Green Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

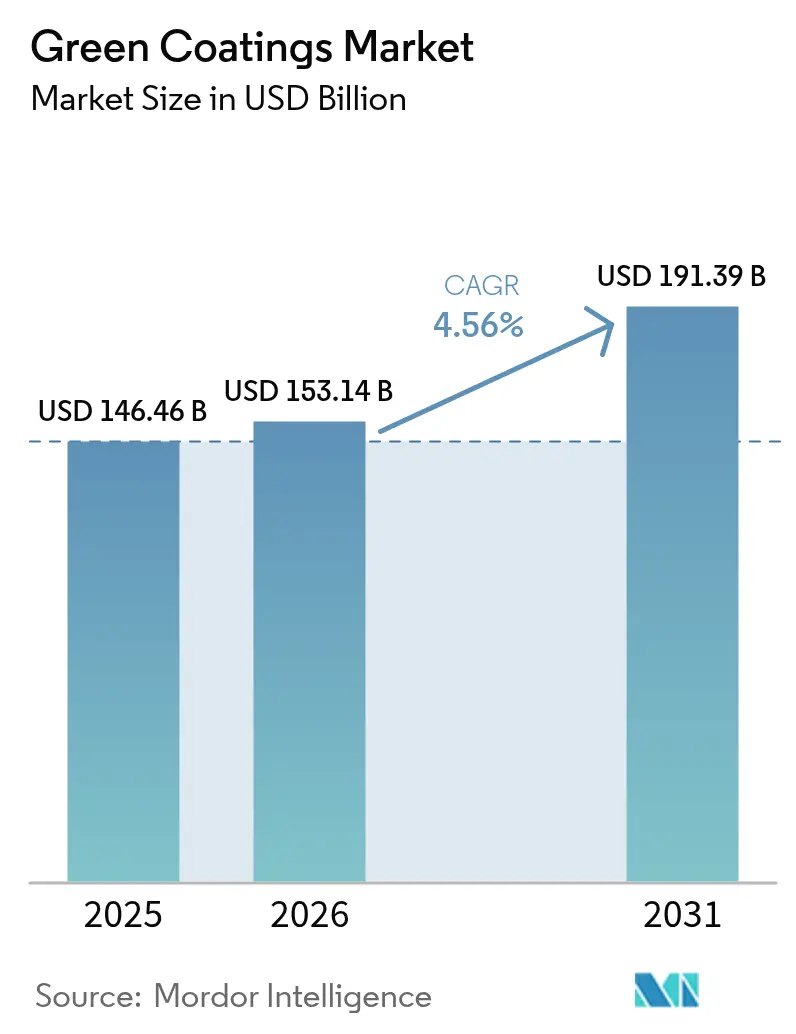

| Market Size (2026) | USD 153.14 Billion |

| Market Size (2031) | USD 191.39 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

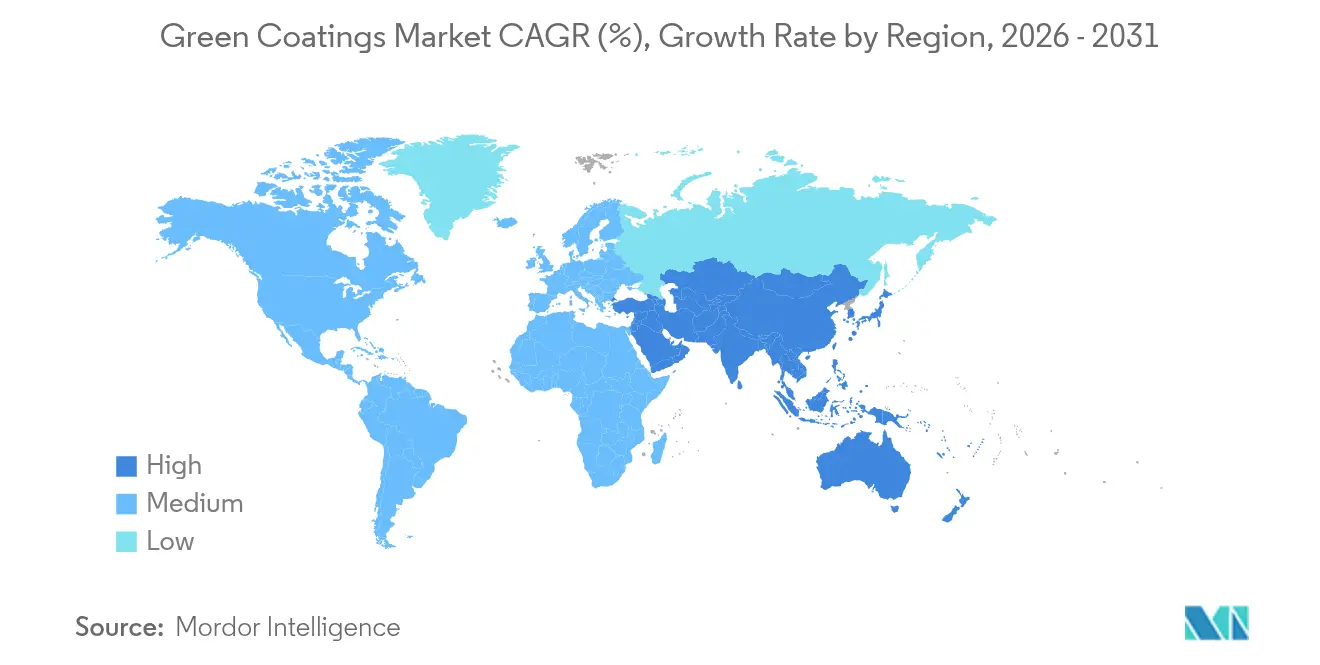

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

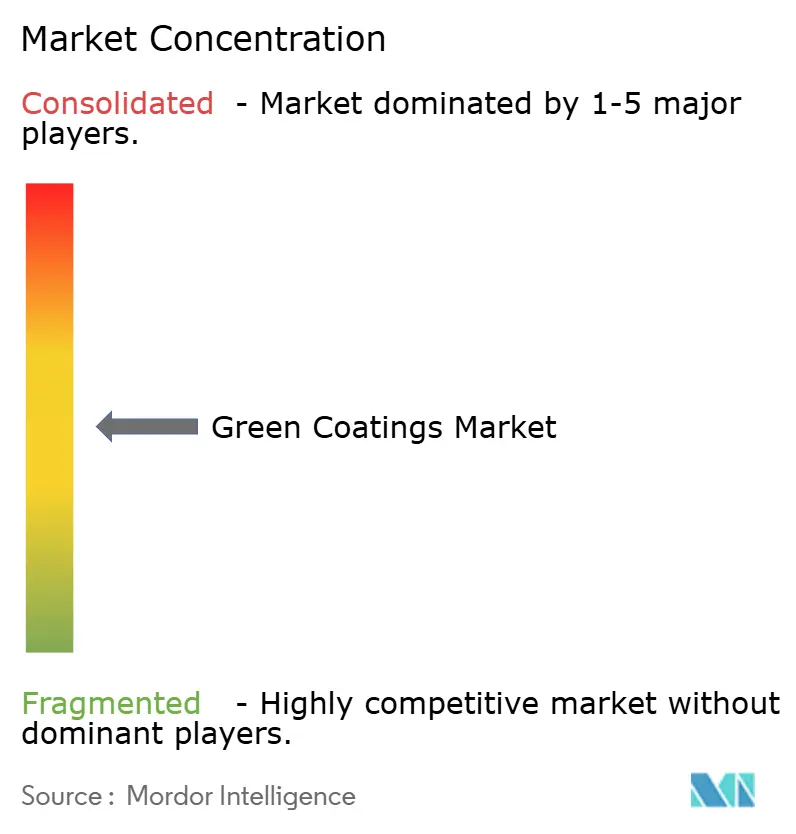

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green Coatings Market Analysis by Mordor Intelligence

The green coatings market size is expected to grow from USD 146.46 billion in 2025 to USD 153.14 billion in 2026 and is forecast to reach USD 191.39 billion by 2031 at 4.56% CAGR over 2026-2031. Regulatory pressure that tightens limits on volatile organic compounds (VOC), rapid progress in water-borne chemistries and powder technologies, and higher penetration in automotive and architectural uses remain the central growth engines of the green coating market. California’s South Coast Air Quality Management District has already cut allowable VOC content in automotive refinish products under amended Rule 1151 and will enforce even stricter levels by 2033. In parallel, the European Union will prohibit per- and polyfluoroalkyl substances (PFAS) in food-contact packaging from August 2026, redirecting packaging formulators toward bio-based barriers. OEMs seeking lower energy paint shops and builders pursuing green certifications are expanding the addressable pool for sustainable solutions, while technology that lifts the durability of water-based resins now rivals solvent-borne systems.

Key Report Takeaways

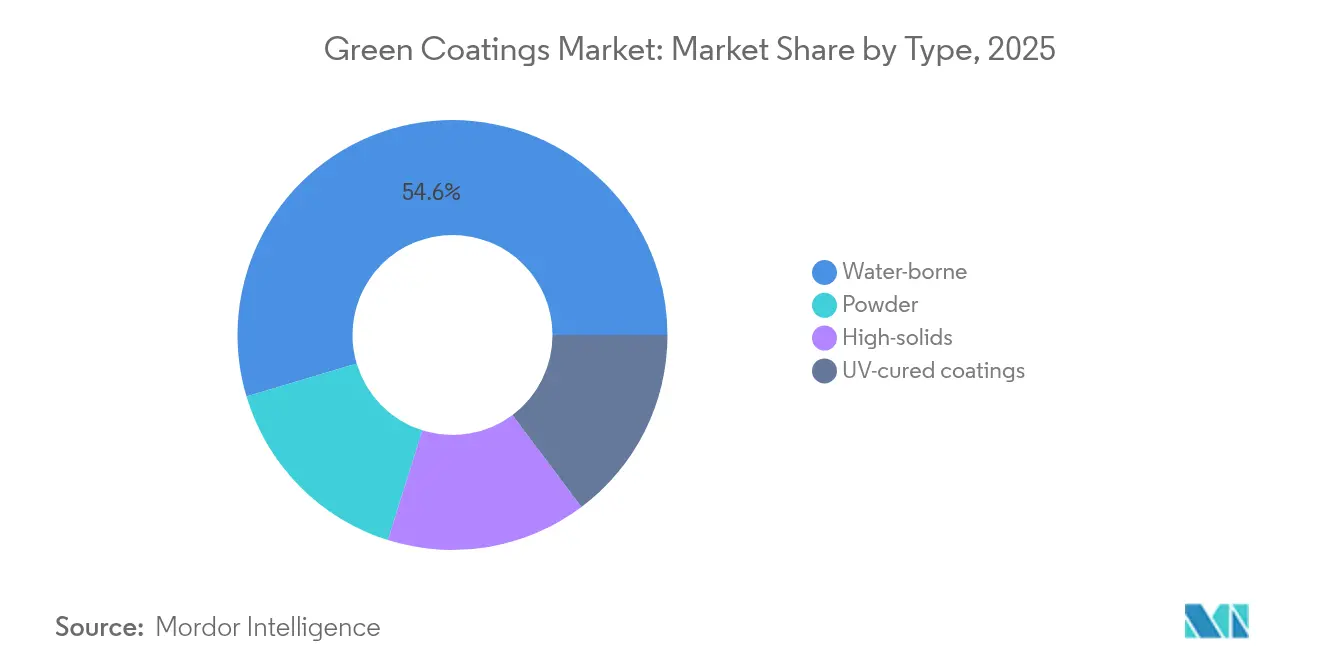

- By type, water-based coatings led with 54.62% revenue share in 2025, whereas powder coatings are projected to post a 6.18% CAGR through 2031, remaining the fastest-growing sub-category.

- By application, architectural coatings accounted for 48.21% of 2025 revenue; packaging coatings are set to expand at 6.1% CAGR through 2031.

- By geography, Asia-Pacific commanded 43.68% of 2025 revenue and is also the quickest-advancing region at 5.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Green Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental regulations on VOC emissions | +1.8% | Global, with California and EU leading | Medium term (2-4 years) |

| Growing demand for low-VOC architectural coatings | +1.2% | North America & EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Automotive OEM shift toward energy-efficient paint shops | +0.9% | Global, concentrated in automotive manufacturing hubs | Medium term (2-4 years) |

| Advances in water-based resin chemistry enhancing durability | +0.7% | Global | Long term (≥ 4 years) |

| Adoption of bio-based resins from agricultural waste | +0.6% | Global, with early gains in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Regulations on VOC Emissions

New VOC limits are redefining acceptable formulation windows for the green coating market. South Coast AQMD’s Rule 1151 phases in lower VOC ceilings for automotive refinish products beginning May 2025 and culminates in the strictest thresholds by 2033, pushing body shops toward water-borne systems[1]South Coast Air Quality Management District, “Rule 1151 – Motor Vehicle and Mobile Equipment Coating Operations,” aqmd.gov. On another front, the EU Packaging and Packaging Waste Regulation caps PFAS at 25 ppb per individual substance and 250 ppb total, steering packaging suppliers to bio-based coatings that avoid fluorinated chemistries[2]European Commission, “Regulation on Packaging and Packaging Waste,” eur-lex.europa.eu . Businesses already holding portfolios of compliant products gain a first-mover advantage, whereas producers tied to legacy solvent-borne lines face incremental compliance cost and potential market exclusion.

Growing Demand for Low-VOC Architectural Coatings

Home repairs, commercial retrofits, and green-building standards continue to draw the construction value chain toward low-VOC alternatives. Sherwin-Williams reports a noticeable shift in residential repaint orders toward paints designed for easy recycling and lower embodied carbon[3]Sherwin-Williams, “Sustainability Report 2025,” sherwin-williams.com. Water-borne formulations now deliver the same gloss retention and scrub resistance as solvent-borne equivalents. AkzoNobel’s RUBBOL WF 3350 exemplifies this transition, pairing 20% bio-based content with warranty-backed durability in indoor and outdoor wood finishes.

Automotive OEM Shift Toward Energy-Efficient Paint Shops

Vehicle makers are updating paint lines to curb operating expenditure and future-proof against carbon tariffs. General Motors’ three-wet process omits the primer-bake stage, trimming 50% of paint-booth energy per car and avoiding 80,000 t of greenhouse gases annually. Joint programs between PPG and the U.S. Department of Energy explore multi-layer systems that cure at lower temperatures, unlocking further gains for water-borne topcoats.

Advances in Water-Based Resin Chemistry Enhancing Durability

Research in self-crosslinking acrylics and bio-epoxies is closing the historical performance gap with solvent lines. Mazda’s Aqua-tech paint technology, for instance, cuts plant VOC emissions 57% yet keeps premium-grade finish quality. New water-borne latex platforms reach salt-spray corrosion resistance comparable to legacy alkyds, expanding their use to industrial machinery coatings often exposed to moisture and abrasion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance gaps versus solvent-borne in harsh environments | -0.8% | Global, particularly in marine and industrial applications | Medium term (2-4 years) |

| Higher total applied cost for end-users | -0.6% | Global, with greater impact in price-sensitive markets | Short term (≤ 2 years) |

| Supply constraints of bio-based feedstocks | -0.4% | Global, with acute impact in regions dependent on imports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Performance Gaps Versus Solvent-Borne in Harsh Environments

Marine hulls, offshore platforms, and chemical storage tanks still demand the long-term fouling resistance and barrier strength of high-solids epoxies rich in solvents. Although self-healing siloxane hybrids and chrome-free inhibitors are emerging, their commercial adoption is gradual because certification cycles are lengthy and shipowners resist untested chemistries.

Higher Total Applied Cost for End-Users

Even as raw VOC-free ingredients fall in price, the installed cost of a water-borne or bio-based system can remain 5–15% higher once extended flash-off or specialized spray equipment is factored in. This differential narrows when operations internalize lower insurance premiums tied to reduced fire risk and when local incentives discount greener materials, yet it persists in cost-sensitive geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Powder Coatings Lead Innovation Drive

Water-borne systems preserved leadership in 2025 with a 54.62% share of the green coating market. Their dominance is rooted in favorable compliance footprints and constant resin upgrades that yield mechanical strength on par with solvent-borne counterparts. Mazda’s plant-wide switch to advanced water-based topcoats alone lowered VOC output by 57% while retaining showroom-grade gloss. Powder coatings, however, offer the most rapid trajectory, advancing at 6.18% CAGR to 2031. Catalyst-assisted infrared ovens now cure thick films in just 2–3 minutes at roughly 225 °C, elevating production throughput and slashing utility bills. Sherwin-Williams’ Powdura ECO illustrates circular design, embedding every pound of powder with recycled PET equal to sixteen half-liter bottles. The green coating market size for powder lines is projected to expand in tandem with low-temperature formulations that harden at 150 °C, opening doors to heat-sensitive plastics and MDF furniture. Meanwhile, UV-curable liquids occupy specialized niches in electronics where near-instant cure is mandatory.

The green coating industry also benefits from higher-solids alkyd and acrylic hybrids. These systems cut the solvent fraction below 250 g/L without sacrificing wet edge or adhesion to metallic substrates. Collectively, such variants reinforce the perception that sustainable chemistries can meet or exceed conventional benchmarks.

By Application: Packaging Drives Sustainability Transition

Architectural paints captured 48.21% of green coating market share in 2025, propelled by construction rebounds and stricter indoor-air credit thresholds within LEED, BREEAM, and WELL frameworks. Formulators migrate toward water-borne emulsions featuring bio-solvents and renewable pigments, exemplified by AkzoNobel’s 20% bio-based wood-care line. Demand is especially resilient in the U.S. repaint segment, where homeowners favor low-odor options for occupied dwellings. Packaging coatings, on the other hand, are scaling fastest at 6.1% CAGR, pushed by EU PFAS bans and rising consumer scrutiny of food-contact safety. This segment alone is expected to enlarge the green coating market size by an incremental USD 6.3 billion between 2026 and 2031, buoyed by edible polysaccharide films that extend shelf life while maintaining compostability.

Industrial coatings, from oil-field equipment to heavy-duty trucks, converge on self-healing and anti-scratch additives that extend maintenance intervals. Automotive clearcoats harness nanoceramic dispersions to resist micro-marring, aligning with multi-coat wet-on-wet processes that pare down oven stages. Wood, electronics, and specialized sectors remain secondary yet critical adopters, turning to niche chemistries such as lignin-based binders and halogen-free flame retardants to address unique functional gaps.

Geography Analysis

Asia-Pacific confirmed its dominance with 43.68% of 2025 revenue while charting the fastest 5.42% CAGR through 2031. Indonesian output surpassed 1 million tons in 2024, with waterborne decorative paints taking a striking 67% share of local production. The region’s green coating market is further stimulated by China’s express-packaging law GB 43352-2023 that forces e-commerce warehouses to switch to compliant coatings. India’s move to tighten food-container rules under the Food Safety and Standards Authority (FSSAI) also underpins demand. Continued urbanization, automotive build-outs, and foreign direct investment into OEM paint shops present long-run momentum.

North America enjoys a resilient path powered by California’s VOC benchmarks and robust residential repaint cycles. General Motors’ three-wet technique underscores the competitive edge of low-energy lines, and multiple Tier 1 suppliers pivot to water-borne primers that simplify color changeover. Canada mirrors this progress through appliance manufacturers investing in powder booths, whereas Mexico’s coil-coating capacity staking USD 3.6 million in upgrades provides the region a cost-efficient supply hub.

Europe remains a heavyweight courtesy of sweeping PFAS restrictions and carbon-border considerations that motivate rapid reformulation. Member states impose antidumping duties on high-solvent titanium dioxide imports, indirectly steering formulators toward lower-solids or water-borne routes that require less pigment. Germany and France continue to incubate bio-based resin start-ups, fostering technical collaborations with existing conglomerates.

Emerging geographies in South America, the Middle East, and Africa post moderate yet accelerating uptake. Brazil’s industrial output and Saudi Arabia’s Vision 2030 mega-projects heighten the relevance of sustainable coatings in protective steelwork and decorative lines. However, fragmented regulatory enforcement and limited access to renewable feedstocks temper pace in several local markets.

Competitive Landscape

The green coatings market exhibits moderate fragmentation. PPG’s USD 550 million carve-out of its non-core architectural line was followed by Nippon Paint’s USD 2.3 billion purchase of AOC, signaling an appetite for assets that strengthen sustainable offerings. ALTANA’s investment in Finnish fire-retardant specialist NORDTREAT underscores the strategic value of bio-based additives.

Technological leadership focuses on one-coat direct-to-metal water-borne solutions, self-healing topcoats, and microwave-curable powders that cut curing cycles to under 90 seconds. Firms with integrated resin-to-colorant chains wield better control over feedstock security, critical as bio-based monomers still face supply and price volatility.

Digital tools accelerate innovation, from high-throughput formulation platforms that screen thousands of resin-pigment combinations to AI-enabled in-line color monitoring that reduces rework. Cost leadership alone no longer suffices; customers evaluate lifecycle emissions, recycled content rates, and energy savings across the coating’s use phase.

Green Coatings Industry Leaders

AkzoNobel N.V.

The Sherwin Williams Company

PPG Industries Inc.

Axalta Coating Systems, LLC

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PPG launched ENVIROLUXE Plus powder coatings containing up to 18% post-industrial recycled PET and no PFAS, broadening substrate compatibility while matching legacy performance.

- February 2025: AkzoNobel introduced RUBBOL WF 3350 water-borne wood coating with 20% bio-based content, combining circularity goals with warranty-backed durability.

Global Green Coatings Market Report Scope

The green coatings market report includes:

| Water-borne |

| Powder |

| High-solids |

| UV-cured coatings |

| Architectural Coatings |

| Industrial Coatings |

| Automotive Coatings |

| Wood Coatings |

| Packaging Coatings |

| Other Applications (Electronics and Electrical Coatings, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Water-borne | |

| Powder | ||

| High-solids | ||

| UV-cured coatings | ||

| By Application | Architectural Coatings | |

| Industrial Coatings | ||

| Automotive Coatings | ||

| Wood Coatings | ||

| Packaging Coatings | ||

| Other Applications (Electronics and Electrical Coatings, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Green Coatings Market size?

The green coating market is valued at USD 153.14 billion in 2026 and is projected to reach USD 191.39 billion by 2031.

Which segment leads in revenue within the green coating market?

Water-based coatings dominate with 54.62% of 2025 revenue.

Which application is growing fastest?

Packaging coatings record the highest CAGR at 6.1% through 2031.

Why is Asia-Pacific pivotal for growth?

The region commands 43.68% of revenue and benefits from stringent regulations and manufacturing expansion, enabling a 5.42% CAGR.

Page last updated on: