Customer Engagement Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

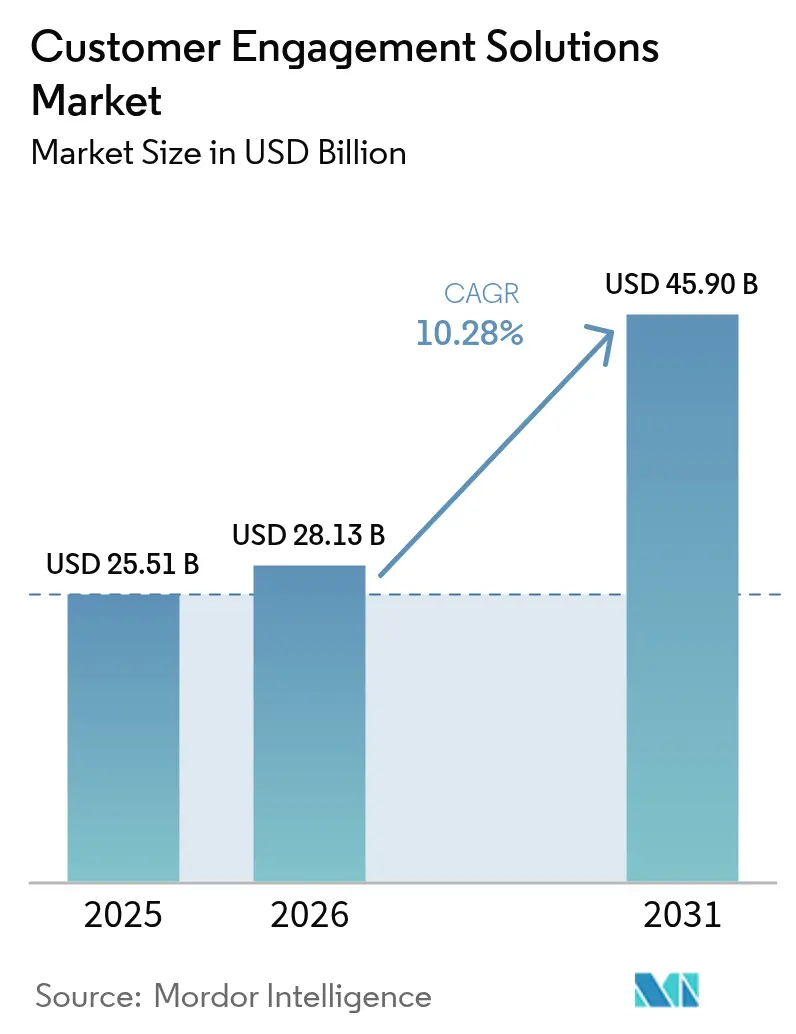

| Market Size (2026) | USD 28.13 Billion |

| Market Size (2031) | USD 45.9 Billion |

| Growth Rate (2026 - 2031) | 10.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Customer Engagement Solutions Market Analysis by Mordor Intelligence

customer engagement solutions market size in 2026 is estimated at USD 28.13 billion, growing from 2025 value of USD 25.51 billion with 2031 projections showing USD 45.9 billion, growing at 10.28% CAGR over 2026-2031. Rapid enterprise migration to cloud contact-center platforms, rising adoption of agentic AI, and the omnichannel customer-experience (CX) imperative are the primary accelerants. Mid-sized companies are closing capability gaps by leveraging low-code generative-AI toolsets, while large enterprises consolidate after-sales tasks into unified customer-facing teams to improve lifetime value. Macro conditions also favor vendors that blend automation with human empathy, as 86% of consumers now acknowledge AI’s role in resolving issues quickly[1]Verint Systems, “2025 State of Digital Customer Experience,” verint.com. Competitive intensity continues to rise because contact-center specialists, CRM platforms, and AI-first start-ups all aim to own the last mile of customer relationships.

Key Report Takeaways

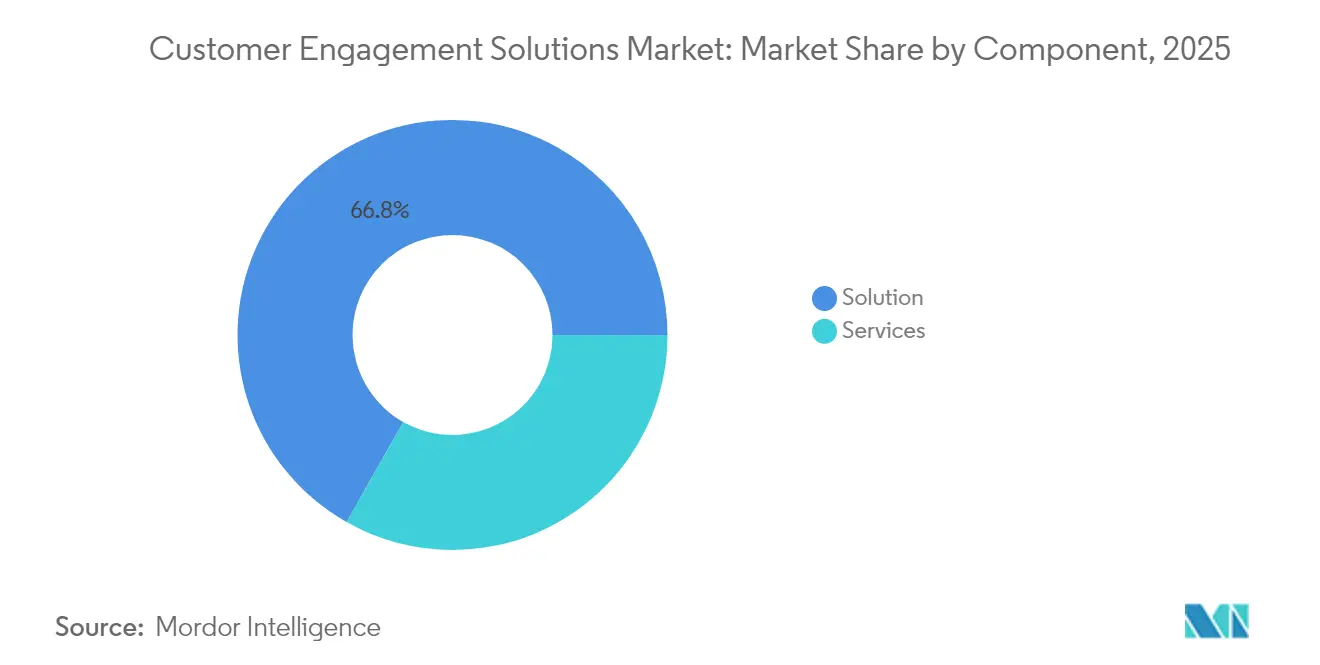

- By component, solutions accounted for a 66.80% customer engagement solutions market share in 2025, whereas the services segment is advancing at an 11.62% CAGR through 2031.

- By deployment, on-premise models held 69.90% of the customer engagement solutions market size in 2025, while cloud deployments are projected to grow at a 12.28% CAGR.

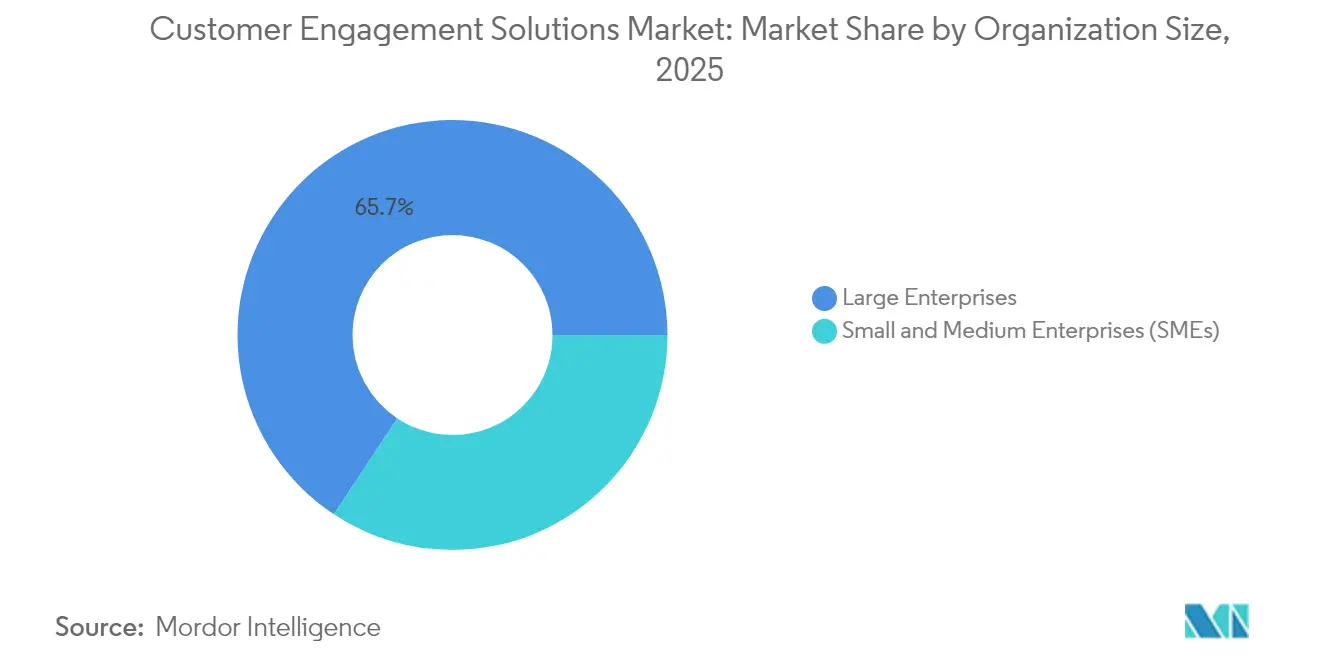

- By organization size, large enterprises captured 65.70% of revenue in 2025; small and medium enterprises are set to expand at an 11.88% CAGR.

- By end-user industry, IT and telecom led with 28.10% revenue share in 2025; media and entertainment is the fastest-growing vertical at a 10.49% CAGR through 2031.

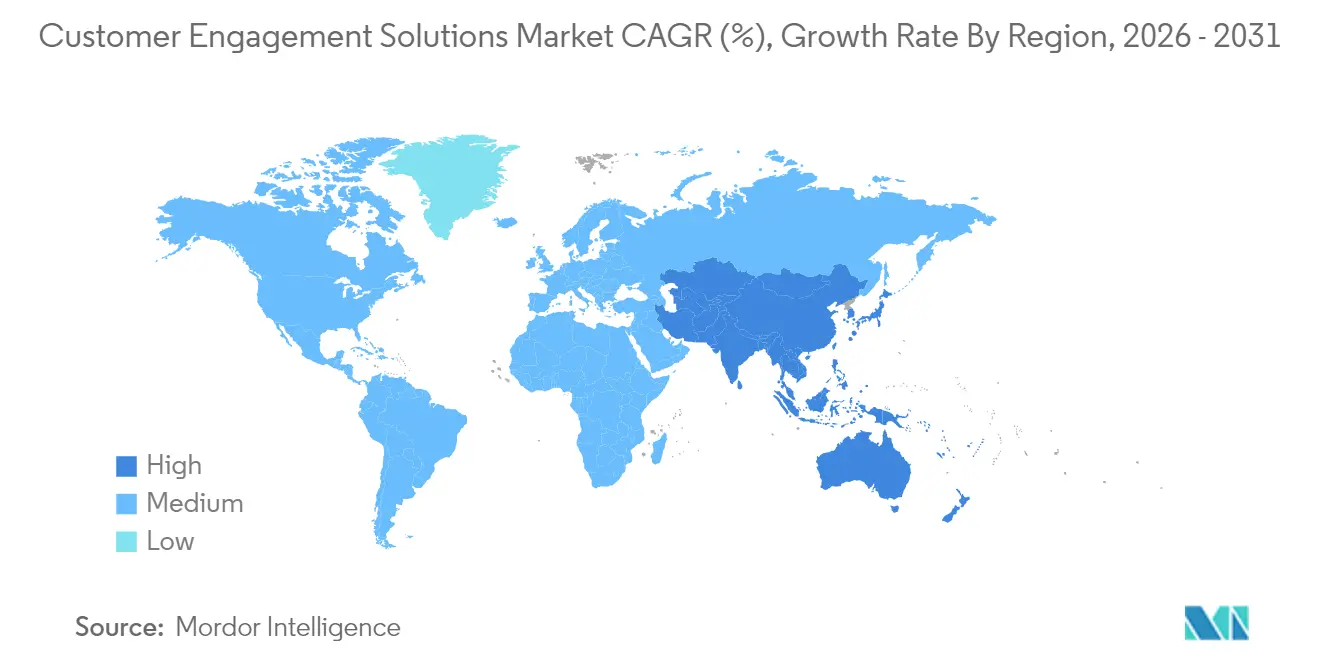

- By geography, North America commanded 40.90% of 2025 revenue, whereas Asia–Pacific is forecast to grow at an 11.17% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Customer Engagement Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-based contact-center adoption surge | +2.8% | Global, with North America & Europe leading | Medium term (2-4 years) |

| Omnichannel CX imperative across industries | +2.1% | Global, strongest in APAC and North America | Short term (≤ 2 years) |

| AI-driven hyper-personalization and analytics | +2.5% | Global, with APAC early adoption advantage | Medium term (2-4 years) |

| Distributed workforce accelerating digital service | +1.9% | Global, particularly North America & Europe | Short term (≤ 2 years) |

| Agentic-AI bots autonomously resolving inquiries | +2.2% | Global, with enterprise-first deployment | Long term (≥ 4 years) |

| Accessibility-first compliance mandates | +1.1% | North America & EU regulatory focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-based Contact-center Adoption Surge

Commercial cloud migration now serves as a structural pivot for CX operations rather than a cost-reduction exercise. 80.4% of enterprises report that cloud contact centers help future-proof technology infrastructures[2]Debbie McGrath, “Contact Centers Go Cloud to Future-Proof CX,” NTT, global.ntt. The architecture delivers elastic scale for globally distributed workforces and integrates natively with AI engines that automate call transcription and sentiment analysis. Less than 40% of businesses have moved unified communications to the cloud, leaving a deep runway for growth. Adoption is strongest among organizations that must quickly spin up seasonal capacity or navigate multi-site operations. Migration complexity, especially for firms with legacy PBX investments, is spawning a robust ecosystem of managed-services providers that orchestrate phased cutovers while ensuring business continuity.

Omnichannel CX Imperative Across Industries

Customer journeys now stretch across messaging apps, live chat, social media, and voice, prompting 87% of users to demand seamless hand-offs between channels. True omnichannel delivery goes beyond simply adding digital touchpoints; it relies on a unified data fabric that preserves interaction context. Brands that remove data silos report higher agent productivity because staff can instantly retrieve prior conversations without toggling interfaces. Voice remains relevant for emotionally charged or high-value transactions, but messaging and asynchronous video gain favor for routine inquiries. Leaders deploy single-agent desktop environments that blend digital and voice routing within one queue, thereby aligning KPIs around customer effort rather than channel utilization.

AI-driven Hyper-personalization and Analytics

Hyper-personalization now leverages behavioral telemetry and real-time intent data instead of static demographic profiles. In Asia–Pacific, 60% of enterprises apply region-specific large-language-model (LLM) variants to tailor promotions in local dialects. Predictive engines simulate journeys through digital twins, allowing teams to test offers before launch and to re-sequence content flows dynamically. Consumers reward such individualization—38% switch brands after impersonal outreach. Operationalizing hyper-personalization, however, demands a privacy-by-design data layer, federated governance, and AI observability tooling that surfaces drift in model outputs. Organizations are therefore creating specialized stewardship roles to balance regulatory compliance with algorithmic experimentation.

Distributed Workforce Accelerating Digital Service

Hybrid work remains entrenched: only 21% of employees report being actively engaged, leading to USD 438 billion in lost productivity that cascades into customer outcomes. Firms counter attrition by deploying AI assistants that guide new agents during live calls, automatically surface knowledge articles, and flag compliance risks when scripts go off-track. Cloud-native workforce-engagement-management suites embed gamification features to motivate dispersed teams and offer real-time performance analytics to supervisors. The distributed model also diversifies talent pipelines by enabling recruitment in lower-cost regions, but it raises cybersecurity stakes, which accelerates investment in zero-trust contact-center architectures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cybersecurity concerns | -1.8% | Global, with EU GDPR and US state regulations | Short term (≤ 2 years) |

| Legacy system integration complexity | -1.5% | Global, particularly large enterprises | Medium term (2-4 years) |

| Generative-AI hallucination brand-risk | -0.9% | Global, with regulated industries most affected | Short term (≤ 2 years) |

| Talent gap in CX-AI governance and ethics | -1.2% | Global, with developed markets facing acute shortages | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and Cybersecurity Concerns

A majority 68% of consumers express anxiety over how brands handle their personal information. Global regulators are responding with stringent rules covering biometric data, call recording, and automated decision-making. Contact-center AI deployments that monitor emotion or track location can trigger legal action if consent workflows are weak, as illustrated by recent U.S. lawsuits involving unauthorized monitoring. Enterprises now prioritize encryption at rest, tokenization of sensitive fields, and “explainable AI” dashboards that document the logic behind automated recommendations. Vendors offering differential-privacy tooling and data-residency controls gain a competitive edge because they de-risk compliance without sacrificing personalization fidelity.

Legacy System Integration Complexity

Many large organizations still rely on proprietary PBX infrastructures and heavily customized CRM stacks that complicate AI rollout. Integration work often consumes more budget than the core software licence because it demands mapping business rules, cleansing decades-old data, and retraining staff on new workflows. Project overruns are common when voice platforms follow different security models than cloud CRMs, resulting in duplicated identity stores and inconsistent authentication regimes. Implementation partners that specialize in bridging Session Initiation Protocol (SIP) trunks with cloud APIs are therefore in high demand. Firms that underestimate the cultural shift required to embrace AI-augmented processes risk falling behind more agile competitors that design greenfield stacks from scratch.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Solution Dominance

Solutions maintained 66.80% of 2025 revenue thanks to robust demand for omnichannel routing engines, conversational bots, and speech analytics modules that underpin modern CX strategy. The services arm, however, is growing faster at an 11.62% CAGR as enterprises lean on external specialists for migration, model-tuning, and governance. Advisory teams help phase out redundant IVR scripts, create persona-based dialog flows, and set up continuous-learning loops so AI agents improve after each interaction. Managed-services contracts increasingly bundle proactive performance monitoring to spot latency spikes that impair voice quality. Professional-services engagements also emphasize change-management programs that coach frontline supervisors on interpreting real-time coaching dashboards. This consultative focus indicates that differentiation in the customer engagement solutions market now tilts toward execution excellence rather than feature checklists.

A parallel investment narrative emerges in managed security for CX stacks, encompassing endpoint hardening, penetration testing, and compliance audits mapped to ISO 27001 controls. Vendors that combine platform IP with mature service desks capture longer annuity streams because clients prefer one throat to choke when outages occur. As more enterprises adopt agentic AI, demand escalates for prompt-engineering workshops and hallucination-mitigation frameworks. Collectively, these trends place services at the center of value creation, cementing their double-digit growth trajectory inside the broader customer engagement solutions market.

By Deployment Type: Cloud Momentum Challenges On-premise Incumbency

Although on-premise deployments still account for 69.90% of the customer engagement solutions market size, the growth engine is squarely in the cloud, which is expanding at a 12.28% CAGR. Hybrid calling services ease the transition by interconnecting legacy time-division-multiplexing trunks with WebRTC endpoints, allowing agents to work from home without compromising voice clarity. The economics also favor consumption-based pricing models that let companies flex capacity during peak shopping periods. Security objections are steadily receding as hyperscalers adopt zero-trust blueprints and provide granular key-management options that align with industry mandates such as PCI-DSS.

Large enterprises often pilot individual business units on the cloud before executing a full rip-and-replace program. Small and medium enterprises, by contrast, jump straight to multitenant architectures because they have fewer legacy baggage. Industry regulators now certify cloud contact-center providers for advanced use cases like real-time mortgage servicing or tele-health triage, further accelerating migration. As a result, vendor roadmaps prioritize API-first design, ensuring seamless integration between contact-center as a service (CCaaS) and workflow platforms. The momentum suggests that cloud will command a decisive lead in incremental bookings within the customer engagement solutions market by the end of the decade.

By Organization Size: SME Growth Outpaces Enterprise Stability

Large enterprises captured 65.70% of 2025 revenue through multi-region deployments that interlace voice, social, and messaging queues under a unified orchestration layer. They continue to invest in workforce-engagement analytics to optimize schedules across thousands of agents. Yet the growth spotlight is on small and medium enterprises, which are expanding at an 11.88% CAGR. Low-code generative-AI builders let SMEs create sophisticated FAQ chatbots without hiring data scientists, flattening historical capability divides. Cloud billing schemes with no minimum-seat commitments further democratize access, allowing a boutique retailer to pay only for minutes consumed during seasonal promotions.

SME buying behavior is also distinct: decision cycles are shorter, proof-of-concepts conclude within weeks, and success metrics revolve around rapid payback rather than enterprise-wide standardization. Vendors therefore package SKU bundles that combine voice, chat, and basic sentiment analysis at a single per-user rate. Partner ecosystems play a pivotal role because SMEs often rely on value-added resellers for IT guidance. Over time, cross-sell motions into marketing-automation modules and loyalty-program tools will raise average revenue per account, underscoring the strategic significance of the SME segment in the customer engagement solutions market.

By End-user Industry: IT and Telecom Leadership Faces Media Disruption

IT and telecom providers held 28.10% of spending in 2025 by virtue of their early cloud adoption and complex subscriber-management needs. They deploy large-scale speech analytics to detect churn intent and route high-risk callers to retention teams in real time. Media and entertainment, meanwhile, is growing fastest at a 10.49% CAGR; streaming platforms and gaming studios adopt AI-moderated community forums and interactive live-chat features that elevate engagement during launch events. Financial-services institutions also allocate sizable budgets to AI-driven fraud detection and personalized advisory tools, spurred by competitive pressures from digital-only banks.

Healthcare organizations embrace HIPAA-compliant conversational bots for appointment scheduling and claims triage, thereby easing call-center congestion. Retailers integrate generative-AI engines with recommendation systems to push hyper-personalized promotions through mobile apps. Each vertical imposes unique compliance regimes, from voice recording retention in finance to accessibility mandates in public services. Solution providers thus increasingly offer industry pre-sets—complete with domain-specific language models—to accelerate deployment timelines. These dynamics diversify the revenue mix and help cushion the customer engagement solutions market against cyclical shocks in any single sector.

Geography Analysis

North America retained its lead at 40.90% of 2025 revenue because enterprises in the United States and Canada possess mature cloud infrastructures and sizable AI budgets. The region is a launchpad for agentic AI pilots that autonomously handle password resets and subscription changes without human escalation. Cloud migration also accelerated after multiple state privacy laws introduced stiff penalties for data breaches, nudging firms toward standardized, certified environments. Large financial services firms in New York deploy multimodal AI assistants that interpret voice stress levels to trigger fraud alerts, reflecting advanced use-case maturity. Canadian telcos pioneer 5G-enabled video-chat support, while Mexican manufacturers implement multilingual chatbots to serve cross-border customers.

Asia–Pacific is the fastest-growing region, posting an 11.17% CAGR through 2031. The conversational-AI submarket alone is expanding 24.1% annually as mobile-first consumers demand round-the-clock support across messaging super-apps. China’s e-commerce giants operate AI-rich live-stream shopping shows that blend entertainment with instant purchasing, driving volumes that reshape global CX expectations. Singapore’s Monetary Authority offers regulatory sandboxes that de-risk AI experimentation in banking, while India’s start-up ecosystem supplies high-quality developers at competitive rates. Combined, these factors create a fertile environment for the rapid adoption of the customer engagement solutions market.

Europe follows a measured trajectory shaped by GDPR and emerging AI-ethics legislation. Firms prioritize privacy-preserving architectures that keep inference data within regional borders, spurring demand for on-premise or sovereign-cloud deployments. Germany leverages customer engagement platforms to support Industry 4.0 after-sales service, United Kingdom fintechs refine real-time KYC verification in chat flows, and France’s luxury houses deliver concierge-style messaging to high-spend clients. Southern and Eastern Europe show a growing appetite as EU recovery funds earmark digital modernization. South America and the Middle East and Africa remain nascent but promising; Brazil’s fintech boom and GCC smart-city projects position both regions to leapfrog legacy voice-centric models by adopting cloud-native platforms from day one. Widespread 4G and rising smartphone penetration underpin the next demand wave for the customer engagement solutions market.

Competitive Landscape

The customer engagement solutions market features moderate fragmentation, with tier-one cloud contact-center specialists, CRM mega-vendors, and AI-only entrants all vying for wallet share. Consolidation is accelerating: Salesforce has added unstructured-data processing (Zoomin) and retail-specific CX modules (PredictSpring) to its stack, while Five9 crossed USD 1 billion in annual revenue and absorbed Acqueon for proactive omnichannel orchestration. Buyers increasingly favor end-to-end platforms that offer routing, analytics, and workforce management through a single pane of glass because this reduces integration overhead.

Beyond product breadth, implementation prowess is now a core differentiator. Up to 75% of firms risk project failure when they attempt DIY AI deployment without skilled partners. This shortfall fuels a services arms race: platform vendors launch certified-consultant programs and invest in post-go-live optimization teams that refine models continuously. Verticalization also gains momentum; vendors ship pre-trained intents for healthcare or utilities to shorten time-to-value. Augmented reality and metaverse labs explore immersive CX scenarios, although commercial traction remains embryonic.

Pricing pressure persists as open-source LLMs lower barriers to entry. Incumbents counter by embedding governance toolkits that monitor bias, drift, and hallucinations, thereby appealing to regulated industries. Partnerships likewise intensify: ServiceNow and Genesys integrated their clouds to furnish a 360-degree view of every customer journey stage[3]Michael Pace, “ServiceNow and Genesys Unite Around AI-First Service,” Genesys, genesys.com. Looking ahead, out-of-the-box agentic AI, privacy-enhancing computation, and cross-domain orchestration will dictate leadership within the customer engagement solutions market.

Customer Engagement Solutions Industry Leaders

Avaya Inc.

Alvaria, Inc.

Calabrio Inc.

Genesys

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Five9 launched Agentic CX with AI agents capable of reasoning and autonomous resolution, adding smart self-service across digital and voice channels.

- May 2025: Press Ganey Forsta acquired InMoment to expand AI-driven experience analytics for healthcare and financial-services clients.

- May 2025: Capillary Technologies purchased Kognitiv to scale omnichannel loyalty solutions in North America.

- May 2025: IgniteTech bought Khoros, augmenting community management and social-engagement features with new AI capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global customer engagement solutions market as all integrated software and associated managed or professional services that orchestrate real-time, omnichannel interaction, automate workflows, analyze experience data, and support agent productivity across web, mobile, social, voice, and in-app touchpoints. The assessment includes cloud and on-premise deployments that are licensed on subscription or perpetual terms to enterprises of every size.

Scope exclusion: stand-alone CRM modules or digital marketing tools that lack multi-channel engagement and agent-assistance features are not counted.

Segmentation Overview

- By Component

- Solution

- Omni-channel Platforms

- Workforce Engagement Management

- Robotic Process Automation

- Self-Service and Chatbots

- Services

- Managed Services

- Professional Services

- Solution

- By Deployment Type

- On-premise

- Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-user Industry

- BFSI

- IT and Telecom

- Retail and Consumer Goods

- Media and Entertainment

- Healthcare

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with solution architects, IT buyers, and customer-service leaders across North America, Europe, Asia-Pacific, and the Gulf clarified license fee bands, seat expansion intentions, and feature adoption timelines, allowing us to verify secondary estimates and adjust regional penetration curves.

Desk Research

We began by mapping demand signals through public sources such as International Telecommunication Union internet-user files, the United States Census Bureau's e-commerce retail indicators, Eurostat digital economy statistics, and filings housed on the U.S. SEC EDGAR system. Analyst teams also screened trade associations, for example, the Contact Center Association of America, and credible technology journals for pricing moves, cloud migration rates, and customer-experience benchmarks.

To enrich those insights, we tapped paid repositories that Mordor subscribes to, including D&B Hoovers for vendor revenue splits and Dow Jones Factiva for acquisition and partnership news that hints at seat additions. This mix anchors historic baselines while revealing competitive pricing corridors. The sources listed here are illustrative; many others supported data collection and cross-checks.

Market-Sizing & Forecasting

A top-down reconstruction starts from enterprise software outlays reported by national statistics offices, which are then filtered by the share allocated to contact-center and customer-experience stacks. Results are corroborated with selective bottom-up roll-ups, sampled average selling price multiplied by probable seat volumes for leading vendors, to reconcile gaps. Key variables driving the model include cloud contact-center seat density, internet penetration growth, agent employment counts, average subscription price erosion, regulatory customer-data mandates, and AI-enabled feature uptake. Multivariate regression ties these indicators to past market values, and scenario analysis extends them to 2030 after expert consensus vetting.

Data Validation & Update Cycle

Outputs pass two-step peer review, variance screens, and anomaly flags against independent signals before sign-off. Mordor refreshes every twelve months, with interim adjustments when material events, such as sizable M&A or regulatory shifts, occur.

Why Our Customer Engagement Solutions Baseline Commands Reliability

Published estimates often differ because each firm selects unique product mixes, price corridors, and refresh cadences.

Key gap drivers include narrower scope that drops services revenue, optimistic seat-price trajectories, or infrequent data updates that miss mid-cycle cloud migrations. By maintaining yearly refreshes, validating assumptions with buyers, and blending top-down spend pools with supplier checks, Mordor Intelligence provides a balanced, repeatable baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.51 B | Mordor Intelligence | - |

| USD 29.39 B | Global Consultancy A | Excludes services discounting, assumes uniform 6-seat expansion per license |

| USD 24.36 B | Industry Association B | Uses historic five-year average ASP, overlooks regional cloud price erosion |

| USD 23.52 B | Trade Journal C | Forecast updated biennially; omits SME adoption in Asia-Pacific |

In sum, the disciplined scope choices, frequent refresh cycle, and dual-layer validation mean decision-makers can rely on Mordor's figures as the most transparent and actionable starting point for strategy.

Key Questions Answered in the Report

What is the customer engagement solutions market size in 2026?

It stands at USD 28.13 billion and is projected to reach USD 45.9 billion by 2031.

Which component segment is growing fastest?

Services are expanding at an 11.62% CAGR because enterprises need expert support for cloud migration, AI tuning, and governance.

Why are SMEs adopting customer engagement platforms quickly?

Low-code generative-AI tools and consumption-based cloud pricing remove traditional cost and skill barriers, driving an 11.88% CAGR among SMEs.

Which region is the main growth engine?

Asia-Pacific leads with an 11.17% CAGR thanks to mobile-first consumer behavior and supportive government AI initiatives.

How are privacy regulations influencing solution design?

Vendors integrate encryption, tokenization, and explainable-AI dashboards to comply with GDPR and similar laws, mitigating a −1.8% drag on forecast CAGR.

What competitive moves are reshaping the market?

Large acquisitions such as Five9’s purchase of Acqueon and Braze’s deal for OfferFit signal a race to offer end-to-end AI-rich engagement platforms.

Page last updated on: