Personal Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

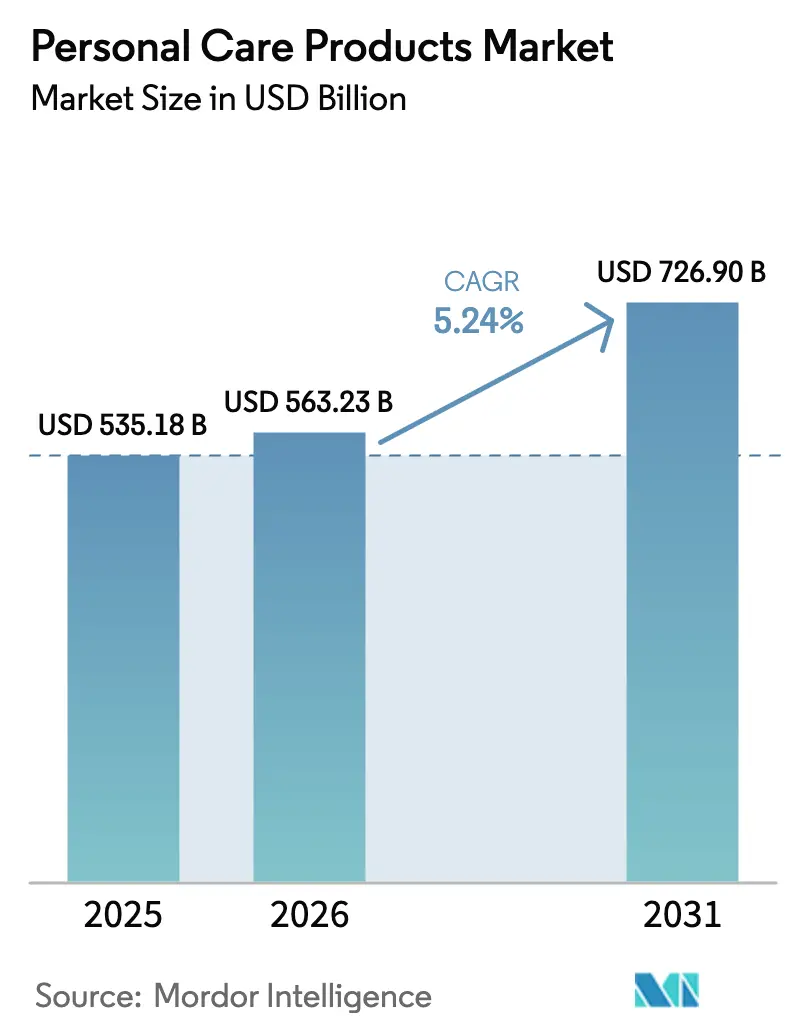

| Market Size (2026) | USD 563.23 Billion |

| Market Size (2031) | USD 726.9 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Care Products Market Analysis by Mordor Intelligence

personal care products market size in 2026 is estimated at USD 563.23 billion, growing from 2025 value of USD 535.18 billion with 2031 projections showing USD 726.9 billion, growing at 5.24% CAGR over 2026-2031. Driven by heightened wellness awareness, shifting gender norms, and a growing appetite for natural, multifunctional products, the global personal care products market is on a steady upward trajectory. Today's consumers are gravitating towards clean-label formulations, steering clear of parabens, sulfates, and synthetic fragrances. This shift has propelled brands championing organic, vegan, and dermatologically tested alternatives into the spotlight. In the Asia-Pacific region, a burgeoning middle class with increased disposable income is rapidly adopting skincare routines. Meanwhile, Western markets are witnessing a pronounced interest in minimalist and anti-aging products. Gen Z, with their emphasis on efficacy and sustainability, often gravitates towards brands that champion transparent sourcing and ethical practices, sometimes at the expense of traditional brand loyalty. Companies are harnessing biotechnology to craft active ingredients that emulate natural compounds. Simultaneously, AI is paving the way for personalized regimens and virtual try-ons. The emergence of gender-neutral and men's skincare linesalso underscores a significant cultural shift, broadening the consumer base.

Key Report Takeaways

- By product type, skin care led with 33.35% revenue share in 2025, while men’s grooming products posted the highest 7.75% CAGR through 2031.

- By category, mass products captured 61.60% of the personal care market share in 2025, whereas premium products are projected to grow at 7.31% CAGR to 2031.

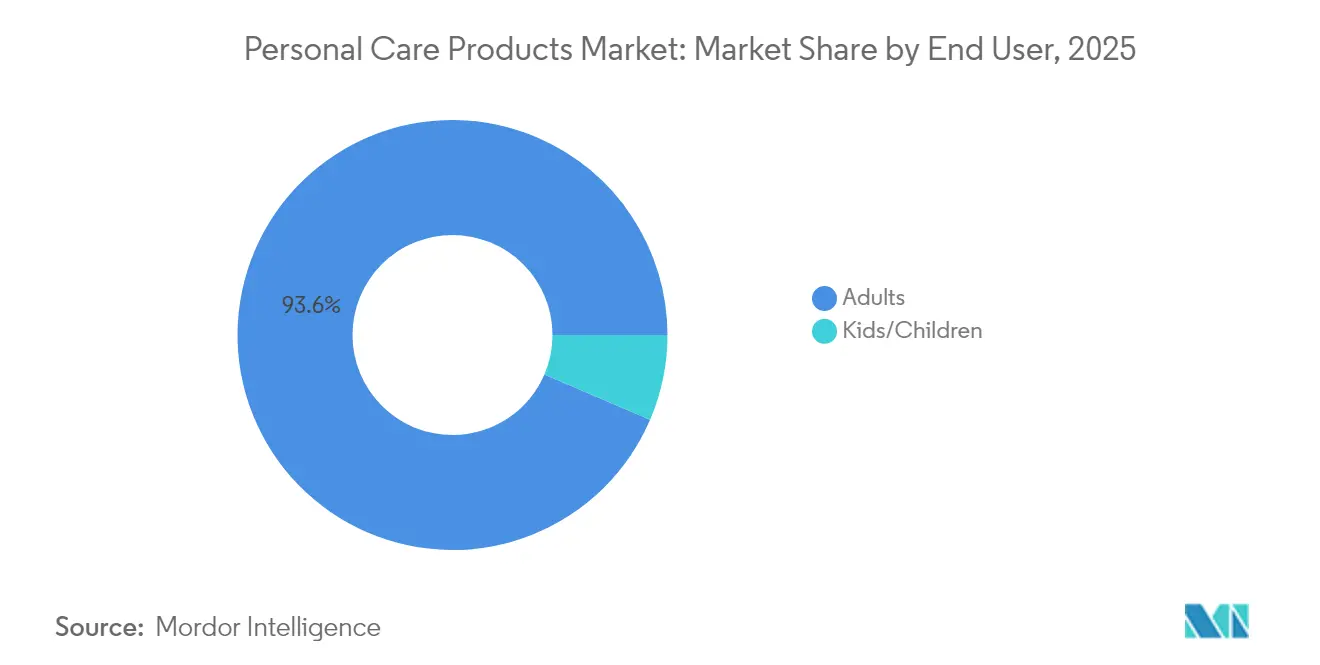

- By end user, adults dominated with a 93.55% share in 2025, the kids/children segment is set to expand at an 8.45% CAGR through 2031.

