Packaging Foams Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.76 Billion |

| Market Size (2031) | USD 15.87 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Foams Market Analysis by Mordor Intelligence

The Packaging Foams Market size was valued at USD 12.22 billion in 2025 and estimated to grow from USD 12.76 billion in 2026 to reach USD 15.87 billion by 2031, at a CAGR of 4.45% during the forecast period (2026-2031). Growth is rooted in rising e-commerce shipping volumes, corporate lightweighting strategies, and stricter environmental mandates that accelerate material substitution toward recyclable and bio-based foams. Asia-Pacific drives both demand and innovation thanks to surging food-delivery services and expanded vaccine cold-chain logistics, while North America and Europe emphasize advanced formulations that comply with evolving chemical regulations. Raw-material volatility, notably styrene and isocyanate price swings, remains a persistent cost challenge that spurs manufacturers to diversify feedstocks and pursue vertical integration. At the same time, merger activity—such as Novolex’s purchase of Pactiv Evergreen—signals a maturing competitive landscape where scale economies and circular-economy capabilities determine strategic advantage.

Key Report Takeaways

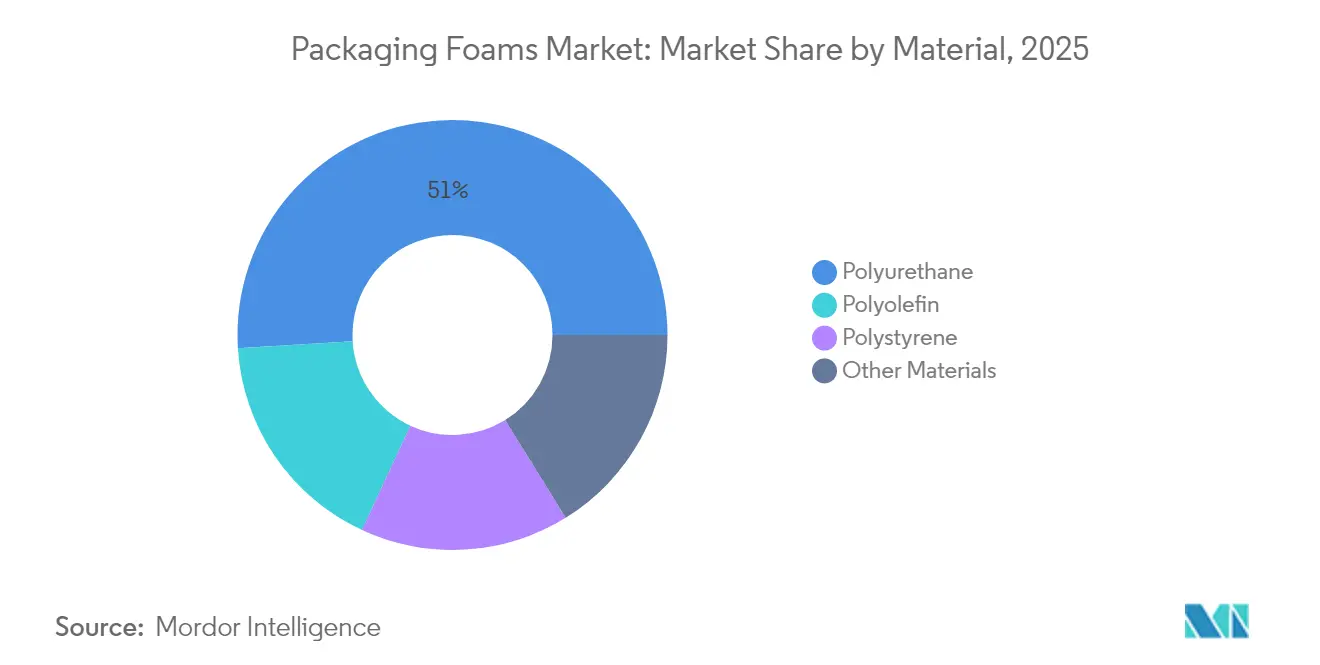

- By material, polyurethane led with 50.98% revenue share in 2025, while polyolefin recorded the highest projected CAGR at 5.43% through 2031.

- By structure, flexible foam captured 60.25% of the packaging foam market share in 2025 and is advancing at a 4.74% CAGR through 2031.

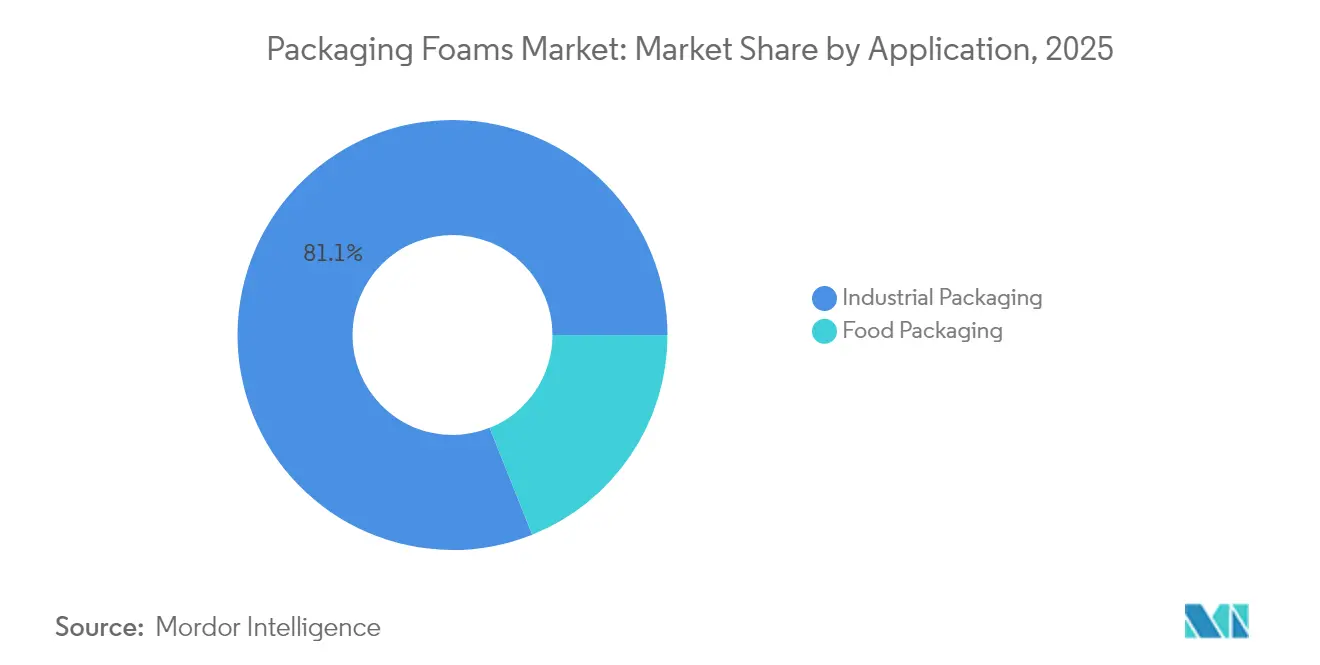

- By application, industrial packaging accounted for 81.05% share of the packaging foam market size in 2025, whereas food packaging is projected to expand at 5.31% CAGR between 2026-2031.

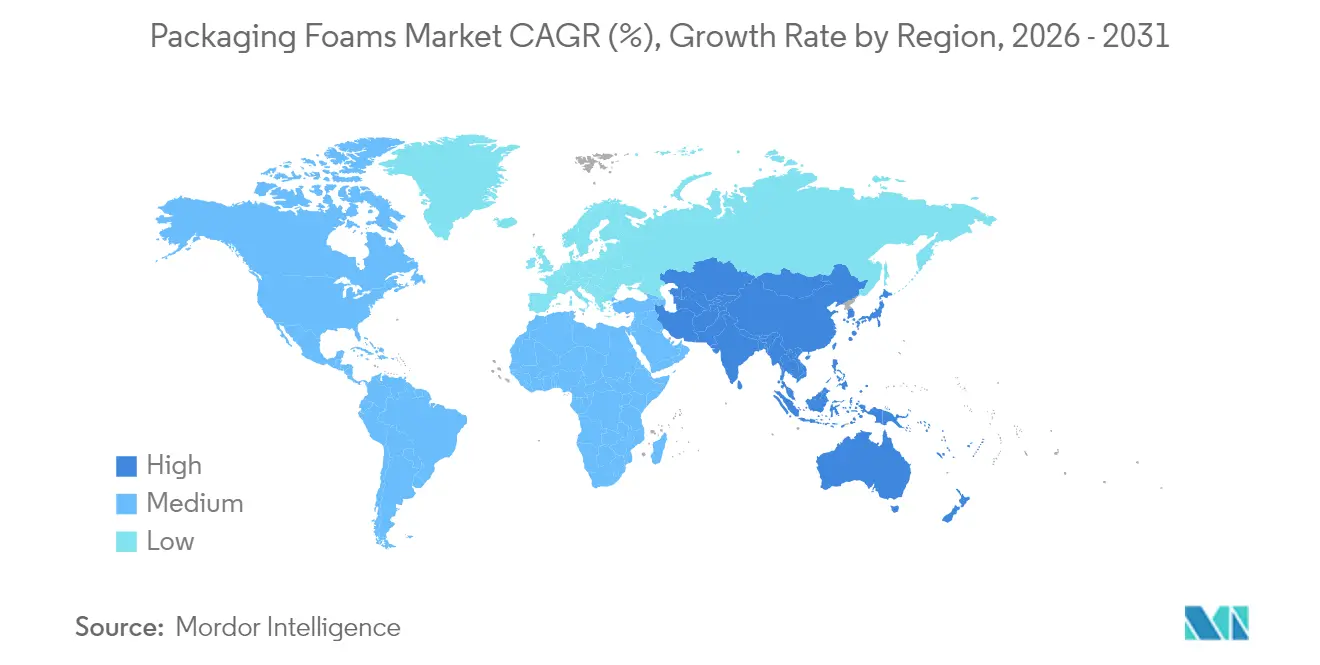

- By geography, Asia-Pacific commanded 40.10% share in 2025 and is forecast to grow at 5.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Packaging Foams Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce led demand for protective shipping foam | +1.20% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| 24-hour food-delivery boom in Asia requiring insulated foam packs | +0.80% | Asia-Pacific core, spill-over to emerging markets | Short term (≤ 2 years) |

| Logistics lightweighting initiatives to cut freight costs | +0.70% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Rapid adoption of bio-based polyols for low-carbon foams | +0.60% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Cold-chain vaccine infrastructure build-out in emerging markets | +0.50% | Africa, Latin America, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Led Demand for Protective Shipping Foam

Automated fulfillment networks handle rising parcel volumes that frequently contain fragile electronics and personal-care items. Operators replace plastic air pillows with engineered foam inserts that absorb shock, resist compression, and meet recycling targets. Dimensional-weight pricing by parcel carriers incentivizes thinner, lightweight cushions that cut freight charges while protecting products. Machine-learning design platforms generate right-sized foam interiors and deliver up to 25% transport savings for shippers. Electronics brand owners specify polyurethane, polyethylene, and EVA foams with embedded ESD protection to maintain warranty compliance. North American adoption has accelerated since 2024 and parallels rapid e-commerce expansion in Southeast Asia, boosting regional shipment volumes that favor compact, sustainable cushioning solutions.

24-Hour Food-Delivery Boom in Asia Requiring Insulated Foam Packs

App-based food aggregators promise full-day delivery windows that stress temperature management across variable climates. Operators therefore adopt multi-layered foam packs integrating reflective films and phase-change inserts that keep meals within 2 °C of target for up to 24 hours. Vietnam’s single-use polystyrene taxes and upcoming plastic bans provoke a pivot toward bio-derived insulation formats, pushing suppliers to qualify compliant polyolefin or cellulose foams. Chinese regulators have tightened migration testing for food-contact materials, reinforcing demand for formulations with low VOC and minimal residual monomer content. In Singapore, temperature thresholds above 100 °C outlined by the Food Agency oblige suppliers to validate foam container safety across hot-food use cases. These directives collectively advance premium, regulation-ready solutions across Asia’s fast-growing meal-delivery networks.

Logistics Lightweighting Initiatives to Cut Freight Costs

Retailers and CPG firms embed “skinny design” principles that minimize package cube and mass while preserving shelf appeal. Hershey’s shift to one-piece display-ready cases eliminated 3.12 million lb of corrugate and reduced associated logistics CO₂ by 1,340 t. Polyethylene foam profiles containing 95% recycled content win favor because they satisfy plastic-tax exemptions and lower fuel use for outbound loads. Automotive suppliers pursue lightweight synthetic leather options built on foamed polyolefin elastomers to trim interior mass and enhance vehicle efficiency. European pet-food brand Mera cut logistics expense 40% after switching from rigid tubs to corrugated formats enabled by automated foam inserts that stabilize loads and reduce manual handling.

Rapid Adoption of Bio-Based Polyols for Low-Carbon Foams

Polyurethane formulators increasingly replace petroleum polyols with lignin, vegetable oil, or castor-oil derivatives that reduce embodied carbon without sacrificing density or compression strength. University of Liège researchers reported isocyanate-free foams that include 70-90% bio-content and expand at ambient temperature in under two minutes[1]University de Liège, “Isocyanate-free, biobased polyurethane foams,” phys.org . Wanhua’s plant-based polyether polyols lower VOC emissions and improve compression resistance, offering attractive drop-in alternatives for furniture and appliance makers. Policy targets such as the US goal to reach 25% bio-based chemical substitution by 2030 accelerate commercialization pipelines, while EU frameworks drive 6-12% replacement of fossil feedstocks. Construction suppliers deploy bio-circular polyiso foam panels to satisfy green-building credits, signaling mainstream acceptance across insulation markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| City-level bans on single-use polystyrene | -0.90% | Global, with early implementation in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Styrene & isocyanate price volatility | -0.60% | Global, with particular impact in Europe and North America | Medium term (2-4 years) |

| Rapid advances in molded-pulp & mushroom packaging substitutes | -0.40% | Europe and North America leading, gradual global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

City-Level Bans on Single-Use Polystyrene

Municipal restrictions accelerate material transition by limiting expanded-polystyrene foodservice items and enforcing eco-fee structures that raise cost parity with bio-based formats. California’s SNAP-aligned prohibitions on specific hydrofluorocarbons in foam cushions further reduce polystyrene competitiveness[2]California Air Resources Board, “Foams,” arb.ca.gov . The EU-backed PolyStyreneLoop facility validates dissolution recycling routes but still requires costly collection systems, adding complexity for converters Vietnam’s staged plastic bans from 2026-2031 intensify regional momentum toward recyclable and compostable foams. As local mandates broaden, packaging producers diversify portfolios to preserve market access and mitigate compliance risks.

Styrene & Isocyanate Price Volatility

Feedstock turbulence stems from plant shutdowns, shipping constraints, and shifting trade flows that move Europe from net exporter to net importer of styrene. Trinseo raised polystyrene list prices by EUR 55/t in January 2025 to absorb elevated benzene costs, squeezing converter margins. In the US, supply tightness intersects with robust e-commerce demand, prompting procurement managers to lock multi-quarter contracts or blend bio-polyols to hedge exposure. Asia remains a demand anchor, with China importing 35% of traded polystyrene volumes and exerting upward price pressure on global indices. Volatility complicates budgeting for converters and encourages evaluation of feedstock-agnostic formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polyurethane Dominance Faces Polyolefin Challenge

Polyurethane held 50.98% of the packaging foam market share in 2025, benefiting from well-established supply chains and adaptable density ranges that suit both cushioning and insulation. Polyolefin, however, is projected to capture expanding demand with a 5.43% CAGR through 2031, supported by formulations containing up to 95% recycled content that comply with plastic-tax exemptions. Bio-based polyurethane research—such as lignin-reinforced foams retaining 0.0289 W/m·K thermal conductivity—indicates future growth potential while addressing greenhouse-gas goals. Regulatory pressure on polystyrene deepens its volume decline, although dissolution recycling projects may moderate the pace in select EU regions. Specialty phenolic foams leveraging hydrofluoroolefin blowing agents emerge in high-temperature cold-chain packaging where low global-warming potential is valuable.

The polyurethane segment of the packaging foam market is anticipated to achieve significant growth, while the polyolefin sub-segment is expected to witness notable expansion over the forecast period. These trajectories underscore a gradual but material shift toward chemistries that lower carbon intensity, improve recyclability, and align with brand-owner pledges on post-consumer content. As new bio-polyol capacity comes onstream, formulators anticipate incremental cost parity that could accelerate substitution in the outer years of the forecast.

By Structure: Flexible Foam Maintains Dual Leadership

Flexible variants accounted for 60.25% of the packaging foam market size in 2025, reflecting their suitability for convoluted shapes and rapid cushioning in automated lines. Rigid foams remain essential in temperature-controlled logistics, yet their market share is limited by higher density and disposal complexity. Expancel BIO microspheres enable thinner flexible cushions with no loss in compression set while delivering up to 15% weight savings, bolstering performance leadership. Bio-based rigid foams integrating kraft lignin exhibit improved fire resistance and VOC profiles that support uptake in medical coolers and pharmaceutical shippers.

Flexible foam is forecast to sustain a 4.74% CAGR to 2031, sustained by electronics, cosmetics, and omni-channel retail packaging. The packaging foam market share trend suggests continued dominance for flexible formats, though regulatory scrutiny on end-of-life recycling may favor rigid options with closed-loop recovery schemes in certain jurisdictions.

By Application: Industrial Packaging Scale Versus Food Packaging Growth

Industrial goods, encompassing automotive parts, electronics, and appliance components, represented 81.05% of 2025 demand, confirming the historical focus of foam cushioning on high-value freight. Food packaging, although smaller in tonnage, is projected as the fastest-expanding niche at 5.31% CAGR thanks to explosive on-demand meal delivery and cold-chain penetration. Electronics assemblers increasingly specify ESD-safe polyurethane inserts that remain functional through multiple shipping cycles, thereby supporting circular supply programs.

Packaging foam market size for food applications is expected to increase by 2031, generating incremental volume that offsets slowing growth in legacy industrial segments. Thermal-insulation films containing silica aerogel for chocolate shipments illustrate the sophistication required to maintain product integrity over extended delivery windows. As retail grocery shifts to omnichannel models, temperature-sensitive foam liners will capture expanded share within urban micro-fulfillment networks.

Geography Analysis

Asia-Pacific leads with 40.10% share and a forecast 5.56% CAGR, propelled by robust e-commerce ecosystems, burgeoning meal-delivery services, and government investment in cold-chain vaccine capacity. Despite setting domestic recycling targets, China remains a significant importer of polystyrene, emphasizing strong regional demand for the raw material. Vietnam’s taxation of single-use styrofoam accelerates substitution toward polyolefin and mushroom-derived foams in Southeast Asia, while Japan and South Korea pursue hydrogen-blown polyurethane for lower GWP profiles.

North America commands a sizable slice of the packaging foam market, supported by sophisticated fulfillment infrastructure and aggressive sustainability roadmaps by leading retailers. Amazon’s exit from air pillows in 2024 nudged the supply base toward recyclable cushions and validated high-volume production scaling. Nouryon’s Wisconsin expansion reflects local demand for lightweight fillers that cut freight intensity while maintaining protective performance. Federal SNAP approvals of next-generation blowing agents provide regulatory certainty for bio-based and low-GWP chemistries.

Europe grapples with elevated feedstock costs and strict chemical regulations, yet remains a hotspot for bio-innovation and circular-economy pilots. Stora Enso’s Papira trials in Germany confirm market appetite for cellulose foams capable of replacing EPS across furniture and consumer-electronics channels. The region’s transition from net exporter to importer of styrene highlights structural supply challenges driving volatility. Eastern European converters increasingly explore molded-pulp formats to comply with single-use directives, while maintaining niche EPS demand in specialty insulation.

South America, the Middle East, and Africa contribute modest but rising shares to the global footprint. Brazil’s e-commerce acceleration fosters adoption of lightweight PE foams in electronics, whereas Gulf Cooperation Council countries apply polyurethane insulation for vaccine transport across desert climates. Africa’s vaccine logistics investments, co-funded by multilateral donors, prioritize recyclable rigid foams that sustain performance in high-temperature corridors, laying groundwork for future demand expansion.

Competitive Landscape

The packaging foam market exhibits moderately fragmented concentration. Industry consolidation is underway as firms chase economies of scale and R&D synergies. Strategic investment in bio-based capacity marks a second competitive axis. BASF earmarked EUR 19.50 billion for capital projects through 2027, including an MDI expansion in Louisiana and a TPU plant in Zhanjiang to tap Asian demand. Armacell’s full purchase of its aerogel joint venture improves control over high-performance insulation pivotal for cold-chain applications. Dow partners with Sealed Air to commercialize REVOLOOP post-consumer resin foams, facilitating circularity and reinforcing brand commitments to recycled content.

Technology differentiation continues as a third lever. Fraunhofer’s heat-activated shape-memory polyurethane foil promises space-saving logistics and reduced storage footprints for converters. Suppliers lacking the capital to pivot toward such innovation risk erosion of share as brand owners adopt multi-criteria supplier scorecards that favor low-carbon and curbside-recyclable solutions.

Packaging Foams Industry Leaders

Armacell

BASF SE

Carpenter Engineered Foams Belgium BV

Sealed Air

Zotefoams PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Stora Enso has partnered with the German company Novapor to pilot a project utilizing Papira, a cellulose-based foam packaging material. This initiative aims to replace traditional foams with a wood fiber-based alternative that retains protective properties while reducing carbon emissions.

- March 2025: EFP has announced a USD 31.5 million investment to expand its operations in Lee County, South Carolina. This initiative will increase production capacity for advanced expanded polystyrene (EPS) and expanded polypropylene (EPP) solutions, with full operations expected to commence by April 2026.

Global Packaging Foams Market Report Scope

Packaging foam is commonly used as cushioning material for boxes, and this packaging solution is known for its versatility and its ability to be customized. The packaging foam market is segmented by material, structure, application, and geography. By material, the market is segmented into polystyrene, polyurethane, polyolefin, and other materials. By structure, the market is segmented into flexible and rigid. By application, the market is segmented into food packaging and industrial packaging. The report also covers the market size and forecasts for the packaging foam market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Polystyrene |

| Polyurethane |

| Polyolefin |

| Other Materials |

| Flexible |

| Rigid |

| Food Packaging | |

| Industrial Packaging | Transportation Components |

| Electrical and Electronics | |

| Personal Care | |

| Pharmaceutical | |

| Other Industrial Packaging |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material | Polystyrene | |

| Polyurethane | ||

| Polyolefin | ||

| Other Materials | ||

| By Structure | Flexible | |

| Rigid | ||

| By Application | Food Packaging | |

| Industrial Packaging | Transportation Components | |

| Electrical and Electronics | ||

| Personal Care | ||

| Pharmaceutical | ||

| Other Industrial Packaging | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the packaging foam market?

The packaging foam market size is USD 12.76 billion in 2026.

How fast is the packaging foam market expected to grow?

The market is projected to register a 4.45% CAGR between 2026 and 2031, reaching USD 15.87 billion.

Which material dominates the packaging foam market?

Polyurethane leads with 50.98% market share in 2025, thanks to its versatility across cushioning and insulation applications.

Which region shows the fastest growth in packaging foam demand?

Asia-Pacific records the highest forecast growth at 5.56% CAGR through 2031, driven by e-commerce and food-delivery expansion.

What key factor is driving adoption of bio-based foams?

Regulatory pressure to reduce greenhouse-gas footprints and replace fossil feedstocks accelerates the deployment of lignin- and vegetable-oil-based polyols.

How are logistics cost-saving strategies influencing foam design?

Companies optimize package dimensions and deploy lightweight foam inserts, delivering up to 25% freight savings and lowering CO₂ emissions.

Page last updated on: