Cochlear Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

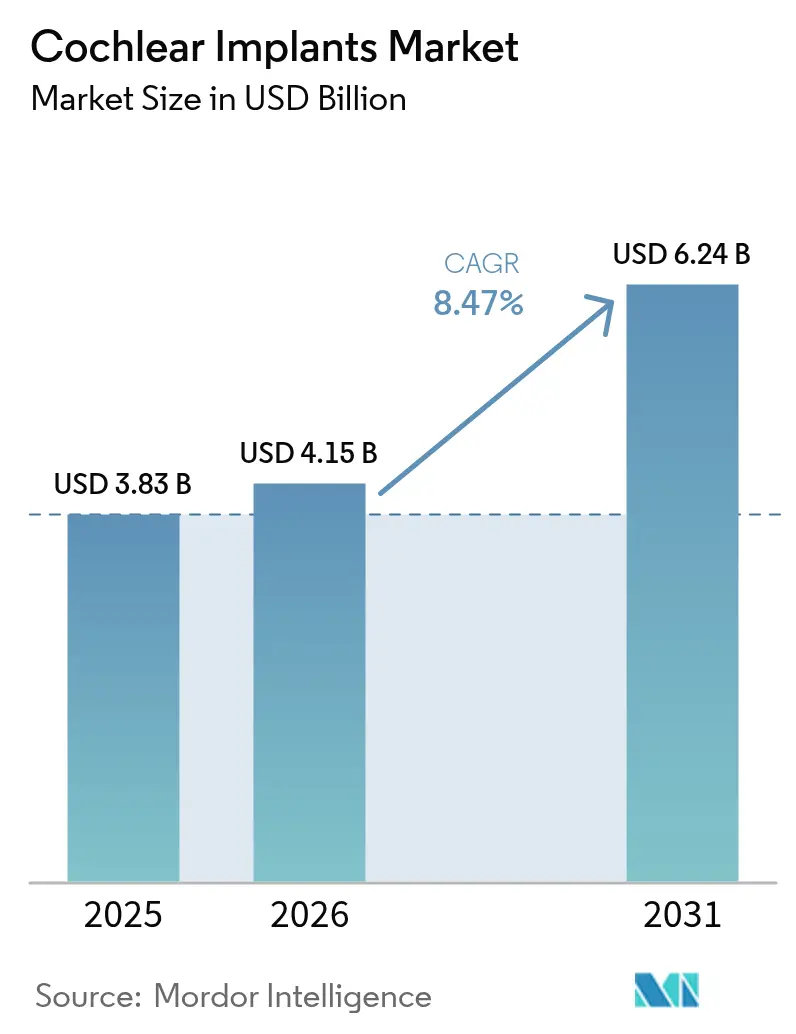

| Market Size (2026) | USD 4.15 Billion |

| Market Size (2031) | USD 6.24 Billion |

| Growth Rate (2026 - 2031) | 8.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cochlear Implants Market Analysis by Mordor Intelligence

The cochlear implants market size was valued at USD 3.83 billion in 2025 and estimated to grow from USD 4.15 billion in 2026 to reach USD 6.24 billion by 2031, at a CAGR of 8.47% during the forecast period (2026-2031). Sustained demand arises from an aging global population, expanding indications that now cover single-sided and asymmetric hearing loss, and continuous innovation in fully implanted devices that remove external hardware. Wider Medicare coverage in the United States and similar reimbursement reforms in Europe are accelerating adult and geriatric uptake. Meanwhile, pediatric volumes are climbing as regulators lower minimum age thresholds and clinicians document superior language development when implantation occurs early. On the competitive front, vertical integration and patent-driven differentiation remain decisive, with fully implantable systems poised to redraw share allocations once commercial launches begin.

Key Report Takeaways

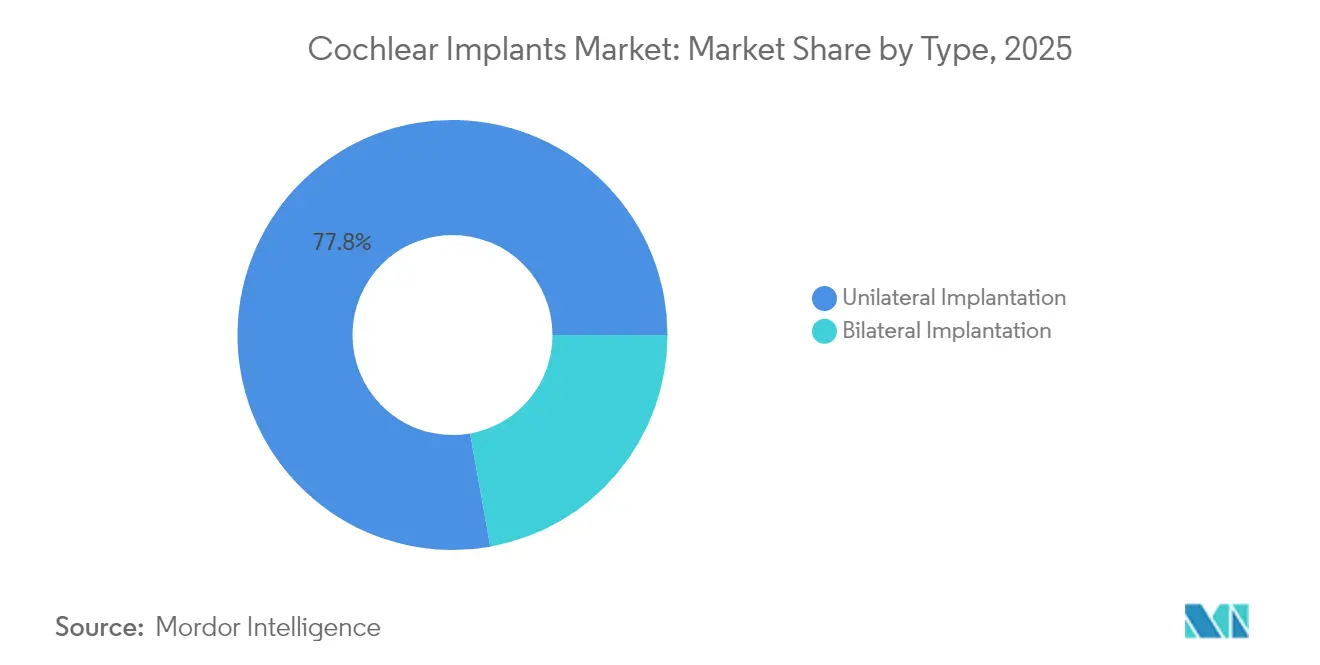

- By type, unilateral procedures held 77.82% of cochlear implants market share in 2025, whereas bilateral implantation is projected to expand at 9.05% CAGR through 2031.

- By hearing-loss severity, severe cases commanded 69.05% share of the cochlear implants market size in 2025, while moderate loss is advancing at 9.18% CAGR to 2031.

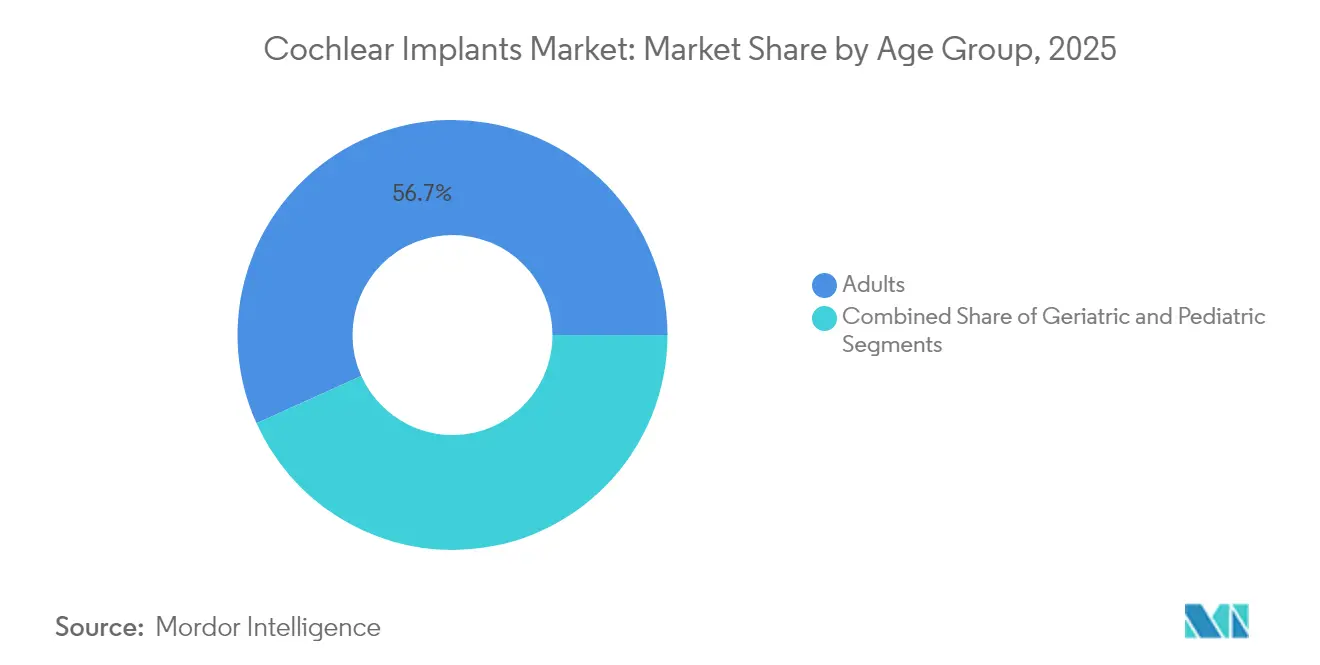

- By age group, adults captured 56.74% revenue in 2025; pediatric volumes are rising fastest at 9.11% CAGR to 2031.

- By end user, hospitals led with 57.61% revenue share in 2025; specialty clinics deliver the highest forecast CAGR at 8.98% through 2031.

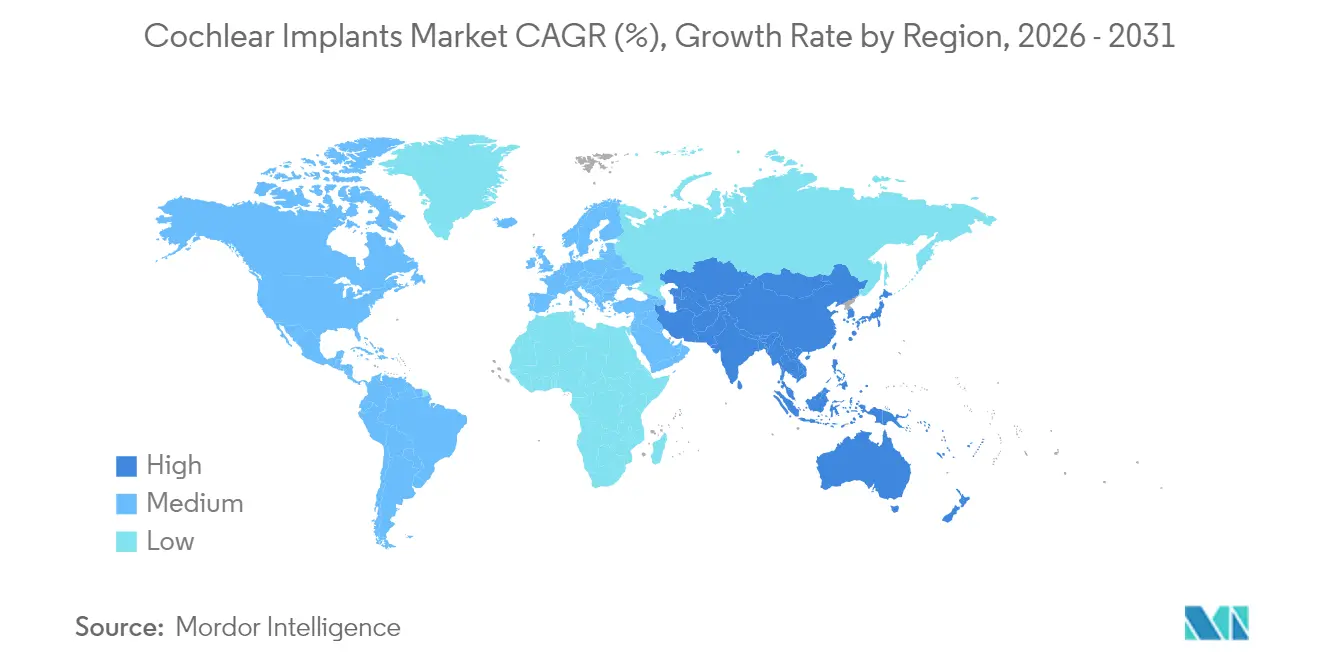

- By geography, North America contributed 41.78% revenue in 2025, whereas Asia-Pacific is tracking a 9.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cochlear Implants Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Geriatric Pool with Severe-To-Profound Hearing Loss | +2.1% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Noise-Induced Hearing Loss in Younger Demographics | +1.8% | Global, particularly developed markets with industrial exposure | Medium term (2-4 years) |

| Miniaturisation & Longer Battery Life of CI Systems | +1.5% | Global | Medium term (2-4 years) |

| Expanded Candidacy for Single-Sided & Asymmetric Hearing Loss | +1.3% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Breakthrough Fully Implanted Cochlear Implants | +0.9% | North America initially, global rollout | Long term (≥ 4 years) |

| Growing Awareness About the Advantages of Cochlear Implants | +0.8% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Pool with Severe-To-Profound Hearing Loss

Older adults already represent most new cochlear implant recipients, and clinical data confirm that implantation substantially improves speech perception even after age 70 years. Expanded Medicare eligibility for asymmetric loss is removing historical reimbursement barriers and could unlock treatment for several million newly qualified seniors [1]Smith HJ, "Hearing Benefits of Cochlear Implantation in Older Adults With Asymmetric Hearing Loss," PUBMED, pubmed.ncbi.nlm.nih.gov. Policy makers emphasize that each implanted senior yields significant societal savings through reduced healthcare utilization and improved independence, supporting the positive economic case advanced by device manufacturers [2]American Cochlear Implant Alliance, "ACI Alliance Submits Formal Request for Medicare Coverage of Cochlear Implantation in Single-Sided Deafness and Asymmetric Hearing Loss," acialliance.org.

Noise-Induced Hearing Loss in Younger Demographics

Industrial noise exposure and prolonged headphone use are driving earlier onset of severe sensorineural deficits, with epidemiological reviews charting sustained increases among adolescents between 1990 and 2021. Younger users show strong adoption of digital health tools and typically experience longer productive work lives, increasing the lifetime return on implantation [3]Zhifeng Guo, "Global, regional, and national burden of hearing loss in children and adolescents, 1990–2021: a systematic analysis from the Global Burden of Disease Study 2021," bmcpublichealth.biomedcentral.com. FDA expansions that authorize implantation in less disabled ears—such as MED-EL’s extended indications—are accelerating uptake in this cohort.

Miniaturization & Longer Battery Life of CI Systems

Patent filings covering passive recharge and biocompatible microphones illustrate the push toward fully internal, cosmetically invisible devices. Researchers at MIT have demonstrated piezoelectric eardrum sensors that can convert mechanical vibration into electrical signals, removing the need for external microphones. These advances directly address the low global penetration rate—estimated at only 5% of candidates—by tackling user concerns over lifestyle disruption.

Expanded Candidacy for Single-Sided & Asymmetric Hearing Loss

The FDA now recognizes cochlear implantation as a clinically sound option for single-sided deafness, citing marked gains in sound localization and speech-in-noise perception. Academic modeling indicates that more than 1 million Americans meet the revised audiological criteria yet remain untreated. Manufacturers that tailor electrode arrays and software to asymmetric profiles are expected to win share as awareness builds among otolaryngologists.

Restraints Impact Analysis of Cochlear Implants Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device, Surgery & After-Care Costs | -1.9% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Surgical-Procedure and Anaesthesia–Related Risks | -1.2% | Global, with higher impact in regions with limited surgical infrastructure | Medium term (2-4 years) |

| Low Awareness in Underdeveloped Regions | -0.8% | Sub-Saharan Africa, parts of Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Supply-Chain Crunch for Medical-Grade Semiconductors | -0.7% | Global, with particular impact on manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device, Surgery & After-Care Costs

Full treatment—device, surgery, anesthesia, programming, and habilitation—typically exceeds USD 100,000 per patient, placing the therapy out of reach in low-income settings. Cost-effectiveness studies in South America and Asia show favorable lifetime economics, yet cash-flow constraints and limited insurance penetration defer adoption. Legislative proposals such as the Hearing Device Coverage Clarification Act aim to widen U.S. reimbursement but remain pending.

Supply-Chain Crunch for Medical-Grade Semiconductors

Chip shortages have lengthened lead times for digital signal processors and power-management ICs, prompting major producers to dual-source or redesign boards. Industry surveys place supply-chain expenses in 2025 at 18-20% of sales, eroding margins and delaying shipments, especially for pediatric backlogs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cochlear Implants Market Segment Analysis

By Type:

Bilateral Uptake Strengthens Quality-of-Life OutcomesUnilateral implantation held 77.82% of the cochlear implants market share in 2025. Although unilateral surgery remains dominant, mounting evidence shows that simultaneous bilateral implantation delivers superior speech understanding and spatial awareness in noisy environments. Sequential procedures remain common in adults due to funding limitations, whereas most pediatric centers now default to concurrent bilateral placement. The cochlear implants market size for bilateral systems is projected to expand at 9.05% CAGR, reflecting improving reimbursement in Europe and Japan. Manufacturers are focusing on synchronizing processor firmware to counter asymmetric outcomes, while surgeons refine atraumatic electrode insertion to preserve residual hearing.

Clinical societies increasingly recommend early bilateral intervention, citing neuroplastic advantages that drive language acquisition and social integration. In response, device makers are extending battery capacity to 48 hours of continuous use and simplifying magnet adjustments to reduce follow-up visits. These technical advances, coupled with outcome data, are nudging payers toward parity coverage, positioning bilateral implantation as the future mainstream standard within the cochlear implants market.

By Hearing Loss Type:

Moderate Cases Expand Addressable PoolModerate hearing loss is growing faster than the severe segment, with a CAGR of 9.18%. FDA guidance now permits implantation when aided speech scores fall below 60%, a threshold that captures patients who previously struggled with conventional amplification. Studies show that early implantation in moderate loss preserves auditory nerve integrity, leading to better long-term outcomes than delayed surgery.

Severe cases still represent the core of the cochlear implants market share, holding 69.05% market share in 2025. Yet growth has plateaued in saturated high-income regions. Profound loss users benefit from next-generation electrode arrays engineered for near-total cochlear coverage, improving music appreciation and tonal language recognition. Together, these shifts extend the cochlear implants market size and emphasize the need for modular product lines that match diverse residual-hearing profiles across all severity bands.

By Age Group:

Pediatric Interventions AcceleratePediatric are expanding fastest with a CAGR of 9.11% due to lower age clearances and universal newborn screening. The FDA’s 2024 approval of Cochlear’s Osia System for children aged 5 years opened a sizeable new cohort. Long-term studies report that implantation before 12 months yields language scores comparable with normal-hearing peers by age 5 years.

Adults continue to dominate volume holding 56.74% market share in 2025, yet growth is shifting toward seniors as Medicare relaxes asymmetric criteria. Clinics now counsel candidates up to 85 years, provided comorbidities and cognitive function are suitable. Early rehabilitation is crucial; multidisciplinary teams integrating audiology and speech therapy are shortening time-to-benefit and improving patient-reported satisfaction across all ages within the cochlear implants market.

By End User:

Specialty Clinics Capture Procedural ShareHospitals handled 57.61% of global implant surgeries in 2025, but ENT specialty clinics and ambulatory centers are taking share as payers reward cost-efficient outpatient settings. These high-volume centers achieve lower infection rates and faster activation timelines through standardized protocols. The cochlear implants market size attributed to specialty clinics is forecast to climb at 8.98% CAGR, supported by tele-programming platforms that let audiologists fine-tune devices remotely.

Academic medical centers remain crucial for complex cases, such as revision surgeries or patients with cochlear ossification. Manufacturers provide on-site engineers and 3D-printed temporal-bone models to optimize electrode selection in these tertiary environments. Collectively, shifting care pathways underscore the importance of flexible service models across the cochlear implants industry.

Geography Analysis

North America Cochlear Implants Market

North America generated USD 1.6 billion revenue in 2025, equal to 41.78% of the cochlear implants market, buoyed by broad private-insurance coverage and Medicare policy shifts. Bilateral implantation is increasingly reimbursed in Canada, further lifting procedure counts. Clinical networks rely heavily on tele-health mapping, which proved effective in rural Alaska and Appalachia, bridging access gaps.

Europe Cochlear Implants Market

Europe contributed significantly with stable single-digit growth. National health systems fund lifelong device support, yet cost containment pressures encourage tender-based procurement, favoring vendors with robust service footprints. German sickness funds now reimburse fully implanted trials, highlighting regulatory openness to disruptive technology.

APAC Cochlear Implants Market

Asia-Pacific delivered USD 0.73 billion in 2025 but charts the fastest expansion at 9.32% CAGR. China’s provincial subsidy programs cover paediatric implantation, and local manufacturer Shanghai Listen is scaling low-cost internal components that comply with domestic content rules. India is piloting public-private cochlear banks to recycle external processors for low-income families, while Japanese hospitals report near-universal neonatal screening. Across the region, rising disposable incomes and urban hospital construction translate into an enlarging cochlear implants market.

MEA and South America Cochlear Implants Market

Middle East & Africa and South America together represent a significant portion of the market. Uptake is hampered by limited surgeon numbers and high out-of-pocket costs, yet private Saudi hospitals and Brazilian social insurers are funding simultaneous bilateral surgeries for paediatric users. Regional ENT societies are partnering with manufacturers to train local surgical teams, demonstrating early but promising momentum for the cochlear implants market.

Regulatory Landscape

Cochlear implants are regulated as high-risk active implantable medical devices in major markets, which shapes both development and post-market obligations. In the United States, cochlear implants are Class III devices under the FDA and typically require Premarket Approval (PMA), with device-specific requirements anchored in 21 CFR Part 874; FDA-recognized consensus standards such as ANSI/AAMI CI86:2017/(R)2025 also guide expectations for safety, functional verification, labeling, and reliability.

In Europe, manufacturers must comply with Regulation (EU) 2017/745 (MDR), with conformity assessments carried out via notified bodies (for example, TUV SUD) that review both quality management systems and technical documentation. Regulatory requirements continued to evolve with Commission Delegated Regulation (EU) 2026/1451 dated 20 March 2026, which amended MDR provisions relevant to implantable devices and clinical investigation exemptions. This increases the need for up-to-date clinical evaluation strategies and ongoing technical-file maintenance. On the manufacturing side, the FDA continues to use established supplement pathways for process changes, illustrated by Cochlear Americas receiving FDA approval in December 2025 (P970051/S240) for an automated electrode welding process for CI532, CI632, and CI1032 models.

Competitive Landscape

The market is moderately concentrated. Cochlear Limited sustains a decent share in developed economies, supported by broad product lines and 100-plus service centers. Its 2024 purchase of Oticon Medical’s implant business for USD 30 million added 20,000 legacy recipients to the service pool. MED-EL emphasizes electrode innovations and recently aligned with Starkey to offer synchronized Bluetooth streaming for bimodal users.

Advanced Bionics focuses on speech-in-noise algorithms and rechargeable power cells, but a U.S. International Trade Commission patent inquiry involving MED-EL underscores fierce IP defense. Envoy Medical stands apart with its Acclaim fully implanted system, now in pivotal trials under FDA Breakthrough Device status. Sonova’s incremental market entry through its SWORD connectivity chip and strategic acquisitions illustrates how established hearing-aid players leverage distribution synergies.

Price competition remains muted, as providers prioritize clinical performance and post-surgical support over upfront cost. Manufacturers therefore differentiate through remote programming platforms, MRI-compatible magnets, and outcome-based service contracts that guarantee minimum speech-score improvements. The arrival of totally implantable solutions is expected to reconfigure brand loyalties and intensify the battle for future cochlear implants market share.

Cochlear Implants Industry Leaders

-

Cochlear Ltd

-

MED-EL Medical Electronics

-

Sonova (Advanced Bionics Corp)

-

Ototronix

-

Zhejiang Nurotron Biotechnology Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Cochlear Implants Market Companies Covered in this Report

- Cochlear

- MED-EL

- Advanced Bionics (Sonova)

- Zhejiang Nurotron Biotech

- Demant A/S (Oticon Medical)

- iotaMotion

- Envoy Medical Corp.

- Neubio

- Ototronix

- Gaes Medica

- Microson S.A.

- Sivantos Pvt Ltd (Signia)

- Inspiration Hearing Inc.

- Oticon Medical India Pvt Ltd

- Neurelec (MXM)

- Alpha Hearing Tech

- Otodyne Inc.

Market Opportunities and Future Outlook

A key whitespace sits in expanding candidacy and earlier intervention while reducing friction from lifetime service needs, particularly in pediatrics and asymmetric hearing loss populations. An FDA pediatric indication expansion by MED-EL in December 2025, approving cochlear implantation for children seven months and older with bilateral sensorineural hearing loss, offers a concrete pathway to earlier implantation where clinical programs and reimbursement align. In parallel, outpatient and specialty-clinic delivery models that pair surgery with scalable follow-up (including tele-programming and standardized activation pathways) create room for vendors and providers to broaden access without relying only on large hospital systems.

Upgrades across products and platforms also shift value toward longer-lived systems that reduce upgrade barriers and improve convenience. Cochlear introduced a platform concept with internal memory and upgradeable firmware via the Nucleus Nexa System launch in South Korea (May 2026), reinforcing opportunities for service-led revenue models tied to software and compatibility roadmaps. Convenience and sustainability are also visible levers: Cochlear received FDA clearance for the Osia 3 Sound Processor in July 2026 with a rechargeable lithium-ion battery (up to 30 hours per charge), and MED-EL rolled out new rechargeable battery options for SONNET processors in 2026 to support adoption where users and clinics prioritize fewer disposable components and simpler day-to-day management. Beyond hardware, manufacturers are extending into biological adjacencies that can expand the long-term addressable pool, including MED-EL acquiring two gene therapy programs from Rescue Hearing Inc. in June 2026 targeting MYO7A and STRC-related hereditary hearing and balance disorders.

Recent Industry Developments in Cochlear Implants Market

- July 2026: Cochlear received US FDA clearance for the Osia 3 Sound Processor, adding a rechargeable lithium-ion battery (up to 30 hours per charge) and an expanded fitting range. The approval strengthens Cochlear's bone conduction portfolio alongside its cochlear implant franchise, supporting upgrades that clinics can deploy without changing the implanted component.

- June 2026: MED-EL acquired two gene therapy programs from Rescue Hearing Inc. focused on MYO7A and STRC mutations linked to hereditary hearing loss and balance disorders. The acquisition broadens MED-EL's pipeline beyond implant hardware into disease-modifying approaches that can complement or reshape future intervention pathways.

- March 2025: Envoy Medical enrolled initial participants in its pivotal clinical trial for the Acclaim fully implanted cochlear implant. Advancing the pivotal study keeps momentum behind totally implantable architectures that remove external sound processors, a step-change that could reframe product differentiation once regulatory submissions progress.

Cochlear Implants Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenues linked to cochlear implant systems used to restore hearing, including the implanted device and the external processing hardware used in clinical practice, along with the core care pathway needed for patient use.

Scope exclusions: Standalone hearing aids, general audiology diagnostic equipment, and ear, nose, and throat procedures not tied to cochlear implantation are excluded.

Segments Covered in This Report

-

By Type

- Unilateral Implantation

- Bilateral Implantation

-

By Hearing Loss Type

- Moderate

- Severe

-

By Age Group

- Adults

- Geriatrics

- Pediatrics

-

By End User

- Hospitals

- Specialty Clinics

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the base context and to avoid building the model on one data stream. We leaned on public, non-paywalled sources such as WHO hearing loss publications, CDC hearing health materials, OECD health statistics, and NIH and PubMed indexed clinical literature to understand prevalence, candidacy, and outcomes that affect uptake.

We also reviewed sources such as national health ministry reimbursement notes, hospital and clinic websites, professional society guidance for cochlear implantation, and investor presentations and annual filings for supply-side signals like installed base and upgrade cycles. In a few places, paid subscriptions for company financials and intelligence, patent databases, and news and financials were used to cross-check timelines and product refresh themes. These examples are not exhaustive, and many other public and paid sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating demand formation and the revenue build, since procedure coverage, clinical pathways, and processor replacement timing can change totals quickly. We spoke with a mix of device-side leaders, distributors, audiologists, and hospital procurement and program managers across APAC, EMEA, and the Americas to confirm candidacy trends, bilateral penetration, reimbursement friction points, and typical pricing movements in local currency.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 48% |

| Mid tier: 53% | Functional/Unit leaders: 33% | EMEA: 29% |

| Smaller Players: 18% | Managers: 51% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build where prevalence and diagnosis signals are translated into an addressable candidacy base, which is then filtered through access and reimbursement realities by country and major region. To keep the totals grounded, we corroborate this with selective bottom-up approximations using sampled average selling prices times estimated annual implant volumes, plus channel checks on typical mix between unilateral and bilateral procedures.

A few of the key inputs used in the model include cochlear implant candidacy and penetration by age cohort, bilateral adoption rates, procedure volumes and capacity constraints at implant centers, reimbursement coverage patterns (public and private), and processor upgrade and replacement timing that drives recurring revenue. Where direct volume indicators are thin, gaps are handled through proxy indicators like center counts, waitlist signals, and clinician feedback on throughput, and then adjusted during review.

For forecasting, scenario analysis is used because reimbursement reforms, indication expansion (including single-sided and asymmetric loss), and program funding can shift the slope more than pure time series trends. Assumptions are then stress-tested with expert views on how fast candidacy conversion and bilateral penetration can realistically move in each geography.

Data Validation & Update Cycle

Validation is done in layers so one assumption does not quietly drive the full outcome. We compare the modeled totals against independent signals such as procedure growth narratives, reimbursement changes, and the expected pace of processor refresh cycles, and then we re-check any large variances by geography before sign-off.

Outliers trigger follow-ups with interviewees or a fresh read of the underlying public data to confirm that the change is real and not a modeling artifact. The work is reviewed by more than one analyst, and key inputs are challenged for unit consistency, currency timing, and year alignment. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive an up-to-date view.

Mordor Intelligence's Cochlear Implants Market Estimate Compared With Other Published Estimates

Published market sizes for cochlear implants can look far apart even when the topic sounds identical, because the counted revenue items and the year used as the starting point are not always the same. Differences also come from how sources treat procedure-related revenue versus hardware-only revenue, and from how quickly pricing and reimbursement assumptions are refreshed.

Surgery, anesthesia, programming, and habilitation revenues sit inside Mordor Intelligence's scope, so a care pathway view can land higher than estimates that mainly count device shipments and processor hardware. On the other side, some figures stay conservative by using slower upgrade assumptions, using older currency conversions, or applying a tighter candidacy filter that does not reflect newer indications like single-sided loss.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.15 B (2026) | |

| Industry Publisher A | USD 1.96 B (2024) | Uses an earlier base year and appears to emphasize device and component revenue, with less explicit capture of surgery, programming, and habilitation value, which reduces the counted revenue pool. |

| Healthcare Publisher B | USD 2.23 B (2024) | Anchors sizing on a 2024 base and presents fitting and end-use splits, but the scope detail is less clear on whether procedure and long-term follow-up services are fully included, which can compress the total versus a full pathway view. |

The spread in the table is mainly explained by what gets counted beyond the implant system itself, plus the base-year choice and refresh timing for pricing and reimbursement. By tying assumptions to observable adoption signals like bilateral penetration and center throughput, and then re-checking with interview feedback, we keep a number that is traceable and repeatable for planning.

Key Questions Answered in the Report

What is the current value of the cochlear implants market?

The market is valued at USD 4.15 billion in 2026.

How fast is the cochlear implants market expected to grow?

It is projected to expand at 8.47% CAGR and reach USD 6.24 billion by 2031.

Which region is growing fastest for cochlear implants?

Asia-Pacific leads with a 9.32% CAGR through 2031.

Why are bilateral cochlear implants gaining momentum?

Clinical studies show better sound localization and speech-in-noise performance compared with unilateral devices.

What technological advance could reshape future market dynamics?

Fully implanted systems that eliminate external processors are in pivotal trials and are expected to disrupt current device architecture.

Page last updated on: