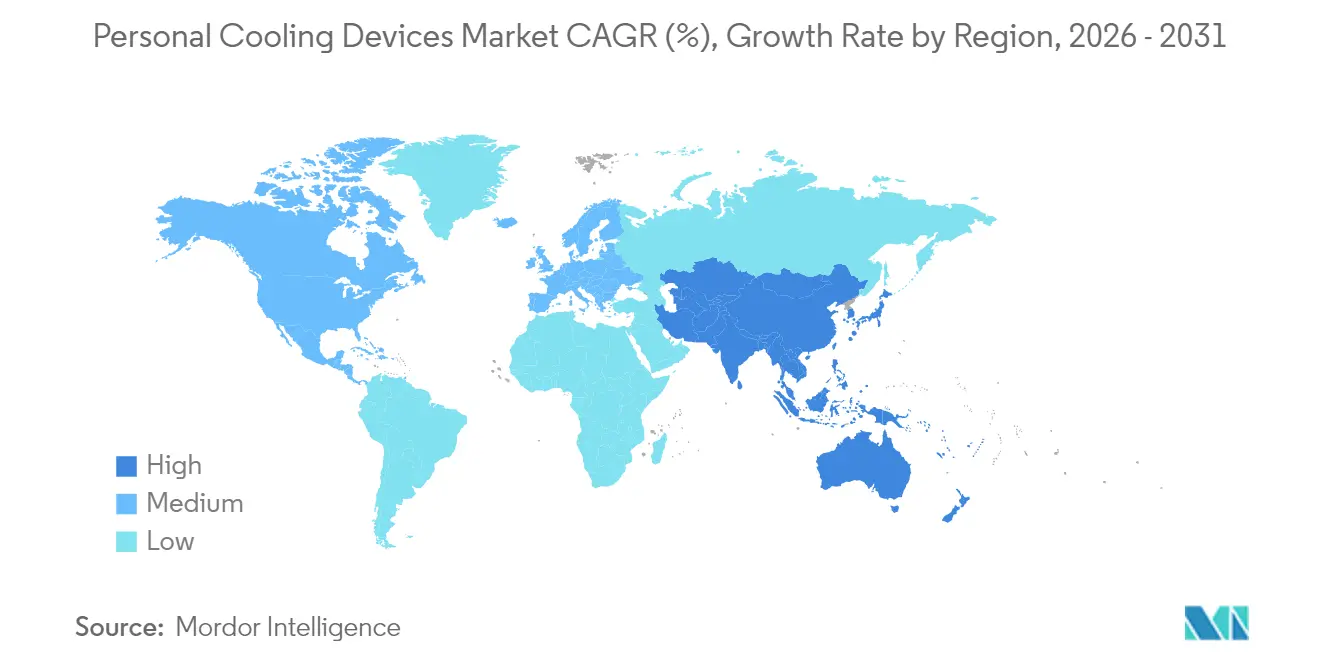

- By geography, Asia-Pacific captured 44.32% revenue share in 2025 and is projected to register a 14.91% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Cooling Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-Resilient Building Codes Pushing Household Adoption | +2.8% | North America, Europe | Medium term (2-4 years) |

| Industrial Heat-Stress Regulations (US OSHA, EU Directive) | +2.5% | Global, early movers in United States, Germany, France | Short term (≤ 2 years) |

| Rapid E-Commerce Availability of Low-Cost USB Fans | +2.1% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Micro-Peltier Cost Drops from Semiconductor Over-Capacity | +2.3% | Global, manufacturing in China and Japan | Medium term (2-4 years) |

| Military Procurement of Wearable Cooling Vests | +1.6% | United States, NATO nations | Medium term (2-4 years) |

| Esports Venues Demand for Silent, Spot-Cooling Gear | +1.2% | North America, Europe, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Resilient Building Codes Pushing Household Adoption

California’s 2022 energy-efficiency amendments and British Columbia’s 2024 Step Code updates embed passive‐cooling mandates that implicitly favor compact, battery-powered devices over power-hungry central air conditioning.[1]California Energy Commission, “2022 Building Energy Efficiency Standards,” energy.ca.gov Developers of multifamily dwellings are turning to portable cooling as a low-capex pathway to code compliance, accelerating household uptake across North America. Early-stage pilots under the European Union’s Energy Performance of Buildings Directive replicate this framework, positioning personal cooling device market products as distributed complements to envelope retrofits. Regulatory lead times of two to four years suggest a steep adoption ramp beginning in 2027. As building energy codes converge on net-zero targets, portable spot-cooling solutions become a default design variable rather than an aftermarket purchase. This policy shift reinforces residential demand resilience even when macroeconomic headwinds curb discretionary spending.

Industrial Heat-Stress Regulations (US OSHA, EU Directive)

OSHA’s National Emphasis Program obliges employers in warehousing, construction, and agriculture to furnish engineering or administrative controls that cut heat illness risk, explicitly listing phase-change vests and evaporative bandanas as acceptable solutions.[2]U.S. Department of Labor, “OSHA National Emphasis Program – Outdoor and Indoor Heat-Related Hazards,” osha.gov Complementary EU rules require mitigation once indoor temperatures exceed 26 °C. Compliance pressure has pulled forward procurement cycles, and uniform standards such as ASTM F1506 simplify purchasing by codifying flame-resistant performance. As claims data increasingly link heat stress to workplace injuries, insurers have begun discounting premiums for employers that deploy certified cooling gear. The net result is an enforceable demand floor that cushions the personal cooling devices market against consumer-spending swings.

Rapid E-Commerce Availability of Low-Cost USB Fans

Cross-border marketplaces and same-day logistics let Chinese brands retail sub-USD 20 neck fans to U.S. and European shoppers without channel mark-ups.[3]Amazon, “Summer Flash Sale Neck Fans,” amazon.com Social-media advertising funnels heat-wave driven impulse purchases directly to checkout pages, creating seasonal demand spikes that brick-and-mortar chains struggle to match. The ubiquity of USB-C chargers removes platform friction, while influencer reviews accelerate trust building among first-time buyers. Pandemic-era work-from-home habits have further entrenched desktop and neck-worn fans as everyday accessories, expanding the addressable household base. As marketplaces tighten product-safety policing, brands that can document battery certifications gain visibility advantages, reinforcing a winner-takes-most dynamic in the personal cooling devices market.

Micro-Peltier Cost Drops from Semiconductor Over-Capacity

Legacy 150 mm and 200 mm wafer lines, facing smartphone demand plateaus, have pivoted to thermoelectric module fabrication, slashing average selling prices by roughly 35% between 2022 and 2025. Sony’s REON POCKET 5, launched at GBP 139 (USD 177) in 2024, embodies this shift, delivering 1.5 times higher heat absorption yet retailing below its 2020 predecessor. Similar cost curves from Japanese and Korean suppliers unlock premium-performance devices for mass-market buyers, especially in heat-prone Asia-Pacific metros. Peltier miniaturization also broadens healthcare use cases by enabling moisture-free cooling under sterile conditions. As module prices trend downward, BOM savings outpace lithium-ion pack cost inflation, preserving gross margins for brands positioned at the top of the personal cooling devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficiency Gains in Room-Scale HVAC Lowering Incremental Benefit | -1.4% | Developed markets with high HVAC penetration | Medium term (2-4 years) |

| Product Safety Recalls (Battery Fires, Neck-Fan Blade Injuries) | -1.1% | United States, European Union | Short term (≤ 2 years) |

| Lack of Recycling Streams for Mini-Li-Ion Packs | -0.7% | European Union, Global | Long term (≥ 4 years) |

| Import Tariffs on Finished Electronics in Key Markets | -0.9% | United States, India, select EU member states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Efficiency Gains in Room-Scale HVAC Lowering Incremental Benefit

ENERGY STAR room air conditioners now post seasonal energy-efficiency ratios above 12, a 25% leap over 2019 baselines. Parallel heat-pump incentives in the United States and Europe reduce cooling operating costs, eroding the value proposition of a USD 50 neck fan inside climate-controlled homes. High-SEER heat pumps can sustain 22 °C ambient temperatures at one-third the electricity draw of legacy compressors, particularly when paired with rooftop photovoltaics. Consequently, households in mature HVAC markets view personal devices as supplemental rather than primary solutions, capping per-capita unit sales. Yet the restraint is asymmetric: in India and parts of Africa where air-conditioning penetration sits below 50%, portable devices remain the first line of defense against heat waves. Divergent grid reliability and income levels thus mediate the overall drag on the personal cooling devices market.

Product Safety Recalls (Battery Fires, Neck-Fan Blade Injuries)

The United States Consumer Product Safety Commission recalled 48,000 Living Glow waist fans in October 2025 and 22,600 IcyBreeze misting fans the prior month after lithium-ion thermal runaway incidents.[4]U.S. Consumer Product Safety Commission, “Living Glow Waist Fans Recall,” cpsc.gov Such events heighten consumer risk perceptions and prompt stricter certification requirements under the EU Battery Regulation. Low-cost brands reliant on Tier-3 cell suppliers face margin compression as they retrofit battery-management systems with redundant thermal fuses. Parallel design pivots toward bladeless architecture, showcased by Razer’s Project Arielle gaming chair unveiled in 2025, aims to mitigate laceration hazards. While premium players monetize safety as a differentiator, short-term recall publicity dents category-wide demand, trimming the growth curve for personal cooling devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wearable Neck Fans Sustain Cost-Led Dominance

Wearable neck fans accounted for 27.32% of the personal cooling devices market share in 2025, moving at a 14.82% CAGR to 2031. Entry-level brands such as Xiaomi retail sub-USD 20 models through flash sales, while Fujitsu General’s next-generation wearable air conditioner, slated for spring 2025 at JPY 60,000 (USD 421), signals a feature-rich ceiling. Design refreshes every 12 months compress product life cycles, and USB-C fast charging lifts daily runtime above 8 hours. Personal air conditioners and desk fans lag but benefit from hybrid home-office setups. Cooling apparel leverages ASTM-compliant flame resistance to serve industrial contracts, whereas handheld fans remain relevant for budget-constrained outdoor recreation. Thermoelectric personal coolers remain a niche but earn outsized media coverage, pulling premium shoppers into the personal cooling devices market.

Evolving ergonomics and modular battery packs allow neck-fan vendors to upsell spare power units, bolstering aftermarket revenues. Meanwhile, mid-tier desk fans integrate IoT sensors to auto-adjust airflow based on skin-temperature readings, a feature first commercialized in Japanese gaming cafes. Rigorous ingress-protection ratings open additional addressable markets in dusty mining and construction sites. Although phase-change vests are slower-moving SKUs, they exhibit low warranty return rates, reinforcing channel margins for industrial distributors. Cumulatively, category diversification locks in multi-tier pricing, cushioning revenue swings and enlarging the personal cooling devices market size.

By Cooling Technology: Evaporative Retains Lead, Hybrid Solid-State Ascends

Evaporative platforms accounted for 36.54% of the personal cooling devices market in 2025, prized for their water-activation simplicity and zero electronics. However, performance drops sharply when relative humidity exceeds 70%, steering Southeast Asian consumers toward Peltier or hybrid options. Thermoelectric systems sidestep moisture concerns and now post battery lifetimes rivaling fan-based units, thanks to higher-density 21700 cells. Phase-change materials dominate heavy-industry niches, providing 18 °C microclimates for welders and utility linemen in compliance with NFPA 70E apparel mandates. Air-circulation devices commoditize fastest as OEM factories in Guangdong scale to 10-million-unit monthly capacity.

Hybrid solid-state designs marry evaporative membranes with Peltier heat pumps to extend runtime in arid regions, underpinning a 14.79% forecast CAGR. Academic breakthroughs in carbon-doped phase-change slurries promise 0.5 °C deeper reductions in core temperature, with first-generation vests entering clinical trials in 2026. Regulatory frameworks like ISO 9920, which define clothing thermal insulation, are beginning to explicitly cite personal devices, standardizing test protocols that accelerate buyer confidence. As intellectual-property portfolios widen, late entrants must choose between licensing premium solid-state stacks or competing solely on evaporative price, a fork that will reshape technology hierarchy within the personal cooling devices market.

By End User: Residential Leads, Healthcare Outpaces

Households contributed 29.62% of 2025 revenue, reflecting telework and social media promotion. The personal cooling devices market size for healthcare, however, is projected to surge at 15.03% CAGR as menopausal and oncology patients seek drug-free thermal relief. MyCelsius’s GBP 229.99 (USD 292) cooling bracelet exemplifies targeted design for symptom management, delivering eight hours of sub-wrist cooling per charge. Japan’s super-aging demographics compound institutional demand, with nursing homes bundling wearable coolers into summer care packages.

Industrial and construction employers remain perennial buyers, motivated by regulatory penalties. Sports and fitness adoption grows through brand collaborations with marathon organizers who preload race kits with reusable neck towels. Military volumes remain modest yet command ASPs three times the consumer average owing to ballistic-fabric overlays and integrated hydration bladders. Outdoor recreation and travel purchases fluctuate with tourism cycles, softening in years when disposable income tightens. Diversified end-use traction therefore cushions cyclical volatility across the personal cooling devices market.

By Power Source: USB Type-C Dominates while Solar Carves a Foothold

USB-C rechargeable models captured 39.80% share in 2025, bolstered by smartphone-style quick-charge ecosystems. Brands now bundle 10,000 mAh clip-on battery packs to extend neck-fan runtime beyond 12 hours, a compelling proposition in blackout-prone geographies. Replaceable alkaline or Ni-MH formats linger in low-income markets but face mounting e-waste criticism under the EU Battery Regulation. Plug-in devices find niche success as desktop companions in shared offices where battery devices contravene fire codes.

Solar-assisted units are expected to log the fastest growth at 14.88% CAGR despite present wattage limitations. Hybrid panels stitched into backpack straps trickle-charge internal cells, delivering three extra hours of fan operation during field shifts, a value proposition resonating with agrarian laborers in India’s Gangetic plains. As per-watt photovoltaic costs slide below USD 0.20, designers aim to embed flexible cells along neck-fan collars without bulk penalties, potentially unlocking fully off-grid SKUs by 2030. Battery recycling mandates could accelerate this pivot, reinforcing the environmental narrative inside the personal cooling devices market.

By Distribution Channel: E-Commerce Leads, Offline Holds Niche Strength

Online platforms owned a 65.33% share in 2025, underpinned by algorithmic merchandising and peer reviews that de-risk first-time purchases. Flash-sale events aligned with meteorological heat alerts spike conversion rates, a tactic pioneered by Southeast Asian marketplaces. Direct-to-consumer storefronts secure higher gross margins but bear reverse logistics costs for warranty claims. Offline retailers, though slower-growing, remain indispensable for industrial procurement, where compliance audits require in-person demonstrations. Brick-and-mortar chains also mitigate last-mile barriers in rural Africa, where parcel networks remain patchy.

Physical store exposure boosts brand credibility, enabling premium SKUs to command prices twice the online median in the personal cooling devices market. Some vendors deploy omnichannel loyalty programs that credit in-store service visits toward extended online warranties, thereby blending channel advantages. Regulatory parity across sales modes, the same CE and FCC certificates apply, means differentiation hinges on experiential retail rather than paperwork. As same-day drone delivery pilots scale, the channel split may tilt further in favor of e-commerce, yet localized fit-testing for cooling vests guarantees a continued role for specialty outlets.

Geography Analysis

Asia-Pacific led with a 44.32% slice of 2025 revenue and is projected to grow at a 14.91% CAGR. Japan’s 2024 heat wave, featuring consecutive 35 °C days, normalized personal cooling as daily attire, while China’s coastal megacities adopted sub-USD 20 neck fans en masse, leveraging abundant e-commerce logistics. India’s tier-2 cities, hammered by grid outages, gravitate toward high-capacity battery or hybrid solar devices. South Korea’s esports arenas prize low-noise bladeless cooling, a niche captured by Razer’s Project Arielle concept. Local manufacturing clusters in Guangdong, Hanoi, and Dhaka shorten supply chains, buffer tariff exposure, and feed the personal cooling devices market.

North America benefits from OSHA heat-stress mandates and California’s building codes, but faces 80% HVAC penetration that dilutes residential benefits. Industrial, military, and outdoor-recreation segments, therefore, dominate incremental growth. Section 301 tariffs at 25%, combined with proposed universal rates, threaten cost structures for import-reliant brands, nudging some assembly to Mexico or the southern United States. Europe’s trajectory intertwines with worker-safety directives and circular-economy rules on battery recycling, which raise compliance costs yet level the playing field by filtering out sub-par imports.

The Middle East posts high per-capita spending owing to 50 °C summer peaks, but fragmented distribution and cash-on-delivery norms slow unit velocity. Africa exhibits dichotomous demand: South Africa’s 2024 load-shedding crisis spurred battery fan sales, while affordability still caps sub-Saharan volumes. South America’s Brazil and Argentina witnessed record 2024 heat, pushing personal cooling onto household wish lists; however, currency volatility and import duties temper growth. Collectively, diverse climatic and regulatory backdrops craft a mosaic of opportunities, ensuring the personal cooling devices market remains geographically balanced.

Competitive Landscape

The market skews toward moderate fragmentation, with consumer-electronics titans Sony, Panasonic, LG, and Dyson facing off against specialized safety outfits Ergodyne and Lakeland Industries and agile start-ups like MyCelsius and Evapolar. Sony’s REON POCKET 5 and Dyson’s USD 650 Zone headphones exemplify premium differentiation, whereas Xiaomi floods online channels with sub-USD 20 SKUs that undercut incumbents by up to 70%. Industrial stronghold Ergodyne leverages ASTM F1506 compliance to secure repeat orders for USD 430 flame-resistant vests, blunting price wars by selling occupational safety rather than gadgets.

R&D pipelines reveal thermal-management technology as the primary moat. Fujitsu General’s 2025 neck-worn Peltier cooler eliminates previous waist-mounted models, slashing donning time to 10 seconds and broadening its appeal among logistics workers. Razer’s bladeless Project Arielle chair targets esports arenas where fan noise is taboo, signaling category expansion beyond wearables. MyCelsius’s medical-grade bracelet scored visibility through the BUPA Eco-Disruptive program, illustrating healthcare white space still open to newcomers. Chinese OEMs, facing tariff headwinds, flirt with Latin American assembly to preserve cost leadership.

Battery-safety certifications and recycling liabilities are emerging differentiation axes. Brands investing in UL 1642 cell testing command higher shelf placement on regulated marketplaces, while compliance failures risk delisting. Intellectual-property skirmishes over hybrid evaporative-Peltier patents intensify as revenue stakes climb. Alliances with logistics and insurance partners round out strategic playbooks, cementing stakeholder ecosystems around the personal cooling devices market.

Personal Cooling Devices Industry Leaders

Honeywell International Inc.

O2COOL LLC

Panasonic Holdings Corp.

Dyson Ltd.

LG Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: MyCelsius launched its Cooling Bracelet in the United Kingdom at GBP 229.99 (USD 292), a thermoelectric wearable aimed at menopausal symptom relief.

- October 2025: The United States Consumer Product Safety Commission recalled 48,000 Living Glow waist fans over lithium-ion fire hazards.

- September 2025: The United States Consumer Product Safety Commission recalled 22,600 IcyBreeze portable misting fans for the same defect category.

- January 2025: Razer unveiled Project Arielle, a concept gaming chair with integrated bladeless cooling, at CES 2025.

Global Personal Cooling Devices Market Report Scope

The Personal Cooling Devices Market Report is Segmented by Product Type (Personal Air-Conditioners and Desk Fans, Hand-Held Cooling Devices, Wearable Neck Fans, Cooling Apparel including Vests and Towels, Thermoelectric Personal Coolers), Cooling Technology (Evaporative, Thermoelectric Peltier, Phase-Change Material, Air-Circulation and Fan-Based, Hybrid and Emerging Solid-State), End User (Industrial and Construction Workers, Military and Defense, Sports and Fitness Enthusiasts, Residential and Household, Healthcare and Elderly Care, Outdoor Recreation and Travel), Power Source (Battery-Powered Replaceable, Rechargeable USB Type-C, Plug-In Electric, Solar-Powered, Hybrid Battery plus Solar), Distribution Channel (Online E-Commerce and D2C, Offline Retail Chains and Specialty), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value in USD.

| Personal Air-Conditioners and Desk Fans |

| Hand-Held Cooling Devices |

| Wearable Neck Fans |

| Cooling Apparel (Vests, Towels) |

| Thermoelectric Personal Coolers |

| Evaporative |

| Thermoelectric (Peltier) |

| Phase-Change Material |

| Air-Circulation / Fan-Based |

| Hybrid / Emerging Solid-State |

| Industrial and Construction Workers |

| Military and Defense |

| Sports and Fitness Enthusiasts |

| Residential / Household |

| Healthcare and Elderly Care |

| Outdoor Recreation and Travel |

| Battery-Powered (Replaceable) |

| Rechargeable (USB Type-C) |

| Plug-In Electric |

| Solar-Powered |

| Hybrid (Battery + Solar) |

| Online (E-Commerce, D2C) |

| Offline (Retail Chains, Specialty) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Personal Air-Conditioners and Desk Fans | |

| Hand-Held Cooling Devices | ||

| Wearable Neck Fans | ||

| Cooling Apparel (Vests, Towels) | ||

| Thermoelectric Personal Coolers | ||

| By Cooling Technology | Evaporative | |

| Thermoelectric (Peltier) | ||

| Phase-Change Material | ||

| Air-Circulation / Fan-Based | ||

| Hybrid / Emerging Solid-State | ||

| By End User | Industrial and Construction Workers | |

| Military and Defense | ||

| Sports and Fitness Enthusiasts | ||

| Residential / Household | ||

| Healthcare and Elderly Care | ||

| Outdoor Recreation and Travel | ||

| By Power Source | Battery-Powered (Replaceable) | |

| Rechargeable (USB Type-C) | ||

| Plug-In Electric | ||

| Solar-Powered | ||

| Hybrid (Battery + Solar) | ||

| By Distribution Channel | Online (E-Commerce, D2C) | |

| Offline (Retail Chains, Specialty) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the personal cooling devices market in 2026?

It is valued at USD 8.37 billion, on track to reach USD 15.99 billion by 2031 at a 13.84% CAGR.

Which product leads unit sales?

Wearable neck fans hold 27.32% of 2025 revenue and keep the top slot thanks to sub-USD 20 price points and annual design refreshes.

What segment is growing fastest?

Healthcare and elderly care users are projected to expand at 15.03% CAGR through 2031 as thermoelectric wearables ease menopausal and medical heat stress.

Why is Asia-Pacific dominant?

Extreme heat events, dense e-commerce networks, and regional manufacturing scale give Asia-Pacific 44.32% of 2025 revenue and a 14.91% CAGR outlook.

How are safety recalls shaping the category?

Lithium-ion fire incidents spurred stricter battery certifications, inflating costs for low-end makers but enabling premium brands to differentiate on safety.

What is driving technology innovation?

Falling micro-Peltier prices and hybrid evaporative-solid-state research fuel new products that offer longer runtimes and moisture-free cooling.

Page last updated on: