Global Photodynamic Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.48 Billion |

| Market Size (2031) | USD 7.79 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Photodynamic Therapy Market Analysis by Mordor Intelligence

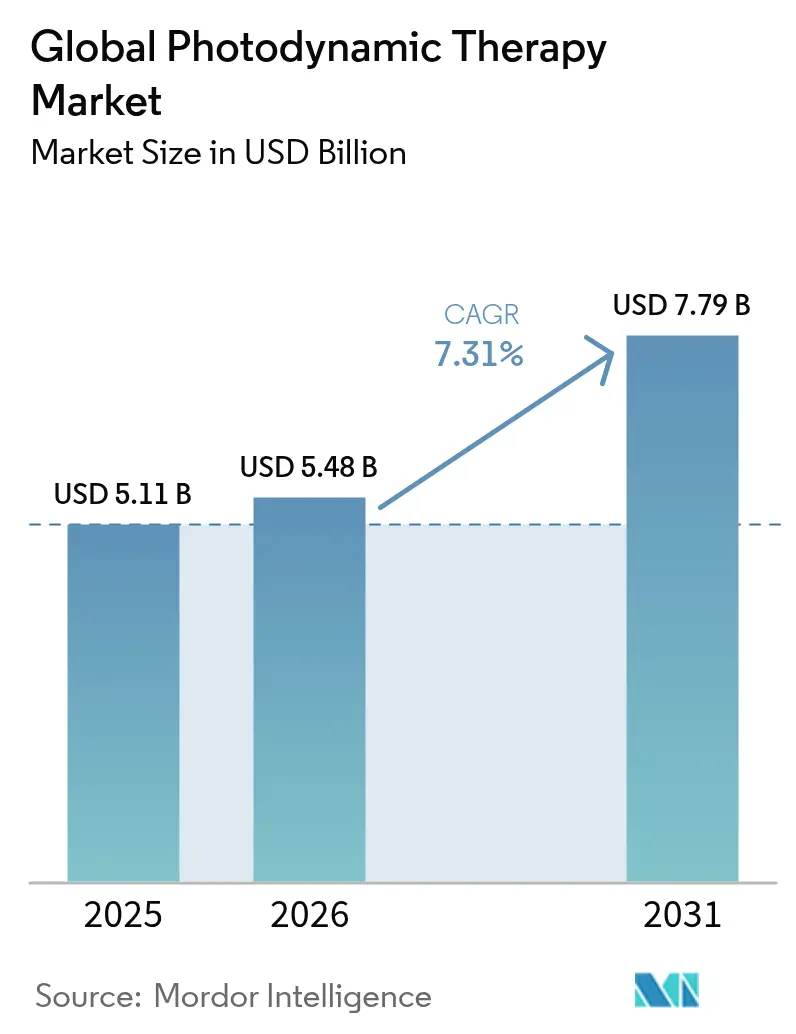

The photodynamic therapy market size in 2026 is estimated at USD 5.48 billion, growing from 2025 value of USD 5.11 billion with 2031 projections showing USD 7.79 billion, growing at 7.31% CAGR over 2026-2031. Wider clinical acceptance across dermatology, ophthalmology, and antimicrobial care underpins this trajectory. The FDA clearance of LumiThera’s Valeda system for dry age-related macular degeneration in November 2024 signaled the therapy’s expansion beyond oncological roots, while Biofrontera’s RhodoLED XL lamp illustrates parallel device innovation fda.gov. Growing reimbursement for actinic keratosis, falling LED array prices, and rising demand for fertility-preserving cervical cancer options further lift the photodynamic therapy market. At the same time, capital constraints for small practices and patient photosensitivity concerns temper the pace of adoption.

Key Report Takeaways

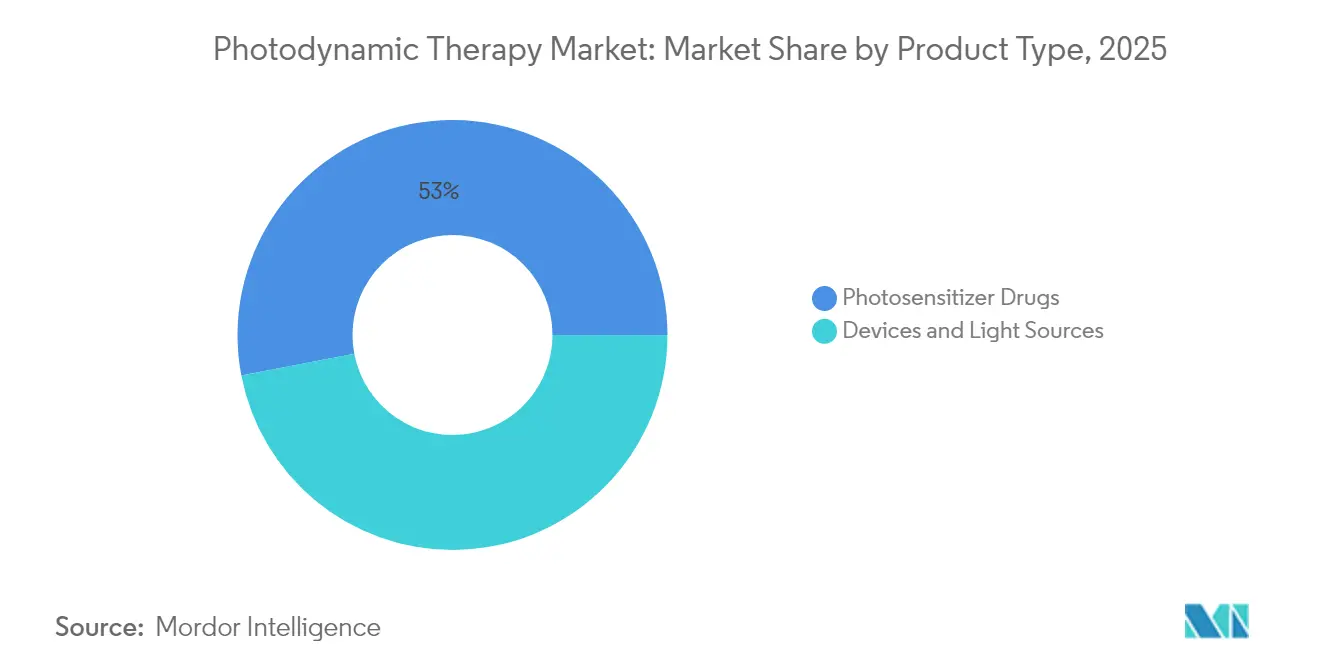

- By product type: Photosensitizer drugs held 53.02% of photodynamic therapy market share in 2025; LED-based light sources are forecast to grow at an 8.02% CAGR through 2031.

- By application: Oncology captured 48.12% photodynamic therapy market share in 2025, while dermatology non-oncology uses are set to expand at a 9.08% CAGR to 2031.

- By end user: Hospitals accounted for 59.72% of the photodynamic therapy market size in 2025; ambulatory surgical centers are projected to rise at an 8.39% CAGR to 2031.

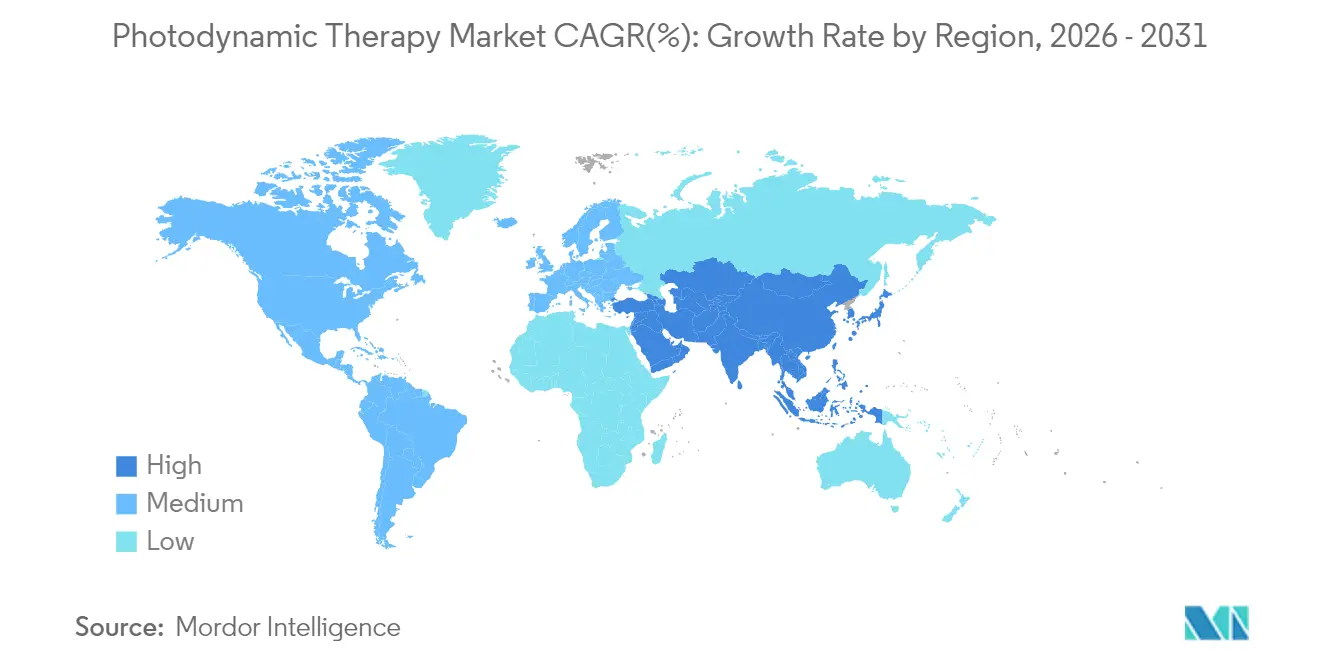

- By geography: North America led with 41.88% revenue share in 2025; Asia-Pacific is forecast to register the fastest 8.74% CAGR between 2026 and 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Photodynamic Therapy Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of non-melanoma skin cancer | +1.8% | Global, with concentration in North America & Australia | Long term (≥ 4 years) |

| Regulatory approvals of next-generation photosensitizers | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expanding reimbursement for actinic keratosis treatment | +0.9% | North America & select EU markets | Short term (≤ 2 years) |

| Cost decline in diode laser & LED light sources | +0.7% | Global, with manufacturing concentration in Asia | Medium term (2-4 years) |

| Daylight-PDT deployment in primary care settings | +0.5% | EU & North America, pilot programs in APAC | Long term (≥ 4 years) |

| AI-guided real-time dosimetry optimization | +0.4% | North America & select EU centers | Long term |

| Source: Mordor Intelligence | |||

Rising Incidence of Non-Melanoma Skin Cancer

Basal and squamous cell carcinoma prevalence is pushing clinicians toward less invasive care options with superior cosmetic outcomes. Photodynamic therapy can achieve 90% complete clearance in superficial basal cell carcinoma while avoiding tissue loss, which appeals to patients with lesions on cosmetically sensitive areas. Organ-transplant recipients and Gorlin syndrome patients benefit from repeatable, non-scarring treatments, creating steady demand in specialist centers. As field cancerization prevention gains traction, proactive protocols amplify procedure volumes across dermatology networks.

Regulatory Approvals of Next-Generation Photosensitizers

The FDA’s flexible review standards have shortened approval cycles for advanced nano-formulations that cut photosensitivity duration without sacrificing depth of action. Biofrontera’s larger Ameluz dose authorization demonstrates regulators’ willingness to support broader lesion coverage. Natural agents[1]Source: David Aebisher et al., “Natural Photosensitizers in Clinical Trials,” Applied Sciences, mdpi.com such as hypericin and curcumin move through late-stage trials, promising lower manufacturing costs that could open price-sensitive markets across Asia-Pacific.

Expanding Reimbursement for Actinic Keratosis Treatment

Dedicated CPT codes and positive coverage determinations allow dermatology clinics to embed PDT into routine care. Blue Cross Blue Shield policies now deem the therapy medically necessary under defined criteria, raising utilization rates in outpatient settings. CMS coverage for verteporfin in ocular PDT sets a precedent for future non-oncology reimbursements, reinforcing the photodynamic therapy market’s revenue stability.

Cost Decline in Diode Laser & LED Light Sources

LED arrays now deliver comparable outcomes to lasers while trimming equipment prices by roughly 60%, boosting affordability for small practices. Portable platforms under investigation suggest home-supervised protocols are plausible, potentially transforming care delivery. Manufacturing scale in East Asia further drives down unit costs, widening global access to the photodynamic therapy market.

Restraint Impact Analysis*

| Restarint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of PDT laser equipment | -1.1% | Global, particularly affecting smaller practices | Medium term (2-4 years) |

| Patient non-compliance due to prolonged photosensitivity | -0.8% | Global, with higher impact in sunny climates | Short term (≤ 2 years) |

| Limited reimbursement for non-oncology indications | -0.6% | North America & EU, expanding coverage gaps | Medium term (2-4 years) |

| Cold-chain gaps for liposomal photosensitizer drugs | -0.4% | Global, with acute impact in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of PDT Laser Equipment

Initial outlays of USD 50,000–150,000 limit adoption among independent dermatologists, who comprise the bulk of potential sites. Leasing programs ease cash burdens but compress margins and spark obsolescence fears amid rapid device refresh cycles. Until lower-priced LED systems reach parity in all indications, the photodynamic therapy market may struggle to penetrate community practices at scale.

Patient Non-Compliance Due to Prolonged Photosensitivity

Traditional agents can impose up to 48 hours of strict light avoidance, discouraging completion of multi-session regimens, especially in equatorial regions with intense sunlight. Daylight-mediated protocols lessen discomfort but rely on weather conditions, adding scheduling complexity. Education requirements raise staff workload, nudging some providers toward competing modalities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Photosensitizer Drugs Drive Innovation

Photosensitizer drugs dominated revenue with 53.02% share in 2025 and are expected to advance at an 7.85% CAGR through 2031. Third-generation formulations employing nanoparticle carriers improve tumor selectivity and shave photosensitivity windows, reinforcing leadership of this segment within the photodynamic therapy market size. Natural agents in late-stage trials may cut production expenses, supporting broader payer adoption and regional market entry in Asia-Pacific.

In contrast, light sources are evolving toward high-output LEDs that decrease procedure time and improve patient comfort. FDA clearance of the RhodoLED XL lamp, which covers wider treatment fields, indicates the pace of device innovation. AI-enabled dosimetry modules now refine fluence delivery in real time, allowing clinicians to tailor sessions, reduce retreatments, and elevate outcomes across the photodynamic therapy market.

By Application: Oncology Leadership with Emerging Diversification

Cancer care retained 48.12% share in 2025, and therapeutic expansion in cervical, head-and-neck, and bladder cancers underpins a segment CAGR of 7.77% to 2031. Superficial basal cell carcinoma remains a high-volume anchor, yet fertility-preserving cervical protocols achieving 94.79% regression broaden the treated population, adding resilience to the photodynamic therapy market.

Dermatology non-oncology indications such as acne benefit from standardized Chinese guidelines, while ophthalmology entered commercial use after Valeda gained FDA approval. Chronic wound and antimicrobial studies position PDT for longer-range diversification, embedding multi-disciplinary relevance throughout the photodynamic therapy industry.

By End User: Hospital Dominance with ASC Growth

Hospitals controlled 59.72% of revenue in 2025 owing to complex case management capabilities and capital budgets that accommodate sophisticated devices, cementing their role as foundational purchasers within the photodynamic therapy market. Multi-modal oncology pathways inside tertiary centers integrate PDT alongside surgery or radiation, cementing patient flow and equipment utilization.

Ambulatory surgical centers, however, are predicted to deliver the fastest 8.39% CAGR, leveraging outpatient efficiencies and lower overheads. The move toward same-day discharge aligns with payer pressures for cost containment, signaling sustained decentralization across the photodynamic therapy market size by decade’s end.

Geography Analysis

North America commanded 41.88% of global sales in 2025 as favorable reimbursement and the world’s highest skin cancer incidence sustained steady procedural volumes. Multiple FDA clearances in 2024, including Valeda for dry AMD, reinforced clinical confidence while Medicare coverage removed cost barriers modernretina.com. Provincial health agencies such as Alberta’s technology assessment office confirm PDT’s cost-effectiveness, hinting at future funding expansions across Canada open.alberta.ca. Cross-border medical tourism from Mexico adds incremental demand at specialized U.S. centers, solidifying the photodynamic therapy market’s regional base.

Asia-Pacific is projected to post a rapid 8.74% CAGR between 2026 and 2031. China’s December 2024 expert consensus on aminolevulinic acid established unified protocols that lower clinical adoption friction . Japan’s aging population fuels macular degeneration procedures, and its stringent device standards boost trust in locally cleared systems. South Korea’s export-oriented medical device sector offers cost-competitive LED units, enhancing affordability for regional providers. India’s large unmet oncologic need presents a long-range opportunity once infrastructure and reimbursement frameworks mature, adding depth to the photodynamic therapy market.

Europe sustains moderate growth under harmonized device regulations that simplify multi-country launches. Daylight-PDT, pioneered in Nordic clinics, addresses photosensitivity compliance and now spreads across Mediterranean nations. Germany and the United Kingdom operate flagship academic programs that test nano-formulations and AI dosimetry, strengthening evidence for broader reimbursement. Cosmetic outcome priorities resonate with PDT’s tissue-sparing profile, driving steady referrals for facial lesion management and reinforcing the photodynamic therapy market’s resilience across the continent.

Competitive Landscape

The photodynamic therapy market shows moderate fragmentation as established pharmaceutical firms acquire niche innovators to secure next-generation assets. Sun Pharmaceutical’s USD 355 million purchase of Checkpoint Therapeutics in March 2025 expands its onco-dermatology pipeline and adds an FDA-approved agent for metastatic cutaneous squamous cell carcinoma. Vertical integration models that pair proprietary photosensitizers with dedicated light systems lock in recurring consumable revenue and raise switching barriers for hospitals.

Product differentiation centers on targeted nano-formulations and AI-guided dosimetry. Biofrontera’s 2024 revenue reached USD 37.3 million, supported by proprietary device-drug combinations, though a net loss of USD 17.8 million underscores heavy R&D and commercialization costs. Theralase pursues bladder cancer with Ruvidar, reporting multi-year responses that could command premium pricing upon approval. Meanwhile, East-Asian LED makers supply cost-effective hardware, intensifying price competition but expanding the global photodynamic therapy market base.

Patent cliffs for first-generation porphyrin agents fuel urgency to launch differentiated drugs before generic erosion compresses margins. Strategic alliances with AI firms aim to automate treatment planning, promising throughput gains for outpatient centers. Across regions, market leaders invest in payer education to solidify reimbursement pathways and de-risk uptake of new indications, stabilizing cash flows even as the photodynamic therapy industry advances into less familiar therapeutic territories.

Global Photodynamic Therapy Industry Leaders

BIOFRONTERA AG

Lumibird (Quantel Medical)

Sun Pharmaceutical Industries Limited

Galderma S.A.

Bausch Health Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sun Pharmaceutical Industries agreed to acquire Checkpoint Therapeutics for USD 355 million, strengthening its onco-dermatology portfolio.

- November 2024: FDA authorized marketing of LumiThera’s Valeda Light Delivery System for dry AMD after trials showed 58% of treated eyes gained ≥5 letters in visual acuity.

- October 2024: FDA approved raising Ameluz dosage to 3 tubes per actinic keratosis treatment, enabling larger lesion coverage

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the photodynamic therapy market as the global sales value of approved photosensitizer drugs together with the lasers, LEDs, fiber-optic catheters, and integrated kits that clinicians deploy to activate those agents across oncology, dermatology, ophthalmology, and emerging antimicrobial settings.

Stand-alone fluorescence imaging devices and purely cosmetic light panels are kept outside the value pool.

Segmentation Overview

- By Product Type

- Photosensitizer Drugs

- First Generation

- Second Generation

- Third-generation / targeted nano Generation / Targeted Nano

- Devices & Light Sources

- Diode Lasers

- LED Array

- Lamps Other

- Photosensitizer Drugs

- By Application

- Oncology

- Non Melanoma Skin cancer

- Actinic Keratosis

- Head & Neck / Oral Cavity Cancer

- Lung & Esophageal Cancer

- Dermatology

- Ophthalmology

- Actimicrobial/Aesthetics

- Oncology

- By End-User (Value)

- Hospitals

- Dermatology & Skin-Cancer Clinics

- Ambulatory Surgical Centers

- Research & Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple semi-structured interviews with dermatologists, radiation oncologists, purchasing managers, and photosensitizer chemists across North America, Europe, and Asia let us validate treatment volumes, price corridors, and learning-curve uptake. These discussions also clarified off-label growth pockets and plausible reimbursement lags that secondary sources seldom capture.

Desk Research

We began by mapping therapy adoption and reimbursement codes using open data from the FDA 510(k)/PMA database, EMA CE-mark dossiers, and ClinicalTrials.gov trial pipelines, which helped us confirm the current generation of drugs, light sources, and indications. Global incidence files from WHO Cancer Observatory, actinic keratosis prevalence surveys by the American Academy of Dermatology, and import-export entries in UN Comtrade provided baseline demand signals. Our team then extracted unit shipments and average selling prices from hospital charge masters, SEC 10-Ks, and investor decks, and supplemented revenue splits with D&B Hoovers and Dow Jones Factiva snapshots. The sources listed are illustrative; many other public publications guided data gathering and sense-checks.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-patient build linked cancer and skin-lesion incidence with therapy penetration, which is then reconciled with selective bottom-up supplier roll-ups and channel checks (our single mention of the top-down and bottom-up blend). Key variables include lesion prevalence by stage, photosensitizer dose per procedure, light-device replacement cycles, regional reimbursement rates, and ASP erosion trends. Multivariate regression anchored on cancer incidence CAGR, dermatology clinic expansion, and LED cost curves projects values through 2030, while scenario analysis stress tests high and low adoption paths.

Data Validation & Update Cycle

Outputs run through variance flags versus independent metrics such as Medicare procedure counts and trade shipment spikes. Senior analysts review anomalies, request clarifications from interviewees, and sign off only when gaps close. We refresh every twelve months and trigger interim updates for regulatory approvals or large tender wins, ensuring clients see the latest baseline each time.

Why Mordor's Photodynamic Therapy Baseline Is Consistently Trusted

Published estimates often diverge because firms choose different product mixes, regional cuts, and forecast cadences. Buyers need clarity on why one figure reads billions higher than another.

Key gap drivers include exclusion of ophthalmic and antimicrobial indications, device-only tallies, unvetted ASP assumptions, or bi-annual refreshes that miss fast FDA approvals. By capturing the full drug-device ecosystem, applying verified price bands, and updating annually, Mordor Intelligence presents a balanced, decision-ready number.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.11 B (2025) | Mordor Intelligence | - |

| USD 4.58 B (2024) | Global Consultancy A | Omits antimicrobial and ophthalmic uses; single global price band |

| USD 1.90 B (2024) | Trade Journal B | Counts device sales only; mixes procedure fees with product revenue |

| USD 4.80 B (2024) | Industry Insights C | Limited country set; fixed FX rates; bi-annual refresh |

These comparisons show that when scope, variables, and refresh discipline differ, totals shift markedly. Our disciplined framing, transparent inputs, and yearly updates give decision-makers a dependable starting point.

Key Questions Answered in the Report

How large is the photodynamic therapy market in 2026?

The photodynamic therapy market size stands at USD 5.48 billion in 2026 and is on track to reach USD 7.79 billion by 2031 at a 7.31% CAGR.

Which segment leads the photodynamic therapy market?

Photosensitizer drugs lead with 53.02% revenue share in 2025, supported by next-generation nano-formulations that shorten photosensitivity periods.

What is the fastest-growing application area?

Dermatology non-oncology indications, including acne management, are forecast to expand at a 9.08% CAGR between 2026 and 2031.

Why is Asia-Pacific considered a high-growth region?

Healthcare infrastructure upgrades, regulatory standardization in China, and cost-effective LED manufacturing underpin a projected 8.74% CAGR for Asia-Pacific through 2031.

How do reimbursement changes influence adoption?

Dedicated CPT codes and favorable insurer policies for actinic keratosis make PDT economically viable for providers, broadening patient access and supporting market expansion.

Page last updated on: