Ortho-Pediatric Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

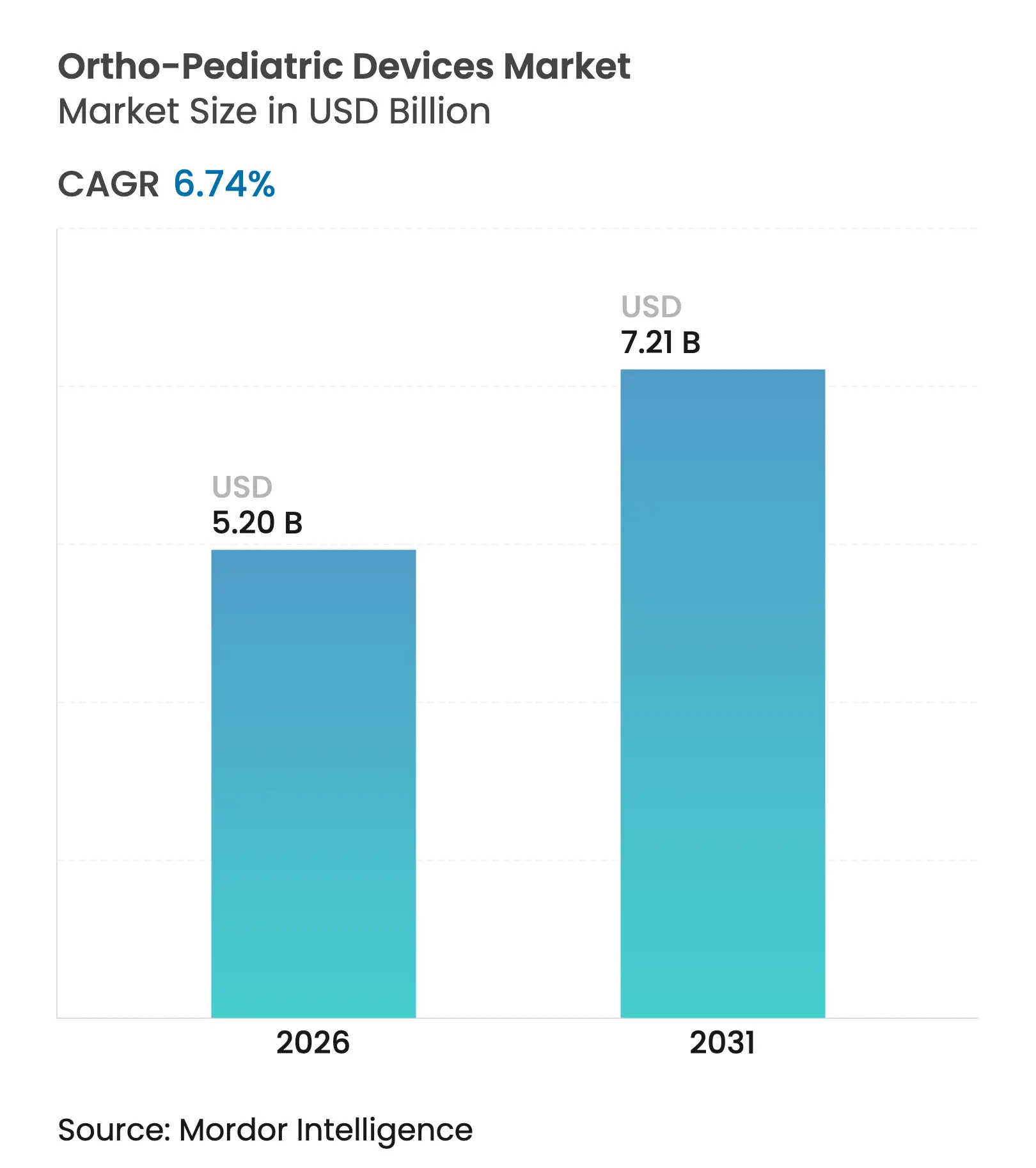

| Market Size (2026) | USD 5.2 Billion |

| Market Size (2031) | USD 7.21 Billion |

| Growth Rate (2026 - 2031) | 6.74 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ortho-Pediatric Devices Market Analysis by Mordor Intelligence

The ortho-pediatric devices market size is expected to grow from USD 4.87 billion in 2025 to USD 5.2 billion in 2026 and is forecast to reach USD 7.21 billion by 2031 at 6.74% CAGR over 2026-2031. Demand gains stem from a rising caseload of childhood fractures and congenital deformities, wider availability of age-adjustable implants, and rapid capacity‐building in emerging surgical hubs. Custom design requirements for growing skeletons yield higher entry barriers than adult orthopedics, helping manufacturers sustain pricing power. Momentum also comes from an 11.23% CAGR shift toward minimally invasive techniques, improving recovery times and lowering revision risks. In parallel, expanding 3D-printing capabilities and supportive reimbursement schemes in mature economies catalyze innovation cycles and bolster global device adoption.

Key Report Takeaways

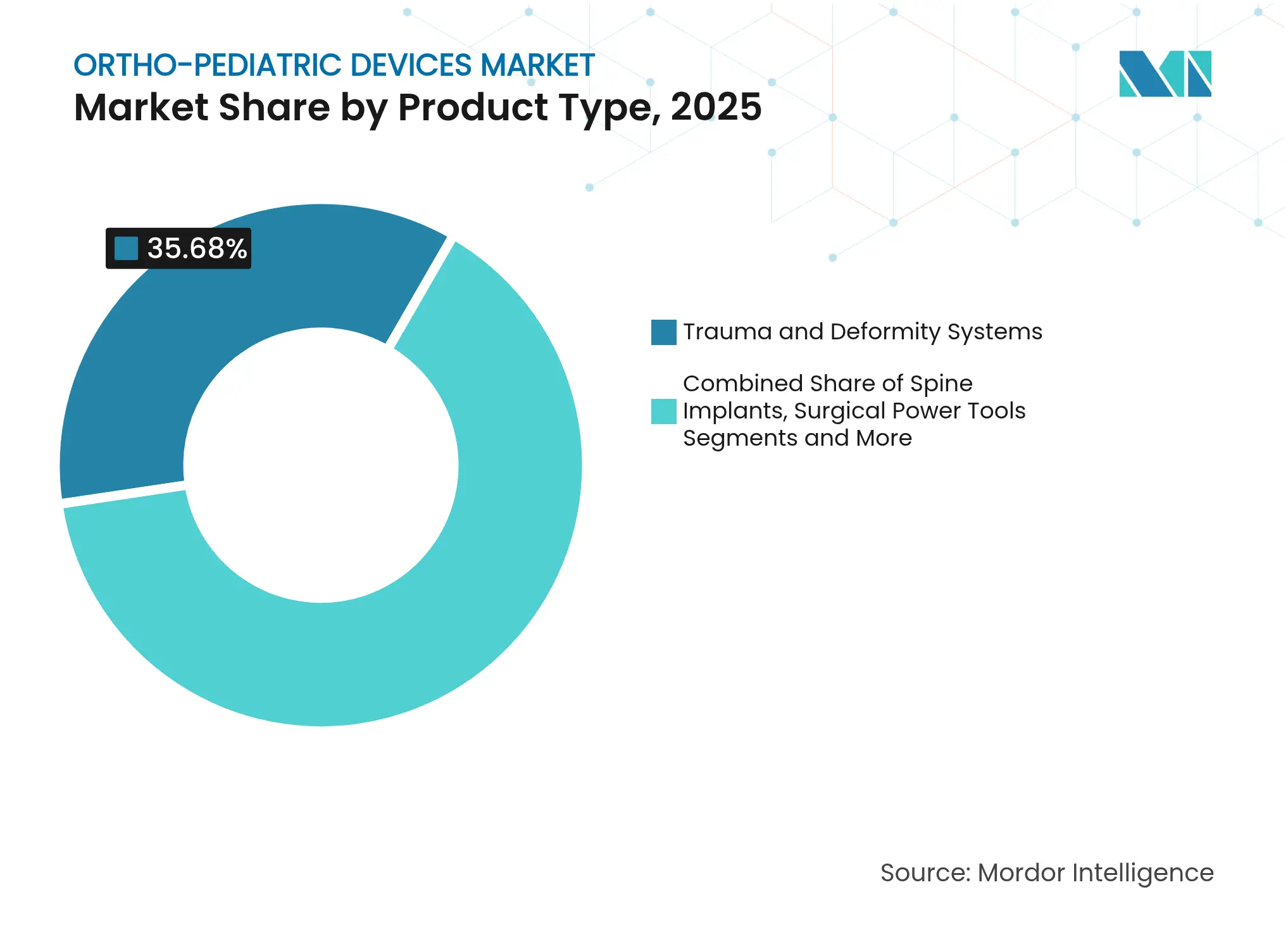

- By product type, Trauma & Deformity Systems led with 35.68% revenue share in 2025, while Sports-Medicine Implants are forecast to grow at a 9.45% CAGR to 2031.

- By application, Trauma retained 39.05% of the ortho-pediatric devices market share in 2025; Sports Injuries show the fastest expansion at 10.12% CAGR through 2031.

- By material, Titanium accounted for 43.90% of the ortho-pediatric devices market size in 2025; Bio-absorbable Polymers are projected to advance at 10.68% CAGR between 2026-2031.

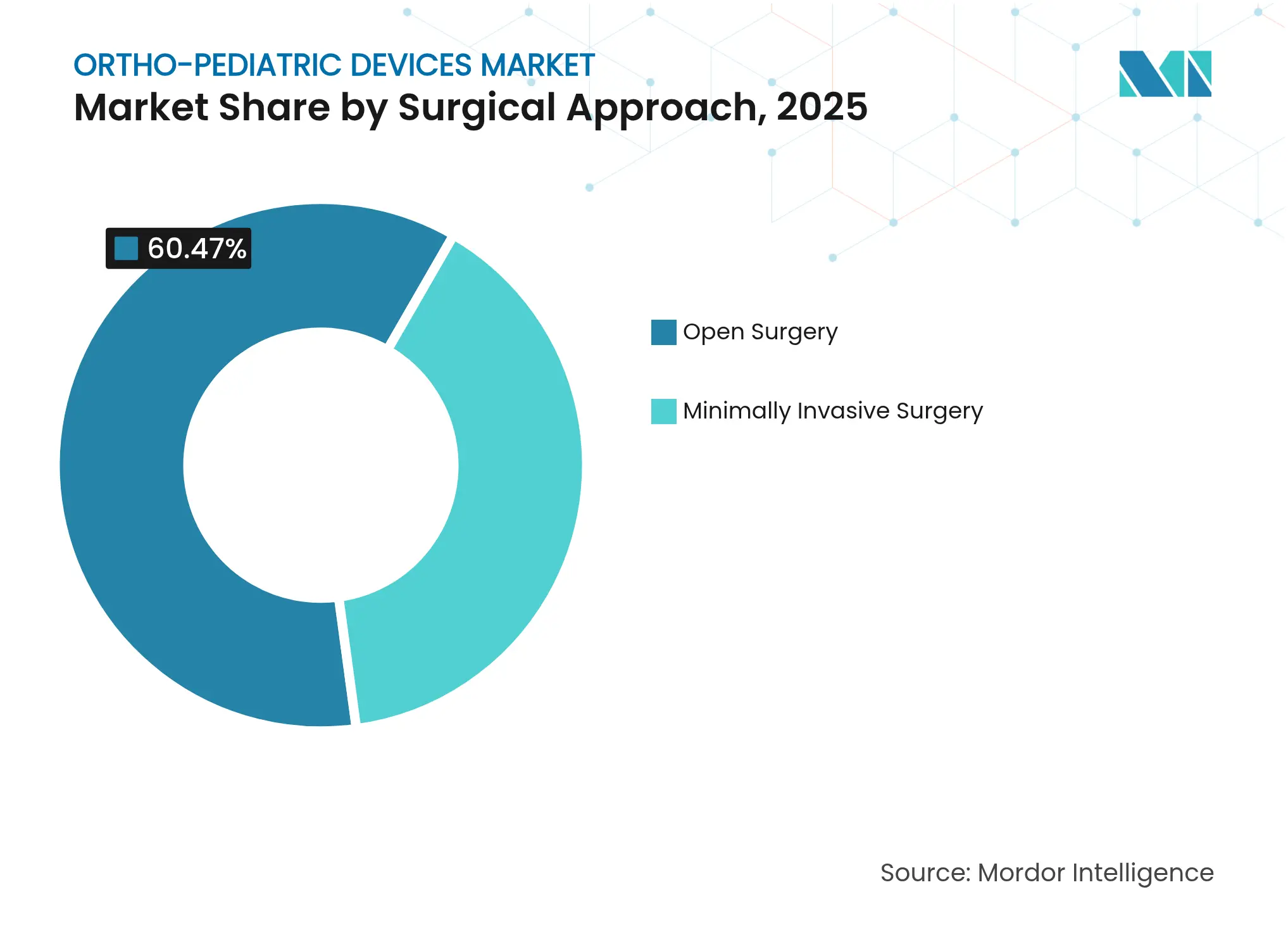

- By surgical approach, Open Surgery dominated with 60.47% revenue share in 2025, whereas Minimally Invasive Surgery is growing at 10.77% CAGR through 2031.

- By end user, Hospitals commanded 50.60% share in 2025, while Ambulatory Surgical Centres are poised for a 8.72% CAGR to 2031.

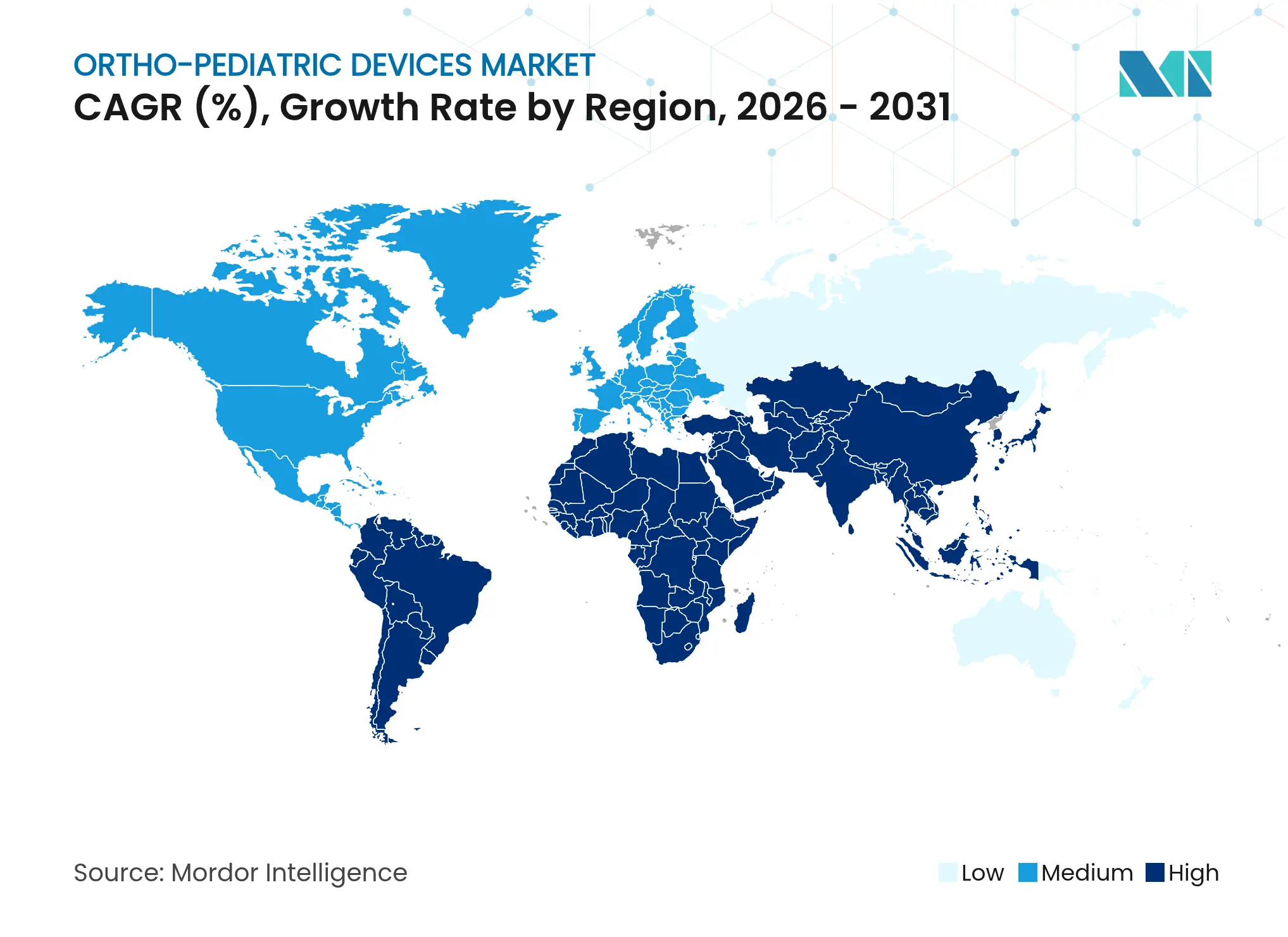

- By geography, North America held 43.85% market share in 2025; Asia Pacific is projected to climb at a 9.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ortho-Pediatric Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising incidence of pediatric

musculoskeletal trauma & congenital deformities

Rising incidence of pediatric

musculoskeletal trauma & congenital deformities

| +1.8% | Global ; higher in developing regions | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.8%

|

Geographic Relevance

:

Global ; higher in developing

regions

|

Impact Timeline

:

Medium term (2-4 years)

|

Technological advancements in pediatric-specific

implants & 3-D printing

Technological advancements in pediatric-specific

implants & 3-D printing

| +1.5% | North America & EU lead ; APAC accelerating | Long term (≥ 4 years) | |||

Increasing youth sport-related

injuries

Increasing youth sport-related

injuries

| +1.2% | North America, Europe, urban APAC | Short term (≤ 2 years) | |||

Favourable reimbursement in

developed economies

Favourable reimbursement in

developed economies

| +0.9% | North America, Western Europe, select APAC | Medium term (2-4 years) | |||

Age-adjustable implant systems

reducing revision surgeries

Age-adjustable implant systems

reducing revision surgeries

| +0.8% | Global ; premium markets first | Long term (≥ 4 years) | |||

Philanthropic ortho-surgical

outreach in low-income nations

Philanthropic ortho-surgical

outreach in low-income nations

| +0.6% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Incidence of Pediatric Musculoskeletal Trauma & Congenital Deformities

Pediatric trauma cases require more complex fixation than adult injuries, and patients under 16 record higher revision rates than older adolescents.[1]Michael Tátrai, “Higher Revision and Secondary Surgery Rates After ACL Reconstruction in Athletes Under 16 Compared to Those Over 16,” Journal of Orthopaedic Surgery and Research, josr-online.biomedcentral.com Clubfoot affects 7.2 per 1,000 children in Ethiopia, underscoring unmet demand in low-resource environments. Early intervention protocols have lifted device utilization, and 28% of rural Indian children still present late because of access barriers, further elevating implant volumes when surgery finally occurs.[2]Deeptiman James, “Epidemiological Determinants of Children’s Orthopedic Care in Rural Central India,” Journal of Orthopaedics, Traumatology and Rehabilitation, journals.lww.com These demographic pressures give the ortho-pediatric devices market consistent growth across economic cycles.

Technological Advancements in Pediatric-Specific Implants & 3-D Printing

Point-of-care 3D printing lets surgeons build patient-specific plates that cut operative time and enhance anatomical fit.[3]Seid Mohammed Abdu, “Prevalence and Pattern of Congenital Clubfoot Among Children in Ethiopia,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com Material breakthroughs such as PLGA nails remove the need for secondary extraction surgery, lowering complication risks. Artificial-intelligence planning tools already achieve >90% accuracy for sizing pediatric implants.[4]Andrea Vescio, “Artificial Intelligence in Pediatric Orthopedics,” Medicina, mdpi.com Collectively, these advances tighten procedure workflows, improve outcomes, and strengthen device differentiation in the ortho-pediatric devices market.

Increasing Youth Sport-Related Injuries

Roughly 3 million U.S. children visit emergency rooms each year for sports injuries. Early specialization boosts overuse lesions, prompting demand for implants tailored to repetitive-stress conditions rather than acute trauma. Sports-related lower-extremity injuries in U.S. youth soccer have declined, reflecting better protective gear, yet device design now must address evolving injury patterns. Pediatric ACL reconstructions continue to rise despite high revision odds, driving innovation in smaller, growth-friendly fixation hardware.

Favourable Reimbursement in Developed Economies

Medicaid and CHIP insure 81.5 million Americans, nearly half of whom are children; this guarantees payment for complex orthopedic procedures. The FDA’s Total Product Life Cycle Advisory Program added orthopedics in 2025, shortening review times for pediatric systems. European payers mirror these models, though local rules vary. Stable reimbursement underpins device adoption, particularly for minimally invasive techniques that command premium tariffs, bolstering the ortho-pediatric devices market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Scarcity of specialised paediatric

orthopaedic surgeons

Scarcity of specialised paediatric

orthopaedic surgeons

| –1.4% | Global ; acute in rural & developing regions | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

–1.4%

|

Geographic Relevance

:

Global ; acute in rural &

developing regions

|

Impact Timeline

:

Medium term (2-4 years)

|

High device costs versus adult implants

High device costs versus adult implants

| –1.1% | Price-sensitive & emerging markets | Short term (≤ 2 years) | |||

Stringent paediatric trial

requirements & small cohorts

Stringent paediatric trial

requirements & small cohorts

| –0.8% | Global regulatory markets | Long term (≥ 4 years) | |||

Custom-implant supply-chain

fragility

Custom-implant supply-chain

fragility

| –0.5% | Global ; concentrated manufacturing hubs | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Scarcity of Specialised Paediatric Orthopaedic Surgeons

Rural regions worldwide experience persistent workforce gaps; the U.S. alone reports uneven distribution despite overall surgeon numbers. Fellowship grads often cluster in urban centers, leaving vast catchment areas underserved. Administrative burdens tied to electronic medical records further depress productivity, constraining the ortho-pediatric devices market even where devices are stocked.

High Device Costs Versus Adult Implants

Smaller production runs, tight tolerances, and extra regulatory steps keep pediatric implants priced higher than adult equivalents. China’s volume-based procurement cut hip-arthroplasty prices by 50%, hinting at cost-containment models that could spill into pediatrics. Until then, budget pressures in emerging markets slow uptake of premium technologies, moderating ortho-pediatric devices market growth.

Segment Analysis

By Product Type: Trauma Systems Drive Innovation

Trauma & Deformity Systems captured 35.68% of 2025 revenue, reflecting universal fracture and angular-correction needs across age groups. Elastic stable intramedullary nailing achieved 100% union in pediatric forearm fractures, reinforcing clinical trust. Sports-Medicine Implants, projected at 9.45% CAGR, ride the youth-sports wave and subspecialty surgeon focus. Spine Implants benefit from magnetically controlled lengthening technologies that enable non-invasive post-operative adjustments.

Cross-fertilization of design principles speeds innovation across categories. For instance, low-profile plates first proven in trauma are now adopted in deformity correction. Biologics & Bone Grafts gain ground as adjuncts that cut healing time, while bioexpandable prostheses address oncologic limb-sparing cases. Overall, technological convergence keeps the ortho-pediatric devices market dynamic and competitive.

Note: Segment shares of all individual segments available upon report purchase

By Application: Sports Injuries Reshape Market Dynamics

Trauma remains the backbone at 39.05% share, yet Sports Injuries lead growth at 10.12% CAGR as young athletes pursue year-round training. Late-presenting trauma cases, common in underserved regions, often entail multi-stage surgery, boosting implant volume. Deformity Correction thrives on improved guided-growth techniques such as eight-plate hemiepiphysiodesis, offering minimally invasive solutions.

Limb Lengthening, though niche, attracts attention through magnetically driven intramedullary nails that lower complication rates. The remaining “Others” segment addresses congenital anomalies and tumor reconstructions, demanding highly bespoke devices. Diversifying applications reinforce resilience in the ortho-pediatric devices market.

By Material: Bio-absorbable Polymers Challenge Titanium Dominance

Titanium kept 43.90% share in 2025 thanks to superior strength and osseointegration. Bio-absorbable Polymers surge at 10.68% CAGR because they obviate second surgeries for hardware removal, a critical advantage for children. Stainless Steel remains useful for temporary fixation, but composite materials like CFR-PEEK add imaging transparency that eases follow-up.

Research into tri-element-doped hydroxyapatite composites merges structural and therapeutic roles, pointing to next-gen constructs capable of both load bearing and antimicrobial delivery. Material breakthroughs therefore continue to expand functionality within the ortho-pediatric devices market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Surgical Approach: Minimally Invasive Techniques Gain Momentum

Open Surgery still represented 60.47% of procedures in 2025 because complex pediatric anatomy often demands direct access. Yet Minimally Invasive Surgery is rising at 10.77% CAGR, aided by 8 mm-incision hemiepiphysiodesis that matches correction rates of open 24 mm cuts. Robotics platforms such as VELYS elevate precision while lowering surgeon fatigue.

Enhanced recovery after surgery protocols, emphasizing reduced tissue trauma, reinforce institutional incentives to adopt minimally invasive approaches. Expanding surgeon training is expected to narrow the skill gap and amplify growth in the ortho-pediatric devices market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Ambulatory Centers Transform Care Delivery

Hospitals held 50.60% share during 2025, reflecting their broader infrastructure and trauma readiness. Ambulatory Surgical Centres, advancing at 8.72% CAGR, leverage cost efficiency and same-day discharge protocols. Specialty Clinics manage routine follow-ups and minor interventions, while tele-orthopedics supports remote rehabilitation—an especially valuable service for families distant from tertiary centers.

The COVID-19 era normalized outpatient care where safe, and 3D-printed casts now facilitate quick, customised bracing outside the hospital. These shifts broaden access and bolster the ortho-pediatric devices market across care settings.

Geography Analysis

North America preserved 43.85% share in 2025, underpinned by robust reimbursement, a mature surgeon workforce, and FDA programs that accelerate device approvals. Medicaid and CHIP collectively guarantee coverage for a vast pediatric cohort, ensuring predictable demand. Nonetheless, rural shortages of specialists create localised gaps, signaling white-space opportunities for tele-consultation and outreach.

Asia Pacific is the growth pacesetter at a 9.21% CAGR through 2031. China’s procurement reforms cut implant prices by 50%, reshaping global price floors, while a burgeoning private-hospital sector expands premium procedure volumes. India benefits from medical tourism inflows and expanding metropolitan health networks, though infrastructural deficits persist in rural districts. Japan and South Korea exhibit low-single-digit growth on high bases, driven by rapid adoption of minimally invasive and robotic techniques. Europe sustains steady progress through coordinated research frameworks, with Germany and the U.K. spearheading clinical trials on bio-absorbable materials. Latin America shows promise as Brazil and Mexico upgrade pediatric trauma centers amid economic volatility. The Middle East and Africa remain early-stage markets where philanthropy and public-private partnerships seed initial uptake, positioning the ortho-pediatric devices market for gradual expansion as training pipelines mature.

Competitive Landscape

Market Concentration

The ortho-pediatric devices market is moderately fragmented. OrthoPediatrics, the only pure-play pediatric company, posted USD 204.7 million revenue in 2024, up 38% year-on-year. Its USD 22 million takeover of Boston Orthotics & Prosthetics broadened its reach into the USD 500 million bracing niche, signalling a platform strategy around full-spectrum pediatric care.

Industry majors pursue pediatric adjacencies via their adult portfolios. Johnson & Johnson integrates digital planning and robotic arms to capture complex deformity cases. Stryker’s bid for soft-tissue repair firm Artelon underscores interest in sports medicine, a high-growth subsegment. Zimmer Biomet sharpened its extremities offering with the Paragon 28 acquisition, chasing limb lengthening and deformity workups.

Supply-chain resilience emerges as a new battleground: OEMs now invest 3–5% of revenue to diversify raw material sources and digitize logistics in response to geopolitical risks. Collectively, these strategies elevate entry barriers and increase the strategic value of specialized pediatric know-how.

Ortho-Pediatric Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: OrthoPediatrics launched the FDA-cleared VerteGlide Spinal Growth Guidance System for early-onset scoliosis treatment.

- March 2025: OrthoPediatrics partnered with the Crossroads Pediatric Device Consortium to accelerate commercialization of novel pediatric implants.

Table of Contents for Ortho-Pediatric Devices Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence Of Pediatric Musculoskeletal Trauma & Congenital Deformities

- 4.2.2Technological Advancements In Pediatric-Specific Implants & 3-D Printing

- 4.2.3Increasing Youth Sport-Related Injuries

- 4.2.4Favourable Reimbursement In Developed Economies

- 4.2.5Age-Adjustable Implant Systems Reducing Revision Surgeries

- 4.2.6Philanthropic Ortho-Surgical Outreach In Low-Income Nations

- 4.3Market Restraints

- 4.3.1Scarcity Of Specialised Paediatric Orthopaedic Surgeons

- 4.3.2High Device Costs Vs. Adult Implants

- 4.3.3Stringent Paediatric Trial Requirements & Small Cohorts

- 4.3.4Custom-Implant Supply-Chain Fragility

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Product Type

- 5.1.1Trauma & Deformity Systems

- 5.1.2Spine Implants

- 5.1.3Surgical Power Tools

- 5.1.4Sports-Medicine Implants

- 5.1.5Biologics & Bone Grafts

- 5.1.6Others

- 5.2By Application

- 5.2.1Trauma

- 5.2.2Deformity Correction

- 5.2.3Sports Injuries

- 5.2.4Limb Lengthening

- 5.2.5Others

- 5.3By Material

- 5.3.1Stainless Steel

- 5.3.2Titanium

- 5.3.3Bio-absorbable Polymers

- 5.3.4Composite Materials

- 5.3.5Others

- 5.4By Surgical Approach

- 5.4.1Open Surgery

- 5.4.2Minimally Invasive Surgery

- 5.5By End User

- 5.5.1Hospitals

- 5.5.2Specialty Clinics

- 5.5.3Ambulatory Surgical Centres

- 5.5.4Others

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1OrthoPediatrics Corp.

- 6.3.2Johnson & Johnson

- 6.3.3Stryker

- 6.3.4Arthrex Inc.

- 6.3.5Zimmer Biomet

- 6.3.6Smith & Nephew

- 6.3.7Orthofix US LLC

- 6.3.8WishBone Medical

- 6.3.9Merete GmbH

- 6.3.10Samay Surgical

- 6.3.11NuVasive

- 6.3.12Medtronic plc

- 6.3.13Globus Medical

- 6.3.14Pega Medical

- 6.3.15KLS Martin Group

- 6.3.16Acumed LLC

- 6.3.17Medartis AG

- 6.3.18EOS Imaging

- 6.3.19Invibio Biomaterial Solutions

- 6.3.20B. Braun Melsungen AG

- 6.3.21Ortho Solutions

- 6.3.22Orthomed SAS

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Ortho-Pediatric Devices Market Report Scope

As per the scope of the report, pediatric orthopedics is defined as a branch of medicine that treats children’s muscles, joints, and bones. Similarly, ortho-pediatric devices are the devices used for treating children who have bone deformities and get their skeletal systems injured.

The ortho-pediatric devices market is segmented by application and geography. By application, the market is segmented into trauma, deformity correction, external fixation, sports, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for the above segments.