Asset Performance Management (APM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 22.34 Billion |

| Market Size (2031) | USD 42.26 Billion |

| Growth Rate (2026 - 2031) | 13.59% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

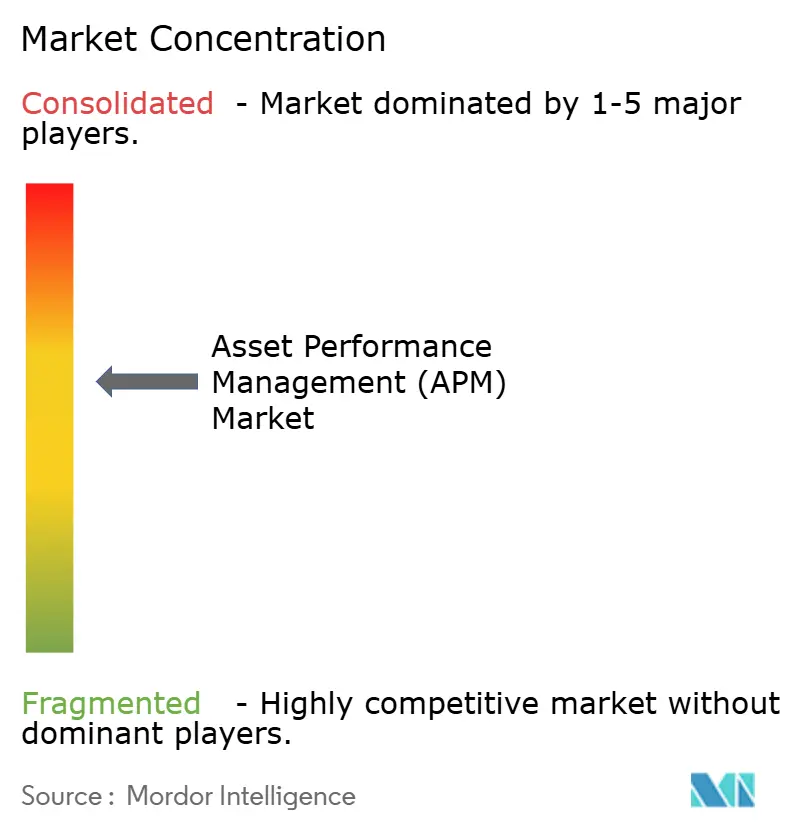

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asset Performance Management (APM) Market Analysis by Mordor Intelligence

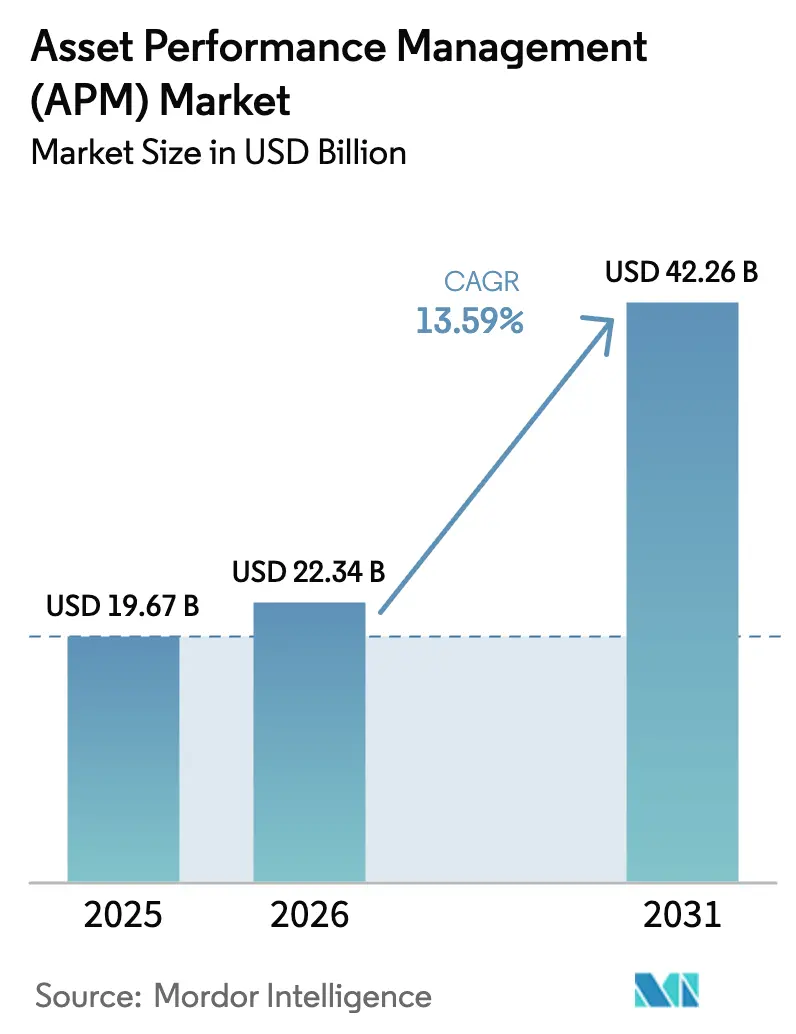

The Asset Performance Management market size is expected to grow from USD 19.67 billion in 2025 to USD 22.34 billion in 2026 and is forecast to reach USD 42.26 billion by 2031 at 13.59% CAGR over 2026-2031. Demand accelerates as organizations link predictive analytics with industrial IoT to curb unplanned downtime, improve safety, and cut maintenance budgets. Cloud-native platforms widen access for small and medium enterprises while hybrid architectures satisfy data sovereignty and cybersecurity mandates. Prescriptive analytics expands quickly because AI engines now recommend specific maintenance actions that lift overall equipment effectiveness. Competitive focus shifts from basic condition monitoring toward embedded digital twins, autonomous workflows, and integrated ESG reporting. Technology partnerships and domain-specific solutions reshape vendor strategies, particularly in fast-growing Asia-Pacific, where industrial digitalization is surging.

Key Report Takeaways

- By component, software captured 58.64% of the Asset Performance Management market share in 2025, whereas services are forecast to post the fastest 14.97% CAGR through 2031.

- By type, predictive asset management led with 59.85% revenue share in 2025; prescriptive analytics is projected to advance at a 18.63% CAGR to 2031.

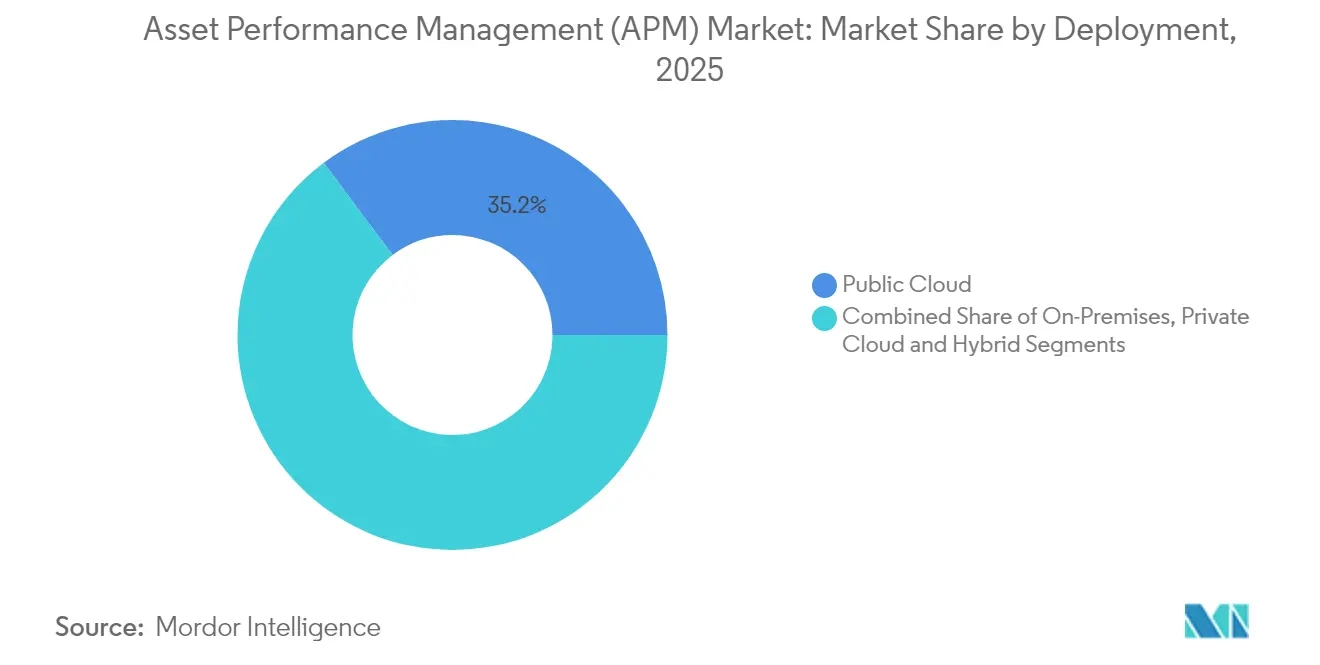

- By deployment model, public cloud accounted for 35.22% of the Asset Performance Management market size in 2025, while hybrid cloud is set to climb at a 21.85% CAGR between 2026 and 2031.

- By end-user industry, oil and gas held a 22.35% share of the Asset Performance Management market size in 2025; chemicals and pharmaceuticals will expand at a 14.62% CAGR through 2031.

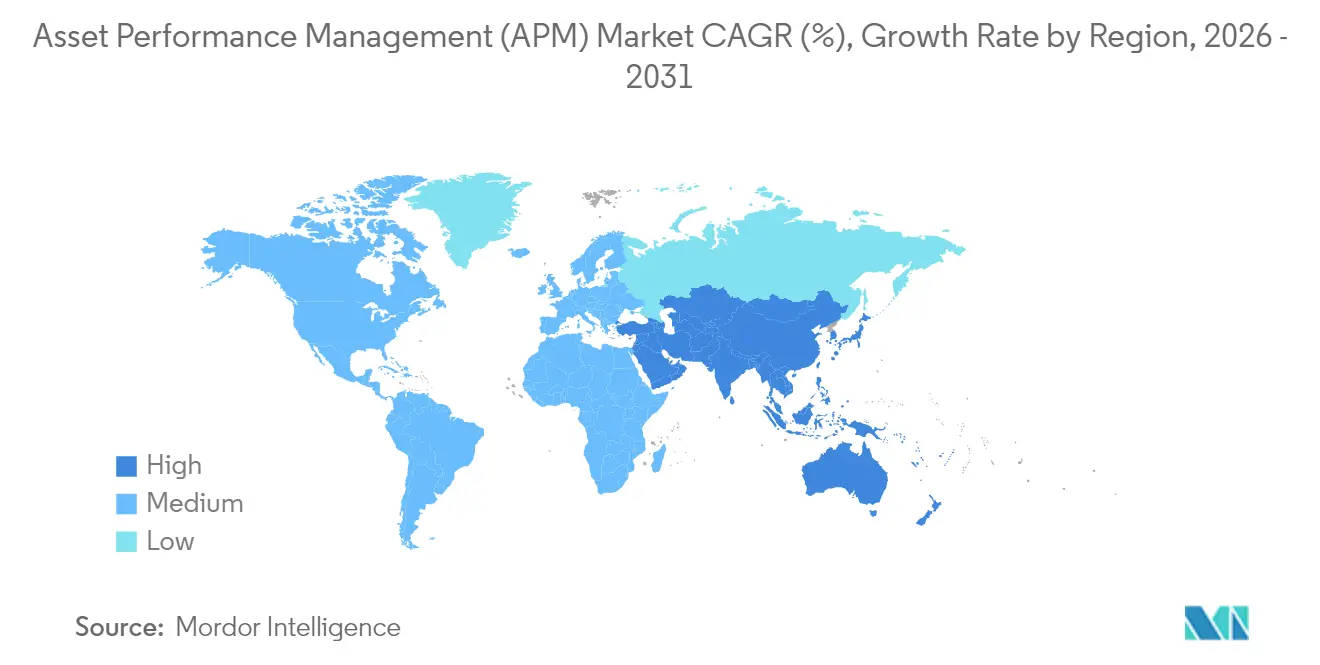

- By geography, North America led with a 32.58% share in 2025, whereas Asia-Pacific is advancing at a 13.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Asset Performance Management (APM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0-linked APM adoption | +2.8% | Germany, Japan, South Korea | Medium term (2-4 years) |

| Surge in demand for predictive maintenance | +3.2% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| Cloud-native APM uptake by SMEs | +2.1% | Core APAC, expanding to Latin America | Medium term (2-4 years) |

| AI-enabled physics-based digital twins | +2.5% | Global, concentrated in process industries | Long term (≥ 4 years) |

| ESG-driven asset-health investments | +1.9% | EU leadership, North America following | Long term (≥ 4 years) |

| Insurance incentives for real-time analytics | +1.4% | North America, expanding to developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Industry 4.0-linked APM adoption

Enterprises integrate APM within broader Industry 4.0 architectures to synchronize predictive maintenance with real-time production analytics. Automotive plants in Germany trimmed unplanned downtime by 25% after connecting APM and MES platforms. Japanese electronics factories recorded a 15% upturn in overall equipment effectiveness from similar convergence. Falling IIoT sensor prices and maturing edge compute hardware accelerate rollouts, while ISO 55000 guidelines reinforce disciplined asset-lifecycle governance across global supply chains. Vendors now bundle APM with quality management and supply-chain visibility modules, allowing management teams to optimize throughput and asset health in a single pane.

Surge in demand for predictive maintenance

Predictive maintenance transitioned from a cost-cutting tactic to a critical reliability strategy. Energy majors applying AI-based models achieved 40% downtime elimination and 30% maintenance cost savings[1]Plant Services, “Oil and Gas Supermajor Uses AI Predictive Analytics to Improve Efficiency and Safety,” plantservices.com. One oil supermajor saved USD 10 million annually after hitting 75% failure-prediction accuracy nine days ahead of incidents. The United States predictive maintenance segment is forecast to rise from USD 3.6 billion in 2024 to USD 15.2 billion by 2029 at a 32.8% CAGR. Vibration analytics dominates mechanical asset monitoring, while machine-learning algorithms refine anomaly detection across compressors, turbines, and rolling stock.

Cloud-native APM uptake by SMEs

Small and medium manufacturers embrace cloud APM to bypass capital-heavy on-premises deployments. Subscription models remove hardware upkeep and patching burdens, letting teams focus on process improvements. Manufacturing SMEs leveraging cloud recorded quick productivity bumps, supported by scalable IoT data ingestion and template-driven analytics[2]T-Systems, “Manufacturing SMEs and the Cloud,” t-systems.com. Enhanced cloud security frameworks and regional data centers alleviate privacy concerns, encouraging adoption in Asia and Latin America, where budgets remain tight. SaaS vendors pair low-code dashboards with preset machine-learning models so non-technical staff can act on alerts without deep data-science skills.

AI-enabled physics-based digital twins

Digital twin adoption grows as platforms merge real-time telemetry with physics simulations to forecast asset behavior under stress. Hydropower operators cut unscheduled downtime by 20% using turbine digital twins that simulate fluid dynamics. Chemical plants applying twin models on centrifugal pumps achieved 15% maintenance cost reduction through optimized service intervals. Combining data-driven and physics-based approaches elevates model accuracy, especially for complex rotating equipment where pure statistical methods struggle. Continuous calibration with edge analytics keeps twins aligned with actual wear patterns, improving prescriptive guidance on replacement parts and operating set points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and privacy risks | –2.3% | Global, acute in regulated sectors | Short term (≤ 2 years) |

| High integration cost with legacy OT | –1.8% | Mature industrial markets with legacy infrastructure | Medium term (2-4 years) |

| Scarcity of asset-data scientists | –1.5% | Global, pronounced in emerging markets | Long term (≥ 4 years) |

| AI-liability regulatory ambiguity | –1.2% | EU and North America, emerging globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-security and privacy risks

Connecting operational technology to enterprise networks exposes critical assets to cyberattacks. The expected USD 36.6 billion IoT cybersecurity market illustrates rising spend to mitigate this threat. Manufacturers fear loss of proprietary process data and potential production shutdowns. Regulatory gaps complicate cross-border data flows, especially in the energy and chemical sectors that intersect national security. Hybrid deployments with edge-first processing and cloud burst capacity offer a compromise, reducing cloud exposure while retaining advanced analytics. Vendors incorporate zero-trust frameworks and encryption-at-rest mandates to retain customer confidence.

High integration cost with legacy OT

Decades-old control systems require protocol converters, retrofitted sensors, and extensive validation before joining modern APM stacks. Integration outlays can double initial budgets, particularly in process plants governed by strict safety certifications[3]FasterCapital, “How Asset Management Supports Regulatory Compliance,” fastercapital.com . Skilled engineers fluent in both OT and AI remain scarce, elongating project timelines. However, documented case studies report 3× return on investment within five months once systems stabilize, supported by lower overtime, spare-parts spend, and failure-related environmental penalties. This payoff encourages phased rollouts, beginning with critical assets that yield rapid benefits before expanding plant-wide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Consolidation Centers on Software

Software applications accounted for 58.64% of the Asset Performance Management market in 2025, reflecting enterprise demand for integrated analytics rather than isolated monitoring tools. Services registered the swiftest 14.97% CAGR because companies need data-science expertise, change-management support, and continuous optimization to unlock full platform value. Historical investment patterns show an accelerating shift toward SaaS delivery that reduces deployment time and ongoing support overhead.

Professional services cover data pipeline construction, algorithm tuning, and ISO 55000 documentation, while managed services handle 24/7 analytics and system health checks. Vendor success hinges on packaged accelerators that lower integration hurdles and predefined AI models that speed value realization. As clients scale from pilot to enterprise rollout, recurring service revenue stabilizes earnings for vendors and ensures continuous improvement for customers.

By Type: Prescriptive Analytics Becomes the Growth Engine

Predictive asset management retained a 59.85% share of the Asset Performance Management market in 2025, yet prescriptive analytics is on course for a 18.63% CAGR through 2031. Predictive models flag impending failures, whereas prescriptive engines recommend specific operational or maintenance actions, creating higher business impact.

Oil and gas operators using prescriptive algorithms extended engine overhaul cycles by 20% and cut maintenance budgets by 25%, translating to three-month paybacks. Asset strategy management modules integrate cost, risk, and performance variables, guiding capital replacement decisions that balance short-term OPEX and long-term CAPEX. Regulatory bodies in hazardous-process industries increasingly view prescriptive maintenance as best practice for preventing safety incidents, embedding it into audit protocols.

By Deployment Model: Hybrid Architectures Gain Ground

Public cloud represented a 35.22% share of the Asset Performance Management market in 2025, delivering elasticity and low upfront cost. Hybrid cloud is expected to climb 21.85% CAGR as firms combine on-premises data sovereignty with cloud analytics scale. GE Vernova already processes over 1 million daily analytics actions across 1,000-plus power plants via cloud monitors.

Private cloud installations persist in defense, nuclear, and pharmaceutical settings where compliance requires dedicated infrastructure. Edge computing nodes now execute first-level analytics near machines, minimizing latency for safety-critical responses while funneling summary insights to centralized models. Technology roadmaps emphasize modular architectures so that workloads can fluidly migrate among edge, core, and cloud based on security policy and cost considerations.

By End-user Enterprise Size: SMEs Accelerate Through SaaS

Large enterprises dominate absolute spending due to sprawling asset fleets, yet SMEs register the fastest take-up thanks to cloud delivery that removes hardware ownership and specialized staffing barriers. SaaS subscriptions allow monthly budgeting aligned with production cycles, appealing to midsize plants with thin margins.

SME adoption often begins with vibration monitoring on a few bottleneck machines and expands to plant-wide digital twins as savings accumulate. Vendors pre-package templates for common equipment classes and deliver mobile apps for frontline maintenance crews, removing the need for advanced analytics teams. ISO 55000 guidelines are filtering down supply chains, pushing SMEs to formalize asset governance to retain contracts with multinational customers.

Geography Analysis

North America commanded 32.58% of the Asset Performance Management market in 2025, buoyed by mature infrastructure, strict OSHA and EPA mandates, and deep collaboration between industrial operators and software leaders. U.S. predictive maintenance spending alone is projected to quadruple by 2029, reinforcing the region’s innovation leadership. Canadian utilities scale AI-based APM to extend equipment lifespans and postpone costly capital projects, contributing additional momentum.

Asia-Pacific posts the fastest 13.74% CAGR as governments promote Industry 4.0 roadmaps and manufacturers modernize to stay competitive. China’s process industries deploy digital twins for energy efficiency, while Japan’s aging asset base triggers predictive maintenance investments to maintain uptime without extensive capital outlays. India’s Asset Performance Management market should climb from USD 66.7 million in 2022 to USD 213 million by 2032 as public-sector steel and rail operators digitize maintenance. Cross-border alliances like AssetWatch-Mitsui speed technology transfer and localization.

Europe advances steadily on the back of stringent ESG frameworks and advanced engineering sectors. Automotive and chemical plants integrate APM with carbon-tracking dashboards to align asset reliability with emissions goals. The forthcoming Corporate Sustainability Reporting Directive encourages enterprises to document maintenance-linked energy savings, spurring demand for platforms that merge performance analytics with sustainability metrics. Uptake in Central and Eastern Europe accelerates as multinationals retrofit acquired plants with standardized digital maintenance stacks.

Competitive Landscape

Competitive intensity is moderate, with diversified industrial software giants and focused AI specialists sharing the Asset Performance Management market. GE Vernova, IBM, Siemens, and ABB leverage broad hardware, software, and service portfolios to secure multi-year enterprise agreements[4]Verdantix, “Leaders in Asset Performance Management Solutions,” verdantix.com . Their advantage lies in installed sensor networks and decades of process know-how that underpin robust anomaly libraries.

Emerging players such as UptimeAI, AssetWatch, and MaxGrip position around cloud-native architectures and pretrained AI models that deploy within weeks. These challengers often partner with system integrators to reach regulated industries. Differentiation turns on depth of domain content, integration ease with existing OT systems, and transparent ROI dashboards that resonate with finance teams.

Strategic mergers and funding rounds shape market evolution. Siemens acquired an Altair division to blend simulation and real-time analytics, while Baker Hughes bought ARMS Reliability to deepen energy-sector offerings. Yokogawa’s investment in UptimeAI illustrates incumbent appetite for best-of-breed AI. Vendors also stress open API ecosystems to embed APM outputs into ERP, CMMS, and risk-management suites, enabling enterprise-wide decision support.

Asset Performance Management (APM) Industry Leaders

ABB Ltd.

AVEVA Group plc

IBM Corporation

SAP SE

GE Digital

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Yokogawa Electric and UptimeAI formed a strategic partnership to combine AI engines with domain libraries for oil, gas, and renewable plants.

- January 2025: Schneider Electric partnered with MaxGrip to add lifecycle services that address maintenance losses valued at USD 864 billion annually.

- January 2025: AssetWatch received USD 1.9 million from Oxygea Ventures within a USD 40 million Series B to enhance cloud-based condition monitoring.

- January 2025: AssetWatch and Mitsui Knowledge Industry partnered to deliver predictive maintenance solutions across Japanese manufacturing sites.

- November 2024: Siemens reported USD 75.9 billion in revenue and announced plans to strengthen APM through the Altair acquisition.

Global Asset Performance Management (APM) Market Report Scope

Asset performance management (APM) solutions enable organizations to monitor assets continuously to identify, diagnose, and prioritize impending equipment problems in real-time, with the primary goal to help them maximize profitability by balancing cost, risk, and performance of the assets, plant, or of the people that are operating all those things. Overall, APM solutions provide unique value to modern industrial operations.

The study considers various segments, including type, deployment, end-user vertical, and geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments. Besides, the study encompasses a detailed analysis of the drivers, restraints, and opportunities of the asset performance management market, along with the analysis of COVID-19 impact, regulatory landscape, as well as trends impacting customers' investment sentiments in these technologies.

| Software |

| Services |

| Predictive Asset Management |

| Asset Reliability Management |

| Asset Strategy Management |

| Prescriptive Asset Management |

| On-premises |

| Public cloud |

| Private cloud |

| Hybrid |

| Large Enterprises |

| SMEs |

| Oil and Gas |

| Metals and Mining |

| Manufacturing |

| Energy and Utilities |

| Transportation and Logistics |

| Government and Public Sector |

| Chemicals and Pharmaceuticals |

| Other Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Software | ||

| Services | |||

| By Type | Predictive Asset Management | ||

| Asset Reliability Management | |||

| Asset Strategy Management | |||

| Prescriptive Asset Management | |||

| By Deployment Model | On-premises | ||

| Public cloud | |||

| Private cloud | |||

| Hybrid | |||

| By End-user Enterprise Size | Large Enterprises | ||

| SMEs | |||

| By End-user Vertical | Oil and Gas | ||

| Metals and Mining | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Transportation and Logistics | |||

| Government and Public Sector | |||

| Chemicals and Pharmaceuticals | |||

| Other Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the Asset Performance Management market?

What is the current value of the Asset Performance Management market?

Which segment is expanding fastest within Asset Performance Management?

Prescriptive analytics posts the quickest 18.63% CAGR as enterprises move beyond failure prediction toward autonomous decision guidance.

Why are hybrid cloud models gaining ground in Asset Performance Management deployments?

Hybrid architectures balance data-sovereignty and cybersecurity needs with the scalability of public cloud analytics, driving a 21.85% CAGR through 2031.

How does Asset Performance Management support ESG goals?

By minimizing unplanned outages and optimizing asset lifecycles, platforms reduce energy waste and emissions, aligning maintenance programs with sustainability targets.

Which region leads spend on Asset Performance Management solutions?

North America currently leads with 32.58% share, yet Asia-Pacific is the fastest-growing region due to aggressive industrial digitalization initiatives.

Page last updated on: