Organic Skin Care Products Market Size and Share

Market Overview

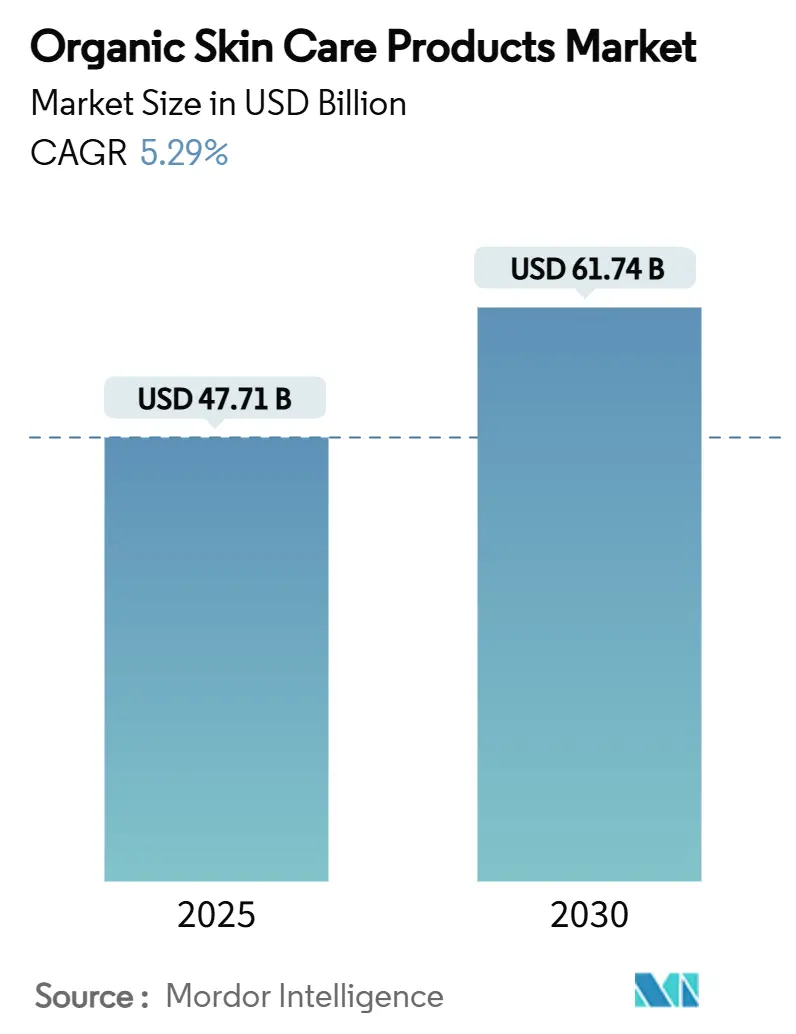

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 47.71 Billion |

| Market Size (2030) | USD 61.74 Billion |

| Growth Rate (2025 - 2030) | 5.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Skin Care Products Market Analysis by Mordor Intelligence

The organic skin care market is expected to reach USD 47.71 billion in 2025, growing at a CAGR of 5.29% to reach USD 61.74 billion by 2030. The market expansion is primarily attributed to heightened health consciousness, environmental considerations, and evolving consumer preferences. Market analysis indicates a significant shift as consumers increasingly avoid synthetic chemicals such as parabens, sulfates, and artificial fragrances in conventional skincare products, subsequently transitioning to plant-based alternatives. Furthermore, the market demonstrates substantial growth potential through companies that implement ethical sourcing practices, environmental responsibility measures, and transparent supply chain operations. The proliferation of social media platforms has substantially enhanced consumer awareness regarding organic and non-toxic personal care products. Industry participants are allocating substantial resources to research and development initiatives, focusing on developing efficacious organic formulations that demonstrate comparable performance to synthetic alternatives.

Key Report Takeaways

- By product type, facial care held 76.44% of the organic skin care products market share in 2024, while body care is projected to grow at a 5.43% CAGR through 2030.

- By category, mass products accounted for 67.35% revenue share of the organic skin care products market in 2024; premium products are forecast to expand at a 5.97% CAGR to 2030.

- By distribution channel, specialty stores led with 32.74% revenue share in 2024, whereas online retail is expected to post the fastest 6.11% CAGR during 2025-2030.

- By geography, Asia-Pacific contributed 41.48% of the organic skin care products market size in 2024 and is advancing at a 6.34% CAGR over 2025-2030.

Global Organic Skin Care Products Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inclination towards clean label products | +1.8% | Global, with highest impact in North America and Europe | Medium term (3-4 yrs) |

| Technological innovations in product formulations | +1.5% | Global, with early adoption in North America, Europe, and developed Asia-Pacific | Long term (≥5 yrs) |

| Growing concerns over effects of synthetic products | +1.2% | Global, with highest impact in Europe and North America | Short term (≤2 yrs) |

| Awareness of vegan and cruelty-free beauty products | +0.9% | Europe, North America, and Urban Asia-Pacific | Medium term (3-4 yrs) |

| Expansion of organic farming practices reduces cost of raw materials | +0.8% | Global, with highest impact in Asia-Pacific and South America | Long term (≥5 yrs) |

| Increasing focus on anti-aging solutions using natural ingredients | +1.1% | Global, with highest impact in developed markets | Medium term (3-4 yrs) |

Source: Mordor Intelligence

Inclination Towards Clean Label Products

Consumer preference for clean label products is driving growth in the organic skincare market, reflecting a shift toward health-conscious, transparent, and sustainable products. Consumers increasingly prefer products with natural, recognizable ingredients that exclude synthetic chemicals, artificial preservatives, and complex additives. This trend stems from increased awareness about potential health risks linked to synthetic ingredients like parabens, sulfates, and artificial fragrances, which may cause skin irritation and allergic reactions. The clean label movement also reflects consumer demand for transparent product labeling and companies that demonstrate commitment to ethical sourcing, cruelty-free practices, and environmentally responsible manufacturing. Companies are responding by developing and launching clean-label skincare products that address consumer requirements for ingredient transparency and safety. In June 2023, Taro Pharmaceuticals Inc. launched Bee Rx in Canada, a natural skincare line featuring 100% naturally-derived ingredients, including high-concentration natural bee venom and Kanuka honey from New Zealand.

Technological Innovations in Product Formulations

The integration of biotechnology into organic personal care formulations constitutes a fundamental market determinant, enabling manufacturers to formulate sustainable ingredients that demonstrate equivalent or superior efficacy in comparison with conventional synthetic alternatives. In December 2024, Estée Lauder Companies established a dedicated BioTech Hub in Belgium for the manufacture of bio-based raw materials, demonstrating substantial industrial investment in sustainable technological advancement. In September 2024, L'Oréal instituted a strategic collaboration with Abolis Biotechnologies and Evonik to advance the development of bio-based ingredients, with the predetermined objective of achieving 95% bio-sourced ingredient composition by 2030. These technological advancements facilitate the formulation of sophisticated textures and delivery systems previously unattainable through natural ingredients, thereby addressing the inherent performance limitations that historically constrained consumer adoption within the organic skincare segment.

Growing Concerns Over the Effects of Synthetic Products on the Body

The prevalence of adverse health implications associated with synthetic ingredients in skincare formulations serves as a primary catalyst for the organic skincare market's expansion. Consumer awareness has heightened regarding synthetic compounds, specifically parabens, sulfates, and artificial fragrances present in conventional beauty products, which demonstrate correlations with dermatological irritation, allergic manifestations, and potential systemic health implications, including endocrine disruption. The American Academy of Dermatology Association reports that acne affects approximately 50 million Americans annually, establishing it as the predominant dermatological condition in the United States [1]Source: American Academy of Dermatology Association, "Skin Conditions By the Numbers,"aad.org. The increasing incidence of dermatological complications, including inflammatory responses, eczematous conditions, and compromised skin barrier function among users of synthetic-based products, has prompted consumers to pursue natural alternatives. This transition has generated substantial demand for organic skincare formulations incorporating natural, botanical ingredients, particularly among individuals presenting with sensitive or problematic skin conditions.

Awareness of Vegan and Cruelty-Free Beauty Products

The prevalence of vegan and cruelty-free beauty products continues to expand, primarily attributed to evolving consumer values regarding ethical consumption, environmental stewardship, and personal well-being. Consumer demand, predominantly from Millennials and Generation Z demographics, emphasizes the importance of sustainability, transparency, and animal welfare in their purchasing behavior. These consumer segments actively seek products devoid of animal-derived ingredients and animal testing protocols, while requiring manufacturers to demonstrate their commitment through third-party certifications, standardized labeling, and responsible sourcing methodologies. Supporting this momentum, the V-Label, an internationally recognized quality seal for vegan and vegetarian products, reported that 85% of consumers already regularly use cruelty-free and vegan cosmetics, and 86% express a desire to buy even more such products in the future [2]Source: V-Label, "Key consumer insights on vegan cosmetics,"v-label.com. This significant consumer preference necessitates that the beauty industry implement product reformulations, incorporate sustainable packaging solutions, and obtain relevant certifications to meet consumer requirements and maintain market competitiveness.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory gaps fueling uncertified products | -0.7% | Global, with highest impact in emerging markets | Medium term (3-4 yrs) |

| Mislabeling/discrepancies in personal care products | -0.4% | Global, with highest impact in regions with weak regulatory enforcement | Short term (≤2 yrs) |

| Limited availability of organic ingredient suppliers creates Supply Bottlenecks | -0.9% | Global, with highest impact in emerging markets and rural regions | Short term (≤2 yrs) |

| Lower Product Stability and Formulation Variations | -0.6% | Global, with highest impact in hot and humid climates | Medium term (3-4 yrs) |

Source: Mordor Intelligence

Regulatory Gaps Fuel Growth of Uncertified Organic and Natural Products

The organic skincare industry encounters significant operational challenges stemming from regulatory disparities and inconsistencies across international markets, which facilitate the proliferation of uncertified organic and natural products. The certification framework exhibits substantial fragmentation, characterized by diverse definitions and standards, resulting in consumer uncertainty and market inequalities. The National Sanitation Foundation (NSF) mandates that products maintain a minimum threshold of 70% organic ingredients by weight to substantiate organic ingredient claims, while alternative certification authorities implement distinct requirements [3]Source: National Sanitation Foundation (NSF), "Organic Personal Care Standards,"nsf.org. The European Union's Directive 2024/825 imposes restrictions on unsubstantiated environmental claims, such as eco-friendly; however, the inconsistent global implementation results in variable enforcement measures and consumer protection standards. These regulatory inconsistencies enable products with questionable certifications to penetrate the market with misleading claims, consequently undermining organizations that invest in legitimate certifications and diminishing consumer confidence.

Mislabeling/Discrepancies in Personal Care Products

The divergence between marketing assertions and product formulations constitutes a fundamental impediment to market integrity and consumer confidence. The Food and Drug Administration (FDA)'s implementation of post-market surveillance protocols rather than pre-market approval mechanisms facilitates the manifestation of unsubstantiated product claims. This circumstance is particularly prevalent within the natural and organic segment, wherein the absence of standardized definitions for terminology, including natural, clean, and green, permits extensive interpretations. Organizations systematically emphasize minimal quantities of natural ingredients while restricting disclosure of conventional base ingredients. In response, regulatory authorities have instituted enhanced compliance measures, including the United States Department of Agriculture (USDA)'s Strengthening Organic Enforcement rule, which mandates comprehensive documentation protocols and standardized organic certificates for heightened traceability measures.

Segment Analysis

By Product Type: Facial Care Dominates While Body Care Accelerates

Facial care commands 76.44% of the market share in 2024, primarily driven by increasing consumer awareness of skin health and rising demand for preventive skincare solutions. The segment's expansion is attributed to the growing preference for scientifically proven natural formulations, particularly in anti-aging and skin barrier repair categories. Consumer demand for personalized skincare solutions remains a significant market driver, as demonstrated by L'Oréal's strategic launch of the Cell BioPrint device at CES 2025. This diagnostic innovation, which delivers personalized skin analysis within five minutes through advanced proteomics technology, represents the increasing convergence of technology and natural skincare formulations.

Body care is projected to grow at a 5.43% CAGR from 2025 to 2030, driven by technological advancements in product functionality and ingredient innovations. Market growth is further supported by evolving consumer preferences, as users increasingly apply facial skincare quality standards to body care products. This shift is evidenced by Natura & Co's sustainability initiatives, including their commitment to 50% recycled packaging content by 2030 and the development of environmentally conscious formulations. The lip care segment, while representing a smaller market share, demonstrates growth through specialized natural formulations that combine cosmetic and therapeutic benefits.

Note: Segment shares of all individual segments available upon report purchase

By Category: Mass Products Evolve While Premium Segment Accelerates

Mass-market organic skin care products maintain a significant presence in the global market, accounting for 67.35% of the market share in 2024. This market dominance is attributed to extensive distribution networks, competitive pricing strategies, and established presence across retail channels. The increasing consumer emphasis on ingredient transparency and safety protocols has substantially contributed to the demand for mass-market organic alternatives. The segment's success is further reinforced by its comprehensive demographic reach, enabling broader access to organic skin care solutions and solidifying its market leadership position.

The premium organic skin care segment demonstrates substantial growth potential, with a projected compound annual growth rate (CAGR) of 5.97% during 2025-2030. This growth trajectory is supported by increasing consumer investment in scientifically validated, natural formulations that demonstrate verifiable sustainability credentials and measurable efficacy. The segment's expansion is particularly evident among higher-income demographics, who demonstrate a clear preference for product efficacy and technological advancement. Premium manufacturers are implementing strategic expansion initiatives to address this market demand. This trend is exemplified by Patyka, the Parisian skincare brand, which executed a strategic market entry into the Middle East in December 2024.

By Distribution Channel: Specialty Stores Lead While Online Retail Surges

Specialty stores command a 32.74% market share in 2024, driven by their strategic focus on curated product selections, highly trained staff expertise, and increasing consumer preference for personalized shopping experiences. These retailers establish comprehensive shopping environments that facilitate consumer understanding of natural brands and validate premium pricing structures. Key growth factors include rising consumer awareness of natural ingredients, demand for expert consultation, and the stores' ability to maintain strong relationships with niche brand manufacturers.

Online retail stores are projected to grow at a 6.11% CAGR during 2025-2030, primarily attributed to their extensive product assortments, data-driven pricing strategies, and sophisticated digital retail infrastructure. Growth drivers include increasing internet penetration, rising smartphone adoption, and evolving consumer preferences for convenient shopping options. The distribution channel has implemented advanced product information systems and educational frameworks that deliver comprehensive insights regarding organic formulations, ingredient efficacy, and certification standards.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific accounts for 41.48% of the organic and natural personal care market in 2024 and is projected to grow at a 6.34% CAGR from 2025 to 2030. The region's market dominance is driven by increasing disposable incomes, growing health consciousness, and traditional skincare practices in Japan, South Korea, and China. Shiseido's launch of the "ANESSA Sunshine Project" across 12 Asian countries in May 2024 highlights the region's importance. The company's "Mirai Shift NIPPON 2025" strategy emphasizes sustainable growth, profitability, and human capital development through technology and Research and Development investments.

North America continues its market growth, with consumers seeking transparency in ingredient sourcing and sustainability practices. The United States Department of Agriculture (USDA)'s Strengthening Organic Enforcement (SOE) rule, implemented on March 19, 2024, introduces major changes to the National Organic Program (NOP). These include expanded certification requirements for brokers and traders, mandatory NOP Import Certificates for organic imports, and enhanced supply chain traceability measures to prevent fraud.

Europe strengthens its market position through robust regulatory frameworks and growing consumer awareness of sustainability. The Soil Association's 2023 report reveals that organic health and beauty product sales in the UK reached GBP 136 million, driven by environmental consciousness, strict certification standards, and expanded organic retail channels. South America, the Middle East, and Africa offer growth potential, with the Middle East showing rising demand for natural personal care products due to a preference for organic over synthetic ingredients.

Competitive Landscape

The organic skin care products market exhibits a fragmented competitive structure, characterized by the presence of multinational corporations, specialized natural brands, and new market entrants. The competitive environment is marked by strategic initiatives from established companies such as L'Oréal S.A., The Estée Lauder Companies Inc., Shiseido Company, Limited, and Natura & Co., which maintains its market positions through continuous portfolio expansion in the organic segment.

These industry leaders implement comprehensive research and development programs, leveraging their substantial technical capabilities and economies of scale to address complex formulation challenges in natural products. Their competitive advantage stems from established distribution networks, brand recognition, and significant investment capabilities in product innovation and market expansion.

The market presents considerable opportunities in specialized segments, particularly in products for sensitive skin, multicultural beauty, and age-specific formulations. Small and emerging brands successfully capture market share by focusing on these niche segments while emphasizing sustainability credentials and ingredient transparency. The competitive landscape continues to evolve with the increasing adoption of direct-to-consumer business models, enabling emerging brands to establish direct consumer relationships through digital channels, circumventing traditional retail distribution networks.

Organic Skin Care Products Industry Leaders

-

L'Oréal S.A.

-

The Estée Lauder Companies Inc.

-

Shiseido Company, Limited

-

Natura & Co

-

Weleda AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Natural Grocers, an organic and natural grocery retailer, introduced a new house brand skincare collection. The product line includes body washes, scrubs, butters, and body creams manufactured in small batches with selected ingredients to ensure quality and effectiveness.

- March 2025: Weleda AG, a natural skincare company with certified products, collaborated with Princess Madeleine Bernadotte to develop minLen, a natural skincare brand.

- February 2025: Organic skincare company Puddles introduced a skincare range for teenagers. The product line features plant-based ingredients with scientific validation, targeting common teenage skin concerns, including acne, while providing gentle and effective skincare solutions.

- September 2024: Dr. Squatch introduced a natural body wash that incorporates the properties of its cold-processed bar soap. The body wash contains more than 98% natural ingredients, including coconut-derived components that hydrate and maintain skin moisture throughout the day.

Global Organic Skin Care Products Market Report Scope

Organic skincare products contain ingredients grown without pesticides through organic farming methods.

The organic skincare products market segments include product type, category, distribution channel, and geography. The product type segment comprises facial care (cleansers, moisturizers, oils/serums, and other facial care products), body care (lotions, body wash, and other body care products), and lip care. The category segment divides into premium and mass products. Distribution channels include supermarkets/hypermarkets, specialty retail stores, online retail stores, and other channels. Geographically, the market covers North America, South America, Europe, Asia-Pacific, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| By Product Type | Facial Care | Cleansers | |

| Moisturizers and Oils/Serums | |||

| Other Facial Care Product | |||

| Body Care | Body Lotions | ||

| Body Wash | |||

| Other Body Care Products | |||

| Lip Care | |||

| By Category | Premium Products | ||

| Mass Products | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Specialty Stores | |||

| Online Retail Stores | |||

| Others Distribution Channel | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

| Facial Care | Cleansers |

| Moisturizers and Oils/Serums | |

| Other Facial Care Product | |

| Body Care | Body Lotions |

| Body Wash | |

| Other Body Care Products | |

| Lip Care |

| Premium Products |

| Mass Products |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Others Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current size of the organic and natural personal care products market?

The market stands at USD 47.7 billion in 2025 and is projected to rise to USD 61.7 billion by 2030 at a 5.29% CAGR.

Which region is the fastest-growing for organic and natural personal care products?

Asia-Pacific leads with a 6.34% CAGR forecast for 2025-2030, supported by higher disposable incomes and entrenched skincare routines.

Which product segment dominates revenue today?

Facial care controls 76.44% of 2024 revenue due to heightened interest in microbiome-friendly and anti-aging formulas.

How important are online channels to future growth?

Online retail is the fastest channel, slated for a 6.11% CAGR as immersive tech like tactile simulation reduces the need for in-store trials.

Page last updated on: July 8, 2025