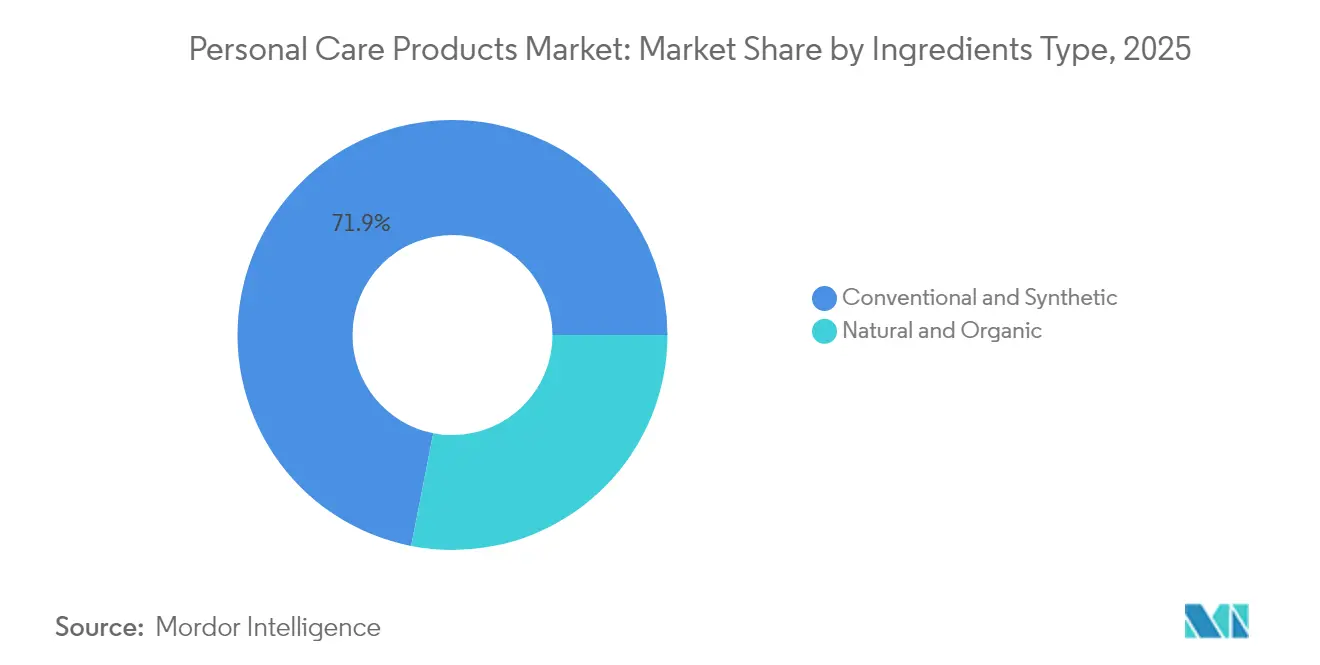

- By ingredients type, conventional and synthetic inputs held 71.92% share in 2025, while natural and organic ingredients advanced at 6.71% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets commanded 45.78% share in 2025, and online retail stores recorded a 7.76% CAGR through 2031.

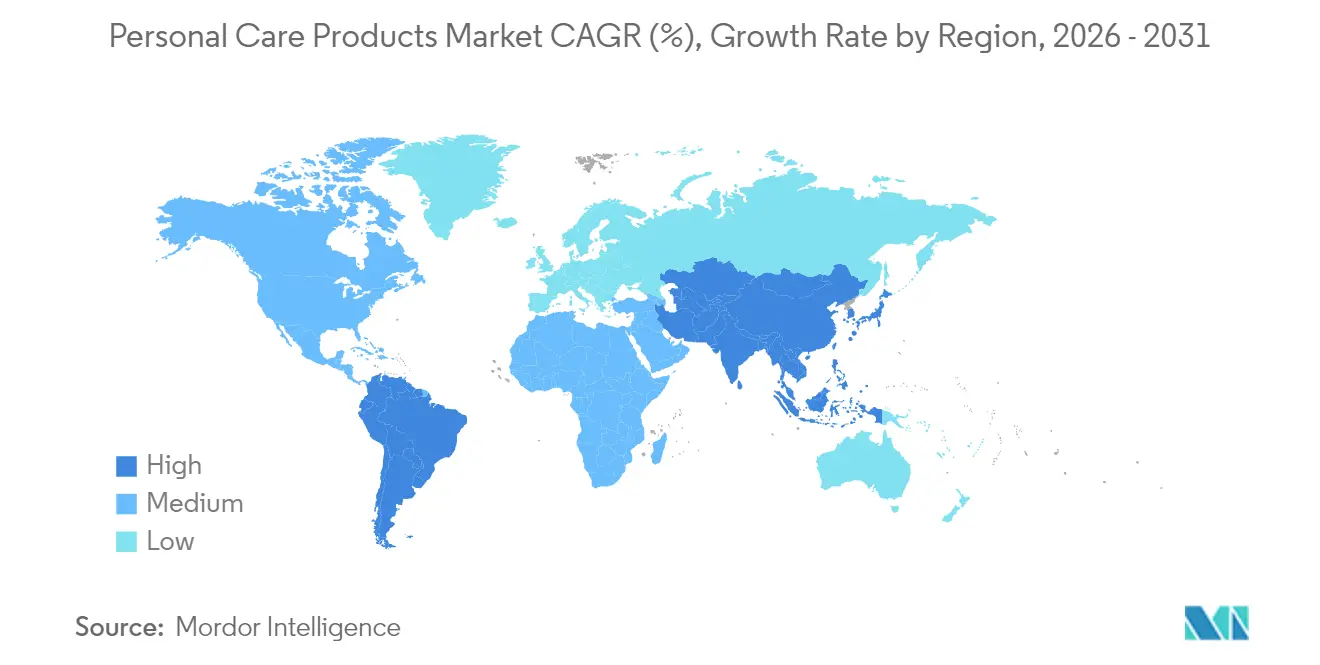

- By geography, Asia-Pacific represented a 34.12% share in 2025, and remains the fastest-growing region at 7.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural and organic product demand | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Personalized and multi-functional innovations | +0.8% | Global, led by Asia-Pacific | Long term (≥ 4 years) |

| Social media influence and brand advertising | +0.9% | Global, pronounced in emerging markets | Short term (≤ 2 years) |

| Oral hygiene awareness | +0.6% | Global, emphasis on developing markets | Medium term (2-4 years) |

| Men’s grooming expansion | +1.1% | Core Asia-Pacific, spill-over to global markets | Medium term (2-4 years) |

| Growth in premium personal care | +0.7% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Natural and organic product demand

As concerns about the health impacts of synthetic chemicals rise, consumers increasingly favor natural and organic personal care products. Many shoppers are steering clear of parabens, phthalates, and sulfates, linked to skin irritation and long-term toxicity, and are gravitating towards clean-label alternatives. A March 2025 study by NSF, a prominent global public health and safety organization, highlighted that 74% of consumers prioritize organic ingredients in personal care, underscoring the importance of formulation transparency [1]Source: NSF International, “2025 Consumer Insights Report: Organic Ingredients in Personal Care,” nsf.org. In India, brands like The Moms Co., Forest Essentials, and Plum are harnessing plant-based ingredients like aloe vera and turmeric, while Unilever’s Love Beauty and Planet tailors its global offerings to align with this trend. Ingredient transparency is now a pivotal factor in purchasing decisions, with apps like Yuka and Think Dirty enabling consumers to scrutinize formulations. In response, brands are broadening their offerings with chemical-free, vegan, and sustainable products, and are adopting blockchain technology to ensure ingredient origin and safety. This evolution is spurring innovation across skincare, haircare, and cosmetics, appealing to both ingredient-conscious and ethically-minded consumers.

Oral hygiene awareness

As consumers increasingly associate oral health with overall wellness, the personal care products market is witnessing significant growth. The World Health Organization (WHO) reported in March 2025 that oral diseases impact nearly 3.7 billion individuals worldwide [2]Source: World Health Organization, “Oral Health Factsheet (March 2025),” who.int. This statistic underscores a rising consumer emphasis on preventive care, leading to a shift from basic toothpaste to a broader range of daily-use products. Health-conscious millennials and Gen Z are driving this trend, showing heightened demand for natural and functional oral care items. These include fluoride-free and whitening toothpastes, as well as alcohol-free mouthwashes. Responding to this trend, Colgate unveiled its 'Visible White O2' oxygenated whitening range in India in 2024, tapping into the burgeoning interest in at-home aesthetic oral care. Concurrently, Hello Products broadened its U.S. offerings with vegan and charcoal-based toothpastes, aligning with the surging appetite for clean-label products. In India, direct-to-consumer brand Perfora is making waves with its subscription-based electric brushes and probiotic mouthwashes, harnessing e-commerce to enhance accessibility. These shifting consumer behaviors highlight a pronounced preference for personalized, multi-benefit solutions, bolstering the personal care market's expansion.

Men’s grooming expansion

Male grooming habits are evolving, reshaping the personal care market. This shift is fueled by changing cultural norms and a heightened awareness of skin and hair health among men. Today's consumers are embracing multi-step routines, opting for targeted skincare and hair care products that go beyond mere hygiene. In April 2024, LeBron James, in partnership with Parlux Fragrances, launched a men's grooming line. The lineup, which includes face wash, beard cream, and scalp-focused hair care, underscores the surging demand for premium, multifunctional products tailored for men. In a similar vein, The Ordinary has repositioned its products to cater to male users, emphasizing minimalist and concern-specific skincare. Indian startups, Beardo and Bombay Shaving Company, are making waves by offering comprehensive grooming kits and personalizing their offerings through direct-to-consumer platforms. Strategies like digital-first approaches, influencer-led campaigns, and YouTube tutorials have amplified male engagement. This is particularly evident among Gen Z and urban millennials, who are now more at ease with skincare, beard maintenance, and scalp care. As a result, there's a notable uptick in market growth, marked by increased purchase frequency, and a greater willingness to invest in performance-driven, lifestyle-aligned personal care solutions.

Social media influence and brand advertising

Social media is reshaping the personal care market, altering how consumers discover, assess, and buy products. Platforms such as TikTok and Instagram play pivotal roles in product education and decision-making, particularly for Gen Z, who value authenticity, ingredient transparency, and peer endorsements. In 2024, TikTok teamed up with L’Oréal, allowing in-app shopping for Garnier and Maybelline, thus streamlining the journey from product discovery to purchase. Likewise, D2C brand Dr. Squatch leveraged influencer-driven YouTube content, humor, and transparency to rapidly engage and convert male consumers. In China, beauty brand Perfect Diary has harnessed live-streaming commerce, using real-time audience engagement and influencer credibility to drive significant sales. Additionally, a 2024 survey from the University of Portsmouth revealed that 60% of consumers placed trust in influencer endorsements, with nearly half of all purchasing decisions swayed by these recommendations [3]Source: University of Portsmouth, “Influencer Credibility and Consumer Trust Survey 2024,” port.ac.uk. In the United States, brands like Glow Recipe and Rare Beauty have capitalized on this trend, achieving viral success through “get ready with me” segments and ingredient-focused tutorials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit products | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Growing concerns over product safety and ingredients | -0.6% | Global, strongest in developed markets | Medium term (2-4 years) |

| Intense market competition and price pressure | -0.9% | Global, severe in mature markets | Long term (≥ 4 years) |

| High manufacturing costs and raw material expenses | -1.1% | Global, impact higher on smaller manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit products

Counterfeit personal care products are increasingly infiltrating digital channels, posing a significant threat to consumer trust and stunting the growth of legitimate brands. E-commerce platforms, along with small, unregulated beauty outlets, have emerged as primary hubs for distributing fake skincare and cosmetics. These outlets often lure consumers with heavily discounted prices, making it challenging to distinguish between authentic and counterfeit products. A stark reminder of this issue came in July 2023, when U.S. Customs and Border Protection (CBP) seized counterfeit pharmaceutical and personal care goods, highlighting violations worth over USD 102.3 million. In 2024, the discovery of counterfeit anti-aging creams in Allentown, Pennsylvania, not only raised public health alarms but also dented confidence in online shopping. Such counterfeit products can harbor harmful or unregulated ingredients, leading to adverse reactions and diminishing consumer openness to new brands. Furthermore, established companies grapple with reputational damage when consumers inadvertently associate fakes with their labels, jeopardizing repeat purchases and long-term loyalty.

Intense market competition and price pressure

The personal care market is experiencing intensified competition and squeezed profit margins. Even industry giants are feeling the pinch. Procter & Gamble, despite boasting above-average profitability, saw its revenue dip by 2.07% in Q1 2025. This decline underscores the challenges posed by market saturation and pricing pressures in mature sectors, which are upending traditional growth trajectories. Meanwhile, nimble D2C brands, harnessing the power of social media and e-commerce, have shaken up the market. In response, legacy firms are ramping up their digital advertising budgets and revamping distribution methods to stay in the game At the same time, retailers such as Whole Foods and Natural Grocers are pushing private label products. These offerings, championing clean ingredients and ethical sourcing, are resonating with both value-seeking and health-conscious consumers, posing a direct challenge to premium national brands. This blend of competitive pressures from pricing and innovation speed to sustainability and digital outreach is stretching brand operational budgets. As a result, maintaining profitability and scaling becomes increasingly challenging, especially in commoditized sectors like haircare, skincare, and hygiene.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skincare Dominance Drives Premium Innovation

In 2025, skin care commands a dominant 33.35% market share, highlighting a pronounced consumer pivot towards preventive and anti-aging solutions, transcending mere cleansing. This leadership position is bolstered by heightened awareness of long-term skin health and the prevalent use of effective actives, including peptides, retinoids, and botanical extracts, known for their clinically validated outcomes. The trend underscores a burgeoning appetite for multifunctional products that tackle issues like dullness, pigmentation, and early aging signs. Brands such as L'Oréal and Estée Lauder are riding this wave, melding dermatological science into their premium lines and broadening reach with hybrid mass-premium offerings.

Men’s grooming emerges as the fastest-growing segment, eyeing a robust CAGR of 7.75% through 2031. This surge is driven by evolving masculinity perceptions and a heightened focus on personal appearance, especially in urban locales. Hair care thrives on innovations, championing sulfate-free and tailored formulations. Oral care, buoyed by strong brand leadership, sees a surge in consumer emphasis on preventive health. Bath and shower products are being rebranded under wellness and premium self-care themes. Sun care and deodorants are adapting, infusing multifunctional and natural ingredients. Fragrances continue to flourish, especially in culturally rich regions like the Middle East. Noteworthy strategic moves, like L’Oréal’s stake in Galderma and its takeover of Color Wow, spotlight global players' efforts to diversify and tap into burgeoning niches within the personal care arena.

By Category: Premium Segment Accelerates Despite Mass Market Dominance

In 2025, the mass market segment dominates the personal care industry, capturing 61.60% of the market share. This dominance is largely attributed to extensive distribution through supermarkets and competitive pricing strategies. Retail giants like Walmart and Target play pivotal roles in bolstering this segment's reach. Meanwhile, private-label products from Whole Foods and Natural Grocers, which emphasize clean-label and ethical standards, are intensifying competition against established legacy brands. In response to inflationary pressures and a rising preference for direct-to-consumer (D2C) channels, mass market players are innovating to retain their cost-conscious clientele. A notable example is Dove's 2024 launch of refillable body wash pouches, a move that underscores both sustainability and affordability.

While the premium segment commands a smaller 38.40% market share, it's the fastest-growing, boasting a 7.31% CAGR. This growth is driven by consumers placing greater emphasis on product efficacy, natural ingredients, and sustainable sourcing. Brands like Tula and Drunk Elephant are leveraging digital skin diagnostics and augmented reality consultations to tailor routines, thereby justifying their premium pricing. These premium brands enjoy elevated margins, which they reinvest into eco-friendly packaging, research and development, and ethically sourced ingredients. The surge of influencer-led campaigns, coupled with the ascent of luxury D2C brands, has amplified consumer interest.

By End User: Adult Dominance Contrasts with Children’s Segment Acceleration

In 2025, adults command a dominant 93.55% share of the personal care market, a testament to their purchasing power and established routines. Their demand spans from daily hygiene essentials to specialized anti-aging and grooming products. With higher disposable incomes, adults not only gravitate towards premium products but also cultivate long-term brand loyalty. For instance, L’Oréal’s Revitalift line holds consistent popularity among adults seeking dermatologist-approved anti-aging solutions.

Kids/children's products are emerging as the market's fastest-growing segment, boasting an 8.45% CAGR projected through 2031. This surge is largely attributed to heightened parental awareness regarding the importance of gentle, specialized formulations for their kids. Colgate-Palmolive exemplifies this trend, having broadened its kids' toothpaste range to include fluoride-free options. They've also launched oral health initiatives in schools, championing the cause of early hygiene habits. Furthermore, generational shifts, especially from Gen Z, are reshaping the market landscape. Brands such as Youth To The People and Bubble are reaping the rewards, having resonated with Gen Z's values through clean ingredients and compelling social media narratives.

By Ingredients Type: Conventional Products Lead While Natural Alternatives Gain Momentum

In 2025, conventional and synthetic ingredients command a dominant 71.92% market share, thanks to their proven efficacy, cost-effectiveness, and broad regulatory compliance. Ingredients such as silicones and synthetic fragrances deliver consistent performance across diverse climates and shelf-life expectations, making them the go-to choice for mass-market formulations. Major brands, including Dove (Unilever) and Olay (Procter & Gamble), lean on these ingredients in their flagship products, ensuring they remain both affordable and effective.

Natural and organic ingredients, with a robust 6.71% CAGR, are on the rise, driven by consumer apprehensions over health risks tied to synthetic compounds like parabens, phthalates, and formaldehyde releasers. Plant-derived alternatives like sugarcane-sourced squalane, bakuchiol as a retinol stand-in, and aloe vera-based humectants are increasingly supplanting petrochemical inputs, thanks to their milder profiles and enhanced skin benefits. In a nod to this trend, L’Oréal is making headlines with its pledge to incorporate 95% bio-based or circular ingredients by 2030. While certifications like COSMOS and USDA Organic are on the rise, the challenge of verifying supply chains and ensuring ethical sourcing remains a complex and costly endeavor.

By Distribution Channel: Traditional Retail Dominates While Digital Channels Accelerate

In 2025, supermarkets and hypermarkets dominated the market with a 45.78% share, thanks to their wide range of products, affordability, and easy accessibility. Major retail chains, including Big Bazaar, Reliance Smart, and Walmart, prominently feature brands like Dove, Lifebuoy, Pond’s, and Clinic Plus, all under the Hindustan Unilever umbrella. These brands boost their visibility through end-aisle displays, value packs, and combo offers. Such strategic partnerships enhance penetration, particularly in mass-market segments of Tier 2 and Tier 3 cities. Furthermore, Hindustan Unilever capitalizes on these retail formats to promote new product trials, employing bundling and sampling tactics.

Online retail has emerged as the fastest-growing channel, boasting a 7.76% CAGR. Trends like personalization, influencer marketing, and the allure of niche and premium products fuel this growth. E-commerce giants, including Nykaa, Amazon Beauty, and Tmall Global, have become platforms for brands like The Ordinary, Minimalist, and Forest Essentials, helping them expand through targeted content and direct-to-consumer strategies. Brands that started online, such as Mamaearth and Plum, are leveraging augmented reality and influencer-led tutorials to turn awareness into sales, all while ensuring convenience with same-day delivery and hassle-free returns.

Geography Analysis

In 2025, the Asia-Pacific region commands a dominant 34.12% share of the personal care market, buoyed by its youthful demographics, swift urbanization, and escalating disposable incomes. China spearheads the global demand for men's grooming, while in India, the burgeoning middle class, championed by digitally-savvy brands like WOW Skin Science, is driving growth. WOW Skin Science, with its direct-to-consumer approach, is particularly resonating with Gen Z. Meanwhile, Southeast Asian nations, notably Indonesia and Vietnam, are emerging as hotspots, spurred by rising internet access and a thirst for affordable yet premium products. With rapid digital advancements, a cultural penchant for grooming, and a swelling middle class, the region is on track to grow at an impressive 7.49% CAGR through 2031.

Europe and North America, both mature markets, exhibit steadier yet slower growth. Europe leads the charge in advocating for natural and organic products. Nations such as Germany and France prioritize premium, eco-certified formulations and spearhead innovations in sustainable packaging, driven by increasing consumer demand for environmentally friendly and health-conscious products. Meanwhile, North America, led by the United States, emerges as a dominant force in the personal care sector, highlighted by its significant per-capita spending and a strong focus on advanced product formulations and technological advancements in the industry.

Meanwhile, South America, the Middle East, and Africa are carving out their niches in the evolving landscape. The Middle East, with its deep-rooted cultural affinity for fragrances, sees nations like Saudi Arabia and the UAE driving a robust demand for premium perfumes and grooming essentials. South America, led by the dynamic markets of Brazil and Mexico, adeptly balances its domestic consumption with its strategic position as a manufacturing hub. To stay pertinent, brands across both regions are doubling down on ingredient transparency, harnessing AI for skincare diagnostics, and adopting omnichannel strategies.

Competitive Landscape

The personal care products market is moderately fragmented, allowing both legacy leaders and agile disruptors to vie for market share. Procter & Gamble, Unilever, and L'Oréal, the dominant players, employ distinct marketing strategies: P&G emphasizes brand superiority and category leadership through enhanced product performance. At the same time, Unilever focuses on premiumization in emerging markets, driven by purpose-oriented branding. L'Oréal harnesses emotional storytelling and influencer campaigns to resonate with Gen Z and Millennials. Companies like Glossier and Mamaearth sidestep traditional retail by fostering community and offering personalized content, engaging consumers directly on digital platforms.

Technology adoption is pivotal in defining competitive edges. L'Oréal distinguishes itself with cutting-edge innovation labs and collaborations, notably its AI partnership with IBM and the pioneering of bioprinted skin for expedited and safer product testing. Unilever harnesses data analytics and predictive modeling to enhance its supply chain and meet sustainability targets. P&G utilizes IoT-enabled packaging and smart shelf systems to gauge consumer behavior in retail settings. Brands increasingly employ AR-driven try-ons and skin diagnostic apps, seamlessly merging online and offline experiences to boost conversion rates.

Market leaders are strategically broadening their global presence and product ranges through acquisitions, partnerships, and scaling manufacturing. L'Oréal’s acquisition of Color Wow and its investment in Galderma underscore its dedication to expanding in both the dermatological and haircare realms. Yellow Wood Partners' acquisition of ChapStick aims to bolster its position in the lip care market. Eternis’s takeover of Sharon Personal Care not only broadens its ingredient capabilities but also extends its global reach.

Personal Care Products Industry Leaders

Procter & Gamble Co.

Unilever PLC

Colgate-Palmolive Company

Este Lauder Companies Inc.

L'Oreal S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: L’Oréal signed an agreement to acquire haircare brand color wow, expanding its professional and consumer portfolios

- January 2025: L'Oréal partnered with IBM to develop sustainable cosmetic formulations using generative artificial intelligence (AI). The company utilized IBM's GenAI technology to analyze cosmetic formulation data, enabling the incorporation of sustainable raw materials while reducing energy consumption and material waste.

- December 2024: Tatcha increased its market presence in the United States through distribution in more than 1,400 ulta beauty retail locations and its e-commerce platform, with primary emphasis on its dewy skin cream product.

- December 2024: Eternis Fine Chemicals purchased Sharon personal care, expanding manufacturing across Italy and Israel.

Global Personal Care Products Market Report Scope

| Hair Care | Shampoo |

| Conditioner | |

| Hair Colorant | |

| Hair Styling Products | |

| Others | |

| Skin Care | Facial Care Products |

| Body Care Products | |

| Lip and Nail Care Products | |

| Bath and Shower | Shower Gels |

| Soap | |

| Others | |

| Oral Care | Toothbrush |

| Toothpaste | |

| Mouthwash and Rinses | |

| Others | |

| Men's Grooming Products | |

| Sun Care Products | |

| Deodorants and Antiperspirants | |

| Perfumes and Fragrances |

| Mass |

| Premium |

| Adults |

| Kids/Children |

| Natural and Organic |

| Conventional and Synthetic |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colorant | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gels | |

| Soap | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwash and Rinses | ||

| Others | ||

| Men's Grooming Products | ||

| Sun Care Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Category | Mass | |

| Premium | ||

| End User | Adults | |

| Kids/Children | ||

| Ingredients Type | Natural and Organic | |

| Conventional and Synthetic | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Personal Care market size and its growth outlook to 2031?

The market is valued at USD 563.23 billion in 2026 and is projected to reach USD 726.9 billion by 2031, advancing at a 5.24% CAGR.

Which region is expanding fastest in the Personal Care market and why?

Asia-Pacific leads with a 7.49% CAGR through 2031, propelled by rising male-grooming adoption in China and growing middle-class spending in India.

How is premiumization influencing the Personal Care market growth?

Premium products, though accounting for 38.40% of 2025 revenue, are growing at 7.31% CAGR as consumers prioritize efficacy, sustainability, and luxury experiences.

Which product segment shows the highest growth within the Personal Care industry?

Men’s grooming products register the strongest 7.75% CAGR, reflecting evolving masculinity norms and targeted digital marketing in Asia-Pacific.

Page last updated on: